21 march 2016 earthport plc (“earthport”, the “company… · 21 march 2016 earthport plc...

TRANSCRIPT

1

21 March 2016

Earthport plc (“Earthport”, the “Company” or the “Group”)

Unaudited Interim Results

Earthport (AIM: EPO.L), the cross-border payments company, is pleased to announce its unaudited interim results for the six month period ended 31 December 2015. Financial and Transactional Highlights

Significant growth in transaction volumes and transaction monetary values o Transaction volume growth of 70%+

75%+ of the increase emanating from pre-existing customers o Transaction monetary value growth of 60%

Almost all of the increase driven by pre-existing customers

Monetary value transacted exceeded an annual run rate of $11 billion at period end

17.6% growth in revenue to £10.6 million (H1 FY 2015: £9.0 million)

o The revenue growth is impacted by the effect of previously disclosed restructuring initiatives in certain non-core business lines, resulting in foregone short-term revenue

o 74% of revenue growth emanated from pre-existing clients

o Transactional revenue was approximately 86% of the total revenue

Gross Profit increased by 5.4% to £7.4 million (H1 FY 2015: £7.0 million)

Adjusted Gross Margin at 73.5% is consistent with long term average (H1 FY 2015 81.6%)

Loss before taxation increased by 4.6% to £5.6 million (H1 FY 2015: £5.3 million)

o Excluding the unrealised fair value gain adjustment, the loss before taxation increased by 68.5%, the loss is attributed to unrealised fair value gain and loss from adjustments on FX and derivatives. These gains and losses would only crystallise in the event that any parties to the transactions default

o The increase is the result of the previously announced strategic decision to invest in global geographic expansion, product development including the Distributed Ledger (“DL”) strategy, enhancement of the leadership team and foregone revenues resulting from previously disclosed restructuring initiatives

Cash balance at 31 December 2015 amounted to £24.1 million (H1 FY 2015: £32.5 million)

o Despite the Baydonhill incident (see “Post Period Material Event” below), Earthport retains a well-funded balance sheet and possesses sufficient capital to execute its growth strategy

Operational Highlights

Strong operational progress:

o 11 new customers were signed during H1 FY 2016 (H1 FY 2015: 17)

o 9 customers went live in the period (H1 FY 2015: 8)

o Customer base now includes six of the world’s largest global Banks by asset size, nine of the top traditional and emerging Money Transfer Organisations, seven of the key “challenger” international payment companies, some of the fastest growing leading eCommerce and sharing economy companies

Growing pipeline of 35 customers under contract and in implementation stage ahead of go-live

Significant growth in transaction volume from existing non-Bank and Bank clients expanding into new countries, with immediate revenue opportunities

An increasing number of deals being originated beyond the traditional markets of the US and Europe, signifying early traction from the geographic expansion strategy.

2

o Non-Europe/US pipeline is expected to be an increasing contributor to revenue growth in FY 17 and FY 18

Distributed Ledger Strategy

o Earthport continues to cement its uniquely strong competitive position in realising the potential of DL for cross-border payments in partnership with Ripple (a DL based settlement network specialist):

Earthport’s Distributed Ledger Hub (DLH) for multiple ledgers was announced

in January 2016. This has been designed to provide full connectivity to

additional DLs as they emerge, all available via a single Earthport Application

Programming Interface (API)

The Company has commenced DL pilot programme with a major Bank and with additional ones in the pipeline with a clear roadmap to implementation

Post Period Material Event

Baydonhill Loss (as reported in the RNS dated 25th February 2016):

o Earthport’s wholly owned foreign exchange subsidiary, Baydonhill, experienced a material financial loss relating to a potential fraud by one of its corporate customers. As a result of this incident, the Company is exposed to a maximum potential loss of £5 million (See Baydonhill Material Event and Response):

While the potential loss is significant, no client funds were affected by this loss, nor are any other client funds at risk of future loss in connection to this incident. Baydonhill’s activities continue as normal

Earthport’s core business is unaffected and continues to experience significant traction as it is based on a wholly “pre-funded” payments model

The average daily transaction volume post the Baydonhill incident to date is more than 15% greater than the average daily transaction volume in December 2015 and January 2016

A full risk review has been initiated and additional controls identified and implemented; including the closure of the legacy programme that precipitated the above incident

Post Period Highlights

Enhancing the Board of Directors and Management Team:

o John B. McCoy, the former Chairman and Chief Executive Officer of Bank One Corporation, has joined Earthport's Board as a Non-Executive Director. John McCoy is currently a director of AT&T (NYSE:T) and Onex Corporation (TSE:OCX)

o Peter Klein, former Global Head of Foreign Exchange Prime Brokerage & Clearing at Bank of America, joined Earthport as Global Head of FX, in charge of all FX products across the Group

Hank Uberoi, CEO Earthport plc commented:

“Earthport’s model continues to see strong traction in the market, evidenced by the growth of existing client relationships and scope and scale of opportunities in the pipeline. From this juncture, the potential for Earthport to address the flaws of the traditional cross-border payments model is clear and the opportunity is significant. We remain committed to our investment in geographic expansion and product development to secure our position and maximise the medium and long term prospects.”

