27134 - fundamentals (edition 1 - nov 2017)reference.scottishwidows.co.uk/docs/27134.pdf · at...

TRANSCRIPT

FUNDSTALKINVESTMENT NEWS AND INSIGHT FROM SCOTTISH WIDOWS

START

WELCOME TO FUNDSTALKAn introduction from our Head of Fund Proposition 1FUNDSTALK: BITESIZESome of this edition’s key insight at a glance

2018 OUTLOOKOur analysis of investment markets in 2018

2

3BRIDGING THE INNOVATION GAPCan drawdown evolve to meet clients’ needs

4Q&A WITH OUR FUND MANAGER ASSESSMENT TEAMWhat makes our approach different

THE RISE OF VALUES-BASED INVESTINGHelping your clients reflect ethical values in their investments

5

6

ISSU

E

JA N UA RY 20 18

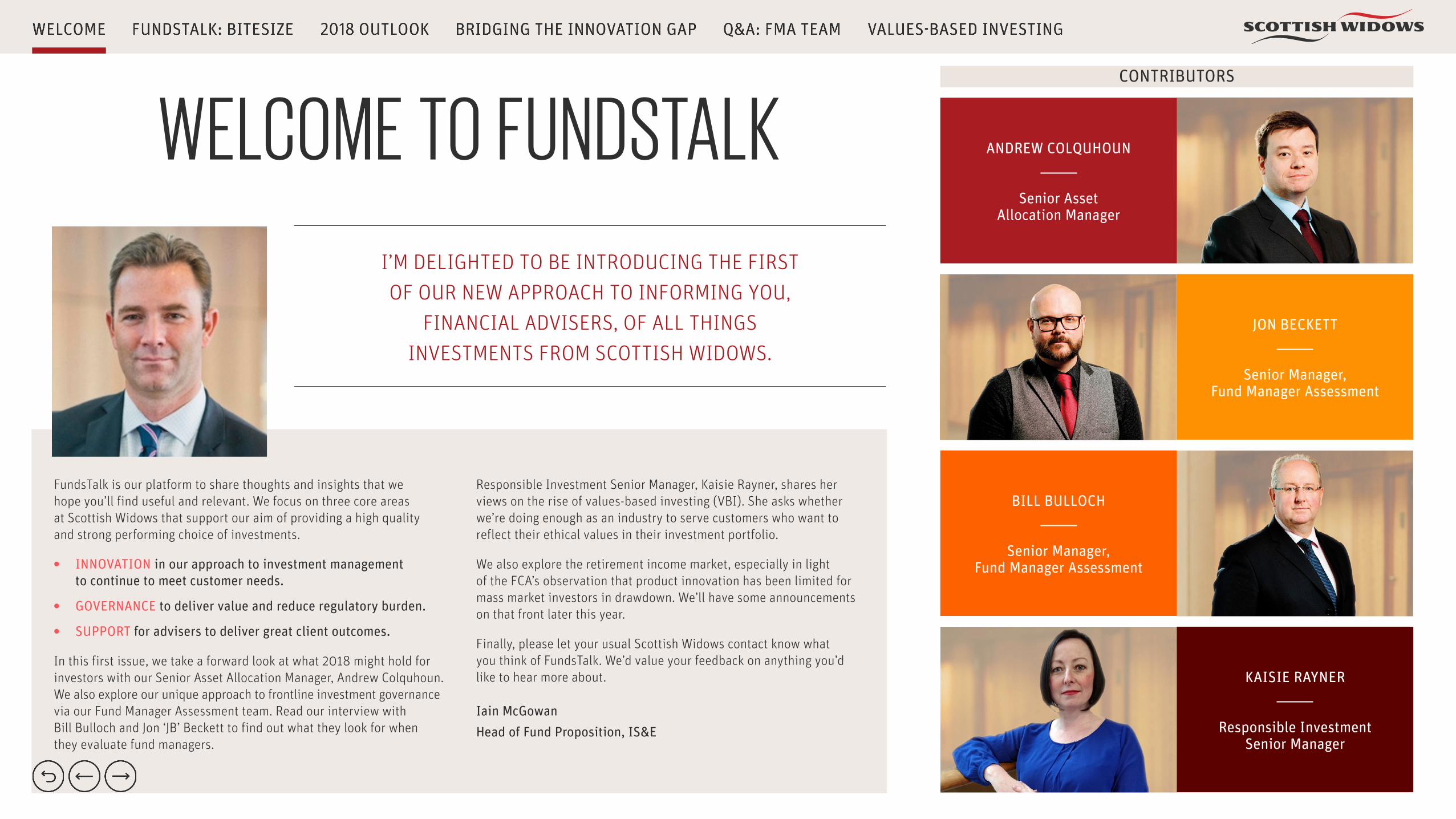

WELCOME TO FUNDSTALK ANDREW COLQUHOUN

Senior Asset Allocation Manager

KAISIE RAYNER

Responsible Investment Senior Manager

JON BECKETT

Senior Manager, Fund Manager Assessment

BILL BULLOCH

Senior Manager, Fund Manager Assessment

CONTRIBUTORS

FundsTalk is our platform to share thoughts and insights that we hope you’ll find useful and relevant. We focus on three core areas at Scottish Widows that support our aim of providing a high quality and strong performing choice of investments.

