alternative investment seminar - jll · • obsolescence in retail and office markets / declining...

TRANSCRIPT

Thursday 26th September 2013

Alternative Investment Seminar Focusing on future trends for alternative investments

Welcome & Introduction Chris Ireland UK Chairman & Lead Director - UK Capital Markets

Survey Findings Jon Neale Head of Research - UK

Alternatives Survey…

• Web based

• 46 fund managers and investors responded

• Mix of company or investor types: • 24% pension funds • 22% asset management • 15% insurance • 11% private equity

• Remainder mix of REITs, banks, family offices, mutual funds, property companies

• Roughly two thirds were property specific

• Response bias!

Overview

Funds under management Mix of investor sizes…

Under £500m 17.39%

£500m-£1bn 17.39%

£1bn-£2bn 21.74%

£2bn-£5bn 15.22%

£5bn+ 28.26%

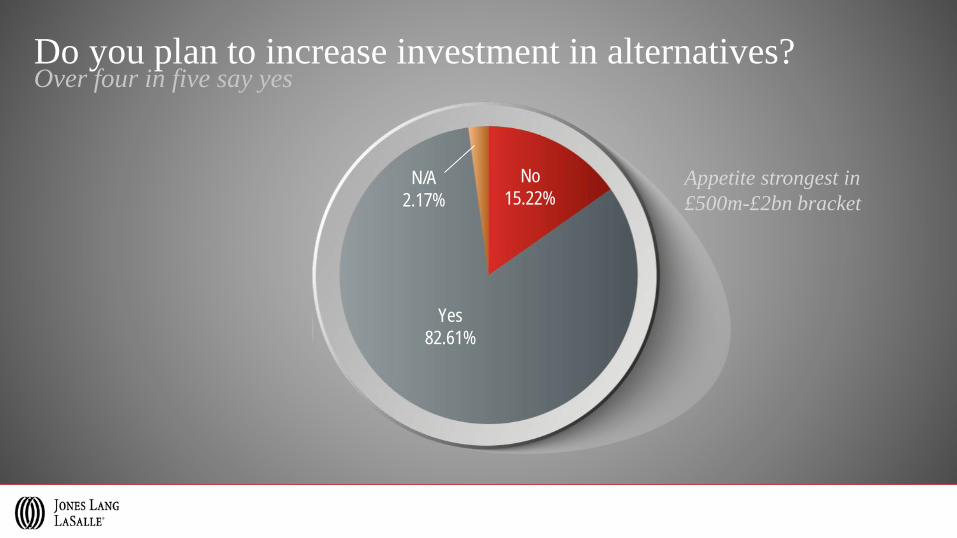

Do you plan to increase investment in alternatives? Over four in five say yes

Appetite strongest in £500m-£2bn bracket

No 15.22%

Yes 82.61%

N/A 2.17%

Why?

• Obsolescence in retail and office markets / declining aggregated demand

• Increased competition for remaining core / prime assets – especially from international investors

• Declining lease lengths in commercial property – alternatives offer long-term income stream

• Income often matched to inflation

• Diversification

• Need for investment in healthcare / infrastructure due to lack of bank and government funding

Key Themes

Why will alternatives become more important? “Stock is becoming increasingly difficult to source in more mature sectors and alternatives diversify risk.”

“Increased competition for conventional commercial property investments, allied with the continued growth in student and retirement accommodation, will see more institutions owning alternative property assets.”

“Structural change is putting pressure on retail and office property in particular, in terms of increasing obsolescence.”

“The long leases offered by the alternative sectors will be integral to maintain the AWUT of portfolios as average lease lengths decline within the traditional commercial sectors.”

“Yes, as many alternative sectors provide long (20 yr+) inflation linked income which is in diminishing supply. Many of the alternative sectors would see revenue/ERV growth in line with RPI unlike some of the conventional main sectors.”

“Requirement from end-investors for more tailored portfolio strategies (e.g. inflation-linked income for de-risking strategies) which alternative sectors offer..”

“Structural change in healthcare and renewables in particular combined with government austerity is likely to drive private sector solutions in these and other sectors.”

