alignment of management control system to corporate ...pertanika.upm.edu.my/pertanika papers/jssh...

TRANSCRIPT

Pertanika J. Soc. Sci. & Hum. 8(2):91 - 102 (2000) ISSN: 0128-7702© Universiti Putra Malaysia Press

Alignment of Management Control System to Corporate CompetitiveOrientation: Some Empirical Evidence in Malaysia

FOONG SOON YAUGraduate School of Management

Universiti Putra Malaysia43400 UPM Serdang, Selangor, Malaysia

Keywords: management control system; accounting control measures; management practices;corporate strategies; intensity of competition; competitive priority or orientation

ABSTRAK

Dengan perubahan pantas dan persaingan yang begitu hebat di persekitaran, peranan sistemkawalan pengurusan di sesuatu organisasi dalam penyediaan maklum balas maklumat kepadapihak pengurusan untuk mengawas keberkesanan dan kesesuaian strategi persaingannya untukmencapai matlamatnya menjadi lebih mustahak. Kajian ini meninjau cara penggunaan pelbagaikaedah kawalan pengurusan dan kesepadanan kaedah kawalan ini dengan keutamaan atauorientasi persaingan firma-firma. Satu soal selidik disediakan dan dikirim secara rawak kepada 250organisasi di Lembah Klang. Sebanyak 93 borang soal selidik dipulangkan dan dianalisis.Keputusan kaijian ini menunjukkan bahawa pada keseluruhannya, organisasi-organisasi berpendapatpersaingan berasaskan harga, kualiti, dan perkhidmatan/promosi keluaran mereka adalah lebihhebat dibandingkan dengan persaingan berasaskan kepelbagaian dan inovasi keluaran. Selarasdengan pendapatan mereka ten tang kehebatan persaingan, keutamaan atau orientasi persainganmereka juga lebih menumpukan kepada persaingan berasaskan harga rendah, kualiti atauperkhidmatan yang tinggi dan kurang menumpukan kepada kepelbagaian dan inovasi keluaran.Penggunaan di antara kawalan perakaunan dan amalan pengurusan moden untuk mengawas,menilai dan mengawal aktiviti organisasi adalah lebih kurang seimbang, kecuali terdapat kawalankewangan melalui perbandingan prestasi sebenar dengan belanjawan luas digunakan. Perusahaankecil menubuhkan sistem kawalan pengurusan secara kurang formal dan mereka juga tidakbegitu mementingkan penggunaan kaedah kawalan pengurusan jika dibandingkan denganperusahaan besar. Bukti ketidaksepadanan penggunaan sebahagian kaedah kawalan pengurusanditandakan dalam kajian ini. Implikasi keputusan kajian ini dibincangkan.

ABSTRACT

With the rapidly changing and increasingly more competitive environment, the role of amanagement control system (MCS) in an organization in providing information feedback tomanagement for monitoring the effectiveness and appropriateness of the organization's competitivestrategy to achieve its goals is becoming more important. This study examines the extent of usageof various management control measures and the compatibility of these control measures with thecompetitive priorities or orientations of firms. A structured questionnaire was prepared andrandomly sent to 250 organizations in the Klang Valley, A total of 93 usable responses wereanalyzed. The results show that organizations, generally, perceived competition based on productprice, quality and service/promotion to be more intense than that based on product variety andinnovation. Consistent to their perceived intensity of competition, their competitive priorities ororientations also stressed more highly on competition based on low price, high quality andservice, with a much lower emphasis on wide product variety and product uniqueness. Except foran apparent pervasive high usage of the "budget vs. actual" financial control measure, there wasa fairly balanced usage of accounting-based controls and modern management practices formonitoring, evaluating and controlling the organizational activities. Small enterprises tended toadopt less formal management control systems and had less extensive usage of the various control

Foong Soon Yau

measures than the large firms. Evidence of a lack of proper alignment or incompatibilities in theusage of certain management control measures was indicated in this study. The implications ofthe findings are discussed.

INTRODUCTIONThe advancements in information technologyand the imminent trend towards tradeliberalization (or globalization) have significantlychanged the environment in which businessesnow operate and intensified competition in themarket place. As a consequence, new competitivestrategies are being formulated andorganizational structures, as well as the relatedmonitoring and control systems, are continuouslymodified to support the new strategies. In thepast when business environment was relativelystable and competition was minimum, themanagement control system (MCS) was designedto rely heavily on accounting or cost informationto monitor and control cost efficiency of dailyoperating activities. The traditional managementaccounting control system with its high emphasison accounting and cost control measures,generally, loses its robustness when the businessenvironment becomes less stable and moreuncertain (Otley 1980). Management controlsystem has to play a more strategic role in thecurrent rapidly changing and highly competitivebusiness environment. Its major role is toeffectively monitor the organization's strategyimplementation and progress, and to provideinformation feedback on the appropriateness ofthe existing strategies for attainment of theorganization's goal(s). There is evidence thatbusiness enterprises, which match their internalstructures and control systems with theirstrategies, may achieve high performance(Govindarajan and Gupta 1985; Chenhall 1997).