• INNOVATION in our approach to investment management to continue to meet customer needs.

• GOVERNANCE to deliver value and reduce regulatory burden.

• SUPPORT for advisers to deliver great client outcomes.

In this first issue, we take a forward look at what 2018 might hold for investors with our Senior Asset Allocation Manager, Andrew Colquhoun. We also explore our unique approach to frontline investment governance via our Fund Manager Assessment team. Read our interview with Bill Bulloch and Jon ‘JB’ Beckett to find out what they look for when they evaluate fund managers.

Responsible Investment Senior Manager, Kaisie Rayner, shares her views on the rise of values-based investing (VBI). She asks whether we’re doing enough as an industry to serve customers who want to reflect their ethical values in their investment portfolio.

We also explore the retirement income market, especially in light of the FCA’s observation that product innovation has been limited for mass market investors in drawdown. We’ll have some announcements on that front later this year.

Finally, please let your usual Scottish Widows contact know what you think of FundsTalk. We’d value your feedback on anything you’d like to hear more about.

Iain McGowanHead of Fund Proposition, IS&E

I’M DELIGHTED TO BE INTRODUCING THE FIRST OF OUR NEW APPROACH TO INFORMING YOU,

FINANCIAL ADVISERS, OF ALL THINGS INVESTMENTS FROM SCOTTISH WIDOWS.

FUNDSTALK: BITESIZE

2

1

3

4

INVESTMENT MARKETS AND CONDITIONS CAN CHANGE RAPIDLY AND, AS SUCH, THE VIEWS EXPRESSED IN THIS UPDATE SHOULD NOT BE TAKEN AS STATEMENTS OF FACT NOR BE RELIED ON WHEN MAKING INVESTMENT DECISIONS. FORECASTS ARE OPINIONS ONLY, CANNOT BE GUARANTEED AND SHOULD NOT BE RELIED ON WHEN MAKING INVESTMENT DECISIONS.

Sustainable investing has grown 107.4% annually since 2012*

The FMA team have over 50 combined years’ experience in fund management and fund research

Our research shows flexibility and access are two of the main priorities for pension investors approaching retirement

Markets priced for benign economic outlook – but beware of risks

*Source: EY sustainable investing: the millenial investor, 2017

READ ARTICLE

READ ARTICLE

READ ARTICLE

READ ARTICLE

OUR SENIOR ASSET ALLOCATION MANAGER, ANDREW COLQUHOUN, PROVIDES AN ANALYSIS ON WHAT WE COULD SEE ACROSS INVESTMENT MARKETS AT HOME AND ABROAD IN 2018.

2018 OUTLOOK Investment markets are starting 2018 against a backdrop of a broadly positive outlook for the global economy. The consensus view is that the world economy is heading into its strongest year since the global financial crisis, with simultaneous upswings across most major economies (with the partial exception of the UK). Risk assets – such as equity and credit – are being supported by expectations for robust growth. Furthermore, the tame inflation backdrop means market analysts generally perceive little pressure for central banks to raise rates quickly, helping to contain bond yields at or near low levels. Meanwhile, volatility remained exceptionally low for most of 2017, boosting risk-adjusted returns for investors. The central view in investment markets is that this broadly benign state of affairs may continue for a while yet.

EQUITY-MARKET VALUATIONS

Within equity, we acknowledge valuations are relatively high already in most markets, but we think the US and to a lesser degree the UK look particularly stretched. As such, we expect Europe, Japan and emerging markets to outperform relative to the US, while generally favourable economic prospects may also prove supportive for these three markets. In the US, an important factor for the

equity market may be the success, or otherwise, of the current administration’s legislative programme. Elsewhere, the final shape of Brexit remains a major uncertainty for UK stocks, and assets more generally, although we think markets already look to be pricing quite a pessimistic view.