“Long term institutional funding is required to fill the void left by banks and the public sector if the demand for "social infrastructure" and housing is to be met. It can provide secure long term cash flows that insurance companies and pension funds need to meet their liabilities.”

“They give investors more investment options and diversity. especially when number of investors focusing on increasing real estate exposure in UK is increasing (e.g. overseas investors are dominating acquisitions in Central London)”

0%5%

10%15%20%25%30%35%40%45%50%

5% 10% 15% 20% 25% 30% 35% 40% 45% 50% 55% 60% 65% 70% 75% 80% 85% 90% 95% 100%

Now 2023

…and what will it be in 10 years’ time? What is your weighting to alternatives now…

Today – 44% indicate a weighting of 5% towards alternatives 2023 – 100% say 10% or more By 2023 25% will have a 15% weighting to alternatives 25% will have 20%-25%

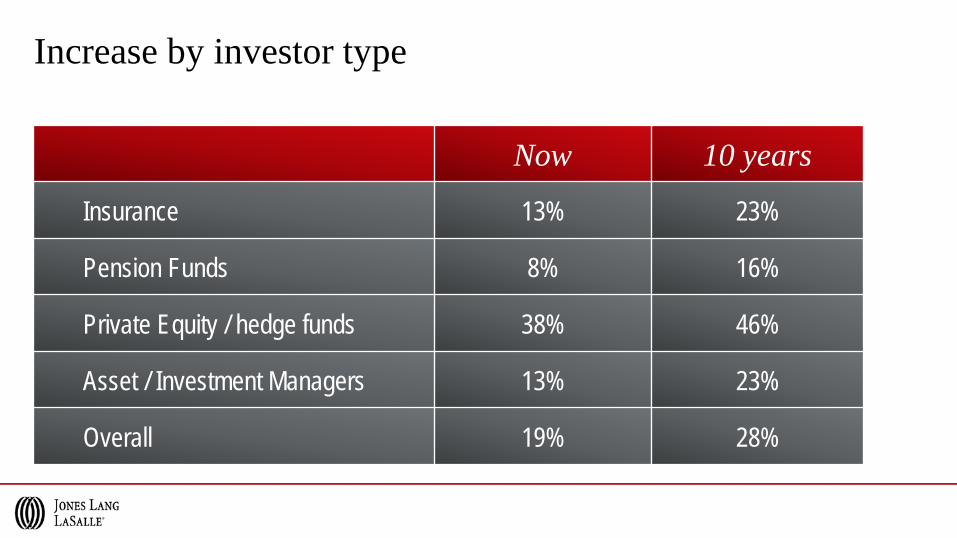

Increase by investor type

Now 10 years

Insurance 13% 23%

Pension Funds 8% 16%

Private Equity / hedge funds 38% 46%

Asset / Investment Managers 13% 23%

Overall 19% 28%

Which sectors will you increase your exposure to?

0% 10% 20% 30% 40% 50% 60% 70% 80%

Student AccommodationPrivately Rented Market Housing

HotelsHealthcare

Conventional commercial real estateRetirement Living

InfrastructureData Centres

Social HousingRenewables

Farmland

But which sectors will see “significant” investment?

0% 5% 10% 15% 20% 25% 30% 35%

Conventional commercial real estatePrivately Rented Market Housing

InfrastructureStudent Accommodation

HealthcareHotels

Social HousingRetirement Living

RenewablesData Centres

Farmland

Which sectors will see disinvestment….?

