2q11 disclosure and results

TRANSCRIPT

1

Earnings Release | Conference Call – 2Q11 August 09th, 2011

2

Agenda

Ricardo Ribeiro

COO

Roberto Senna

CEO

Carlos Wollenweber

CFO | IR

2Q11 Highlights

Operating Highlights

Financial Highlights

Highlights

3

1. Adjusted by non-cash expenses (Stock-Options Program).

2Q11 1H11

Launched PSV% Direcional

R$ million 288 511

Contracted PSV% Direcional

R$ million 169 344

VSO (Sales Over Total Supply) % PSV 18.5% 31.5%

Net Revenues R$ million 245 479

Adjusted Net Income¹ R$ million 41 91

Adjusted Net Margin¹ 17% 19%

4

June

R$ 56.4 million

R$ 75,000

R$ 1,770

752

Launch

Total PSV

Price (R$/unit)

Price (R$/sq.m)

# Units

Manaus - AM Location

Total Ville Vida Nova – 3rd phase

June

R$ 48.0 million

R$ 75,000

R$ 1,769

640

Launch

Total PSV

Price (R$/unit)

Price (R$/sq.m)

# Units

Marituba - PA Location

Bella Città Algodoal – 3rd phase

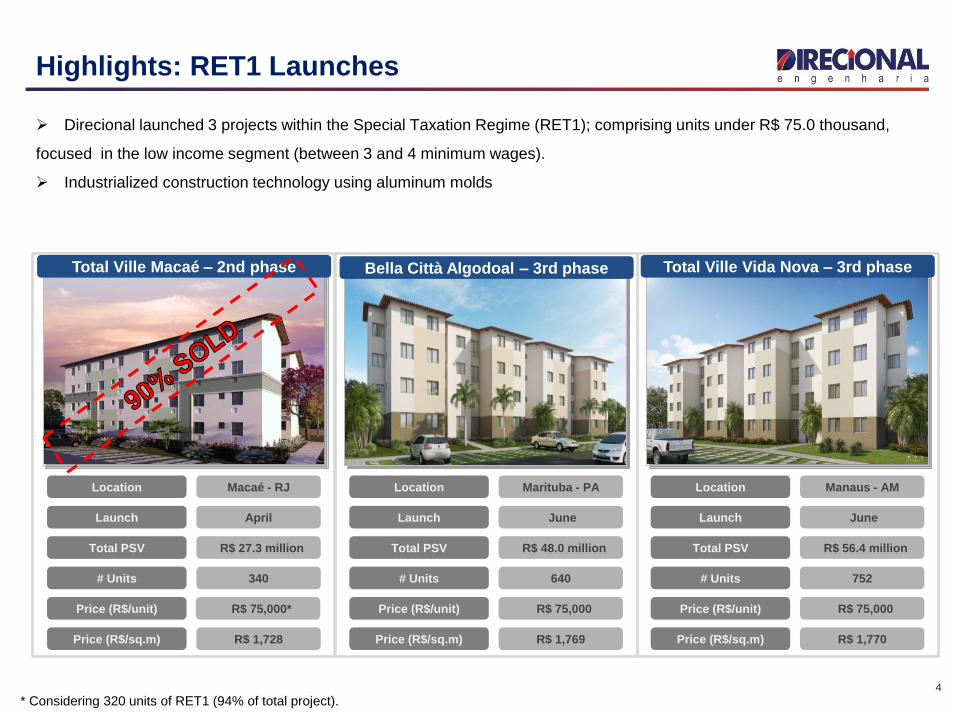

Highlights: RET1 Launches

Direcional launched 3 projects within the Special Taxation Regime (RET1); comprising units under R$ 75.0 thousand,

focused in the low income segment (between 3 and 4 minimum wages).

Industrialized construction technology using aluminum molds

* Considering 320 units of RET1 (94% of total project).

