afma submission to: productivity commission inquiry · the australian financial markets association...

TRANSCRIPT

AFMA Submission to: Productivity Commission Inquiry

Competition in the Australian Financial System Draft Report Consultation

March 2018

1

Executive Summary The Australian Financial Markets Association (AFMA) welcomes the opportunity to comment on the Productivity Commission Draft Report - Competition in the Australian Financial System. AFMA is a strong proponent of market-based outcomes and competition in the financial system. AFMA is a member-driven and policy-focused industry body that represents participants in Australia’s financial markets and providers of wholesale banking services. AFMA has a broad church membership that reflects the spectrum of industry participants including wholesale banks, traders, brokers, market makers, fund managers, market infrastructure providers and treasury corporations. It is a formal objective of AFMA to promote and facilitate the development and maintenance of efficient and competitive financial markets. AFMA’s operating principles require its policy positions to be competitively neutral. This provides the context for our feedback on the Draft Report. In Section 1 we note that the financial system is a complex and highly integrated organic system, involving financial institutions, markets and related infrastructure, and needs to be assessed accordingly for competition purposes. We believe the Final Report should build on this understanding when setting out the potential for competition and recommend to the Government that it should develop a strategic plan to guide the further development of the financial system. Experience has shown that improving competition and competitiveness in the provision of retail financial services depends on a competitive wholesale banking and financial market sector. We suggest that the Final Report should give more attention to the tax and regulatory factors that weaken the competitiveness and effectiveness of the wholesale financial sector and financial markets. Section 2 notes that the financial system is highly regulated and the financial regulators can have a significant impact on competition in the markets for financial services. Recent announcements by the Government show that it is on the right path to ensure the financial regulators give the right priority to its competition policy objectives. We believe reform of the Council of Financial Regulators (CFR) as proposed in Draft Recommendation 17.1 is unnecessary given the Government’s actions, is not the best option to promote competition policy priorities and would conflict with the findings of the last two major financial system inquires. We note the vital contribution of CFR to well-coordinated and effective financial system regulation and caution against any measures that might adversely affect this. AFMA supports Draft Recommendation 15.1 concerning the priority that should be accorded to Statements of Expectations (SOEs), regulators’ Statements of Intent and associated reporting by regulators. SOEs provide greater clarity about the Government’s policy priorities and objectives that are relevant to financial regulators and are a valuable governance tool for their implementation. Many of the other recommendations of the Commission are not within AFMA’s financial markets focus and as such we generally do not offer comment on them. Section 3 considers an exception

2

to this concerning the recommendation about general advice, which is a relevant matter for many market participants. In relation to Draft Recommendation 12.1 to rename ‘general advice’, we argue that a more comprehensive process to understand and assess operational issues would need to be undertaken before recommending change. While we do not comment on Draft Recommendation 10.5, we do note it is important to maintain a business environment conducive to attracting large scale investment for financial infrastructure. The Draft Report does consider some of the aspects of international competition in the Australian markets but we argue in Section 4 that there is more work to do in properly assessing where improvements can be made in facilitating international competition. The Final Report should give more consideration to the relevant tax and regulatory barriers that currently exist. The Final Report should recommend the following steps to improve competition in the financial system and its international competitiveness:

• Abolition of the ‘LIBOR Cap’ on foreign bank branch parent funding to remove a tax non-neutrality and promote competition;

• Removal of interest withholding tax on offshore funding by financial institutions to remove significant competition distortions and lower costs of finance;

• Reduce the tax burden on corporates to improve international competitiveness; and • Periodic Productivity Commission review of the various financial system regulation cost

recovery programs to ensure they are delivering the intended outcomes. Australia’s financial markets are advanced in global terms and the manner of their operation, including competition between their participants, may provide some insights to assist the Commission conduct its evaluation of competition more broadly in the financial system. Section 5 provides information and comments from this perspective that may assist the Commission in completing its analysis of competition in the financial system.

3

1. Contextual Setting – A Complex, Highly Integrated Financial System

Key points: • The financial system is a complex and highly integrated organic system, involving financial

institutions, markets and related infrastructure, and needs to be assessed accordingly for competition purposes.

• The Final Report should build on this understanding when setting out the potential for competition and recommend to the Government that it should develop a strategic plan to guide the further development of the financial system.

The financial system is comprised of financial institutions (including banks, investment managers, insurance funds and superannuation entities), financial markets and the associated infrastructure required to support their activities. It is a complex and highly integrated organic system and needs to be assessed accordingly. The Draft Report does not capture the full nature of this system and the Final Report should more fully consider the role of competition between sub-sectors and different product types. For example, this understanding is important in a world where market based finance is expected to increase in importance over time, as the cost of banking rises consequent to regulatory reform post the global financial crisis (GFC). There are many aspects of government policy that already have a very material impact competition in the financial system (eg tax as it applies to financial institutions and products) or has the potential to (eg. the application of technology standards). Thus, the task of promotion competition in the Australian financial system embodies a range of public policy actions involving technology and innovation, regulation, taxation and international integration. There is also a positive competition agenda through the promotion of innovation, which will generate new products and services, testing incumbents and unlocking productivity gains in the financial system. In its response to the Murray Financial System Inquiry (FSI), the Government agreed to establish an Innovation Collaboration Committee, linked with ASIC’s Digital Finance Advisory Committee. The task of improving competition can be successfully completed only if it is conducted within a structured framework that incorporates an integrated plan to develop the financial system that addresses all of these public policy issues. Consequently, the Commission’s work should place the specific objective to promote and enable competition within this broader framework. In particular, the Final Report should recommend to the Government that it should work in conjunction with industry participants to develop a strategic plan to develop the financial services sector in Australia in a way that balances competition, innovation, regulation and revenue raising objectives. It is important that the principle of regulatory and policy neutrality between different products and different providers is applied. There is a strong desire for policy that provides the level of stability, consistency and certainty required for market participants to make decisions about the long term commitment of capital and other resources to their business in Australia. The Government’s strategic plan should include long term integrated policy settings that provide business with sufficient certainty for planning and facilitate the further development of the financial system.

