arqiva fy 15 results update presentation final version 2 · sound digital is a consortium which...

TRANSCRIPT

Copyright © Arqiva Limited 2015 1

Arqiva

Year ending 30 June 2015 results presentation Version 2

Copyright © Arqiva Limited 2015 2

This material has been prepared by and is the sole responsibility of Arqiva Broadcast Holdings Limited and its subsidiaries (the “Company”) and has been prepared for information only and has not been verified, approved or endorsed by any arranger, lead manager, bookrunner, underwriter or other advisers retained by the Company.

No representation or warranty, either express or implied, is given or made by any person in relation to the fairness, accuracy, completeness or reliability of the information or any opinions contained herein and no reliance whatsoever should be placed on such information or opinions. No responsibility or liability is or will be accepted by the Company or by any of its respective directors, officers, servants, advisers, agents or affiliates as to or in relation to the accuracy, sufficiency or completeness of this document or the information forming the basis of the document or for any reliance placed on the document by any person whatsoever. No representation or warranty, expressed or implied, is or will be made as to the achievement or reasonableness of, and no reliance should be placed on, any projection, targets, estimates, forecasts and nothing in this document should be relied on as a promise or representation as to the future.

The financial information set forth in this presentation has been subjected to rounding adjustments for ease of presentation. Accordingly, in certain instances, the sum of the numbers in a column or a row in tables may not conform exactly to the total figure given for that column or row. Furthermore, percentage figures included in this presentation have not been calculated on the basis of rounded figures but have been calculated on the basis of such amounts prior to rounding.

This material should not be regarded by recipients as a substitute for the exercise of their own judgement and assessment. Any opinions expressed in this material are subject to change without notice and neither the Company nor any other person is under any obligation to update or keep current the information contained herein. This material, which does not purport to be comprehensive, has not been independently verified by the Company or any other party. The document does not constitute an audit or a due diligence review and should not be construed as such.

No representation or warranty, expressed or implied, is or will be made and, save in the case of fraud, law or other regulation may restrict the distribution of this document in certain jurisdictions. Accordingly, recipients of this material should inform themselves about and observe all applicable legal and regulatory requirements. This document does not constitute an offer to sell or an invitation to purchase securities in any jurisdiction. This document is being distributed on the basis that each person in the United Kingdom to whom it is issued is reasonably believed to be such a person as is described in Article 19 (Investment professionals) or Article 49 (High net worth companies, unincorporated associations etc.) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005, or is a person to whom this document may otherwise lawfully be distributed. Persons who do not fall within such descriptions may not act upon the information contained in this document.

Disclaimer

Copyright © Arqiva Limited 2015 3

Contents Executive summary

Divisional review

Detailed financials

Financing

Summary

A

B

C

D

E

Copyright © Arqiva Limited 2015 4

Executive summary

Copyright © Arqiva Limited 2015 Company confidential 5

LEADING POSITION IN SMART METERING

Sole provider for smart metering communication services in Northern England and Scotland to cover 9.3m premises and provider of smart water metering for Thames Water to cover up to 3m homes

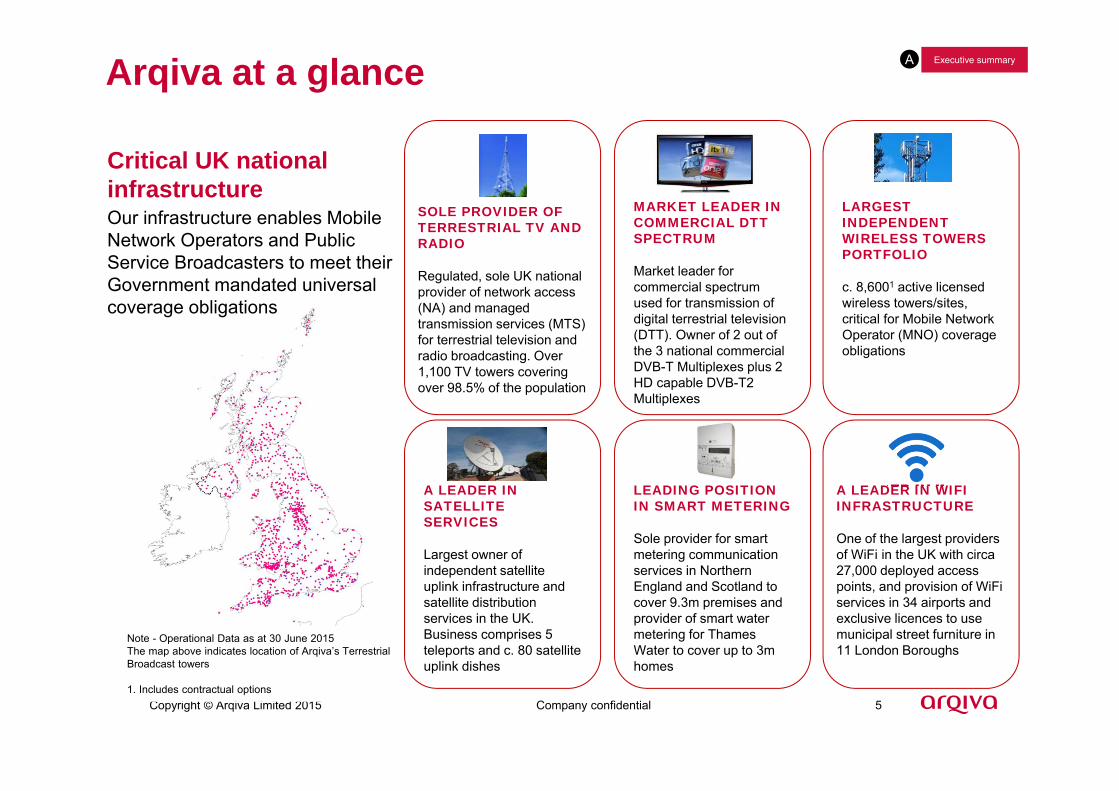

Arqiva at a glance

Critical UK national infrastructureOur infrastructure enables Mobile Network Operators and Public Service Broadcasters to meet their Government mandated universal coverage obligations

Note - Operational Data as at 30 June 2015The map above indicates location of Arqiva’s Terrestrial Broadcast towers

1. Includes contractual options

A Executive summary

SOLE PROVIDER OF TERRESTRIAL TV AND RADIO

Regulated, sole UK national provider of network access (NA) and managed transmission services (MTS) for terrestrial television and radio broadcasting. Over 1,100 TV towers covering over 98.5% of the population

MARKET LEADER IN COMMERCIAL DTT SPECTRUM

Market leader for commercial spectrum used for transmission of digital terrestrial television (DTT). Owner of 2 out of the 3 national commercial DVB-T Multiplexes plus 2HD capable DVB-T2 Multiplexes

LARGEST INDEPENDENT WIRELESS TOWERS PORTFOLIO

c. 8,6001 active licensed wireless towers/sites, critical for Mobile Network Operator (MNO) coverage obligations

A LEADER IN WIFI INFRASTRUCTURE

One of the largest providers of WiFi in the UK with circa 27,000 deployed access points, and provision of WiFi services in 34 airports and exclusive licences to use municipal street furniture in 11 London Boroughs

A LEADER IN SATELLITE SERVICES

Largest owner of independent satellite uplink infrastructure and satellite distribution services in the UK. Business comprises 5 teleports and c. 80 satellite uplink dishes

Copyright © Arqiva Limited 2015 Company confidential 6

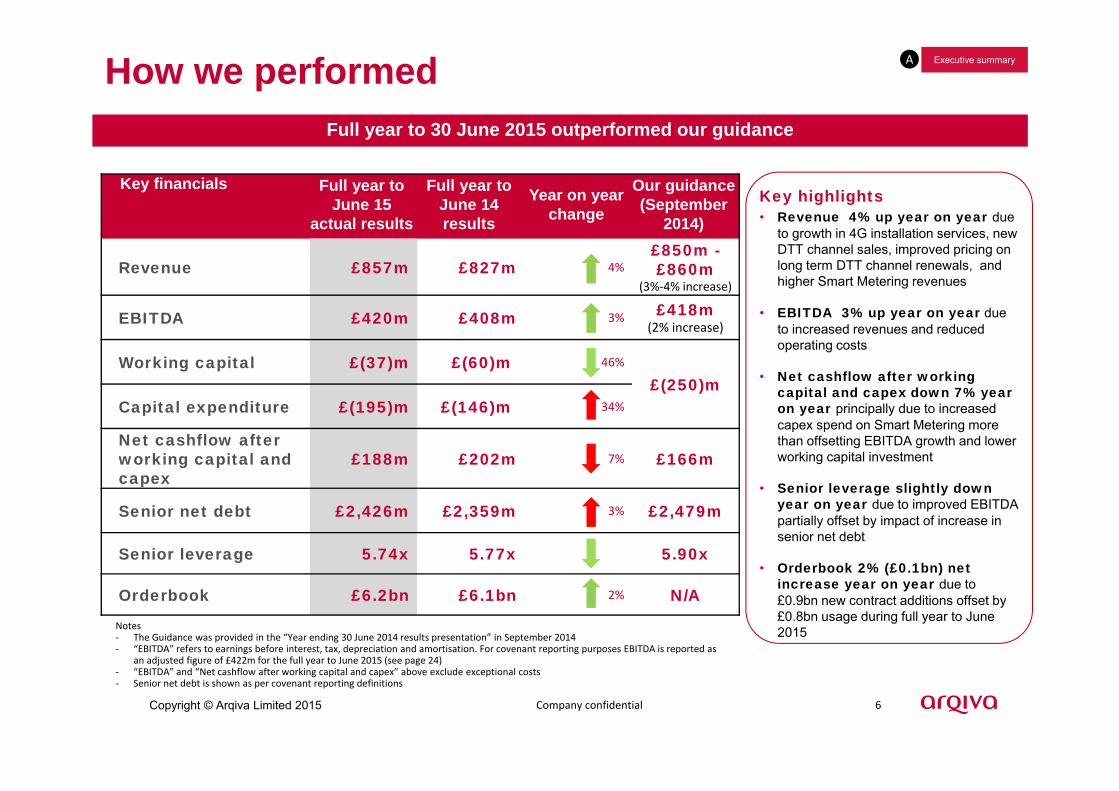

How we performed

Key financials Full year to June 15

actual results

Full year to June 14 results

Year on year change

Our guidance (September

2014)

Revenue £857m £827m 4%£850m -£860m

(3%‐4% increase)

EBITDA £420m £408m 3% £418m(2% increase)

Working capital £(37)m £(60)m 46%

£(250)mCapital expenditure £(195)m £(146)m 34%

Net cashflow after working capital and capex

£188m £202m 7% £166m

Senior net debt £2,426m £2,359m 3% £2,479m

Senior leverage 5.74x 5.77x 5.90x

Orderbook £6.2bn £6.1bn 2% N/A

A Executive summary

Full year to 30 June 2015 outperformed our guidance

Notes ‐ The Guidance was provided in the “Year ending 30 June 2014 results presentation” in September 2014‐ “EBITDA” refers to earnings before interest, tax, depreciation and amortisation. For covenant reporting purposes EBITDA is reported as

an adjusted figure of £422m for the full year to June 2015 (see page 24)‐ “EBITDA” and “Net cashflow after working capital and capex” above exclude exceptional costs‐ Senior net debt is shown as per covenant reporting definitions

Key highlights• Revenue 4% up year on year due

to growth in 4G installation services, new DTT channel sales, improved pricing on long term DTT channel renewals, and higher Smart Metering revenues

• EBITDA 3% up year on year due to increased revenues and reduced operating costs

• Net cashflow after working capital and capex down 7% year on year principally due to increased capex spend on Smart Metering more than offsetting EBITDA growth and lower working capital investment

• Senior leverage slightly down year on year due to improved EBITDA partially offset by impact of increase in senior net debt

• Orderbook 2% (£0.1bn) net increase year on year due to £0.9bn new contract additions offset by £0.8bn usage during full year to June 2015

Copyright © Arqiva Limited 2015 Company confidential 7

Business highlights A

Activity Update

Leadership

New Chairman, MikeParton

Mike Parton appointed in April 2015. Mike, a Chartered Management Accountant, was CEO of Marconi until 2006 before overseeing a sale of the company to Ericsson. Mike takes over from Peter Shore who had been Chairman of Arqiva from 2007.

