2nd quarter 2011 data - relações com...

TRANSCRIPT

2nd Quarter 2011 data

2

Disclaimer

The material that follows is a confidential presentation of general background information about Qualicorp S.A. and its subsidiaries (collectively,

“Qualicorp”) as of the date of the presentation. It is information in summary form and does not purport to be complete. No representation or

warranty, express or implied, is made concerning, and no reliance should be placed on, the accuracy, fairness, or completeness of this information.

This confidential presentation may contain certain forward-looking statements and information relating to Qualicorp that reflect the current views

and/or expectations of Qualicorp and its management with respect to its performance, business and future events. Forward looking statements

include, without limitation, any statement that may predict, forecast, indicate or imply future results, performance or achievements, and may

contain words like “anticipate”, “believe”, “estimate”, “expect”, “forecast”, “plan”, “predict”, “project”, “target” or any other words or phrases of similar

meaning. Such statements are subject to a number of risks, uncertainties and assumptions. We caution you that a number of important factors

could cause actual results to differ materially from the plans, objectives, expectations, estimates and intentions expressed in this presentation,

including: market acceptance of Qualicorp’s products or services; volatility in the healthcare industry, the Brazilian economy and the financial

markets; changes in legislation, accounting standards, taxation and government policies affecting the healthcare sector; ability to stay abreast of

changes in technology; ability to continuously introduce competitive new products and services, while staying competitive in existing ones. In no

event, neither Qualicorp nor any of its affiliates, directors, officers, agents or employees, nor the selling shareholder, placement agents or

underwriters, shall be liable before any third party (including investors) for any investment or business decision made or action taken in reliance on

the information and statements contained in this presentation or for any consequential, special or similar damages.

All forward-looking statements in this presentation are based on information and data available as of the date they were made, and Qualicorp

undertakes no obligation to update them in light of new information or future developments. This presentation and its contents are proprietary

information and may not be reproduced or otherwise disseminated in whole or in part without Qualicorp’s prior written consent.

Securities may not be offered or sold in the United States unless they are registered or exempt from registration under the United States Securities

Act of 1933, as amended. Any offering of securities to be made in the United States will be made solely by means of a confidential offering circular

that may be obtained from the placement agents or the underwriters. Such confidential offering circular will contain detailed information about

Qualicorp and its business and financial results, as well as its financial statements. This presentation does not constitute an offer, or invitation, or

solicitation of an offer, to subscribe for or purchase any securities. Neither this presentation nor anything contained herein shall form the basis of

any contract or commitment whatsoever.

3

Investor Relation Executives

Wilson Olivieri

CFO and Investor Relations Officer

Elton Carluci

Planning, M&A and IR Executive

Heráclito de Brito Gomes Júnior, MD

CEO

Former CEO of Bradesco Saúde

Over 25 years of experience in Brazilian managed care

industry, health consulting and sales

Former member of Odontoprev and Fleury boards

E-Mail: [email protected]

Phone: 55-11-3191-4008

Financial and Administrative Officer of Fidelity BPO and

Fidelity Processadora de Cartões from 2005 to 2008

35 years of experience, including Medial Saúde from 2001 to

2004, Philip Morris, PepsiCo Group among others.

E-Mail: [email protected]

Phone: 55-11-3191-4040

Working with Qualicorp for more than 10 years

Responsible for all M&As, Planning and IR reporting

E-mail: [email protected]

Phone: 55-11-3191-4032

4

Qualicorp and Market Overview

Hyperinflation

Junior - Individual

Salesman

First Affinity

Contract

Foundation of

Qualicorp

General

Atlantic

Carlyle

1986 1987 1997 2008 2010

Until 1994

Private Healthcare

Plan Law

1998

Creation of

ANS

2000

ANS Regulations

on Affinity Plans

2009 2011

Present

First set of

acquisitions

and TPA

Public Co.

