air france alitalia

TRANSCRIPT

www.exanebnpparibas-equities.com

Please refer to important disclosures at the end of this report.

Air France-KLM

Transport / France

Equity Research

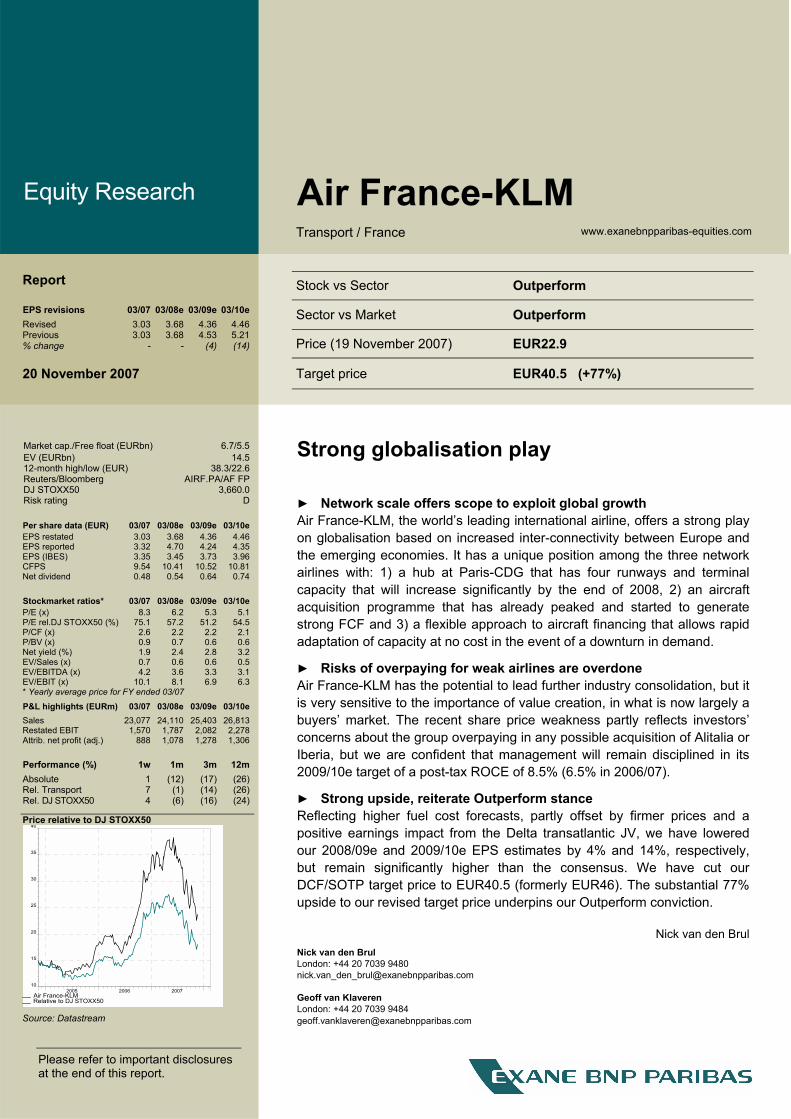

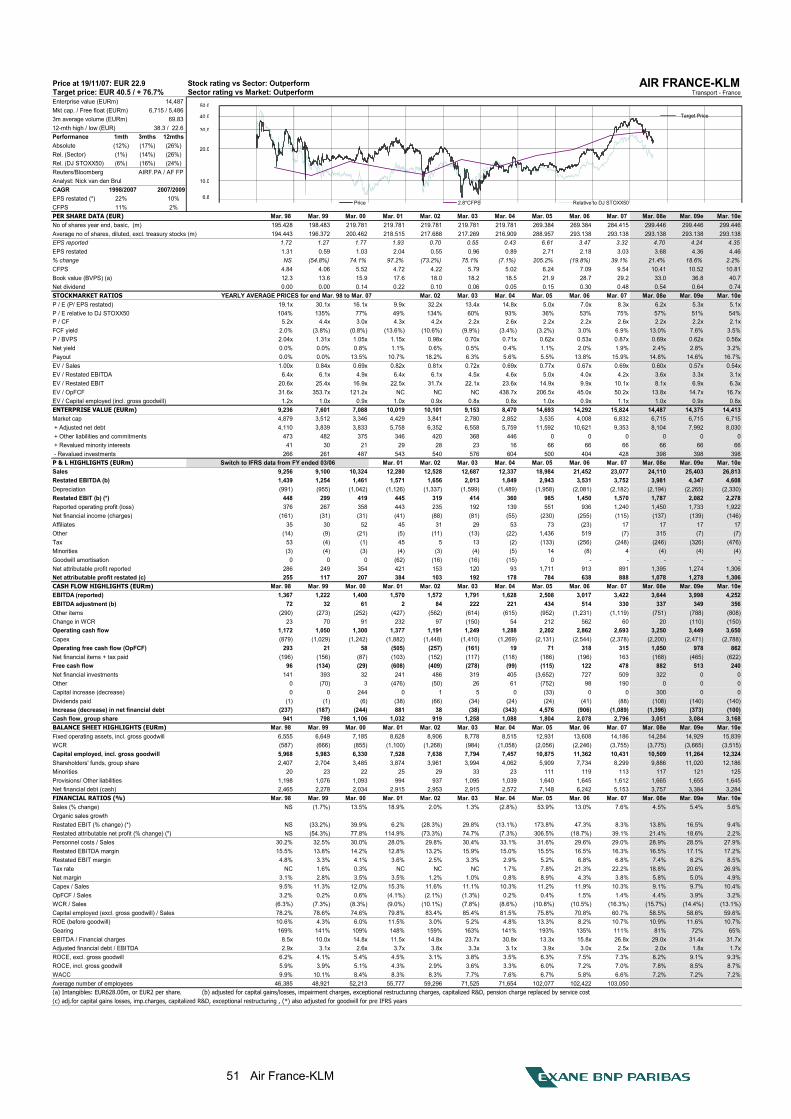

Report Stock vs Sector Outperform

Sector vs Market Outperform EPS revisions 03/07 03/08e 03/09e 03/10e Revised 3.03 3.68 4.36 4.46 Previous 3.03 3.68 4.53 5.21 % change - - (4) (14)

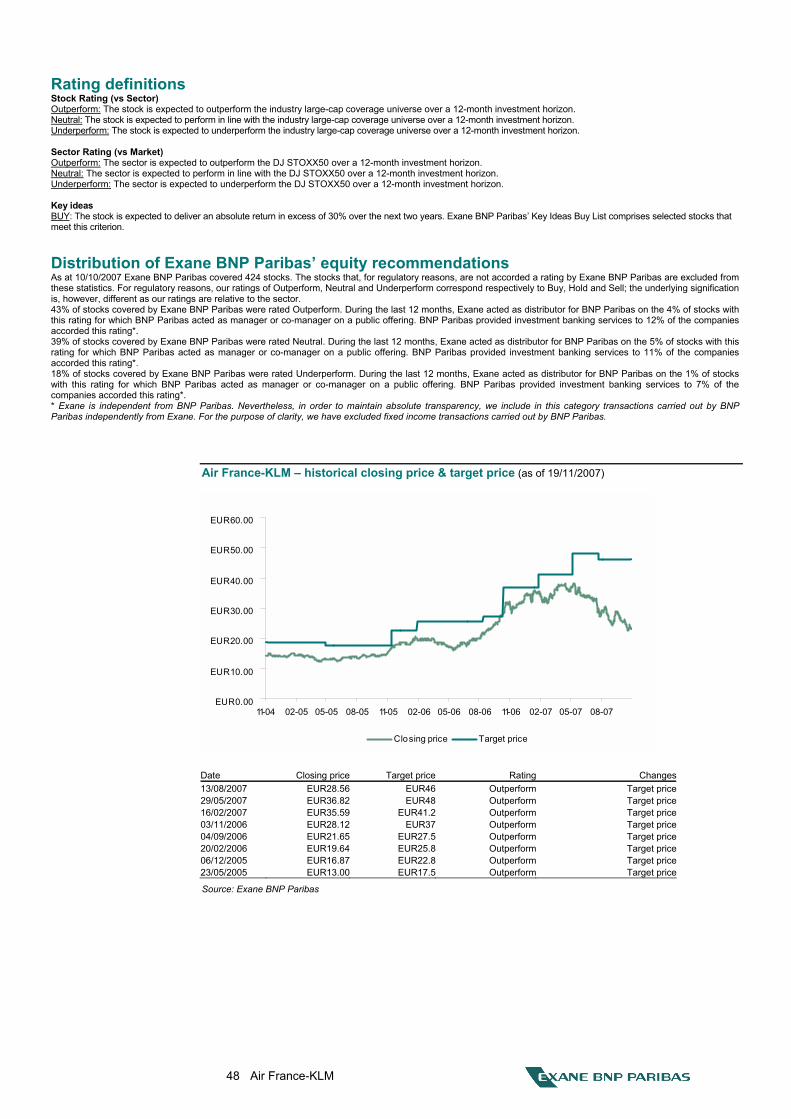

Price (19 November 2007) EUR22.9

20 November 2007

Target price EUR40.5 (+77%)

Strong globalisation play

► Network scale offers scope to exploit global growth Air France-KLM, the world�s leading international airline, offers a strong play on globalisation based on increased inter-connectivity between Europe and the emerging economies. It has a unique position among the three network airlines with: 1) a hub at Paris-CDG that has four runways and terminal capacity that will increase significantly by the end of 2008, 2) an aircraft acquisition programme that has already peaked and started to generate strong FCF and 3) a flexible approach to aircraft financing that allows rapid adaptation of capacity at no cost in the event of a downturn in demand.

► Risks of overpaying for weak airlines are overdone Air France-KLM has the potential to lead further industry consolidation, but it is very sensitive to the importance of value creation, in what is now largely a buyers� market. The recent share price weakness partly reflects investors� concerns about the group overpaying in any possible acquisition of Alitalia or Iberia, but we are confident that management will remain disciplined in its 2009/10e target of a post-tax ROCE of 8.5% (6.5% in 2006/07).

► Strong upside, reiterate Outperform stance Reflecting higher fuel cost forecasts, partly offset by firmer prices and a positive earnings impact from the Delta transatlantic JV, we have lowered our 2008/09e and 2009/10e EPS estimates by 4% and 14%, respectively, but remain significantly higher than the consensus. We have cut our DCF/SOTP target price to EUR40.5 (formerly EUR46). The substantial 77% upside to our revised target price underpins our Outperform conviction.

Nick van den BrulNick van den BrulLondon: +44 20 7039 [email protected] Geoff van KlaverenLondon: +44 20 7039 9484

Market cap./Free float (EURbn) 6.7/5.5 EV (EURbn) 14.5 12-month high/low (EUR) 38.3/22.6 Reuters/Bloomberg AIRF.PA/AF FP DJ STOXX50 3,660.0 Risk rating D

Per share data (EUR) 03/07 03/08e 03/09e 03/10e EPS restated 3.03 3.68 4.36 4.46 EPS reported 3.32 4.70 4.24 4.35 EPS (IBES) 3.35 3.45 3.73 3.96 CFPS 9.54 10.41 10.52 10.81 Net dividend 0.48 0.54 0.64 0.74

Stockmarket ratios* 03/07 03/08e 03/09e 03/10e P/E (x) 8.3 6.2 5.3 5.1 P/E rel.DJ STOXX50 (%) 75.1 57.2 51.2 54.5 P/CF (x) 2.6 2.2 2.2 2.1 P/BV (x) 0.9 0.7 0.6 0.6 Net yield (%) 1.9 2.4 2.8 3.2 EV/Sales (x) 0.7 0.6 0.6 0.5 EV/EBITDA (x) 4.2 3.6 3.3 3.1 EV/EBIT (x) 10.1 8.1 6.9 6.3 * Yearly average price for FY ended 03/07

P&L highlights (EURm) 03/07 03/08e 03/09e 03/10e Sales 23,077 24,110 25,403 26,813 Restated EBIT 1,570 1,787 2,082 2,278 Attrib. net profit (adj.) 888 1,078 1,278 1,306

Performance (%) 1w 1m 3m 12m Absolute 1 (12) (17) (26) Rel. Transport 7 (1) (14) (26) Rel. DJ STOXX50 4 (6) (16) (24)

Price relative to DJ STOXX50

2005 2006 200710

15

20

25

30

35

40

Air France-KLMRelative to DJ STOXX50

Source: DATASTREAM Source: Datastream [email protected]

2 Air France-KLM

Contents

Investment case__________________________________________ 3

Valuation upside on DCF/SOTP metrics _______________________ 8

Scale effects/cost cutting support margins ____________________ 12

Delta JV: taking advantage of Open Skies ____________________ 22

Airline acquisitions: risk/return trade-off_______________________ 28

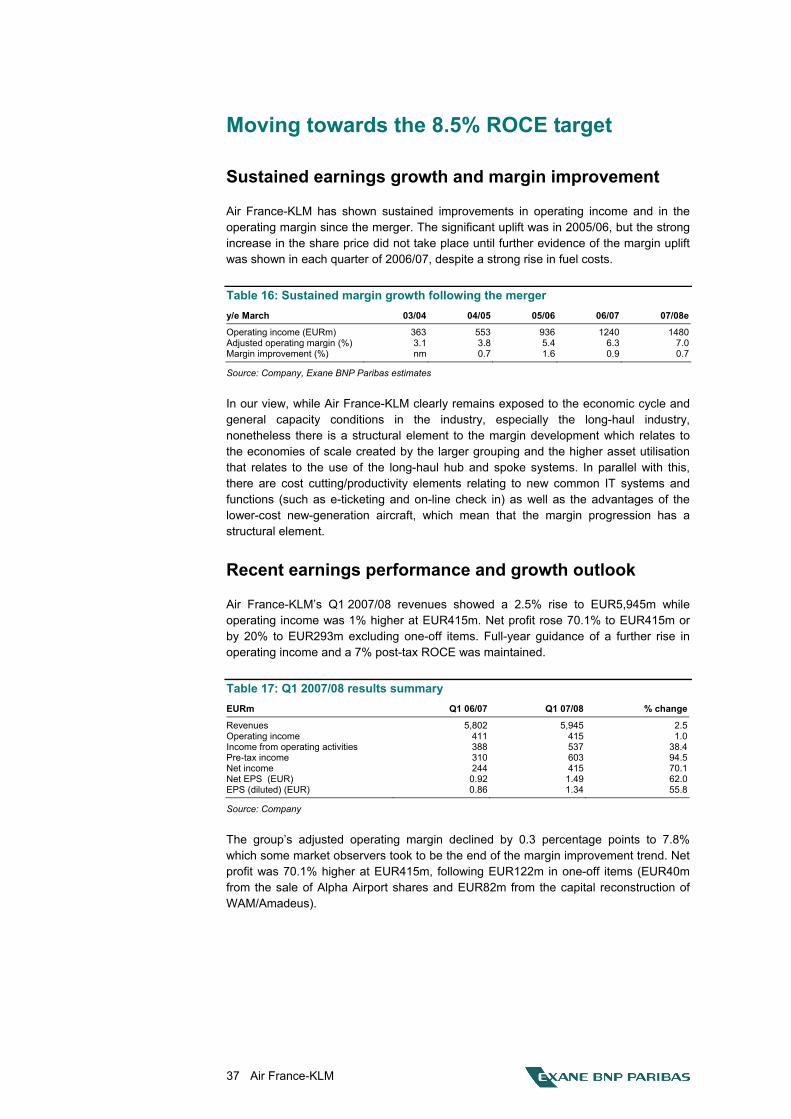

Moving towards the 8.5% ROCE target_______________________ 37

Strong FCF leading to net debt reduction _____________________ 44

Glossary_______________________________________________ 47

Company profile and financial highlights ______________________ 50

3 Air France-KLM

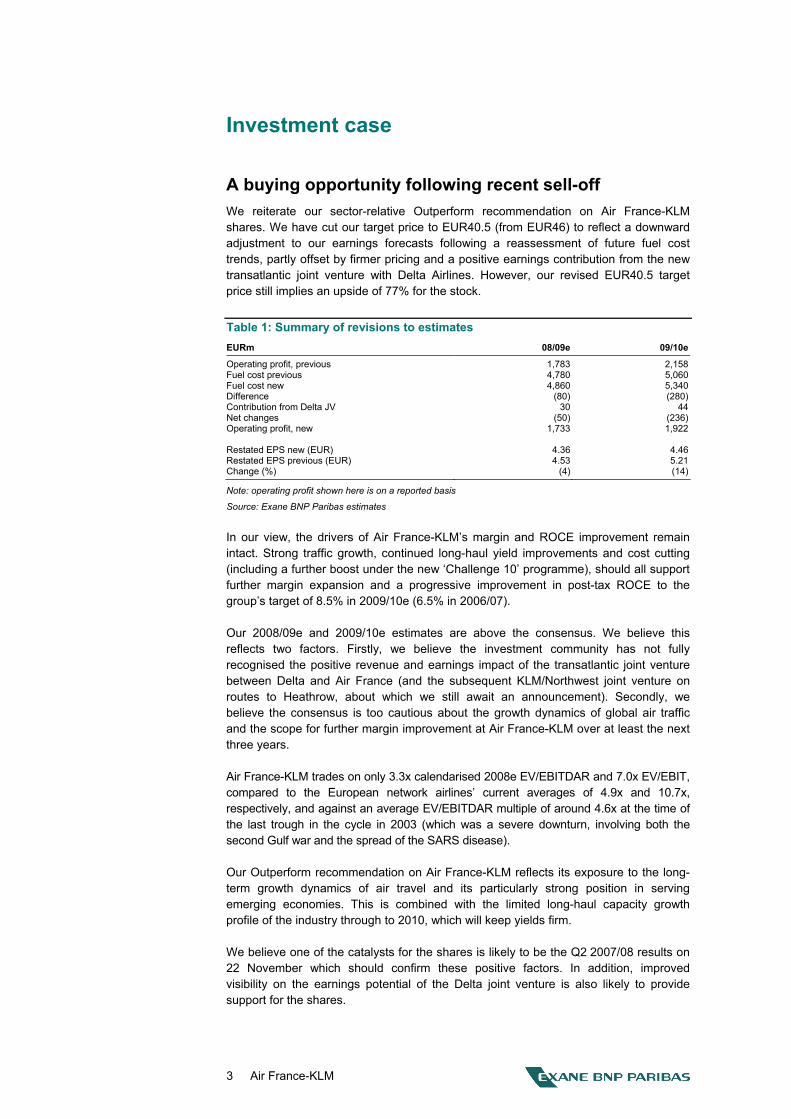

Investment case

A buying opportunity following recent sell-off We reiterate our sector-relative Outperform recommendation on Air France-KLM shares. We have cut our target price to EUR40.5 (from EUR46) to reflect a downward adjustment to our earnings forecasts following a reassessment of future fuel cost trends, partly offset by firmer pricing and a positive earnings contribution from the new transatlantic joint venture with Delta Airlines. However, our revised EUR40.5 target price still implies an upside of 77% for the stock.