BOND MARKETS AND INTEREST RATES

The market consensus is still of the view that interest rates will rise relatively slowly across major economies. At the time of writing, the market is still pricing in a 40% chance of only two further rate increases by the US Federal Reserve in 2018.1 And sterling futures markets are pricing in only one rate increase by the Bank of England in 2018, with the next increase not until 2020.2 We think the balance of risk is that benchmark rates will rise faster than markets currently expect, and will drag longer-dated rates up with them. However, we do not expect interest rates to return to the much higher pre-financial-crisis levels, somewhat containing the possible price impact for bond investors, partly because of deep-rooted structural factors, including changing savings and investment behaviour. Moreover, we think bonds retain an important role in multi-asset portfolios as a diversifier, particularly in an environment of high equity valuations.

INFLATION IS A KEY RISK

We believe investors should be mindful of the risks to the above case for a slow rise in rates, including the potential for inflation to stage a surprise return. Despite solid growth, inflation has been puzzlingly weak in most major economies – except in the UK, where it has picked up despite lower growth. The relatively high inflation

level in the UK is viewed by many as a temporary adjustment, mainly on the back of the decline in sterling after the Brexit referendum. A resurgence of inflation, should it happen, would force central banks to raise interest rates and/or curtail asset-purchase programmes more aggressively than market participants currently expect. This would undermine a key assumption on which the current market regime is based, and, in our view, could be a trigger for an increase in market volatility.

“INFLATION HAS BEEN PUZZLINGLY WEAK IN MOST MAJOR ECONOMIES”

INVESTMENT MARKETS AND CONDITIONS CAN CHANGE RAPIDLY AND, AS SUCH, THE VIEWS EXPRESSED IN THIS UPDATE SHOULD NOT BE TAKEN AS STATEMENTS OF FACT NOR BE RELIED ON WHEN MAKING INVESTMENT DECISIONS. FORECASTS ARE OPINIONS ONLY, CANNOT BE GUARANTEED AND SHOULD NOT BE RELIED ON WHEN MAKING INVESTMENT DECISIONS.