Empirical evidence on the effects of strategyon management control systems or how thesecontrol systems influence strategy and specifically,how top management could organize and usethe control systems to assist the attainment ofthe corporate goals or objectives, is still scarce(Simons 1990). In fact, empirical studies on this

issue only began to emerge in the 1990s(Langfield-Smith 1997).

With the growing interest in the relationshipbetween management control system andstrategy, the definition of management controlshas been broadened to encompass both theaccounting-based and non-accounting-basedcontrols that are instituted for the attainment oflong-term strategic goal(s) of an organization.Most of the literature on the effect of strategyon the design of management control system orvice versa has been normative in nature (Milesand Snow 1978; Porter 1980; Miller and Friesen1982). Relatively few studies have examined theempirical relationships between corporatecompetitive priority or orientation and usage ofmanagement control measures or practices inthe lesser-developed economies, like Malaysia1,Besides, the existing empirical evidence on therelationships between strategy types andmanagement control system attributes, andenvironmental characteristics is generally limited,mixed and inconclusive (Sim and Teoh 1997;Langfield-Smith 1997). With the impendingthreats arising from globalization of the marketplace, management of business enterprises musttake heed of the need to design the "right"management control systems to manage theiremerging strategies for competitive advantage inthe new environment (Simons 1990). This isespecially critical for firms in the lesser-developedcountries due to their relative disadvantages inboth financial resources and human skills. Aproper matching of management control systemand competitive strategy is necessary to enablethe management of an organization to obtainthe relevant information feedback to gauge theappropriateness of its corporate competitivestrategy and to use the formal control feedbackprocesses to modify its existing strategy. Thisstudy aims to provide some empirical evidence

1 Chung (1996) and Sim and Teoh (1997) examined the relationships between management control system attributesand business strategy type based on Miles and Snow's (1978) categorization. Chung's study focused on theelectronics and electrical firms in Singapore; while Sim and Teoh's study was a comparative study of Australian,Singapore and Malaysian firms. This study differs from these two studies in that the current study examines forevidence of compatibility or incompatibility between a firm's competitive priority or orientation and its usage ofmanagement control measures or practices.

Pertanika J. Soc. Sci. & Hum. Vol. 8 No. 2 2000

Alignment of Management Control System to Corporate Competitive Orientation: Some Empirical Evidence in Malaysia

on the extent of usage and compatibility ofmanagement control measures or practices inrelation to the competitive priorities ororientations of firms in Malaysia.

LITERATURE REVIEW

The growing interest in the relationship betweenmanagement control system and strategy arisesfrom the awareness that environment and strategyare important determinants of the managementcontrol system used in an organization. Toillustrate the need to modify the traditionalcontrol system when environment changes,Hoque and Hopper (1994) provided empiricalevidence, which suggests that the standard costingsystems and variance analysis are ineffective andirrelevant in times of environmental uncertainty.The traditional type of management controlsystem design, very often, is used as organizationaldefensive routines to protect and continueexisting practices, regardless of changes in theenvironment. The traditional device ofmonitoring performance using financial budgetsmay not only be ineffective, but also may evenbe "anti-learning" (Argyris 1990), when budgetsor standards are made easily achievable to coverup fundamental problems and to continue pastinefficiencies. The accounting-based controlsystem, however, can be designed to play asignificant integrative role to resolve internalconflicts and facilitate flow of pertinentinformation, such as relevant product costingdata and benchmarking information oncompetitors' relative performance, to arouseawareness of impending external threats anddrive the need for organizational change.

Earlier research studies focus the natureand role of management control systems indifferent organizational types. Miles and Snow(1978) provided descriptions of control systemattributes of organizations following a defender-like strategy and those of organizations followinga prospector-like strategy. Due to the stableenvironment that a defender firm is expected tooperate in, its control system is typicallycharacterized by centralized decision-making withformalized job descriptions and standardoperating procedures. A defender firm adopts acompetitive pricing strategy and hence,emphasizes heavily on cost controls and otherefficiency matters. Porter (1980) also suggestedthat tight cost controls were appropriate forfirms, which followed a cost leadership strategy.

In contrast, a prospector firm tends to have aflexible structure to enable it to respond rapidlyto changes in its environment. Jobs in aprospector firm are normally broadly definedand standard operating procedures are oftenfew in order to encourage innovation. Controlin a prospector firm tends to be decentralizedand the firm is very much results oriented.Similarly, Porter (1980) associated firms, whichwere pursuing the differentiation strategy, toheavy reliance of control through coordination,rather than on formal accounting-based controls,to encourage creativity and innovation. Chung(1996) found that defender firms and prospectorfirms placed different emphasis on control systemattributes and his results were congruent withresults of studies in other cultures. However,Sim and Teoh (1997) reported that severalenvironmental and control system attributesdiffered by national context in their discriminantfunctions that was used to classify firms into thethree Miles and Snow's (1978) strategiccategories.