Table 1: Summary of revisions to estimates EURm 08/09e 09/10e

Operating profit, previous 1,783 2,158Fuel cost previous 4,780 5,060Fuel cost new 4,860 5,340Difference (80) (280)Contribution from Delta JV 30 44Net changes (50) (236)Operating profit, new 1,733 1,922 Restated EPS new (EUR) 4.36 4.46Restated EPS previous (EUR) 4.53 5.21Change (%) (4) (14)

Note: operating profit shown here is on a reported basis

Source: Exane BNP Paribas estimates

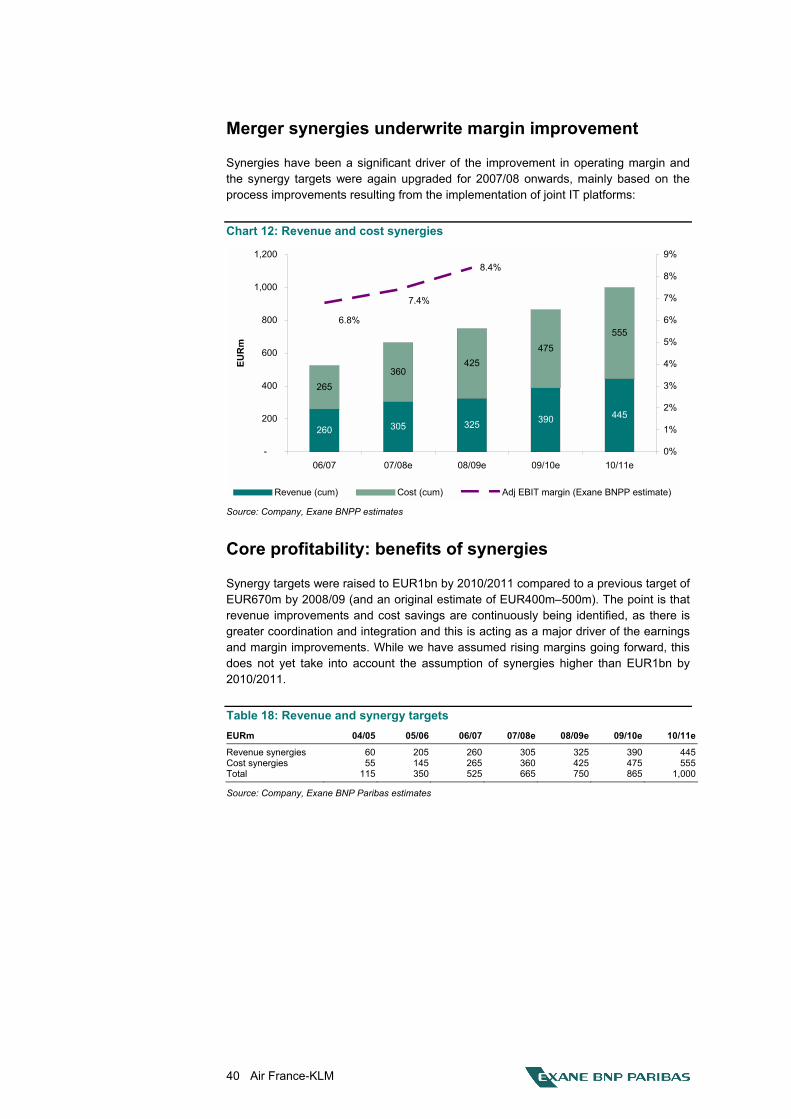

In our view, the drivers of Air France-KLM�s margin and ROCE improvement remain intact. Strong traffic growth, continued long-haul yield improvements and cost cutting (including a further boost under the new �Challenge 10� programme), should all support further margin expansion and a progressive improvement in post-tax ROCE to the group�s target of 8.5% in 2009/10e (6.5% in 2006/07).

Our 2008/09e and 2009/10e estimates are above the consensus. We believe this reflects two factors. Firstly, we believe the investment community has not fully recognised the positive revenue and earnings impact of the transatlantic joint venture between Delta and Air France (and the subsequent KLM/Northwest joint venture on routes to Heathrow, about which we still await an announcement). Secondly, we believe the consensus is too cautious about the growth dynamics of global air traffic and the scope for further margin improvement at Air France-KLM over at least the next three years.

Air France-KLM trades on only 3.3x calendarised 2008e EV/EBITDAR and 7.0x EV/EBIT, compared to the European network airlines� current averages of 4.9x and 10.7x, respectively, and against an average EV/EBITDAR multiple of around 4.6x at the time of the last trough in the cycle in 2003 (which was a severe downturn, involving both the second Gulf war and the spread of the SARS disease).

Our Outperform recommendation on Air France-KLM reflects its exposure to the long-term growth dynamics of air travel and its particularly strong position in serving emerging economies. This is combined with the limited long-haul capacity growth profile of the industry through to 2010, which will keep yields firm.

We believe one of the catalysts for the shares is likely to be the Q2 2007/08 results on 22 November which should confirm these positive factors. In addition, improved visibility on the earnings potential of the Delta joint venture is also likely to provide support for the shares.

4 Air France-KLM

Share price performance In 2006 and H1 07, Air France-KLM outperformed the CAC 40 index by 28.4% and strongly outperformed its benchmark competitors, Lufthansa and British Airways (BA). The main reason for this was Air France-KLM�s significant improvement in earnings and the trend towards higher margins that followed the merger (April 2004) between Air France and KLM, as efficient reorganisation of route networks and greater economies of scale led to improved asset utilisation.

In August 2007, Air France-KLM fell by over 30% in absolute terms and underperformed the CAC 40 index by 7.6%. Despite a recent recovery, the share price remains 72% below its June peak of EUR39.4.

In our view, the current share price assumes a collapse of passenger revenue growth and operating profit in 2008/2009. We have undertaken a worst case sensitivity analysis which assumes that growth in the passenger business falls to 0.4% and costs remain static in that year. As a result, operating profit for 2008/09 would more than halve from an estimated EUR1,733m to EUR727m, representing a 2.98% margin. Air France-KLM believes that with its new operating structure and cost profile, 3% would be the worst-case margin at the bottom of the cycle. Our DCF valuation using this scenario would give a valuation per share of EUR23.91, implying 4% upside to the current share price.

We have identified three reasons for the stock�s relative underperformance after the period of strong outperformance: 1) a perception from the Q1 2007/08 results (for the three months to end-June 2007) that the trend of margin improvement had stalled, 2) concerns that the turbulence in financial markets could herald a downturn in air traffic markets, and 3) speculation that the pending round of further airline consolidation in Europe (involving Alitalia, Iberia, Austrian Airlines, bmi and possibly SAS) could lead to Air France-KLM overpaying for second-tier airline assets in order to gain market share. We believe all these concerns are misconceived.

Margin trend remains positive

The group�s Q1 2007/08 results (announced 9 August) contained two major negative factors; a one-off adverse impact on business class travel reflecting the timing of public holidays in France and a negative impact from the US dollar�s decline against the euro, which had an adverse effect on intercontinental yields (but a positive effect on costs).

However, Air France-KLM confirmed its strong current performance in terms of traffic and yield at the Investor Day at Paris-CDG airport in October. The aberration of Q1 (which was impacted negatively by holidays) has not continued into Q2 and since July, cargo has been on a recovery trend.

The Q2 2007/08 results (to be announced on 22 November) are likely to benefit from the new cost-cutting programme, �Challenge 10�. This had a minimal impact on the Q1 2007/08 results because it had only been launched in May. Recent comments from management suggest that this Challenge 10 programme is likely to have had a positive impact on Q2 2007/08 results.

5 Air France-KLM

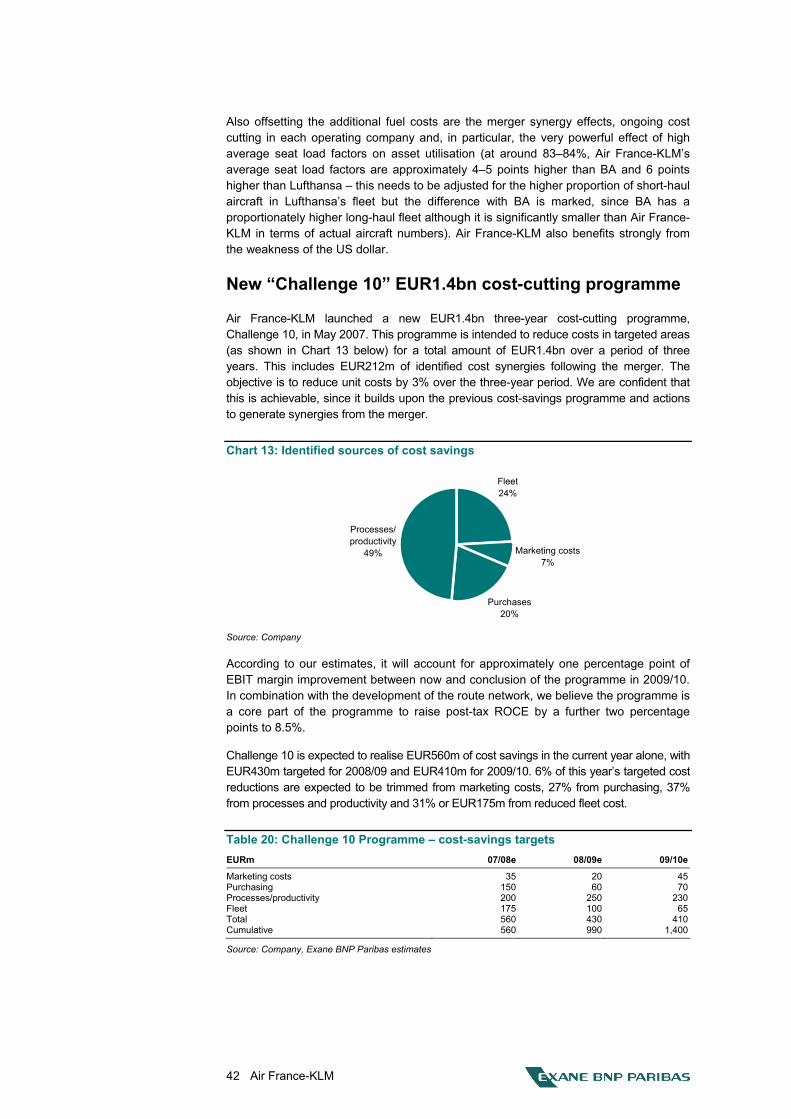

Around EUR130m of the EUR560m of targeted cost savings from the new Challenge 10 cost-savings programme for 2007/08 have been achieved. These EUR560m cost savings include EUR35m from marketing costs, EUR150m from purchasing costs, EUR200m in processes and productivity and EUR175m from the fleet modernisation. This programme is expected to achieve total savings of EUR1.4bn over three years.

Furthermore, management confirmed that the 7% post-tax ROCE target (implying a 0.9 percentage point increase in the EBIT margin to 7.4% in 2007/08e) should be easily achieved. The implication is a small increase in our full year 2007/08 estimates, but this is neutralised by the estimated EUR60m EBIT cost of the cabin crew strike at the end of October. Consequently, we leave our 2007/08 EPS forecasts unchanged.

We are confident that the rising trend of EBIT margins should continue in at least 2007/08e, 2008/09e and 2009/10e.

Air traffic still growing, boosted by emerging economies

In our view, Air France-KLM remains one of the best European plays on globalisation, as the leading connector of Europe to the growth economies in Asia, Latin America, Middle East/Africa and Eastern Europe. Our analysis shows that, while US�Europe and domestic US traffic have clearly started to slow, traffic to and from the emerging economies remains very robust. Air France-KLM, as the world�s largest international airline, looks particularly well placed to benefit from the continued growth of the global economy.

Air France-KLM is a well-managed airline with an increasing long-haul orientation and has moved from the number three position in Europe to the clear market leader in both Europe and the international airline business within the space of three years. Much of the reason for this lies in the scale and continuous improvements in the structure of the group�s hub and spoke network.

Air France-KLM has the greatest exposure of all European airlines to the world's growth economies in Asia, Latin America and Middle East/Africa. (These three regions accounted for 48% of passenger revenues in 2006/07). Furthermore, new capacity growth in the next five years is concentrated in these areas so this percentage will increase. The group, therefore, enjoys a growth dynamic which, in our view, will continue to perform strongly despite an anticipated slowdown in the US and European economies. (By contrast, BA is heavily exposed to UK�US traffic which accounts for around 65% of its operating profit. The US domestic air travel market has started to weaken and US airlines are suffering more from higher oil prices as they do not gain from the sharp fall in the US dollar this year. In contrast, the fall in the US dollar is helping to contain fuel, depreciation and other costs of European airlines).

We believe the new joint venture agreement with Delta and closer ties with China Southern also offer good long-term growth opportunities for the group and that these have possibly not been fully recognised by the investment community.

6 Air France-KLM

Strict ROCE criteria in any acquisition scenario In our view, industry consolidation will accelerate as Open Skies between Europe and the US starts to put pressure on protected �national� niche operations (for example, Milan�New York), eroding the profitability of those routes. Therefore, we believe the industry is in a process of voluntary consolidation for those smaller airlines which will need to seek the protection of economies of scale, the support of an efficient fuel hedging programme, access to capital for investment and participation in the large corporate account programmes which drive network airlines� profitability. Air France-KLM should benefit significantly from this consolidation process.

