acetic acid • vinyl acetate - orbichemorbichem.com/userfiles/kichem...

TRANSCRIPT

Acetic Acid • Vinyl Acetate

Keiji Wakatsuki

Tecnon OrbiChem Seminar at KICHEM 2012Seoul - 2 November, 2012

KICHEM 2012PRESENTATION OUTLINE

• Current Acetic Acid Market Conditions

• Major Downstream Markets

• Summary and Conclusions

Source: Tecnon OrbiChem

KICHEM 2012

TECNON ORBICHEM’S VIEW OF THE MARKETAcetic Acid• Global acetic acid markets have not been as robust in 2012 as

originally expected due to ongoing economic headwinds in Europe and overcapacity in Asia. Market participants expected to retain a wait-and-see attitude in Q3-Q4.

• Despite the gloomy macro-economic outlook, global acetic acid consumption was expected to increase by more than 5% in 2012 compared to 2011.

• Global acetic acid prices spiked briefly in March-April 2012 but fell just as quickly as major production outages failed to offer long-term support. Production problems in the US led to moderate price increases in August.

• Capacity increases are set to continue in China for next 1-2 years, but the period of seemingly non-stop acetic acid plant expansions in the country is coming to an end.

• Global utilisation rates at 70-75% in 2012 as producers cut production in order to reduce supplies and maintain margins.