New CEO,SimonBeresford-Wylie

Simon Beresford-Wylie appointed in August 2015. Simon joins Arqiva with over 30 years’ experience in the information technology and telecoms sector. He has held roles globally, most recently helping guide the strategy and operations of Samsung Electronics’ network business in Seoul, Korea. He takes over from John Cresswell who led the company since January 2011.

New business

Contracted orderbook

£0.9bn of new contract additions since 30 June 2014 across all business areas

Delivery

4G rollout and MobileInfrastructure Project (MIP)

Activity from the MNOs is resulting in a significant increase in Installation Services revenue for Arqiva. Rollout to not-spot areas continues

Smart Metering All DCC contracted milestones met to date. Network coverage has exceeded 60% of target population.

BBC New Radio Agreement

Programme delivery of DAB rollout has been progressing with the coverage of UK’s BBC DAB networkover 95% as at 30 June 2015

Second national DAB service

Rollout underway for second commercial national DAB radio service for Sound Digital to launch 45 site network by March 2016. Sound Digital is a consortium which includes Arqiva (40%), Bauer and UTV Media GB

Internet of Things Focus on activities to bring the Sigfox network to operational and commercial readiness whilst running proof of concepts with a number of potential customers

Financing Continued progress on refinancing

A new 15-year amortising, floating rate US Private Placement was completed during July 2014, raising £300m, leaving only £353.5m outstanding (maturing in February 2018) from original bank term loans of £1,586m put in place at refinancing

Executive summary

Copyright © Arqiva Limited 2015 Company confidential 8

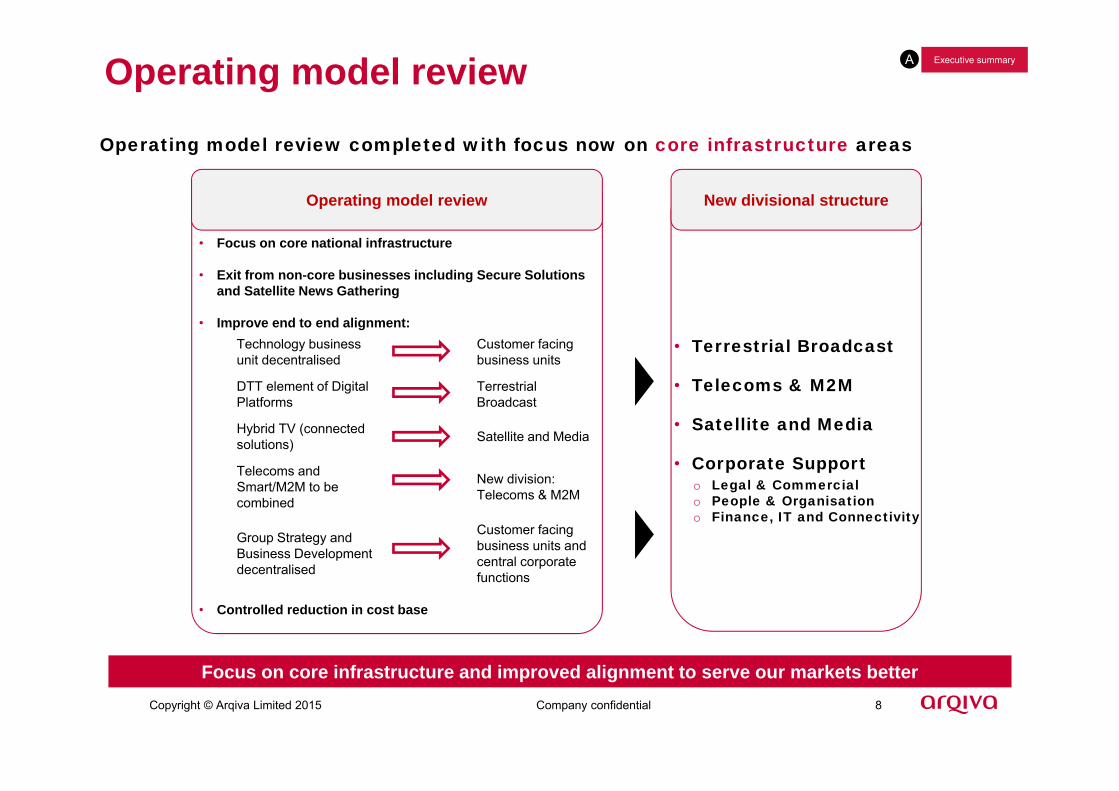

Operating model review

A Executive summary

Operating model review completed with focus now on core infrastructure areas

• Focus on core national infrastructure

• Exit from non-core businesses including Secure Solutions and Satellite News Gathering

• Improve end to end alignment:

• Controlled reduction in cost base

Operating model review

Technology business unit decentralised

Customer facing business units

DTT element of Digital Platforms

Terrestrial Broadcast

Hybrid TV (connected solutions) Satellite and Media

Telecoms and Smart/M2M to be combined

New division:Telecoms & M2M

Group Strategy and Business Development decentralised

Customer facing business units and central corporate functions

• Terrestrial Broadcast

• Telecoms & M2M

• Satellite and Media

• Corporate Supporto Legal & Commercialo People & Organisation o Finance, IT and Connectivity

New divisional structure

Focus on core infrastructure and improved alignment to serve our markets better

Copyright © Arqiva Limited 2015 9

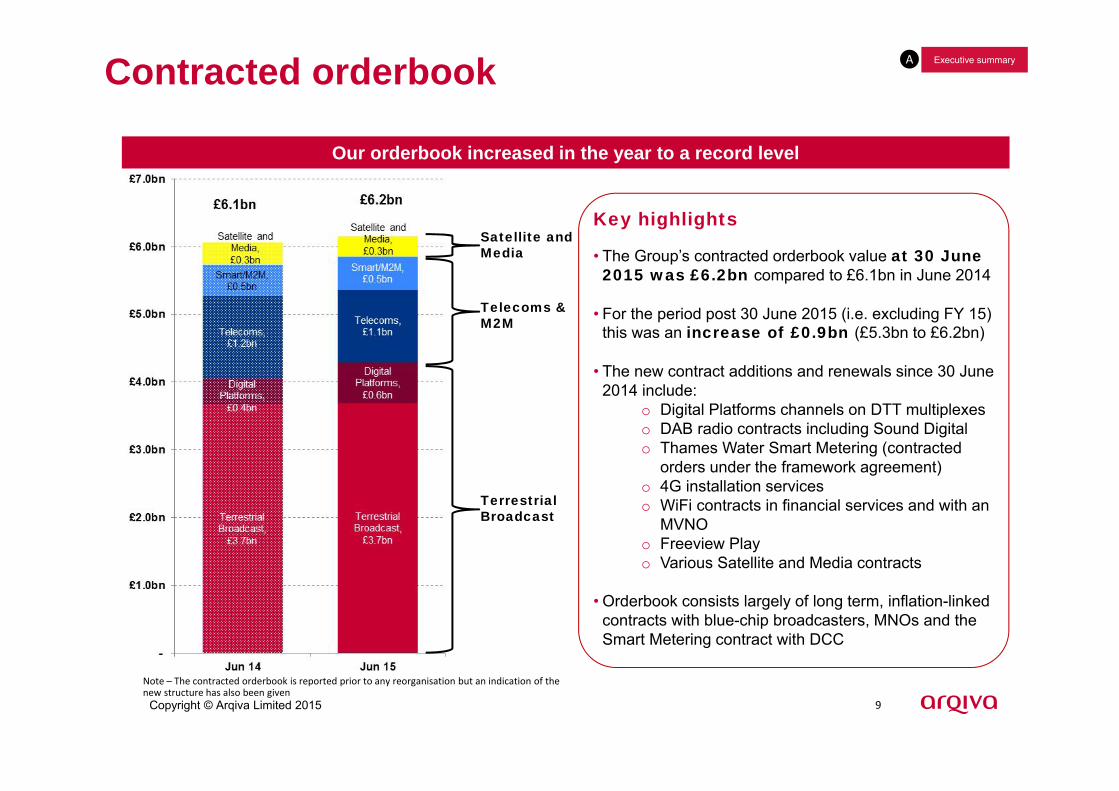

Our orderbook increased in the year to a record level

A Executive summary

Key highlights

• The Group’s contracted orderbook value at 30 June 2015 was £6.2bn compared to £6.1bn in June 2014

• For the period post 30 June 2015 (i.e. excluding FY 15) this was an increase of £0.9bn (£5.3bn to £6.2bn)

• The new contract additions and renewals since 30 June 2014 include:

o Digital Platforms channels on DTT multiplexeso DAB radio contracts including Sound Digitalo Thames Water Smart Metering (contracted

orders under the framework agreement)o 4G installation services o WiFi contracts in financial services and with an

MVNO o Freeview Play o Various Satellite and Media contracts

• Orderbook consists largely of long term, inflation-linked contracts with blue-chip broadcasters, MNOs and the Smart Metering contract with DCC

Contracted orderbook

Note – The contracted orderbook is reported prior to any reorganisation but an indication of the new structure has also been given