3

For further information, please contact: Earthport plc Hank Uberoi, Chief Executive Officer Simon Adamiyatt, Chief Financial Officer

020 7220 9700

Panmure Gordon (Nomad and Joint Broker) Fred Walsh / Charles Leigh-Pemberton / Duncan Monteith

020 7886 2500

N+1 Singer (Joint Broker) Shaun Dobson / James White

020 7496 3000

Shore Capital (Joint Broker) Bidhi Bhoma / Toby Gibbs

020 7408 4090

Newgate Communications Bob Huxford / Helena Bogle

020 7653 9850

About Earthport: Earthport plc is a financial services organisation providing cross-border payments services to banks, e-commerce providers, money transfer companies and payment administrators. Earthport is headquartered in London with a regional office in New York. Earthport provides the industry with access to a global payment network through a single contract, a single technical integration, and a single service relationship. Worldwide, more than 50 banks are connected into Earthport's network for the efficient clearing of low value payments. Through a single relationship, clients benefit from sophisticated validation, message transformation and compliance services, efficiently serving their customers with more innovative payment products. One of the FinTech50 2015 - judged to be the game-changers transforming the future of finance. Earthport is also winner of the Grant Thornton Quoted Company Awards 2015 Technology company of the year award and FStech/Retail Systems’ B2B Payments Innovation of the Year (2014). Earthport is listed on the Alternative Investment Market (AIM) on the London Stock Exchange. Earthport plc is authorised and regulated by the Financial Conduct Authority under the Payment Service Regulations 2009 for the provision of payment services. Find out more at www.earthport.com and on Twitter @Earthport, LinkedIn, Youtube, Slideshare and Google+.

4

BOARD STATEMENT Introduction Earthport is a regulated financial institution, providing compliant cross-border payment services to banks, e-commerce providers, money transfer companies and payment aggregators. The Earthport model is revolutionising global payments to provide a faster, safer, lower cost solution for managing payments internationally. A pioneering technology success story, Earthport is rapidly growing and in 2015 was referred to in the FinTech 50 as a “game-changer transforming the future of finance.” Earthport provides clients with access to a global payment network, maintaining local banking partnerships, through which client business is settled directly via local clearing to banked beneficiaries in more than 60 countries. As a regulated entity under the governance of the UK’s Financial Conduct Authority (FCA) and Her Majesties Revenue and Customs (HMRC), Earthport operates stringent compliance processes and risk management controls and conducts risk-based analyses of all clients.

Operational Review Earthport maintains a leading position among banks, eCommerce providers, money transfer organisations and payments aggregators as their one-stop-shop solution for cross-border payments.

Earthport’s success with clients in the highly regulated banking industry is a testament to its best-in class compliance processes. Earthport’s reputation with banks and non-bank payment service providers has enabled relationships with eCommerce and sharing economy companies, which present a more scalable model and can accelerate revenues and reduce sale cycle times. Furthermore, the recent addition of a post office to the Earthport network (Japan Post Bank – one of the largest financial institutions in the world) further diversifies the Company’s client and geographical mix.

It is important to emphasise the strengthening of existing relationships with major clients, the majority of which are interested in expanding their reach to new geographies outside of Europe and the US. Some of the world’s top financial institutions are already piloting subsequent phases of Earthport’s service offering and are adopting new aspects of the core product, such as the DLH.

The Company continues to prioritise investments that will come into fruition during FY17 and FY18 – focusing namely on geographical expansion, core product offering improvements via technology enhancements and key hires:

Certain non-core businesses were modified, thus resulting in some foregone short-term revenues in favour of more scalable prospective opportunities

De-emphasised businesses include some traditional FX activities as well as activities focused on individual clients

Enhanced focus areas include expansion into Asia and certain specific large opportunities in India and the Middle East – Asia corridors, details of which will be shared as they progress

Network Review

Earthport’s network development throughout the period will allow the Company to continue providing its clients with a robust and growing global network. Earthport optimised its network of global routes and new network partnerships were established in major Asian and Caribbean markets, while payments were executed across 182 destination countries, in 54 currencies.