55

Qualicorp Has a Unique Business Model and is Strategically

Positioned Within the Healthcare Market

Qualicorp Adds Value to All Constituents

Broker

Benefit

Administration

Health Management

Administration

“Service company” without underwriting / reimbursement risk

Client‟s Ownership

Infrastructure

IT Proprietary

Knowledge / intelligence

Services

Billing

Collection

Call center

Scale

Sales Force

MLR

TPA, HCIT, PBM

and PPO

66

Bridging the Gap and Capitalizing on the Existing Cost

Opportunities of the Private Health System

Health Insurance Company Profitability

Cli

en

t P

rem

ium

Individual Market Price

Administrative Expenses

Brokerage

Claims

Without QualicorpIn

su

ran

ce

Pre

miu

m

Qualicorp Helps to Reduce

Market Costs

Qualicorp Price

Benefit Administrator Fee

Cli

en

t P

rem

ium

Health InsuranceCompany Profitability

Claims

Ins

ura

nc

e P

rem

ium

Administrative Expenses

Brokerage

With Qualicorp

Investment Opportunity and Industry Dynamics

8

Fast Growing, Underpenetrated and Large Addressable Market

Proprietary IT platform and superior operational capabilities

Leading market position in Brazil‟s most attractive markets

Leading Position with Significant Scale and Long-Standing Customer Relationships

Management Team Led by Respected Industry Pioneers

Unique Business Model which Creates Value for All Constituencies and does not take Underwriting nor Reimbursement Risk

Industry-Leading Financial Profile with Proven Track Record

Key Investment Highlights

Multiple Large and Attractive Growth Channels

9

Economic Growth is Driving Healthcare Penetration

08‟-10‟ CAGR: 6.0%

Source: World Health Organization Statistics 2010 – Data as of 2007, World Bank, ANS and Analise Institute.

Dramatic Shift in Income Classes

Classes A/B: monthly income above R$4,855 | Class C: monthly income between R$1,126 and R$4,854 | Class D: monthly income between R$706 and R$1,125 | Class E: monthly income below R$705

56

20

7696

66 93113

13

31

0

50

100

150

200

2003 2008 2014E

Class D/E Class C Class A/B

+18 mm(2003-14E)

+47 mm(2003-14E)

Less Than One-Quarter of Population is Covered

31.8 33.7 35.1 36.9 38.6 40.6 42.145.6

21.3%

23.9%

18.0%18.8%

19.0% 19.7%20.3%

21.9%

2003 2004 2005 2006 2007 2008 2009 2010

Millions of Lives Covered Penetration

(Million of people)

Record low

unemployment

GDP Growth

Significant increase in

income classes A/B/C

Healthcare spending

highly correlated with

disposable income

Private healthcare plans

generally one of the first

things families buy with

disposable income

increases

Low private health plan

penetration

Free Public Health

System has limitations

03‟-10‟ CAGR: 5.3%

10

76%

8%14%2%

Large Addressable Market is one of the Fastest-Growing

Category and Still Under Penetrated

Affinity Market Still Under Penetrated

Source: Target, IBGE, Qualicorp and ANS, as of December 2010.

142M lives

Current estimated potential

affinity market size

24 No plan,

eligible

Affinity

others

Indiv.

plans newQualicorp

affinity

~50M lives

Affinity market is one of the

fastest growing category

within private health plans

Further development

and growth of the

affinity segment will

help alleviate the

burden on the public

health system

Qualicorp is the affinity

market leader: ~10x larger

than the next competitor

Market penetration is

around ~2% of the

estimated potential

addressable affinity

market

Brazil

Population

11

Well Positioned to Aggregate Interests and Demands in the

Affinity Market

Accountants Medical Lawyers DentistsPublic

ServantsBank

EmployeesEngineers

400* 100* 1,000* 500* 400* 300* 300*

Brokerage

Health Insurance

Favorable Demographics

Pooling of Risk

Relationship with the Beneficiary and

Professional Associations

Ability to Negotiate good Terms

* Hypothetical numbers

3,000*

Professional Associations

12

Public Policy Supports Qualicorp Business Model

November 2009 ANS passed resolutions to regulate

relationships between health plan operators, benefits

administrators, and associations

Framework positions Qualicorp for further private health

plan uptake

Regulations dictate strict standards to define

eligible association

Direct relationship between operators and

associations is highly limited

Qualicorp experienced strong growth before resolution was passed and is well-positioned to take advantage of the ANS framework