Source: Tecnon OrbiChem

Total 201217.949 Million Tons

6%

4%

3%

12%

9%

16%

50%

Americas

W Europe

NE Asia

SE Asia

ME/Africa

E Europe

China

Source: Tecnon OrbiChem

KICHEM 2012

WORLD CAPACITY TO PRODUCE ACETIC ACID

1%

4%

15%

15%

29%

21%

15%

Total 200510.554 Million Tons

Source: Tecnon OrbiChem

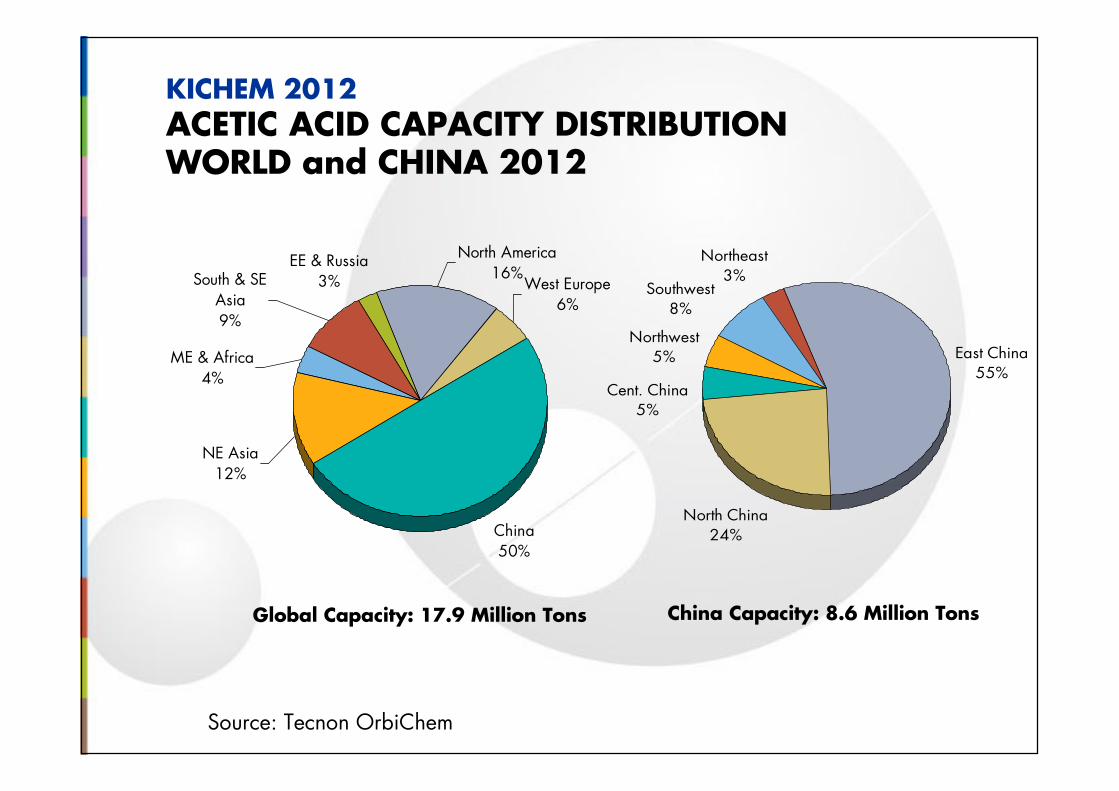

KICHEM 2012

ACETIC ACID CAPACITY DISTRIBUTION WORLD and CHINA 2012

Northeast3%

Southwest8%

Northwest5%

North China24%

Cent. China5%

East China55%

China50%

NE Asia12%

West Europe6%

North America16%

ME & Africa4%

South & SE Asia9%

EE & Russia3%

Global Capacity: 17.9 Million Tons China Capacity: 8.6 Million Tons

1%

19%

19%

23%

28%

10%

14%

3%

38%

12%

9%

16%2012 =12.489 Million Tons

Americas

W/E Europe

NE Asia

SE Asia

ME/Africa

China

Source: Tecnon OrbiChem

KICHEM 2012

WORLD ACETIC ACID CONSUMPTION:2005 vs 2012