Terrestrial Broadcast

Telecoms & M2M

Satellite and Media

Copyright © Arqiva Limited 2015 Company confidential 10

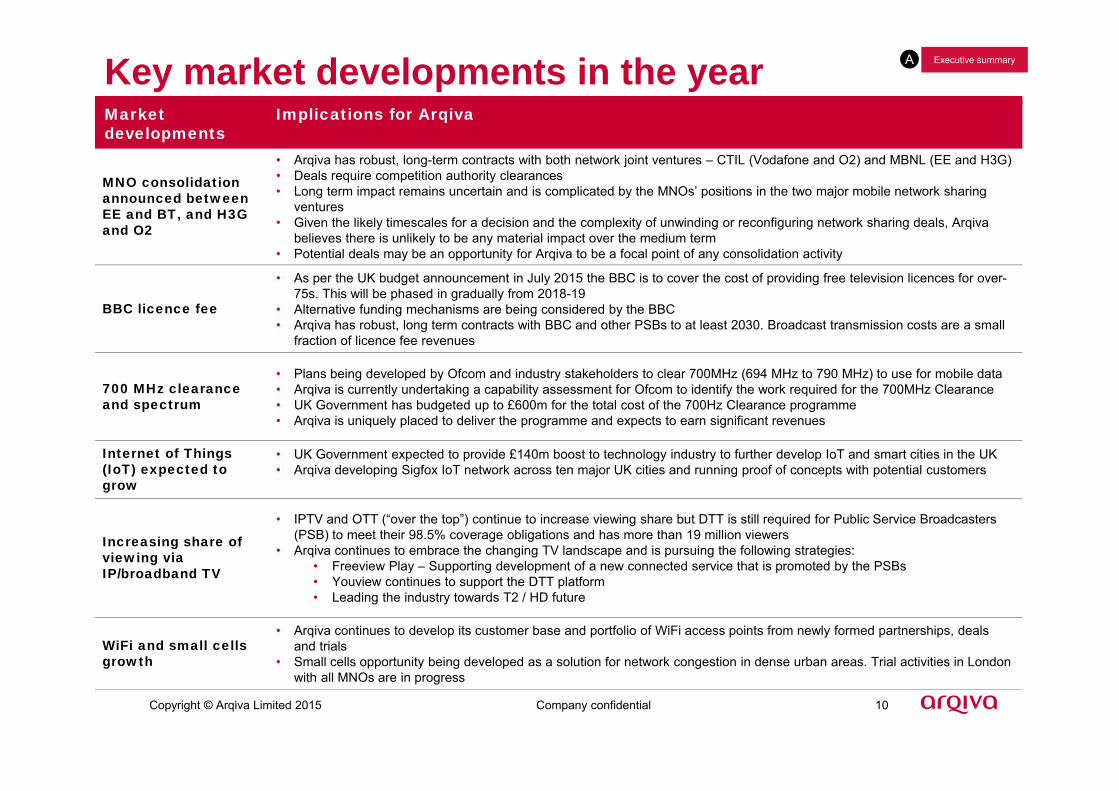

Key market developments in the year A Executive summary

Market developments

Implications for Arqiva

MNO consolidation announced between EE and BT, and H3G and O2

• Arqiva has robust, long-term contracts with both network joint ventures – CTIL (Vodafone and O2) and MBNL (EE and H3G)• Deals require competition authority clearances • Long term impact remains uncertain and is complicated by the MNOs’ positions in the two major mobile network sharing

ventures• Given the likely timescales for a decision and the complexity of unwinding or reconfiguring network sharing deals, Arqiva

believes there is unlikely to be any material impact over the medium term• Potential deals may be an opportunity for Arqiva to be a focal point of any consolidation activity

BBC licence fee

• As per the UK budget announcement in July 2015 the BBC is to cover the cost of providing free television licences for over-75s. This will be phased in gradually from 2018-19

• Alternative funding mechanisms are being considered by the BBC • Arqiva has robust, long term contracts with BBC and other PSBs to at least 2030. Broadcast transmission costs are a small

fraction of licence fee revenues

700 MHz clearance and spectrum

• Plans being developed by Ofcom and industry stakeholders to clear 700MHz (694 MHz to 790 MHz) to use for mobile data• Arqiva is currently undertaking a capability assessment for Ofcom to identify the work required for the 700MHz Clearance• UK Government has budgeted up to £600m for the total cost of the 700Hz Clearance programme • Arqiva is uniquely placed to deliver the programme and expects to earn significant revenues

Internet of Things (IoT) expected to grow

• UK Government expected to provide £140m boost to technology industry to further develop IoT and smart cities in the UK• Arqiva developing Sigfox IoT network across ten major UK cities and running proof of concepts with potential customers

Increasing share of viewing via IP/broadband TV

• IPTV and OTT (“over the top”) continue to increase viewing share but DTT is still required for Public Service Broadcasters (PSB) to meet their 98.5% coverage obligations and has more than 19 million viewers

• Arqiva continues to embrace the changing TV landscape and is pursuing the following strategies:• Freeview Play – Supporting development of a new connected service that is promoted by the PSBs• Youview continues to support the DTT platform• Leading the industry towards T2 / HD future

WiFi and small cells growth

• Arqiva continues to develop its customer base and portfolio of WiFi access points from newly formed partnerships, deals and trials

• Small cells opportunity being developed as a solution for network congestion in dense urban areas. Trial activities in Londonwith all MNOs are in progress

Copyright © Arqiva Limited 2015 11

Business Review

Copyright © Arqiva Limited 2015 12

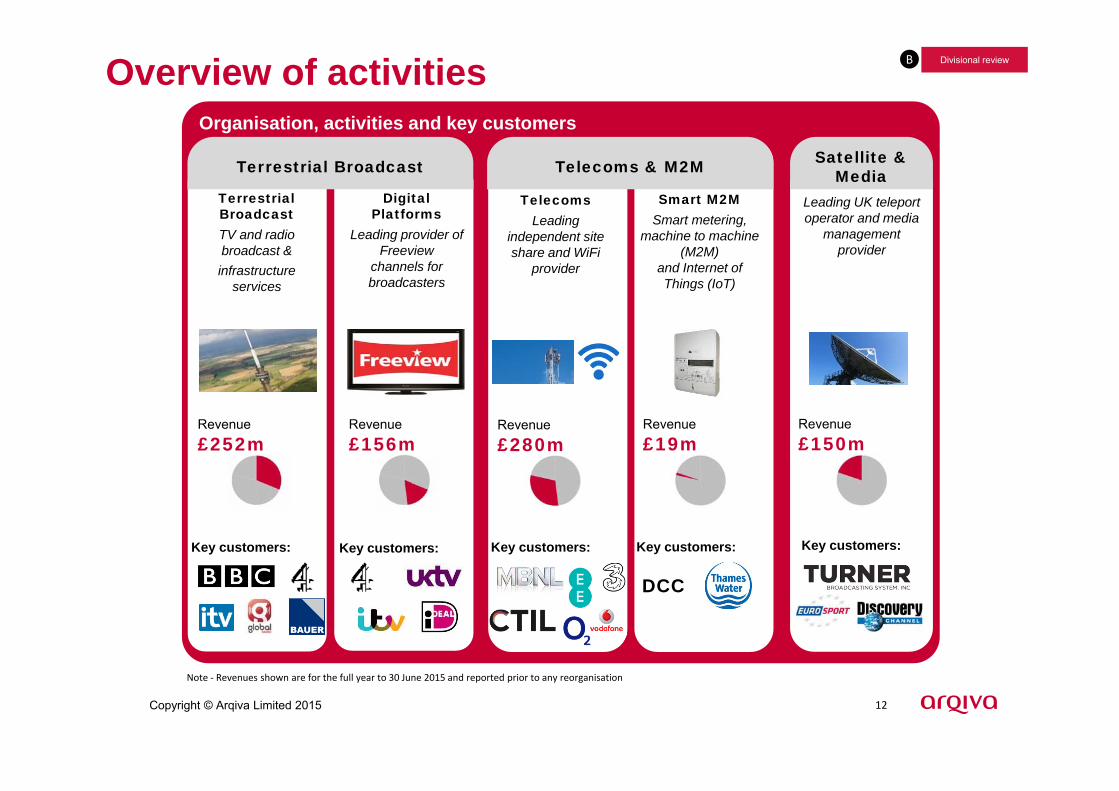

Terrestrial Broadcast Satellite & Media

Terrestrial BroadcastTV and radio broadcast & infrastructure

services

Digital Platforms

Leading provider of Freeview

channels for broadcasters

Leading UK teleport operator and media

management provider

Revenue£252m

Revenue£156m

Revenue£150m

Overview of activities

Key customers: Key customers: Key customers:

Organisation, activities and key customers

TelecomsLeading

independent siteshare and WiFi

provider

Revenue£280m

Key customers:

Smart M2MSmart metering,

machine to machine (M2M)

and Internet of Things (IoT)

Revenue£19m

Key customers:

DCC

B Divisional review

Telecoms & M2M

Note ‐ Revenues shown are for the full year to 30 June 2015 and reported prior to any reorganisation

Copyright © Arqiva Limited 2015 13

B Divisional review

Strategy

New customer contracts

Recent/market

developments

Revenue analysis

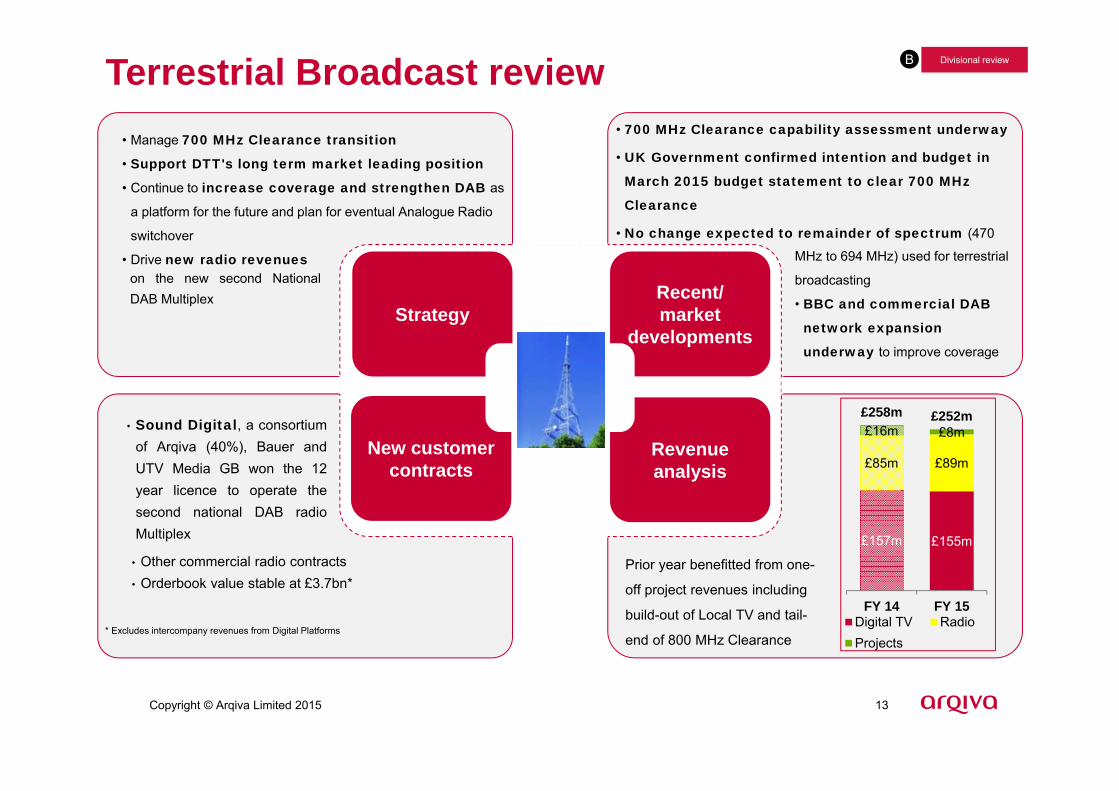

Terrestrial Broadcast review

on the new second NationalDAB Multiplex

• Manage 700 MHz Clearance transition

• Support DTT's long term market leading position

• Continue to increase coverage and strengthen DAB as

a platform for the future and plan for eventual Analogue Radio

switchover

• Drive new radio revenues

• 700 MHz Clearance capability assessment underway

• UK Government confirmed intention and budget in

March 2015 budget statement to clear 700 MHz

Clearance

• No change expected to remainder of spectrum (470

MHz to 694 MHz) used for terrestrial

broadcasting

• BBC and commercial DAB

network expansion

underway to improve coverage

• Sound Digital, a consortiumof Arqiva (40%), Bauer andUTV Media GB won the 12year licence to operate thesecond national DAB radioMultiplex