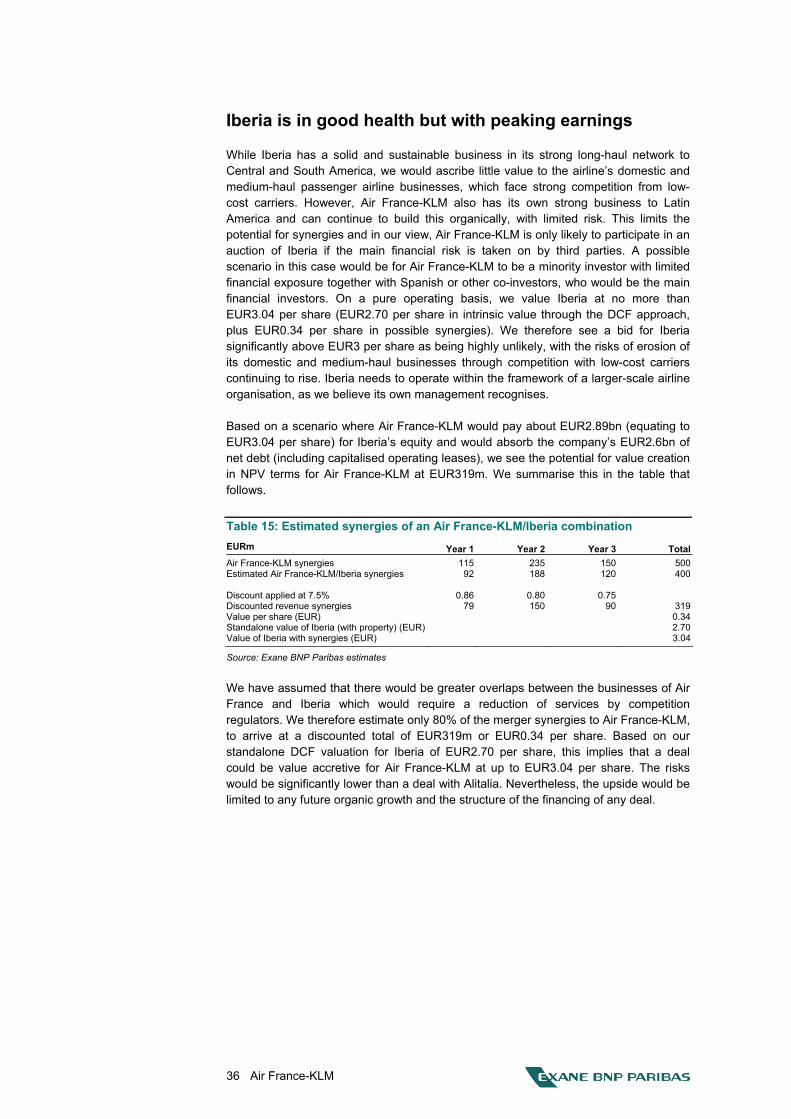

Iberia and Alitalia have put themselves up, or been put up, for sale now for almost a year. However, Air France-KLM and Lufthansa, the two most obvious acquirers, have sensibly waited for potentially improved acquisition terms. The conditions have improved and the �speculative� appetite from private equity funds has probably diminished as highly leveraged bids appear less likely in the current market climate. In these circumstances, we believe Air France-KLM is much less likely to overpay for vulnerable operating airline assets, especially as the experience of acquiring KLM (and also Swiss) shows that the balance of advantages in terms of scale and strength of balance sheet is with the acquirer.

The benefits of consolidation are closely linked to improvements in operations, which have a direct impact on asset utilisation and thus on earnings and margins. Linking hub and spoke networks allows airlines to concentrate routes, allowing larger, more efficient aircraft and more frequent services. As occurred following the merger with KLM, the addition of a new spoke to a hub and spoke airline network significantly increases the city-pair combinations served by the network, at minimal additional cost. Thus, while small-scale, standalone airline operations can be unprofitable (such as Alitalia) within the framework of linked hub and spoke networks, they can turn round their fortunes relatively quickly if the network is reconstructed and linked effectively and overlapping costs are eliminated quickly.

Air France-KLM has commented that it is "interested in" Iberia and Alitalia, but as yet there do not appear to be any concrete negotiations. Indeed, it seems more likely that Iberia will be acquired by a Spanish investor group. Furthermore, Air France-KLM�s President and CEO, J-C Spinetta, has consistently stated that no deal would be done with either Alitalia or Iberia which could jeopardise the group�s achievement of its 2009/2010 post-tax ROCE target of 8.5%.

EPS forecasts trimmed reflecting oil price

We have revised our 2008/09e and 2009/10e EPS estimates downwards by 4% and 14%, respectively, to reflect, in part, the group�s revised oil price forecasts. The negative impact of these higher oil price assumptions is partly offset by firmer prices (see below). The new estimates assume structurally higher oil prices because of tight capacity, higher extraction costs and (implicitly) sustained global demand. Our forecasts are based on the group�s assumptions of an average Brent oil price of USD81/bbl for 2007/08, USD88/bbl for 2008/09 and USD84/bbl for 2009/2010.

The group is 78% hedged against the fuel price this year, giving a net price of USD66/bbl, and is 67% hedged next year (2008/09e), giving a USD69/bbl final price.

Incorporating the group�s revised estimates and the impact of the fuel cost hedge, we keep our estimate of hedged fuel costs for Air France-KLM for the current year at EUR4.6bn, but increase our estimates for 2008/09 to EUR4.86bn (+1.7%), for 2009/10 to EUR5.34bn (+5.5%) and for 2010/11 to EUR5.62bn (+7.5%).

7 Air France-KLM

Price component of yield remains firm

Air France-KLM has managed to compensate for fuel price increases with a progressive increase in fuel surcharges on tickets, which reached EUR72 on a long-haul flight for Air France and EUR70 for KLM in early November (following an earlier increase in September). This is because capacity constraints and rising load factors on long-haul routes have given the leading long-haul airlines pricing power which is partly compensating for the sharp rises in oil prices. While there has been a strong increase in short-haul, low-cost capacity this year, capacity remains constrained on long-haul routes. We do not see this easing until 2009 at the earliest.

Yields should continue to be supported by further consolidation (Alitalia, Iberia and closer relationships between members of the three international airline alliances, SkyTeam, Star and oneworld). Air France-KLM�s passenger traffic has been growing at over 5% this year to date, focused on growth areas in the global economy. Capacity is scheduled to increase by 5.2% for the winter season (October�March) and this is focused on destinations in high-growth emerging economies (China, Latin America, Middle East/Africa and Eastern Europe). Additional frequencies to Shanghai and Hong Kong alone will increase capacity on those specific routes by 20% in anticipation of strongly rising demand.

Delta joint venture to boost earnings from 2008/09e

Partly offsetting the impact of the higher fuel price, the group�s transatlantic joint venture with Delta, announced in October, will provide a further boost to earnings. We estimate that the Delta joint venture (which is entirely incremental to earnings for Air France-KLM until 2010/11, when the joint venture�s parameter will be expanded to include existing routes) will add EUR31m to operating earnings in 2008/09 and EUR44m for 2009/10. This has a positive effect on our EPS estimates of EUR0.10 for 2008/09e and EUR0.15 for 2009/10e.

The net effect, taking into consideration a higher fuel cost and a positive contribution from the joint venture, is that our EPS estimates decline by 4% to EUR4.36 for 2008/09e and by 14% to EUR4.46 for 2009/10e. Consolidation and closer cooperation within alliances has a positive net effect that partly compensates for higher oil prices, the remaining unmanageable variables being the movement of the US dollar (a US dollar decline is positive for Air France-KLM�s costs, although it would have a negative impact on the joint venture�s contribution) and the group�s ability to increase fuel surcharges (mainly long-haul passenger airline prices) further. We consider our estimates for the potential benefits of the Delta joint venture, which is the only quantifiable effect of the proposed joint venture initiatives at present as very conservative and see room for upgrades.

8 Air France-KLM

Valuation upside on DCF/SOTP metrics

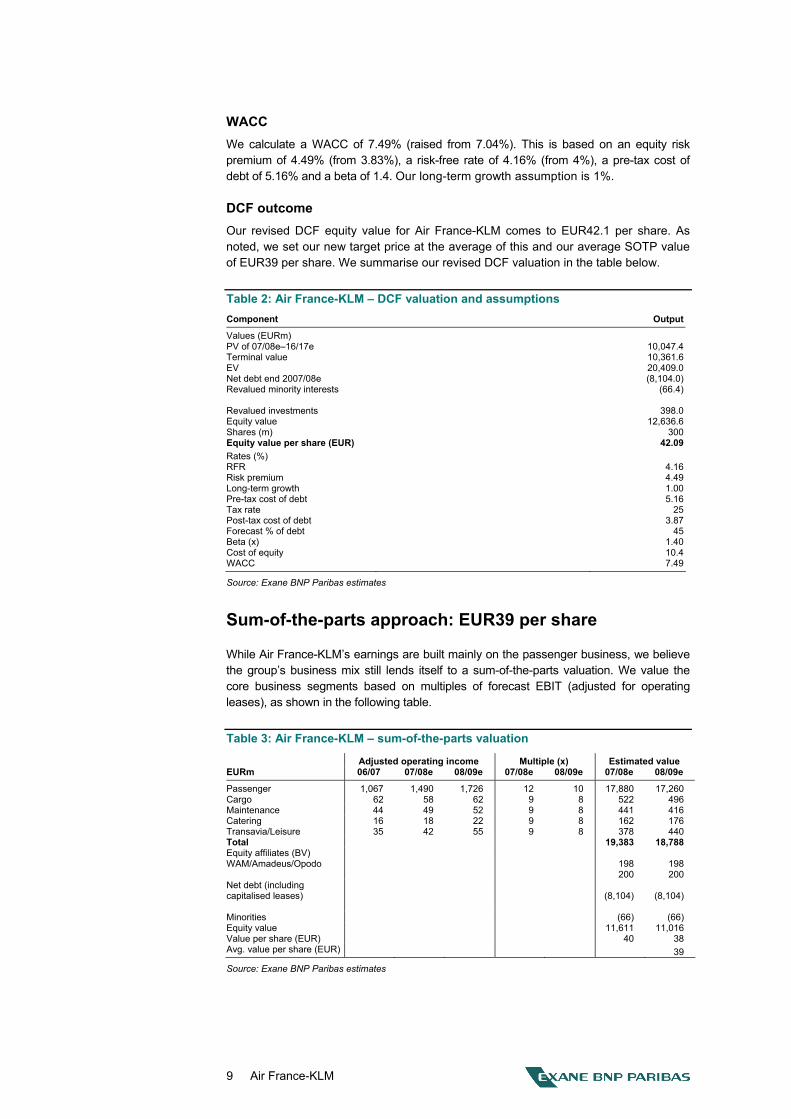

Our approach to the value of Air France-KLM is to look at comparative and sum-of-the-parts metrics around a core DCF valuation. The DCF method captures both the airline�s cash flow generation and capital expenditure on replacement fleet assets. Based on an average of our DCF and SOTP approaches, we calculate an equity value for Air France-KLM of EUR12,158m, corresponding to EUR40.5 per share. Our DCF approach produces a value of EUR42.1 per share and our sum-of-the-parts model produces a range of EUR38�40 per share with an average of EUR39. Our revised target price of EUR40.5 is based on the average of the DCF and SOTP outcomes.

Air France-KLM�s valuation discount to BA of 27% on calendarised 2008e EV/EBITDAR multiples at current price levels looks unjustified. Air France-KLM�s earnings growth outlook is strongly positive and better than BA�s, with a positive earnings increment from Open Skies (not included in the current guidance) but without the significant risks posed by the sudden impact of new competition for BA at Heathrow, for example.

We are confident in the ability of Air France-KLM�s management to deliver increased earnings growth and higher margins from the implementation of the Challenge 10 cost-cutting programme and the realisation of further synergies from the merger, notably through the introduction of common IT systems. Our valuation takes into account a raised fuel cost assumption (detailed below) and rolls forward our DCF valuation to the end of 2008.

DCF model: EUR42.1 per share

Our DCF valuation is based on our assessment of the network and cost synergies still to be extracted from the merger, along with the ongoing boost to forecast earnings from the Challenge 10 cost-savings programme under way and the positive impact of the Delta joint venture, set against a higher medium-term fuel cost forecast of approximately USD81/bbl Brent equivalent. We set out our key assumptions as follows.

Traffic and yields Our passenger traffic growth assumptions are 6% for 2007/08 and 5% for 2008/09. The main driver is likely to be intercontinental traffic, continuing the trend of recent months. We assume a (post-currency effect) trend in yields (in terms of revenue per RPK) of -0.5% this year, +0.2% for 2008/09eand approximately +0.5% p.a. thereafter.

Oil price and fuel costs We have used higher oil price assumptions as the basis for our post-hedge fuel price estimates for Air France-KLM. Our Oil & Gas team�s current oil price estimates (revised in early October 2007) assume structurally higher oil prices because of tight capacity, higher extraction costs and (implicitly) sustained global demand. Our actual fuel cost estimates are based on the Air France-KLM group�s latest assumptions of an average Brent oil price of USD81/bbl for 2007/08, USD88/bbl for 2008/09, USD84/bbl for 2009/10 and USD82/bbl for 2010/11. Using these revised assumptions, we keep our estimate of hedged fuel costs for the current year at EUR4.6bn but increase our estimates for 2008/09 to EUR4.86bn (+1.7%), for 2009/10 to EUR5.34bn (+5.5%) and for 2010/11 to EUR5.62bn (+7.5%).

9 Air France-KLM

WACC We calculate a WACC of 7.49% (raised from 7.04%). This is based on an equity risk premium of 4.49% (from 3.83%), a risk-free rate of 4.16% (from 4%), a pre-tax cost of debt of 5.16% and a beta of 1.4. Our long-term growth assumption is 1%.

DCF outcome Our revised DCF equity value for Air France-KLM comes to EUR42.1 per share. As noted, we set our new target price at the average of this and our average SOTP value of EUR39 per share. We summarise our revised DCF valuation in the table below.

Table 2: Air France-KLM � DCF valuation and assumptions Component Output

Values (EURm) PV of 07/08e�16/17e 10,047.4Terminal value 10,361.6EV 20,409.0Net debt end 2007/08e (8,104.0)Revalued minority interests (66.4) Revalued investments 398.0Equity value 12,636.6Shares (m) 300Equity value per share (EUR) 42.09Rates (%) RFR 4.16Risk premium 4.49Long-term growth 1.00Pre-tax cost of debt 5.16Tax rate 25Post-tax cost of debt 3.87Forecast % of debt 45Beta (x) 1.40Cost of equity 10.4WACC 7.49

Source: Exane BNP Paribas estimates

Sum-of-the-parts approach: EUR39 per share

While Air France-KLM�s earnings are built mainly on the passenger business, we believe the group�s business mix still lends itself to a sum-of-the-parts valuation. We value the core business segments based on multiples of forecast EBIT (adjusted for operating leases), as shown in the following table.

Table 3: Air France-KLM � sum-of-the-parts valuation

Adjusted operating income Multiple (x) Estimated value EURm 06/07 07/08e 08/09e 07/08e 08/09e 07/08e 08/09e

Passenger 1,067 1,490 1,726 12 10 17,880 17,260 Cargo 62 58 62 9 8 522 496 Maintenance 44 49 52 9 8 441 416 Catering 16 18 22 9 8 162 176 Transavia/Leisure 35 42 55 9 8 378 440 Total 19,383 18,788 Equity affiliates (BV) WAM/Amadeus/Opodo 198 198 200 200 Net debt (including capitalised leases) (8,104) (8,104) Minorities (66) (66) Equity value 11,611 11,016 Value per share (EUR) 40 38 Avg. value per share (EUR) 39

Source: Exane BNP Paribas estimates

10 Air France-KLM

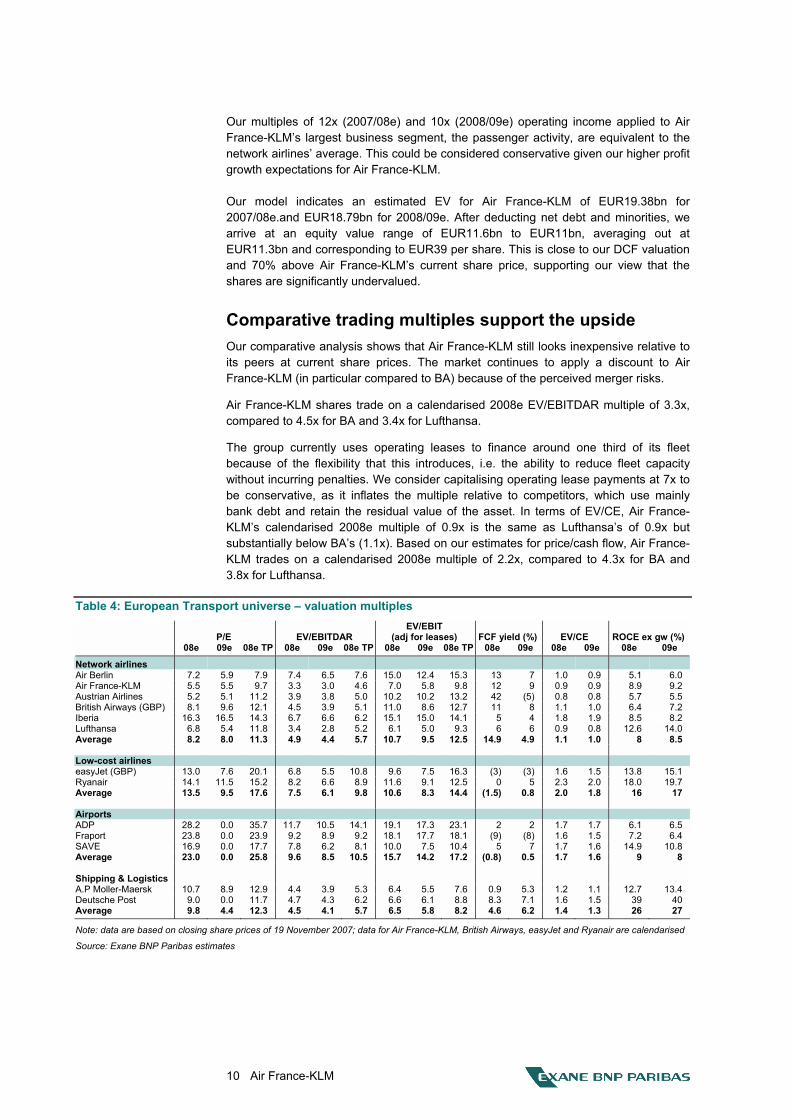

Our multiples of 12x (2007/08e) and 10x (2008/09e) operating income applied to Air France-KLM�s largest business segment, the passenger activity, are equivalent to the network airlines� average. This could be considered conservative given our higher profit growth expectations for Air France-KLM.