2005 = 8.474 Million Tons

Production12.4 Million Tons

NE Asia

N & S America

E & W Europe

S & SE Asia

ME & Africa

China

Source: Tecnon OrbiChem

KICHEM 2012

WORLD ACETIC ACID SUPPLY & DEMAND - 2012

41%

8%5%

15%

10%

21%

37%

3%

15%

15%

20%

10%

Consumption12.4 Million Tons

250

350

450

550

650

750

850

950

1,050

Jan-09Apr-0

9Jul-

09Oct-0

9Jan-1

0Apr-1

0Jul-

10Oct-1

0Jan-1

1Apr-1

1Jul-

11Oct-1

1Jan-1

2Apr-1

2Jul-

12

Dollars per Ton

USGExport

TaiwanImport

ChinaImport

Source: Tecnon OrbiChem

KICHEM 2012

ACETIC ACID PRICES: Q1 2009-2012

EuroContract

ChinaExport

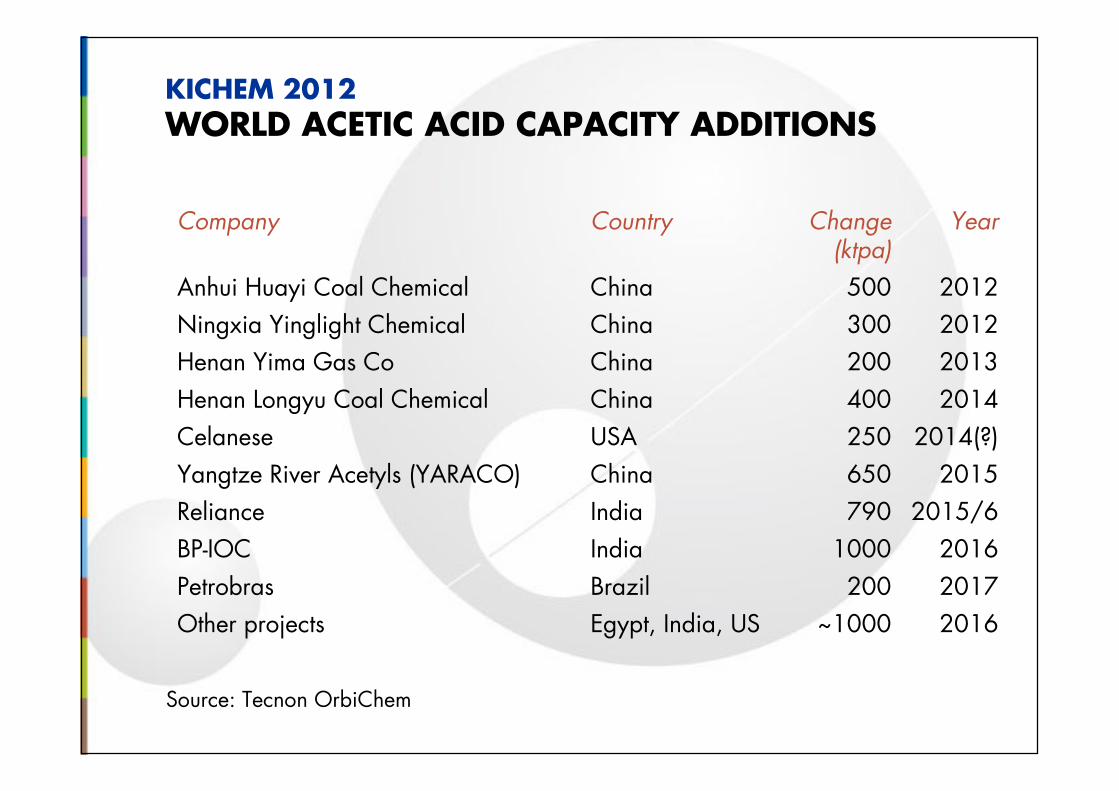

Company Country Change Year(ktpa)

Anhui Huayi Coal Chemical China 500 2012

Ningxia Yinglight Chemical China 300 2012

Henan Yima Gas Co China 200 2013

Henan Longyu Coal Chemical China 400 2014

Celanese USA 250 2014(?)