April

R$ 27.3 million

R$ 1,728

340

Launch

Total PSV

Price (R$/unit)

Price (R$/sq.m)

# Units

Macaé - RJ Location

Total Ville Macaé – 2nd phase

R$ 75,000*

New Opportunities in 0-3 Minimum Wages Segment

5

# Units

Segment

Development

Infrastructure

3,511

MCMV – 0-3 mw

R$ 149,2 million

R$ 41,4 million

Total PSV R$ 190,6 million

Location Manaus - AM

“Residencial Meu Orgulho” Minha Casa Minha Vida Program

Minha Casa, Minha Vida 2nd phase was approved in June

Launch 2Q10

400,000

1,200,000400,000

600,000

200,000

200,000

Income limit R$ 1.6k limit R$ 3.1k limit R$ 5.0k

MCMV1

BRL 34 Billion1,000,000 Units

MCMV2

BRL 72 Billion1,000,000 Units

6

Operating Highlights

Launches

Sales

Land Bank

Inventory

Ricardo Ribeiro

Operating Highlights

Total

(R$'000)

% Direcional

(R$'000)

1 Verano Residencial - 1st Phase April Belém - PA 36,968 36,931 184 539 Medium

2 Total Ville Macaé - 2nd Phase - RET 1 April Macaé - RJ 27,264 13,632 340 1,145 Popular

3 Parque Ponta Negra - 3rd Phase April Manaus - AM 47,711 47,706 137 820 Upper-Middle

4 Tulip Inn Savassi - Hotel June Belo Horizonte - MG 86,238 85,376 240 240 Commercial

5 Total Ville Vida Nova - 3rd Phase - RET 1 June Manaus - AM 56,400 56,344 752 3,848 Popular

6 Bella Città Algodoal - 3rd Phase - RET 1 June Marituba - PA 48,000 47,995 640 4,938 Popular

302,581 287,984 2,293 11,530

1 Acquisition of Project - Parque Ponta Negra May Manaus - AM 131,289 131,289 545 n/a Medium

433,870 419,272 2,838 11,530

# of Units

Launched

Total Units

(All Phases)Segment

Launches 2Q11

Launches + Project Acquisition

2Q11 Projects Date City - State

PSV

158 288 300

511 191

191 131

131

2Q10 2Q11 1H10 1H11

Launched PSV (R$million)

Development 0-3 mw projects Project Acquisition

176

710 783

1,067

511

2007 2008 2009 2010 1H11

Evolution Launched PSV (R$million)

7

Launches

+82%

CAGR 07-10: 82%

+71%

Launched PSV

(R$ million)

Launched PSV - Evolution

(R$ million)

54.6%65.6%

58.1% 56.2%

45.4% 37.7%

9.7%

34.4%

4.2%

34.0%

2Q10 2Q11 1H10 1H11North Midwest Southeast

Tulip Inn Savassi - Hotel – PSV R$ 85.4 MM Total Ville Vida Nova 3rd phase – PSV R$ 56.4 MM Verano Residencial – PSV R$ 36.9 MM

Launches Breakdown

8

Launches

(Segment Breakdown – PSV)

Launches

(Geographic Breakdown - PSV)

Parque Ponta Negra – PSV R$ 47.7 MM Total Ville Macaé 2nd phase – PSV R$ 13.6 MM Bella Cittá Algodoal – PSV R$ 47.9 MM

58.9%

39.1%

24.2%

24.3%

36.5%

30.4%

9.2%

47.2%

13.7%

49.4%

7.8%

11.8%

10.8%

10.4%16.7% 9.7%

2Q10 2Q11 1H10 1H11

0 - 3 MW Popular Medium Upper Middle Commercial

# Units

Segment

Price (R$/unit)

Price (R$/sq.m)

240

Commercial

R$ 347.9 thousand

R$ 15,590

Total PSV R$ 86.2 million

Location Belo Horizonte - MG

Hotel Tullip Inn

2Q11 Highlights

9

# Units

Segment

Price (R$/unit)

Price (R$/sq.m)

820

medium/upper middle

R$ 395.2 thousand

R$ 3,167

Total PSV R$ 324.1 million

Location Manaus - AM

Acquisition of Parque Ponta Negra

PSV of R$ 85.4 million (% Direcional);

25% of units sold to BHG;

The goal is to sell all the remaining units during the

project development.