5

Additional services and enhancements to the network include:

o Bahamas and Dominican Republic to strengthen Caribbean capability in response to growing demand for payment services to the region

o Bank partnerships in Bangladesh and Sri Lanka to support efficient, secure and cost effective payment services into key strategic regions further strengthening payment capability into South Asia

o This marks a significant milestone in the continued expansion of Earthport’s Asia footprint and the fulfilment of our vision to become a global payment utility

Product and Services Enhancements

Earthport continues to invest in developing its product offering in order to meet its clients’ growing demands.

The previously announced DL capability has evolved into a holistic product offering – the DLH – which offers a tiered and scalable connectivity feature for clients to execute transactions via the Ripple protocol and network

The Company has commenced a DL pilot programme with a major Bank and with additional ones in the pipeline, with implementation expected in H2 FY16

Building on the Company’s industry-first deployment of the DL Gateway, the DLH will provide full connectivity into Ripple, including private Ripple instances, Ripple market makers and, in time, other Distributed Ledgers.

The new DLH will offer a solution for banks which are increasingly being constrained by lower budgets and the need to adhere to radical changes in technology. Through the DLH, Earthport’s clients can reap the full benefits of DL technology with minimal effort and cost through a single API; a global first for the industry.

Expanding Global Footprint – Middle East and Asia

Significant opportunities continue to unfold in new geographies across Asia and the Middle East, with ongoing negotiations in the Indian, Indonesian, and Chinese markets. In the Middle East, the Company is focusing in fostering relationships with clients in Saudi Arabia and the UAE, as well as the Israel. 2015 investments in the APAC, ME, and LACA markets have resulted in 35 qualified pre-contract opportunities from these regions.

Earthport is confident it will receive a greater revenue contribution from Non-European and Non-US clients in FY17.

Regulatory Compliance Update

Earthport has received widespread industry acknowledgement for its compliance procedures, which include automated backend controls and general due diligence. As the regulatory space becomes increasingly complex, organisations rely on Earthport’s compliance expertise to ensure that all requirements will be met under full transparency. Earthport’s compliance processes successfully manage increasing transaction volumes and high expectations of its bank partners.

Baydonhill Material Event and Response

While the materialisation of such a large exposure and potential loss necessitates a thorough review of the broadest range of preventative and detective controls, the following facts are also apparent:

Where the loss is likely to prove to be related to preventative controls, it is evident that the extant controls in this area were deliberately undermined through the fraudulent actions of external parties; and that existing detection mechanisms immediately highlighted both the delayed intraday payment and concomitant duplicate payment requests, which were promptly challenged and prevented

6

Having been rapidly identified, the incident was urgently escalated and focused management attention triggered the following actions:

Compliance: With regulatory obligations including the filing of a Suspicious Activity Report (SAR) with the UK National Crime Agency (NCA), appropriate external notices in accordance with the publicly listed status of the company and the submission of a report of ‘Business Fraud’ to the relevant law enforcement agency ‘Action Fraud’

Containment: Evaluation of the relevant internal control framework and any associated gaps,

to ensure that immediate losses were finite and further exposure contained

Consultation: Promptly held between the Chairman, Board of Directors, executive management team, external counsel, the entity’s Administrators, insolvency experts and Earthport’s insurance underwriters

Investigation: Formal assignment of Earthport Executive Committee members to investigate all Baydonhill payment release processes and promptly determine and implement additional restrictions on maximum client exposure

Oversight: The establishment of a core team to coordinate and prioritise internal investigation and external stakeholder related activities and to diagnose and pursue all potential avenues of recovery of loss

Communication: Pro-active engagement with clients, bank partners, investors and employees Additional actions continue to be undertaken to ensure that, while the proper momentum is maintained with regard to facilitating and supporting the detailed internal and external investigation and recovery efforts, the business remains cognisant of the need to pursue its existing strategy without undue distraction, in-line with its obligations to all stakeholders, in particular to shareholders and clients. The circumstances that gave rise to this loss are specific to the risks and controls around the legacy ‘programme which was available to a limited number of Baydonhill clients, and without precedent within Earthport, where the core business was fully protected against these risks by virtue of operating a wholly pre-funded payments model entirely dissimilar to these agreed exceptions to the Baydonhill model. This product has been withdrawn with immediate effect. The Group’s clients continue to trust Earthport and Baydonhill; with transaction volume and monetary value trend analysis for the period immediately following the incident showing significant (greater than 15%) growth over the previous months and remaining consistent with expectations and anticipated run-rate. Legacy Baydonhill revenues executed on a non-cleared funds basis was 15% of Group revenues for the six months ended 31 December 2015. As a result of the amended controls implemented post-event, non-cleared Baydonhill revenues are now approximately 9% of Group revenues and declining. The Executive Committee remains focused on recovery of the loss, and the assigned management group continues to engage pro-actively with all interested parties.