Yangtze River Acetyls (YARACO) China 650 2015

Reliance India 790 2015/6

BP-IOC India 1000 2016

Petrobras Brazil 200 2017

Other projects Egypt, India, US ~1000 2016

KICHEM 2012

WORLD ACETIC ACID CAPACITY ADDITIONS

Source: Tecnon OrbiChem

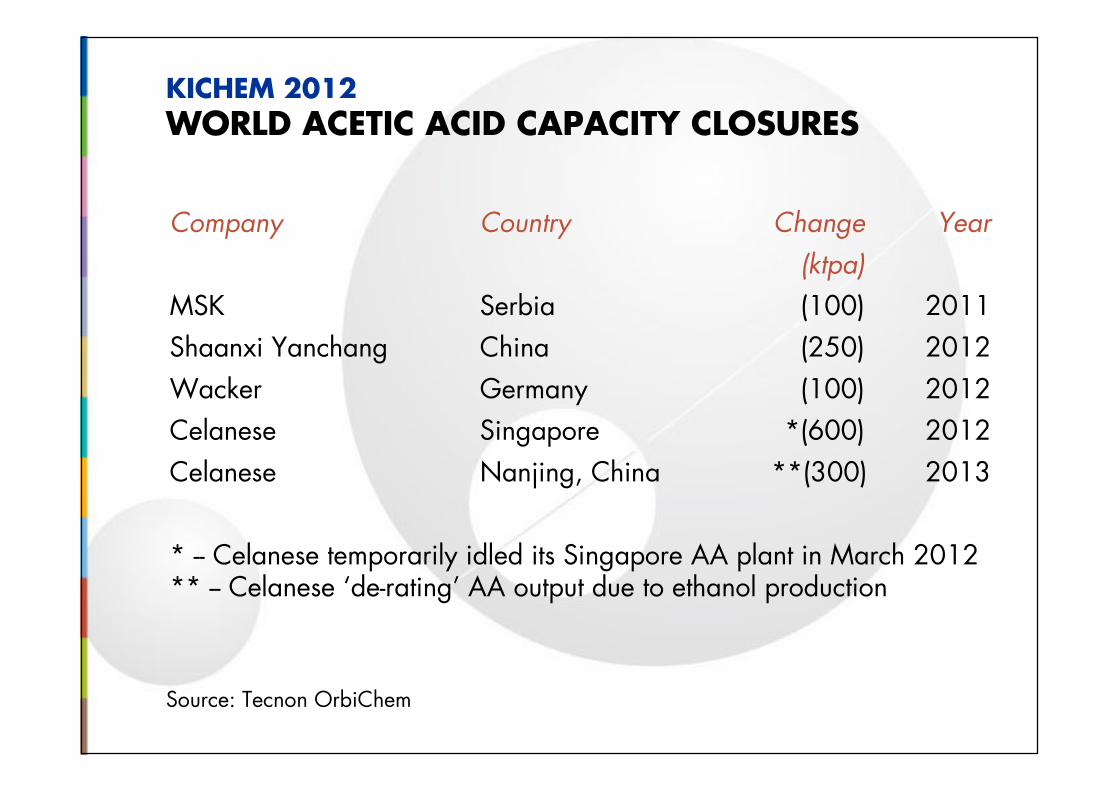

Company Country Change Year

(ktpa)

MSK Serbia (100) 2011

Shaanxi Yanchang China (250) 2012

Wacker Germany (100) 2012

Celanese Singapore *(600) 2012

Celanese Nanjing, China **(300) 2013

* -- Celanese temporarily idled its Singapore AA plant in March 2012** -- Celanese ‘de-rating’ AA output due to ethanol production