Research interests later were extended tostudies that examined empirically for systematicrelationships between specific attributes of themanagement control system and a particularcorporate strategy. Daniel and Reitsperger (1991)examined on how the management controlsystems of Japanese automotive manufacturersand consumer electronics companies weremodified to complement and support their totalquality or zero-defect strategy. They found thatmanagers adhering to zero defect strategy weremore frequently provided with informationfeedback on achievement of quality goals, rejectsand downtime than those managers, who wereonly adhering to economic conformance level.This finding supports their proposition that thecorporate strategy that focuses on continuousimprovement and reduction of defective unitshas to be complemented by frequent feedbackon achievement of the combined goals to fostereffective quality improvements. The competitiveinroads experienced by Japanese automotive andconsumer electronics firms in the global marketmay be a consequence of the consistency oralignment between their strategy on productquality and their management control system'sattributes. This is in accord with the claims byHiromoto (1988) that Japanese managementaccounting systems are designed to influenceemployees to behave in accordance with the

Pertanika J. Soc. Sci. & Hum. Vol. 8 No. 2 2000 93

Foong Soon Yau

corporate long-term strategic goals, rather thanto keep accurate product cost information. Inanother study by Ittner and Larcker (1997), whoexamined management control practices in theautomotive and computer industries in Canada,Germany, Japan and the United Sates, it wasfound that quality-related strategic controlpractices tended to be used more extensively inorganizations that followed quality-orientedstrategy than organizations with different strategicorientations. However, their hypothesis thatorganizations, which have aligned their strategiccontrol practices more closely to their competitivestrategies, achieve higher performance only hasmixed support. The effects of some strategiccontrol practices on performance were found tovary with industry and several strategic controlpractices even exhibited negative relationshipswith performance. Perera, Harrison and Poole(1997) also found support for a significantassociation between customer-focus strategy andthe use of non-financial performance measures,an attribute of management control system.However, they too found that the performanceof organizations that pursued customer-focusstrategy was not significantly linked to anincreasing use of non-financial performancemeasures. The lack of a significant relationshipbetween corporate performance andmanagement control attributes might be due tothe lagging effect and limitation of using apoint-in-time measure for organizationalperformance.

Khandwalla (1972) provided the firstempirical evidence of the relationship betweenmanagement control systems and level ofcompetition, a critical determinant of the natureof strategy adopted by an organization. He founda strong positive relationship between theintensity of competition and reliance on theformal accounting control systems. Although,his study did not explicitly consider the natureof strategy adopted by organizations, but it isimplicit that organizations that face intensecompetition are likely to adopt strategies of aprospector (Miles & Snow 1978) or adifferentiator (Porter 1980). In view of that,Langfield-Smith (1997) opined that the formalaccounting controls examined in Khandwalla'sstudy were not those consistent with theprospector type of organizations that emphasizedon flexibility and innovation, and hence, implyingthat Khandwalla's study did not consider the

compatibility of those controls in supporting aparticular strategy or level of competition. Severalother empirical studies (Chung 1996: Mak 1989),however, provided evidence that was consistentwith Khandwalla's study. Prospector firms werefound to be associated with more sophisticatedand frequent use of operational controls,including cost controls, than the defender firmsbecause of the greater uncertainties faced by theprospector firms.

The increasing competition and theaccelerating technological changes have led tothe establishment of more flexible organizationalstructures to facilitate rapid responses to changesin market demands. The change is necessarybecause the traditional hierarchicalorganizational structures that focus onbureaucracy and activities by individualdepartments or units tend to dampen employees'initiatives and innovations (Bartlett and Ghoshal1993). The management control systems in thenew organizational models that haveincorporated a greater level of employeeempowerment and a flatter or networkorganizational structure are expected to play anintegrative role that focus on the contributionsand interrelationships of units within thoseorganizations. Modern management practices,such as total quality management, businessprocesses re-engineering, employeeempowerment, cross-functional work teams andadoption of non-financial performance measures,are increasingly being adopted to complementthe traditional accounting-based controls, to meetthe serious challenges posed by the uncertaintiesand turbulence in the external environment.The flatter organizational structure and anenhancement in employee empowerment havemade the traditional hierarchical responsibilitycenter reporting system less necessary. Non-financial performance indicators, such as thosesuggested in the balanced scorecard concept(Kaplan and Norton 1992), are increasingly beingincorporated to complement the traditionalfinancial performance indicators to effectivelyassess the performance of the critical successfactors of organizations

The earlier studies provided empiricalevidence that firms in the more developedcountries generally adapted their managementcontrol practices to changes in their corporatestrategies. Most of the control measuresexamined were, however, accounting-based

94 Pertanika J. Soc. Sci. & Hum. Vol. 8 No. 2 2000

Alignment of Management Control System to Corporate Competitive Orientation: Some Empirical Evidence in Malaysia

controls. This study examines empirically therelationships between types of control practices(both accounting-based and modernmanagement practices) and competitive prioritiesor orientations of firms in Malaysia. The findingswould provide further empirical evidence onthe adaptability of management control practicesto changes in the competitive orientations offirms in the lesser-developed country likeMalaysia.

RESEARCH METHODOLOGYData Collection

A structured questionnaire was prepared andpre-tested on several practising managers toensure clarity of terms used. Two hundred andfifty copies were sent to managers and executivesof a randomly selected sample of organizationslocated in the Klang Valley. A total of 93 (37.5%)completed and useable questionnaires werereturned and analyzed.

