an analysis of connecticut’s state · o today’s funded status if sers had been adequately...

TRANSCRIPT

Jean-Pierre Aubry and Anek Belbase

Center for Retirement Research at Boston College

Connecticut Pension Analysis

Oct 28th, 2015

Hartford, CT

An Analysis of Connecticut’s State

Employees Retirement System:

Final Report

1

Overview

• Looking back

o SERS’ historical funded status

o The source of SERS’ unfunded liability (UAAL)

o Today’s funded status if SERS had been adequately funded

• Looking forward

o Funded level and cost under status-quo and alternative

funding methods

o Other ways to address the UAAL

o A better system for handling risk going forward

2

Looking back….

Over the past 2 decades, SERS’ funded status

has lagged behind the national average.

3

Sources: Various actuarial valuations for Connecticut SERS; PENDAT (1990-2000); and Public Plans Database (2001-2014).

Funded Ratio, 1969-2014

0%

20%

40%

60%

80%

100%

120%

1969 1974 1979 1984 1989 1994 1999 2004 2009 2014

Connecticut SERS

National average

SERS provided benefits as far back as 1939,

but did not pre-fund benefits until 1971.

4

Percentage of State and Local Plans Established or Significantly Restructured, by Date

Sources: Various actuarial valuations for Connecticut SERS; PENDAT (1990-2000); and Public Plans Database (2001-2014).

6.1%

3.0%1.8%

5.3% 5.0%

16.1%

29.6%

14.6%15.6%

5.8%

0%

10%

20%

30%

40%

SERS

5

But today’s poor funded ratio has to do with

more than SERS’ late start.

Methodology for UAAL Analysis

• Each SERS valuation provides data on the UAAL, the change

in the UAAL from the prior year, and some information on

factors behind the change.

• We combine the factors into meaningful groups and sum the

data from 1985-2014 to highlight the factors that have played a

role in the development of the UAAL over the past 29 years.

Since 1985, actuarial experience, returns, and

contributions have driven UAAL growth.

6

Source: Authors’ calculations based on various actuarial valuations for Connecticut SERS.

Sources of Change to UAAL, 1985-2014

1.3

-0.5 -0.5

1.1

4.1

0.11.4

12.5

-$4

$0

$4

$8

$12

$16B

illi

ons Contributions < ARC, 3.2

ARC < UAAL growth, 2.3

But not much happened before 2000.

7

Sources of Change to UAAL, 1985-1999

Source: Authors’ calculations based on various actuarial valuations for Connecticut SERS.

-1.9

0.0 0.0

-0.9

0.90.1

1.6 1.5

-$4

$0

$4

$8

$12

$16B

illi

ons

ARC < UAAL growth, 0.1

Contributions < ARC growth, 1.8

Since 2000, the UAAL has grown by $11

billion.

8

Sources of Change to UAAL, 2000-2014

Source: Authors’ calculations based on various actuarial valuations for Connecticut SERS.

3.2

-0.5 -0.5

2.03.1

0.0

-0.2

11.0

-$4

$0

$4

$8

$12

$16B

illi

ons

ARC < UAAL growth, 2.2

Contributions < ARC, 1.4

9

Two of the factors contributing to the UAAL

growth were controllable.

1. Contributions

• SEBAC agreements and other negotiated reductions in

contributions allowed account for nearly $2 billion in

unfunded liabilities.

• Starting in 2000, UAAL payments were calculated using a

level-percent-of-payroll method instead of level-dollar,

and no longer kept up with UAAL growth.

2. Assumed Investment Return

• SERS’ assumed return was higher than average.

Actual contributions fell short of required

amounts.

10

Contributions to CT SERS, 1985-2014, in Billions

Source: Authors’ calculations based on various actuarial valuations for Connecticut SERS.

$0

$400

$800

$1,200

$1,600

1985 1989 1993 1997 2001 2005 2009 2013

Mil

lions

Minimum required contribution to prevent UAAL growthAnnual Required ContributionActual Contribution

Also, the assumed rate of return was

unusually high.

11

Assumed Investment Return, 1990-2014

Sources: Actuarial valuations for Connecticut SERS; PENDAT (1990-2000); and Public Plans Database (2001-2014).

6.0%

6.5%

7.0%

7.5%

8.0%

8.5%

9.0%

1990 1993 1996 1999 2002 2005 2008 2011 2014

Connecticut SERS

National average

12

Two of the factors contributing to the UAAL

growth were less controllable.

• Deviations from actuarial experience

• Actual investment returns

13

Key demographic assumptions were

continually off.