KICHEM 2012

WORLD ACETIC ACID CAPACITY CLOSURES

Source: Tecnon OrbiChem

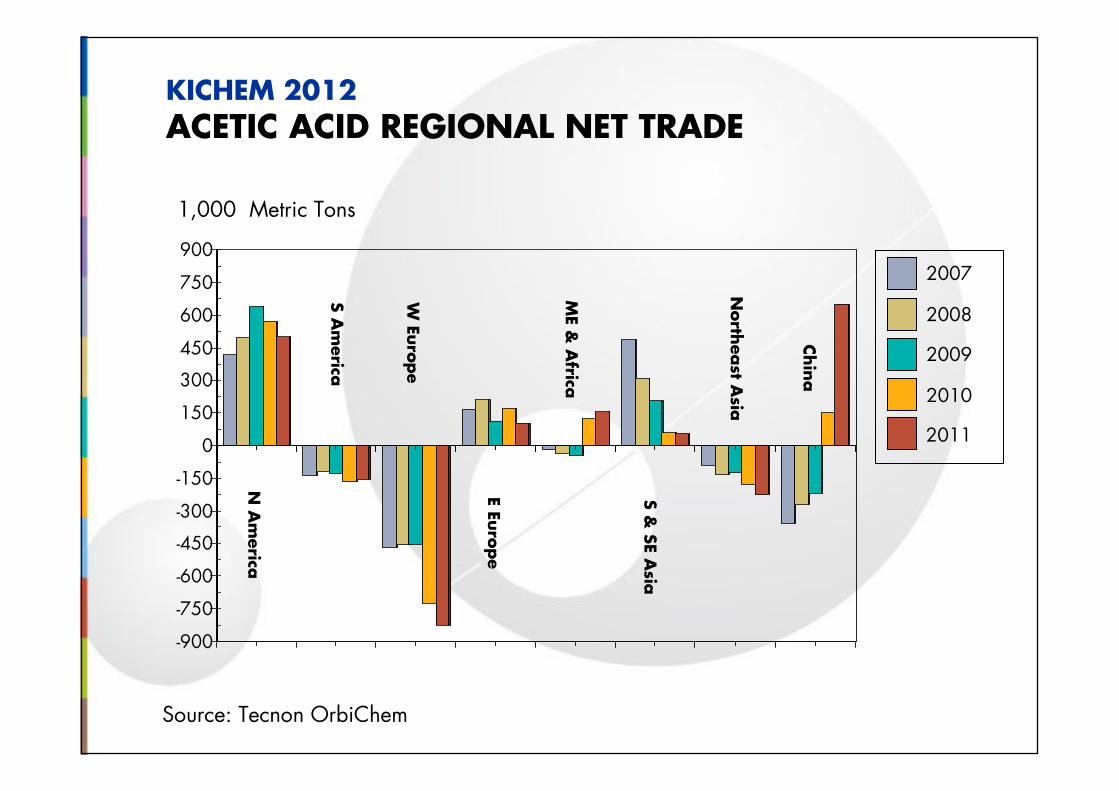

-900

-750

-600

-450

-300

-150

0

150

300

450

600

750

900

1,000 Metric Tons

Source: Tecnon OrbiChem

KICHEM 2012

ACETIC ACID REGIONAL NET TRADE

S &

SE A

sia

E E

uro

pe

W E

uro

pe

N A

merica

S A

merica

ME &

Africa

North

east A

sia

Chin

a2008

2007

2009

2010

2011

0

200

400

600

800

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

e

0

100

200

300

400

500

600

700

800

1,000 Metric Tons

Source: Tecnon OrbiChem

US Dollars

KICHEM 2012

CHINA ACETIC ACID IMPORTS and EXPORTS

Import Volume

Export Volume

Import Price

Export Price

KICHEM 2012PRESENTATION OUTLINE

• Current Acetic Acid Market Conditions

• Major Downstream Markets

• Summary and Conclusions

Source: Tecnon OrbiChem

KICHEM 2012

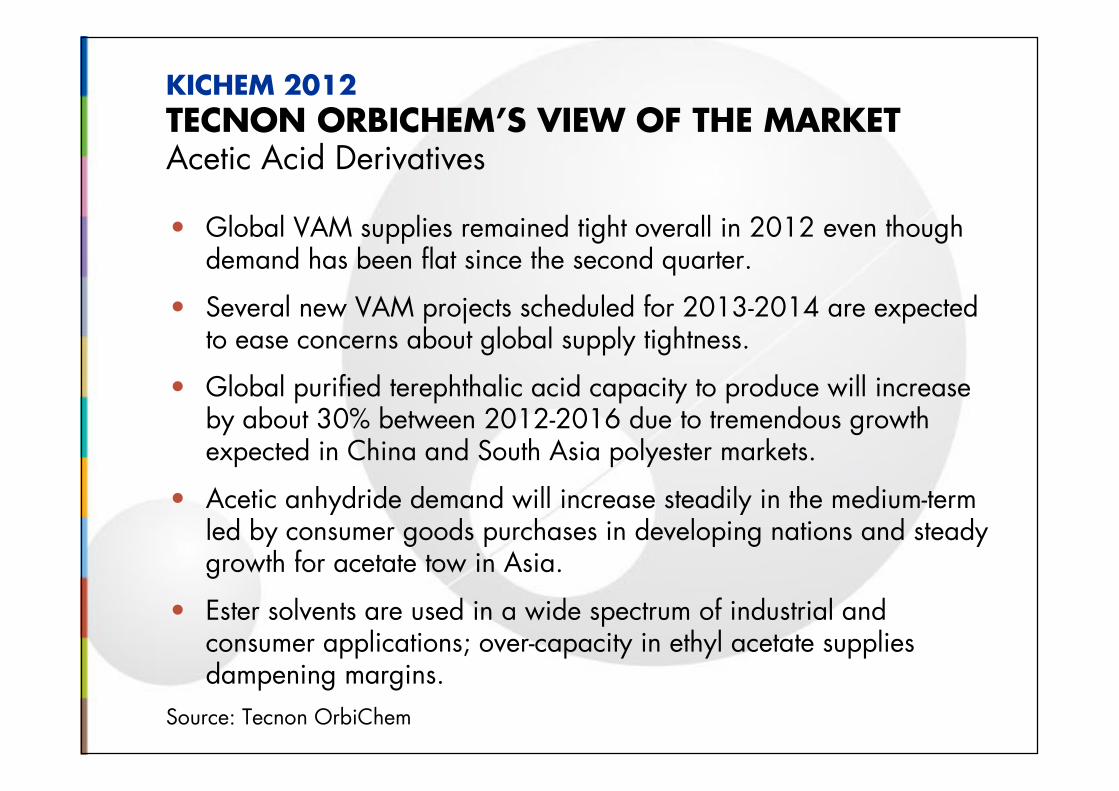

TECNON ORBICHEM’S VIEW OF THE MARKETAcetic Acid Derivatives

• Global VAM supplies remained tight overall in 2012 even though demand has been flat since the second quarter.