Awards and Distinctions

FS Tech Awards 2016

o Barry Holland Memorial Award for Outstanding Individual Achievement, Hank Uberoi, Earthport CEO

Grant Thornton Quotes Company Awards 2015

o Technology company of the year

Cfi.co Finance Awards

7

o Best Cross-Border Money Transfer Solution 2015

Fintech Excellence Awards 2015

o Cross-Border Payment Network of the Year

Payments Awards 2015

o Best Alternative Payments Project

o Payment Pioneer Award: Hank Uberoi, Earthport CEO

Financial Review Revenues increased by 17.63% to £10.61 million (H1 FY15: £9.02 million), with 74% of the growth emanating from pre-existing customers, spurred by strong increase from recurring transactional revenues. Transaction volume growth was more than 70%, with 75% of the increase emanating from pre-existing customers. Transaction monetary value grew by 60%, with almost all the increase driven by pre-existing customers. Professional services fees contributed 14% of total revenues. Adjusted gross profit for the period increased by 5.98% to £7.80 million (H1 FY15: £7.36 million). The gross margin of 73.53% represented a decrease from H1 FY15 levels (81.63%), primarily driven by unanticipated increases in network costs.

Administrative expenses increased by 51.78% to £14.10 million (H1 FY15: £9.29 million), mainly due to increased staff and contractor costs. The Company has committed to investing in geographical expansion and added senior executive talent to the various teams around the world. Additional one-off investments in technology and process improvement initiatives also contributed to the increasing cost base during the period.

Adjusted operating loss increased to £6.68 million (H1 FY15: £2.25 million), driven by a comparable increase in administrative expenses.

Cash and cash equivalents as at 31 December 2015 were £24.15 million. (30 June 2015: £30.19 million, 31 December 2014: £32.52 million).

Outlook The Earthport Payment Network is recognised as a unique and credible solution for resolving the flaws and inefficiencies of the traditional cross-border payments model. Size and volume of prospective new business is growing across all regions. Growing transaction volumes, both from existing clients and from newly implemented customers are expected to continue, demonstrating the strength of the product. Significant opportunities continue to unfold in new geographies across Asia and the Middle East, accelerating revenue growth from Non-European and Non-US clients. While Bank clients continue to be the core focus of the Earthport strategy, the credibility and strategic position of the platform is attracting clients from multiple sectors that have the potential to scale faster. Earthport will continue to invest in expanding its geographic footprint and product development in order to maximise medium and long-term success. The Company’s capacity to successfully process and sustain this growth is a testament to the business’ scalability. Earthport’s management will share more details of the Company’s strategy at an investor day expected to be in late April 2016, further details of which will be announced in due course. Hank Uberoi 21 March 2016

8

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME for the six months ended 31 December 2015 Unaudited Unaudited Audited 6 months 6 months 12 months ended ended ended 31 Dec 2015 31 Dec 2014 30 Jun 2015 Continuing operations: Notes £’000 £’000 £’000 Revenue 10,612 9,021 19,267 Cost of sales (2,809) (1,657) (3,612)

Adjusted gross profit 7,803 7,364 15,655 Cost of sales – warrant charge (379) (326) (728)

Gross profit 7,424 7,038 14,927 Administrative expenses (14,105) (9,293) (19,941)

Adjusted operating loss (6,681) (2,255) (5,014) Share-based payment charge (287) (1,893) (3,289) Unrealised fair value gain/(loss) 1,333 (1,248) 345

Operating loss (5,635) (5,396) (7,958) Finance income 13 22 52 Unwinding of discount on deferred consideration - - (803)

Loss before taxation (5,622) (5,374) (8,709) Income tax (expense)/Income (469) - 18

Loss for the period and total comprehensive income attributable to owners of the parent

(6,091) (5,374) (8,691)

Loss per share attributable to the owners of the parent – basic and diluted

4 (1.30p) (1.28p) (1.91p)

9

CONSOLIDATED STATEMENT OF FINANCIAL POSITION at 31 December 2015 Unaudited Unaudited Audited as at as at as at 31 Dec 2015 31 Dec 2014 30 Jun 2015 Notes £’000 £’000 £’000 Non-current assets Goodwill 2,709 2,709 2,709 Intangible assets 6,312 6,276 6,406 Investment 273 225 250 Deferred tax asset - 541 327 Property, plant and equipment 604 457 709

9,898 10,208 10,401

Current assets Trade and other receivables 5 4,102 3,309 8,329 Derivative financial assets 2,197 1,009 976 Cash and cash equivalents 24,154 32,520 30,195

