asgard employee super account - ernst & young€¦ · about asgard employee super account -...

TRANSCRIPT

Asgard Employee SuperAccount - Ernst & YoungProduct Disclosure Statement

Issued 20 May 2020

About this Product Disclosure StatementContents

This PDS summarises the key information you need to make adecision about the Asgard Employee Super Account - Ernst & Young(Asgard Employee Super). It includes references to important31. About Asgard Employee Super

Account - Ernst & Youngadditional information contained in the Additional Information Bookletwhich is incorporated by reference into, and taken to be included inthis PDS – marked with .32. How super works

The Additional Information Booklet is comprised of three parts:

43. How your Asgard Employee Superaccount works

Part 1 - General (Issued 20 May 2020)

Part 2 - Investment (Issued 20 May 2020)

64. How we invest your money Part 3 - Insurance (Issued 20 May 2020)

You should read the PDS and the Additional Information Booklet(Parts 1 to 3) (which together form part of the PDS) before making adecision about Asgard Employee Super.95. Benefits and features of Asgard

Employee SuperThe information in the PDS and Additional Information Booklet maychange at any time. The updated information, if it is not materiallyadverse, is available at asgardcorporatesuper.com.au/ey/.

In addition, the Asgard Employee Super Account List of AvailableInvestment Options Booklet (List of Available Investment OptionsBooklet) sets out the list of available investment options and includesthe investment selection form.

106. Risks of super

107. Fees and other costs

218. Insurance in your super The PDS, Additional Information Booklet and the List of AvailableInvestment Options Booklet are available free of charge atasgardcorporatesuper.com.au/ey/forms.asp, or by calling us on1800 155 235.

Asgard Employee Super is available from financial advisers acrossAustralia. The offer or invitation to which the PDS and the AdditionalInformation Booklet relates is only available to persons receiving thePDS and the Additional Information Booklet in Australia. The Trusteemay at its discretion refuse to accept applications from any person.

239. How to open an account

About the Trustee

Asgard Employee Super, the PDS and the Additional Information Booklet are issued by BT Funds Management Limited ABN 63 002 916458, AFSL 233724 (‘BTFM’, ‘we’, ‘us’, ‘our’, or ‘the Trustee’), the trustee of, and the issuer of interests in the superannuation fund knownas the Asgard Independence Plan Division Two, ABN 90 194 410 365 (the Fund) which Asgard Employee Super is a part of. BTFM formspart of the Westpac Banking Corporation ABN 33 007 457 141. The Unique Superannuation Identifier (USI) for Asgard Employee Superis ASG0007AU. BTFM is also the trustee of, and the issuer of interests in the BT Institutional Conservative Growth Pooled SuperannuationTrust ABN 87 612 819 950 (the Asgard MySuper PST).

About the Administrator

Asgard Capital Management Ltd ABN 92 009 279 592, AFSL 240695 (‘Asgard’ or ‘the Administrator’) is the custodian and administratorof Asgard Employee Super. Advance Asset Management Limited ABN 98 002 538 329, AFSL 240902 (Advance) is the responsible entityof some of the managed investments available through Asgard Employee Super.

Your rights

The PDS and the Additional Information Booklet have been prepared in accordance with our obligations under superannuation law andthe general law.

We reserve the right to change the features and provisions relating to Asgard Employee Super as contained in the PDS and AdditionalInformation Booklet, but will provide you with notice of any such change or the ability to access such information as required bysuperannuation law and the general law (please see the ‘Keeping you informed’ section of the Additional Information Booklet Part 1 -General for information about how we will keep you informed).

Your rights in relation to Asgard Employee Super are governed by the Asgard Independence Plan – Superannuation Trust Deed dated12 May 1988, as amended from time to time (Trust Deed).

General advice warning

The information in the PDS and Additional Information Booklet is general information only and does not take into account your objectives,financial situation or needs. Before acting on the information in the PDS and the Additional Information Booklet, you should consider theappropriateness of this information having regard to your objectives, financial situation and needs. You should consult a financial adviserto obtain financial advice tailored to suit your personal circumstances. In deciding whether to open, or continue to hold an Asgard EmployeeSuper account, you should consider the PDS and the Additional Information Booklet.