Acquisition of 60% in the residential part of Parque

Ponta Negra in Manaus;

Total PSV of residential towers: R$ 324 million;

65% of launched units already sold

58.9%

39.1%

24.2%

24.3%

36.5%

30.4%

9.2%

47.2%

13.7%

49.4%

7.8%

11.8%

10.8%

10.4%

18.1% 10.4%

2Q10 2Q11 1H10 1H11

0 - 3 MW Popular Medium Upper Middle Commercial

77.9%

48.1%

72.8%

40.1%

13.2%

19.8%

17.0%

21.7%

8.9%

32.1%

10.2%

38.2%

2Q10 2Q11 1H10 1H11

North Midwest Southeast

127

441 661

1,037

344

2007 2008 2009 2010 1H11

133 169 297 344

191

191

89

89

2Q10 2Q11 1H10 1H11Development 0-3 mw projects Project Acquisition

10

Sales

CAGR 07-10: 101%

+27%

+16%

Contracted PSV

(R$ million)

Contracted PSV - Evolution

(R$ million)

Sales

(Geographic Breakdown)

Sales

(Segment Breakdown)

33.8%

38.3%

20.6%

23.7%

19.4% 20.8%

27.6%

22.1%18.5%

1Q10 2Q10 3Q10 4Q10 1Q11 2Q11

With 0.3. MW project Without 0.3. mw project

89%

17%

87%

48%

20%

4%

27%

4%

31%

3%

14%

1%2Q10

3Q10

4Q10

1Q11

2Q11

3M 6M 9M 12M 15M

69%

92%

67%

97%

51%*

11

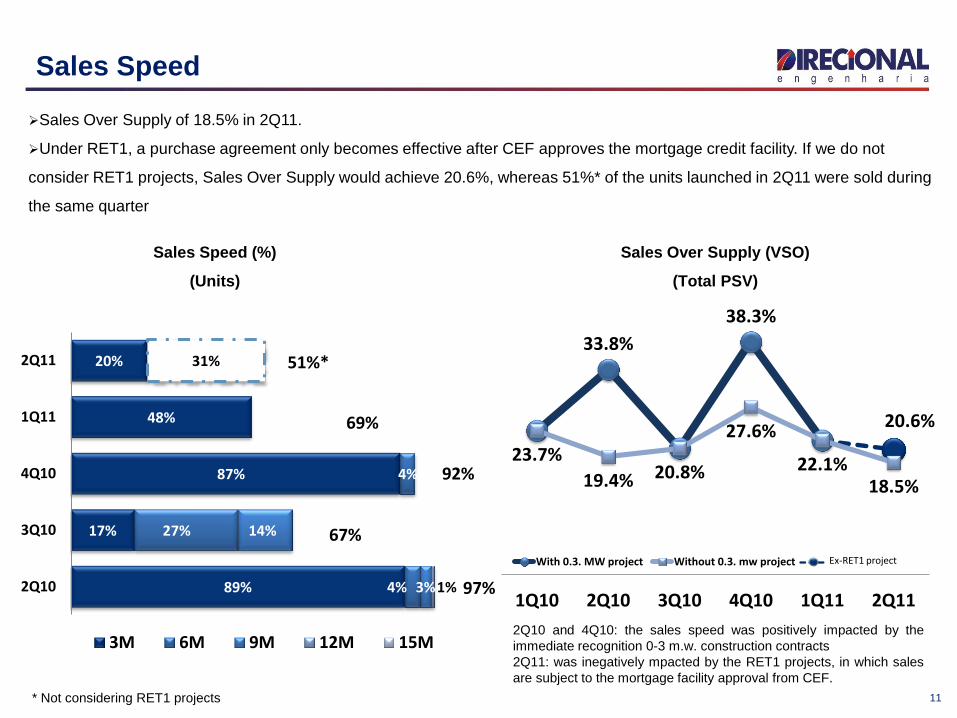

Sales Speed

Sales Over Supply of 18.5% in 2Q11.