0% 2% 4% 6% 8% 10% 12% 14% 16% 18% 20%

Conventional commercial real estate

Farmland

Hotels

Renewables

Infrastructure

Data Centres

Healthcare

Student Accommodation

Privately Rented Market Housing

Social Housing

Retirement Living

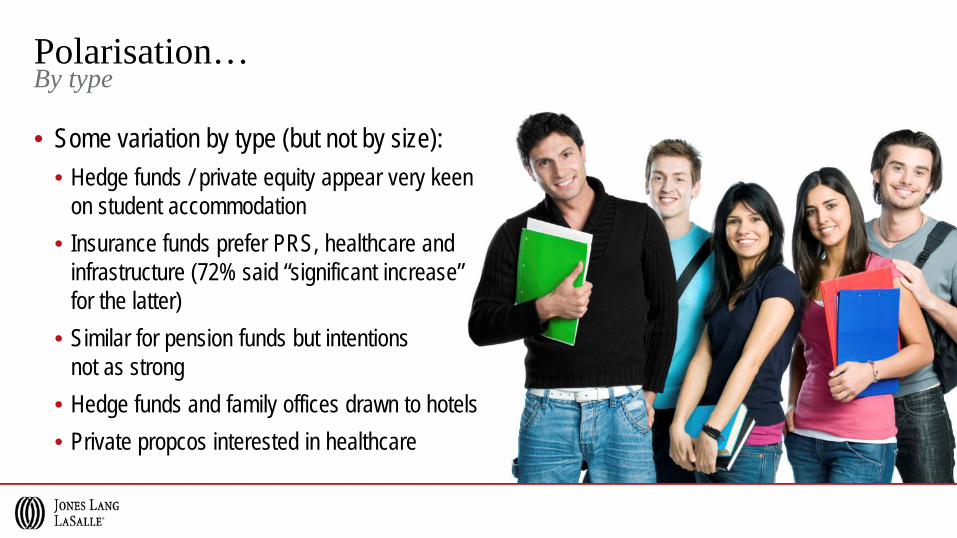

Polarisation

• Half of all multi-asset funds said they would “significantly increase” exposure to conventional commercial real estate • But just 17% of specialist funds

• Almost a quarter (23%) of property-specific funds said they would disinvest from conventional commercial real estate • Compared to only 6% of multi-asset • Investment & Asset management firms seem most likely to want to disinvest

Key Themes

Polarisation…

• Some variation by type (but not by size): • Hedge funds / private equity appear very keen

on student accommodation • Insurance funds prefer PRS, healthcare and

infrastructure (72% said “significant increase” for the latter)

• Similar for pension funds but intentions not as strong

• Hedge funds and family offices drawn to hotels • Private propcos interested in healthcare

By type

What are the risks?

0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0% 70.0%

Lack of liquidity

Exit strategies

Lack of scale

Lack of transparency

Benchmarking issues

Business models

Policy risk

Reputational risk

Data issues

0% 10& 20% 30% 40% 50% 60% 70%

Some themes….

• Pension funds / insurance more concerned about policy and reputational risk

• Hedge funds, banks etc anxious about exit strategies

• Lack of transparency & data issues for asset managers

• Data issues raised by banks & pension funds

Other issues…

• Alternative Use Value

• Management & covenant risk – “dependency on the quality of the operator”

• Lack of knowledge & experience

• “Institutional Inertia” / fear of the unknown

• Stock availability –pricing issues

• Need to understand operational issues

JLL ALTERNATIVES SEMINAR 26 SEPTEMBER 2013

26 SEPTEMBER 2013

Alternative sectors - Fad or Fixture?

Rob Martin, CFA Director of Research, Legal & General Property

JLL ALTERNATIVES SEMINAR 26 SEPTEMBER 2013 21

Agenda

• L&G managed alternative real estate

• Investment case

• Issues / Challenges

• Future direction

JLL ALTERNATIVES SEMINAR 26 SEPTEMBER 2013 22

L&G managing £1.6 billion across c.90 assets

Sector % AUM

Leisure (including Hotels) 7%

Student Accommodation & Education 6%

Residential inc Social Housing 1%

Health & social infrastructure 0.4%

Economic infrastructure 2%

Total 17%

JLL ALTERNATIVES SEMINAR 26 SEPTEMBER 2013 23

The investment case (highlights)

• Accessing liability-matching income streams

• Broadening the real estate universe

• Diversification

• Alignment with structural change

JLL ALTERNATIVES SEMINAR 26 SEPTEMBER 2013 24

Falling gilt yields have put pressure on pension funding

Source: BNY Mellon / Pension Protection Fund / Datastream

Pension Fund Asset Allocation

0

10

20

30

40

50

60

70

80

90

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

% of assets

0

2

4

6

8

10

12

14

16

%Equities (left scale) Fixed Interest 10-yr Gilt Yields (right scale)