Insurance

Asgard Employee Super - Ernst & Young provides insurance through group policies (Master Policies) which are issued by OnePath LifeLimited ABN 33 009 657 176, AFSL 238341 (‘OnePath’ or ‘the Insurer’) and administered by us. Insurance offered through AsgardEmployee Super Account – Personal Membership category and BT Protection Plans (BTPP) is issued by Westpac Life Insurance ServicesLimited ABN 31 003 149 157, AFSL 233728 (WLISL) and also administered by us. All insurance benefits are subject to the terms andconditions contained in the relevant Master Policies.

The insurance benefits provided by the Master Policies and described in the PDS and Additional Information Booklet are liabilities ofOnePath and WLISL. They are not deposits in, or liabilities of, and are not guaranteed by any other bank or company whether related toOnePath, WLISL or not. We are the policyholder under the Master Policies with OnePath and WLISL.

Consent to be named

Each of Asgard, Advance, WLISL and OnePath has consented to being named in the PDS and the Additional Information Booklet andfor the inclusion of information attributed to it, in the form and context in which it appears, and has not withdrawn its consent before thedate the PDS and the Additional Information Booklet was prepared.

Investment in Asgard Employee Super

BTFM, Asgard and Advance are subsidiaries of Westpac Banking Corporation ABN 33 007 457 141, AFSL 233714 (Westpac).

Your Asgard Employee Super account and the underlying investments (other than deposit products provided by Westpac) do not representdeposits or liabilities of Westpac or any other company in the Westpac Group and are subject to investment risk, including possible delaysin repayment and the loss of income or capital invested. Except as expressly disclosed in the PDS, or the Additional Information Booklet,neither Westpac, nor any other company in the Westpac Group in any way stands behind or guarantees the capital value and/or theperformance of any of the underlying investments or Asgard Employee Super generally.

Related party remuneration

The Trustee, Asgard, Advance, Westpac and other companies in the Westpac Group receive fees in connection with operating AsgardEmployee Super or the underlying investments (as applicable). For more information, see the 'Fees and other costs' section in the PDSand the Additional Information Booklet Part 1 – General. You can also find information on executive remuneration at bt.com.au > AboutBT > Who we are > Additional disclosure > BT Funds Management Limited.

1. About AsgardEmployee SuperAccount - Ernst &Young

Brought to you by BTBT has been helping Australians create and manage wealthsince 1969.

BT provides a diverse range of investment options, includingfunds managed by local and international investmentmanagers.

BT is a wealth management specialist that’s wholly owned byWestpac.

Overview of Asgard Employee SuperAsgard Employee Super is a super product that has beenselected by Ernst & Young (EY) as the default super fund for theiremployees.

It has the added benefit of also being available for an employee'sspouse and family to join. Asgard Employee Super offers youchoice and flexibility with your retirement savings. You receiveconsolidated transaction and valuation reporting on your AsgardEmployee Super investments, as well as the convenience of onecentral point of contact for all your account queries.

Asgard Employee Super offers a MySuper authorised product,Asgard MySuper, and the investment option for this product isthe Asgard MySuper Lifestage Investment Option. The AsgardMySuper Lifestage Investment Option invests into the BTInstitutional Conservative Growth Pooled Superannuation TrustABN 87 612 819 950 (Asgard MySuper PST). The AsgardMySuper PST is a pooled superannuation fund which is onlyavailable for investment by superannuation funds. Alternatively,you can choose from a diverse range of investment options inAsgard Separately Managed Account – Funds (Asgard SMA -Funds) and Asgard Managed Profiles. For more information,please see the ‘4. How we invest your money’ section of thisPDS.

You can find the latest product dashboard for the AsgardMySuper Lifestage Investment Options atasgardcorporatesuper.com.au/ey/ > Investment options > AsgardMySuper.

Please visit asgardcorporatesuper.com.au/ey/ for the latestproduct updates on Asgard Employee Super.

You can find the latest versions of all documentsat asgardcorporatesuper.com.au/ey/.

For more general information about Asgard Employee Super- Ernst & Young and what it offers such as consolidatedreporting, investment expertise accessible through AsgardEmployee Super, the types of insurance cover available andspouse and family accounts please see '1. About AsgardEmployee Super - Ernst & Young' in the AdditionalInformation Booklet Part 1 - General.

