airline cost management group (acmg) report - iata - · pdf file ·...

TRANSCRIPT

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

1

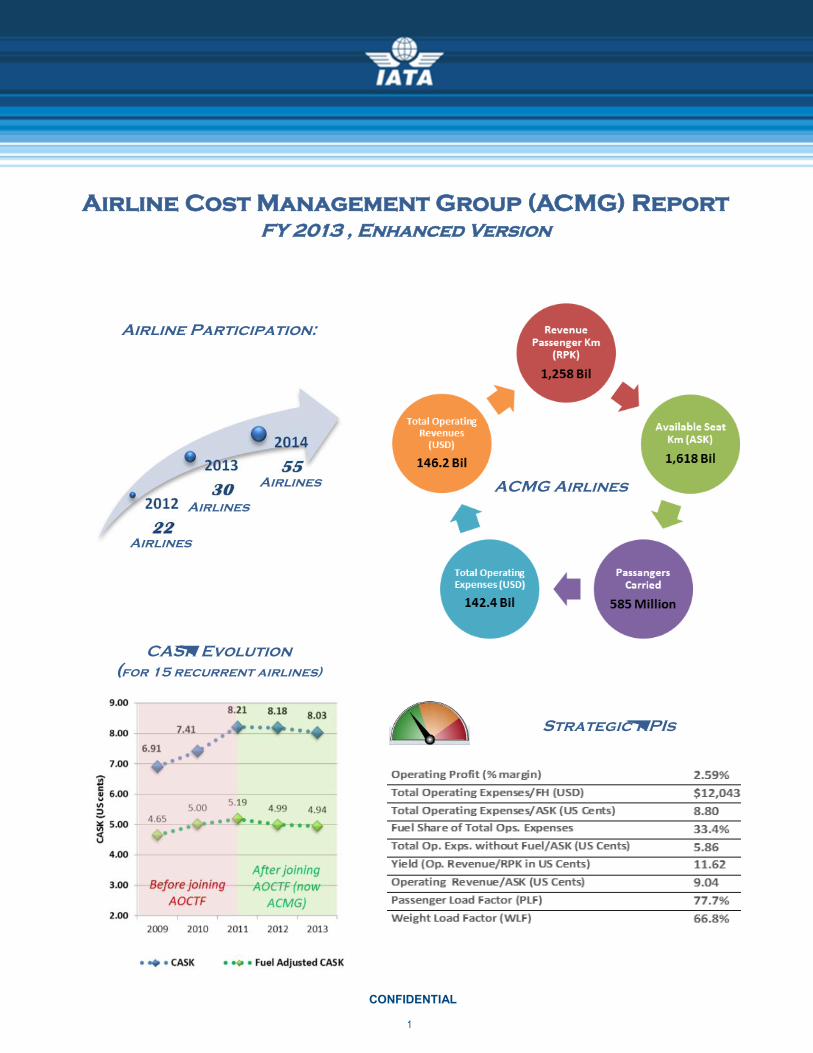

Airline Participation:

Airline Cost Management Group (ACMG) Report

FY 2013 , Enhanced Version

CONFIDENTIAL

ACMG Airlines

Strategic KPIs

CASK Evolution

(for 15 recurrent airlines)

Airlines

Airlines

Airlines

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

2

Table of Contents

CONFIDENTIAL

Executive Summary ......................................................................................................................................... 3

Definitions & Acronyms .................................................................................................................................... 4

Data & Analysis Methodology ................................................................................................................................. 4

1. Introduction....................................................................................................................................... 5

Airline Industry Landscape 2013 .............................................................................. 6

2. Overview of the ACMG Airlines ....................................................................................................... 7

3. Airline Cost Structure ..................................................................................................................... 14

4. Strategic Key Performance Indicators .......................................................................................... 16

Financial Performance .................................................................................................. 17

Special focus on impact of currency exchange fluctuations ........................... 19

Yearly Trends Analysis ................................................................................................. 20

5. Operational Key Performance Indicators ..................................................................................... 22

Fuel Cost and Efficiency .............................................................................................. 22

Special focus on impact of fuel hedging .......................................................... 26

Employment Cost Structure ......................................................................................... 27

Staff Productivity .......................................................................................................... 30

6. Aircraft Type Analysis .................................................................................................................... 32

7. Detailed Analysis of B737NG and A320 Family ........................................................................... 35

B737NG .......................................................................................................................... 35

A320 Family ................................................................................................................... 37

8. Specialized ACMG Report .............................................................................................................. 40

ACMG Steering Committee .................................................................................................................................. 41

ACMG Developments ........................................................................................................................................... 42

Disclaimer

This study is to inspire discussions around the cost drivers and cost elements related to airline/aircraft operations. It is intended to provide high level

benchmarks that individual airlines could analyze to achieve efficiencies and cost savings.

This study is not meant to derive direct cost comparisons. Every airline operates in a unique environment not only in terms of geographic location, net-

work schedule, and fleet types. Elements such as aircraft age, fleet size, proximity to major OEMs, currency exchange rates, and many other parameters

play a very significant role, making direct comparisons unreal. Cost Benchmark is not a science and no existing normalization is available that allows any

form of direct comparisons. In addition, our sample includes airlines of different size, A/C size, and operational profile.

This report, including the collection of data, and publication of the results, complies strictly with all relevant competition laws. It is exclusively available to

the airlines which participated in the data collection. Any use by third parties must first be cleared with IATA.

Despite our efforts to provide accurate and up-to-date information, IATA declines any responsibility for inaccurate, incomplete, or outdated information

that may be posted herein, and expressly disclaims liability for errors or omissions in its contents. IATA disclaims all warranties of any kind, either ex-

pressed or implied, including, but not limited to, implied warranties of satisfactory quality, fitness for a particular purpose, or non-infringement. IATA shall

not be liable for any loss which may arise from the use of the information contained in this presentation.

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

3

This publication builds upon the FY2012 Report which has already

been tailored to improve the value to ACMG (formerly AOCTF)

member airlines with new segments on airline staff and financial

performance. FY2013 report clearly defines Strategic and

Operational Key Performance Indicators (KPIs) and adds additional

bits and pieces, largely an influence of diligent ACMG Steering

Committee (SC).

Before diving into the contents, why the name change?

In order to better reflect the mission and objectives of IATA’s cost

management initiative, in the past several years known as Airline

Operational Cost Task Force (AOCTF), the name has been changed

to Airline Cost Management Group (ACMG) and the terms of

reference expanded.

Amidst the biggest yearly membership growth so far (from 30 to

55 airlines) our SC decided to take a broader look on the airline

costs and add even more value to participating airlines.

The report examines airline costs for 2013. More precisely, it

consolidates and analyzes ACMG airlines’ operational data, cost

structures, and unit costs.

A total of 55 airlines from all major regions with 585 million

passengers carried submitted data for 2013. One third of them

rank among Top 50 airlines by financial results! (IATA WATS 2013).

The statistical snapshot shows the ACMG member airlines now

represent more than 20% of the industry, offering an invaluable

insight into the real data and operations.

ACMG airlines operated 3,730 aircraft, including 47% Boeing/

McDonnell-Douglas, 35% Airbus, 8% Bombardier, and 4% Embraer

aircraft. They mostly favored narrowbodies (NB), and new and

more fuel efficient aircraft. NBs represented approx. 58%,

widebodies 24%, while regional jets and turboprops held 9% and

6% market share, respectively. The average age of ACMG fleet

was 9.88 years. Majority of the airlines were essentially without

cargo traffic, however those with a significant cargo activity were

generally larger, representing 40% of total ATK and 37% of total

ASK.

This year the analysis was structured around Strategic KPIs,

usually of much interest to senior level management, comprising

key statistical and financial figures, and Operational Key

Performance Indicators examining the areas of fuel cost and

efficiency, staff productivity, and employment costs.

Relevant benchmarking is provided in all those areas. Whereas

this Report focuses on a group as a whole, specialized reports,

either focusing on a region, similar fleet size, or similar stage

length, will be available upon request. Please check page 41 for

more information on this newest and utmost valuable feature.

Again, we “rewarded” the most dedicated ACMG members with

yearly trends analysis; a priceless insight into real savings of

devoted ACMG members.

It shows their unit costs have been decreasing consistently ever

since they joined ACMG* (formerly AOCTF). Consequently millions

of dollars have been saved.

Another interesting finding shows that the low cost carriers are

not necessary the profitable carriers as the “revenue size

indicated against RASK and CASK chart” illustrates there is still

profitability in the higher RASK levels. The ACMG airlines** are

profitable as a whole; with an overall average operating margin of

2.6%. However, 24 airlines in the group still incurred losses.

Passenger volumes continued to increase steadily, while cargo

demand has rebounded throughout 2013, which resulted in

encouraging RPK and RTK increases. ACMG carriers were

successfully keeping passenger and freight capacity growth

slightly slower than expansion in demand which led passenger

load factor to a record high of 77.7% (and weight load factor to

66.8%).

The ACMG fleet analysis showed that B737NG and A320 family

were two most popular aircraft families representing 26.1% and

22.8% of ACMG active fleet count, respectively.

Last but not least, ACMG delivered the 2nd Airline Cost

Conference last month, featuring many prominent speakers, and

received excellent feedback from the airline participants.

Executive Summary

CONFIDENTIAL

* The first Report of the revitalized AOCTF was covering years 2009/10/11 together whereas every subsequent Report is covering only one year at a time

** 52 airlines provided validated revenue and expenditure data

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

4

DEFINITIONS & ACRONYMS

ACMG

The Airline Cost Management Group

(ACMG) collects operational data such as

traffic and capacity and high-level financial

data from Member airlines.

ACMG Airlines

These are the air carriers that participate in

the IATA ACMG annual survey questionnaire

on Airline Costs. The resulting analysis is

shared among the participants; identity of

airlines remains confidential.