• Several new VAM projects scheduled for 2013-2014 are expected to ease concerns about global supply tightness.

• Global purified terephthalic acid capacity to produce will increase by about 30% between 2012-2016 due to tremendous growth expected in China and South Asia polyester markets.

• Acetic anhydride demand will increase steadily in the medium-term led by consumer goods purchases in developing nations and steadygrowth for acetate tow in Asia.

• Ester solvents are used in a wide spectrum of industrial and consumer applications; over-capacity in ethyl acetate supplies dampening margins.

Source: Tecnon OrbiChem

VAM33%

Anhydride14%

Ethyl Acetate12%

Butyl Acetate7%

PTA19%

Others15%

KICHEM 2012

GLOBAL ACETIC ACID CONSUMPTION 2012

Source: Tecnon OrbiChem Total = 12.4 Million Metric Tons

KICHEM 2012ACETIC ACID/ACETYLS CHAIN

Vinyl AcetateMonomer

Vinyl AcetateMonomer

PolyvinylAcetate

PolyvinylAcetate

PolyvinylAlcohol

PolyvinylAlcohol

PolyvinylButyral

PolyvinylButyral

EVA/VAEEVA/VAE

EthyleneEthylene

MethanolMethanol

Acetic AcidAcetic Acid

Natural GasNatural Gas

PTAPTA

Polyester/PET Resin

Polyester/PET Resin

AceticAnhydride

AceticAnhydride Ester SolventsEster Solvents

CoalCoal

MCAAMCAA

Butyl AcetateButyl Acetate

Ethyl AcetateEthyl AcetateAcetate Flake/Acetate Tow

Acetate Flake/Acetate Tow

Construction, Paper,

Packaging

Automotive,Solar

Adhesives, Film, Solar, Coatings

Ag/Pharma,Consumer

Goods

Textiles, Auto,

Packaging

Paints, Coatings, Automotive, Consumer

Goods, Cosmetics

Consumer Goods, Textiles,

Ag/Pharma

Source: Tecnon OrbiChem

Source: Tecnon OrbiChem

KICHEM 2012

ACETIC ACID CONSUMPTION GROWTH

1,000 Metric Tons

0

5,000

10,000

15,000

2009 2010 2011 2012 2013

0

10

20

30

40

50

60

70

80

90

100

VAM

Anhydride

Ethyl Acetate

Butyl/OtherAcetates

PTA

All Others

AA Utilisation

% Utilisation

North America23%

West Europe13%

E Europe2%

NE Asia22%

SE Asia3%

China32%

ME/Africa5%

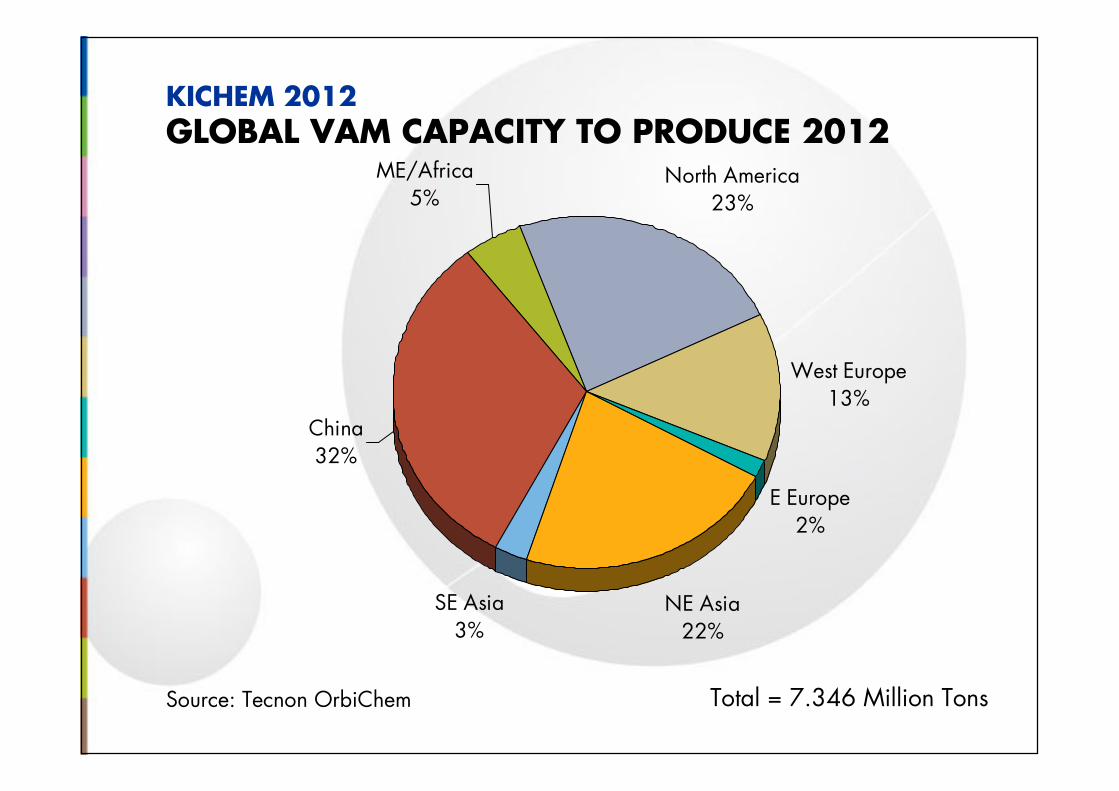

KICHEM 2012