Under RET1, a purchase agreement only becomes effective after CEF approves the mortgage credit facility. If we do not

consider RET1 projects, Sales Over Supply would achieve 20.6%, whereas 51%* of the units launched in 2Q11 were sold during

the same quarter

Sales Over Supply (VSO)

(Total PSV)

Sales Speed (%)

(Units)

2Q10 and 4Q10: the sales speed was positively impacted by the

immediate recognition 0-3 m.w. construction contracts

2Q11: was inegatively mpacted by the RET1 projects, in which sales

are subject to the mortgage facility approval from CEF.

33,8% 38,3%

21,1%

23,7% 19,4% 20,8% 27,6% 22,1% 18,9%

1

1Q10 2Q10* 3Q10 4Q10* 1Q11 2Q11*

Com Projetos 0-3 SM Ex projetos 0-3 SM Ex Projetos RET1

* Not considering RET1 projects

Ex-RET1 project

12

Concluded Projects - 2Q11

Total

(R$'000)

% Direcional

(R$'000)

1 Equilibrium Manaus - AM 49,501 43,561 136

2 Águas do Madeira Porto Velho - RO 61,520 40,973 426

3 Grand Prix Manaus - AM 42,026 36,983 192

4 Lake View Resort Brasília - DF 89,513 87,812 232

5 Garden Club - 1st Phase Porto Velho- RO 34,394 27,515 313

6 Dream Park Serra - ES 44,629 35,704 282

Completed Projects - 2Q11 321,584 272,547 1,581

Completed Projects - 2Q11 City - State

PSV

# of Units

7,004 6,986 152 118

288

1Q11 ACQUIRED LANDSON 2Q11

REVIEW OFPROJECTS

LAUNCHES IN 2Q11 2Q11

6,757 6,986 580 160

511

4Q10 ACQUIRED LANDSON 1H11

REVIEW OFPROJECTS

LAUNCHES IN 1H11 1H11

13

Land Bank Acquisitions

In 2Q11, Direcional acquired 2 lots with total PSV of R$ 152.3 million* (67% paid through financial or physical swap);

Average acquisition cost was12% of the total PSV in 2Q11.

In 1H11, Direcional acquired 6 lots with total PSV of R$ 580.0 million (59% paid through financial or physical swap);

Average acquisition cost was 14% of the total PSV in 1H11.

Land Bank Inventory in 06/30/2011 - Geographic Breakdown

* In the Operational Preview released on 05 July, we reported a of R$ 254.7 million. However, in July we canceled the purchase of a lot

located in the city of Belo Horizonte during the Due Diligence process, with potential PSV of R $ 102.3 million

Land Bank Acquisitions 2Q11

(PSV - R$ million)

Land Bank Acquisitions 1H11

(PSV - R$ million)