4

Key points: • Improving competition and competitiveness in the provision of retail financial services

depends on a competitive wholesale financial sector and financial markets. • The Final Report should give more attention to the tax and regulatory factors that would

materially improve the competitiveness and effectiveness of wholesale financial sector and financial markets.

Recommendation 30 of FSI provides a sound basis for competition by proposing measures to ensure that there is a strong ongoing focus on competition in the financial system. One of the component elements in Recommendation 30 that deserves more attention in the Draft Report is the proposal to identify barriers to the cross-border provision of financial services. The Australian financial system, as well as the broader economy, has benefited enormously from increased international competition. Reforms since the early 1980s, most notably foreign bank entry and the deregulation of domestic interest rates, have improved the efficiency of the Australian financial system and directly benefited consumers. This has occurred through more competitive pricing and innovation that delivered a broadening range of financial products that can better meet the particular needs of retail clients. Moreover, policy settings that promote Australia as a financial centre are those that support the international competitiveness of the Australian economy more generally and can be expected to have direct benefits for domestic and retail competition in financial services. Improving competitiveness in relation to the provision of retail financial services depends on a competitive wholesale financial sector and financial markets. Regulatory, tax and other burdens imposed on the wholesale financial sector are necessarily passed on to consumers and end-users of financial services. While consumer benefit is the appropriate benchmark for reform, the best competitive outcomes for consumers are unlikely to be achieved in the absence of an improvement in policy settings for wholesale financial services. Competitive innovations in wholesale financial intermediation and markets have direct implications for consumers as the end-users of financial services. The residential mortgage market is a significant focus of the Draft Report and the history of home loan securitisation in Australia that it draws attention to provides a striking example of this. As the Draft Report notes, the cost at which banks and non-bank financial institution source their funds has a substantial influence on their competitive position. 1 The Keating government announced in December 1995 that it would amend section 128F of the Income Tax Assessment Act with the intention of enabling home loan securitisation vehicles to access offshore funding free of interest withholding tax. The Howard government subsequently enacted the necessary legislation in 1996. Although this particular tax reform impacted the wholesale funding market and improved access to international markets, the extent to which this helped competition through securitisation provided a significant benefit to households with home loans through downward pressure on related interest rates.

1 Draft Report, p. 105.

5

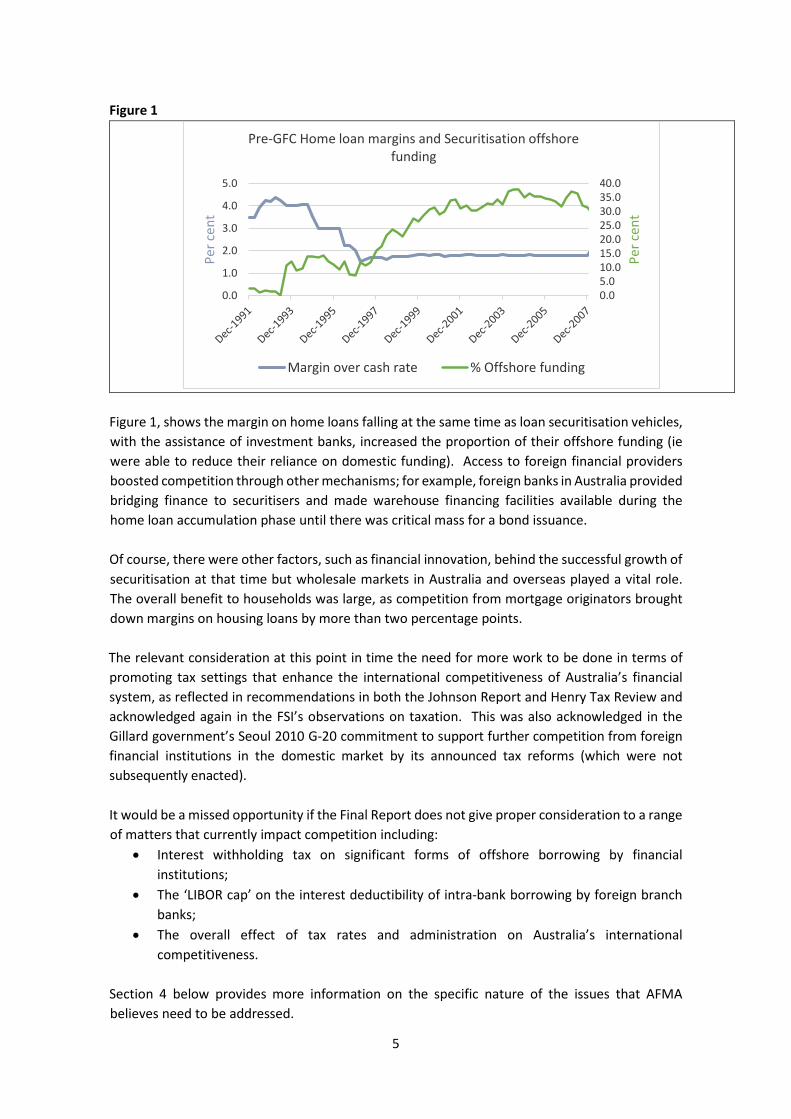

Figure 1

Figure 1, shows the margin on home loans falling at the same time as loan securitisation vehicles, with the assistance of investment banks, increased the proportion of their offshore funding (ie were able to reduce their reliance on domestic funding). Access to foreign financial providers boosted competition through other mechanisms; for example, foreign banks in Australia provided bridging finance to securitisers and made warehouse financing facilities available during the home loan accumulation phase until there was critical mass for a bond issuance. Of course, there were other factors, such as financial innovation, behind the successful growth of securitisation at that time but wholesale markets in Australia and overseas played a vital role. The overall benefit to households was large, as competition from mortgage originators brought down margins on housing loans by more than two percentage points. The relevant consideration at this point in time the need for more work to be done in terms of promoting tax settings that enhance the international competitiveness of Australia’s financial system, as reflected in recommendations in both the Johnson Report and Henry Tax Review and acknowledged again in the FSI’s observations on taxation. This was also acknowledged in the Gillard government’s Seoul 2010 G-20 commitment to support further competition from foreign financial institutions in the domestic market by its announced tax reforms (which were not subsequently enacted). It would be a missed opportunity if the Final Report does not give proper consideration to a range of matters that currently impact competition including:

• Interest withholding tax on significant forms of offshore borrowing by financial institutions;

• The ‘LIBOR cap’ on the interest deductibility of intra-bank borrowing by foreign branch banks;

• The overall effect of tax rates and administration on Australia’s international competitiveness.

Section 4 below provides more information on the specific nature of the issues that AFMA believes need to be addressed.

0.05.010.015.020.025.030.035.040.0

0.0

1.0

2.0

3.0

4.0

5.0

Per c

ent

Per c

ent

Pre-GFC Home loan margins and Securitisation offshore funding

Margin over cash rate % Offshore funding

6

2. Financial Regulators and Competition - Recommendation 17.1, 17.2, 15.1

Key points: • The vital contribution of the Council of Financial Regulators (CFR) to well-coordinated and

effective financial system regulation was evident in the period during and after the GFC. • There is no room for complacency about the preservation of financial stability, so CFR’s

process should not be materially changed without good reason. • Recent announcements by the Government show that it is on the right path to ensure the

financial regulators give the right priority to its competition policy objectives. • The proposed reform to CFR is unnecessary given the Government’s actions, is not the best

option to promote competition policy priorities and would conflict with the findings of the last two major financial system inquires.

Draft Report Recommendation 17.1 proposes reform of the Council of Financial Regulators (CFR) to enable an existing regulator to take the lead on matters related to competition in the financial system. The CFR is the coordinating body for Australia's specialist financial regulatory agencies. CFR aims to facilitate cooperation and collaboration between its member bodies; the Reserve Bank of Australia, APRA, ASIC and Treasury and helps to resolve any issues where members' responsibilities overlap. Its ultimate objective is to contribute to the efficiency and effectiveness of regulation and to promote stability of the Australian financial system.2 CFR members share information, discuss regulatory issues and, if the need arises, coordinate responses to potential threats to financial stability. CFR also advises the Government on the adequacy of Australia's financial regulatory arrangements. As necessary, CFR members invite other government agencies to participate in Council meetings. For example, the ACCC has been invited to participate on issues relating to contestability and competitiveness. CFR has proven itself to be a vital component of our regulatory framework and has a high level of standing and trust within the financial markets community. 3 CFR has the capability to act expeditiously and it coordinated the regulatory response to the global financial crisis to the great benefit of all Australians. From AFMA’s perspective, CFR has exhibited a balanced level of openness with financial market participants. In this context, we note that AFMA had many dealing with CFR officials in connection with implementation of G20 reforms concerning OTC derivatives. In addition, AFMA has had a long standing dialogue with CFR on issues concerning financial market infrastructure, financial benchmarks and competition among clearing and settlement service providers, amongst other things. While CFR determines its own view on relevant regulatory matters, AFMA has had the opportunity to have its concerns considered by CFR, if not always accepted. In framing the case for establishing CFR in its current form, the Wallis Financial System Inquiry stated that CFR’s effectiveness is reliant on maintaining clarity of its scope and frankness in discussions and, for this purpose, recommended that its membership should not be extended to other agencies or representatives. The Murray Financial System Inquiry (FSI) consulted on an

2 Information on the Council is available at https://www.cfr.gov.au/ 3 This addresses the need for trust in regulators cited by the Draft Report on p. 415.

7

expansion of the CFR to include ACCC, ATO and AUSTRAC but having reflected on the issues decided that there is no basis for change, especially as these agencies can already attend CFR meetings as necessary. Having regard the above, it seems reasonable to assert that both Inquiries would have been concerned about making a critical change to the collaborative dynamic of CFR by giving one of its members explicit authority to hold the others ‘to account’ for competition. As noted, effective financial system regulation is dependent on CFR working cohesively, so there would have to be compelling reasons to set aside the considered views of the last two major inquiries into the financial system. In AFMA’s view, this case has not been made. We agree with the Government’s comment in its response to the FSI that we cannot afford to be complacent about resilience and, in this regard, would urge caution about adopting measures that might impact the effectiveness of the CFR. Good Governance The order of governance for financial system regulation can be summarised as follow:

i. The Government determines financial system policies in accordance with the needs of the community and this may be adjusted over time;

ii. Treasury provides analysis and advice to assist the Government in forming and assessing its policy;

iii. The Government gives financial regulators a mandate and sets out their responsibilities in legislation and the regulators are accountable to it for their exercise of the associated powers;

iv. The Government issues Statements of Expectations (SOE) to statutory agencies, including ASIC and APRA, to provide greater clarity about government policies and objectives relevant to them, including the priorities they are expected to observe in conducting their operations;

v. CFR is the forum to facilitate coordination and cooperation by the financial regulators and Treasury within the boundaries of the Government’s policy settings.

SOEs are a particularly important tool in the context of the issues about regulator governance raised in the Draft Report, as they serve the specific purpose of providing greater clarity about government policies and objectives relevant to ASIC, APRA and the Payments System Board (PSB). AFMA supports Draft Report Recommendation 15.1 concerning the priority that should be accorded to SOEs, regulators’ Statements of Intent and associated reporting by regulators. In AFMA’s view, this approach provides the optimal basis to ensure that the financial regulators meet their mandate in relation to competition, as their mandate derives directly from the authority of the Government. If there is a trade-off between the regulatory objectives like financial stability and market integrity on the one hand and competition on the other, then it is entirely appropriate for the Government to determine how that balance should ultimately be struck. An elected government is given the political authority to set and manage its policy priorities. Moreover, the Government would have to bear part of the cost of any financial instability.