Our model indicates an estimated EV for Air France-KLM of EUR19.38bn for 2007/08e.and EUR18.79bn for 2008/09e. After deducting net debt and minorities, we arrive at an equity value range of EUR11.6bn to EUR11bn, averaging out at EUR11.3bn and corresponding to EUR39 per share. This is close to our DCF valuation and 70% above Air France-KLM�s current share price, supporting our view that the shares are significantly undervalued.

Comparative trading multiples support the upside Our comparative analysis shows that Air France-KLM still looks inexpensive relative to its peers at current share prices. The market continues to apply a discount to Air France-KLM (in particular compared to BA) because of the perceived merger risks.

Air France-KLM shares trade on a calendarised 2008e EV/EBITDAR multiple of 3.3x, compared to 4.5x for BA and 3.4x for Lufthansa.

The group currently uses operating leases to finance around one third of its fleet because of the flexibility that this introduces, i.e. the ability to reduce fleet capacity without incurring penalties. We consider capitalising operating lease payments at 7x to be conservative, as it inflates the multiple relative to competitors, which use mainly bank debt and retain the residual value of the asset. In terms of EV/CE, Air France-KLM�s calendarised 2008e multiple of 0.9x is the same as Lufthansa�s of 0.9x but substantially below BA�s (1.1x). Based on our estimates for price/cash flow, Air France-KLM trades on a calendarised 2008e multiple of 2.2x, compared to 4.3x for BA and 3.8x for Lufthansa.

Table 4: European Transport universe � valuation multiples

P/E EV/EBITDAR EV/EBIT

(adj for leases) FCF yield (%) EV/CE ROCE ex gw (%) 08e 09e 08e TP 08e 09e 08e TP 08e 09e 08e TP 08e 09e 08e 09e 08e 09e

Network airlines Air Berlin 7.2 5.9 7.9 7.4 6.5 7.6 15.0 12.4 15.3 13 7 1.0 0.9 5.1 6.0 Air France-KLM 5.5 5.5 9.7 3.3 3.0 4.6 7.0 5.8 9.8 12 9 0.9 0.9 8.9 9.2 Austrian Airlines 5.2 5.1 11.2 3.9 3.8 5.0 10.2 10.2 13.2 42 (5) 0.8 0.8 5.7 5.5 British Airways (GBP) 8.1 9.6 12.1 4.5 3.9 5.1 11.0 8.6 12.7 11 8 1.1 1.0 6.4 7.2 Iberia 16.3 16.5 14.3 6.7 6.6 6.2 15.1 15.0 14.1 5 4 1.8 1.9 8.5 8.2 Lufthansa 6.8 5.4 11.8 3.4 2.8 5.2 6.1 5.0 9.3 6 6 0.9 0.8 12.6 14.0 Average 8.2 8.0 11.3 4.9 4.4 5.7 10.7 9.5 12.5 14.9 4.9 1.1 1.0 8 8.5

Low-cost airlines easyJet (GBP) 13.0 7.6 20.1 6.8 5.5 10.8 9.6 7.5 16.3 (3) (3) 1.6 1.5 13.8 15.1 Ryanair 14.1 11.5 15.2 8.2 6.6 8.9 11.6 9.1 12.5 0 5 2.3 2.0 18.0 19.7 Average 13.5 9.5 17.6 7.5 6.1 9.8 10.6 8.3 14.4 (1.5) 0.8 2.0 1.8 16 17

Airports ADP 28.2 0.0 35.7 11.7 10.5 14.1 19.1 17.3 23.1 2 2 1.7 1.7 6.1 6.5 Fraport 23.8 0.0 23.9 9.2 8.9 9.2 18.1 17.7 18.1 (9) (8) 1.6 1.5 7.2 6.4 SAVE 16.9 0.0 17.7 7.8 6.2 8.1 10.0 7.5 10.4 5 7 1.7 1.6 14.9 10.8 Average 23.0 0.0 25.8 9.6 8.5 10.5 15.7 14.2 17.2 (0.8) 0.5 1.7 1.6 9 8

Shipping & Logistics A.P Moller-Maersk 10.7 8.9 12.9 4.4 3.9 5.3 6.4 5.5 7.6 0.9 5.3 1.2 1.1 12.7 13.4 Deutsche Post 9.0 0.0 11.7 4.7 4.3 6.2 6.6 6.1 8.8 8.3 7.1 1.6 1.5 39 40 Average 9.8 4.4 12.3 4.5 4.1 5.7 6.5 5.8 8.2 4.6 6.2 1.4 1.3 26 27

Note: data are based on closing share prices of 19 November 2007; data for Air France-KLM, British Airways, easyJet and Ryanair are calendarised

Source: Exane BNP Paribas estimates

11 Air France-KLM

At 12% for 2008e and 9% for 2009e (both calendarised), Air France-KLM�s projected FCF yield is higher than those of BA and Lufthansa, largely because Air France-KLM already generates strong cash flow, reflecting in part its decision to renew the long-haul fleet earlier than its main rivals.

We believe the discount applied to Air France-KLM is unjustified, as we see considerably fewer operational risks for Air France-KLM than for BA. This is particularly the case because of the vulnerability of the latter�s North Atlantic yields to an Open Skies agreement and its free cash flow erosion following the sharply increased capex requirements in connection with the long-haul fleet renewal from 2009.

Our adjusted EBIT margin forecasts have changed in accordance with our revised fuel cost assumptions but synergy upgrades, and in particular the contribution from the new joint ventures, should provide scope to increase them in the future.

Valuation risks The main risk to our valuation scenario for Air France-KLM relates to the possibility of a downturn in traffic based on a fall-off in demand. However, the consensus remains in favour of a positive outlook for global growth in airline traffic volumes and for Air France-KLM in particular, based on sustained growth of the emerging economies.

There is also the threat of a much higher level of jet fuel prices, and as noted we have raised our cost estimates for 2008/09 and onwards to take account of this. However, these are chiefly short/medium-term earnings risks that apply to all airlines. As noted, Air France-KLM has a highly protective hedge in place through 2007/08 and lower, but still significant, levels of hedging that are higher than those of competitors for 2008/09 and 2009/10. Our emphasis is on the medium-term opportunities for cash flow enhancement through the greater market presence and higher asset utilisation achieved through the merger, as well as the opportunities to cut costs. We believe the fuel price risk is factored into the shares� current valuation and the valuation discount has been overstated. As discussed in the section, �Airline acquisitions: risk/return trade-off�, later in this report, we believe the possibility of a loss of value as a consequence of overpaying for second-tier airlines is minimal, given management�s track record and continuing cautious approach to acquisitions.

12 Air France-KLM

Scale effects/cost cutting support margins

The logic behind the Air France-KLM merger in 2004 was to increase revenues through a widening of the marketing reach (economies of scope) and to reduce joint costs and improve aircraft utilisation through process reorganisation and integration (economies of scale). In our view, both factors are already resulting in, and continue to underpin, progressive improvements in asset utilisation and thus in margins and ROCE. Air France-KLM brought forward its 7% post-tax ROCE target by two years to the current year and raised its 2009/10 target by 1.5% to 8.5%. In our view, this implies that Air France-KLM is confident of achieving a 2009/10 EBIT margin adjusted for leases of at least 8%.

In this section, we examine two areas where margin has or could grow, based on increased scale effects. The first is an analysis of the scale effects which have built margin expansion since the merger between Air France and KLM and which create the platform for further growth. The second, more speculative, but nonetheless, real analysis is an attempt to quantify the potential earnings enhancement that could be created through an acquisition of either Alitalia or Iberia, as well as the potential benefits from the establishment of transatlantic joint venture operations between Air France-KLM and their US SkyTeam alliance partners, Delta and Northwest Airlines.

Earnings driven by the global network The group�s main revenue drivers are the larger network/schedule choice available to customers through the densification of international services from the two European hubs (Paris and Amsterdam) and fusion of pricing and distribution channels of the two airlines, combined with code-share links to the global SkyTeam alliance network. The improvement in profits and margins is coming from both higher revenues and savings in costs. Our SWOT analysis shown below indicates that Air France-KLM has significant advantages over its main competitors, especially the growing focus on long-haul services to emerging economies and the significant increase in scale and the development of the twin hub and spoke system, which benefits from an unconstrained airport asset base.

Table 5: Air France-KLM � SWOT analysis

Strengths Weaknesses

! Leading European/global airline group with significant economies of scale.

! Enhanced European catchment area

! Twin hub focus reinforcing pricing/marketing power

! Efficient new fleet

! Growing proportion of long-haul flights

! Greater proportion of �unique� destinations from Europe

! High capex but lower than competitors going forward

! Need to promote further a �competitive� culture

! Financial leverage (but declining)

! �Complexity� cost cutting needs to be ongoing

Opportunities Threats

! Capitalise on central dual hub-based network

! Capture European sourced international traffic

! Use SkyTeam alliance to strengthen margins

! Improve labour relations via employee ownership programme

! Generate cost cuts to raise margins

! Short-haul pricing pressure as competition intensifies

! Persistently high fuel costs

! Personnel cost increases despite long-term agreements in place

! Collapse or weakness of partner airlines

Source: Exane BNP Paribas

13 Air France-KLM

New management structure in place

Earlier this year, Air France-KLM introduced a new combined executive management structure on a functional basis, replacing the separate management structures in Air France and KLM. In place of the Strategic Management Committee, which had supervised the development of Air France and KLM over 2004�2007, the business is being managed from 2007 through an Executive Committee whose members have a group level responsibility and can come from either Air France or KLM while retaining their responsibilities at a company level. This should facilitate the introduction of the process and productivity improvements which are part of the �Challenge 10� cost-savings programme, discussed in the later section, �Moving towards the 8.5% ROCE target�.

Global network is a platform for growth

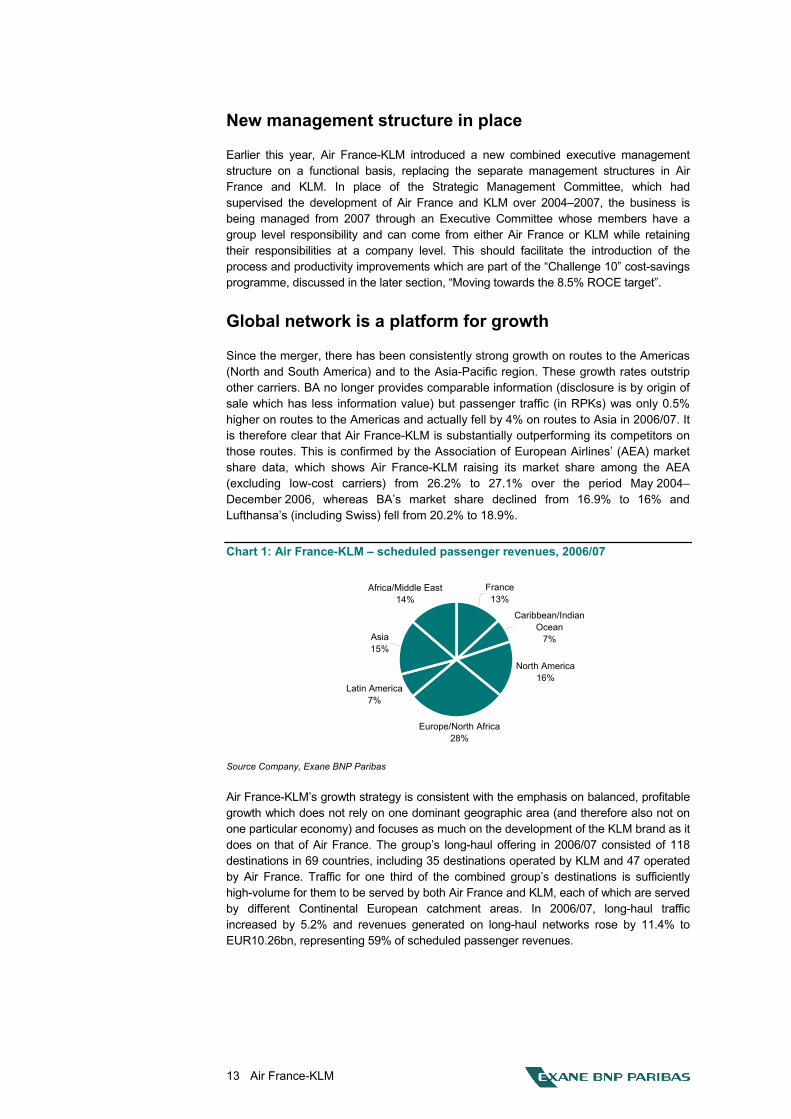

Since the merger, there has been consistently strong growth on routes to the Americas (North and South America) and to the Asia-Pacific region. These growth rates outstrip other carriers. BA no longer provides comparable information (disclosure is by origin of sale which has less information value) but passenger traffic (in RPKs) was only 0.5% higher on routes to the Americas and actually fell by 4% on routes to Asia in 2006/07. It is therefore clear that Air France-KLM is substantially outperforming its competitors on those routes. This is confirmed by the Association of European Airlines� (AEA) market share data, which shows Air France-KLM raising its market share among the AEA (excluding low-cost carriers) from 26.2% to 27.1% over the period May 2004�December 2006, whereas BA�s market share declined from 16.9% to 16% and Lufthansa�s (including Swiss) fell from 20.2% to 18.9%.

Chart 1: Air France-KLM � scheduled passenger revenues, 2006/07

France13%

Caribbean/Indian Ocean

7%

North America16%

Europe/North Africa28%

Latin America7%

Africa/Middle East14%

Asia15%

Source Company, Exane BNP Paribas

Air France-KLM�s growth strategy is consistent with the emphasis on balanced, profitable growth which does not rely on one dominant geographic area (and therefore also not on one particular economy) and focuses as much on the development of the KLM brand as it does on that of Air France. The group�s long-haul offering in 2006/07 consisted of 118 destinations in 69 countries, including 35 destinations operated by KLM and 47 operated by Air France. Traffic for one third of the combined group�s destinations is sufficiently high-volume for them to be served by both Air France and KLM, each of which are served by different Continental European catchment areas. In 2006/07, long-haul traffic increased by 5.2% and revenues generated on long-haul networks rose by 11.4% to EUR10.26bn, representing 59% of scheduled passenger revenues.

14 Air France-KLM

KLM appears to be participating equally in long-haul growth. This has been the consistent trend since the merger took place, showing the predicted benefits to KLM of access to Air France�s much larger network and customer base. Both operating companies have started to see a greater correlation of their business with the global economy rather than with their home markets, as evidenced by recent traffic figures. Air France-KLM is successfully expanding its premium passenger base from destination countries and through connecting passengers, as reflected in the results (2006/07 showed a 17% increase in the premium transfer passenger yield, the RASK, excluding currency effects) on long-haul traffic compared to a rise in the economy class yield of only 6%). Around 40% of passengers on Asian routes originate in Asia.

The merged Air France-KLM group is now playing to its strength, which is the increasing power of its combined schedules and common ticketing system to attract long-haul business and leisure passengers (hence load factors that are significantly higher than at either BA or Lufthansa). This is not a weak position which relies too heavily on lower-yield transfer passengers. In our view, it is more important to fill the aircraft with a mix of connecting and point-to-point high yield passengers as this maximises revenues and asset utilisation while spreading the traffic risks. Whereas BA�s earnings look vulnerable to traffic or yield erosion on North Atlantic traffic, Air France-KLM has a more robust spread of business (with, for example, the strongest European carrier position in Japan which is now showing good growth, along with leading positions in all long-haul markets).