Annual Impact of Actuarial Experience on Unfunded Liabilities, 1990-2014

Sources: Authors’ calculations based on CT SERS actuarial valuations; and the 1996 and 2002 Gain/Loss Studies for Connecticut SERS.

$0.3

$0.8

$1.0

-$0.4

$0.0

$0.4

$0.8

$1.2

1990 1994 1998 2002 2006 2010 2014

Bil

lions

14

Recently, retirement assumptions have

accounted for much of the poor experience.

Impact of Specific Actuarial Assumptions on Unfunded Liabilities, 2009-2014

Sources: Authors’ calculations based on 2009-2014 actuarial valuations for CT SERS;

$1.21

$0.00

-$0.09

$0.05

$0.38

-$0.5

$0.0

$0.5

$1.0

$1.5

Retirement Separation Salary Mortality Other

Bil

lions

15

Up to 2000, SERS’ actual investment returns

were above the assumed return.

Actual vs. Assumed Investment Return, 1983-2000

Sources: Actuarial valuations for Connecticut SERS; and Census of Governments (1983-2000).

8.5%

11.3%

0%

5%

10%

15%

2000 Assumed return

Average return from 1983-2000

16

But since 2000, investment returns have

fallen considerably short of the assumed.

Actual vs. Assumed Investment Return, 2001-2014

Sources: Actuarial valuations for Connecticut SERS; and Census of Governments (2001-2014).

8.0%

5.4%

0%

5%

10%

15%

2014 Assumed return

Average return from 2001-2014

17

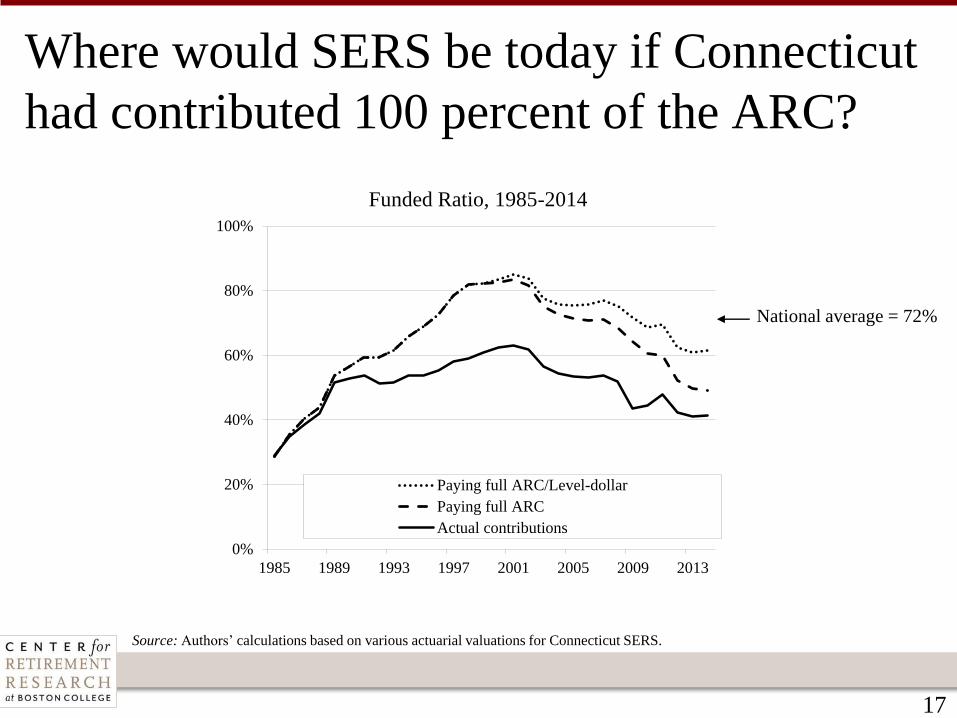

Where would SERS be today if Connecticut

had contributed 100 percent of the ARC?

Funded Ratio, 1985-2014

Source: Authors’ calculations based on various actuarial valuations for Connecticut SERS.

National average = 72%

0%

20%

40%

60%

80%

100%

1985 1989 1993 1997 2001 2005 2009 2013

Paying full ARC/Level-dollar

Paying full ARC

Actual contributions

18

Looking forward….

19

The key question is how to deal with the

existing UAAL.

2014 Actuarial Costs as a Percent of Payroll, by Element

Sources: Actuarial valuation for Connecticut SERS; and Public Plans Database (2014).

2.2%6.6%

8.0%

7.0%

35.4%

9.0%

0%

10%

20%

30%

40%

50%

Connecticut SERS National average

Employer UAAL payment

Employer normal cost

Employee contribution

20

Three factors determine the trajectory of

UAAL amortization payments.