8

Government oversight of financial regulators is being strengthened Significant steps are currently being taken to ensure that the right priority is given to competition issues throughout the financial regulation process and that competition matters are given full consideration by the financial regulators. In particular, the Government in its response to the FSI stated that it will strengthen the accountability of the financial regulators, review the SOEs for APRA, ASIC and the Payments System Board (PSB) and increase requirements for the regulators’ annual reports. Thus, the Government has already committed to action to strengthen performance assessment in the SOEs in order to ensure regulators are focusing on their capabilities and performance against their mandate, including competition. On 19 March 2018, the Minister for Revenue and Financial Services confirmed the Government has settled on the new SOE for ASIC, which will reflect a new competition mandate for ASIC. In addition, on 28 March 2018, the Government introduced Treasury Laws Amendment (Enhancing ASIC's Capabilities) Bill 2018 that will require ASIC to consider the effect that the performance of its functions and the exercise of its powers will have on competition in the financial system. This governance process provides the only effective framework within which assurance checks can be made that the Government’s policy to engender competition in the financial system is being fulfilled. Government is the supreme policy authority and must ultimately be the adjudicator of choices to be made in the administration of its policy. Government decisions draw principally on advice from Treasury as its own adviser, which is best placed to provide objective and balanced views on other sources of advice, particularly from the independent financial regulators who may separately provide their own views. The Final Report recommendations should fully factor in the Government’s commitments and the steps it is now taking to ensure that the financial regulators properly reflects its policy priorities, including that concerning competition. The proposed reform to CFR is unnecessary in light of the Government’s plans. The Government has also committed to conduct subsequent periodic reviews of competition in the financial system as appropriate, which provides a framework within which competition can be comprehensively assessed on an ongoing basis. Thus, the Productivity Commission can avoid the need to pre-judge the effectiveness of the Government’s measures underway, including implementation of other relevant policies such as those arising from the Review into Open Banking. Moreover, given the balance of risks in relation to regulator governance, it would be sensible for the Final Report to adopt a graduated approach to the testing of competition actions by the financial regulators. An effective, low risk enhancement Treasury is a policy body with comprehensive coverage of national financial priorities. It is in the unique position of being a government agency that is required to take a whole of financial system policy perspective on regulatory matters. It can internally balance these competing priorities with a full understanding of the Government’s views on the appropriate balance both within each area and across areas. As such it uniquely placed to promote the coordination of the regulators and

9

their activities in a manner that would ensure a whole-of-government perspective is brought to their work. Moreover, Treasury is best placed within the CFR to report to the Government on any issues that arise in balancing priorities, including those that may need to be addressed through revised a SOE. The Government can use Treasury’s participation in CFR as a vital means to get additional assurance that the financial regulators are giving the intended priority to competition matters. The intended clarity of CFR’s scope and frankness in discussions would be protected in this environment. AFMA would support the provision of additional resources to Treasury, if it is necessary to enable it to fulfil this role. CFR public transparency – Recommendation 17.2 In terms of the transparency of the CFR, Treasury’s participation in CFR should ensure well-informed government decision making. While CFR is not itself a regulator, there is also a benefit to information on its activities being made available to the public. AFMA uses information about CFR that is published in Financial Stability Reviews and the various reports of its members and we would welcome additional insights. We acknowledge that CFR must continue to provide a venue for candid discussion between regulators and appreciate that the provision of more information needs to be consistent with this objective. A recommendation by the Commission for greater transparency of CFR discussions should be formulated in a manner that would, if implemented, preserve the effectiveness of the Council. Practical challenges to proposed CFR reform The Draft Report proposes that a designated entity (either ASIC or ACCC) would be a ‘competition champion’ whose purpose would be to “hold(s) all parties in the financial system to account for competition.”4 Notwithstanding the Draft Report’s stated desire to not create a ‘regulator of regulators’, the de facto effect of the proposal would have elements of this in respect of competition, given the intention for one CFR member to hold the others to account in respect of their actions in this area. The more pressing problem with this approach is that it would infringe upon the collaborative way in which CFR operates. The proposal also warrants caution because of the intertwined nature of the objectives that financial regulators are tasked to achieve. Matters like fairness, market integrity, efficiency, competition and financial stability must be jointly determined. Thus, if the ‘competition champion’ were to conclude, for example, that APRA had misjudged a regulatory decision concerning competition for banks, it necessarily implies it must have also misjudged the application of its associated prudential responsibilities. 5 This would place a weight of responsibility on the ‘competition champion’ that ultimately could not be properly serviced by its technical expertise and experience. A better option would be for a CFR member to outline to the other members how it considered competition as a factor in making a decision that is of material significance and receive feedback on this from other members based on their own regulatory experience, including in making decisions that required similar judgements to be made. 4 Draft Report, p. 22. 5 Hence, for example, the Draft Report states that the ACCC (were it to be the ‘competition champion’) would have to expand its knowledge in relation to prudential compliance.