Long-haul passenger demand remains strong, exceeding supply, and supporting yields and load factors. Despite some aberrations in May traffic figures because of the number of holidays (traffic was nevertheless 3.9% higher in that month with the load factor flat, compared to a 2.1% traffic decline and a 1.5 point fall in the load factor for BA) long-haul demand remains strong for Air France-KLM, powered by the hub synchronisation effect (linked schedules) between Paris and Amsterdam which is driving Air France-KLM's growth, both in absolute terms and in terms of market share. Overall long-haul capacity grew at 5.6% this summer, with the leading European carriers increasing capacity by 6% and capacity from non-European competitors increasing by 4%. KLM�s transatlantic capacity is increasing at a higher rate because Northwest is raising capacity more than the average and KLM is seeking to rebalance its contribution to the existing transatlantic joint venture. Such strategic changes in capacity are likely to be seen increasingly after Open Skies in March 2008 following the joint venture with Delta, especially if Air France-KLM is successful in achieving the four-party anti-trust immunity for Air France, KLM, Delta and Northwest, for which an application to the US Department of Justice has been made.

The synchronised hub strategy works

This progressive construction of the twin hub system in Paris and Amsterdam, both of which are relatively unconstrained in terms of infrastructure capacity compared to Heathrow and Frankfurt, is paying off. Between May 2004 and December 2006, Air France-KLM increased its market share (AEA traffic) from 26.2% to 27.1% and now has critical mass in most of its main markets. In contrast, BA and Lufthansa have both lost market share.

15 Air France-KLM

Chart 2: Medium-haul, long-haul connections under two hours (summer 2007)

20,695

7,193

3,0974,110

13,020

7,070

0

5,000

10,000

15,000

20,000

25,000

Paris-CDG Amsterdam Zurich Munich Frankfurt London-Heathrow

MH

-LH

con

nect

ions

Source: Exane BNP Paribas estimates

This is because Air Fance-KLM offers more destinations and route combinations through its twin hubs. This is attractive for the large corporate accounts. BA's alternative strategy of focusing on point-to-point premium business from Heathrow produces high yields on dense long-haul routes but is highly vulnerable to new competition, such as the business class only airlines, Eos and Maxjet, and after March 2008 from new services by the large US airlines which are currently excluded from the rich Heathrow�US market (9 out of the 12 most profitable routes from Europe to the US are from Heathrow).

Network improvements drive gains

Network improvements and increasing coordination of sales and revenue management activities have contributed to sustainable improvements in the group�s market position, especially with global corporate accounts. This is expected to be given a further boost in 2008�2010 from the introduction of a common sales and marketing IT backbone (the Amadeus Altea system) which is also expected to lead to increased on-line sales and e-ticketing. This leads to a virtuous circle in terms of customer capture and retention, along with lower sales and distribution costs.

In 2006/07, traffic in Asia traffic (RPKs) was 9.9% higher, while capacity grew by 7.9%. The seat load factor rose by 1.5 points to 86.8%. In Latin America, growth was even stronger; traffic was 11.2% higher while capacity increased by 6.6% and the yield (RASK) was up 22%. Routes to Middle East/Africa saw traffic grow by 6.8%, 0.8 points higher than the growth in capacity. Even in Europe, there was a difference between growth in traffic at 6.3% and capacity at 5.2%. Traffic grew by over 6% yoy over June�August. Statistics for September showed traffic growth of 5.3% and seat load factors broadly stable at high levels with the exception of the Americas, where a capacity increase of 12.3% yoy and traffic growth of 9.2% saw a 2.4 point fall in the seat load factor.

The October traffic figures showed underlying growth of 4.5% yoy and a seat load factor maintained at the high level of 80.6%, although the reported figures showed a decline of 0.7% because of the impact of the strike (which mainly affected European traffic).

16 Air France-KLM

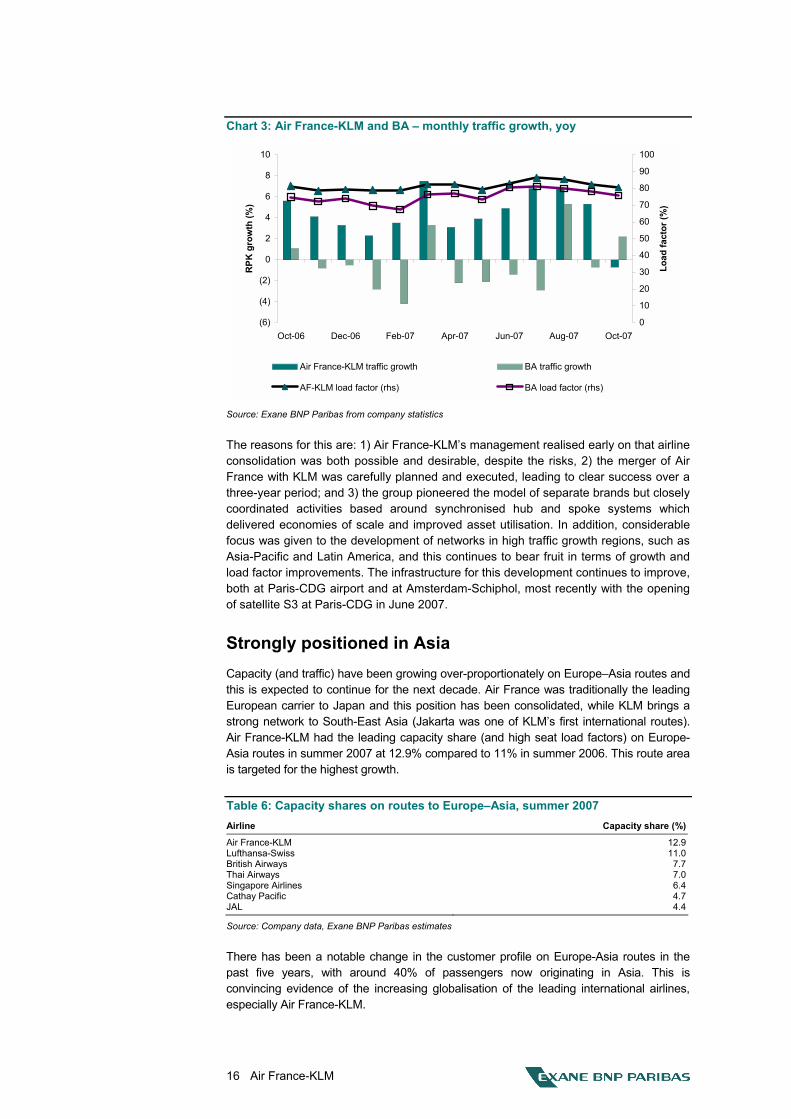

Chart 3: Air France-KLM and BA � monthly traffic growth, yoy

(6)

(4)

(2)

0

2

4

6

8

10

Oct-06 Dec-06 Feb-07 Apr-07 Jun-07 Aug-07 Oct-07

RPK

gro

wth

(%)

0

10

20

30

40

50

60

70

80

90

100

Load

fact

or (%

)

Air France-KLM traffic growth BA traffic growth

AF-KLM load factor (rhs) BA load factor (rhs)

Source: Exane BNP Paribas from company statistics

The reasons for this are: 1) Air France-KLM�s management realised early on that airline consolidation was both possible and desirable, despite the risks, 2) the merger of Air France with KLM was carefully planned and executed, leading to clear success over a three-year period; and 3) the group pioneered the model of separate brands but closely coordinated activities based around synchronised hub and spoke systems which delivered economies of scale and improved asset utilisation. In addition, considerable focus was given to the development of networks in high traffic growth regions, such as Asia-Pacific and Latin America, and this continues to bear fruit in terms of growth and load factor improvements. The infrastructure for this development continues to improve, both at Paris-CDG airport and at Amsterdam-Schiphol, most recently with the opening of satellite S3 at Paris-CDG in June 2007.

Strongly positioned in Asia Capacity (and traffic) have been growing over-proportionately on Europe�Asia routes and this is expected to continue for the next decade. Air France was traditionally the leading European carrier to Japan and this position has been consolidated, while KLM brings a strong network to South-East Asia (Jakarta was one of KLM�s first international routes). Air France-KLM had the leading capacity share (and high seat load factors) on Europe-Asia routes in summer 2007 at 12.9% compared to 11% in summer 2006. This route area is targeted for the highest growth.

Table 6: Capacity shares on routes to Europe�Asia, summer 2007 Airline Capacity share (%)

Air France-KLM 12.9Lufthansa-Swiss 11.0British Airways 7.7Thai Airways 7.0Singapore Airlines 6.4Cathay Pacific 4.7JAL 4.4

Source: Company data, Exane BNP Paribas estimates

There has been a notable change in the customer profile on Europe-Asia routes in the past five years, with around 40% of passengers now originating in Asia. This is convincing evidence of the increasing globalisation of the leading international airlines, especially Air France-KLM.

17 Air France-KLM

El Dorado in Latin America Air France-KLM�s strong expansion in Latin America following the merger appears to have been a successful strategic move, as the Latin American economies grew strongly and demand for airline services rose strongly, but financial difficulties at national airlines, such as Varig, meant that supply was restricted.

Middle East/Africa also showing good growth Development of the African market has likewise been a success for Air France-KLM, as Air France�s dominant presence in French speaking West African markets was complemented by KLM�s presence in Eastern and Southern Africa. KLM�s route network to the Middle East also boosted the group�s presence considerably in this fast-growing region.

Premium transfer growing at fastest pace The fastest growing passenger group has been premium transfer passengers, as the strength of the long-haul schedules has attracted new passengers to the network.

Air France-KLM�s short-haul passenger markets have faced strong competition from new entrants and management�s response has been to cut in-cabin costs, reduce capacity and to refocus capacity on the connecting network. There were already significant adjustments of capacity in response to the opening of the TGV route to Marseilles, Strasbourg and in the medium term Air France-KLM will itself be seeking (from the customer retention perspective) to participate in the rail market in France, possibly with a competitor to SNCF, such as Veolia, in order to ensure an efficient connection service to medium/long-haul airline flights (unlike in the US, intermodality of passenger transport systems is likely to be an important development in Europe). Ryanair has started services from Marseilles to European destinations but has already had to withdraw three routes (Marseilles to Bremen, Baden-Baden and Rome) for lack of traffic. By contrast, Transavia, France, the leisure specialist airline which operates as a joint venture between KLM�s subsidiary, Transavia, and Air France, has started well out of Paris to the first leisure destinations of Porto, Monastir and Djerba.

Chart 4: Air France-KLM�s network shows strong ability to attract premium transfer passengers

6%

10%11%

16%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

Passengers Revenues Transfer revenues Premium transferrevenues

Perc

enta

ge g

row

th

Source: Company, Exane BNP Paribas, data for FY06/07

18 Air France-KLM

Growth in airport infrastructure will improve efficiency Of all the network airlines, Air France and KLM enjoy the best hub airport infrastructure. Heathrow will have additional terminal capacity following the commissioning of Terminal 5 from March 2008 but is constrained by only having two runways. Frankfurt, Lufthansa�s main hub, similarly has adequate terminal capacity, which is being extended but only two parallel runways and a cross runway. If it is not delayed further, the earliest date for a new runway at Frankfurt is 2011. There are no runway constraints at Paris-CDG, which has four runways arranged in twin parallel systems, and Amsterdam-Schiphol, which operates five runways.

Next year, Air France will gain considerably from the expansion of infrastructure capacity at Paris-CDG airport, with incremental capacity for 19.4m passengers and a large number of additional contact stands by the end of 2008. The first phase of this expansion, a spacious new boarding terminal, Satellite S3, with capacity for 7m passengers, was opened in June 2007.

Paris-CDG airport�s four parallel runways are sufficient for at least 120m passengers, or a doubling of current capacity. Satellite S3 (�La Galérie Parisienne�) a boarding satellite for Terminal 2, was completed in June 2007, adding space for an extra 8.5m passengers. The reconstructed Terminal 2E, a refurbished CDG1 and a new terminal for Air France-KLM�s regional airline subsidiaries will be completed in 2008, adding capacity for a further 10.9m passengers (19.4m in total). These are served by a new light rail system connecting the terminals and a new automatic baggage handling system under Terminal 2. More importantly, the number of contact stands for Air France is rising dramatically and brings an A380 docking capability. This greatly improves efficiency for the airline and significantly reduces internal airport transport and passenger transfer costs.

KLM similarly enjoys unconstrained infrastructure capacity at Amsterdam-Schiphol, with its new terminal, five runways and direct road and rail links into Europe.

Long-haul growth: is the cycle stronger for longer? The infrastructure for growth is therefore available but the questions arise as to whether the cycle will be stronger for longer and therefore whether growth in demand will remain at high levels for the next few years. In our view, the key to this question is the continuing impact of emerging economies on global growth. There is a lack of long-haul capacity growth in emerging economies, which face massive investment in aviation infrastructure (aircraft and airport infrastructure) to support anticipated economic growth. In 2006/07, total long-haul passenger traffic growth was 5.2% while capacity rose by 4.2%.

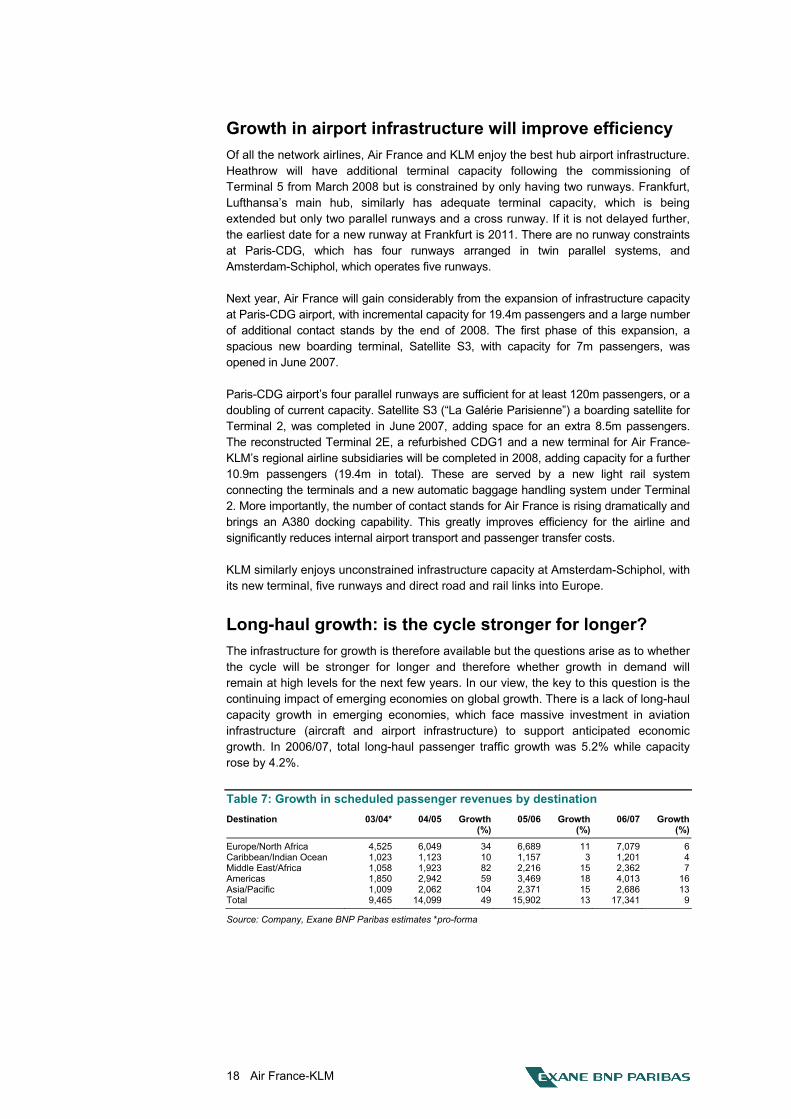

Table 7: Growth in scheduled passenger revenues by destination Destination 03/04* 04/05 Growth

(%)05/06 Growth

(%) 06/07 Growth

(%)

Europe/North Africa 4,525 6,049 34 6,689 11 7,079 6Caribbean/Indian Ocean 1,023 1,123 10 1,157 3 1,201 4Middle East/Africa 1,058 1,923 82 2,216 15 2,362 7Americas 1,850 2,942 59 3,469 18 4,013 16Asia/Pacific 1,009 2,062 104 2,371 15 2,686 13Total 9,465 14,099 49 15,902 13 17,341 9

Source: Company, Exane BNP Paribas estimates *pro-forma

19 Air France-KLM

The previous table shows the growth in revenues by destination since the merger. The figures for 2004/05, the first year of the merger, show that KLM brought to Air France a strong rise in revenues on routes to the Asia-Pacific region (+104%), Middle East/Africa (+82%) and the Americas (+59%). Given the proportionately higher long-haul business of KLM, the increase in revenues on European routes was less spectacular (+34%).