The questionnaire was divided into threesections: Section A requested for backgroundinformation on the organization and therespondent, Section B focused on the attributesof the organization's management control systemand the extent of usage of those control measuresor practices; Section C required a respondent torate, on a 5-point Likert scale, the perceivedintensity of five different types of competitionfaced by his or her organization andconsequently, their perceived importance of thecorresponding five types of competitive prioritiesor orientations.

The types of competition examined in thisstudy were based on the three of types ofcompetition in Khandwalla's (1972) study, exceptthat Khandwalla's product competition wasfurther segregated into product quality, varietyand innovation. With this modification, the fivetypes of competition examined in this studywere product price, quality, variety, innovationand service/promotion. The competitive priorityor orientation in this study was defined as afirm's emphasis in its competitive strategy toachieve its competitive advantage and this isconceptually similar to Khandwalla's measure ofimportance of each type of competition to a

firm's profitability. Each of the five types ofcompetition was related to a competitive priorityor orientation. For example, when a firmperceives a high intensity of competition in price,it is expected that the firm would place a highpriority (or orientation) in formulating a lowproduct price competitive strategy. A total oftwelve management control measures or practiceswere listed2. Six of the management controlmeasures or practices were accounting-basedcontrols, such as use of financial budgets,standard cost variances and discounted cash flowtechniques; while the other six were modernmanagement control practices, such as totalquality management, business process re-engineering, employee empowerment and inter-departmental work-team.

RESULTS AND DISCUSSIONProfiles of Respondents and Organizations

The profiles of respondents and theirorganizations are summarized in Table 1. About88.6% of the participating organizations wereincorporated enterprises or limited companies.All limited companies in Malaysia are requiredlegally to comply with stringent record-keepingand corporate disclosure or governanceregulations. Most of the participating firms(46.2%) were from the manufacturing sectorwith services sector firms constituted 34.4% ofthe sample and more than two thirds of theorganizations were Malaysian-owned enterprises.As for the respondents, more than 60% of therespondents held middle or senior managementpositions and about 90% of the respondents hadeither tertiary or professional qualification.

Perceived Intensity of Competition and CompetitivePriorities or Orientations

The mean rating scores (and standard deviations)of the perceived intensity of the five types ofcompetition, as well as those for the perceivedimportance of the corresponding competitivepriorities or orientations are presented in Tables2 and 3, respectively. On overall, the respondentsperceived competition in product quality to bemost intense and consistently, they ratedproducing high quality product to be their most

2 The control measures or practices were adopted from measures used in Khandwalla's study as well as those modernmanagement practices discussed in the management literature. Respondents, however, were also allowed to stateother management control practices used in their organizations.

Pertanika J. Soc. Sci. 8c Hum. Vol. 8 No. 2 2000 95

Foong Soon Yau

TABLE 1Profiles of respondents and organizations

Position held:Senior management levelMiddle management levelJunior management level

Age:< 30 years30 -45 years> 45 years

Qualification:TertiaryProfessionalOthers

Industrial Sector:ManufacturingServicesOthers

Number of Employees:< 100100 - 500>500

Ownership:LocalForeign

18.2%44.3%37.5%

37.2%56.4%6.4%

52.7%37.4%9.9%

46.2%34.4%19.4%

30.9%45.7%23.4%

69.8%30.2%

important competitive priority or orientation. Ascan be seen from Table 3, the correlationbetween the intensity of each type of competitionand importance of the correspondingcompetitive priority or orientation was highlysignificant ( p < 0.001), except that for theproduct service and promotion competitivepriority or orientation.

TABLE 2Mean rating scores and standard deviations of

perceived intensity of the five types of competition

Type of Competition MeanRatingScore

StandardDeviation

Product Quality 4.48 0.70Product Price 4.05 0.94Product Service & Promotion 3.90 1.12Product Uniqueness 3.82 1.07Product Variety 3.66 1.11

Scale: l=very low; 5= very high

Analysis of the perceived intensity ofcompetition by industry type generally shows thesimilar ranking as that in Table 2 for themanufacturing and the services sectors. Firms inthe "other" sector, however, ranked intensity ofprice competition to be more intense thanproduct quality. The firms in the "other" sectorincluded several commodity-type firms, such asfirms in the plantation sector and oil and gassector. Despite of their higher perceived intensityof competition on price, firms in the "other"sector were, however, consistent with firms inthe manufacturing and services sectors in rankingproducing high product quality as their mostimportant competitive priority. Local-owned firmsperceived competition in product service/promotion to be more intense than the foreign-owned firms (4.07 vs. 3.61; F=2.987; p=0.088).Generally, the rating scores of the large firmsfor both the perceived intensity of each type of

TABLE 3Mean rating scores, standard deviations and correlations of perceived importance

of five competitive priorities or orientations

Competitive Priority or Orientation

High Product QualityGood Customer Service & PromotionLow Product PriceWide Product VarietyHigh Product Uniqueness

MeanRatingScore

4.614.173.873.853.74

StandardDeviation

0.730.901.021.171.17

Correlation withthe Corresponding

Intensity ofCompetition

0.516**0.1660.66**0.703**0.522**

Scale: l=very unimportant; 5=very important** significant at 0.01

PertanikaJ. Soc. Sci. & Hum. Vol. 8 No. 2 2000

Alignment of Management Control System to Corporate Competitive Orientation: Some Empirical Evidence in Malaysia

competition and the perceived importance ofthe corresponding competitive priority werehigher than those of the small firms. However,the differences were not statistically significant.