AC = Aircraft

ASK = Available Seat Km

ATK = Available Tonne Km

CASK = Cost per Available Seat Km

FC = Flight Cycle

FH = Flight Hour

FTE = Full Time Equivalent

NB: Narrow-body aircraft with more than 100

seats

Passenger Load Factor (PLF) = RPK / ASK

RJ: Regional-jets up to 100 seats

RPK = Revenue Passenger Kms

RTK = Revenue Tonne Km

TP: Turbo-props

Unit Cost Before Int. (¢) = Ops Exp. / ATK

WB: Wide-body aircraft with more than one

aisle or equivalent freighter

Weight Load Factor (WLF) = RTK / ATK

DATA & ANALYSIS Methodology

ACMG gathers operational cost data from airlines worldwide. The

data is recorded and coded. The report uses data as reported by

airlines. In certain cases, airlines are contacted to clarify issues with data con-

sistency. All the cost data presented in this publication are is US dollars.

In 2013 reporting, 55 Airlines participated, majority of whom submitted complete

data in all categories.

Identified Critical Parameters

These are the parameters affecting airline operational cost:

Fuel Cost

Fleet Composition & Size

Commonality between Airframes, Engines & Systems

Aircraft usage in terms of Flight Hours, Flight Cycles, Stage Length, Daily Utilization and Age

Material & Labor Costs

Outsourcing Costs

Currency exchange fluctuations

Geographical location (end-of-hemisphere vs mid-hemisphere carriers)

Metrics for Analysis

To measure the effect of the Identified Cost Drivers, the following steps were tak-

en:

Grouping aircraft into Categories (WB, NB, RJ, and TP)

Grouping aircraft into Families (e.g. A320 Family, B737 NG, etc)

Grouping cost into Cost Elements (Flight Operations, Maintenance & Over-haul, Ground Operations, System Operations)

Measuring Operations and Age: Fleet Size, Flight Hours, Flight Cycles, and Fleet Age

Defining Strategic and Operational Key Performance Indicators (KPI)

Measuring Unit Costs: $/ASK, $/ATK, $/FH, $/Cycle, $/AC

Measuring Load Factors; PLF and WLF

55 airline members in 2013

Representing 20% of the industry*

* Representing over 20% of both the world spend and

the number of revenue passenger kms (RPK)

From AOCTF to ACMG

In order to better reflect the mission and objectives of IATA’s cost management initiative, in the past several years known as Airline Operational Cost Task Force (AOCTF), the name has been changed to Airline Cost Management Group (ACMG) and the terms of reference expanded.

Amidst the biggest yearly membership growth so far (from 30 to 55 airlines) our Steering Committee decided to take a broader look on the airline costs and add even more value to participating airlines.

The Airline Cost Management Group strives to further increase memberships, provide annual benchmarking reports on strategic and operational KPIs in cost management area, and organize yearly Airline Cost Conference gathering top industry experts.

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

5

1. INTRODUCTION

This publication builds upon the FY2012 Report which has already been tailored to improve the value to ACMG member airlines with

new segments on airline staff and financial performance. FY2013 report clearly defines Strategic and Operational Key Performance

Indicators (KPIs) and adds additional bits and pieces, largely an influence of recently formed ACMG Steering Committee (SC).

Keeping SC’s suggestions in mind the ACMG team, holding expertise in operational costs area, analyzed thoroughly the data sub-

mitted by 55 airlines.

This Enhanced version of the ACMG Report is following a very successful Airline Cost Conference in Geneva, where many partici-

pating airlines gathered to discuss the benchmarking results (on an industry-wide basis as individual data is confidential) and latest

trends in cost management area. Their feedback as well as Special focus on impact of Fuel Hedging and Exchange rates fluctua-

tions are included.

The report examines airline costs for 2013. More precisely, it consolidates and analyzes ACMG airlines’ operational data, cost struc-

tures, and unit costs.

It starts with an overview of the participating airlines and continues with an insight into operational cost structure.

Then it focuses on two major groups of KPIs; Strategic Key Performance Indicators and Operational Key Performance Indicators.

Strategic KPIs, usually of much interest to senior level management, comprise key statistical and financial figures. Benchmarking on

financial performance is also provided before the section ends with yearly trends analysis for many recurrent airlines; a priceless

insight into real savings of devoted ACMG members.

Section 5 examines main areas of Operational Key Performance Indicators; namely fuel cost and efficiency, staff productivity, and

employment costs.

In the last part, the report looks into Top 12 reported aircraft types and provides operational and cost data for each type. At the end,

the two most popular aircraft families were selected (A320 and B737NG) and analyzed in greater detail, offering valuable bench-

marking on its use by different airlines.

One should carefully look into the results of our analysis as main findings are highlighted in hopes to aid towards more efficient cost

management. Tackling airline costs in a prudent manner should consequently improve airlines’ bottom lines, the area where air line

industry has been struggling.

About Airline Cost Management Group (ACMG)

IATA is leading an initiative to develop and expand the ACMG (formerly known as the AOCTF) - a group of airlines focusing on

matters concerning airline costs and measures to optimize them. ACMG’s main task is to undertake annual collections of detailed

airline cost data for major cost areas, including flight, maintenance, ground, and system, broken down by aircraft type when applica-

ble. As the final delivery of ACMG data collection, this annual Report provides ACMG member airlines access to a key source of

data, unavailable elsewhere, that can be used to benchmark carriers against their peers at a global level.

Throughout past few years the number of ACMG member airlines increased significantly, ensuring greater data diversity and sup-porting more accurate or representative benchmark information. Last year, 30 ACMG airlines reported $87.4B expenditures, which represented more than 13% of world spend and this year record high 55 ACMG airlines reported $139.7B expenditures, which represents more than 20% of world spend! One third of them rank among Top 50 airlines by financial results! (IATA WATS 2013)

The recent successes of ACMG are undoubtedly related to the formation of its Steering Committee, which has been excellently

operating under the guidance of Chairman Richard W. Creagh (UIA). Nevertheless, he concluded his 2-year mandate during the

Airline Cost Conference and was pleased to pass the torch to his Vice-Chairman Josua du Plessis (SAA).

Whereas ACMG is a unique opportunity for airlines to exchange cost related industry experience, relevant trend information, new

developments, and best practices, participating in the ACMG Steering Committee is an additional opportunity to network with cost

management counterparts from all over the world.

Last but not least, IATA is fully aware of airline concerns regarding the confidentiality of such proprietary and competitive infor-

mation. Maintaining the confidentiality of all data is guaranteed. All of the data submitted to IATA is de-identified (each airline has

been arbitrarily attributed a two-letter code), and only published as industry or airline group aggregate information. Correspondingly,

the report is exclusively available to the airlines which participated in the data collection.

Notes:

Airline codes used in this report were carefully created to hide the identity of the participating airlines.

Unless otherwise specified or illustrated all 55 airlines are included in the analysis. When the number of included airlines is clearly seen from the chart, no addition-

al explanation follows. When any ratio was calculated, only the data that include all the involved items was used; consequently the number of airlines varies.

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

6

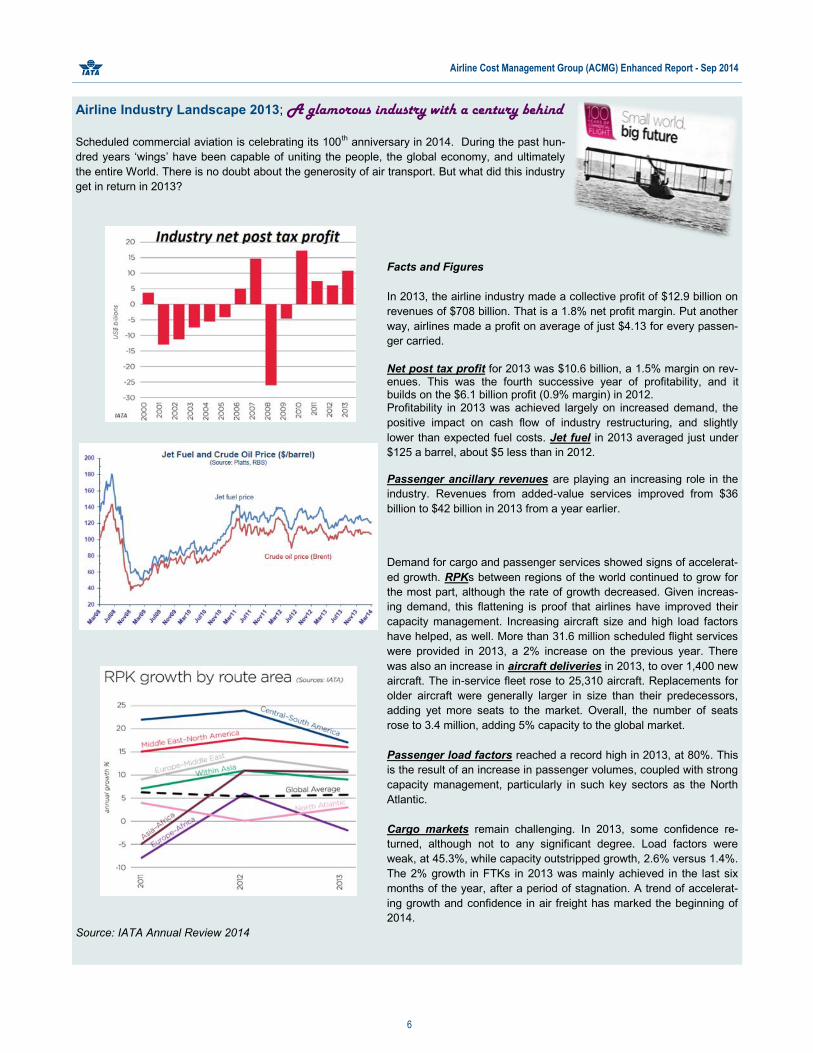

Airline Industry Landscape 2013; A glamorous industry with a century behind

Scheduled commercial aviation is celebrating its 100th anniversary in 2014. During the past hun-

dred years ‘wings’ have been capable of uniting the people, the global economy, and ultimately

the entire World. There is no doubt about the generosity of air transport. But what did this industry

get in return in 2013?

Facts and Figures

In 2013, the airline industry made a collective profit of $12.9 billion on

revenues of $708 billion. That is a 1.8% net profit margin. Put another

way, airlines made a profit on average of just $4.13 for every passen-

ger carried.