Average % # Units Usable Area

Total % Direcional Direcional (sq. m) R$/Unit R$/sq.m

MG 3,582,221 2,637,310 73.6% 27,234 1,551,187 131,535 2,309

DF 2,715,609 1,573,977 58.0% 19,565 1,111,915 138,799 2,442

AM 954,069 941,598 98.7% 5,529 353,674 172,557 2,698

PA 937,455 937,361 99.9% 8,335 458,929 112,472 2,043

SP 541,420 445,158 82.2% 2,849 173,856 190,039 3,114

RO 298,557 270,030 90.4% 2,806 133,083 106,400 2,243

RJ 139,367 77,051 55.3% 937 55,750 148,738 2,500

ES 129,361 103,489 80.0% 752 51,745 172,023 2,500

TOTAL 9,298,060 6,985,975 75.1% 68,007 3,890,138 136,722 2,390

State PSV (R$'000) Average Price

ES1.5%

AM13.5%

MG37.8%

RO3.9%

SP6.4%

PA13.4%

DF22.5%

RJ1.1%

Manaus Total Ville AM Under construction 3,848 2,136

Total Ville Bella Cittá PA Under construction 4,938 3,316

Total Ville Marabá PA Under construction 5,604 4,664

Allegro Residencial Club AM Under construction 1,648 704

Setor Total Ville DF Under construction 4,362 2,064

Total Ville Porto Velho RO Under construction 2,852 1,868

Dream Park ES Under construction 1,034 752

Eliza Miranda AM Under construction 1,406 128

Cachoeiras do Madeira RO Under construction 1,278 426

Total Ville Macaé RJ Under construction 1,145 399

Águas Claras DF To be Launched 1,148 1,148

Floramar MG To be Launched 1,172 1,172

Granjas Werneck MG To be Launched 15,000 15,000

Sítio São João MG To be Launched 2,500 2,500

Ferroeste MG To be Launched 2,388 2,388

Samambaia DF To be Launched 14,614 14,614

Total 64,937 53,279

Project Status Total UnitsUnits to be

launched

14

Land Bank Breakdown Land Bank of R$ 7.0 billion with potential to build 68,007 units;

Average acquisition cost is 9.3% of total PSV (76.7% paid through financial or physical swap);

78.3% of units (60.0% of PSV) to be lanched are related to large scale projects.

Geographic Distribution (PSV)

(% Direcional)

“MINHA CASA, MINHA VIDA”

49.9k units elegible for the program

73.4% of total land bank

Segment Breakdown

(PSV)

Pipeline of Projects

Popular, 52.8%

Commercial, 4.2% Medium,

36.1%

Upper Middle,

6.9%

Total % Direcional

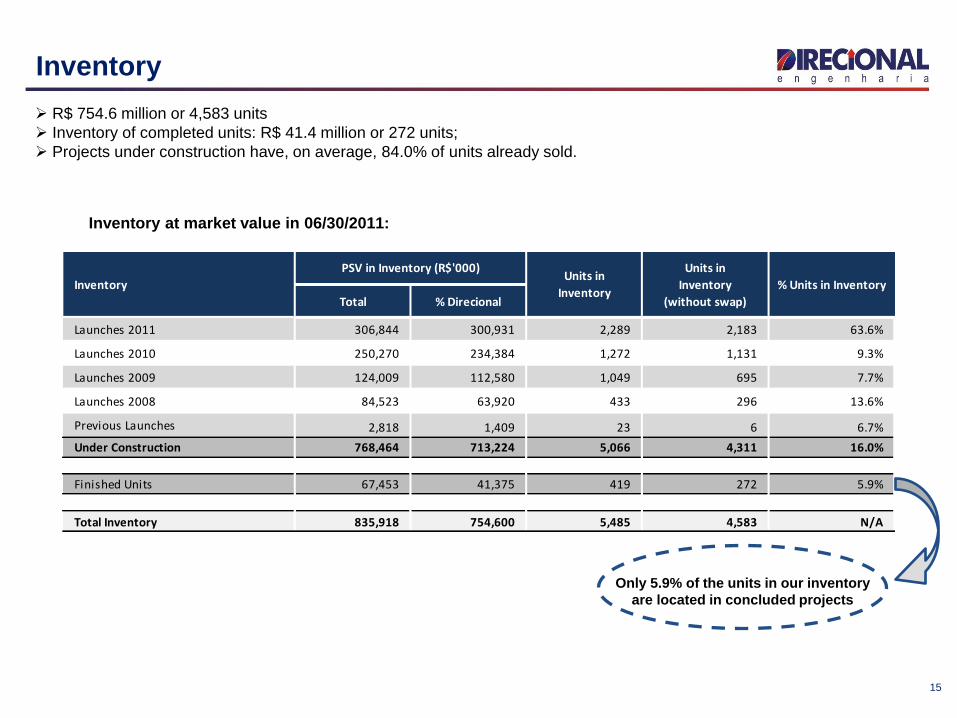

Launches 2011 306,844 300,931 2,289 2,183 63.6%

Launches 2010 250,270 234,384 1,272 1,131 9.3%

Launches 2009 124,009 112,580 1,049 695 7.7%

Launches 2008 84,523 63,920 433 296 13.6%

Previous Launches 2,818 1,409 23 6 6.7%

Under Construction 768,464 713,224 5,066 4,311 16.0%

Finished Units 67,453 41,375 419 272 5.9%

Total Inventory 835,918 754,600 5,485 4,583 N/A

Inventory

PSV in Inventory (R$'000)Units in

Inventory

Units in

Inventory

(without swap)

% Units in Inventory

15

Inventory

R$ 754.6 million or 4,583 units

Inventory of completed units: R$ 41.4 million or 272 units;

Projects under construction have, on average, 84.0% of units already sold.