Management Control Measures or PracticesThe twelve control items were classified intoeither accounting-based controls or modernmanagement control practices. Items 1 to 6 inTable 4 were the accounting-based controls; whileitems 7 to 12 were the management controlpractices. The average of the mean scores of thesix accounting-based controls3 was higher thanthat for the management control practices4 (3.20vs. 3.00). A closer analysis of the mean scores inTable 4, however, indicates that there was afairly balanced usage of accounting-basedcontrols and modern management control

practices, except for an apparent pervasive highor extensive usage of the budget vs. actual controlmeasure, which was the only control measurewith a mean rating score above 4.00. Besidesbudget vs. actual, there were two other accounting-based controls, namely Internal Audit andResponsibility Reporting, with mean rating scoresabove 3.00; while in the modern managementpractices category, there were four measures,namely empowerment, inter-departmental work team,TQM and non-financial measures, with mean ratingscores above 3.00. This finding suggests that thefirms, as a whole, are using a combination ofaccounting-based controls and non-accountingmodern management practices to monitor andcontrol their operations, as suggested in themanagement literature.

TABLE 4Mean rating scores and standard deviations of management

control measures or practices

Type of Control Measure or Practice Mean RatingScore

Accounting-Based Controls:1. Budget vs. Actual2. Internal Audit3. Responsibility Reporting4. Flexible Budgeting5. Standard Cost Variances6. Discounted Cash Flow Techniques

Modern Management Practices:7. Inter-departmental Work Team8. Empowerment9. Total Quality Management (TQM)10. Non-Financial Measures11. Business Process Re-engineering (BPR)

12. Economic Order Quantity (EOQ)

Overall Accounting-Based Controls

Overall Management Control Practices

3.20

3.00

Scale: l=very low; 5=very high

StandardDeviation

4.083.343.292.892.872.64

3.313.313.063.042.692.61

1.031.271.161.161.171.26

1.100.871.141.141.111.24

0.74

0.75

3 The measure of the overall accounting controls was a composite measure, which was computed based on the meanrating scores of the six accounting-based controls. The reliability analysis of this overall measure showed a Cochran'salpha of 0.7041.

4 The measure of management control practices was a composite measure, which was computed based on the meanrating scores of the six management control practices. The reliability analysis of this overall measure showed aCochran's alpha of 0.7642.

Pertanika J. Soc. Sci. & Hum. Vol. 8 No. 2 2000 97

Foong Soon Yau

Relationships Between Competitive Priorities orOrientations and Management Control Measuresor Practices

The results of the correlations between themanagement control variables and competitiveorientations are summarized in Table 5 and theyindicate a few instances of lack of properalignment or incompatibilities as discussed below.

Low Product Price Competitive OrientationFirms with a high priority for low product priceas a competitive strategy are expected toemphasize highly on accounting-based controlsto manage cost efficiency. Contrary toexpectation, the correlation coefficients in Table5 show that firms with high competitive priorityor orientation for low product price wereassociated with low usage of four of the fiveaccounting-based controls, namely discounted cashflow techniques, internal audity standard cost variancesand responsibility reporting. Budget vs. actual wasthe only accounting-based control that waspositively correlated to low product price orientationand even then the association was not statisticallysignificant. These firms with a high priority forlow product price were also associated with lowusage of all of the five modern managementcontrol practices. The association of low productprice competitive priority with the overall usageof modern management control practices wasnegative and significant (r = -0.197; p< 0.05).The two specific modern management practicesthat exhibited significant negative relationshipswere business process re-engineering (BPR) and inter-departmental work-teams. BPR is used in activityanalysis to eliminate non-value added activitiesto improve cost efficiency and yet this approachwas seemingly "unpopular" with firms whosecompetitive priority was to compete based oncost efficiency.

High Product Quality Competitive OrientationFirms with a high priority for product quality areexpected to be positively associated with usageof Total Quality Management (TQM). This studyfound a positive association between priority forproduct quality and usage of TQM, but therelationship was not statistically significant. Theoverall association between this product qualityorientation and the extent of usage ofaccounting-based controls and that of modernmanagement control practices were positive, butnot statistically significant.

Wide Product Range and Product UniquenessCompetitive Orientations

Firms with a high priority for either wide productrange or product uniqueness are likely to be theprospector type of organizations that emphasizeon flexibility and innovation. Table 5 shows thatthese firms were significantly associated with ahigh usage of control practices, irrespective ofwhether accounting-based controls or modernmanagement practices. The finding of a highlysignificant association with flexible budgetingmeasure suggests that firms with high priorityfor wide product range or product uniquenessare aware of the need to constantly revise theirbudgets to reflect changes in the environment.A high emphasis on budget vs. actual inperformance evaluation, however, couldinfluence managers to favour short-term profitsat the expense of long-term competitiveadvantage. The highly significant associationbetween firms with product variety or innovationorientation and usage of discounted cash flowtechniques for evaluating investment projectproposals in these firms may also be incompatiblewith the notion that the traditional financialappraisal techniques are inappropriate forappraisal of certain strategic investment projects,which are very long-term in nature and whosefuture economic benefits are difficult to predictor ascertain. The need to satisfy the conventionalfinancial criteria under discounted cash flowtechniques often result in radical innovations beingunfairly inhibited and discouraged (Finnie 1998).