2. How super works

About superSuper is a means of saving for your retirement which is in partcompulsory. It may become one of the biggest investments youmake in your lifetime. Nearly every Australian has the right tochoose the super fund into which their employer pays their super.The Australian Government has provided tax concessions andother benefits which generally make super one of the bestlong-term investment vehicles.

ContributionsDifferent types of contributions can be made to super – forexample, employer, personal and government contributions.Generally, if you’re under 65 years of age, contributions can beaccepted from you, your spouse, your employer and thegovernment. Once you turn 65, there are strict rules aroundaccepting contributions. Asgard Employee Super can accept allSuperannuation Guarantee (SG) contributions from youremployer. Limits (known as ‘caps’) generally apply to the amountof most contributions that can be made to your super. If youexceed the caps, additional tax is payable.

For more information on choosing your own super fund,ways to add to your super, acceptable contributions

and contributions caps please see the 'Choice of fund','Adding to your super', 'Acceptable contributions','Additional information for certain contributions' and'Contributions caps' sections in '2. How super works' andthe 'Adding to your super' section in '3. How your accountworks' in the Additional Information Booklet Part 1 - General.

WithdrawalsLimitations apply to withdrawals because your super is intendedto provide for your retirement. Generally, you cannot access yoursuper until you turn 65, or retire after reaching your preservationage (between 55 and 60, depending on your date of birth). Inlimited circumstances, your super can be accessed before youretire if a condition of release is met.

For more information on accessing your super, yourpreservation age, unclaimed money, temporary residents

and illiquid or suspended managed investments please seethe 'Access to your super', 'Your preservation age','Unclaimed money' and 'Temporary residents' sections in'2. How super works' and the 'Accessing your AsgardEmployee Super', 'Withdrawals' and 'Illiquid or suspendedmanaged investments' sections in '3. How your accountworks' in the Additional Information Booklet Part 1 - General.