Net post tax profit for 2013 was $10.6 billion, a 1.5% margin on rev-enues. This was the fourth successive year of profitability, and it builds on the $6.1 billion profit (0.9% margin) in 2012. Profitability in 2013 was achieved largely on increased demand, the

positive impact on cash flow of industry restructuring, and slightly

lower than expected fuel costs. Jet fuel in 2013 averaged just under

$125 a barrel, about $5 less than in 2012.

Passenger ancillary revenues are playing an increasing role in the

industry. Revenues from added-value services improved from $36

billion to $42 billion in 2013 from a year earlier.

Demand for cargo and passenger services showed signs of accelerat-

ed growth. RPKs between regions of the world continued to grow for

the most part, although the rate of growth decreased. Given increas-

ing demand, this flattening is proof that airlines have improved their

capacity management. Increasing aircraft size and high load factors

have helped, as well. More than 31.6 million scheduled flight services

were provided in 2013, a 2% increase on the previous year. There

was also an increase in aircraft deliveries in 2013, to over 1,400 new

aircraft. The in-service fleet rose to 25,310 aircraft. Replacements for

older aircraft were generally larger in size than their predecessors,

adding yet more seats to the market. Overall, the number of seats

rose to 3.4 million, adding 5% capacity to the global market.

Passenger load factors reached a record high in 2013, at 80%. This

is the result of an increase in passenger volumes, coupled with strong

capacity management, particularly in such key sectors as the North

Atlantic.

Cargo markets remain challenging. In 2013, some confidence re-

turned, although not to any significant degree. Load factors were

weak, at 45.3%, while capacity outstripped growth, 2.6% versus 1.4%.

The 2% growth in FTKs in 2013 was mainly achieved in the last six

months of the year, after a period of stagnation. A trend of accelerat-

ing growth and confidence in air freight has marked the beginning of

2014.

Source: IATA Annual Review 2014

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

7

2.1. Fleet Counts

Below are the aircraft count snapshots based on all 55 airlines. On the following pages one can obtain more information about the

fleet composition and size, as well as its age.

2. OVERVIEW of the ACMG AIRLINES

A total of 55 airlines from all major regions with 585 million passengers carried submitted data for 2013, which is a significant in-crease from the year before. One third of them rank among Top 50 airlines by financial results! (IATA WATS 2013)

Although participation is confidential, we can reveal that Star Alliance is heavily represented in this study with more than half of its member airlines reporting their data to ACMG.

Consequently, since so many airlines are new in ACMG, our analysis is largely focused on year 2013.

Nevertheless, 15 dedicated airlines consistently submitting their data over past many years were “rewarded” with the trends analysis

covering years 2009/10/11/12/13. As an incentive to airlines to consistently provide data we also performed trends analysis covering

years 2012 and 2013 with 23 recurrent airlines included.

Last but not least, although most airlines have submitted complete data, in particular cases, airlines which have not provided com-

plete data in relevant category were excluded from the sample used for that particular category analysis.

Fully available only to the Airline Cost Man-

agement Group (ACMG) member airlines.

Please contact us on [email protected] to

find out how you can get involved free of

charge!

Fully available only to the Airline Cost Man-

agement Group (ACMG) member airlines.

Please contact us on [email protected] to

find out how you can get involved free of

charge!

Fully available only to the Airline Cost Man-

agement Group (ACMG) member airlines.

Please contact us on [email protected] to

find out how you can get involved free of

charge!

Fully available only to the Airline Cost Man-

agement Group (ACMG) member airlines.

Please contact us on [email protected] to

find out how you can get involved free of

charge!

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

8

Parked aircraft represented roughly 2.5% of total fleet. Although not clearly seen from the diagrams, the introduction of new and

more fuel efficient aircraft while retiring old fleets continued in 2013. The efficiency implications of modernizing the fleets are pre-

sented throughout this Report. The financial implications are most clearly visible in Section 4.2 - Yearly Trends Analysis.

Top 12 active aircraft types accounted for 90% of the total active fleet. They are thoroughly analyzed in Section 7 - Aircraft Type

Analysis, with the exception of B717, which was operated by only one reporting airline. Consequently, we included A380 in the

abovementioned analysis.

Participating Airlines Fleet Size Fleet ≤ 10 10 < Fleet ≤ 30 30 < Fleet ≤ 100 Fleet > 100 Total

Europe 7 10 7 3 27

Americas 1 1 3 5

Asia Pacific 3 2 1 5 11

Middle East and North Africa 2 4 1 7

Africa 2 3 5

Total 12 15 16 12 55

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

9

Average Fleet Age

Average ACMG Airline: Overall average as one group of reporting airlines

Fu

lly a

vaila

ble

only

to the A

irlin

e C

ost M

anagem

ent G

roup (

AC

MG

) m

em

ber

airlin

es. P

lease c

onta

ct us o

n A

CM

G@

iata

.org

to fin

d o

ut

how

you c

an g

et

involv

ed f

ree o

f charg

e!

Fu

lly a

vaila

ble

only

to the A

irlin

e C

ost M

anagem

ent G

roup (

AC

MG

) m

em

ber

airlin

es. P

lease c

onta

ct us o

n A

CM

G@

iata

.org

to fin

d o

ut

how

you c

an g

et

involv

ed f

ree o

f charg

e!

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

10

2.2. Load Factors

Fu

lly a

vaila

ble

only

to the A

irlin

e C

ost M

anagem

ent G

roup (

AC

MG

) m

em

ber

airlin

es. P

lease c

onta

ct us o

n A

CM

G@

iata

.org

to fin

d o

ut

how

you c

an g

et

involv

ed f

ree o

f charg

e!

Fu

lly a

vaila

ble

only

to the A

irlin

e C

ost M

anagem

ent G

roup (

AC

MG

) m

em

ber

airlin

es. P

lease c

onta

ct us o

n A

CM

G@

iata

.org

to fin

d o

ut

how

you c

an g

et

involv

ed f

ree o

f charg

e!

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

11

2.3. Average Stage Length

The below diagram is a clear indicator of the diversity of participating airlines. Whereas this Report focuses on a group as a whole,

specialized reports, either focusing on a region, similar fleet size, or similar stage length, will be available upon request. Please

check the last page for more information on this newest and utmost valuable feature.

Fu

lly a

vaila

ble

only

to the A

irlin

e C

ost M

anagem

ent G

roup (

AC

MG

) m

em

ber

airlin

es. P

lease c

onta

ct us o

n A

CM

G@

iata

.org

to fin

d o

ut

how

you c

an g

et

involv

ed f

ree o

f charg

e!

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

12

2.4. Cargo vs Pax Operators

In order to characterize the nature of airlines’ main operations (Cargo vs Pax airlines), a cluster analysis approach based on RTK-

Freight/RTK parameter has been used.

The airlines were clustered into three classes which have been identified by Lorenzo Castelli, Walter Ukovich in their study Charac-

terizing cargo airlines in Europe: a cluster analysis approach.

Class 1 includes airlines essentially without cargo traffic, class 2 carriers devoted to passenger traffic, but a significant cargo activity,

and class 3 airlines mostly devoted to cargo traffic.

It clearly shows the majority of the ACMG airlines are devoted to passenger operations, thus ASK and RPK unit measures are very

appropriate when comparing reporting airlines. Nevertheless, as there are also some large airlines partially devoted to cargo activity,

one might look into ATK and RTK unit measures for a thorough comparison among the reporting airlines. The reason is that passen-

gers are included into tonne kilometers units through their average weight (normally 90-100kg per pax) whereas cargo is not includ-

ed into passenger kilometers units.

IndexClass 1 - Airlines essentially

without cargo traffic

Class 2- Carriers devoted to passenger

traffic, but a significant cargo activity

Class 3 - Airlines mostly

devoted to cargo traffic

RTK-Freight/RTK ≤ 0,155 more than 0,155 and less than 0,578 > 0,578

Class 2- Carriers devoted to passenger

traffic, but a significant cargo activity

Class 3 - Airlines mostly

devoted to cargo traffic

EE GG CM DD

FA GZ PP

IA MC ID

JJ 3T N2

LL QQ CB

MB RR JS

RP KK MM

SS AS BL

UL TT 9B

Z1 KV JR

Z5 3F 8T

HH JU 77

NN CC TH

2K TX TF

GC FF WW

X6 EY RE

KT U2

JA BB

C3 AG

16 airlines representing 1 airline representing

40% of total ATK 7% of total ATK

37% of total ASK non-significant ASK

Class 1 - Airlines essentially without cargo traffic

38 airlines representing

53% of total ATK

63% of total ASK

Fully available only to the Airline Cost Management Group (ACMG) member airlines.

Please contact us on [email protected] to find out how you can get involved free of charge!

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

13

2.5. Airline Staff

This year the ACMG survey encompassed even more detailed employment data with a separate reporting on flight deck crew and

cabin crew block hours. 50 ACMG airlines reported a total of more than 300,000 employees in 7 different staff categories, along with

their total salaries. This consequently allows us to offer a very beneficial insight into the employment cost structure in Section 5 -

Operational KPIs. Moreover, staff productivity, as well as employment of flight deck crew and cabin crew members are also exam-

ined in that section.