Inventory at market value in 06/30/2011:

Only 5.9% of the units in our inventory

are located in concluded projects

16

Financial Highlights

Financial Performance

Liquidity Indicators

Results to be Recognized

Performance Shares

Carlos Wollenweber

Financial Highlights

56 64 106 130

35.4%

29.8%36.2%

30.3%33.6%

26.2%

34.3%

27.1%

2Q10 2Q11 1H10 1H11

Gross Margin Ex- SFH (%) Gross Margin (%)

63.4 102.3 263.2 377.6 781.9 478.7

24.0% 21.1%24.5% 22.5% 22.6%

19.1%

2006 2007 2008 2009 2010 1H11

Adjusted net Margin (%)

165 245

308

479

2Q10 2Q11 1H10 1H11

+48%

+55%

17

Financial Highlights

Net Margin: Adjusted by non-cash expenses (Stock-Options Program).

Gross Margin Ex-SFH: excluding the costs of funding allocated in the cost of production

Net Revenues

(R$ million)

CAGR: 87,4%

Net Revenues - Evolution

(R$ million)

15%

+23%

Gross Profit and Gross Margin

41 41

78 91

24.8%16.6%

25.5%

19.1%

2Q10 2Q11 1H10 1H11

Adjusted net Margin (%)

21 58

36

114

12.2%23.0%

11.2%

23.4%

2Q10 2Q11 1H10 1H11

% Gross Revenue

18

Financial Highlights

Gross Revenue Breakdown 1H11

Adjusted Net Income and net Margin¹

(R$ million)

-1%

+16%

Revenue of Services

+179%

+222%

1. Adjusted by non-cash expenses (Stock-Options Program).

Development, 76.6%

Management Fee, 0.8%

0-3 MW Projects, 22.1%

Brokerage, 0.5%

45 48

87 106

27.1%19.7%

28.3%

22.1%

2Q10 2Q11 1H10 1H11

Adjusted EBITDA Margin (%)

4 7 8 12

1.2%

3.9%

1.5%

3.0%2.6% 2.3%

2Q10 2Q11 1H10 1H11

% Sales % Sales without 0-3 m.w. projects

11 17 19

34

6.7% 7.1% 6.3% 7.0%

2Q10 2Q11 1H10 1H11

% Net revenue

19

Financial Highlights

Adjusted Ebitda and Ebitda Margin¹

Adjusted G&A¹ (R$ million) Commercial Expenses (R$ million)