Table 8: Long-haul capacity and demand growth, 2007e�2011e

Country/region Demand growth Air France-KLM capacity growth

Europe 6.2 4.5Latin America 8.3 8.0Africa 4.8 4.5Middle East 7.7 3.5India 8.0 11.0China 12.0 14.5Japan 5.0 8.0

Source: Company, Exane BNP Paribas estimates

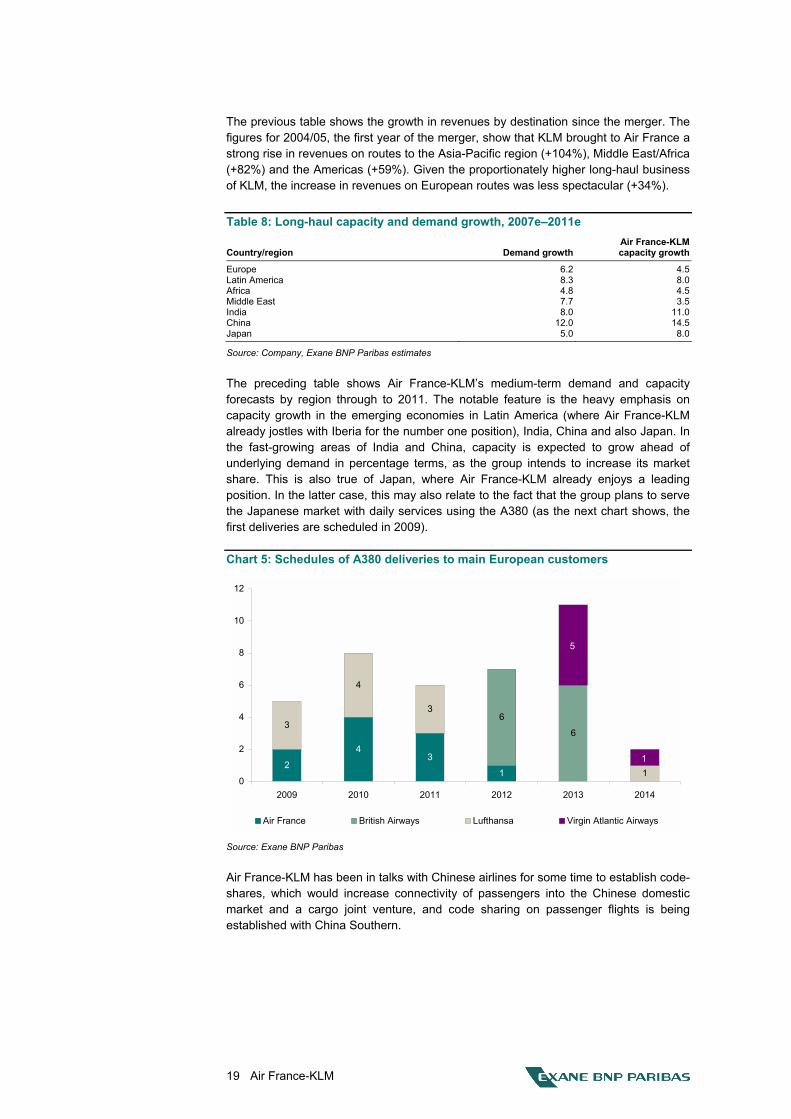

The preceding table shows Air France-KLM�s medium-term demand and capacity forecasts by region through to 2011. The notable feature is the heavy emphasis on capacity growth in the emerging economies in Latin America (where Air France-KLM already jostles with Iberia for the number one position), India, China and also Japan. In the fast-growing areas of India and China, capacity is expected to grow ahead of underlying demand in percentage terms, as the group intends to increase its market share. This is also true of Japan, where Air France-KLM already enjoys a leading position. In the latter case, this may also relate to the fact that the group plans to serve the Japanese market with daily services using the A380 (as the next chart shows, the first deliveries are scheduled in 2009).

Chart 5: Schedules of A380 deliveries to main European customers

2

43

1

6

63

4

3

1

5

1

0

2

4

6

8

10

12

2009 2010 2011 2012 2013 2014

Air France British Airways Lufthansa Virgin Atlantic Airways

Source: Exane BNP Paribas

Air France-KLM has been in talks with Chinese airlines for some time to establish code-shares, which would increase connectivity of passengers into the Chinese domestic market and a cargo joint venture, and code sharing on passenger flights is being established with China Southern.

20 Air France-KLM

Consolidation underpins asset utilisation improvements

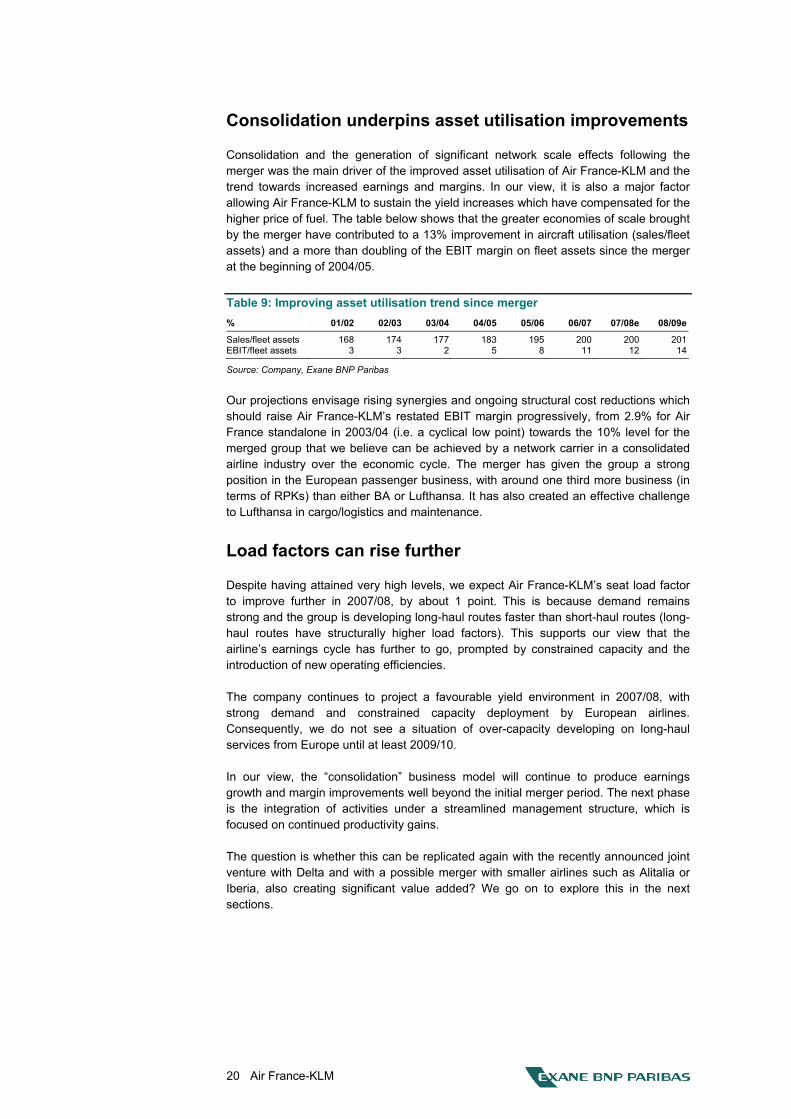

Consolidation and the generation of significant network scale effects following the merger was the main driver of the improved asset utilisation of Air France-KLM and the trend towards increased earnings and margins. In our view, it is also a major factor allowing Air France-KLM to sustain the yield increases which have compensated for the higher price of fuel. The table below shows that the greater economies of scale brought by the merger have contributed to a 13% improvement in aircraft utilisation (sales/fleet assets) and a more than doubling of the EBIT margin on fleet assets since the merger at the beginning of 2004/05.

Table 9: Improving asset utilisation trend since merger % 01/02 02/03 03/04 04/05 05/06 06/07 07/08e 08/09e

Sales/fleet assets 168 174 177 183 195 200 200 201EBIT/fleet assets 3 3 2 5 8 11 12 14

Source: Company, Exane BNP Paribas

Our projections envisage rising synergies and ongoing structural cost reductions which should raise Air France-KLM�s restated EBIT margin progressively, from 2.9% for Air France standalone in 2003/04 (i.e. a cyclical low point) towards the 10% level for the merged group that we believe can be achieved by a network carrier in a consolidated airline industry over the economic cycle. The merger has given the group a strong position in the European passenger business, with around one third more business (in terms of RPKs) than either BA or Lufthansa. It has also created an effective challenge to Lufthansa in cargo/logistics and maintenance.

Load factors can rise further

Despite having attained very high levels, we expect Air France-KLM�s seat load factor to improve further in 2007/08, by about 1 point. This is because demand remains strong and the group is developing long-haul routes faster than short-haul routes (long-haul routes have structurally higher load factors). This supports our view that the airline�s earnings cycle has further to go, prompted by constrained capacity and the introduction of new operating efficiencies.

The company continues to project a favourable yield environment in 2007/08, with strong demand and constrained capacity deployment by European airlines. Consequently, we do not see a situation of over-capacity developing on long-haul services from Europe until at least 2009/10.

In our view, the �consolidation� business model will continue to produce earnings growth and margin improvements well beyond the initial merger period. The next phase is the integration of activities under a streamlined management structure, which is focused on continued productivity gains.

The question is whether this can be replicated again with the recently announced joint venture with Delta and with a possible merger with smaller airlines such as Alitalia or Iberia, also creating significant value added? We go on to explore this in the next sections.

21 Air France-KLM

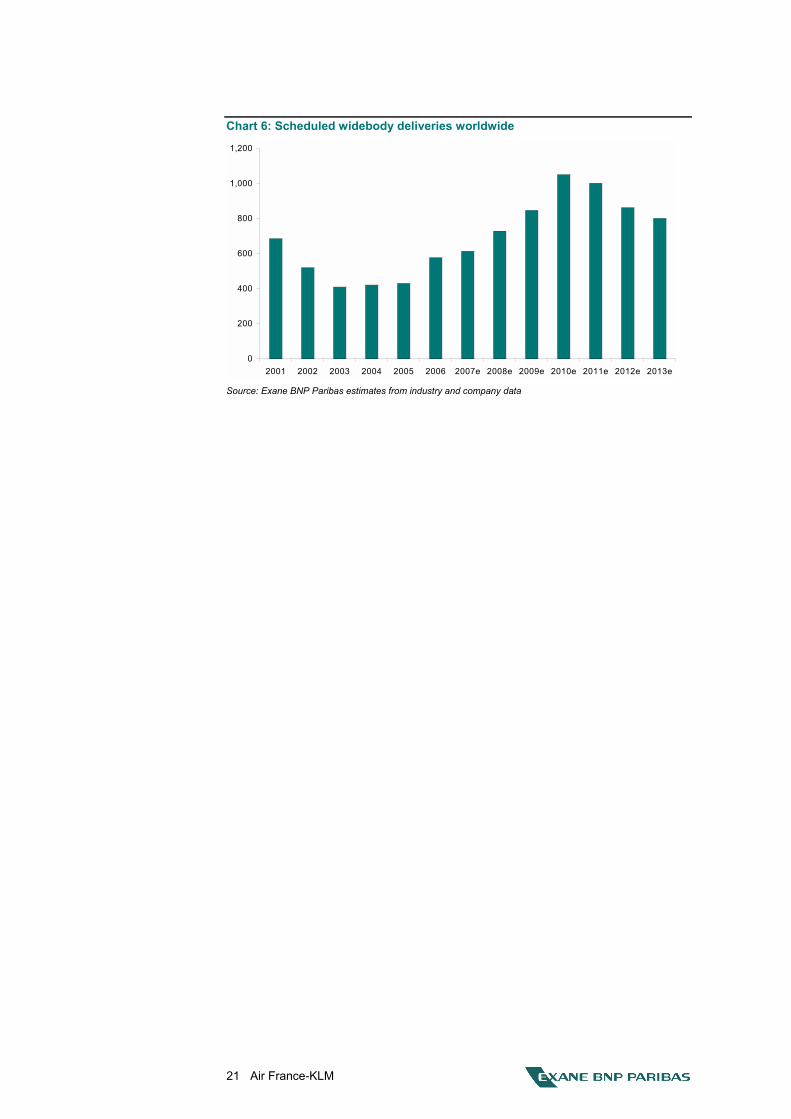

Chart 6: Scheduled widebody deliveries worldwide

0

200

400

600

800

1,000

1,200

2001 2002 2003 2004 2005 2006 2007e 2008e 2009e 2010e 2011e 2012e 2013e Source: Exane BNP Paribas estimates from industry and company data

22 Air France-KLM

Delta JV: taking advantage of Open Skies

In the global airline industry, one clear form of consolidation is through capacity-sharing joint ventures, which restrict the amount of capacity that is introduced on selected routes or �sub-systems�. In late October 2007, the Air France airline announced a major new joint venture with Delta which is initially aimed at targeting the premium yield market for business travellers from the US to London-Heathrow. Air France-KLM has applied for four-party anti-trust immunity for Air France and KLM with Delta and Northwest (and also for Alitalia). It expects to have a new joint venture structure in place with Delta by the end of 2007, followed by Northwest afterwards. This could strengthen considerably the position of SkyTeam on transatlantic routes where it currently trails BA/oneworld and Lufthansa/United Airlines. We expect this to be a major source of revenue growth, complementing the strong organic revenue growth that we expect to see on Asian and Latin American routes.

The new joint venture constitutes a positive development for Delta, which was hitherto blocked from entering the lucrative US-Heathrow market because of the restrictive Bermuda II agreement between the UK and the US. It is also positive for Air France, which has an (almost) asset-free way of developing its presence in the US�Europe transatlantic market, where it currently trails both BA and Lufthansa. It is expected that KLM will follow suit with the announcement of a joint venture with Northwest airlines on routes from the US to Heathrow, building on their existing joint venture on routes from the US to Amsterdam-Schiphol, which has been in place since 1993 and currently has structurally high margins.

It is intended that, following approval of anti-trust immunity, all four airlines will share a common four-party joint venture.

Air France/Delta announcement is a virtual merger On 17 October, Air France and Delta signed an agreement to extend their joint venture across the Atlantic. The two airlines already have anti-trust immunity on routes between the US and France, which permits them to cooperate on pricing, capacity and routes. J-C Spinetta, Air France-KLM�s President and CEO, confirmed that slots operated by Air France and KLM at Heathrow will be available to their respective alliance partners, Delta and Northwest, to operate direct flights between London and the US, probably through a series of joint ventures. It was also confirmed that 9 of 12 top point-to-point destinations to the US from Europe are from London-Heathrow.

In our view, Open Skies will lead to an increased interest in cooperation between those alliance partners which enjoy anti-trust immunity. This should also reinforce the consolidation effects on aircraft capacity levels, since closer cooperation implies joint targeting of routes, frequencies and seats on offer.