FOR MORE INFORMATION ON ACMG

Contact us: [email protected]

Visit our website: www.iata.org/ACMG

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

14

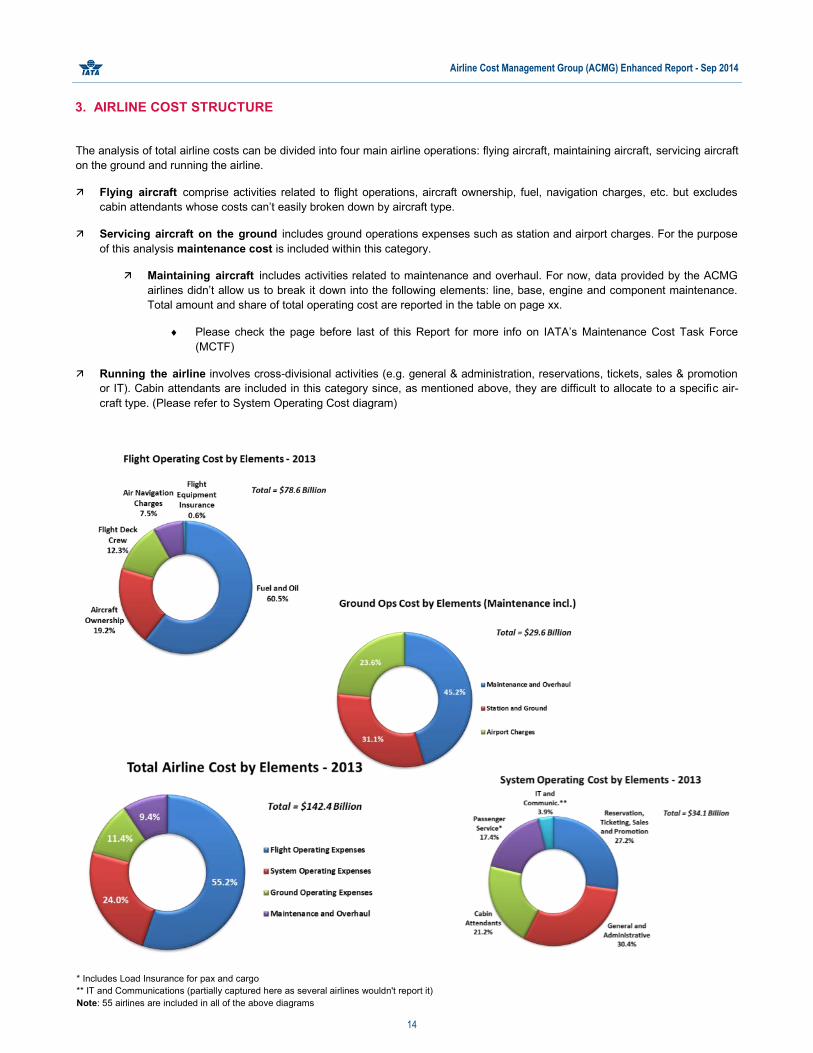

The analysis of total airline costs can be divided into four main airline operations: flying aircraft, maintaining aircraft, servicing aircraft

on the ground and running the airline.

Flying aircraft comprise activities related to flight operations, aircraft ownership, fuel, navigation charges, etc. but excludes

cabin attendants whose costs can’t easily broken down by aircraft type.

Servicing aircraft on the ground includes ground operations expenses such as station and airport charges. For the purpose

of this analysis maintenance cost is included within this category.

Maintaining aircraft includes activities related to maintenance and overhaul. For now, data provided by the ACMG

airlines didn’t allow us to break it down into the following elements: line, base, engine and component maintenance.

Total amount and share of total operating cost are reported in the table on page xx.

Please check the page before last of this Report for more info on IATA’s Maintenance Cost Task Force

(MCTF)

Running the airline involves cross-divisional activities (e.g. general & administration, reservations, tickets, sales & promotion

or IT). Cabin attendants are included in this category since, as mentioned above, they are difficult to allocate to a specific air-

craft type. (Please refer to System Operating Cost diagram)

* Includes Load Insurance for pax and cargo

** IT and Communications (partially captured here as several airlines wouldn't report it)

Note: 55 airlines are included in all of the above diagrams

3. AIRLINE COST STRUCTURE

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

15

Figures from the above table are displayed graphically in the diagram below. Not surprisingly, fuel and oil represented the largest

chunk of airline cost by far. Please mind that this cost structure represents more than 20% of the industry (55 ACMG airlines).

*Includes Load Insurance for pax and cargo

**Flight Equipment Insurance plus IT and Communications (partially captured here as several airlines wouldn't report it)

55 Participating Airlines Total $ US Cents/RPK US Cents/ASK US Cents/RTK US Cents/ATK $/FH $/pax

Fuel and Oil $47.6 Bil 3.78 2.94 30.89 20.65 4,022 81.3

Maintenance and Overhaul $13.4 Bil 1.07 0.83 8.70 5.82 1,133 22.9

General and Administrative $10.4 Bil 0.83 0.64 6.75 4.51 878 17.8

Flight Deck Crew $9.7 Bil 0.77 0.60 6.30 4.21 820 16.6

Reservation, Ticketing, Sales and Promotion $9.3 Bil 0.74 0.57 6.02 4.02 784 15.9

Station and Ground $9.2 Bil 0.73 0.57 5.99 4.01 780 15.8

Aircraft Ownership $15.1 Bil 1.20 0.93 9.79 6.55 1,275 25.8

Airport Charges $7.0 Bil 0.56 0.43 4.55 3.04 592 12.0

Cabin Attendants $7.2 Bil 0.57 0.45 4.69 3.14 611 12.4

Passenger Service* $5.9 Bil 0.47 0.37 3.86 2.58 503 10.2

Air Navigation Charges $5.9 Bil 0.47 0.36 3.82 2.55 497 10.1

Other** $1.7 Bil 0.14 0.11 1.13 0.76 148 3.0

Total $142.4 Bil 11.32 8.80 92.49 61.83 12,043 243.5

*Includes Load Insurance for pax and cargo

**Flight Equipment Insurance plus IT and Communications (partially captured here as several airlines wouldn't report it)

The following table shows total airline cost structure comprised of different cost groups. Moreover, several unit costs are offered for

more flexible benchmarking self-evaluation.

Fully available only to the Airline Cost Management Group (ACMG) member airlines.

Please contact us on [email protected] to find out how you can get involved free of

charge!

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

16

4. STRATEGIC KEY PERFORMANCE INDICATORS

Strategic KPIs, usually of much interest to senior level management, comprise key statistical and financial figures. Benchmarking on

financial performance is also provided before the section ends with yearly trends analysis for many recurrent airlines; a priceless

insight into real savings of devoted ACMG members.

Strategic KPIs

ACMG Statistical Snapshot

Note: Expense and cost are very much related in this study; expense is an accounting term for a cost of resources used up or consumed while a company is

performing its main revenue-generating activities

Strategic KPIs* ACMG Airlines

Total Operating Expenses/FH (USD) $12,043Total Operating Expenses/ASK (US Cents) 8.80Total Operating Expenses/ATK (US Cents) 61.83Fuel Share of Total Ops. Expenses 33.4%Total Ops Expenses without Fuel/ASK (US Cents) 5.86Yield (Op. Revenue/RPK in US Cents) 11.62Operating Revenue/ASK (US Cents) 9.04Operating Profit (% margin) 2.59%Passenger Load Factor (PLF) 77.7%Weight Load Factor (WLF) 66.8%Daily Utilization (Hours) 9.48Average Fleet Age (Years) 9.88

* Based on 55 reporting airlines

Statistical Snapshot* ACMG Airlines Industry total** ACMG share

Revenue Passenger Km (RPK) 1,257.9 Bil 5,839.4 Bil 21.5%Available Seat Km (ASK) 1,617.9 Bil 7,327.0 Bil 22.1%Revenue Tonne Km (RTK) 154.0 Bil 738.3 Bil 20.9%Available Tonne Km (ATK) 230.3 Bil 1,097.5 Bil 21.0%Passengers Carried 584.8 Mil 3.1 Bil 18.7%Total Flight Hours 11.8 Mil

Total Flight Cycles 5.729 MilTotal Operating Expenses (USD) 142.4 Bil 686.0 Bil 20.8%

Total Operating Revenues (USD) 146.199 Bil 708.000 Bil 20.6%

* Based on 55 reporting airlines

** According to IATA WATS FY2013

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

17

4.1. Financial Performance

The ACMG airlines* are profitable as a whole; with an overall average operating margin of 2.6%. However, 24 airlines in the group

still incurred losses.

From the below bubble chart, it is clear that the sample of airlines used in this compact represents a wide range of different cost

basis as well as revenue levels. It can be seen that the low cost carriers are not necessarily profitable and higher cost loss making.

The average of the RASK for each 0.5c interval value of CASK shows for the cohort two clear areas that are profitable (CASK 7.5

US cents and 10 US cents). The percentage profit margin though seems to be higher for the lower cost option.

Revenue size indicated against RASK and CASK

On the following page respective airlines’ revenues and costs per unit (both ASK and ATK) are graphically displayed. Average

ACMG airline** earned 8.9 US cents/ASK and expensed 8.7 US cents/ASK.

* 52 airlines provided validated revenue and expenditure data

** Average ACMG Airline: Overall average as one group of 52 included airlines

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

18

Financial Performance Industry Benchmarking

Fully

ava

ilable

on

ly t

o t

he A

irlin

e C

ost

Ma

na

ge

me

nt

Gro

up

(A

CM

G)

mem

ber

airlin

es.

Ple

ase

co

nta

ct

us o

n A

CM

G@

iata

.org

to

fin

d o

ut

how

yo

u c

an

get

involv

ed f

ree o

f ch

arg

e!

Fully

ava

ilable

on

ly t

o t

he A

irlin

e C

ost

Ma

na

ge

me

nt

Gro

up

(A

CM

G)

mem

ber

airlin

es.

Ple

ase

co

nta

ct

us o

n A

CM

G@

iata

.org

to

fin

d o

ut

how

yo

u c

an

get

involv

ed f

ree o

f ch

arg

e!

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

19

Special focus on impact of exchange rates fluctuations

One of our identified critical parameters affecting airline operational cost, which is very difficult to account for, is currency exchange

fluctuations. Given that majority of costs are tied to US dollars and revenues come in various currencies, respective currency ex-

change rates can significantly affect the bottom line. In the same vein, it can affect benchmarking, although less so since this study

is predominantly benchmarking costs.

For the purpose of this report, 35 airlines have reported their gains or losses obtained from foreign exchange transactions, including

foreign exchange hedge. Below diagram illustrates:

absolute ($) values of foreign exchange financial impact, and

relative (%) impact on airlines’ bottom lines; a share in respective airline’s profit or loss.

19 airlines have seen their bottom lines improving due to favorable exchange rates, while 16 airlines were not so fortunate and lost

significant amount of money. Collectively, 35 airlines lost 375 million dollars.

Successful currency management and exchange rate risk mitigation could easily add 10-20 % to the bottom line. On the opposite

side, lack of it could erode the profits or increase the losses by as much as 50 %!

In conclusion, exchange rate risks are definitely worth airlines’ close attention as they can, in this razor-thin profit margin industry,

mean the difference between a net profit or loss.