+57%

+73%

+67%

+48%

+8%

+22%

1. Adjusted by non-cash expenses (Stock-Options Program).

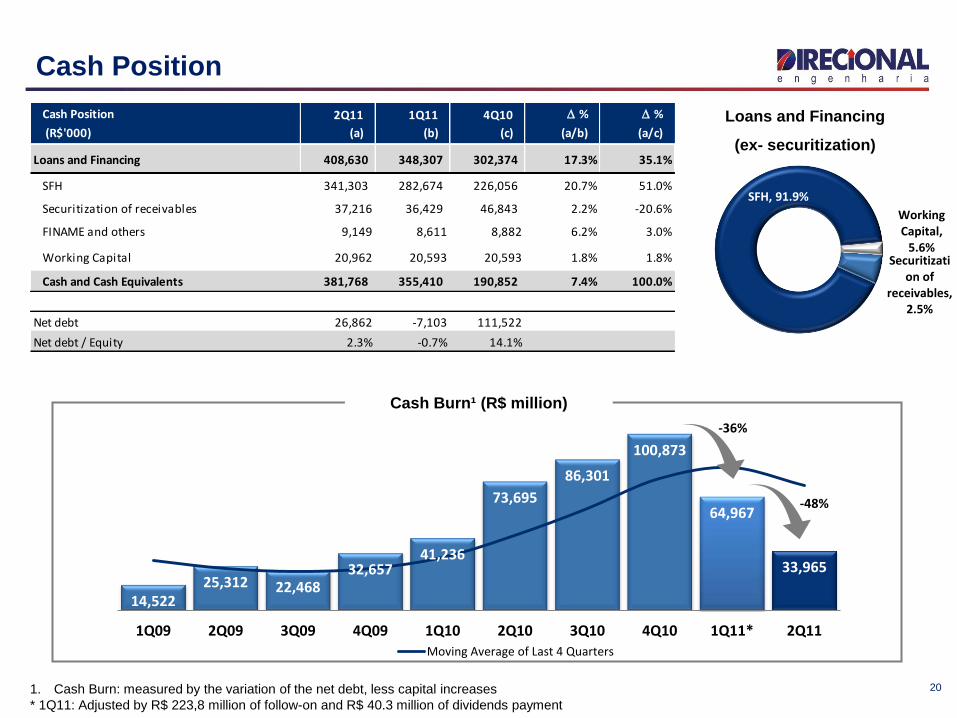

14,52225,312 22,468

32,65741,236

73,695

86,301

100,873

64,967

33,965

1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10 1Q11* 2Q11

Moving Average of Last 4 Quarters

20

Cash Position

Cash Burn¹ (R$ million)

Loans and Financing

(ex- securitization)

-36%

-48%

1. Cash Burn: measured by the variation of the net debt, less capital increases

* 1Q11: Adjusted by R$ 223,8 million of follow-on and R$ 40.3 million of dividends payment

Cash Position 2Q11 1Q11 4Q10 D % D %

(R$'000) (a) (b) (c) (a/b) (a/c)

Loans and Financing 408,630 348,307 302,374 17.3% 35.1%

SFH 341,303 282,674 226,056 20.7% 51.0%

Securitization of receivables 37,216 36,429 46,843 2.2% -20.6%

FINAME and others 9,149 8,611 8,882 6.2% 3.0%

Working Capital 20,962 20,593 20,593 1.8% 1.8%

Cash and Cash Equivalents 381,768 355,410 190,852 7.4% 100.0%

Net debt 26,862 -7,103 111,522

Net debt / Equity 2.3% -0.7% 14.1%

SFH, 91.9%

Securitization of

receivables, 2.5%

Working Capital,

5.6%

Book Value 2Q11 1.107

(+) Results to be Recognized 413

Adjusted Book Value 1.520

Market Cap (08/05/2011) 1.529

Market Cap/Adjusted BV 1,01

Adjusted Book Value (R$ million)

40,0%52,3%

7,6%

2011 2012 2013+

21

Deferred Results

REF Recognition Schedule

Results to be Recognized (R$'000) 2Q11 1Q11 4Q10 D % D %

(a) (b) (c) (a/b) (a/c)