10

The Draft Report’s proposal is also problematical at a functional level because, were ASIC to be the competition champion, it cannot be expected to hold itself to account in the manner envisaged for how it implements its (upcoming) competition mandate. Nor could the ACCC be expected to hold itself to account for how it might determine industry standards should the recommendations in the Open Banking Final Report be adopted by the Government, were it to be the competition champion. Many ‘competition champions’ More generally, an assessment of the need for a ‘competition champion’ of this type should take account the governance process outlined above and of the regular engagement of financial regulators with industry bodies, consumer groups and other stakeholders in relation to proposed regulatory changes. In AFMA’s experience, competition and competitive neutrality of regulation is a constant theme in this dialogue, as industry participants (users and providers) seek to hold regulators to account to these principles. Indeed, the range of submissions to the Commission’s ongoing inquiry is evidence of the vibrancy of community representations. In instances where a financial regulator cannot or does not wish to implement a suggestion concerning a significant matter, it is common for the interested group to seek a policy response by the Government. This process both informs the Government of prevalent concerns about competition and other matters and it leaves the decision with the Government, which is best placed to make a holistic policy assessment and then has the authority to act on it. The strengthening of the government review process described above is relevant in this context and is viewed as a positive development by AFMA. Financial regulator oversight The FSI acknowledged the need for a better mechanism to allow Government to assess the performance of financial regulators and specifically recommended that reporting of how they balance competition against their core objectives should be improved.6 AFMA sees merit in having greater external oversight of regulatory bodies and in undertaking annual ex post reviews of overall regulator performance against their mandates.7 While the scope of external oversight would cover all of a regulator’s responsibilities, it would be an obvious mechanism to get the desired re-assurance that the financial regulators are giving competition issues the right priority. It is surprising that the Draft Report gives only cursory consideration to this FSI recommendation. If the Productivity Commission has significant residual concerns about financial regulators implementing the Government’s competition policy, notwithstanding the above analysis, then it could take on board the FSI recommendation and recommend the appropriate structure for such external oversight.

6 Recommendation 30. 7 AFMA argued for a strong external oversight mechanism in its FSI submission.

11

3. Other Draft Report Recommendations (12.1 and 10.5)

Key points: • In relation to general advice, a more comprehensive process to understand and assess

operational issues would need to be undertaken before recommending change; • It is important to maintain a business environment conducive to attracting large scale

investment for financial infrastructure. Many of the other recommendations of the Commission are not within AFMA’s financial markets focus and as such we do not offer comment on them. The exceptions to this are the recommendation and questions around general advice and the proposed changes to regulatory structures which will directly affect all areas of financial services including financial markets. General Advice Recommendation and Questions AFMA has considered the Commission’s recommendations in relation to general advice and our comments are set out below.

DRAFT RECOMMENDATION 12.1 RENAME GENERAL ADVICE TO IMPROVE CONSUMER UNDERSTANDING General advice, as defined in the Corporations Act 2001 (Cth), is misleading and should be renamed. The Commission supports consumer testing of alternative terminology to ensure that misinterpretation and excessive reliance on this type of promotional information is minimised. The term ‘advice’ should only be used in association with ‘personal advice’ that takes into consideration personal circumstances.

As per section 766B(4) of the Corporations Act 2001 general advice is defined as “financial product advice that is not personal advice”. We note that ASIC also uses this definition in Regulatory Guide 244 (see RG244.43). The experience of firms with the current statutory arrangements can vary across the different strata of customers. For more sophisticated investors, the current arrangements have caused fewer issues and may not warrant change. For more general retail customers, there are some Court rulings expected that will likely consider the current definitions and interpretations as to where the appropriate boundaries might rest. As such, there may be benefit in considering enhancing rather than simply renaming general advice. It may be appropriate to approach such a task with the benefit of the Court rulings and a more broad-based approach beyond consumer testing that takes into accounts the challenges that have been faced with existing arrangements but also where they are working well. We do not agree the term ‘advice’ should necessarily only be used in association with ‘personal advice’. Often, general advice is critical in enabling consumers to make a timely decision about the appropriateness of a particular investment without having to pay for personal advice. For example, financial product research can help reduce the amount of time consumers need to spend on investigating investment options.

12

It may be that there should be a space for the presentation of sales materials and information that takes into account some basic information but not all of an individual’s situation and circumstances. We note that the definition of advice in ASIC Regulatory Guide 36 is “any recommendation or statement of opinion ….that is intended to influence a person in making a decision about a particular financial product”. If the word ‘advice’ could only be used in association with ‘personal advice’ the definition of advice would also need to be amended.

INFORMATION REQUEST 12.2 RENAMING GENERAL ADVICE AND MERITS OF FURTHER CHANGES In implementing draft recommendation 12.1, we request feedback on: · how the scale of transition costs associated with renaming general advice could be minimised, including the effect of varying the transition timeframe · barriers or unintended consequences of such a change, including licensing implications.

The costs of implementing draft recommendation 12.1 for participants in the financial services industry would be significant. For example Australian Financial Services Licence holders would be required to provide extensive training to all client facing employees, update client documentation, their websites and the systems they use to document Statements of Advice and Records of Advice. As an indicative guide to the time costs of the proposed change a minimum 24 month transition period would likely be required if the proposal were to proceed. At a broader level, a comprehensive investor education and financial literacy program would be required to ensure that consumers of financial services are better equipped to understand the difference between personal and other advice, or personal advice and other services as the case may be (depending on any legislative change that is made). The current regime of personal advice and general advice has been in place since 2002, and regardless of whether one agrees that the current regime is flawed or not, a substantive change such as the one suggested will only achieve the desired outcome if consumers more fully understand the nature of the services they receive. Based on the experience of implementing the Financial Services Reform Act reforms (which introduced the concepts of personal and general advice), the effort involved in implementation of a change of this scale should not be underestimated.

We also seek information on the merits of: · redefining the activities that are currently regulated under general advice and providing a more customised regime for some activities · removing licensing and regulatory obligations currently associated with some or all forms of general advice.

Any regulatory change in relation to these activities should be subject to a proper assessment and process, and would have to satisfy a full cost benefit analysis, given the currently sound consumer protections that are in place, to ensure these are not compromised. We would caution against a recommendation on the basis of the work done by the Commission so far, given the need for a more comprehensive process to understand and assess operational issues.