30,453 36,838 39,500

Total assets 40,351 47,046 49,901 Current liabilities Trade and other payables 6 (3,326) (3,551) (5,711) Derivative financial liabilities (750) (1,396) (2,766)

(4,076) (4,947) (8,477)

Non-current liabilities Earn-out consideration (3,292) (2,489) (3,292) Deferred tax liability (879) (867) (737)

(4,171) (3,356) (4,029)

Total liabilities (8,247) (8,303) (12,506)

NET ASSETS 32,104 38,743 37,395

Equity Capital and reserves Ordinary shares 7 70,738 70,638 70,695 Share premium 8 78,331 78,271 78,272 Own shares 9 (1,220) (1,365) (1,252) Merger reserve 9,200 9,200 9,200 Share-based payment reserve 12,647 11,395 12,557 Warrant reserve 1,424 643 1,045 Retained earnings (139,016) (130,039) (133,122)

EQUITY ATTRIBUTABLE TO 32,104 38,743 37,395

OWNERS OF THE PARENT

10

CONSOLIDATED STATEMENT OF CASH FLOWS for the six months ended 31 December 2015 Unaudited Unaudited Audited 6 months 6 months 12 months ended ended ended 31 Dec 2015 31 Dec 2014 30 Jun 2015 Notes £’000 £’000 £’000 Net cash used in operating activities 10 (4,946) (2,100) (2,903) Investing activities Purchase of property, plant and equipment (129) (538) (757) Capitalised intangible fixed assets (1,077) (537) (1,916) Trade investment (23) - (25)

Net cash used in investing activities (1,229) (1,075) (2,698)

Financing activities Proceeds on issuance of ordinary share capital (net of costs paid) - 26,312 26,567 Proceeds on exercise of options 134 154 - Proceeds on exercise of options through - Joint Share Ownership Plan - 112 112 Loan repayment - (344) (344)

Net cash from financing activities 134 26,234 26,335

Net (decrease)/increase in cash and cash (6,041) 23,059 20,734 cash equivalents

Cash and cash equivalents at the beginning of the period 30,195 9,461 9,461

Cash and cash equivalents at the end of the period 24,154 32,520 30,195

11

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY for the six months ended 31 December 2014 (Unaudited)

Attributable to the owners of the Parent Interest Share-based

Share Share In own Merger Payment Warrant Retained Capital Premium Shares Reserve Reserve Reserve Earnings Total £’000 £’000 £’000 £’000 £’000 £’000 £’000 £’000

Balance at 1 July 2014

64,016 58,213 (1,456) 9,200 9,632 317 (124,795) 15,127

Loss for the

period, being total

comprehensive income for

the period - - - - - - (5,374) (5,374)

Transactions with owners

Share-based payments

- employee share options

60 115 91 - (130) - 130 266

- employee share options charge

- - - - 1,893 - - 1,893

- warrants - - - - - 326 - 326 Issue of ordinary

shares 6,562 20,242 - - - - - 26,804

Cost of share issue - (299) - - - - - (299)

Total transactions

with owners of the Parent, recognised

directly in equity

6,622 20,058 91 - 1,763 326 (5,244) 23,616

Balance at 31 December 2014

70,638 78,271 (1,365) 9,200 11,395 643 (130,039) 38,743

12

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY for the six months ended 31 December 2015 (Unaudited)

Attributable to the owners of the Parent Interest Share-based

Share Share In own Merger Payment Warrant Retained Capital Premium Shares Reserve Reserve Reserve Earnings Total £’000 £’000 £’000 £’000 £’000 £’000 £’000 £’000

Balance at 1 July 2015

70,695 78,272 (1,252) 9,200 12,557 1,045 (133,122) 37,395

Loss for the

period, being total

comprehensive income for

the period - - - - - - (6,091) (6,091)

Transactions with owners

Share-based payments

- employee share options

43 59 32 - (197) - 197 134

- employee share options charge

- - - - 287 - - 287

- warrants - - - - - 379 - 379

Total transactions

with owners of the Parent, recognised

directly in equity

43 59 32 - 90 379 (5,894) (5,291)