3

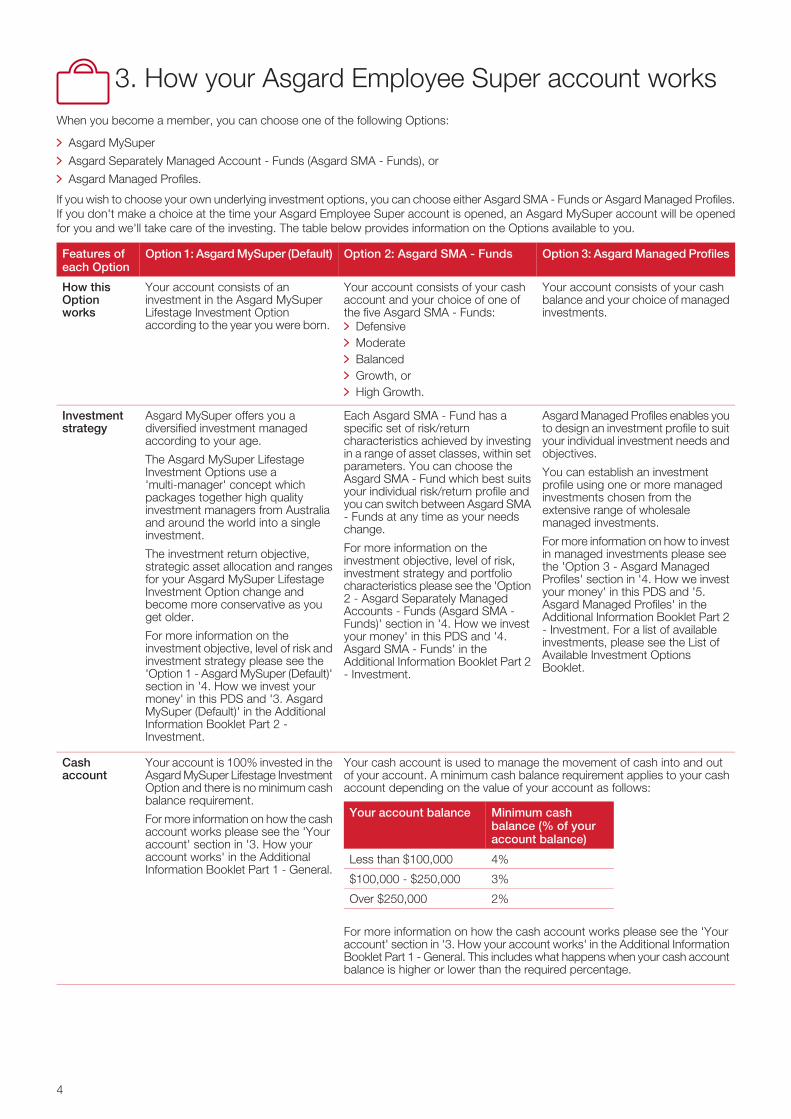

3. How your Asgard Employee Super account worksWhen you become a member, you can choose one of the following Options:

Asgard MySuper

Asgard Separately Managed Account - Funds (Asgard SMA - Funds), or

Asgard Managed Profiles.

If you wish to choose your own underlying investment options, you can choose either Asgard SMA - Funds or Asgard Managed Profiles.If you don't make a choice at the time your Asgard Employee Super account is opened, an Asgard MySuper account will be openedfor you and we'll take care of the investing. The table below provides information on the Options available to you.

Option 3: Asgard Managed ProfilesOption 2: Asgard SMA - Funds Option 1: Asgard MySuper (Default)Features ofeach Option

Your account consists of your cashbalance and your choice of managedinvestments.

Your account consists of your cashaccount and your choice of one ofthe five Asgard SMA - Funds:

Your account consists of aninvestment in the Asgard MySuperLifestage Investment Optionaccording to the year you were born.

How thisOptionworks

DefensiveModerateBalancedGrowth, or High Growth.

Asgard Managed Profiles enables youto design an investment profile to suityour individual investment needs andobjectives.

Each Asgard SMA - Fund has aspecific set of risk/returncharacteristics achieved by investingin a range of asset classes, within set

Asgard MySuper offers you adiversified investment managedaccording to your age.

The Asgard MySuper LifestageInvestment Options use a'multi-manager' concept which

Investmentstrategy

You can establish an investmentprofile using one or more managedinvestments chosen from theextensive range of wholesalemanaged investments.

parameters. You can choose theAsgard SMA - Fund which best suitsyour individual risk/return profile andyou can switch between Asgard SMA- Funds at any time as your needschange.

packages together high qualityinvestment managers from Australiaand around the world into a singleinvestment. For more information on how to invest

in managed investments please seethe 'Option 3 - Asgard Managed

For more information on theinvestment objective, level of risk,investment strategy and portfolio

The investment return objective,strategic asset allocation and rangesfor your Asgard MySuper Lifestage Profiles' section in '4. How we investcharacteristics please see the 'OptionInvestment Option change andbecome more conservative as youget older.

your money' in this PDS and '5.Asgard Managed Profiles' in theAdditional Information Booklet Part 2

2 - Asgard Separately ManagedAccounts - Funds (Asgard SMA -Funds)' section in '4. How we invest

For more information on theinvestment objective, level of risk andinvestment strategy please see the

- Investment. For a list of availableinvestments, please see the List ofAvailable Investment OptionsBooklet.

your money' in this PDS and '4.Asgard SMA - Funds' in theAdditional Information Booklet Part 2- Investment.'Option 1 - Asgard MySuper (Default)'

section in '4. How we invest yourmoney' in this PDS and '3. AsgardMySuper (Default)' in the AdditionalInformation Booklet Part 2 -Investment.

Your cash account is used to manage the movement of cash into and outof your account. A minimum cash balance requirement applies to your cashaccount depending on the value of your account as follows:

Your account is 100% invested in theAsgard MySuper Lifestage InvestmentOption and there is no minimum cashbalance requirement.

Cashaccount

Minimum cashbalance (% of youraccount balance)

Your account balanceFor more information on how the cashaccount works please see the 'Youraccount' section in '3. How youraccount works' in the AdditionalInformation Booklet Part 1 - General.

4%Less than $100,000

3%$100,000 - $250,000

2%Over $250,000

For more information on how the cash account works please see the 'Youraccount' section in '3. How your account works' in the Additional InformationBooklet Part 1 - General. This includes what happens when your cash accountbalance is higher or lower than the required percentage.

4

Option 3: Asgard Managed ProfilesOption 2: Asgard SMA - Funds Option 1: Asgard MySuper (Default)Features ofeach Option

Taxed at a maximum rate of up to 15%1. Tax is deducted from your cashaccount through Pay As You Go (PAYG) Tax Instalments, annual taxpayments, on the closure of your account or if you choose to move to AsgardMySuper.