A PROTRACTED ECONOMIC UPSWING

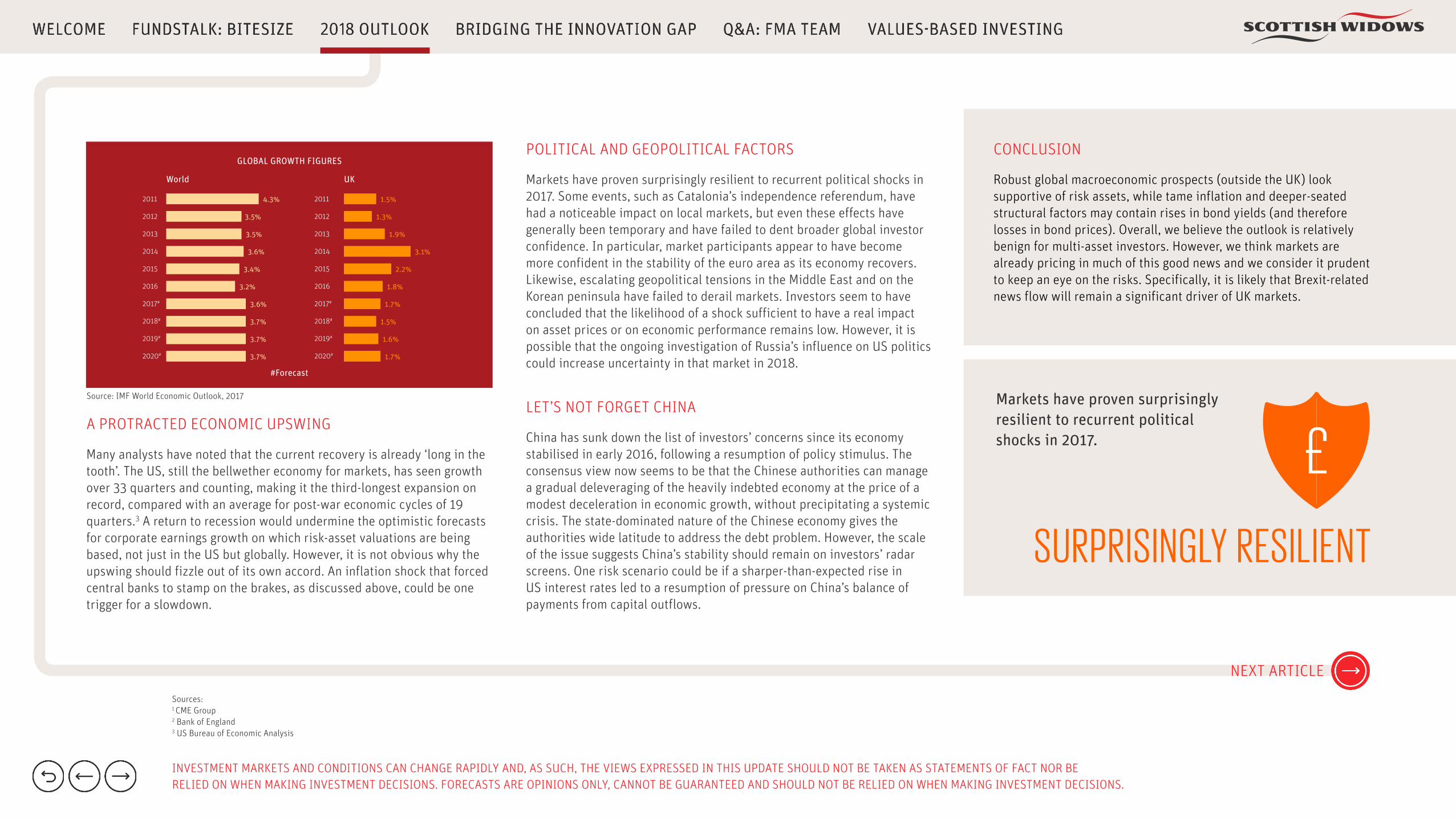

Many analysts have noted that the current recovery is already ‘long in the tooth’. The US, still the bellwether economy for markets, has seen growth over 33 quarters and counting, making it the third-longest expansion on record, compared with an average for post-war economic cycles of 19 quarters.3 A return to recession would undermine the optimistic forecasts for corporate earnings growth on which risk-asset valuations are being based, not just in the US but globally. However, it is not obvious why the upswing should fizzle out of its own accord. An inflation shock that forced central banks to stamp on the brakes, as discussed above, could be one trigger for a slowdown.

POLITICAL AND GEOPOLITICAL FACTORS

Markets have proven surprisingly resilient to recurrent political shocks in 2017. Some events, such as Catalonia’s independence referendum, have had a noticeable impact on local markets, but even these effects have generally been temporary and have failed to dent broader global investor confidence. In particular, market participants appear to have become more confident in the stability of the euro area as its economy recovers. Likewise, escalating geopolitical tensions in the Middle East and on the Korean peninsula have failed to derail markets. Investors seem to have concluded that the likelihood of a shock sufficient to have a real impact on asset prices or on economic performance remains low. However, it is possible that the ongoing investigation of Russia’s influence on US politics could increase uncertainty in that market in 2018.

LET’S NOT FORGET CHINA

China has sunk down the list of investors’ concerns since its economy stabilised in early 2016, following a resumption of policy stimulus. The consensus view now seems to be that the Chinese authorities can manage a gradual deleveraging of the heavily indebted economy at the price of a modest deceleration in economic growth, without precipitating a systemic crisis. The state-dominated nature of the Chinese economy gives the authorities wide latitude to address the debt problem. However, the scale of the issue suggests China’s stability should remain on investors’ radar screens. One risk scenario could be if a sharper-than-expected rise in US interest rates led to a resumption of pressure on China’s balance of payments from capital outflows.

CONCLUSION

Robust global macroeconomic prospects (outside the UK) look supportive of risk assets, while tame inflation and deeper-seated structural factors may contain rises in bond yields (and therefore losses in bond prices). Overall, we believe the outlook is relatively benign for multi-asset investors. However, we think markets are already pricing in much of this good news and we consider it prudent to keep an eye on the risks. Specifically, it is likely that Brexit-related news flow will remain a significant driver of UK markets.

Sources:

1 CME Group 2 Bank of England 3 US Bureau of Economic Analysis

Source: IMF World Economic Outlook, 2017

NEXT ARTICLE

SURPRISINGLY RESILIENT

Markets have proven surprisingly resilient to recurrent political shocks in 2017.

GLOBAL GROWTH FIGURES

4.3%2011

2012

2013

2014

2015

2016

2017#

2018#

2019#

2020#

3.5%

3.5%

3.6%

3.4%

3.2%

3.6%

3.7%

3.7%

3.7%

World

2011

2012

2013

2014

2015

2016

2017#

2018#

2019#

2020#

1.5%

1.3%

1.9%

3.1%

2.2%

1.8%

1.7%

1.5%

1.6%

1.7%

UK

#Forecast

When the Financial Conduct Authority (FCA) published its Retirement Outcomes Review interim paper 1 in July it was the findings around consumer behaviour and non-advised drawdown that grabbed the headlines.

However, the regulator also flagged up concerns around the level of innovation it had seen since the pension freedoms took effect in 2015.

The industry, given just a year to ramp up for the April 2015 implementation of those major reforms, has been focused on overhauling systems, refreshing drawdown propositions and repositioning in response to changing consumer needs. Firms have also been digesting and responding to a slew of regulatory reviews addressing the various issues created by the freedoms, including increased demand for transfers from DB to DC schemes.