1. Payment schedule:

• Level dollar: front-loaded payments

• Level percent of pay: back-loaded payments

2. Funding period

• Closed amortization period: fixed date for full funding

• Open amortization period: no fixed date

3. Length of amortization period

21

Projection methodology

• We begin with data from SERS 2014 actuarial valuation.

• The Actuary provides projection for payroll, normal costs, and

benefit payments.

• We calculate the UAAL and amortization payment in each year.

• We assume the plan pays its full projected ARC (normal cost +

amortization payment) and achieves its assumed return.

• Market assets in each year equal the prior year’s assets plus

contributions and investment earnings, minus benefit payments.

• SERS’ actuarial smoothing method is used for actuarial assets.

22

One way forward is pay off the UAAL by

2032 (current law)...

SERS Funded Ratio under Alternative Funding Methods, 2014-2046

Source: Authors’ calculations based on various actuarial valuations for Connecticut SERS.

0%

20%

40%

60%

80%

100%

120%

2014 2019 2024 2029 2034 2039 2044

Current Law

Level-dollar

23

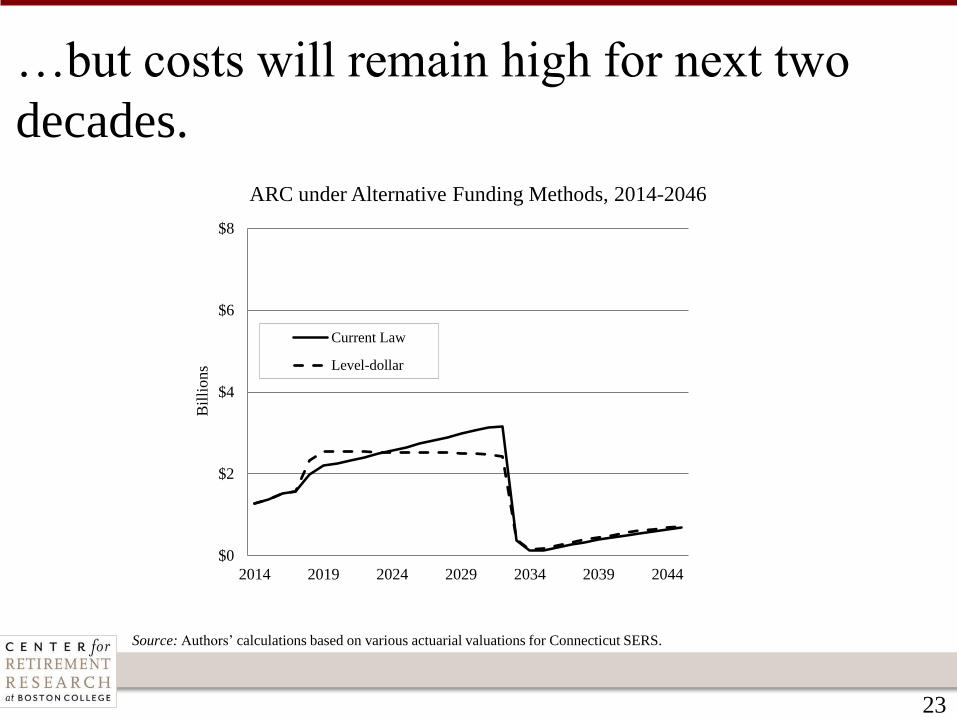

…but costs will remain high for next two

decades.

ARC under Alternative Funding Methods, 2014-2046

Source: Authors’ calculations based on various actuarial valuations for Connecticut SERS.