JLL ALTERNATIVES SEMINAR 26 SEPTEMBER 2013 25

Schemes looking to ‘alternative’ matching assets

Source: Aon Hewitt Global Pension Risk Survey 2013

Net balance of respondents (%) expecting to increase exposure

-40 -30 -20 -10 0 10 20 30 40

UK equities

Global equities

Fixed gilts

Index Linked gilts

Corporate bonds

Alternatives

Derivative strategies

Relative value drivers

• Long lease terms (20-45 yrs)

• Investment grade credit rating

• Rents indexed to inflation

• Non-assignable leases

• FRI structures

JLL ALTERNATIVES SEMINAR 26 SEPTEMBER 2013 26

‘Alternatives’ as much as 40% of the investible universe

Owner Occupied residential

PRS & Social residential

Retail

Student Accom & Education

Leisure

Economic infra

Health & social infra

Office / Industrial

Source: UK National Statistics (various), LGP calculations

Indicative Investible Universe, 2012

JLL ALTERNATIVES SEMINAR 26 SEPTEMBER 2013 27

Diversification across a number of dimensions

• Occupier types

• Credit rating

• Lease length

• Review provisions ie. open mkt vs RPI

• Risk profile

10-yr correlation to equities (2002-11)

0.0 0.1 0.2 0.3 0.4 0.5 0.6 0.7

IPD AllProperty

Hotels

Market LetResidential

Forestry

Source: IPD

JLL ALTERNATIVES SEMINAR 26 SEPTEMBER 2013 28

‘Alternative’ comprises a wide risk / return spectrum

% Initial yield

1 2 3 4 5 6 7 8 9

Inco

me

Ris

k R

ank

(Sub

ject

ive

LGP

view

)

Investment Grade/Annuity Lease

Primary Care

Prime Leisure

PRS Residential

Student Accommodation (Direct Let)

High Spec Care Homes (Non Investment Grade)

Source: LGP

JLL ALTERNATIVES SEMINAR

Consumer Spending

5%

10%

15%

20%

25%

1963 2011 1963 2011

% Food Housing

26 SEPTEMBER 2013 29

Creating alignment with structural change

Source: UK National Statistics, Government Actuary’s Department, Wittenberg et al (2011) for the Dilnot Commissio

Population 2010-30, % pa

UK population 0.7

65+ years population 2.1

Elderly care residents 2.6

JLL ALTERNATIVES SEMINAR 26 SEPTEMBER 2013 30

Issues / challenges

• Liquidity / exit strategies - Investors price liquidity differently

• Data / benchmarks - Circular argument

- But risk premium required

• Skillsets - Draws on disciplines beyond those

traditionally involved in real estate

Private Equity

Real Estate

Infrastructure

Debt Equity

JLL ALTERNATIVES SEMINAR 26 SEPTEMBER 2013 31

Indicative IPD split in 10 years time; 25-30% ‘Other’

0%

25%

50%

75%

100%Current 2023

Source: IPD, LGP Calculations

Indicative IPD annual index Sector 2023 Change

Economic Infrastructure 4% +4%

Residential 10% +9%

Student accom & education 5% +4%

Health & social infra 6% +4%

Leisure 4% 0%

Office / Industrial 35% -7%

Retail 36% -14%

JLL ALTERNATIVES SEMINAR 26 SEPTEMBER 2013 32

Closing thoughts

• Demand for liability matching assets linked to appetite for alternatives

• But also a role for conventional return-seeking investors

• ‘Other’ may be 25-30% of IPD in 10 years time

• Investing in alternatives with confidence will be a core manager competency

JLL ALTERNATIVES SEMINAR 26 SEPTEMBER 2013 33

Legal & General Investment Management does not provide advice on the suitability of its products or services

This document is intended for educational purposes and should not be relied on for any other reason

Legal & General Investment Management

Authorised and regulated by the Financial Conduct Authority

One Coleman Street

London, EC2R 5AA

North American appetite for investing in alternatives in the UK Tim Edghill Director – Corporate Finance

North American Capital Sources

• North American Pension Funds account for 24 of the top 50 global pension funds, reflecting 35% by value (or $2.75 trn)

• Top 50 Global Asset Managers have AUM totalling $2.2trn, of that total $660bn, or 30% by value is allocated to Real Estate and managed by North American Asset Managers

• 50% of the Top 10 are allocated to Real Estate and 4 of those 5 are based in North America

• Of the Top 50 Life insurance companies, 18 are North American with total assets of $3.9trn.