Balance at 31 December 2015

70,738 78,331 (1,220) 9,200 12,647 1,424 (139,016) 32,104

13

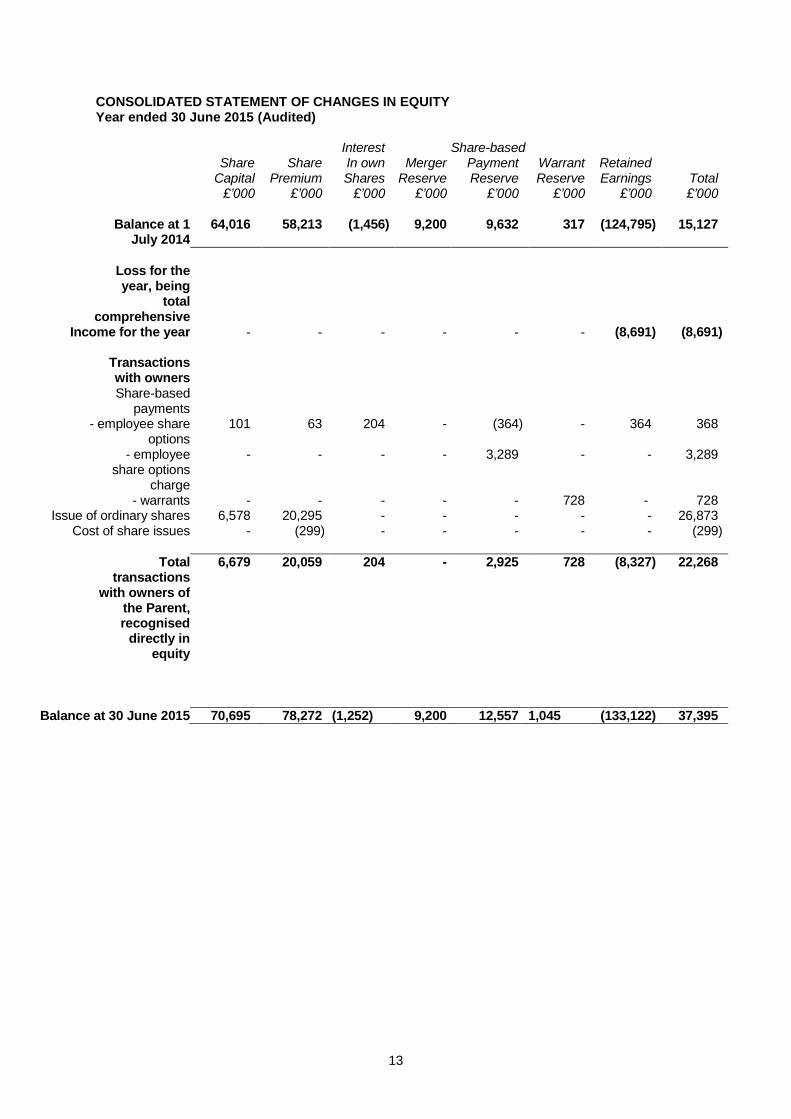

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY Year ended 30 June 2015 (Audited)

Interest Share-based Share Share In own Merger Payment Warrant Retained Capital Premium Shares Reserve Reserve Reserve Earnings Total £’000 £’000 £’000 £’000 £’000 £’000 £’000 £’000

Balance at 1 July 2014

64,016 58,213 (1,456) 9,200 9,632 317 (124,795) 15,127

Loss for the year, being

total

comprehensive Income for the year - - - - - - (8,691) (8,691)

Transactions with owners

Share-based payments

- employee share options

101 63 204 - (364) - 364 368

- employee share options

charge

- - - - 3,289 - - 3,289

- warrants - - - - - 728 - 728 Issue of ordinary shares 6,578 20,295 - - - - - 26,873

Cost of share issues - (299) - - - - - (299)

Total transactions

with owners of the Parent, recognised

directly in equity

6,679 20,059 204 - 2,925 728 (8,327) 22,268

Balance at 30 June 2015 70,695 78,272 (1,252) 9,200 12,557 1,045 (133,122) 37,395

14

NOTES TO THE UNAUDITED INTERIM RESULTS

for the six months ended 31 December 2015 1. GENERAL INFORMATION

Earthport plc is a public limited company listed on Alternative Investment Market (AIM), incorporated and domiciled in the England and Wales under the Companies Act 2006. The address of its principal place of business and registered office is 21 New Street, London EC2M 4TP.

2. GOING CONCERN

The interim financial information has been prepared on the assumption that the Group is a going concern.

When assessing the foreseeable future the directors have looked at a period of twelve months from the date of approval of the interim financial information. The directors believe that the Group has demonstrated progress in achieving its objective of positioning the Group as an infrastructure supplier to the global payments industry, and therefore consider that it is appropriate to prepare the Group’s interim financial information on a going concern basis, which assumes that the Company is to continue in operational existence for the foreseeable future.

3. ACCOUNTING POLICIES

Basis of preparation The interim financial information is prepared using accounting policies consistent with International Financial Reporting Standards (“IFRS’’) as adopted by the European Union. The financial statements have been prepared under the historical cost convention and the principal accounting policies are set out in the 30 June 2015 financial statements.