Fully available only to the Airline Cost Management Group (ACMG) member airlines.

Please contact us on [email protected] to find out how you can get involved free of charge!

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

20

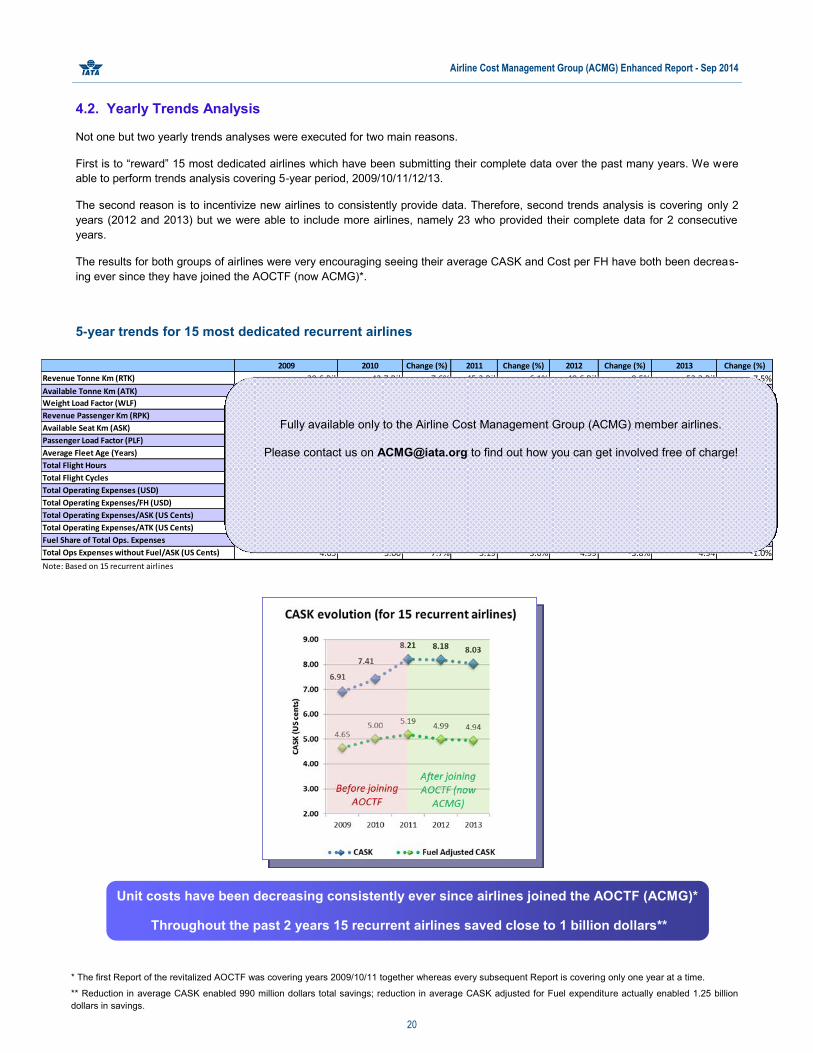

4.2. Yearly Trends Analysis

Not one but two yearly trends analyses were executed for two main reasons.

First is to “reward” 15 most dedicated airlines which have been submitting their complete data over the past many years. We were

able to perform trends analysis covering 5-year period, 2009/10/11/12/13.

The second reason is to incentivize new airlines to consistently provide data. Therefore, second trends analysis is covering only 2

years (2012 and 2013) but we were able to include more airlines, namely 23 who provided their complete data for 2 consecutive

years.

The results for both groups of airlines were very encouraging seeing their average CASK and Cost per FH have both been decreas-

ing ever since they have joined the AOCTF (now ACMG)*.

Unit costs have been decreasing consistently ever since airlines joined the AOCTF (ACMG)*

Throughout the past 2 years 15 recurrent airlines saved close to 1 billion dollars**

* The first Report of the revitalized AOCTF was covering years 2009/10/11 together whereas every subsequent Report is covering only one year at a time.

** Reduction in average CASK enabled 990 million dollars total savings; reduction in average CASK adjusted for Fuel expenditure actually enabled 1.25 billion

dollars in savings.

5-year trends for 15 most dedicated recurrent airlines

2009 2010 Change (%) 2011 Change (%) 2012 Change (%) 2013 Change (%)

Revenue Tonne Km (RTK) 39.6 Bil 42.7 Bil 7.6% 45.3 Bil 6.1% 49.6 Bil 9.5% 53.3 Bil 7.5%

Available Tonne Km (ATK) 61.4 Bil 63.9 Bil 4.1% 69.7 Bil 9.0% 75.3 Bil 8.1% 82.0 Bil 8.9%

Weight Load Factor (WLF) 64.6% 66.8% +2.2 pt 65.0% -1.8 pt 65.9% +0.9 pts 65.0% -0.9 ptsRevenue Passenger Km (RPK) 312.4 Bil 327.1 Bil 4.7% 349.7 Bil 6.9% 380.6 Bil 8.8% 424.6 Bil 11.6%

Available Seat Km (ASK) 428.6 Bil 434.2 Bil 1.3% 471.7 Bil 8.6% 500.4 Bil 6.1% 552.0 Bil 10.3%

Passenger Load Factor (PLF) 72.9% 75.3% +2.4 pts 74.1% -0.8 pts 76.1% +2.0 pts 76.9% +0.8 pts

Average Fleet Age (Years) 9.08 8.88 -2.2% 8.85 -0.4% 8.31 -6.1% 7.76 -6.6%Total Flight Hours 2.449 Mil 2.554 Mil 4.3% 2.757 Mil 8.0% 3.0 Mil 7.8% 3.3 Mil 10.6%Total Flight Cycles 914.082 K 945.648 K 3.5% 1.007 Mil 6.5% 1.1 Mil 9.9% 1.2 Mil 11.6%

Total Operating Expenses (USD) $29.6 Bil $32.2 Bil 8.6% $38.7 Bil 20.4% $40.9 Bil 5.7% $44.3 Bil 8.3%

Total Operating Expenses/FH (USD) $12,098 $12,597 4.1% $14,052 11.5% $13,772 -2.0% $13,477 -2.1%

Total Operating Expenses/ASK (US Cents) 6.91 7.41 7.2% 8.21 10.9% 8.18 -0.4% 8.03 -1.9%Total Operating Expenses/ATK (US Cents) 48.28 50.35 4.3% 55.61 10.5% 54.39 -2.2%

Fuel Share of Total Ops. Expenses 32.7% 32.4% -0.3 pts 36.9% +4.5 pts 39.0% +2.1 pts 38.5% -0.5 pts

Total Ops Expenses without Fuel/ASK (US Cents) 4.65 5.00 7.7% 5.19 3.6% 4.99 -3.8% 4.94 -1.0%

Note: Based on 15 recurrent airlines

Fully available only to the Airline Cost Management Group (ACMG) member airlines.

Please contact us on [email protected] to find out how you can get involved free of charge!

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

21

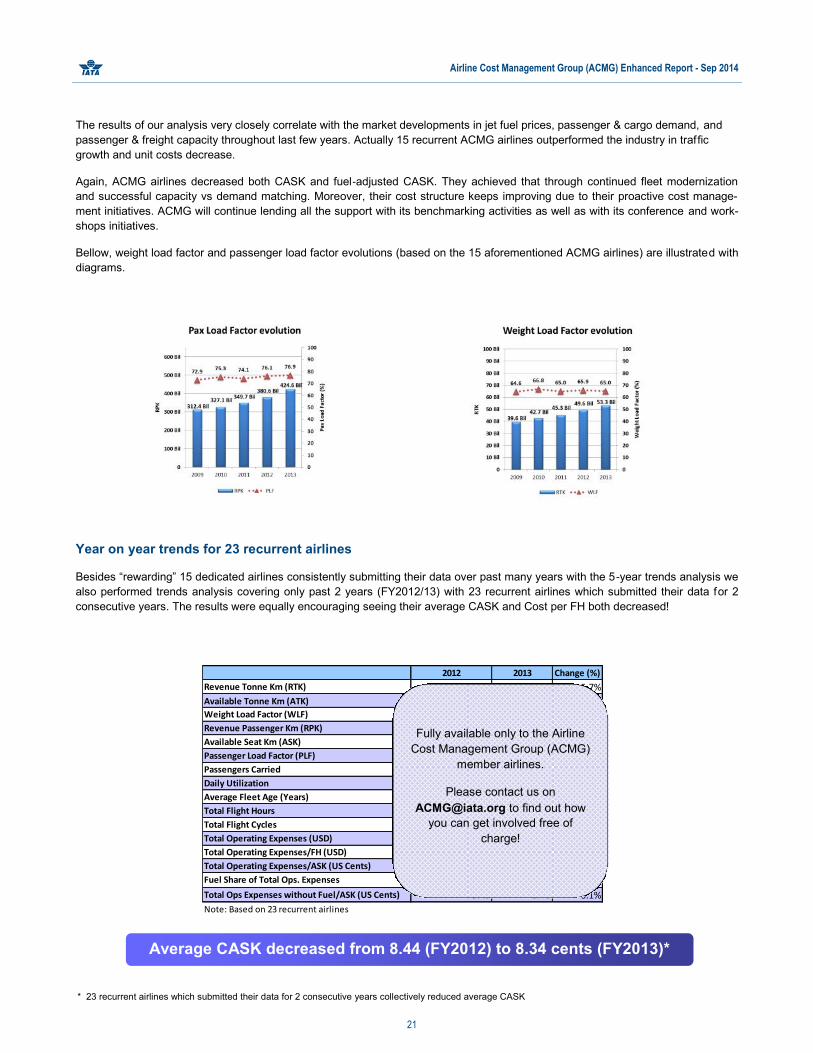

The results of our analysis very closely correlate with the market developments in jet fuel prices, passenger & cargo demand, and

passenger & freight capacity throughout last few years. Actually 15 recurrent ACMG airlines outperformed the industry in traffic

growth and unit costs decrease.

Again, ACMG airlines decreased both CASK and fuel-adjusted CASK. They achieved that through continued fleet modernization

and successful capacity vs demand matching. Moreover, their cost structure keeps improving due to their proactive cost manage-

ment initiatives. ACMG will continue lending all the support with its benchmarking activities as well as with its conference and work-

shops initiatives.