$0

$2

$4

$6

$8

2014 2019 2024 2029 2034 2039 2044

Bil

lion

s

Current Law

Level-dollar

24

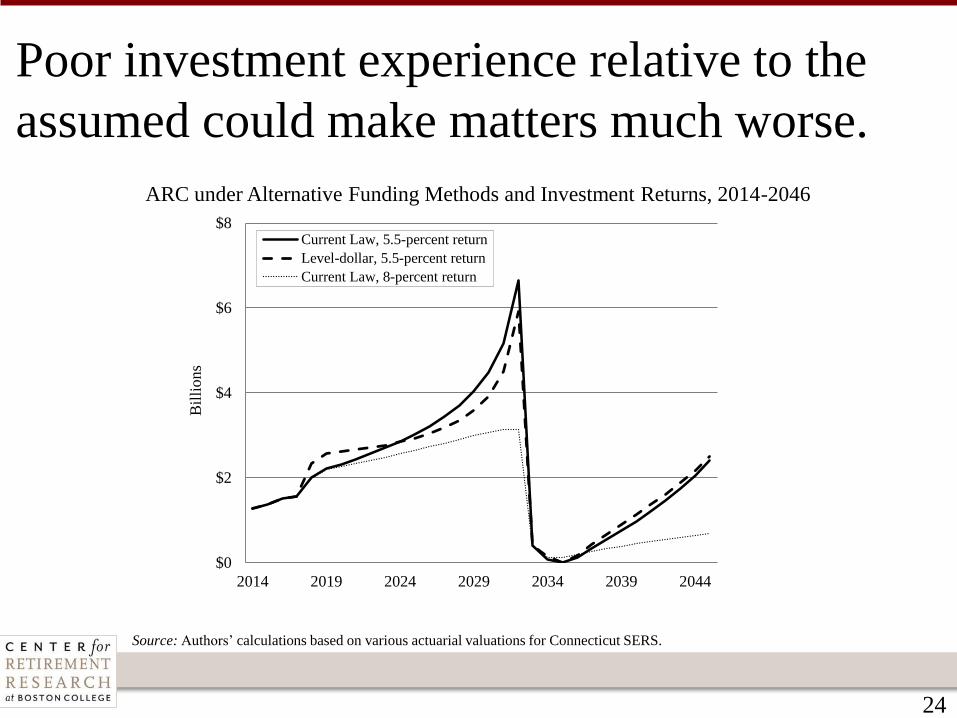

Poor investment experience relative to the

assumed could make matters much worse.

ARC under Alternative Funding Methods and Investment Returns, 2014-2046

Source: Authors’ calculations based on various actuarial valuations for Connecticut SERS.

$0

$2

$4

$6

$8

2014 2019 2024 2029 2034 2039 2044

Bil

lions

Current Law, 5.5-percent return

Level-dollar, 5.5-percent return

Current Law, 8-percent return

25

Relaxing the requirement to pay off the

UAAL by 2032 will delay full funding...

SERS Funded Ratio under Alternative Funding Methods, 2014-2046

Source: Authors’ calculations based on various actuarial valuations for Connecticut SERS.

0%

20%

40%

60%

80%

100%

120%

2014 2019 2024 2029 2034 2039 2044

Level-dollar, 15-yr open, 8-percent return

Current Law, 8-percent return

26

…but will reduces annual costs significantly

over the next 20 years.

ARC under Alternative Funding Methods, 2014-2046

Source: Authors’ calculations based on various actuarial valuations for Connecticut SERS.

$0

$2

$4

$6

$8

2014 2019 2024 2029 2034 2039 2044

Bil

lion

s

Level-dollar, 15-yr open, 8-percent return

Current Law, 8-percent return

27

Even with a more conservative investment

return assumption, costs remain lower.

ARC under Alternative Funding Methods and Assumed Returns, 2014-2046

Source: Authors’ calculations based on various actuarial valuations for Connecticut SERS.

$0

$2

$4

$6

$8

2014 2019 2024 2029 2034 2039 2044

Bil

lions

Current Law, 8% Discount Rate

Level Dollar, 15-yr open, 8% Discount Rate

Level Dollar, 15-yr open, 7% Discount Rate

28

Can Connecticut address the UAAL in other

ways?

Separate the funding of the UAAL from ongoing plan financing

to clarify the cost of benefits for current workers vs. legacy costs.

• Issue a POB or establish a dedicated tax/revenue stream.

• This is NOT an arbitrage or cost-saving mechanism. In fact, to

ensure policy goals are met, it requires valuing the UAAL with

a conservative interest rate.

29

What about the less controllable factors?

• Investment risk can be shared equitably among the plan

stakeholders through a predetermined pattern of contribution

increases and benefit cuts.

• Incremental increases to the normal cost due to revised actuarial

assumptions can be shared evenly between employees and

employers.

Conclusions

30

• SERS’ current troubles are mainly the result of three things:

1. Inadequate contributions

2. Poor investment performance compared to the assumed

investment return.

3. Actuarial Experience

• The key to the future is making full required contributions.

• But paying off the UAAL by 2032 comes at a significant cost.

• Extending the payment horizon or issuing a POB could spread

out the pain over a longer period.

• Lowering the assumed return and instituting procedures that

automatically respond to bad outcomes would mitigate risk.

31

• The Center for Retirement Research at Boston College

http://crr.bc.edu

• Public Plans Database (PPD)

http://publicplansdata.org

• State and Local Pension Research

http://crr.bc.edu/special-projects/state-local-pension-plans/

Jean-Pierre Aubry

Assistant Director of State and Local Research