• Other commercial radio contracts• Orderbook value stable at £3.7bn*

Prior year benefitted from one-

off project revenues including

build-out of Local TV and tail-

end of 800 MHz Clearance

£157m £155m

£85m £89m

£16m £8m£258m £252m

FY 14 FY 15Digital TV RadioProjects

* Excludes intercompany revenues from Digital Platforms

Copyright © Arqiva Limited 2015 14

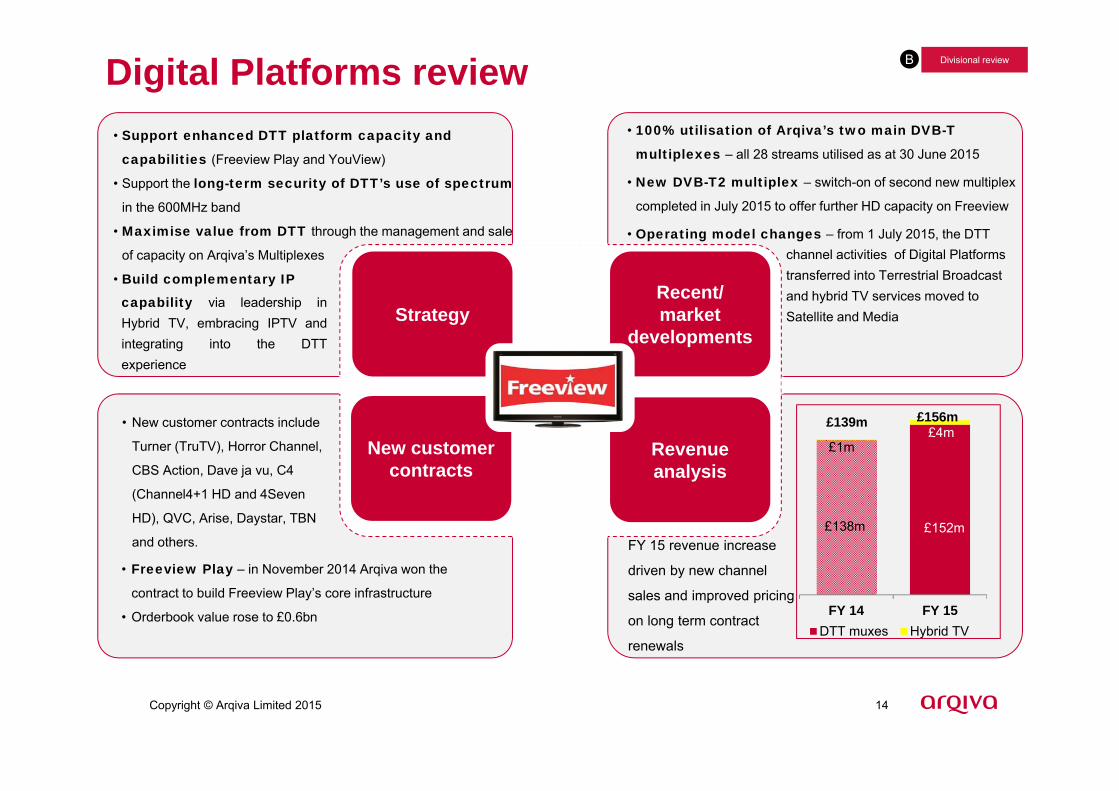

B Divisional reviewDigital Platforms review• Support enhanced DTT platform capacity and

capabilities (Freeview Play and YouView)

• Support the long-term security of DTT’s use of spectrum

in the 600MHz band

• Maximise value from DTT through the management and sale

of capacity on Arqiva’s Multiplexes

• Build complementary IP

capability via leadership inHybrid TV, embracing IPTV andintegrating into the DTTexperience

• 100% utilisation of Arqiva’s two main DVB-T

multiplexes – all 28 streams utilised as at 30 June 2015

• New DVB-T2 multiplex – switch-on of second new multiplex

completed in July 2015 to offer further HD capacity on Freeview

• Operating model changes – from 1 July 2015, the DTTchannel activities of Digital Platforms transferred into Terrestrial Broadcast and hybrid TV services moved to Satellite and Media

• New customer contracts include

Turner (TruTV), Horror Channel,

CBS Action, Dave ja vu, C4

(Channel4+1 HD and 4Seven

HD), QVC, Arise, Daystar, TBN

and others.

• Freeview Play – in November 2014 Arqiva won the

contract to build Freeview Play’s core infrastructure

• Orderbook value rose to £0.6bn FY 14 FY 15DTT muxes Hybrid TV

£138m £152m

£1m£4m

£139m £156m

FY 15 revenue increase

driven by new channel

sales and improved pricing

on long term contract

renewals

Strategy

New customer contracts

Recent/market

developments

Revenue analysis

Copyright © Arqiva Limited 2015 15

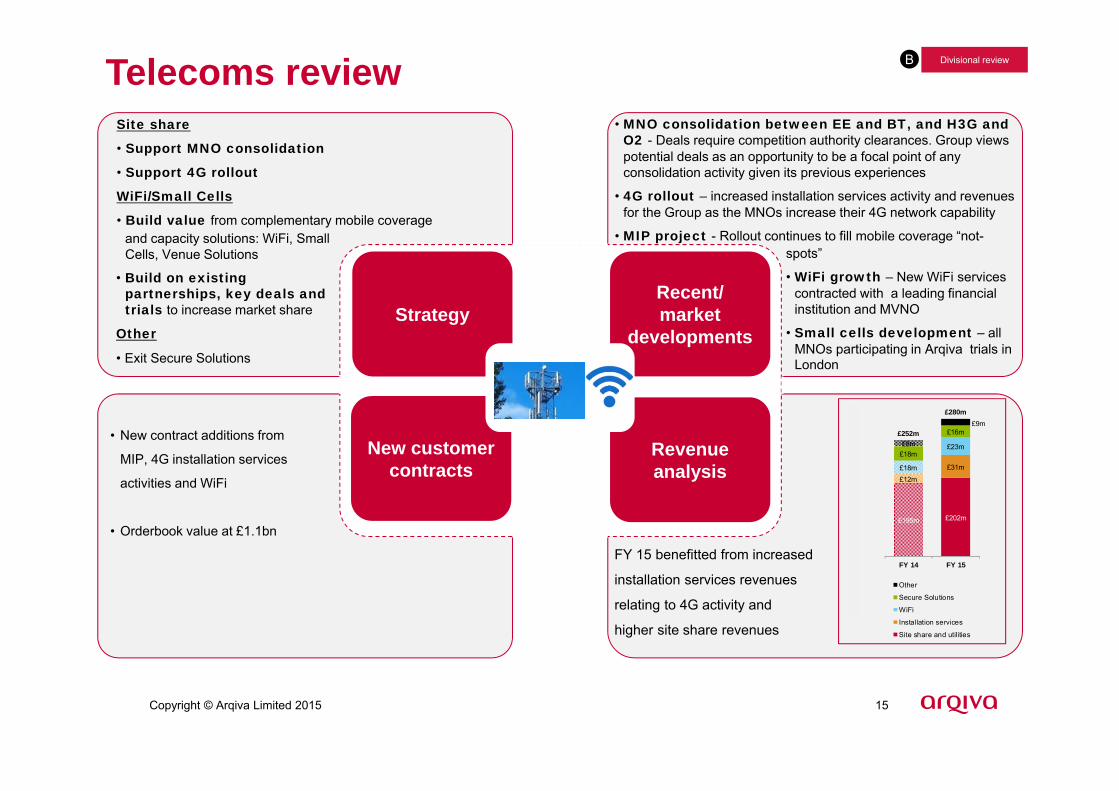

B Divisional reviewTelecoms reviewSite share

• Support MNO consolidation

• Support 4G rollout

WiFi/Small Cells

• Build value from complementary mobile coverageand capacity solutions: WiFi, Small Cells, Venue Solutions

• Build on existing partnerships, key deals and trials to increase market share

Other

• Exit Secure Solutions

• MNO consolidation between EE and BT, and H3G and O2 - Deals require competition authority clearances. Group views potential deals as an opportunity to be a focal point of any consolidation activity given its previous experiences

• 4G rollout – increased installation services activity and revenues for the Group as the MNOs increase their 4G network capability

• MIP project - Rollout continues to fill mobile coverage “not-spots”

• WiFi growth – New WiFi services contracted with a leading financial institution and MVNO

• Small cells development – all MNOs participating in Arqiva trials in London

• New contract additions from

MIP, 4G installation services

activities and WiFi

• Orderbook value at £1.1bn

FY 15 benefitted from increased

installation services revenues

relating to 4G activity and

higher site share revenues

Strategy

New customer contracts

Recent/market

developments

Revenue analysis

£195m £202m

£12m

£31m£18m

£23m£18m

£16m

£8m

£9m£252m

£280m

FY 14 FY 15

Other

Secure Solutions

WiFi

Installation services

Site share and utilities

Copyright © Arqiva Limited 2015 16

B Divisional reviewSmart M2M reviewSmart • Deliver landmark Smart Metering and Smart Water

Metering contracts and develop further opportunities from

these wins

• Continue to position for a Smart Grid win in medium term

Internet of Things (IoT)

• Smart Metering contract milestones on target as at 30 June 2015

• Smart Metering specification changes and revised timescales will result in additional revenues for Arqiva

• Smart water metering build for Thames underway

• Internet of Things (IoT) network being developed using Sigfox

technology starting with ten major UK cities. Product being testedwith potential clients

• Execute our IoT strategy centred on

industry alignment, direct sales in

key verticals, wider indirect sales

arrangements and target roll out

• Smart water metering contract

signed with Thames in March 2015

• Further orders expected in financial

year ending 30 June 2016 from

Smart Metering specification

changes

Increased revenues due to:

• Continued progress on design

and development milestones

• Orderbook stands at £0.5bn

• Additional revenues from smart metering specification changes

• Water meter sales for Thames contract

Strategy

New customer contracts

Recent/market

developments

Revenue analysis

Copyright © Arqiva Limited 2015 17

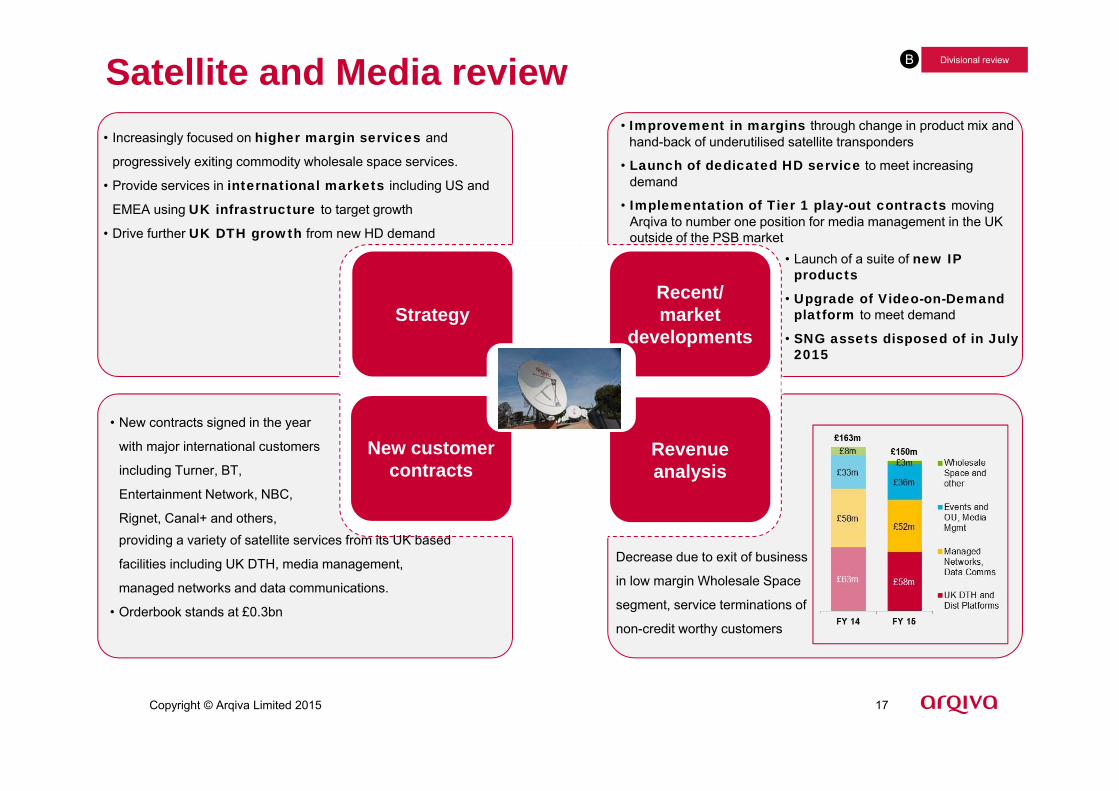

B Divisional reviewSatellite and Media review• Increasingly focused on higher margin services and

progressively exiting commodity wholesale space services.

• Provide services in international markets including US and

EMEA using UK infrastructure to target growth

• Drive further UK DTH growth from new HD demand

• Improvement in margins through change in product mix and hand-back of underutilised satellite transponders

• Launch of dedicated HD service to meet increasing demand

• Implementation of Tier 1 play-out contracts moving Arqiva to number one position for media management in the UK outside of the PSB market

• New contracts signed in the year

with major international customers

including Turner, BT,

Entertainment Network, NBC,

Rignet, Canal+ and others,

Decrease due to exit of business

in low margin Wholesale Space

segment, service terminations of

non-credit worthy customers

providing a variety of satellite services from its UK based

facilities including UK DTH, media management,

managed networks and data communications.

• Orderbook stands at £0.3bn

• Launch of a suite of new IP products

• Upgrade of Video-on-Demand platform to meet demand

• SNG assets disposed of in July 2015

Strategy

New customer contracts

Recent/market

developments

Revenue analysis

Copyright © Arqiva Limited 2015 18

Detailed financials

Copyright © Arqiva Limited 2015 19

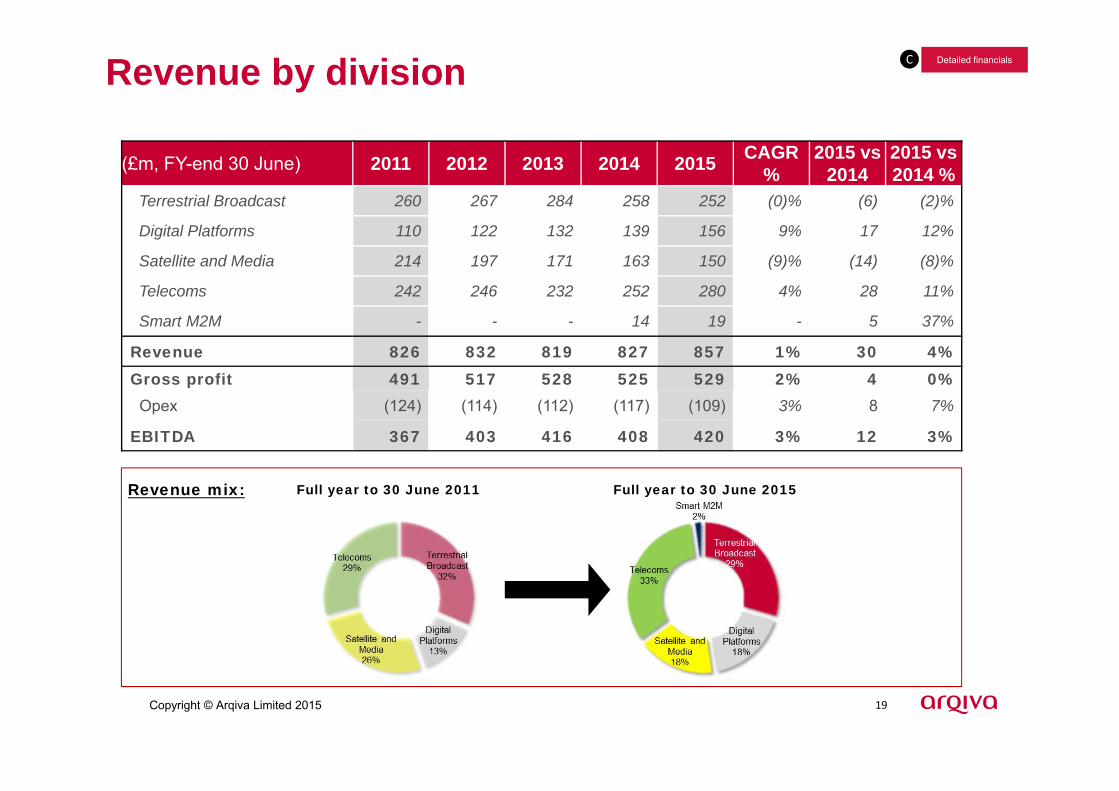

(£m, FY-end 30 June) 2011 2012 2013 2014 2015 CAGR %

2015 vs2014

2015 vs2014 %

Terrestrial Broadcast 260 267 284 258 252 (0)% (6) (2)%

Digital Platforms 110 122 132 139 156 9% 17 12%

Satellite and Media 214 197 171 163 150 (9)% (14) (8)%

Telecoms 242 246 232 252 280 4% 28 11%

Smart M2M - - - 14 19 - 5 37%

Revenue 826 832 819 827 857 1% 30 4%Gross profit 491 517 528 525 529 2% 4 0%

Opex (124) (114) (112) (117) (109) 3% 8 7%

EBITDA 367 403 416 408 420 3% 12 3%

C Detailed financials

Full year to 30 June 2011 Full year to 30 June 2015Revenue mix:

Revenue by division

Copyright © Arqiva Limited 2015 20

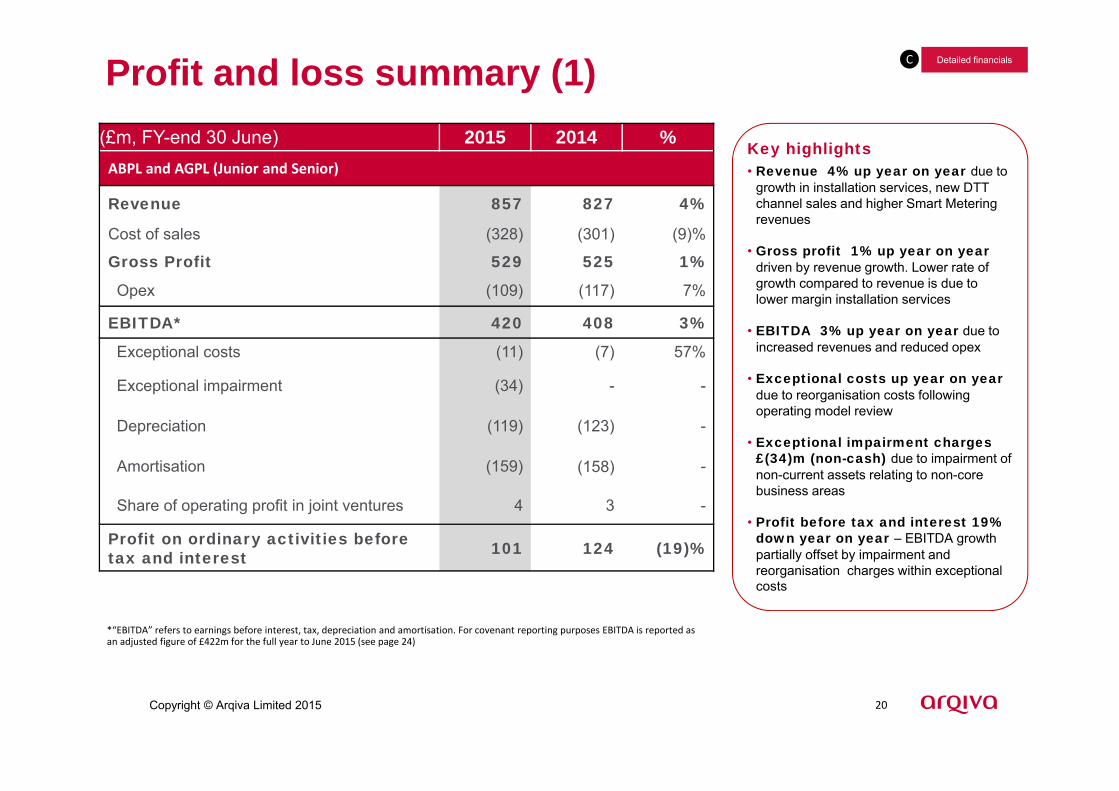

(£m, FY-end 30 June) 2015 2014 %ABPL and AGPL (Junior and Senior)

Revenue 857 827 4%

Cost of sales (328) (301) (9)%

Gross Profit 529 525 1%

Opex (109) (117) 7%

EBITDA* 420 408 3%

Exceptional costs (11) (7) 57%

Exceptional impairment (34) - -

Depreciation (119) (123) -

Amortisation (159) (158) -

Share of operating profit in joint ventures 4 3 -

Profit on ordinary activities before tax and interest 101 124 (19)%

C

Key highlights• Revenue 4% up year on year due to

growth in installation services, new DTT channel sales and higher Smart Metering revenues

• Gross profit 1% up year on yeardriven by revenue growth. Lower rate of growth compared to revenue is due to lower margin installation services