13

New Payments Platform We note Draft Report Recommendation 10.5 in relation to the Government mandating an access regime to the New Payments Platform (NPP), with PSB review of the fees set by New Payments Platform Australia, and a requirement to share de-identified transaction level data. The NPP has only recently commenced operation and is, as the Draft Report notes, a significant piece of national infrastructure. However, it is important to note that it has been built with large investments by participating institutions including the RBA. Mutuals have a long history of constructive contribution to financial infrastructure including stock exchanges, investment and insurance firms. While we do not comment on the specifics of the Recommendation 10.5 for government intervention in relation to the NPP, we do note more generally that it is important to maintain a business environment conducive to attracting large scale investment for financial infrastructure. Project developers should have confidence that they will not be subject to unnecessary government intervention on completion of their project. Investors should be confident their investments in financial infrastructure should be entitled to earn a commercial return and not a regulated return unless this is clearly indicated at the beginning of the project. We also note that the question of whether the security and stability of the system will be best addressed by allowing non-ADI “new entrants” direct access to the NPP or whether intermediated access gives the best balance in regard to these outcomes is a complex systemic question that has not been yet considered by the Commission. Intermediated arrangements have worked well for many years in markets with brokers assessing and taking responsibility for the access of many smaller firms.

14

4. AFMA Proposals to Enhance the Wholesale Markets Uplift to Competition

Key points: The Final Report should recommend the following steps to improve competition in the financial system and its international competitiveness: i. Abolition of the ‘LIBOR Cap’ on foreign bank branch parent funding to remove a tax

non-neutrality and promote competition. ii. Removal of interest withholding tax on offshore funding by financial institutions to

remove significant competition distortions and lower costs of finance; iii. Reduce the tax burden on corporates to improve international competitiveness; iv. Periodic Productivity Commission review of the various financial system regulation cost

recovery programs to ensure they are delivering the intended outcomes. Section 1 above illustrates the importance of having competitive wholesale financial markets to improving the competitiveness in the provision of retail financial services and the important influence of tax and regulation to this outcome. While the Draft Report does consider some of the aspects of international competition in the Australian markets, there is more work to do in properly assessing where improvements can be made in facilitating international competition. The Final Report should give more consideration to the relevant tax and regulatory barriers that currently exist. LIBOR Cap for Foreign Bank Branches A significant competitive friction between participants in Australia’s financial system arises in a taxation context by virtue of the LIBOR8 Cap. The LIBOR Cap, which applies only to foreign bank branches, caps deductibility of interest on internal funding to the applicable LIBOR, thereby exposing foreign banks that operate in Australia via a branch to significant non-deductible interest. AFMA has long maintained that the LIBOR Cap is inconsistent with appropriate competition, regulatory or tax policy and continues to strongly recommend the removal of the LIBOR Cap. In our view, the taxation inequity imposed by the LIBOR Cap was one of a number of factors that contributed to a sharp decline in market share held by foreign banks when compared to the levels exhibited prior to the GFC. Foreign bank branches provide competition in the wholesale banking and financial markets, which benefits Australian business and the broader community. Thus, the LIBOR Cap has the effect of reducing bank competition by increasing the funding costs for foreign banks and thereby hinders the ability of foreign banks to compete in the business loan market. It can be especially penal for new market entrants who may have greater reliance on parent funding as they establish their business and funding capacity in Australia. Further, to the extent that the LIBOR Cap unnecessarily inhibits the flow of capital into Australia, it increases the availability and cost of credit to Australian business. Abolition of the LIBOR Cap would be viewed as a welcome step towards allowing Australia to compete with regimes such as Singapore and Hong Kong. The abolition would encourage foreign banks to conduct more

8 LIBOR is the London interbank offered rate.

15

business in Australia and help provide the critical mass and diversity of business required to sustain financial services exports at the desired level. The continued existence of the LIBOR Cap is particularly perplexing given the number of reviews that have called for its abolition. The 2010 report conducted by the Australian Financial Centre Forum into Australia as a financial centre (the Johnson Report), in recommending the abolition of the LIBOR Cap, stated:

“in periods of stress in credit markets there can be appreciable differences between the LIBOR rate and the rates at which parent banks are able to offer their Australian branches on a commercial basis…any tax avoidance concerns resulting from removing the LIBOR cap could be adequately dealt with by applying the usual transfer pricing guidelines.”

This was a theme picked up by the Final Report of the Financial System Inquiry, which observed:

“(f)or foreign bank branches in Australia, interest paid on funds borrowed from the offshore parent is deductible, limited to the London Interbank Offered Rate (LIBOR) cap. This can prevent the branch from claiming the full interest cost of borrowing.”

The cessation of AUD LIBOR in 2013 and the likely cessation of LIBOR in its entirety in 2021, once the Financial Conduct Authority in the United Kingdom will not use its influence or legal powers to persuade or compel panel banks to make LIBOR submissions, provide tangible examples of the anachronistic nature of the LIBOR Cap. Abolition of the LIBOR Cap would remove a significant distortion in the application of taxation measures to participants in the Australian financial system and promote a tax-neutral environment. Phase-Down of Interest Withholding Tax for Financial Institutions As noted above, Australia is a net importer of capital and, therefore, has an imperative to prioritise settings that enhance access to offshore capital. Presently, and absent an exemption either in the domestic taxation legislation or in a Double Taxation Agreement, a payer of interest by an Australian borrower to an overseas lender will attract Interest Withholding Tax (IWT) at a rate of 10%. Various reviews, such as the Johnson Report, the Henry Tax Review and the Financial System Inquiry, have highlighted that the imposition of such IWT as a key policy setting that is stymying access by Australian borrowers to offshore debt markets. Further, it has been noted that the IWT burden has two principal effects:

• To raise the cost of capital for Australian banks borrowing from offshore, and hence for Australian businesses and households that borrow from banks, particularly given the market practice to require the borrower to “gross-up” for the amount of any IWT; and

• To introduce significant competitive distortions and inconsistencies by virtue of the application of IWT to some, but not all, offshore borrowings, given the existence of the domestic and treaty exemptions.