Good Sales Service & Promotion Competitive OrientationFirms with a high priority for good sales serviceand promotion, generally, exhibited positiveassociations with usage of both the accounting-based controls and modern managementpractices. The significant negative associationwith usage of inter-departmental work team suggeststhat firms with a high priority for good salesservice and promotion may be still veryhierarchical in their setups. The criticism for thetraditional hierarchical structure is that itsbureaucracy delays decision-making process andas a consequence, the firm is not likely to bevery responsive to changes in customers' needs.Inter-departmental work team aims to facilitatedecision-making by having team members fromvarious functional areas to jointly respond to thechanging demands of the markets.

98 PertanikaJ. Soc. Sci. & Hum. Vol. 8 No. 2 2000

Alignment of Management Control System to Corporate Competitive Orientation: Some Empirical Evidence in Malaysia

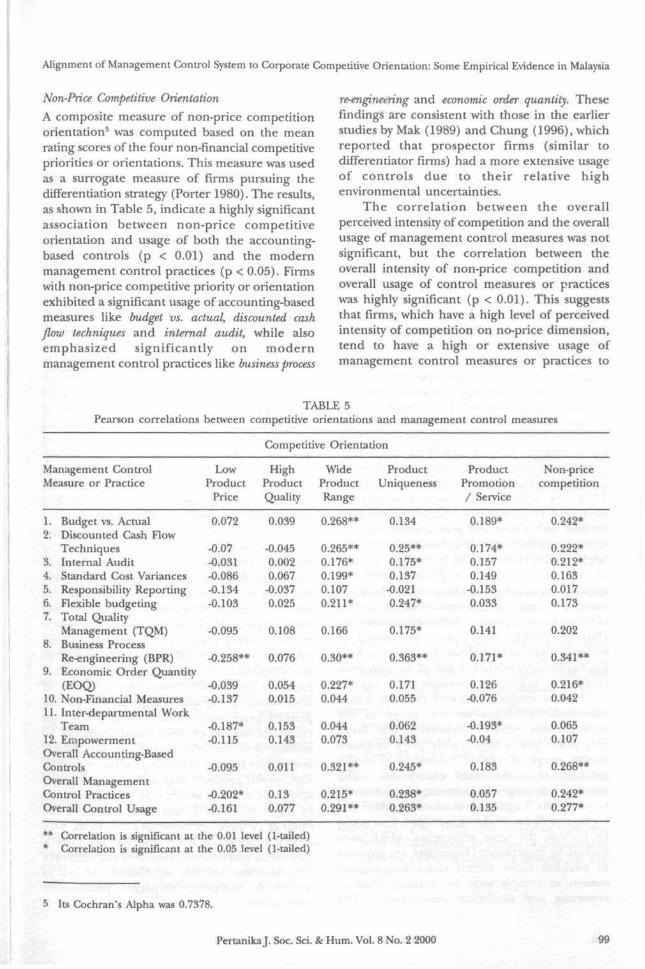

Non-Price Competitive Orientation

A composite measure of non-price competitionorientation5 was computed based on the meanrating scores of the four non-financial competitivepriorities or orientations. This measure was usedas a surrogate measure of firms pursuing thedifferentiation strategy (Porter 1980). The results,as shown in Table 5, indicate a highly significantassociation between non-price competitiveorientation and usage of both the accounting-based controls (p < 0.01) and the modernmanagement control practices (p < 0.05). Firmswith non-price competitive priority or orientationexhibited a significant usage of accounting-basedmeasures like budget vs. actual, discounted cashflow techniques and internal audit, while alsoemphasized significantly on modernmanagement control practices like business process

re-engineering and economic order quantity. Thesefindings are consistent with those in the earlierstudies by Mak (1989) and Chung (1996), whichreported that prospector firms (similar todifferentiator firms) had a more extensive usageof controls due to their relative highenvironmental uncertainties.

The correlat ion between the overallperceived intensity of competition and the overallusage of management control measures was notsignificant, but the correlation between theoverall intensity of non-price competition andoverall usage of control measures or practiceswas highly significant (p < 0.01). This suggeststhat firms, which have a high level of perceivedintensity of competition on no-price dimension,tend to have a high or extensive usage ofmanagement control measures or practices to

TABLESPearson correlations between competitive orientations and management control measures

Competitive Orientation

Management ControlMeasure or Practice

Low High Wide Product Product Non-priceProduct Product Product Uniqueness Promotion competition

Price Quality Range / Service

1. Budget vs. Actual 0.072 0.039 0.268** 0.134 0.189* 0.242*2. Discounted Cash Flow

Techniques -0.07 -0.045 0.265** 0.25** 0.174* 0.222*3. Internal Audit -0,031 0.002 0.176* 0.175* 0.157 0.212*4. Standard Cost Variances -0.086 0.067 0.199* 0.137 0.149 0.1635. Responsibility Reporting -0.134 -0.037 0.107 -0.021 -0.153 0.0176. Flexible budgeting -0.103 0.025 0.211* 0.247* 0.033 0.1737. Total Quality