15

NOTES TO THE INTERIM RESULTS

for the six months ended 31 December 2015

4. LOSS PER SHARE

Loss per share is calculated by dividing the loss attributable to equity holders of the Company by the weighted average number of ordinary shares in issue during the period.

The loss attributable to Ordinary shareholders and weighted average number of ordinary shares for the purposes of calculating the diluted loss per share are identical to those used for basic loss per ordinary share. This is because the exercise of share options and other benefits would have the effect of reducing loss per share and is therefore not dilutive under the terms of IAS33 “Earnings per share”.

5. TRADE AND OTHER RECEIVABLES

Unaudited Unaudited Audited as at as at as at 31 Dec

2015 31 Dec

2014 30 Jun

2015 £’000 £’000 £’000 Trade receivables 2,610 2,185 6,464

Other receivables 968 795 1,098

Prepayments 628 477 767

4,206 3,457 8,329 Less: Provision for impairment (104) (148) -

Net trade and other receivables 4,102 3,309 8,329

Unaudited Unaudited Audited 6 months 6 months 12 months ended ended ended

31 Dec 2015 31 Dec 2014 30 Jun 2015 £’000 £’000 £’000 Loss attributable to owners of the parent (6,091) (5,374) (8,691)

Number Number Number Weighted average number of ordinary shares in issue (thousands)

476,458 428,488 461,444

Less: own shares held (thousands) (6,926) (7,775) (7,113)

469,532 420,713 454,331

Basic and fully diluted loss per share (pence) (1.30p) (1.28p) (1.91p)

16

NOTES TO THE INTERIM RESULTS

for the six months ended 31 December 2015 6. TRADE AND OTHER PAYABLES

Unaudited Unaudited Audited as at as at as at 31 Dec

2015 31 Dec

2014 30 Jun

2015 £’000 £’000 £’000 Trade payables 668 1,237 3,662 Other payables 3 2 4 Other taxation and social security 290 252 356 Accruals and deferred income 2,365 2,060 1,689

3,326 3,551 5,711

Trade payables and accruals principally comprise amounts outstanding in respect of operating costs. The directors consider that the carrying amounts for trade and other payables approximate their fair value.

7. SHARE CAPITAL

Authorised The Articles of Association were amended on 24 March 2010. The Company has no authorised share capital limit. Issued Unaudited Unaudited Audited

6 months 6 months 12 months

ended ended ended

31 Dec 2015

31 Dec 2014

30 Jun 2015

£’000 £’000 £’000

At start of period 47,636 40,957 40,957

Shares issued in the period 43 6,622 6,679

At end of period 47,679 47,579 47,636

Deferred shares 23,059 23,059 23,059

Total 70,738 70,638 70,695

During the period ended 31 December 2015: 432,488 ordinary shares of 10p were issued against exercise of share options.