16

Successive Governments have acknowledged the incongruity of a net importer of capital imposing IWT on payments of interest offshore and have committed, in principle, to phasing down such IWT. However, implementation of this commitment has not occurred. Implementation of the phase-down of IWT for financial institutions would significantly enhance the international competitiveness of the Australian financial sector. Corporate Tax Rate and Administration A further drag on the competitiveness of the sector, particularly from an international perspective, is Australia’s high corporate tax rate of 30%. This issue has become even more significant since the US has moved to a federal corporate headline rate of 21% (the headline rate excludes relevant state and local corporate taxes). As observed by the Government’s Re:Think Tax Discussion Paper in 2015, “Australia’s corporate tax rate is higher than many countries we compete with for investment.9” As at March 2018, Australia had the third highest headline corporate tax rate in the OECD10. While the Government has committed to its Enterprise Tax Plan, which seeks to lower the corporate tax rate to 25%, at this stage agreement from Parliament has been to lower the corporate tax rates only for those companies with turnover of less than $50 million per annum. Australia is heavily reliant on corporate income tax, which in 2016 represented 4.0% of GDP as against an OECD average of 2.9%.11 While it may be that the burden of company tax is relieved through the dividend imputation system, which allows investors to claim a credit for underlying company tax paid in respect of dividend income, the imputation system does not provide any benefits for foreign investors. As such, the burden of Australia’s company tax rate falls squarely, and in full, on international investors into Australian companies Cost Recovery and ‘Industry Contribution’ Levies The Government has sought to cost recover much of the cost of regulation from the financial services industry via cost recovery and other levies. This includes levies for ASIC from 1 July 2017, the APRA levy (that also recovers certain costs for ASIC until 2020, the ACCC and ATO) and the AUSTRAC ‘industry contribution’ levy that is outside the Government’s Cost Recovery Guidelines but is clearly cost recovery. These levies can be particularly burdensome on new entrants and marginally profitable firms, leading to exit from the industry. Where offshore businesses have discretion over the jurisdiction from which financial services are provided, such cost burdens may lead to a loss of activity in Australia, reducing local competition. Governments have paid little attention to the cumulative burden of ad hoc increases in cost recovery levies and have persisted in failing to recognise that the primary beneficiaries of regulation are consumer and end-users of financial services, who are not directly levied, although may ultimately be subject to the pass through of levies by financial intermediaries. In 2016, Australian banks paid $510 million in APRA, AUSTRAC and RBA Committed Liquidity Facility

9 “Re Think Tax Discussion Paper,” Australian Government, March 2015, p. 74. 10 http://taxexecutive.org/oecd-corporate-tax-rates/ tied for third with Mexico. 11 Ibid, p. 75.

17

levies.12 The ASIC industry funding model which commenced on 1 July 2017 will add to this burden by in net terms by $246 million 13 , charged across both financial and non-financial businesses. This represents a total of over $750 million per year of direct cost burden on Australian businesses from the regulators. The structures around these recoveries present little incentive to keep costs low or even efficient, as costs are not a burden to the regulator or to government but only to the invoiced entities. The mapping of regulator costs on to the regulated community is necessarily imperfect and creates distortions, particularly where the cost burden is poorly calibrated to regulatory risk. AFMA has previously recommended that financial system regulatory cost recovery methodologies should be the subject of periodic Productivity Commission review to ensure they are delivering the intended efficiencies. The current inquiry could usefully address this issue. Other Areas There are many other areas where changes in regulation could increase the scope of the system to produce competitive outcomes. We note in this regard the opportunities to review the large increases in regulatory burden faced by businesses in the financial sector over recent years, which are expected to grow further. The Commission has a valuable role to play in assisting Government to understand the undesirability of continuing to increase the regulatory and cost burden on business given its impact on competition, amongst other things.

12 Australian Bankers’ Association, “Taxes and Other Levies Paid to Governments in Australia by the Banking Industry,” Economic Report, June 2017. 13 ASIC Cost Recovery Implementation Statement, October 2017.

18

5. Financial Market Insights into Competition in the Financial System Australia’s financial markets are advanced in global terms and the manner of their operation, including competition between their participants, may provide some insights to assist the Commission conduct its evaluation of competition more broadly in the financial system. Appropriate Weighting of Evidence In financial markets the factors that drive market efficiency are many and varied such as the number of brokers, their technological sophistication and the amount of capital deployed in the service of market making. These and many other factors are often difficult to quantify, and whether a particular factor is material to competitive outcomes can be hard to determine. In contrast, the outputs of the system present themselves as spreads, market depth and transaction costs. These are a much better guide to the level of competition in the system, they are empirical and more often readily comparable. Further, they reflect the consumers’ experience of the system, which is the important assessment benchmark. On this basis we believe the macro output measures on the state of inter-firm competition such as net interest margin, variance in market share over time, cost to income ratios, measures of banks’ return on equity, a wide range of products, product providers and innovation, should accepted as the most relevant evidence of the actual state of competition on a systemic basis. Similar conclusions were reached by the FSI (which, as the Commission notes, found competition to be “generally adequate”14, noting only potential future limits to the benefits of competition. A multiple of factors affect observed outcomes in the financial sector including the evolving mix of institutions’ funding sources, the stage of the economic cycle, structural changes in the financial system and developments in overseas markets, amongst other things. The RBA and APRA draw on the significant breadth of knowledge and skills necessary to make an informed judgement in what is, given the interconnections and moving parts, a complex area, so it makes sense for the Final Report to attach a significant weight to their insights and conclusions. Price Convergence We note the Commission’s concerns about price convergence:

“Prices of many comparable banking products tend to converge (but not necessarily to the marginal cost of provision) between the different providers — with a congruence in underlying influences on bank pricing and with smaller players (including the so-called challenger banks) following the pricing decisions of the major providers. For competition analysis it is significant that the state of the market persistently allows this.”15

14 http://fsi.gov.au/publications/final-report/, pp. 18, 255. 15 Draft Report, p. 8.