Management (TQM) -0.095 0.108 0.166 0.175* 0.141 0.2028. Business Process

Re-engineering (BPR) -0,258** 0.076 0,30** 0.363** 0.171* 0.341**9. Economic Order Quantity

(EOQ) -0.039 0.054 0.227* 0.171 0.126 0.216*10. Non-Financial Measures -0.137 0.015 0.044 0.055 -0.076 0.04211. Inter-departmental Work

Team -0.187* 0.153 0.044 0.062 -0.193* 0.06512. Empowerment -0.115 0.143 0.073 0.143 -0.04 0.107Overall Accounting-BasedControls -0.095 0.011 0.321** 0.245* 0.183 0.268**Overall ManagementControl Practices -0.202* 0.13 0.215* 0.238* 0.057 0.242*Overall Control Usage -0.161 0.077 0.291** 0.263* 0.135 0.277*

** Correlation is significant at the 0.01 level (1-tailed)* Correlation is significant at the 0.05 level (1-tailed)

5 Its Cochran's Alpha was 0.7378.

Pertanika J. Soc. Sci. & Hum. Vol. 8 No. 2 2000 99

Foong Soon Yau

monitor performance. This finding is partlyconsistent to that reported in Khandwalla (1972),who found a significant positive relationshipbetween overall competition and the overallusage of controls with price competition havingthe least impact on usage of controls and productcompetition showing the greatest impact. Heattributed that to the increasing expected netbenefits from application of controls ascompetition intensified and the increase inexpected net benefits was more evident withincreasing product competition. This study didnot find an overall significant positiverelationship between overall intensity ofcompetition and usage of controls because ofthe negative relationship between intensity ofprice competition and overall usage of controls.

From the analysis by type of competitivepriority or orientation, the apparent lack ofproper alignment or incompatibilities may besummarized as follows. Firms with a highcompetitive priority for low product price did notexhibit an extensive or high usage of accounting-based controls. Even though firms with a highcompetitive priority or orientation for high productquality did exhibit a positive association usage ofTQM, the relationship was not statisticallysignificant. Firms with high competitive prioritiesfor wide product range and product uniqueness usedextensively some accounting-based controls thatmight inhibit creativity and innovation. Despiteof the trend towards a greater employeeempowerment and greater usage of non-financialmeasures to monitor the critical success factorsof firms pursuing product differentiation strategy(Porter 1980), the usage of employeeempowerment and non-financial measures werenot significantly related to any of the non-pricecompetitive priority or orientation.

Further analysis indicated that size had asignificant influence on the usage of themanagement control measures. The largeenterprises had a significantly more extensiveoverall usage of control measures (F=3.677;p=0,029) than the small enterprises. Thedifference in usage of accounting-based controlsbetween the large and small enterprises washighly significant (F=3.399; p=0.038). This mightbe because the large enterprises, which werelikely to be incorporated businesses, are requiredto establish more formal accounting controlsystems to comply with the existing financialreporting and disclosure requirements. The

difference in the usage of modern managementcontrol practices between the large and thesmall enterprises, was, however, only moderatelysignificant (F=2.779; p=0.067).

SUMMARY AND IMPLICATIONS

With the impending threats from globalizationof the market place, businesses have to becomemore agile and responsive to the rapid changesin customers* needs. Competition based on non-price dimension is becoming more prevalent astrade barriers are being removed. Product lifecycle is also becoming shorter and shorter, asmore and more competitors enter the market.Hence, business enterprises are placingincreasing emphasis on speed and responsivenessto satisfy the rapid changing needs of the marketplace, and on innovation to replace the rapiddemise of their existing products and services.This study examines the perceptions oforganizations on the intensity of five types ofcompetition and their competitive orientationsor priorities in response to their perceivedintensity of the different types of competition.The results of this study indicate that theorganizations were competing mainly based onproduct price, quality and service. Productuniqueness or innovation and wide productvariety were rated as the lowest and the secondlowest, respectively, in their list of competitivepriorities. This observation is disturbing becausesurvival in the new environment depends verymuch on the ability of a firm to innovate andextend its range of goods or services to theincreasingly sophisticated and demanding buyersin the market place. This study also foundevidence of a lack of proper alignment orincompatibilities between the use of controlmeasures and certain competitive priorities ororientations. Firms with a high priority for lowproduct price were found not to place highemphasis on accounting-based controls tomanage their cost efficiency. Firms with a highcompetitive priority or orientation for producinghigh quality products were also not significantlyassociated to those with a high or extensive useof TQM and this is not in accord with thefindings in the more developed countries, suchas that reported in Ittner and Larcker (1997).The use of non-financial measures and employeeempowerment was not significantly related toany of the non-price competitive priorities ororientations.