• EBITDA 3% up year on year due to increased revenues and reduced opex

• Exceptional costs up year on year due to reorganisation costs following operating model review

• Exceptional impairment charges £(34)m (non-cash) due to impairment of non-current assets relating to non-core business areas

• Profit before tax and interest 19% down year on year – EBITDA growth partially offset by impairment and reorganisation charges within exceptional costs

Profit and loss summary (1)

*“EBITDA” refers to earnings before interest, tax, depreciation and amortisation. For covenant reporting purposes EBITDA is reported as an adjusted figure of £422m for the full year to June 2015 (see page 24)

Detailed financials

Copyright © Arqiva Limited 2015 21

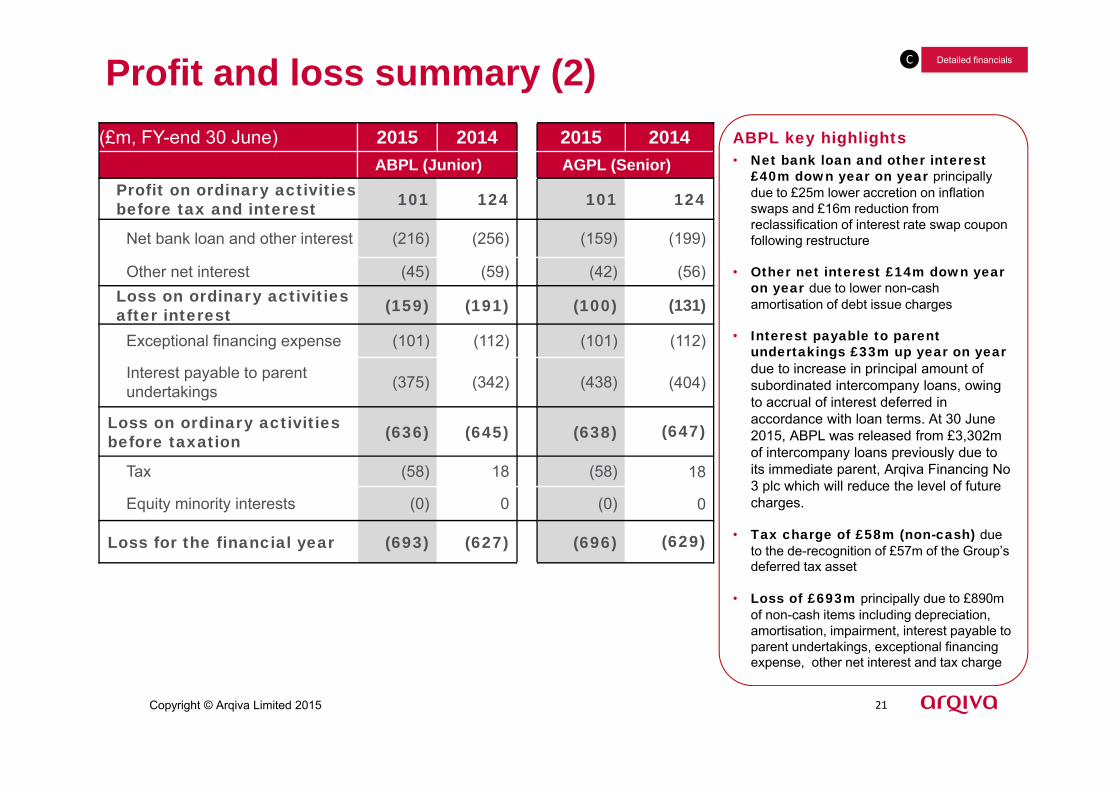

(£m, FY-end 30 June) 2015 2014 2015 2014ABPL (Junior) AGPL (Senior)

Profit on ordinary activities before tax and interest 101 124 101 124

Net bank loan and other interest (216) (256) (159) (199)

Other net interest (45) (59) (42) (56)Loss on ordinary activities after interest (159) (191) (100) (131)

Exceptional financing expense (101) (112) (101) (112)

Interest payable to parentundertakings (375) (342) (438) (404)

Loss on ordinary activitiesbefore taxation (636) (645) (638) (647)

Tax (58) 18 (58) 18

Equity minority interests (0) 0 (0) 0

Loss for the financial year (693) (627) (696) (629)

C

ABPL key highlights• Net bank loan and other interest

£40m down year on year principally due to £25m lower accretion on inflation swaps and £16m reduction from reclassification of interest rate swap coupon following restructure

• Other net interest £14m down year on year due to lower non-cash amortisation of debt issue charges

• Interest payable to parent undertakings £33m up year on yeardue to increase in principal amount of subordinated intercompany loans, owing to accrual of interest deferred in accordance with loan terms. At 30 June 2015, ABPL was released from £3,302m of intercompany loans previously due to its immediate parent, Arqiva Financing No 3 plc which will reduce the level of future charges.

• Tax charge of £58m (non-cash) due to the de-recognition of £57m of the Group’s deferred tax asset

• Loss of £693m principally due to £890m of non-cash items including depreciation, amortisation, impairment, interest payable to parent undertakings, exceptional financing expense, other net interest and tax charge

Profit and loss summary (2) Detailed financials

Copyright © Arqiva Limited 2015 22

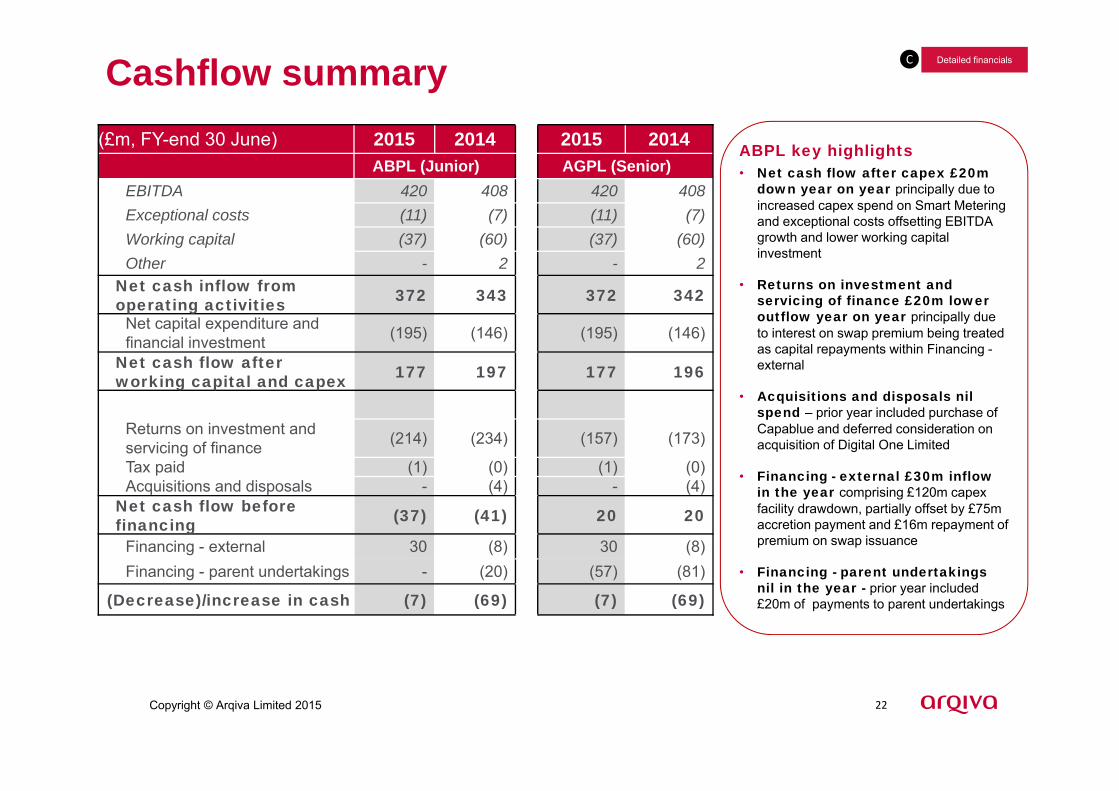

(£m, FY-end 30 June) 2015 2014 2015 2014ABPL (Junior) AGPL (Senior)

EBITDA 420 408 420 408Exceptional costs (11) (7) (11) (7)Working capital (37) (60) (37) (60)Other - 2 - 2

Net cash inflow from operating activities 372 343 372 342

Net capital expenditure and financial investment (195) (146) (195) (146)

Net cash flow after working capital and capex 177 197 177 196

Returns on investment and servicing of finance (214) (234) (157) (173)

Tax paid (1) (0) (1) (0)Acquisitions and disposals - (4) - (4)

Net cash flow before financing (37) (41) 20 20

Financing - external 30 (8) 30 (8)Financing - parent undertakings - (20) (57) (81)

(Decrease)/increase in cash (7) (69) (7) (69)

CCashflow summary

ABPL key highlights• Net cash flow after capex £20m

down year on year principally due to increased capex spend on Smart Metering and exceptional costs offsetting EBITDA growth and lower working capital investment

• Returns on investment and servicing of finance £20m lower outflow year on year principally due to interest on swap premium being treated as capital repayments within Financing -external

• Acquisitions and disposals nil spend – prior year included purchase of Capablue and deferred consideration on acquisition of Digital One Limited

• Financing - external £30m inflow in the year comprising £120m capex facility drawdown, partially offset by £75m accretion payment and £16m repayment of premium on swap issuance

• Financing - parent undertakings nil in the year - prior year included £20m of payments to parent undertakings

Detailed financials

Copyright © Arqiva Limited 2015 23

Maintenance capex is limited and substantial majority of growth capex is contract-related

1 Growth capex also includes cash sales of fixed assets and change in capital creditors.

C

Growth capex:

[1]