Bellow, weight load factor and passenger load factor evolutions (based on the 15 aforementioned ACMG airlines) are illustrated with

diagrams.

Year on year trends for 23 recurrent airlines

Besides “rewarding” 15 dedicated airlines consistently submitting their data over past many years with the 5-year trends analysis we

also performed trends analysis covering only past 2 years (FY2012/13) with 23 recurrent airlines which submitted their data for 2

consecutive years. The results were equally encouraging seeing their average CASK and Cost per FH both decreased!

Average CASK decreased from 8.44 (FY2012) to 8.34 cents (FY2013)*

2012 2013 Change (%)

Revenue Tonne Km (RTK) 85.3 Bil 90.2 Bil 5.7%

Available Tonne Km (ATK) 131.4 Bil 139.5 Bil 6.2%Weight Load Factor (WLF) 64.9% 64.6% -0.3 pt

Revenue Passenger Km (RPK) 709.7 Bil 770.8 Bil 8.6%

Available Seat Km (ASK) 914.6 Bil 988.7 Bil 8.1%Passenger Load Factor (PLF) 77.6% 78.0% +0.4 pts

Passengers Carried 320.3 Mil 351.4 Mil 9.7%

Daily Utilization 9.43 10.35 9.7%Average Fleet Age (Years) 10.13 10.23 1.0%

Total Flight Hours 6.75 Mil 7.38 Mil 9.3%

Total Flight Cycles 3.06 Mil 3.48 Mil 13.5%Total Operating Expenses (USD) $77.2 Bil $82.4 Bil 6.8%

Total Operating Expenses/FH (USD) $11,437 $11,168 -2.3%

Total Operating Expenses/ASK (US Cents) 8.44 8.34 -1.2%Fuel Share of Total Ops. Expenses 35.0% 34.3% -0.7 pts

Total Ops Expenses without Fuel/ASK (US Cents) 5.49 5.48 -0.1%

Note: Based on 23 recurrent airlines

* 23 recurrent airlines which submitted their data for 2 consecutive years collectively reduced average CASK

Fully available only to the Airline

Cost Management Group (ACMG)

member airlines.

Please contact us on

[email protected] to find out how

you can get involved free of

charge!

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

22

5. OPERATIONAL KEY PERFORMANCE INDICATORS

Operational Key Performance Indicators examine the following areas:

Fuel cost and efficiency

Staff productivity

Employment costs.

5.1. Fuel Cost and Efficiency

Fuel cost consistently remains the biggest concern of airlines which unfortunately have little control over its price. The only efficiency

they can gain is to decrease the fuel consumption; of course not by less flying but with more efficient fuel management, fleet and

routes!

On the next pages, the ACMG airlines are benchmarked on the following fuel indicators:

Fuel and CO2 burned per RTK

Fuel burned per 100 passenger kms

The 2 diagrams clearly show some airlines are more fuel efficient than others; besides different aircraft types they operate

there is a number of factors to look into within the operations of every respective airline.

Average Fuel price

Average ACMG Airline paid $1.00 per kg of jet fuel. Again, the scope of this analysis doesn’t permit looking into more de-

tails (such as currency exchange rates effect, fuel purchasing strategy, geographical location, etc.) but the diagram should

be a good inspiration for some airlines to further look into their fuel supply chain.

Fuel share in total operating expenses

The proportion of fuel and oil expenses in total operating expenses ranges between 21% and 46%, with the average of

33.4%.

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

23

Fu

lly a

vaila

ble

only

to the A

irlin

e C

ost M

anagem

ent G

roup (

AC

MG

) m

em

ber

airlin

es. P

lease c

onta

ct us o

n A

CM

G@

iata

.org

to fin

d o

ut

how

you c

an g

et

involv

ed f

ree o

f charg

e!

Fu

lly a

vaila

ble

only

to the A

irlin

e C

ost M

anagem

ent G

roup (

AC

MG

) m

em

ber

airlin

es. P

lease c

onta

ct us o

n A

CM

G@

iata

.org

to fin

d o

ut

how

you c

an g

et

involv

ed f

ree o

f charg

e!

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

24

Fu

lly a

vaila

ble

only

to the A

irlin

e C

ost M

anagem

ent G

roup (

AC

MG

) m

em

ber

airlin

es. P

lease c

onta

ct us o

n A

CM

G@

iata

.org

to fin

d o

ut

how

you c

an g

et

involv

ed f

ree o

f charg

e!

Fu

lly a

vaila

ble

only

to the A

irlin

e C

ost M

anagem

ent G

roup (

AC

MG

) m

em

ber

airlin

es. P

lease c

onta

ct us o

n A

CM

G@

iata

.org

to fin

d o

ut

how

you c

an g

et

involv

ed f

ree o

f charg

e!

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

25

The fuel indicators graphically displayed on the previous pages are gathered in the table below.

FA 407.68 1,284.18 3.96 1.03 31.7%

Z1 327.70 1,032.25 3.28 1.02 35.1%

RE 379.84 1,196.51 5.06 0.81 40.6%

AG 303.70 956.64 3.67 1.03 29.8%

U2 285.35 898.85 3.25 1.06 37.7%

WW 302.72 953.57 3.62 1.06 40.1%

BL 376.70 1,186.62 4.32 0.79 36.0%

8T 266.70 840.10 3.73 1.01 37.0%

MB 284.93 897.54 2.81 1.35 41.3%

77 282.58 890.12 4.10 1.06 29.8%

JS 398.42 1,255.02 4.45 0.85 35.1%

CC 342.41 1,078.58 3.52 1.02 28.3%

CM 339.82 1,070.42 3.64 1.07 41.1%

CB 368.50 1,160.79 3.76 1.07 36.4%

KV 329.33 1,037.40 3.24 1.08 33.7%

9B 260.12 819.36 3.78 0.94 29.6%

TH 285.28 898.63 3.83 1.09 45.8%

TX 374.03 1,178.19 3.41 1.06 35.7%

EY 327.23 1,030.79 3.31 1.00 41.7%

MM 296.00 932.41 3.82 0.98 34.7%

3F 407.89 1,284.84 3.77 0.31 11.1%

UL 244.64 770.61 2.88 1.04 29.2%

ID 408.57 1,287.00 3.89 1.05 36.0%

RR 318.81 1,004.26 3.01 0.88 20.5%

JR 301.33 949.18 3.51 0.76 36.7%

TF 387.33 1,220.08 4.27 0.89 29.0%

FF 262.32 826.31 2.68 1.15 38.0%

MC 348.89 1,099.01 3.08 1.11 34.6%

2K 498.57 1,570.49 3.66 0.85 26.9%

GZ 343.89 1,083.27 3.23 1.01 32.6%

NN 286.86 903.62 2.82 1.06 31.7%

PP 362.53 1,141.98 3.53 1.03 35.4%

EE 356.64 1,123.42 3.19 1.04 38.9%

KK 278.47 877.17 2.72 0.88 30.2%

C3 433.76 1,366.36 3.41 1.06 30.5%

TT 595.44 1,875.63 4.95 0.66 28.1%

N2 369.09 1,162.64 3.44 1.07 26.8%

GG 431.88 1,360.42 3.20 0.95 29.6%

3T 340.36 1,072.14 3.19 1.09 31.3%

RP 235.15 740.72 2.22 1.09 29.7%

Z5 305.48 962.26 2.73 0.98 32.6%

BB 311.88 982.41 3.03 1.15 31.5%

LL 309.47 974.82 2.79 1.10 27.8%

JA 418.34 1,317.77 3.58 1.03 21.5%

KT 459.44 1,447.25 4.07 1.11 25.0%

AS 370.60 1,167.39 3.39 1.17 32.0%

JU 425.38 1,339.96 3.98 1.21 27.7%

SS 424.24 1,336.36 3.21 0.88 28.0%

GC 527.96 1,663.06 3.95 1.18 10.3%

IA 441.95 1,392.14 3.40 1.14 30.5%

HH 408.84 1,287.84 3.34 1.09 28.6%

Fule Price

($ per kg)

% of Total

Expenses

More than 1 billion

100 million to 1

billion

Up to 100 million

Airline Fuel Expense in $ Fuel burned per RTK

(grams)

CO2 per RTK

(grams)

Fuel burned per 100

passenger kms (liters)

Fully available only to the Airline Cost Management Group (ACMG) member airlines.

Please contact us on [email protected] to find out how you can get involved free of charge!

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

26

Special focus on impact of fuel hedging

Whereas many airlines advocate fuel hedging as a proper mechanism to alleviate the impact of the jet fuel volatility there are many

who believe fuel hedging is not airlines’ core competency and rather shy away from it.

In our study, 23 airlines reported their fuel hedging financial results. Below diagram shows 16 airlines managed to decrease fuel

expenses while 7 airlines increased their fuel expenses by fuel hedging. Collectively, 23 airlines saved close to 100 million dollars.

Nevertheless, as many believe current fuel prices are unjustified one might think twice before hedging at these high price levels.

Fully available only to the Airline Cost Management Group (ACMG) member airlines.

Please contact us on [email protected] to find out how you can get involved free of charge!

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

27

5.2 Employment Cost Structure

50 ACMG airlines reported a total of more than 300,000 employees in 7 different staff categories, along with their total salaries. This

consequently allows us to offer a very beneficial insight into the employment cost structure below.

Indeed, outsourcing practices differ significantly from airline to airline, but given the large sample we can take below diagrams as an

industry average employment cost structure.

Cabin attendants represent the largest staff group (30%), followed by administrative employees (20%). Nevertheless, the largest

chunk of salaries is paid to flight deck crew (29%), followed by cabin attendants (24%) and administrative employees (20%).

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

28

Employment Cost (by Regions)

Examination of average employment cost, more specifically flight deck crew, cabin crew, and general & administrative compensation

cost shows the differences among regions as well as among 50 ACMG airline participants. As expected the deviations are much

bigger within cabin crew and general & administrative categories than within flight deck crew compensation.

Again, as outsourcing practices differ significantly from airline to airline, it is not appropriate to benchmark this number within the

industry. However, it is a measure that an airline may want to monitor on an annual basis.