The Qualicorp Solution

14

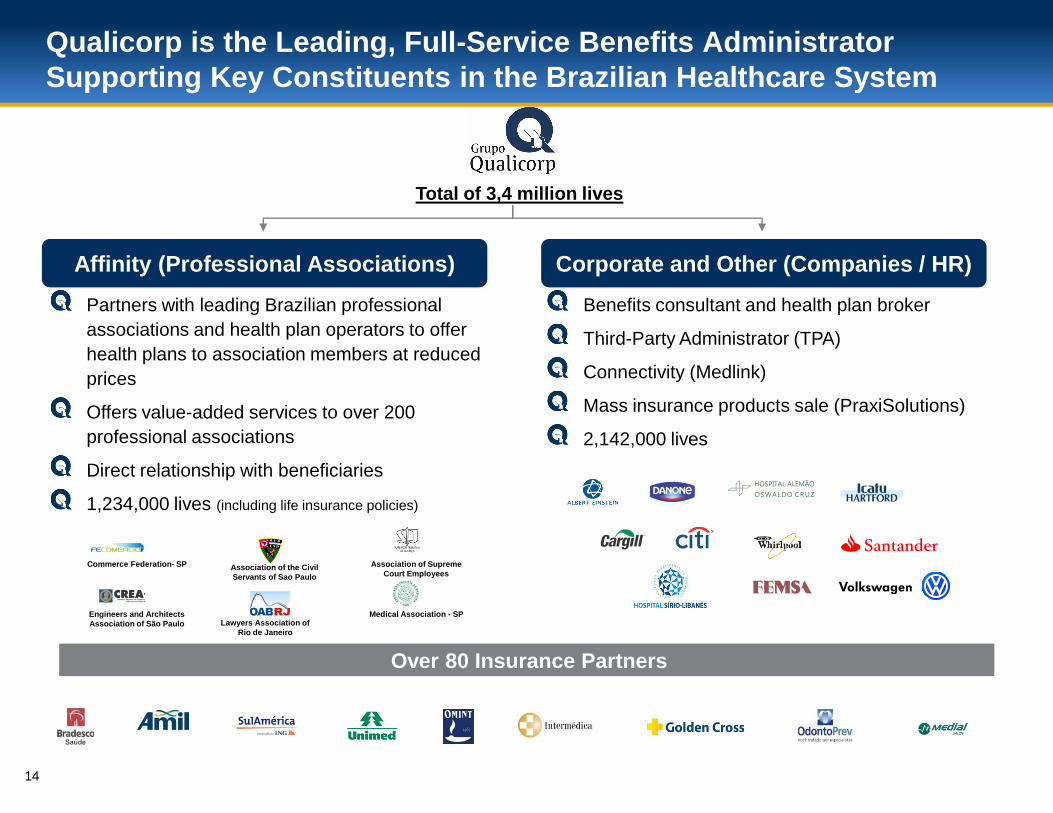

Qualicorp is the Leading, Full-Service Benefits Administrator

Supporting Key Constituents in the Brazilian Healthcare System

Partners with leading Brazilian professional

associations and health plan operators to offer

health plans to association members at reduced

prices

Offers value-added services to over 200

professional associations

Direct relationship with beneficiaries

1,234,000 lives (including life insurance policies)

Association of Supreme

Court Employees

Medical Association - SP

Commerce Federation- SP

Engineers and Architects

Association of São Paulo

Benefits consultant and health plan broker

Third-Party Administrator (TPA)