23 Air France-KLM

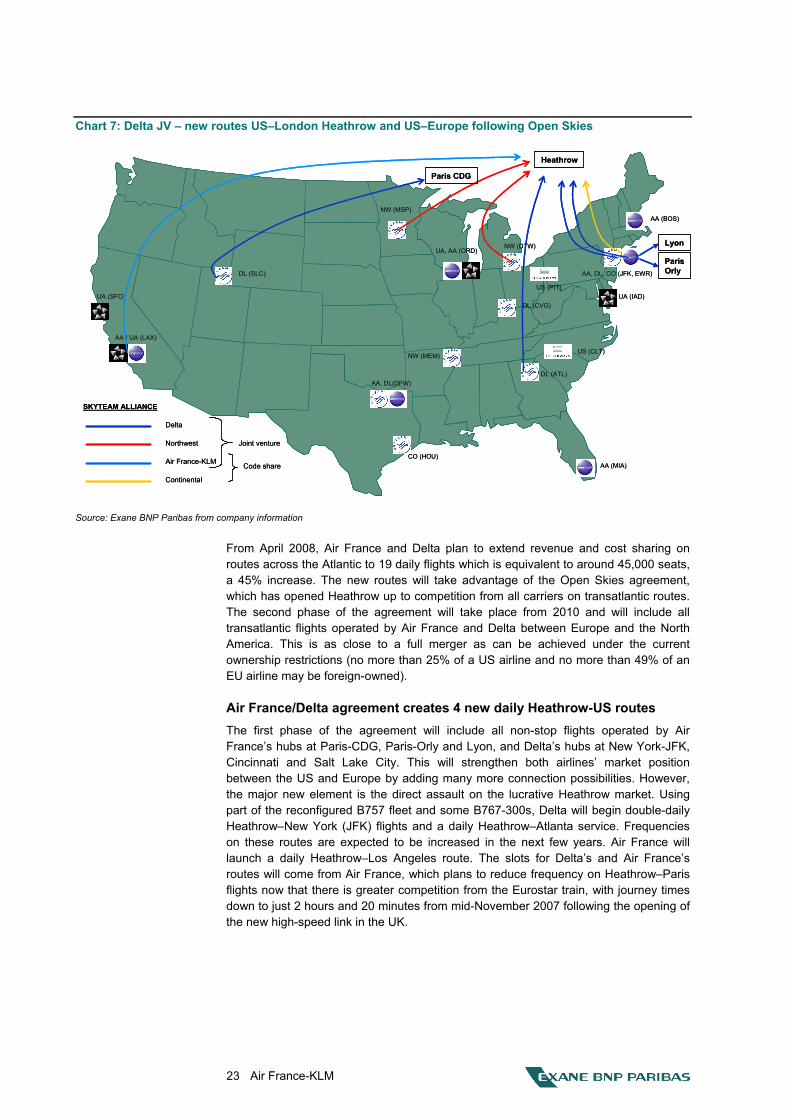

Chart 7: Delta JV � new routes US�London Heathrow and US�Europe following Open Skies

NW (MEM)

NW (DTW)

NW (MSP)

AA, DL(DFW)

CO (HOU)

AA / UA (LAX)

UA, AA (ORD)

DL (SLC)

DL (CVG)UA (SFO)

DL (ATL)

UA (IAD)

AA, DL, CO (JFK, EWR)

AA (BOS)

AA (MIA)

US (PIT)

US (CLT)

Air France-KLM

Delta

Northwest Joint venture

Continental

SKYTEAM ALLIANCE

Code share

Paris CDG

Heathrow

Lyon

Paris Orly

NW (MEM)

NW (DTW)

NW (MSP)

AA, DL(DFW)

CO (HOU)

AA / UA (LAX)

UA, AA (ORD)

DL (SLC)

DL (CVG)UA (SFO)

DL (ATL)

UA (IAD)

AA, DL, CO (JFK, EWR)

AA (BOS)

AA (MIA)

US (PIT)

US (CLT)

Air France-KLM

Delta

Northwest Joint venture

Continental

SKYTEAM ALLIANCE

Code share

Paris CDG

Heathrow

Lyon

Paris Orly

Source: Exane BNP Paribas from company information

From April 2008, Air France and Delta plan to extend revenue and cost sharing on routes across the Atlantic to 19 daily flights which is equivalent to around 45,000 seats, a 45% increase. The new routes will take advantage of the Open Skies agreement, which has opened Heathrow up to competition from all carriers on transatlantic routes. The second phase of the agreement will take place from 2010 and will include all transatlantic flights operated by Air France and Delta between Europe and the North America. This is as close to a full merger as can be achieved under the current ownership restrictions (no more than 25% of a US airline and no more than 49% of an EU airline may be foreign-owned).

Air France/Delta agreement creates 4 new daily Heathrow-US routes The first phase of the agreement will include all non-stop flights operated by Air France�s hubs at Paris-CDG, Paris-Orly and Lyon, and Delta�s hubs at New York-JFK, Cincinnati and Salt Lake City. This will strengthen both airlines� market position between the US and Europe by adding many more connection possibilities. However, the major new element is the direct assault on the lucrative Heathrow market. Using part of the reconfigured B757 fleet and some B767-300s, Delta will begin double-daily Heathrow�New York (JFK) flights and a daily Heathrow�Atlanta service. Frequencies on these routes are expected to be increased in the next few years. Air France will launch a daily Heathrow�Los Angeles route. The slots for Delta�s and Air France�s routes will come from Air France, which plans to reduce frequency on Heathrow�Paris flights now that there is greater competition from the Eurostar train, with journey times down to just 2 hours and 20 minutes from mid-November 2007 following the opening of the new high-speed link in the UK.

24 Air France-KLM

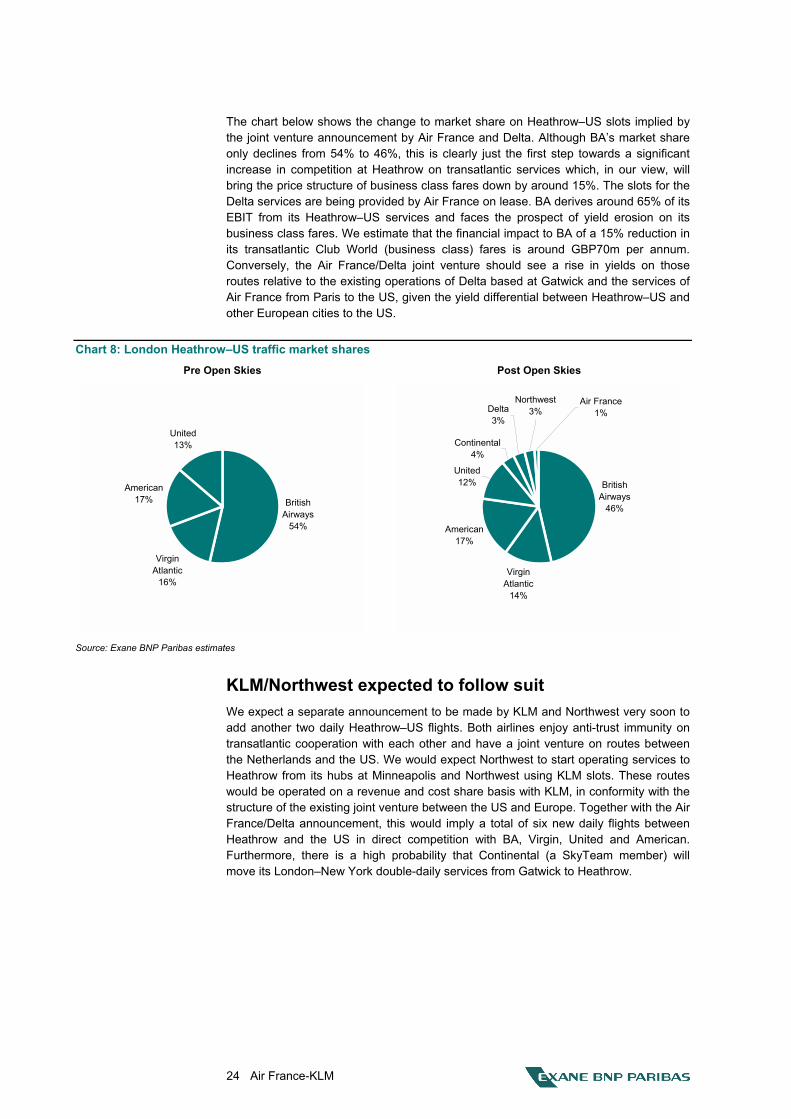

The chart below shows the change to market share on Heathrow�US slots implied by the joint venture announcement by Air France and Delta. Although BA�s market share only declines from 54% to 46%, this is clearly just the first step towards a significant increase in competition at Heathrow on transatlantic services which, in our view, will bring the price structure of business class fares down by around 15%. The slots for the Delta services are being provided by Air France on lease. BA derives around 65% of its EBIT from its Heathrow�US services and faces the prospect of yield erosion on its business class fares. We estimate that the financial impact to BA of a 15% reduction in its transatlantic Club World (business class) fares is around GBP70m per annum. Conversely, the Air France/Delta joint venture should see a rise in yields on those routes relative to the existing operations of Delta based at Gatwick and the services of Air France from Paris to the US, given the yield differential between Heathrow�US and other European cities to the US.

Chart 8: London Heathrow�US traffic market shares Pre Open Skies Post Open Skies

British Airways

54%

Virgin Atlantic

16%

American17%

United13%

British Airways

46%

Virgin Atlantic

14%

American17%

United12%

Continental4%

Delta3%

Air France1%

Northwest3%

Source: Exane BNP Paribas estimates

KLM/Northwest expected to follow suit We expect a separate announcement to be made by KLM and Northwest very soon to add another two daily Heathrow�US flights. Both airlines enjoy anti-trust immunity on transatlantic cooperation with each other and have a joint venture on routes between the Netherlands and the US. We would expect Northwest to start operating services to Heathrow from its hubs at Minneapolis and Northwest using KLM slots. These routes would be operated on a revenue and cost share basis with KLM, in conformity with the structure of the existing joint venture between the US and Europe. Together with the Air France/Delta announcement, this would imply a total of six new daily flights between Heathrow and the US in direct competition with BA, Virgin, United and American. Furthermore, there is a high probability that Continental (a SkyTeam member) will move its London�New York double-daily services from Gatwick to Heathrow.

25 Air France-KLM

Preliminary assessment of the earnings impact We expect Air France-KLM to give new information on the transatlantic joint ventures at its H2 2007/08 results conference on 22 November and subsequently as the route plans are developed. The CEO of Delta, Richard Anderson, has already indicated that the joint ventures could bring incremental pre-tax profit of USD125m�USD200m from 2011. The joint ventures are expected to operate in a manner similar the current joint venture between KLM and Northwest, namely targeting 50% capacity by each partner airline as far as possible, with revenues and costs pooled and a profit adjustment (which can be either way) at the end of the year. Our estimates shown below assume that the joint venture achieves a 6% operating margin in 2008/2009, rising to 8% in 2009/10 and 2010/2011, with traffic increasing by 6% per annum and yields stable. We believe this is conservative given that, in our view, BA makes around 65% of its profit on North Atlantic routes (i.e. on approximately 30% of its revenues), implying a margin in excess of 15% (based on its 2006/07 earnings).

Table 10: Estimated Air France-KLM/Delta JV contribution USDm 08/09e 09/10e 10/11e 11/12e

Revenues 1,500 1,590 1,685 8,000EBIT 90 127 135 640Operating profit share for AF-KLM 45 64 68 320

Source: Exane BNP Paribas estimates

If the same EBIT margin as our estimated margin for BA in 2006/07 (15%) on its North Atlantic routes were applied to the same projected revenues, we estimate that the joint venture�s EBIT would be USD225m in 2008/09, USD238m in 2009/10, USD253m in 2010/11 and USD1.2bn in 2011/12, when the perimeter of the joint venture is expanded.

The structure of transatlantic partnerships

In our view, significant revenue gains for Air France-KLM are possible through joint management of capacity on routes across the North Atlantic in cooperation with Delta and Northwest Airlines following Open Skies after the end of March 2008. Open Skies between the US and Europe does not threaten the �hub and spoke� operating model of the three leading European network airlines, but it does offer scope to build the existing airline alliances into a more valuable source of earnings. It is more ambitious than KLM/Northwest and envisages revenues of EUR1.5bn in 2008/09, rising to EUR8bn from 2010/11.

The current joint venture arrangement between KLM and Northwest relates to operations on the North Atlantic routes, the routes between the Netherlands and India and related feeder routes. It relates to all passenger and cargo traffic and the routes cover all air traffic between the US, Canada and Mexico on the one hand and Europe on the other. Each partner contributes the difference between its traffic revenues and operating expenses to the joint venture and shares on a 50:50 basis in the total contribution generated. The assets (including aircraft) used in the joint venture are managed separately by the two airlines, while the related operating expenses are part of the joint venture. Typical annual transfer amounts have varied been EUR75m and EUR150m in earnings. Revenues from the joint venture were USD2,313m in 2000/01.

26 Air France-KLM

The relationship of Air France with Delta Air Lines was originally negotiated in June 1999. Air France�s alliance with Delta, which was followed by an �Open Skies� agreement between France and the US, expanded the number of connecting opportunities for Air France in the US from nine to 110 over a three-year period, drawing potential European passengers seeking US destinations away from competing networks and leading to an increase in Air France�s overall AEA market share at the time from 14% to 17%. The relationship was strengthened further following the granting of anti-trust immunity on North Atlantic routes in January 2002 to Air France and the other European SkyTeam members (Alitalia and CSA Czech Airlines) for their alliance with Delta on North Atlantic routes. Anti-trust immunity was extended to SkyTeam members, including Korean Airlines, on Pacific routes, in June 2002. KLM, Northwest and Continental Airlines became part of the SkyTeam Alliance in September 2004.

The prospect now is of intensification of the SkyTeam connections and shared anti-trust immunity, so as to reinforce the profitable network across the Atlantic from Amsterdam and Paris and extend its scope via joint ventures for example from Heathrow.

Background to the relationship with Alitalia

A joint venture has operated between Air France and Alitalia since April 2002, with a focus on the Italy�France �bundle� of routes. It is designed to optimise operating profits from passenger traffic between France and Italy by coordinating flight destinations and frequencies as well as aircraft types and crew rosters. J-C Spinetta (Air France-KLM�s President and CEO), joined the Board of Alitalia from 2002 and was a member until the first auction process was launched in 2006. He is therefore very well aware of the value of Alitalia (or lack of value, if the correct restructuring measures are not allowed to be taken).

On 30 September 2003, Air France, KLM and Alitalia entered into a tripartite agreement listing the conditions and principles under which to conduct a three-way commercial alliance.

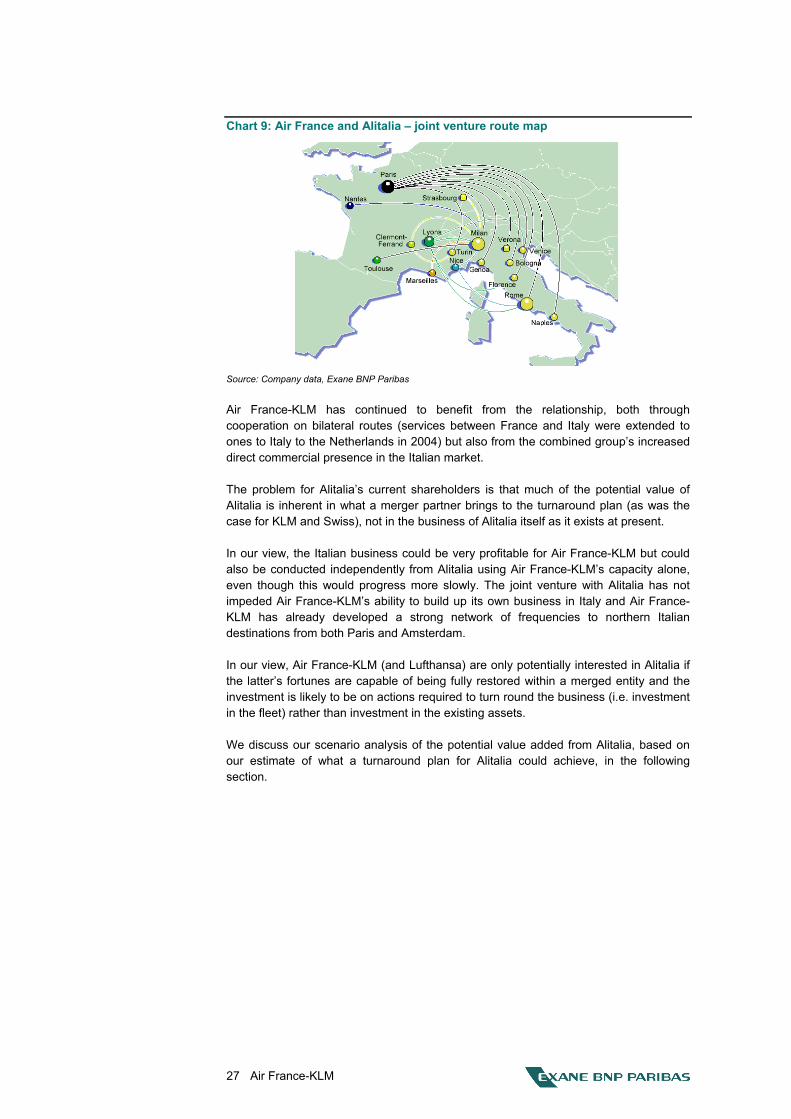

The original joint venture with Air France was cemented by the purchase of a 2% shareholding by each company in the other. It is focused on trunk routes into and out of Italy, on both premium and leisure traffic. As displayed in the chart that follows, these routes connect Alitalia�s twin hubs at Milan and Rome and other Italian cities with Paris-CDG, and also Air France�s secondary hubs at Lyon, and Marseilles. Point-to-point routes are also operated to major cities such as Toulouse, Nice and Strasbourg.

Air France and Alitalia also cooperate on long-haul business across the Paris hub, given the developing sophistication of Air France�s connecting network through Paris-CDG and Alitalia�s funding constraints and the relatively underdeveloped nature of its long-haul fleet network. The framework for sharing the economic benefits from joint ventures on specific routes was established in July 2001, with a profit-sharing formula of 60:40 in favour of Air France initially (reflecting its network contribution), reverting to 50:50 after three years.

27 Air France-KLM

Chart 9: Air France and Alitalia � joint venture route map

Source: Company data, Exane BNP Paribas

Air France-KLM has continued to benefit from the relationship, both through cooperation on bilateral routes (services between France and Italy were extended to ones to Italy to the Netherlands in 2004) but also from the combined group�s increased direct commercial presence in the Italian market.