FY15 FY14

• Smart Metering £55m £46m

• Radio £23m £16m

• Satellite and Media £17m £31m

• Terrestrial engineering £12m £18m

• MIP and site share £11m £1m

• Smart Water Metering £2m -

• Other smart M2M £4m £2m

• WiFi £3m £7m

• Digital Platforms £1m £2m

• Capital creditors/accruals £34m £(19)m

• Sales of fixed assets £(1)m £(8)m

• Net other £8m £10m

£169m £106m

Detailed financials

Copyright © Arqiva Limited 2015 24

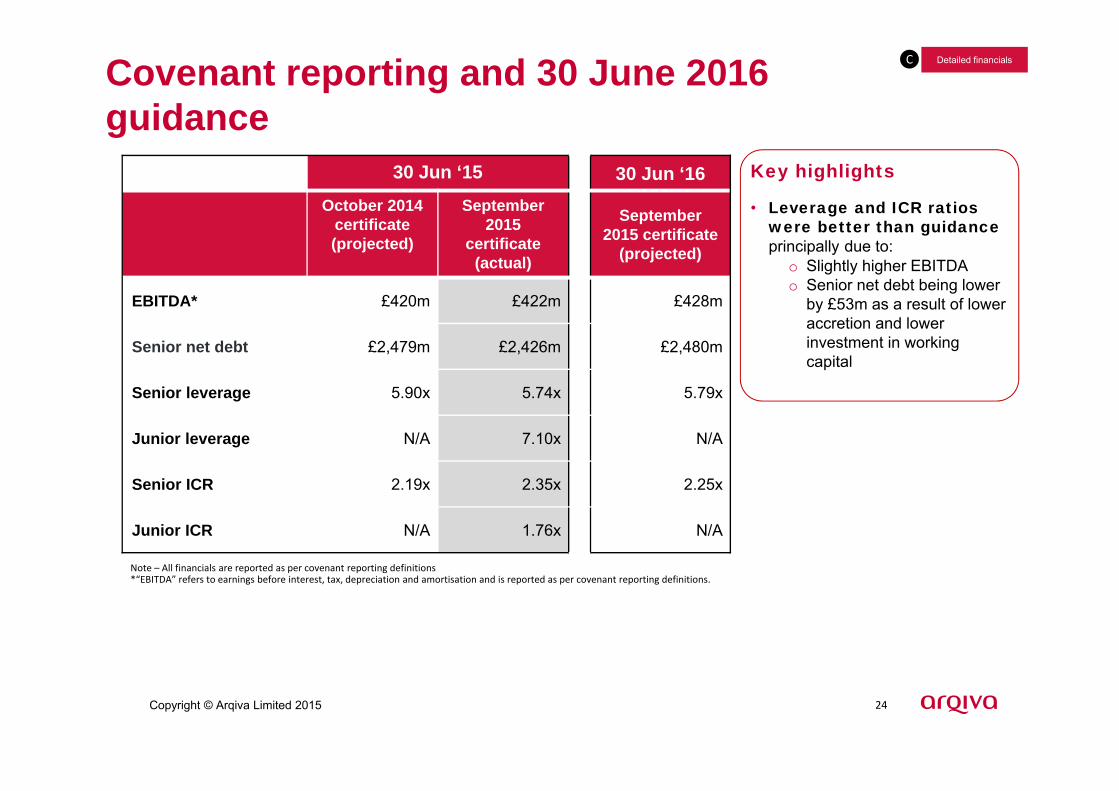

C

30 Jun ‘15 30 Jun ‘16October 2014

certificate (projected)

September 2015

certificate (actual)

September 2015 certificate

(projected)

EBITDA* £420m £422m £428m

Senior net debt £2,479m £2,426m £2,480m

Senior leverage 5.90x 5.74x 5.79x

Junior leverage N/A 7.10x N/A

Senior ICR 2.19x 2.35x 2.25x

Junior ICR N/A 1.76x N/A

Key highlights

• Leverage and ICR ratios were better than guidance principally due to:

o Slightly higher EBITDAo Senior net debt being lower

by £53m as a result of lower accretion and lower investment in working capital

Covenant reporting and 30 June 2016 guidance

Note – All financials are reported as per covenant reporting definitions*“EBITDA” refers to earnings before interest, tax, depreciation and amortisation and is reported as per covenant reporting definitions.

Detailed financials

Copyright © Arqiva Limited 2015 25

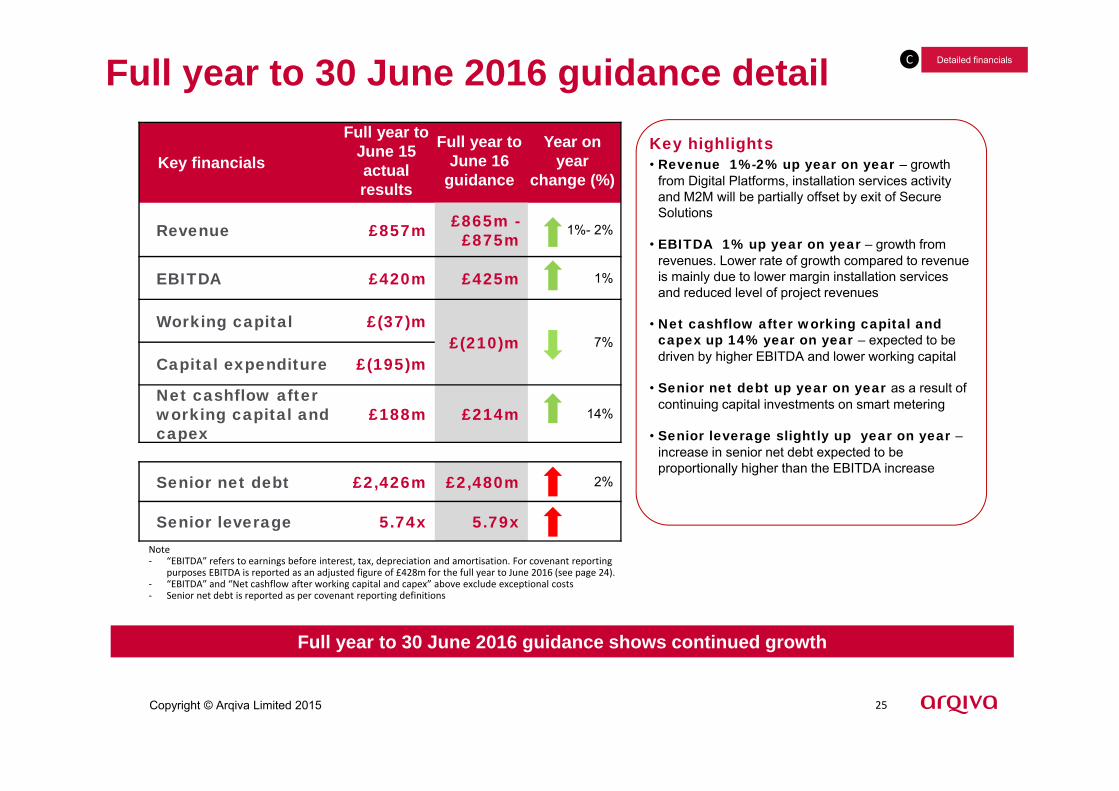

C

Key financials

Full year to June 15 actual results

Full year to June 16

guidance

Year on year

change (%)

Revenue £857m £865m -£875m

1%- 2%

EBITDA £420m £425m 1%

Working capital £(37)m£(210)m 7%

Capital expenditure £(195)m

Net cashflow after working capital and capex

£188m £214m 14%

Senior net debt £2,426m £2,480m 2%

Senior leverage 5.74x 5.79x

Full year to 30 June 2016 guidance detailKey highlights• Revenue 1%-2% up year on year – growth

from Digital Platforms, installation services activity and M2M will be partially offset by exit of Secure Solutions

• EBITDA 1% up year on year – growth from revenues. Lower rate of growth compared to revenue is mainly due to lower margin installation services and reduced level of project revenues

• Net cashflow after working capital and capex up 14% year on year – expected to be driven by higher EBITDA and lower working capital

• Senior net debt up year on year as a result of continuing capital investments on smart metering

• Senior leverage slightly up year on year –increase in senior net debt expected to be proportionally higher than the EBITDA increase

Note‐ “EBITDA” refers to earnings before interest, tax, depreciation and amortisation. For covenant reporting

purposes EBITDA is reported as an adjusted figure of £428m for the full year to June 2016 (see page 24).‐ “EBITDA” and “Net cashflow after working capital and capex” above exclude exceptional costs‐ Senior net debt is reported as per covenant reporting definitions

Detailed financials

Full year to 30 June 2016 guidance shows continued growth

Copyright © Arqiva Limited 2015 26

Financing

Copyright © Arqiva Limited 2015 Company confidential 27

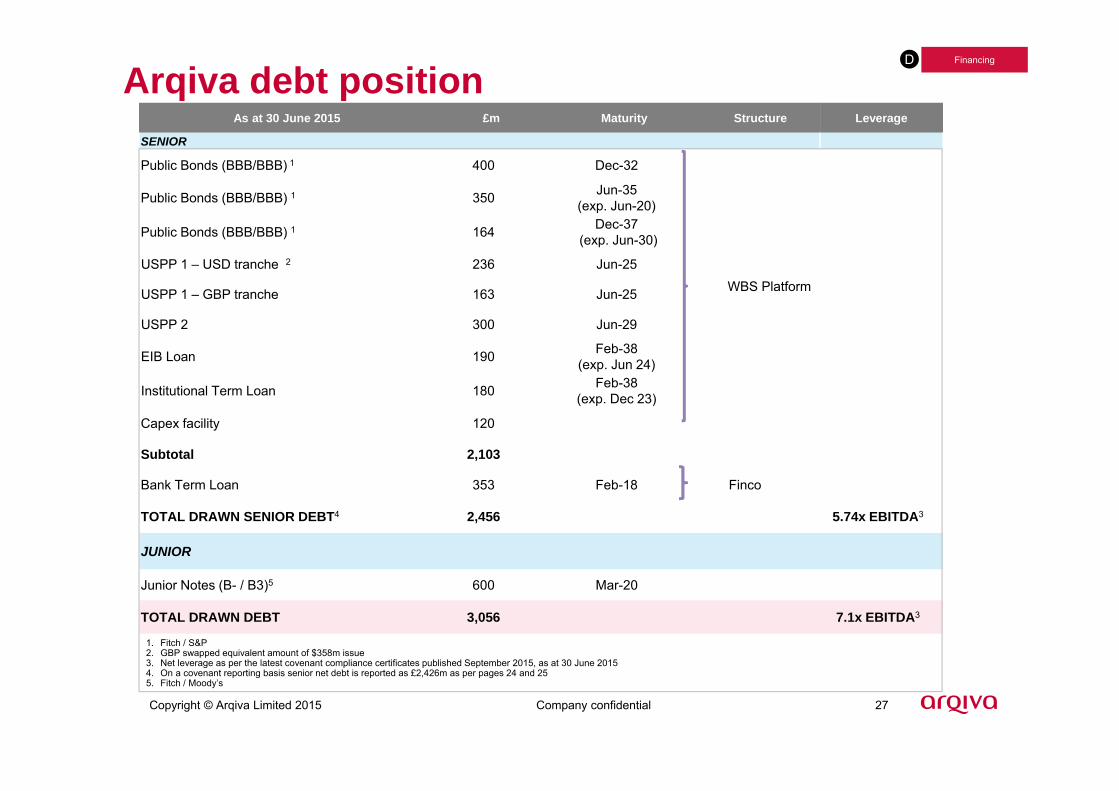

As at 30 June 2015 £m Maturity Structure Leverage

SENIOR

Public Bonds (BBB/BBB) 1 400 Dec-32

Public Bonds (BBB/BBB) 1 350 Jun-35 (exp. Jun-20)

Public Bonds (BBB/BBB) 1 164 Dec-37(exp. Jun-30)

USPP 1 – USD tranche 2 236 Jun-25

USPP 1 – GBP tranche 163 Jun-25

USPP 2 300 Jun-29

EIB Loan 190 Feb-38 (exp. Jun 24)

Institutional Term Loan 180 Feb-38 (exp. Dec 23)