Deferred revenues Consolidated (1+2) 413.476 382.339 404.563 8,1% 2,2%

Deferred costs 1.076.829 967.047 1.011.455 11,4% 6,5%

Deferred results 663.353 584.708 606.892 13,5% 9,3%

Deferred results - Margin 38,4% 39,5% 40,0% -2,9% -4,0%

Deferred revenues Development (1) 312.496 325.687 315.467 -4,0% -0,9%

Deferred costs 723.042 762.873 740.269 -5,2% -2,3%

Deferred results 410.545 437.186 424.802 -6,1% -3,4%

Deferred results - Margin 43,2% 42,7% 42,6% 1,4%

Deferred revenues 0-3 mw projects (2) 100.979 56.652 89.096 78,2% 13,3%

Deferred costs 353.787 204.174 271.186 73,3% 30,5%

Deferred results 252.808 147.522 182.090 71,4% 38,8%

Deferred results - Margin 28,5% 27,7% 32,9%

22

Shares Performance Since IPO

Since IPO

DIRR3: +4,2%

IBOVESPA: -6,2%

IMOB: -1,3%

0

20

40

60

80

100

120

140

160

-

1.000

2.000

3.000

4.000

5.000

6.000

7.000

8.000

9.000

10.000

19

-no

v-0

9

3-d

ez-0

9

16

-dez

-09

4-j

an-1

0

15

-jan

-10

29

-jan

-10

11

-fe

v-1

0

26

-fe

v-1

0

11

-mar

-10

24

-mar

-10

7-a

br-

10

20

-ab

r-1

0

4-m

ai-1

0

17

-mai

-10

31

-mai

-10

15

-ju

n-1

0

28

-ju

n-1

0

12

-ju

l-1

0

26

-ju

l-1

0

10

-ago

-10

24

-ago

-10

13

-set

-10

30

-set

-10

14

-ou

t-1

0

27

-ou

t-1

0

10

-no

v-1

0

26

-no

v-1

0

9-d

ez-1

0

27

-dez

-10

10

-jan

-11

21

-jan

-11

4-f

ev-

11

17

-fe

v-1

1

2-m

ar-1

1

17

-mar

-11

30

-mar

-11

12

-ab

r-1

1

27

-ab

r-1

1

10

-mai

-11

23

-mai

-11

3-j

un

-11

16

-ju

n-1

1

30

-ju

n-1

1

Pre

ço d

a A

ção

Vo

lum

e (

R$

mil)

Volume (R$ mil)

0

20

40

60

80

100

120

140

160

-

1.000

2.000

3.000

4.000

5.000

6.000

7.000

8.000

9.000

10.000

18

-No

v-0

9

02

-De

c-0

9

15

-De

c-0

9

30

-De

c-0

9

14

-Jan

-10

28

-Jan

-10

10

-Fe

b-1

0

25

-Fe

b-1

0

10

-Mar

-10

23

-Mar

-10

06

-Ap

r-1

0

19

-Ap

r-1

0

03

-May

-10

14

-May

-10

28

-May

-10

14

-Ju

n-1

0

25

-Ju

n-1

0

08

-Ju

l-1

0

23

-Ju

l-1

0

06

-Au

g-1

0

23

-Au

g-1

0

10

-Se

p-1

0

29

-Se

p-1

0

13

-Oct

-10

26

-Oct

-10

09

-No

v-1

0

25

-No

v-1

0

08

-De

c-1

0

23

-De

c-1

0

07

-Jan

-11

20

-Jan

-11

03

-Fe

b-1

1

16

-Fe

b-1

1

01

-Mar

-11

16

-Mar

-11

29

-Mar

-11

11

-Ap

r-1

1

26

-Ap

r-1

1

09

-May

-11

20

-May

-11

02

-Ju

n-1

1

15

-Ju

n-1

1

29

-Ju

n-1

1

Sto

ck P

erf

orm

ace

Vo

lum

e (

R$

'00

0)

Average Volume (21 days) Direcional Ibovespa IMOB

23

Disclosure

This presentation contains certain forward-looking statements concerning the business prospects,

projections of operating and financial results and growth potential of the Company, which are based on

management’s current expectations and estimates of the future performance of the Company. Although the

Company believes such forward-looking statements are based on reasonable assumptions, it can give no

assurance that its expectations will be achieved. Expectations and estimates that are based on the future

prospects of the Company are highly dependent upon market behavior, Brazil’s political and economic

situation, existing and future regulations of the industry and international markets and, therefore, are

subject to changes outside the Company’s and management’s control. The Company undertakes no

obligation to update any information contained herein or to revise any forward-looking statement as a result

of new information, future events or other information.

24

Contacts

Carlos Wollenweber CFO | IR Officer

Lucas Bousas IR Analyst

Paulo Sousa IR Assistant

www.direcional.com.br

+55 (31) 3214-6200

+55 (31) 3214-6450