GLOBAL VAM CAPACITY TO PRODUCE 2012

Source: Tecnon OrbiChem Total = 7.346 Million Tons

E Europe~1%

ME/Africa3%

China40%

S America~1%

N America10% W Europe

7%

NE Asia23%

SE Asia16%

Total = 59.6 Million Metric Tons

KICHEM 2012

PTA CAPACITY TO PRODUCE 2012

Source: Tecnon OrbiChem

PTA installed capacity in China to reach 36 million tpaduring 2013/14

E Europe3%

ME/Africa1%

China60%

S America5%

N America4% W Europe

8%NE Asia

6%

SE Asia13%

Total = 4.2 Million Metric Tons

KICHEM 2012

ETHYL ACETATE CAPACITY TO PRODUCE 2012

Source: Tecnon OrbiChem

China Etac plantsoperating close to 50% rates in 2012

South/SE Asia5%

NE Asia9%

China33%

N America37%

W Europe13%

E Europe1%

ME & Africa2%

Total = 3 Million Metric Tons

KICHEM 2012

ACETIC ANHYDRIDE CAPACITY TO PRODUCE 2012

Source: Tecnon OrbiChem

Majority of Acetic Anhydride output used for production of acetate flake/tow

KICHEM 2012PRESENTATION OUTLINE

• Current Acetic Acid Market Conditions

• Major Downstream Markets

• Summary and Conclusions

Source: Tecnon OrbiChem

KICHEM 2012SUMMARY AND CONCLUSIONS

• Growth in downstream derivative capacity has not kept pace with acetic acid capacity growth, but expansion over the next 2-3 years in VAM, PTA and acetate esters markets are expected to make headway into lessening the oversupply of acetic acid.

• Acetic acid utilisation rates globally are forecast to remain between 70%-75% during the period of 2012-2018 based on current capacity figures. Improved business conditions and further rationalisation will impact operating rates moving forward.

• Acetic acid prices remain more sensitive to regional supply/demand problems rather than changes in feedstock prices, but not immune. Feedstock volatility is a constant threat throughout the value chain.

• US acetic acid producers currently enjoy low production costs compared with other regions. Development of shale gas supplies could help US producers maintain cost advantage over many years.

Source: Tecnon OrbiChem

…..your source of expert chemical industry knowledge