But the government’s expectation that the reforms would drive new innovation in the market has not yet been fully realised. In the drawdown market in particular, pressure is growing on the industry to support sustainability of income in retirement.

THE FCA WARNED IN ITS INTERIM REPORT ON THE RETIREMENT OUTCOMES REVIEW THAT PRODUCT INNOVATION HAD BEEN “LIMITED”.

“For example, we have not seen products emerge for the mass market that combine flexibility with an element of guaranteed income,” the regulator’s report stated.

The paper did acknowledge that providers had faced obstacles to innovation, including “the pace of policy change” and “uncertainty about how the market may develop in the future”.

SOME OF THE BOXES ARE TICKED – BUT NOT ALL

The preference for both investors and advisers has been to enter drawdown, rather than buy an annuity. However products that provide investors with sustainability of income, potential for capital growth and, ultimately, peace of mind, remain conspicuous by their absence.

This is where the main innovation challenge lies, as there are competing needs to be met. People want to have some control of their pension fund. At the same time, however, they are concerned about the prospect of running out of money before they die.

HEAD OF FUND PROPOSITION, IAIN MCGOWAN, TAKES A LOOK AT WHAT’S ON OFFER TO INVESTORS IN THE DRAWDOWN MARKET AND WHERE INNOVATION MAY LEAD US.

BRIDGING THE INNOVATION GAP

INVESTMENT MARKETS AND CONDITIONS CAN CHANGE RAPIDLY AND, AS SUCH, THE VIEWS EXPRESSED IN THIS UPDATE SHOULD NOT BE TAKEN AS STATEMENTS OF FACT NOR BE RELIED ON WHEN MAKING INVESTMENT DECISIONS. FORECASTS ARE OPINIONS ONLY, CANNOT BE GUARANTEED AND SHOULD NOT BE RELIED ON WHEN MAKING INVESTMENT DECISIONS.

READY MADE SOLUTIONS

Simple, off-the-shelf solutions designed specifically for sustainability of retirement income, while also providing access and flexibility, remain thin on the ground.

Our research found these two factors were consistently the main priorities (or among them) for DC pension holders in or approaching retirement.2

ACCESS AND FLEXIBILITY

1 https://www.fca.org.uk/publication/market-studies/retirement-outcomes-review-interim-report.pdf 2 Retirement Income Solutions customer research for Scottish Widows by Optimisa, Aug 2016

The middle ground between those offerings remains sparsely populated, despite some attempts to tick all the above boxes. One such effort came in the form of guaranteed drawdown. Metlife UK launched a low-cost guaranteed drawdown proposition in 2015, but has since closed its wealth management operation to new business. Other providers have stalled on entering that market, citing the cost of providing guarantees.

It may also be that guaranteed drawdown products don’t easily provide investors with two of their biggest requirements in the post-freedoms market – access and flexibility. Our research found these two factors were consistently among the priorities for people with DC pensions in or approaching retirement.2

There are also investment-linked and deferred annuities, providing security but only a limited element of investment flexibility. Elsewhere some firms have launched governance services for drawdown propositions. These can bring benefits but they are typically overlays for existing products and not standalone solutions in themselves.

Simple, off-the-shelf solutions designed specifically for sustainability of retirement income, while also providing access and flexibility, remain thin on the ground, however.

Many advisers are navigating this area by helping clients manage a phased strategy, initially with drawdown followed at a later stage by annuitisation (of at least some of the pension pot). This offers a combination of short-term flexibility and long-term certainty and longevity hedging. What it doesn’t do, however, is blend the two in a way that ensures the drawdown investment stage doesn’t undermine the ability to provide certainty later in life.

THE NEEDS THAT ARE YET TO BE MET

This is why the focus now is on drawdown investment strategies that counter the various risks faced by investors in drawdown, not least sequence risk, pound-cost ravaging and inflation.

In an ideal world what would the components of a product, or combinations of products, in this area ideally look like? They would be built to last, account for longevity risk, inflation, volatility, sequence risk and pound-cost ravaging and also offer potential for investment growth, at the same time being understandable. They would help advisers satisfy regulatory as well as client requirements too, with a focus on transparency, simplicity, suitability, risk appetite and good outcomes.

Long after the dust has settled on the pension freedoms, the retirement needs of many consumers are arguably still not being met. But the gap can yet be filled, and it doesn’t always need to be expensive or complex.

NEXT ARTICLE

At one end of the scale, there are products

meeting the need for security, primarily in

the shape of annuities, but they don’t offer flexibility or access.

At the other end, there are products that provide access, flexibility and autonomy, as well as allowing for funds to be passed on at death. What they lack is the security that

investors still crave.