Connectivity (Medlink)

Mass insurance products sale (PraxiSolutions)

2,142,000 lives

Over 80 Insurance Partners

Affinity (Professional Associations) Corporate and Other (Companies / HR)

Association of the Civil

Servants of Sao Paulo

Lawyers Association of

Rio de Janeiro

Total of 3,4 million lives

15

Underwriting

risk

Unique Affinity Business Model as the Primary Interface with

the Beneficiary

Health Plan Operator

Professional

Association

Individual

Beneficiary

Qualicorp deals directly with the beneficiary

Pro

vid

es

he

alth

ca

re c

ove

rag

e to

be

ne

ficia

ries

Sells and

service direct

the individual

members of

association

Initiates

exclusive

distribution

relationship

Designs and

negotiates

options with

health plan

operators

Delinquency

risk

16

Revenue-sharing

agreements with Qualicorp

provide source of income -

helps attract new members

Improves

negotiating power

Professional Associations

Individual Beneficiaries

Discounts up to 50% compared

to individual plans

Improved

access to

private healthcare

Health Plan Operators

Lower MLRs and zero

delinquency

Most effective

way to address

individuals

Qualicorp Adds Significant Value to All Constituents in

The Affinity Segment

Additional value-added services

Brazilian Government

Improves accessibility of private

healthcare system

Augments association database through

tracking and data management

17

Corporate Segment Extends Qualicorp‟s Reach

Services Provided

Benefits Consulting

Brokerage

TPA / Connectivity

Health Management / Mass insurance products

Source: Company.

# of Lives („000s)

1.5001,481

1.344

394314

171698 644

752

2006 2007 2008 2009 2010 2Q 2011

2,0422,125Corporate & SME

TPA

2,142

Value-added, Consultative Approach Differentiates Qualicorp from Competitors

1,390

18

Sophisticated Marketing Strategies

Captive and Third-Party Brokers Close the

Deal

Captive Salesforce Third-Party Brokers

Large database of more than 6 million names

Unique analytical techniques generate

qualified leads (Business Intelligence Dept)

160 professionals

Receive inbound

leads

Active outbound

calling effort

200+ brokerage

firms with over

2,500 brokers

Lower fixed costs

Benefit from

Company’s

marketing efforts

Marketing campaigns build brand awareness

and generate leads

Call center gathers inbound leads

Direct Marketing Strategy

Indirect Marketing Strategy

19

Significant Barriers to Entry Give Qualicorp a Strong

Competitive Advantage

Value Proposition for All Constituents Involved

Long-Standing Relationships with the Associations and Beneficiaries

High Switching Costs for Associations

Distribution Platform with good Brand, Marketing and Distribution Channels

(individual door to door sales process)

Proprietary IT Platform and Operational Capabilities

Solid Health Plan Operator Partnerships

Significant Scale Creates Positive Negotiation Conditions With Health Plan

Operators

Growth Strategy

21

Multiple Avenues to Continue to Drive Long Term

Sustainable Growth

Organic

Geographic

expansion

Cross-sell

new products

Acquisitions /

Partnerships

Opportunities

from Market

Evolution

Currently, Qualicorp is pursuing all of these growth avenues

1

2

3

4

5

22

Significant Organic Growth Opportunities1

Penetrate Existing

Associations

Add New Associations

Expand Membership of

Existing Associations

23

25

46

14

55

7

44

Expand Geographically to New Markets in Brazil

Target high growth markets

outside São Paulo and Rio

de Janeiro

Identify attractive new

regions

Leverage strong local

partners

Successful expansions to-

date into Brasilia, Salvador,

Recife and Belo Horizonte

2

Current Geographic Location

Geographic Expansion

AM

AC

RR AP

PA

MT

RO

MS

GO

TO

MA

PI

BA

CE RNPBPEAL

SE

RS

SC

PR

SP

MG

ES

RJ

Current MarketsPriority New

Markets Rest of Brazil

With Health Plans Without Health Plans

(In million of lives)