The problem for Alitalia�s current shareholders is that much of the potential value of Alitalia is inherent in what a merger partner brings to the turnaround plan (as was the case for KLM and Swiss), not in the business of Alitalia itself as it exists at present.

In our view, the Italian business could be very profitable for Air France-KLM but could also be conducted independently from Alitalia using Air France-KLM�s capacity alone, even though this would progress more slowly. The joint venture with Alitalia has not impeded Air France-KLM�s ability to build up its own business in Italy and Air France-KLM has already developed a strong network of frequencies to northern Italian destinations from both Paris and Amsterdam.

In our view, Air France-KLM (and Lufthansa) are only potentially interested in Alitalia if the latter�s fortunes are capable of being fully restored within a merged entity and the investment is likely to be on actions required to turn round the business (i.e. investment in the fleet) rather than investment in the existing assets.

We discuss our scenario analysis of the potential value added from Alitalia, based on our estimate of what a turnaround plan for Alitalia could achieve, in the following section.

28 Air France-KLM

Airline acquisitions: risk/return trade-off

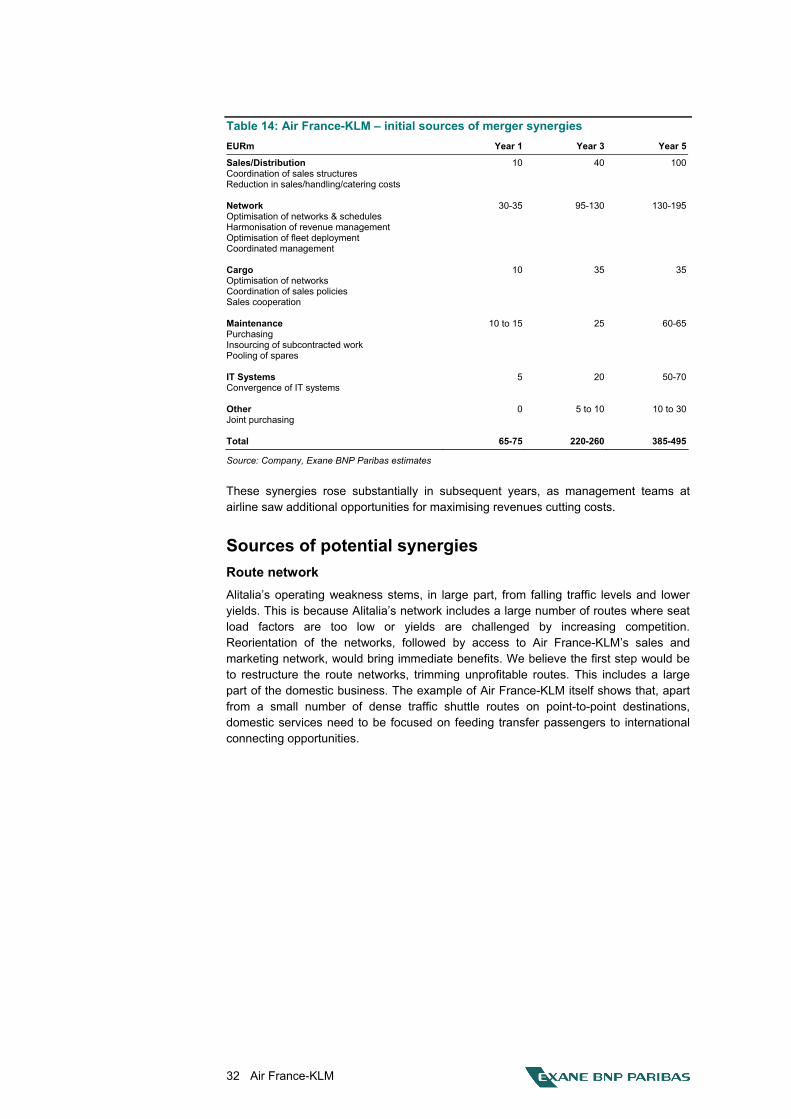

Air France-KLM has stated that it is open to new consolidation opportunities, as it is now clear from Air France�s merger with KLM and the takeover of Swiss International by Lufthansa that full synergies in Europe�s airline business can only be delivered through mergers, with immediate and substantial benefits in terms of revenue synergies and improvements in asset utilisation, followed by both revenue and cost synergies over several years following such mergers. Consolidation activity so far has shown that the scale effects and improved asset utilisation have a positive impact on average margins. In our view, the competitive environment after Open Skies will put great pressure on smaller airlines with limited networks to seek to merge with larger partners, which have bigger scale and stronger balance sheets. For Air France-KLM, the successful merger with KLM has given the group considerable integration experience and we expect this to be deployed by its participation in further consolidation.

Alitalia or Iberia, it�s a buyers� market

The most immediate consolidation targets in the European airline industry (excluding low-cost carriers) are Alitalia and Iberia, both of which have been put up for sale. We expect that Austrian Airlines and SAS will attempt to negotiate entry into one of the larger airline groups once their current restructuring programmes are at, or near, completion. There has been some concern that Air France-KLM might overpay for these assets in order to obtain market share.

In our view, there is no need for Air France-KLM to overpay for either company. Indeed, J-C Spinetta (the group�s President and CEO) has said that he would not do a deal that was not in the interests of shareholders. Moreover, he has further committed that any deal should not jeopardise the group�s ability to achieve its 2009/10 post-tax ROCE target of 8.5%. Each of the two airlines, Alitalia and Iberia, represents a different and specific business opportunity and we believe it is worth reviewing the history of engagement and the potential synergies and NPV benefits that we estimate can accrue to Air France-KLM from each consolidation opportunity.

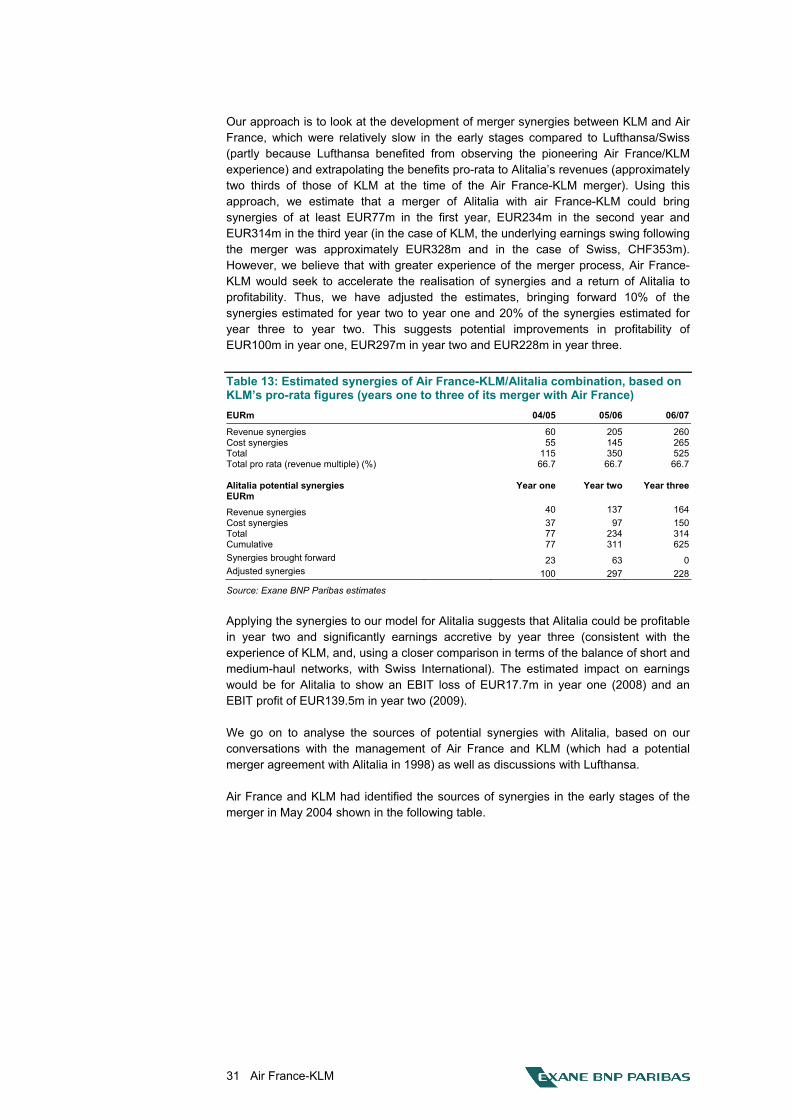

A summary of our analysis is set out in the table below. This shows that the potential NPV benefits, based on our assumptions of the potential acquisition price, would be greater for a merger of Air France-KLM with Alitalia than for a merger of Air France-KLM with Iberia. Closer cooperation on a multilateral basis (rather than the present, separate bilateral relationships between Air France and Delta and KLM and Northwest) is a �win-win� situation which we estimate could potentially generate synergy benefits of EUR625m for a merged Air France-KLM/Alitalia entity.

Table 11: Potential merger with Iberia or Alitalia � estimated merger synergies EURm Year one Year two Year three Total

Estimated Air France-KLM/Iberia synergies 92 188 120 400Discount applied at 7.5% 0.86 0.80 0.75 Discounted synergies 79 150 90 319Value per share to Air France-KLM (EUR) 1.06 Estimated Air France-KLM/Alitalia synergies 100 297 228 625Discount applied at 7.5% 0.86 0.80 0.75 Discounted synergies 86 238 171 495Value per share to Air France-KLM (EUR) 1.65

Source: Exane BNP Paribas estimates

This is not included in our valuation and target price but shows the potential upside to the share price if consolidation moves can be managed successfully.

29 Air France-KLM

Alitalia: currently a chronically sick company Investors� reaction to speculation about Air France-KLM�s possible interest in acquiring Alitalia has frequently been negative, leading to short-term selling pressure on the shares. In our view, this is misguided since it is apparent that Air France-KLM can negotiate from a position of considerable strength and will not do a deal unless the risks are minimised and the group has a significant chance of success. We recall the negative sentiment at the time the KLM deal was negotiated in 2003 (when KLM was loss-making), when Air France�s competitors commented that they had taken on an unacceptable level of risk. Clearly, the risks are greater for a merger with Alitalia than for one with Iberia, given the fact that Alitalia has accumulated losses, partly through mismanagement and political interference. However, we would expect this to be reflected in the respective takeout valuations of the two airlines. In our view, Iberia is holding out for a valuation that is excessive given the poor outlook for its domestic and European passenger business as it faces steeper competition (already reflected in yield declines). For Alitalia, the situation is different, since we believe the value of the company lies only in its turnaround potential.

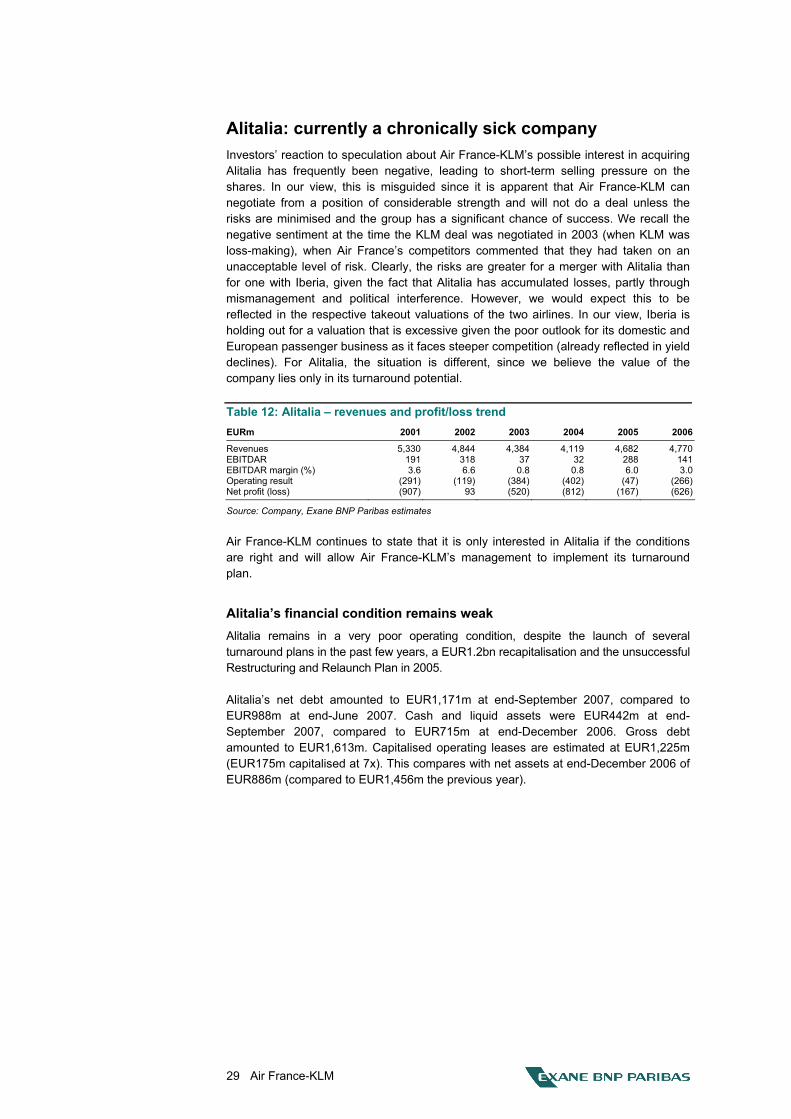

Table 12: Alitalia � revenues and profit/loss trend EURm 2001 2002 2003 2004 2005 2006

Revenues 5,330 4,844 4,384 4,119 4,682 4,770EBITDAR 191 318 37 32 288 141EBITDAR margin (%) 3.6 6.6 0.8 0.8 6.0 3.0Operating result (291) (119) (384) (402) (47) (266)Net profit (loss) (907) 93 (520) (812) (167) (626)

Source: Company, Exane BNP Paribas estimates

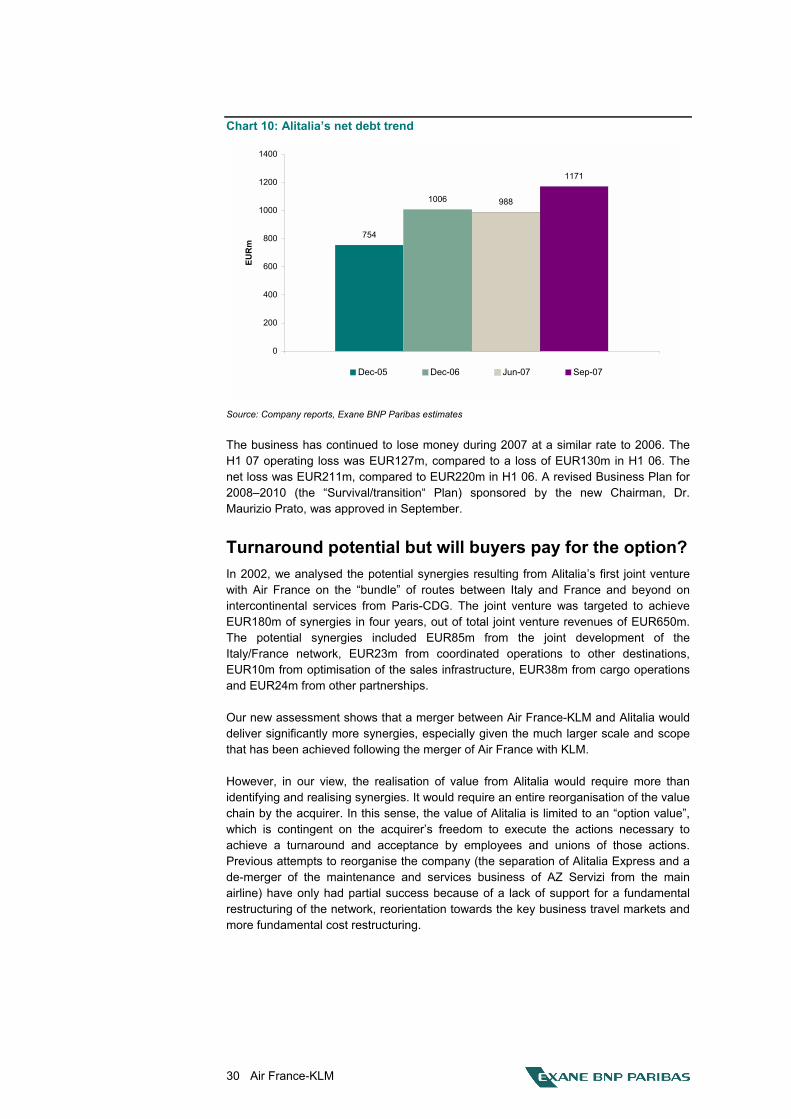

Air France-KLM continues to state that it is only interested in Alitalia if the conditions are right and will allow Air France-KLM�s management to implement its turnaround plan.