Fund manager assessment forms a frontline for Scottish Widows’ governance process, engaging with our fund managers. Together, Jon ‘JB’ Beckett and Bill Bulloch act as an internal rating agency, which is an unusual feature among pension providers, as many opt to rely on services such as Morningstar, Financial Express or Square Mile. Their combined expertise and experience make JB and Bill well placed to know what makes fund managers tick and what the broader trends are, both in financial markets and within the pensions marketplace.

We asked them to tell us more about their unique process.

Q: How do you find your best ideas?

JB: Research is the key to finding best-in-class funds. For example, we attend fund manager events and conferences across the UK and keep an eye on new innovations and fund launches, but we also meet lots of fund managers on a one-on-one basis. Being a large player like Scottish Widows makes better access possible and helps us do the job effectively.

Bill: There are also about 30 companies we’re in regular contact with, who know Scottish Widows as a major distributor – so they seek us out and bring ideas to us. But we know what we’re looking for, versus passively letting people ‘pitch’ to us.

JB: Applying the multi-asset manager approach to the process makes us different among insurers. It’s incumbent on us to filter out the noise, spin and trends, to try to find the quality funds – which are not always found in the companies with the biggest marketing budgets.

Q: How important is it to you to stay up-to-date on trends?

Bill: Part of our role as merchandisers is to have the right products on the shelf. When it comes to multi-asset portfolios, we recommend an array of funds that we have thoroughly researched and vetted – then let our colleagues in the Asset Allocation team decide which funds to put in which pension portfolios. To do our jobs well, we have to be aware of what’s happening out there in the market, but not be driven by it.

Q&A: OUR UNIQUE FUND MANAGER ASSESSMENT APPROACH

THE FUND MANAGER ASSESSMENT (FMA) TEAM IS TASKED WITH EVALUATING THE FUNDS PROVIDED BY SCOTTISH WIDOWS.

IN THIS ARTICLE WE PUT OUR FMA TEAM UNDER THE SPOTLIGHT TO LEARN MORE ABOUT THEIR UNIQUE PROCESS.

INVESTMENT MARKETS AND CONDITIONS CAN CHANGE RAPIDLY AND, AS SUCH, THE VIEWS EXPRESSED IN THIS UPDATE SHOULD NOT BE TAKEN AS STATEMENTS OF FACT NOR BE RELIED ON WHEN MAKING INVESTMENT DECISIONS. FORECASTS ARE OPINIONS ONLY, CANNOT BE GUARANTEED AND SHOULD NOT BE RELIED ON WHEN MAKING INVESTMENT DECISIONS. PAST PERFORMANCE IS NOT AN INDICATOR FOR FUTURE RESULTS.

Q: What are some of your top reasons for selecting a fund?

JB: From a fund-specific perspective, it is the consistency of past outperformance that is important to us. Advisers may often look for managers that topped the charts over the last 3 years; we are looking for managers for 5-10 years and longer. We need to have strong conviction that a fund manager has that high probability of delivering performance consistently, in excess of fees.

Bill: Awareness of the marketplace is important. I like to look for the best ideas that advisors may also be aware of – and that’s a function of knowing what’s happening in the market, just as much as understanding regulation.

Q: What’s the assessment process for reviewing a fund’s performance?

JB: With around 800 funds being monitored in the Scottish Widows system, a number of material factors can trigger a review of a fund: performance, external market events, fund manager changes, company mergers, and so forth.

Bill: With underperforming funds, it’s important to understand that performance might be down to the investment style (sector) being out of favour in the short term. But when the market rotates back again and favours that particular style, then we want funds that offer a real difference from their competitors. A fund manager’s style can also drift over time, and understanding this is key to discerning skill from lucky market timing. That’s why we especially look for managers who have been through market cycles; who have some experience with boom and bust periods, style rotations, and macro events; and who understand the signals in the market and try to get ahead of them.