Fully available only to the Airline Cost Management Group (ACMG) member airlines.

Please contact us on [email protected] to find out how you can get involved free of charge!

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

29

Employment Cost - continued

Besides employment cost by regions all the reported average compensations for flight deck crew, cabin crew, and gen-

eral&administration staff are presented below.

Moreover, the ratio (by number of posts) between these types of employees are calculated on the right. Given the extremely sensi-

tive nature of these figures airlines are listed as positions sorted by flight deck crew cost.

Airline Position Flight Deck Crew Cabin Crew General and Admin #Flight Deck Crew to

#Gen & Admin

#Cabin Crew to

#Gen & Admin

#Cabin Crew to

#Flight Deck Crew

1 $38,125 $11,607 $17,496 0.62 1.24 2.01

2 $43,032 $19,217 $16,619 0.86 0.29 0.333 $44,338 $6,443 $22,791 1.10 2.04 1.86

4 $47,598 $21,496 $6,976 0.34 0.53 1.555 $58,822 $16,083 $18,524 0.30 1.20 3.94

6 $64,097 $11,438 $32,899 2.11 4.00 1.907 $64,425 $8,793 $16,503 0.33 0.78 2.37

8 $71,522 $6,844 $8,016 0.31 0.73 2.39

9 $77,156 $20,564 $19,569 0.16 0.28 1.7810 $81,297 $19,161 $21,970 0.59 0.83 1.40

11 $85,014 $15,404 $16,698 0.51 1.74 3.4212 $85,458 $57,824 $18,128 0.67 0.85 1.27

13 $86,120 $13,467 $29,227 0.46 0.99 2.1214 $88,379 $35,252 $80,700 2.30 1.70 0.74

15 $90,772 $22,587 $17,711 0.48 1.20 2.4916 $92,722 $17,541 $21,594 0.45 1.13 2.49

17 $95,450 $19,463 $22,917 0.48 0.64 1.33

18 $105,542 $15,543 $46,102 0.43 1.06 2.4719 $108,233 $17,319 $25,465 0.69 1.13 1.64

20 $109,482 $22,031 $14,761 0.18 0.47 2.5921 $111,646 $18,746 $32,242 0.98 2.12 2.17

22 $112,581 $23,042 $36,518 2.43 5.20 2.1423 $113,557 $16,664 $29,168 0.31 0.53 1.71

24 $115,360 $18,575 $44,115 0.97 1.49 1.5425 $115,464 $33,173 $27,090 0.57 1.57 2.7626 $117,346 $48,466 $46,998 1.01 0.89 0.88

27 $117,600 $47,040 $64,680 2.46 4.93 2.0028 $119,302 $40,774 $57,606 0.83 1.73 2.10

29 $122,494 $36,354 $60,200 2.44 2.57 1.0530 $124,620 $34,523 $25,063 0.60 0.75 1.26

31 $125,851 $68,912 $114,106 3.20 5.43 1.7032 $137,951 $35,887 $65,826 0.27 1.41 5.32

33 $140,769 $53,067 $111,199 0.79 0.51 0.65

34 $146,533 $50,155 $130,493 1.39 2.06 1.4835 $158,590 $30,581 $57,192 1.63 3.59 2.21

36 $160,292 $68,269 $190,360 2.16 7.09 3.2837 $162,222 $51,111 $121,053 2.37 2.37 1.00

38 $162,436 $25,438 $59,570 0.89 4.30 4.8139 $172,968 $73,214 $73,980 1.62 3.79 2.34

40 $176,066 $72,094 $66,588 1.18 2.17 1.8441 $178,020 $24,870 $44,559 0.47 1.02 2.19

42 $188,130 $43,847 $44,169 0.40 0.99 2.49

43 $188,429 $64,402 $48,012 0.97 2.62 2.7144 $196,140 $36,928 $74,723 0.66 1.51 2.28

45 $207,203 $62,183 $90,944 0.69 1.52 2.2046 $219,086 $58,400 $137,059 0.35 1.19 3.39

47 $232,259 $82,345 $90,277 1.03 2.66 2.5748 $243,052 $83,102 $95,760 0.54 1.94 3.60

49 $284,111 $92,287 $112,164 0.40 1.35 3.36

50 $297,018 $92,260 $97,814 0.94 4.17 4.44

* Sorted by flight deck crew cost

Average cost per employee type* Employee type ratio

Fully available only to the Airline Cost Management Group (ACMG) member airlines.

Please contact us on [email protected] to find out how you can get involved free of charge!

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

30

5.3 Staff Productivity

When studying ASK and ATK per employee productivity indicators one should acknowledge that regulations, different aircraft type

and operations (e.g. long vs. short haul) along with the airline schedule and business model are important in explaining differences

around the world.

Note: As outsourcing practices differ significantly from airline to airline, it may not be appropriate to benchmark this number within the industry. However, it is a

measure that an airline may want to monitor on an annual basis.

Fully available only to the Airline Cost Management Group (ACMG) member airlines. Please contact us on [email protected] to find out how you

can get involved free of charge!

Fully available only to the Airline Cost Management Group (ACMG) member airlines. Please contact us on [email protected] to find out how you

can get involved free of charge!

Fully available only to the Airline Cost Management Group (ACMG) member airlines. Please contact us on [email protected] to find out how you

can get involved free of charge!

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

31

Flight Deck Crew and Cabin Attendants employment

Similar to the previous page, when observing the first two diagrams one should acknowledge that regulations, different aircraft type

and operations (e.g. long vs. short haul) along with the airline schedule and business model are important in explaining differences

around the world.

The third diagram, however, is directly comparing monthly use of workforce for 23 airlines that correctly provided separate f light deck

crew and cabin crew block hours.

Fully available only to the Airline Cost Management Group (ACMG) member airlines. Please contact us on [email protected] to find out how you

can get involved free of charge!

Fully available only to the Airline Cost Management Group (ACMG) member airlines. Please contact us on [email protected] to find out how you

can get involved free of charge!

Fully available only to the Airline Cost Management Group (ACMG) member airlines. Please contact us on

[email protected] to find out how you can get involved free of charge!

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

32

6. AIRCRAFT TYPE ANALYSIS

6.1. Overview

6.2. Operational Data

Top 12 active aircraft accounted for 90% of the total active

fleet. Nevertheless, due to incomplete data submissions by

some airlines a number of them are excluded from the de-

tailed analysis on the next pages. The total number of thor-

oughly analyzed aircraft therefore sums up to 2,483 aircraft,

representing 67% of the total reported aircraft.

Also, as B717 was operated by only one reporting airline it

was excluded from the abovementioned analysis. A380 has

been included.

In general, the results support airlines’ efforts to modernize

their fleet.

6.3. Unit Costs

A320 Family 807 26

B737 NG 497 17

A330 233 21

B777 229 14

A340 158 12

Dash 8 146 6

B737 Classic 93 11

B747 78 10

EMB-190 74 6

CRJ 64 4

B767 63 8

A380 41 4

Fleet Type # Active Aircraft# of Airlines

reporting

A320 Family $24.0 Mil $8,229 7.85 33.7%

B737 NG $21.7 Mil $6,859 6.31 44.1%

A330 $50.9 Mil $12,052 5.81 47.5%

B777 $61.3 Mil $14,318 5.81 48.7%

A340 $66.8 Mil $14,732 6.55 53.4%

Dash 8 $8.8 Mil $3,921 15.54 23.4%

B737 Classic $17.2 Mil $7,771 9.81 35.5%

B747 $78.1 Mil $19,242 5.84 54.9%

EMB-190 $18.2 Mil $7,102 10.36 33.1%

CRJ $12.7 Mil $5,009 11.33 36.0%

B767 $38.5 Mil $9,798 5.87 51.1%

A380 $103.4 Mil $22,877 5.74 55.9%

Fuel as % of Direct

Operating* $

*Direct Operating Cost includes Flying Cost, Ground and Maintenance Cost, and excludes

System Operating Cost

Fleet Type Direct Operating

$*/AC

Direct Operating

$*/FH

Direct Operating

$*/ASK (in US cents)

Weight Load Factor

A320 Family 8.62 9.4 2,355,213 1,292,185 1.8 76.6% 67.7%

B737 NG 9.90 6.6 1,568,863 890,746 1.8 74.5% 65.9%

A330 12.01 5.4 984,109 195,071 5.0 77.3% 67.4%

B777 12.39 7.7 979,393 162,911 6.0 78.9% 65.1%

A340 12.05 11.8 715,917 85,928 8.3 80.4% 72.5%

Dash 8 6.59 13.3 328,268 324,428 1.0 70.5% 66.7%

B737 Classic 6.78 19.6 206,583 159,345 1.3 73.6% 68.3%

B747 11.60 14.5 316,633 40,428 7.8 82.4% 76.3%

EMB-190 8.08 5.7 189,803 109,406 1.7 80.1% 65.5%

CRJ 6.42 8.1 162,645 120,160 1.4 71.6% 62.8%

B767 11.97 17.7 247,790 45,282 5.5 79.7% 55.7%

A380 13.90 2.6 185,293 19,466 9.5 81.4% 79.1%

Fleet Type Average Fleet Age Flight CyclesFlight Hours Hour-to-Cycle ratioDaily Utilization Pax Load Factor

Fully available only to the Airline Cost Management Group (ACMG) member airlines.

Please contact us on [email protected] to find out how you can get involved free of charge!

Fully available only to the Airline Cost Management Group

(ACMG) member airlines.

Please contact us on [email protected] to find out how you

can get involved free of charge!