17

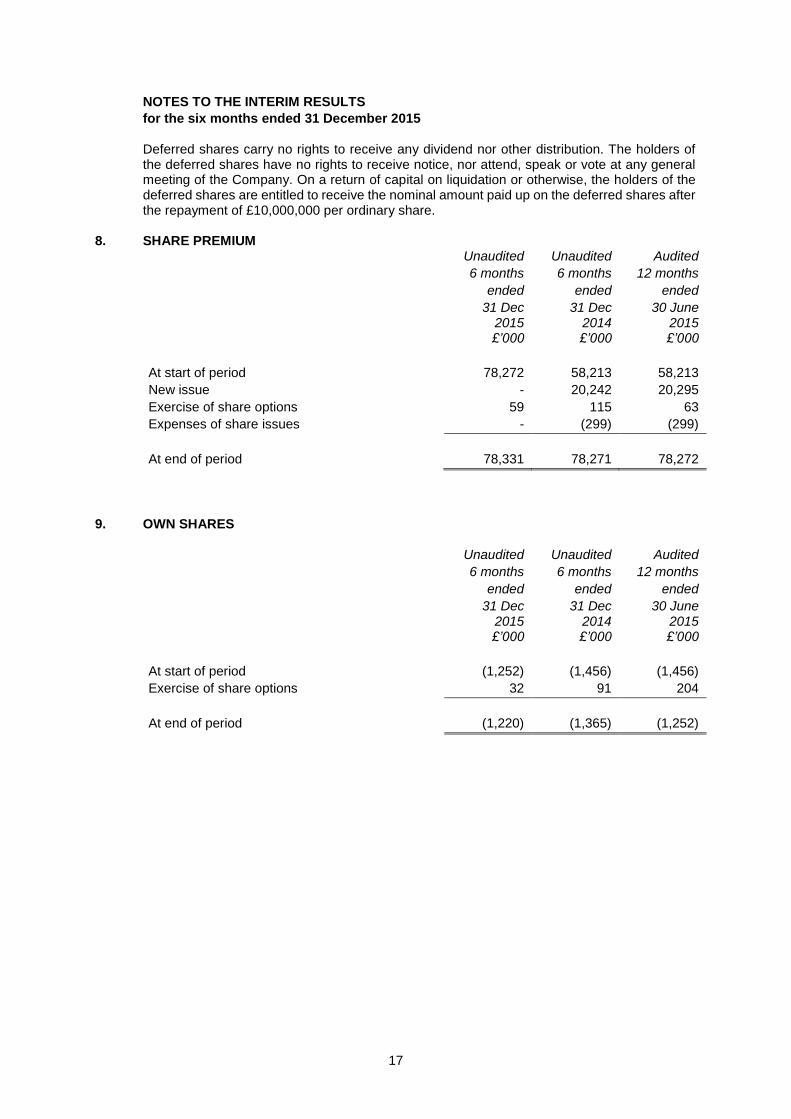

NOTES TO THE INTERIM RESULTS

for the six months ended 31 December 2015 Deferred shares carry no rights to receive any dividend nor other distribution. The holders of the deferred shares have no rights to receive notice, nor attend, speak or vote at any general meeting of the Company. On a return of capital on liquidation or otherwise, the holders of the deferred shares are entitled to receive the nominal amount paid up on the deferred shares after the repayment of £10,000,000 per ordinary share.

8. SHARE PREMIUM

Unaudited Unaudited Audited

6 months 6 months 12 months

ended ended ended

31 Dec 2015

31 Dec 2014

30 June 2015

£’000 £’000 £’000

At start of period 78,272 58,213 58,213

New issue - 20,242 20,295

Exercise of share options 59 115 63

Expenses of share issues - (299) (299)

At end of period 78,331 78,271 78,272

9. OWN SHARES

Unaudited Unaudited Audited

6 months 6 months 12 months

ended ended ended

31 Dec 2015

31 Dec 2014

30 June 2015

£’000 £’000 £’000

At start of period (1,252) (1,456) (1,456)

Exercise of share options 32 91 204

At end of period (1,220) (1,365) (1,252)

18

NOTES TO THE INTERIM RESULTS

for the six months ended 31 December 2015 10. RECONCILIATION OF LOSS BEFORE TAX TO NET CASH OUTFLOW FROM

OPERATING ACTIVITIES

Unaudited Unaudited Audited 6 months 6 months 12 months ended ended ended 31 Dec

2015 31 Dec

2014 30 Jun

2015 £’000 £’000 £’000

Loss before tax (5,622) (5,374) (8,709) Amortisation of intangible assets 1,171 793 1,904 Depreciation of property, plant and equipment 234 237 342 Share-based payment charge and warrant 666 2,219 4,017 charge Shares issued in lieu of consultancy fees - 193 263

R & D Tax Credit Received - - 106 Finance income (13) (22) (52) Current Year Tax Credit - - (4) Unwinding of discount on Deferred consideration - - 803

Operating cash out flow before movements in (3,564) (1,954) (1,330) working capital Decrease/(Increase) in receivables 3,006 3,347 (1,640) (Decrease)/Increase in payables (4,401) (3,515) 15

Cash used by operations (4,959) (2,122) (2,955) Interest received 13 22 52

Net cash used in operating activities (4,946) (2,100) (2,903)

19

NOTES TO THE INTERIM RESULTS

for the six months ended 31 December 2015

11. PUBLICATION OF NON-STATUTORY FINANCIAL STATEMENTS

The results for the six months ended 31 December 2015 and 31 December 2014 are unaudited and have not been reviewed by the auditor. The results for the year ended 30 June 2015 do not constitute statutory financial statements as defined in section 434 of the Companies Act 2006, but have been derived from the full audited financial statements for the year ended 30 June 2015. Statutory accounts for the year ended 30 June 2015, on which the auditors gave an audit report which was unqualified and did not contain a statement under section 498(2) or (3) of the Companies Act 2006, have been filed with the Registrar of Companies. The interim financial information has been prepared on the basis of the same accounting policies as published in the audited financial statements for the year ended 30 June 2015 and the accounting policies to be adopted in the financial statements for the year ended 30 June 2016. The annual financial statements of the Group are prepared in accordance with International Financial Reporting Standards and International Financial Reporting Interpretations Committee (“IFRIC”) pronouncements as adopted by the European Union. Comparative figures for the year ended 30 June 2015 have been extracted from the statutory financial statements for that period.

12. The interim results for the six months ended 31 December 2015 are available on the Company’s website: www.earthport.com.