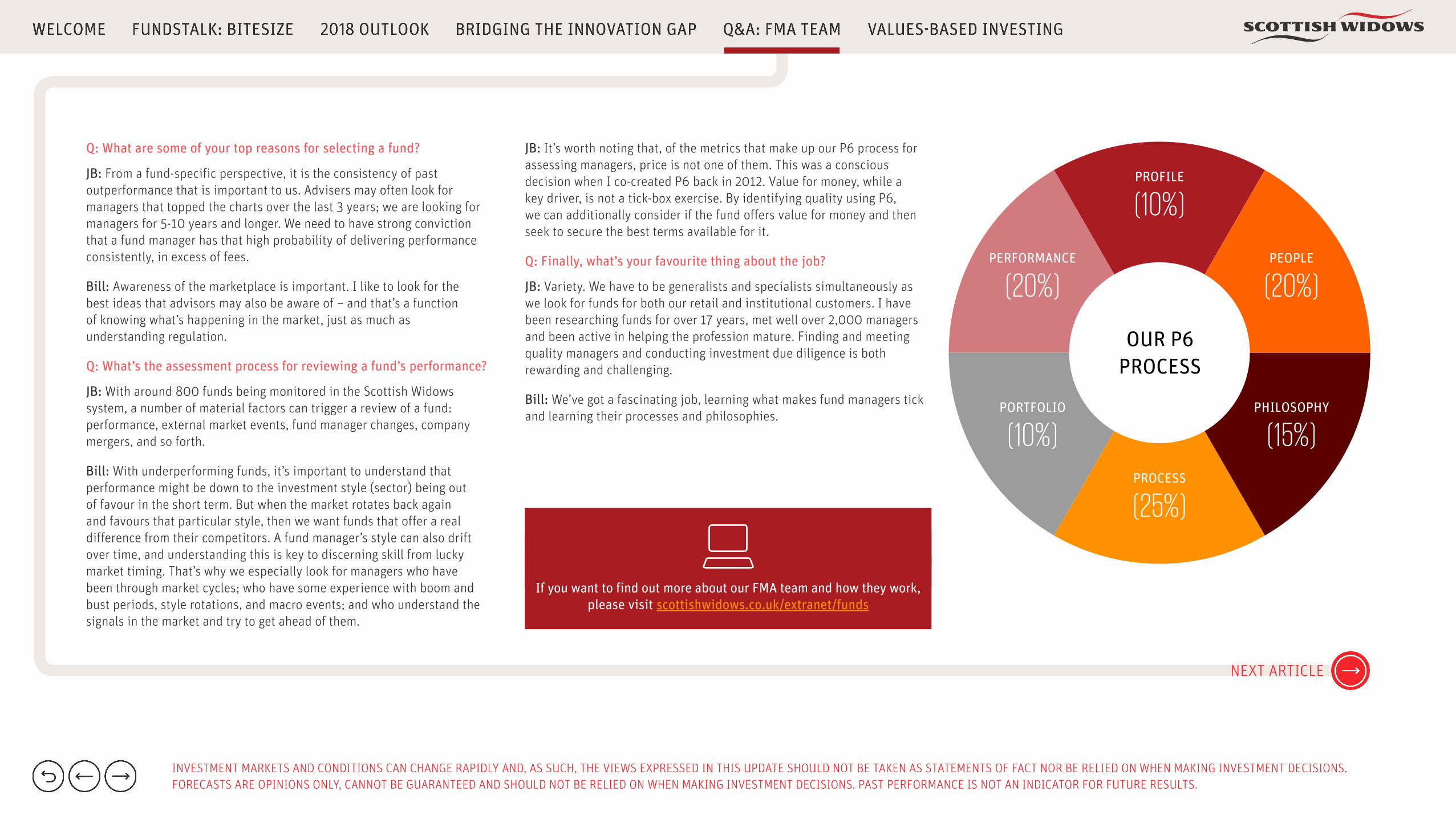

JB: It’s worth noting that, of the metrics that make up our P6 process for assessing managers, price is not one of them. This was a conscious decision when I co-created P6 back in 2012. Value for money, while a key driver, is not a tick-box exercise. By identifying quality using P6, we can additionally consider if the fund offers value for money and then seek to secure the best terms available for it.

Q: Finally, what’s your favourite thing about the job?

JB: Variety. We have to be generalists and specialists simultaneously as we look for funds for both our retail and institutional customers. I have been researching funds for over 17 years, met well over 2,000 managers and been active in helping the profession mature. Finding and meeting quality managers and conducting investment due diligence is both rewarding and challenging.

Bill: We’ve got a fascinating job, learning what makes fund managers tick and learning their processes and philosophies.

If you want to find out more about our FMA team and how they work, please visit scottishwidows.co.uk/extranet/funds

NEXT ARTICLE

OUR P6 PROCESS

PERFORMANCE

(20%)

PORTFOLIO

(10%)

PEOPLE

(20%)

PHILOSOPHY

(15%)

PROFILE

(10%)

PROCESS

(25%)

So what is values-based investing (VBI)? Well, a good number of the financial services professionals I’ve spoken to don’t really know. This highlights a lack of awareness and clarity, which probably comes down to the lack of a common definition. But as one of the fastest growing investment sectors1, it’s increasingly important for investment providers and advisers alike to consider client demand for VBI and how well we’re responding to it.

WHAT IS IT?