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

33

As mentioned in the disclaimer on page 2 please note that in this study only raw data provided by airlines were used. No attempt to

normalize the data was done. Therefore, the significant differences in maintenance cost between the reported B737NG and A320

families can be explained as follows:

Impact of external factors on B737NG carriers A320 Family carriers

Currency fluctuations neutral neutral

Local labor rates positive impact negative impact

Operational environment neutral negative impact

Age of aircraft positive impact negative impact

Fleet size (economies of

scale

neutral neutral

6.3. Unit Costs - continued

A320 Family $15.5 Mil $5,317 $9,692 5.07 52.2%

B737 NG $16.6 Mil $5,270 $9,282 4.85 57.4%

A330 $37.8 Mil $8,940 $45,099 4.31 64.0%

B777 $47.0 Mil $10,978 $66,001 4.46 63.5%

A340 $51.7 Mil $11,396 $94,948 5.07 69.0%

Dash 8 $5.2 Mil $2,311 $2,338 9.16 39.8%

B737 Classic $10.8 Mil $4,890 $6,339 6.17 56.4%

B747 $57.8 Mil $14,228 $111,430 4.32 74.3%

EMB-190 $11.1 Mil $4,317 $7,489 6.30 54.5%

CRJ $9.0 Mil $3,562 $4,822 8.06 50.7%

B767 $29.1 Mil $7,411 $40,554 4.44 67.5%

A380 $83.8 Mil $18,533 $176,409 4.65 69.0%

Flight Ops. $/FC Flight Ops. $/ASK

(US Cents)Flight

Operations

Flight Ops. $/AC Flight Ops. $/FH Fuel as % of Flight

Ops. Expenses

A320 Family $3.6 Mil $1,223 $2,229 1.17

B737 NG $2.1 Mil $670 $1,180 0.62

A330 $5.6 Mil $1,336 $6,740 0.64

B777 $7.6 Mil $1,764 $10,607 0.72

A340 $8.6 Mil $1,895 $15,788 0.84

Dash 8 $1.7 Mil $758 $767 3.00

B737 Classic $2.5 Mil $1,109 $1,438 1.40

B747 $8.2 Mil $2,028 $15,882 0.62

EMB-190 $3.3 Mil $1,287 $2,233 1.88

CRJ $1.7 Mil $679 $919 1.54

B767 $5.1 Mil $1,299 $7,111 0.78

A380 $6.4 Mil $1,419 $13,508 0.36

Maintenance $/AC Maintenance $/FHMaintenance &

Overhaul

Maintenance $/FC Maintenance $/ASK

(US Cents)

Fully available only to the Airline Cost Management Group (ACMG) member airlines.

Please contact us on [email protected] to find out how you can get involved free of

charge!

Fully available only to the Airline Cost Management Group

(ACMG) member airlines.

Please contact us on [email protected] to find out how you can

get involved free of charge!

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

34

To conclude on aircraft type analysis, 2 self-explanatory aircraft unit cost matrix are provided below. Please note that they are based

on raw data provided by ACMG airlines. As every airline operates in a unique environment, this analysis might deviate from the one

provided by OEMs.

Fully available only to the Airline Cost Management Group (ACMG) member airlines.

Please contact us on [email protected] to find out how you can get involved free of charge!

Fully available only to the Airline Cost Management Group (ACMG) member airlines.

Please contact us on [email protected] to find out how you can get involved free of charge!

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

35

7. DETAILED ANALYSIS of B737NG and A320 Family

To conduct the aircraft type analysis we selected two most popular aircraft families; B737NG and A320 Family representing 26.1%

and 22.8% of ACMG active fleet count, respectively.

The purpose of this section is for a respective airline to compare its aircraft utilization with other involved airlines. Nevertheless, the

average values are provided on previous pages should they be of reader’s interest.

7.1. B737NG

A strong trend of introducing new and more fuel efficient aircraft while retiring old fleets paved the way for B737NG Family. It is the

most popular aircraft family in our analysis with total of 974 reported aircraft.

17 airlines reported B737NG in their active fleet and 16 of them are represented in most of the charts.

Fully available only to the Airline Cost Management Group (ACMG) member airlines. Please contact us on [email protected] to find out

how you can get involved free of charge!

Fully available only to the Airline Cost Management Group (ACMG) member airlines. Please contact us on [email protected] to

find out how you can get involved free of charge!

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

36

Note: Direct

Fully available only to the Airline Cost Management Group (ACMG) member airlines. Please contact us on [email protected] to find out

how you can get involved free of charge!

Fully available only to the Airline Cost Management Group (ACMG) member airlines. Please contact us on [email protected] to find out

how you can get involved free of charge!

Fully available only to the Airline Cost Management Group (ACMG) member airlines. Please contact us on [email protected] to find out

how you can get involved free of charge!

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

37

7.2. A320 Family

30 airlines reported A320 family aircraft in their active fleet for a total of 849 aircraft, although most of the charts include 28 airlines

and slightly less aircraft.

Fully available only to the Airline Cost Management Group (ACMG) member airlines. Please contact us on

[email protected] to find out how you can get involved free of charge!

Fully available only to the Airline Cost Management Group (ACMG) member airlines. Please contact us on

[email protected] to find out how you can get involved free of charge!

Fully available only to the Airline Cost Management Group (ACMG) member airlines. Please contact us on [email protected] to find out how

you can get involved free of charge!

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

38

Note:

Fully available only to the Airline Cost Management Group (ACMG) member airlines. Please contact us on [email protected] to find out how

you can get involved free of charge!

Fully available only to the Airline Cost Management Group (ACMG) member airlines. Please contact us on [email protected] to find out how

you can get involved free of charge!

Fully available only to the Airline Cost Management Group (ACMG) member airlines. Please contact us on [email protected] to find out how

you can get involved free of charge!

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

39

Fully available only to the Airline Cost Management Group (ACMG) member airlines. Please contact us on [email protected] to

find out how you can get involved free of charge!

Fully available only to the Airline Cost Management Group (ACMG) member airlines. Please contact us on [email protected] to find out how

you can get involved free of charge!

Fully available only to the Airline Cost Management Group (ACMG) member airlines. Please contact us on [email protected] to find out how

you can get involved free of charge!

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

40

8. SPECIALIZED ACMG REPORT

As ACMG is constantly striving to improve and provide even better value to our members, we are for the first time ever offering spe-

cialized reports, either focusing on a region, similar fleet size carriers, or similar stage length carriers.

We truly believe these customized solutions will offer even more insight into industry best practices and cost efficiencies through

improved benchmarking precision.

Pricing

How do I get my customized solution?

Please contact us for the detailed price prior to ordering your Specialized ACMG Report at [email protected] or give us a call on +1

514 874 0202 Ext. 3262

Furthermore, it would be our pleasure to answer any questions regarding both, the Enhanced ACMG Report and Specialized ACMG

Report.

Specialized Regional

Report

(unique to every airline)

Contact us for the detailed price

Africa

Americas

Asia Pacific

Europe

Middle East and Northern Africa

Fully Customized Report

(tailored to individual airline

needs; e.g. choice of

region, similar fleet size,

similar stage length, etc.)

Contact us for the detailed price

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

41

Chris MARKOU

Assistant Director,

IATA Operations

IATA’S MAINTENANCE

COST TASK FORCE (MCTF)

Similar in concept to the ACMG,

IATA developed the MCTF almost

50 years ago to serve as a focal

point for gathering industry infor-

mation on commercial airline

maintenance costs, including MRO

(Maintenance, Repair and Over-

haul) cost strategies.

Objectives and Activities

Define and standardize the re-

porting of commercial airline

maintenance costs

Benchmark with own airline’s

historical data and compare with

industry best practices

Identify high cost drivers and

target areas for Maintenance

Cost reduction, as an individual

operator or as part of an airline

group (i.e. Cargo, Low-Cost,

Latin American, etc.).

Collaborate with OEMs and other

suppliers to define and imple-

ment Aircraft Maintenance Cost

Reduction initiatives

Provide a forum for airlines to

exchange/share knowledge, best

practices and industry know-how

(Lean Six Sigma, outsourcing

trends, etc.), as well as to net-

work in the airline Maintenance

world

Organize IATA’ s annual Mainte-

nance Cost Conference with

airline industry experts, OEMs

and MROs.

Contact

Website: www.iata.org/mctf

Email: [email protected]

Geraldine CROS

Operational Cost Manager,

IATA Operations

CONTRIBUTORS

ACMG’s STEERING COMMITTEE

MEMBERS

The ACMG’s Steering Committee (SC) is made up of Member Airlines, IATA represent-atives and Strategic Partners.

Up to 10 Airlines can have seats on this Steering Committee, including Chairman and Vice Chairman, for a 2-year mandate.

ACTIVITIES

The SC collaborates to define efficient ways to monitor cost structures and trends (KPIs and metrics) as well as cost management best practices.

The SC may also initiate cost-related surveys to investigate the most relevant cost driv-ers.

Standard definitions and data collection toolset are debated amongst the committee members.

The committee communicates by email on a regular basis, and will hold telephone con-ferences and/or face-to-face meetings at least once a year.

BENEFITS FOR MEMBERS

Be an active member of a worldwide airline industry community

Be updated with the industry trends in terms of cost performance, cost monitoring and cost management

Get the opportunity to network with airline industry professionals involved in finance and cost management, and exchange experience and best practices

PARTICIPATION

Membership to the ACMG and its Steering Committee is open to all airlines, including cargo, charter and low cost carriers, one last spot available!

Visit ACMG website (www.iata.org/ACMG) and download the nomination form

Contact ACMG at [email protected] to submit the completed nomination form

We look forward to having you onboard!

Klemen FERJAN

Cost Management Consultant,

IATA Operations

Steering Committee formed in 2013, consists of 9 airline members:

Chairman, Josua du Plessis, SAA

Vice-Chairman, Ramanpreet Boparai / Dimitrios Tziortzis, Air Canada

Larry Gibbons, Atlas Air

Hassan Mohamed, Egyptair

Valdimar Bjornsson, Primera Air

Ashraf Suleman, Saudi Airlines

Luis Miguel Pestana Rosa, TAP Portugal

Faik Ozan Dulger, Turkish Airlines

Yuliya Gerasymchuk, Ukraine International Airlines

Airline Cost Management Group (ACMG) Enhanced Report - Sep 2014

42

ACMG DEVELOPMENTS

AIRLINE COST CONFERENCE

The 2nd Airline Cost Conference in Geneva was a great success with more than 30 airlines participating from around the world.

You may check here to enjoy all the presentation material.

Stay tuned for 2015 ACMG campaign

We will start collecting FY2014 data early March

The memberships are expected to increase up to 70 airlines

The Steering Committee is presently at 9 members, please contact us for the last available spot