24

Salvador Case Study

Aggressive local media

Highlights

38.067

1.523

11.652

31.863

2008 2009 2010 2Q 2011

# of Associations: 7 14 17 21

# of lives

2

Local presence with own management

Leverage strong local partners

25

7,1%

11,0%

25,4%

6,0%

2008A 2009A 2010A 2Q11A

Cross-Sell New Products and Services to Existing Customers

151

2.142

Medical Management Corporate

and Others

Only 7% of total

Corporate client base

Affinity (Professional Associations)

Dental insurance plans

Other non-risk products insurance

(life, auto, assistance)

Corporate (Companies / HR)

Qualicorp Health Management, TPA,

Connectivity and Mass insurance

products

Represents unique product offering

relative to other brokers / benefits

consultants

Take advantage of brand, association relationships, providerrelationships and existing customer base

% Cross Selling (% of Lives)

Corporate and Other (Lives in „000s)

3

26

Grow Through Selective Acquisitions and Strategic

Partnerships

Build scale and expand geographically through selected acquisitions of affinity

brokerage portfolios

Fragmented market Qualicorp is the natural consolidator

Operational leverage

Add new capabilities

Broaden product offering

Cross-sell new capabilities

Disciplined acquirer with strict selection criteria and successful integration track

record

1-Athon-Bruder

(Corporate and H.M.)

3-Med Company

(Affinity)

5-Medlink

(Connectivity)

7-Divicom

(Affinity)

2-Salutar

(Affinity)

4-75% stake in

Vectorial (Affinity)

6-Acquisition of the

Remaining 25% of Vectorial

8-Unimed-Rio

(Selected Portfolio)

June 2009 December 2009 July 2010 April 2011

4

Jun/Jull 2011 July 2011

9-PraxiSolution

(Mass Products)

27

Significant collection of medical data

Acquisition of one of the largest connectivity

companies in Brazil (Medlink)

12 million transactions with 17,000

providers nationwide

Acquisition of PraxiSolutions

Leveraging distribution channels

Leverage Existing Platform to Expand as Healthcare Market

Evolves

Healthcare

Information

Technology

(HCIT)

Mass Insurance

Products

PPO and PBM Being evaluated according to the opportunity

5

Third Party

Administrator

(TPA)

Services already provided by Qualicorp

Leading TPA in Brazil

Qualicorp Financial Overview

29

Multiple Recurring Revenue Streams

Payer Recurrence

Individual Beneficiary

Health Plan Operator

Monthly

Monthly

Monthly

Initial

Initial

Benefits Admin Fee

Brokerage

Royalty

Membership Fee

New Sales Fee

Around 90% of all revenues are recurring

Revenue to Qualicorp

30

Margin (%)

42

64

78

102

25

54

2007 2008 2009 2010 2Q 2010 2Q 2011

Consistent Revenue Growth and Profitability

167

228

309

470

111

160

2007 2008 2009 2010 2Q 2010 2Q 2011

64

89101

174

46

63

2007 2008 2009 2010 2Q 2010 2Q 2011

YoY growth (%)

YoY growth (%)

Adjusted EBITDA (R$ million) (1)Net Revenues (R$ million)

Adjusted Cash Net Income (R$ million) (1)

YoY growth (%)

(1) Excludes non recurring expenses.

Note: Cash Net Income = IFRS Net Income + Non-recurring/non-cash expenses + Stock options plan expenses.

37% 36% 52% 39% 13% 72%

52% 22% 31%

44%- 37%-

116%-

39% 33% 37% 39%40%

31

Key Takeaways

Powerful Organic Growth and Attractive Acquisition

Opportunities

Unique Business Model Creates Value for All

Constituencies

Large and Underpenetrated Market