Taxed at a maximum rate of up to15%1. Tax is deducted through PayAs You Go (PAYG) Tax Instalments,annual tax payments and on closure

Tax onconcessionalcontributions

of your account. Tax is deducted from For more information on tax on concessional contributions for Asgard SMA- Funds and Asgard Managed Profiles please see the 'How tax is calculatedand paid' section in '4. How super is taxed' in the Additional InformationBooklet Part 1 - General.

your account which will reduce yourinvestment in the Asgard MySuperLifestage Investment Option.

For more information on tax onconcessional contributions for AsgardMySuper please see the 'How tax iscalculated and paid' section in '4.How super is taxed' in the AdditionalInformation Booklet Part 1 - General.

Taxed at a maximum rate of up to 15%, while certain capital gains may betaxed at a concessional rate of 10%.

Taxed at a maximum rate of up to15%, while certain capital gains maybe taxed at a concessional rate of10%.

Tax onearnings(investmentincome andcapitalgains)

Tax is deducted from your cash account when the Fund is required to makePAYG Tax Instalments, annual tax payments, on the closure of your accountor if you choose to move to Asgard MySuper.

For more information on tax on earnings for Asgard SMA - Funds and AsgardManaged Profiles please see the 'Earnings' and 'Valuations' sections in '3.How your account works' and the 'How tax is calculated and paid' sectionin '4. How super is taxed' in the Additional Information Booklet Part 1 -General.

Tax on investment income and capitalgains is reflected in the AsgardMySuper PST unit price.

For more information on tax onearnings for Asgard MySuper pleasesee the 'Earnings' and 'Valuations'section in '3. How your accountworks' and the 'How tax is calculatedand paid' section in '4. How super istaxed' in the Additional InformationBooklet Part 1 - General.

If you're aged 60 or over, withdrawals from your account are generally tax-free. Tax onwithdrawals If you're under age 60, you will be taxed on lump-sum withdrawals as follows:

Rate of taxComponent

NilTax-free component

If under preservation age (between 55 and 60 depending on yourdate of birth) tax is paid at 20% plus Medicare levy.

Taxable component (taxedelement)

If aged between preservation age and age 59, tax-free up to the lowrate cap2, then 15% plus Medicare levy.

Different tax rates and rules for withdrawing your super may apply if you are, or were, a holder of a temporary visaunder the Migration Act 1958.

For more information on tax on withdrawals please see the 'Tax on benefits', 'Rolling over your super to anotherfund', 'Taking a cash lump sum benefit' and 'Tax payable on death benefits' sections in '4. How super is taxed' inthe Additional Information Booklet Part 1 - General.

1 Additional tax may apply to high income earners. For more information, please see the 'High income earners 15% additional tax (known as Division293 tax)' section in '4. How super is taxed' in the Additional Information Booklet Part 1 - General.

2 The low rate cap (or lifetime limit) may change from time to time. Up to date information is available at ato.gov.au.

Important: When deciding how you want your super to be invested, you must consider the likely investment return, risk andyour investment timeframe.

Whilst you can contribute as much as you like, there are limits (caps) on how much you can contribute without penalty. The twomain caps available to you are the concessional and non-concessional caps. It's your responsibility to make sure you don't exceedthem.

You should provide your Tax File Number (TFN) as part of opening your account. If you don't supply us with your TFN, we're requiredunder law to only accept employer contributions and additional tax may apply.