Capex facility 120

Subtotal 2,103

Bank Term Loan 353 Feb-18 Finco

TOTAL DRAWN SENIOR DEBT4 2,456 5.74x EBITDA3

JUNIOR

Junior Notes (B- / B3)5 600 Mar-20

TOTAL DRAWN DEBT 3,056 7.1x EBITDA3

1. Fitch / S&P2. GBP swapped equivalent amount of $358m issue3. Net leverage as per the latest covenant compliance certificates published September 2015, as at 30 June 20154. On a covenant reporting basis senior net debt is reported as £2,426m as per pages 24 and 255. Fitch / Moody’s

D

WBS Platform

Arqiva debt positionFinancing

Copyright © Arqiva Limited 2015 Company confidential 28

Inflation linked swaps► ILS now convert fixed rate liabilities into inflation linked liabilities

► ILS match inflation exposure in Arqiva’s revenue contracts

► Coupon and principal amount accrete with RPI

► ILS are overlaid on fixed rate bond and PP debt

Notional c. £1.3bn

Maturity 2027

Inflation accretion Repayments every 3 years

Mark To market (£925.1m)

RankingSuper senior to senior debt (but carries no voting or enforcement rights)

Long term structural protection – no crystallisation of MTM

£1.1bn notional has no mandatory break £0.2bn notional has break in 2023

First accretion payment of £74.8m was in June 2015Next payment due 30 June 2018

[1]

1. Mark to market reported as at 30 June 2015 excluding accretion.

D Financing

Copyright © Arqiva Limited 2015 29

Arqiva has £1,023m notional principal interest rate swaps comprising £670m in WBS and £353m in Finco

Finco swaps with breaks being progressively replaced with new swaps in WBS with no breaks

£670m swaps now restructured to match underlying EIB, ITL and USPP2 floating rate facilities

Migrating swaps from Finco to WBS has resulted in £213m P&L exceptional financing expenses recognised to date with £206m cash premium received, amortised over remaining life of swaps

Mark to market comprises £189m recorded in the accounts as unamortised swap premium and reported mark to market of £202m as at 30 June 2015o

Interest rate swaps

Platform Notional Maturity Break Underlying Debt Mark to market

Finco £353m 2027 2018 5 year bank £(134)m

Finco Subtotal £353m £(134)m

WBS £180m 2024 None ITL £(57)m

WBS £190m 2024 None EIB £(72)m

WBS £300m 2029 None USPP 2 £(127)m

WBS Subtotal £670m £(256)m

Total £1,023m £(390)m

D Financing

Copyright © Arqiva Limited 2015 30

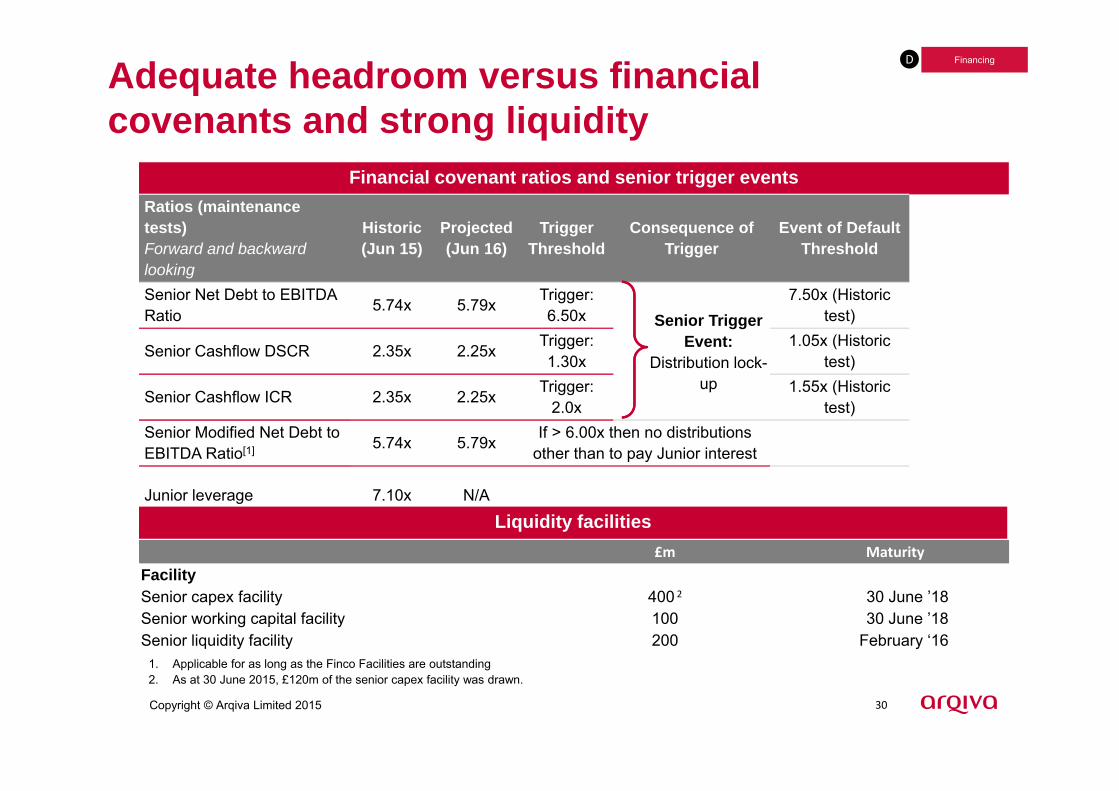

Adequate headroom versus financial covenants and strong liquidity

Financial covenant ratios and senior trigger eventsRatios (maintenance tests)Forward and backward looking

Historic(Jun 15)

Projected (Jun 16)

Trigger Threshold

Consequence of Trigger

Event of Default Threshold

Senior Net Debt to EBITDA Ratio 5.74x 5.79x Trigger:

6.50x 7.50x (Historic

test)

Senior Cashflow DSCR 2.35x 2.25x Trigger: 1.30x

1.05x (Historictest)

Senior Cashflow ICR 2.35x 2.25x Trigger: 2.0x

1.55x (Historictest)

Senior Modified Net Debt to EBITDA Ratio[1] 5.74x 5.79x If > 6.00x then no distributions

other than to pay Junior interest

Junior leverage 7.10x N/A

Senior Trigger Event:

Distribution lock-up

1. Applicable for as long as the Finco Facilities are outstanding2. As at 30 June 2015, £120m of the senior capex facility was drawn.

£m MaturityFacilitySenior capex facility 400 2 30 June ’18Senior working capital facility 100 30 June ’18Senior liquidity facility 200 February ‘16

Liquidity facilities

D Financing

Copyright © Arqiva Limited 2015 31

Summary

Copyright © Arqiva Limited 2015 Company confidential 32

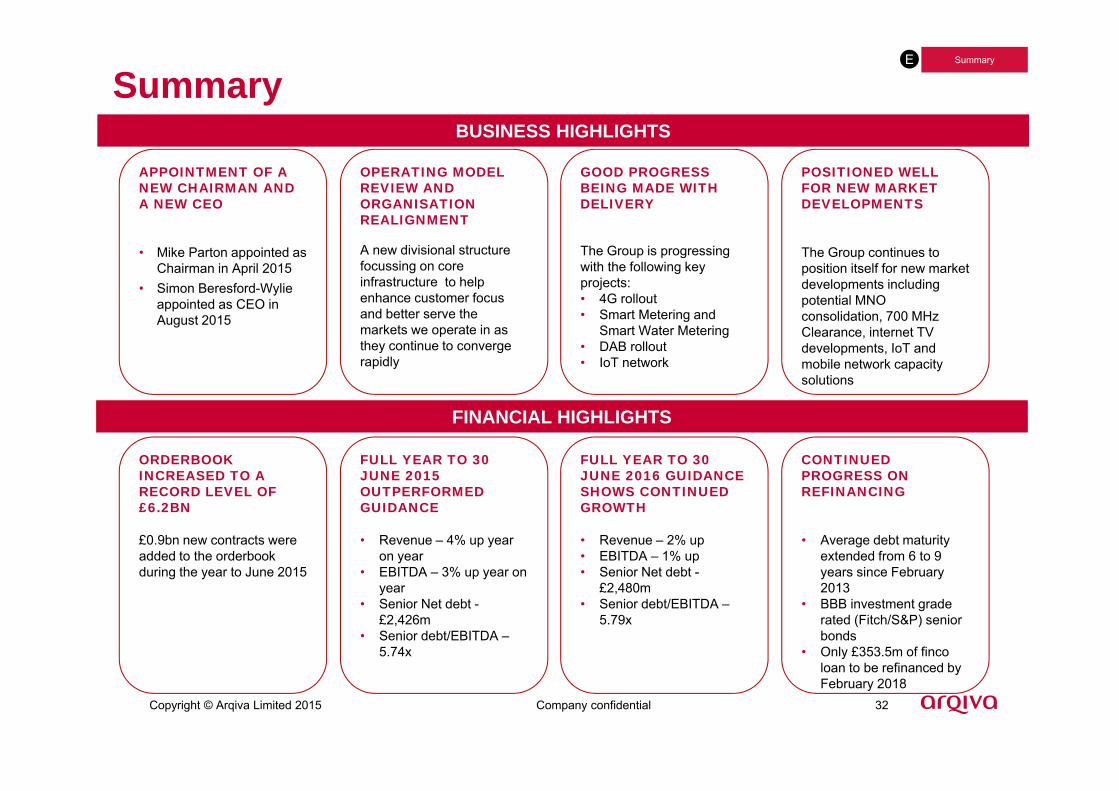

BUSINESS HIGHLIGHTS

FINANCIAL HIGHLIGHTS

OPERATING MODEL REVIEW AND ORGANISATION REALIGNMENT

A new divisional structure focussing on core infrastructure to help enhance customer focus and better serve the markets we operate in as they continue to converge rapidly

POSITIONED WELL FOR NEW MARKET DEVELOPMENTS

The Group continues to position itself for new market developments including potential MNO consolidation, 700 MHz Clearance, internet TV developments, IoT and mobile network capacity solutions

GOOD PROGRESS BEING MADE WITH DELIVERY

The Group is progressing with the following key projects:• 4G rollout• Smart Metering and

Smart Water Metering• DAB rollout• IoT network

ORDERBOOK INCREASED TO A RECORD LEVEL OF £6.2BN

£0.9bn new contracts were added to the orderbookduring the year to June 2015

FULL YEAR TO 30 JUNE 2015 OUTPERFORMED GUIDANCE

• Revenue – 4% up year on year

• EBITDA – 3% up year on year

• Senior Net debt -£2,426m

• Senior debt/EBITDA –5.74x

CONTINUED PROGRESS ON REFINANCING

• Average debt maturity extended from 6 to 9 years since February 2013

• BBB investment grade rated (Fitch/S&P) senior bonds

• Only £353.5m of finco loan to be refinanced by February 2018

E Summary

Summary

APPOINTMENT OF A NEW CHAIRMAN AND A NEW CEO

• Mike Parton appointed as Chairman in April 2015

• Simon Beresford-Wylie appointed as CEO in August 2015

FULL YEAR TO 30 JUNE 2016 GUIDANCE SHOWS CONTINUED GROWTH

• Revenue – 2% up• EBITDA – 1% up• Senior Net debt -

£2,480m• Senior debt/EBITDA –

5.79x

Copyright © Arqiva Limited 2013