• The mature REIT sector in North America has over 200 listed REITs with over $900 billion market capitalisation..

• Private investors / developers have built up considerable wealth and depth in the US. A number of these groups are seeking to expand into Europe..

Pension & Life Co’s, REITs, Fund Managers, Private Investors / Developers

North American Investment 2008-2013

Source: JLL Global Capital Flows Source: JLL Global Capital Flows

$0bn$1bn$2bn$3bn$4bn$5bn$6bn$7bn$8bn$9bn

2008 2009 2010 2011 2012 H1 2013

North American Investment into the UK (2008 to 2013)

Forecast

UK$25,491

$6,680

$7,930

$2,310 $3,356

$1,014 $822 $1,114 $272

North American Investment into Europe 2008-H1 2013

Unlisted Funds

Listed REIT

Institutions

Listed Developers/Prop Co's

Unlisted Developers/Prop Co's

Private Individual

Corporate

Hotel Owner/Operator

Unknown

The North American REIT Sector

2.00%2.50%3.00%3.50%4.00%4.50%5.00%5.50%6.00%

$0.0$20.0$40.0$60.0$80.0

$100.0$120.0

Divid

end Y

ield

(%)

Mark

et C

ap ($

Bn)

Market Cap and Dividend Yield by REIT Sector

Alternative Sectors

$0bn$10bn$20bn$30bn$40bn$50bn$60bn$70bn$80bn$90bn

$100bn

2007 2008 2009 2010 2011 2012 f2013

US REIT Capital Raisings 2007 - 2013

Debt

Equity

Source: NAREIT.com

• Currently 207 Listed REITS, the majority of which are sector specialist investors.

• There are 131 US Equity REITS with a Market Cap of $583bn and a weighted average dividend yield of 3.88%

• The Alternative sector REITs have over $250 billion market cap

Motivation to Invest

• The US investment cycle ahead of the UK and Europe

• Low interest rate environment brings significant capital inflows

• Competition for domestic stock (including Canada) is strong

• Prime assets and the best operators in high demand

• The search for yield

• Desire for diversification

• Differing motivations between US and Canadian Capital.

• Specialist investors seeking a more global presence

Some recent transaction examples

Caring Homes – Elderly Care Group Restructuring - £380 million • Corporate 35-year sale and leaseback of Elderly

Care assets to Griffin American Healthcare. • Californian based private REIT. • Completed August 2013.

RHM Klinik- und Altenheimbetriebe GmbH & Co. KG ("RHM") - €184 million • 27-year sale and leaseback of 11 post

acute facilities in Germany. • Purchased by Medical Properties Trust,

a hospital focussed REIT. • Completed September 2013.

Nido Student Living - £415 million • Sale of 3 student living assets and their operations. • Purchased by Round Hill Capital. • Platform purchase – completed 2012.

Impact on the Alternative Investment Sectors • Highly selective on opportunities.

• Investment based on US market perspectives

• Focus on quality - both assets and operators.

• Partnering mentality – long term relationships with top operators.

• Default focus on domestic (Northern American) markets.

Conclusion: The larger more expansive specialists will be a force in the UK and Europe Those that invest will be long term players, BUT… as global economics recover, domestic markets will remain the focus

Panel Discussion Dominic Reilly Director – JLL Corporate Finance

Panel Members

• Jon Neale - Head of Research – UK, JLL

• Rob Martin - Director of Research, Legal & General Property

• Brett Lashley - Managing Director, Greystar Real Estate Partners

• Martin Hadland - Director - Student Housing & Higher Education, JLL

Thank you joneslanglasalle.co.uk/alternatives

Thursday 26th September 2013

Alternative Investment Seminar Focusing on future trends for alternative investments