100 Pertanika J. Soc. Sci. 8c Hum. Vol. 8 No. 2 2000

Alignment of Management Control System to Corporate Competitive Orientation: Some Empirical Evidence in Malaysia

The finding of a lack of proper alignmentor incompatibilities between usage of type ofcontrol measures and certain competitivepriorities or orientations of firms suggests thatthere may be deficiencies in the design ofmanagement control systems in these firms andas a consequence, managers in these firms maynot be able to effectively utilize the formal controlprocesses to coordinate and control theiroperating activities to achieve competitiveadvantages, as intended in their firms*competitive strategies. The current study,however, is unable to identify the causes for thelack of alignment or incompatibilities, except toprovide some empirical evidence of the extentof alignment in the usage of managementcontrols to firms* competitive priorities ororientations. With the imminent trend towardsglobalization, the apparent lack of properalignment may be detriment to these firms'abilities to formulate the appropriate strategiesto compete with other world-class players.

Management literature has stressed on theimportance of a strategic fit in the designingtheir management control systems and thesecontrol systems have to be modified when strategychanges in response to environmental changes.Unfortunately, management control systemsoften remain unchanged even thoughcompetitive strategy might have already beenchanged, resulting in incompatibilities as thoseobserved in this study. Although Khandawalla(1972) opined that firms were still far fromdesigning optimal control systems, he, however,reckoned that accountants could help the designof better control systems with properquantification of the intangible costs and benefitsof controls. In order for the designers ofmanagement control systems to be able toevaluate the effectiveness of various controlmeasures, there must be effectivecommunications between the formulators of thenew strategy and the designers of managementcontrol systems to avoid any strategicmisalignment. This is in accord with Simons(1990) who advocated the interactivemanagement control processes, whereby a firm'scompetitive strategic positioning, managementcontrol measures and process of strategyformulation influence one another as the firmevolves and adapts over time, to manage andalign management controls to the emerging

strategy. The implementation of an effectiveinteractive management control process requiresa more open communication structure and freerflow of information within the firm.

REFERENCES

ARGYRIS, C. 1990. The dilemma of implementingcontrols: the case of managerial accounting.Accounting, Organizations and Society 15: 503-512.

BARLETT, C.A. and S. GHOSAL. 1993. Beyond the M-

form: toward a managerial theory of the firm.Strategic Management Journal 14: 23-46.

CHENHALL, R.H. 1997, Reliance on manufacturingperformance measures, total qualitymanagement and organizational performance.Management Accounting Research 8: 187-206.

CHUNG, L.H. 1996. Management control systemsand business strategy: an empirical study ofelectronics and electrical firms in Singapore.Singapore Management Review 18: 39 - 54.

DANIEL, SJ. and W.D. REITSPERGER. 1991. Linking

quality strategy with management controlsystems: empirical evidence from Japaneseindustry. Accounting, Organizations and Society16(7): 601-618.

GOVINDARAJAN, V. and A.K. GUPTA.1985. Linking

control systems in business unit strategy: impacton performance. Accounting, Organizations andSociety 10: 51-66.

HIROMOTO, T. 1988. Another hidden edge -Japanesemanagement accounting. Harvard BusinessReview 66(4): 22-26.

HOQUE, Z. and T. HOPPER. 1994. Rationality,

accounting and politics: a case study ofmanagement control in a Bangladeshi JuteMill. Management Accounting Research 5: 5-30.

ITTNER, CD. and D.F. LARCKER. 1997. Quality strategy,strategic control systems and organizationalperformance. Accounting, Organizations andSociety 22 (3/4): 294- 314.

KAPLAN, R.S. and D.P. NORTON. 1992. The balanced

scorecard - measures that drive performance.Harvard Business Review 70(1): 71-79.

KHANDWALLA, P.N. 1972. The effect of differenttypes of competition on the use of managementcontrols. Journal oj Accounting Research 10: 275- 286.

PertanikaJ. Soc. Sci. & Hum. Vol. 8 No. 2 2000 101

Foong Soon Yau

LANCFIELD-SMITH, K. 1997. Management controlsystems and strategy: a critical review.Accounting, Organizations and Society 22(2): 207-232.

MAK, Y. 1989. Contingency fit, internal consistencyand financial performance. Journal of BusinessFinance and Accounting 16(1): 273 - 300.

MILES, R.E. and C.C. SNOW. 1978. OrganizationalStrategy, Structure and Process. N.Y.: McGraw-Hill.

MILLER, D. and P.H. FRIESEN.1982. Innovation inconservative and entrepreneurial firms: twomodels of strategic momentum. StrategicManagement Journal 3: 1-25.

OTLEY, D.T. 1980. The contingency theory ofmanagement accounting: achievement andprognosis. Accounting, Organizations and Society5: 413 - 428.

PERERA, S., G. HARRISON and M. POOLE. 1997.Customer-focused, manufacturing strategy andthe use of operation-based non-financialperformance measures: a research note.Accounting, Organizations and Society 22(6): 557-572.

PORTER, M. E. 1980. Competitive Strategy. New York:Free Press.

SIM, A.B. and H.Y. TEOH. 1997. Relationshipsbetween business strategy, environment andcontrols: a three country study. Journal of AppliedBusiness Research 13(4): 57- 69.

SIMONS, R. 1990. The role of management controlsystems in creating competitive advantage: newperspectives. Accounting, Organizations and Society12(1/2): 127-143.

102 PertanikaJ. Soc. Sci. & Hum. Vol. 8 No. 2 2000