VBI is an investment philosophy that considers criteria based on environmental, social and governance (ESG) values as well as potential financial returns. In other words, it caters for clients who want to incorporate their ethical values into their investment portfolio. According to an EY report on sustainable investing, this strategy has ‘grown 107.4% annually since 2012 and accounts for 18% of assets under management in the wealth and asset management industry’.2

KAISIE RAYNER, RESPONSIBLE INVESTMENT SENIOR MANAGER AT SCOTTISH WIDOWS, SHARES HER THOUGHTS ON THE RISE OF VALUES-BASED INVESTING. SHE ASKS WHETHER WE COULD DO MORE TO SERVICE CLIENTS WHO WANT TO REFLECT ETHICAL VALUES IN THEIR INVESTMENT PORTFOLIO.

“VBI ACCOUNTS FOR 18% OF ASSETS UNDER MANAGEMENT IN THE WEALTH AND ASSET MANAGEMENT INDUSTRY.”2

OVER 1,750 SIGNATORIES

The number of signatories of the UN Principles for Responsible Investment since it was established in 2006.

Sustainable investing has ‘grown 107.4% annually since 2012 and accounts for 18% of assets under management in the wealth and asset management industry’.

107.4% GROWTH

THE RISE OF VALUES-BASED INVESTING AND WHAT IT MEANS FOR ADVICE

INVESTMENT MARKETS AND CONDITIONS CAN CHANGE RAPIDLY AND, AS SUCH, THE VIEWS EXPRESSED IN THIS UPDATE SHOULD NOT BE TAKEN AS STATEMENTS OF FACT NOR BE RELIED ON WHEN MAKING INVESTMENT DECISIONS. FORECASTS ARE OPINIONS ONLY, CANNOT BE GUARANTEED AND SHOULD NOT BE RELIED ON WHEN MAKING INVESTMENT DECISIONS.Scottish Widows Limited. Registered in England and Wales No. 3196171. Registered office in the United Kingdom at 25 Gresham Street, London EC2V 7HN. Authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. Financial Services Register number 181655. 27134 01/18

MYTH BUSTING

As with any relatively new concept, there are inevitable misconceptions.

The first is that it’s the preserve of a minority of green investors and millennials.

Auto enrolment and pension freedoms have encouraged consumers to take more personal responsibility for how and where their money is invested. It’s therefore reasonable to assume that clients across the age spectrum will become more engaged with their portfolios. The rise in intergenerational wealth transfer via pension savings has sustainability at its heart and is primarily the concern of clients entering or in retirement.

Macro-economic and legal considerations also contribute to the growth in responsible investing – and neither are confined to millennials. As we grapple with the global challenge of meeting the demand for food, clean water and energy, it stands to reason that demand will increase for investment in sustainable infrastructure projects. And European law as set out in the IORP (Institutions for Occupational Retirement) II directive, states that ESG factors must be included in pension scheme risk assessments.

The second misconception is that clients must sacrifice return to invest in line with their values.

This has repeatedly been shown not to be the case. A recent study from Morgan Stanley3 says:

“Investing in sustainability has usually met, and often exceeded, the performance of comparable traditional investments. This is on both an absolute and a risk-adjusted basis, across asset classes and over time.”

SUPPORTING CLIENTS WITH VBI

If we assume that clients of all ages are increasingly likely to demand that their portfolio invests in a positive future as well as generating positive returns, are we doing enough to cater for demand? I believe our industry must take steps to evolve financial advice and move responsible investing from niche to mainstream. For advisers, this could mean routinely including it as part of their client fact-find process.

There are many funds that meet ESG criteria - the Morgan Stanley study mentioned earlier analysed 10,000 funds and managed accounts. But until the broader investment industry supports VBI with easy to understand and easy to access ‘go-to’ solutions, it’s unlikely to move from niche to mainstream. With the growth in popularity of passive investing, one of the key challenges will be how to satisfy the demand for low cost and passive investing in a fully ethical and responsible way.

There are positive signs that things are changing. The UN Principles for Responsible Investment were established in 2006. Since then, the number of signatories has reached 1,7844. They include large investors such as Vanguard, Fidelity Investors and Scottish Widows, as part of Lloyds Banking Group.

At Scottish Widows we’re committed to moving the debate on. We’re keen to be part of the discussions on issues like default funds of the future and building sustainable portfolios. In the coming months we plan to run a number of events designed to debate and shape the ‘go-to’ solutions of the future. We’ll keep you up to date with news and progress as it comes.

1 Interactive Investor article http://www.iii.co.uk/values-based-investing 2 EY Sustainable investing: the millennial investor, 2017 http://www.ey.com/Publication/vwLUAssets/ey-sustainable-investing-the-millennial-investor-gl/%24FILE/ey-sustainable-investing-the-millennial-investor.pdf 3 http://www.morganstanley.com/ideas/sustainable-investing-performance-potential 4 https://www.unpri.org/about

2

1