19

Financial markets allow greater visibility of the dynamics of price competition than perhaps most product markets. In financial markets the products within a particular market are often identical16 and there is often high transparency of bids, offers and trades. These factors simplify the comparison. Prices in financial markets almost always tend towards a single market clearing price for identical products. This is viewed as indicative of an efficient market. Variance in pricing is generally only expected for large size transactions, which may trade at a discount or a premium to the prevailing prices depending on the circumstances. It is the very efficiency of the market that drives the single price outcome. The tendency of efficient markets to generate a single clearing price is the not just the norm in financial markets, it is an expectation of market participants and market regulators. “Trading away” from a market price can be an offence enforced by the market regulator in certain circumstances. For competition analysis a market that consistently allows pricing to find a common level for similar products should suggest a competitive market, not a deficiency in competition. This feature of financial markets may be relevant in helping to resolve the apparent puzzle in the Draft Report that “Rivalry through price competition is rarely evident”.17 Price Competition Dynamics The Commission also expresses concern that the larger market participants are the price leaders with smaller institutions responding to their initiatives. The Commission may wish to consider the parallels of these behaviours with the market dynamics in financial markets. It is also the case in financial markets that larger market participants tend to lead pricing changes and smaller participants follow. This dynamic is intuitive when we consider that a retail investor wishing to buy or sell a small parcel of shares is unlikely to materially affect the pricing of a liquid security that might trade $200 million worth of shares daily. The prevailing market price is likely to be set by larger participants in the market (the so called ‘price makers’), who have large trading volume backed by a deep research and analytical capability not available to the average retail investor. This outcome is indicative of an efficient market that absorbs new information in an effective manner. Switching Thresholds The Commission raises concerns about the low levels of bank switching. There are parallels with this type of behaviour in the financial markets that it may be of assistance to consider. In modern markets trading is often available on a wide range of venues, including multiple exchanges, multiple venues for the same security within exchanges and internal matching engines at multiple brokers offering the same executions services.

16 This is not always the case - in debt markets they may differ by credit rating of the issuer etc. 17 Draft Report, p. 7.

20

Whether to switch venues will often be a calculation based on the net benefit of pricing gains versus switching costs. There are threshold levels that arise from the costs of switching (or ensuring that a particular venue is available as an alternative). While investors have a clear motivation to ensure their trades are conducted at the best priced venue they will switch venues less often when there are fewer pricing advantages offered by alternative venues. That is to say, low levels of switching can be indicative of either high switching costs or low pricing gains or both. Putting to one side switching costs, a more competitive environment between venues will produce less pricing gains and lower switching volumes. This effect occurs even in wholesale markets with sophisticated investors who are fully aware of the potential benefits of alternative venues, have full information and need no advice to make informed decisions. In this context, we note the surprising conclusion of the Draft Report that high levels of customer satisfaction combined with low levels of switching should be implied to demonstrate “a substantial failure in information and advice”18. The Commission may wish to explore if there are circumstances in which consumers do not want to incur switching costs (including time and effort) because they are satisfied with their choice or because potential gains are small etc. An important objective in this context would be to ensure that switching costs are maintained at their lowest economic level. Sectoral Efficiency In relation to market concentration, there are efficiencies that need to be considered at the sectoral level. In some cases, high concentration may be an indicator of productive efficiency rather than market power. The finance and insurance services sector has outperformed most other sectors in terms of multi-factor productivity growth over the last 25 years. Northcott notes that “Contestability is not necessarily related to concentration or the number of banks.”19 In financial markets infrastructure, it is not unusual for there to be relatively few or even a single firm offering core services. While increasing numbers of providers can increase competitive pressures, where the incremental cost of an additional provider is high the market will weigh such questions carefully. As such, outcomes with relatively modest numbers of providers can be efficient when balanced with the real world costs associated with increasing provider numbers. We are more optimistic than the Draft Report about the potential for future innovation and competition – in particular, the Draft Report’s statement that “This revolution [the 1990s and 2000s financial sector competition bringing innovation and pricing competition] is over”20. In a market based system, when business opportunities arise the market can be relied on to respond. Certainly, there is more work to do to ensure that the regulatory and tax settings are optimised to make certain that businesses are allowed to compete effectively. In Section 4 above, we discuss potential avenues for improvements to the regulatory environment.

18 Draft Report, p. 7. 19 Carol Northcott, “Competition in Banking: A Review of the Literature,” Working Paper 2004-24 (Ottawa: Bank of Canada, 2004), 30. 20 Report, p. 5.

21

Product Proliferation Product proliferation is a common feature of competitive market outcomes across a wide range of industries. Market based economies can produce a surprising wide range of products within each class of goods and services. However, a more planned economy might have a more limited range of consumer products and deter innovation. In the financial system, the institutional OTC financial markets thrive by balancing the demand for customised products with arrangements that support liquidity and efficient pricing. It is the dynamic of a free market driven by providers and users responding to their unique requirements and incentives that determine the shape of the aggregate market. In the retail market, the Draft Report observes that “The current approach to the provision of many financial products still, ultimately, puts the onus on consumers to find better deals and negotiate with providers, which places many at a disadvantage”21. The need for consumers to act and choose is a feature of market economies. The challenge of discriminating between a wide range of products can create consumer demand for assistance to sift through the alternatives that are available. This can be met by services like comparison websites, brokers and financial advisers, which if provided in an efficient and trustworthy manner, justify their cost to consumers and contribute to competition. The Commission also notes that “white labelling as a practice does not offer different features, just proliferation”. While white labelling may not increase real product choice, it can be economically efficient for the consumer by enabling them to reduce their search effort as they they can rely on a service provider or brand that they trust. The white labeller may be better placed to compete against others who have the scale to offer the product on their own account. It may also be efficient for the product initiator to leverage wider distribution channels and build scale that could reduce costs for consumers.

****

21 Draft Report, p. 7.