5

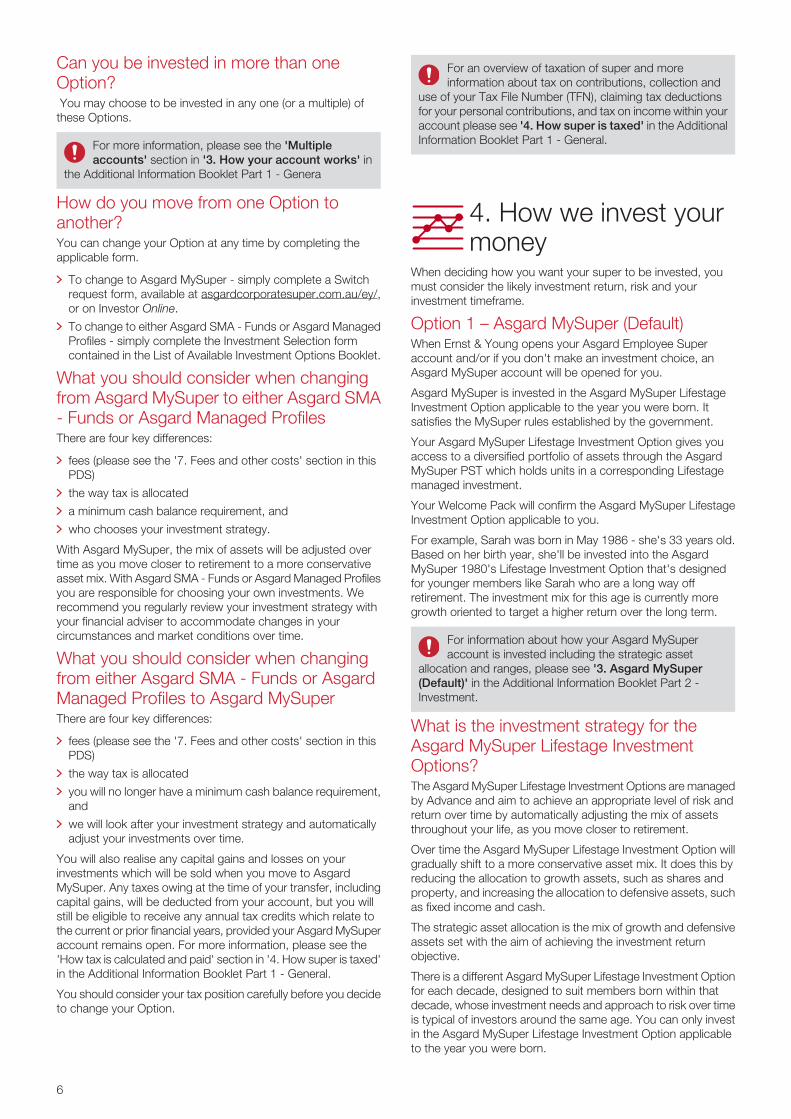

Can you be invested in more than oneOption? You may choose to be invested in any one (or a multiple) ofthese Options.

For more information, please see the 'Multipleaccounts' section in '3. How your account works' in

the Additional Information Booklet Part 1 - Genera

How do you move from one Option toanother?You can change your Option at any time by completing theapplicable form.

To change to Asgard MySuper - simply complete a Switchrequest form, available at asgardcorporatesuper.com.au/ey/,or on Investor Online.

To change to either Asgard SMA - Funds or Asgard ManagedProfiles - simply complete the Investment Selection formcontained in the List of Available Investment Options Booklet.

What you should consider when changingfrom Asgard MySuper to either Asgard SMA- Funds or Asgard Managed ProfilesThere are four key differences:

fees (please see the '7. Fees and other costs' section in thisPDS)

the way tax is allocated

a minimum cash balance requirement, and

who chooses your investment strategy.

With Asgard MySuper, the mix of assets will be adjusted overtime as you move closer to retirement to a more conservativeasset mix. With Asgard SMA - Funds or Asgard Managed Profilesyou are responsible for choosing your own investments. Werecommend you regularly review your investment strategy withyour financial adviser to accommodate changes in yourcircumstances and market conditions over time.

What you should consider when changingfrom either Asgard SMA - Funds or AsgardManaged Profiles to Asgard MySuperThere are four key differences:

fees (please see the '7. Fees and other costs' section in thisPDS)

the way tax is allocated

you will no longer have a minimum cash balance requirement,and

we will look after your investment strategy and automaticallyadjust your investments over time.

You will also realise any capital gains and losses on yourinvestments which will be sold when you move to AsgardMySuper. Any taxes owing at the time of your transfer, includingcapital gains, will be deducted from your account, but you willstill be eligible to receive any annual tax credits which relate tothe current or prior financial years, provided your Asgard MySuperaccount remains open. For more information, please see the'How tax is calculated and paid' section in '4. How super is taxed'in the Additional Information Booklet Part 1 - General.

You should consider your tax position carefully before you decideto change your Option.

For an overview of taxation of super and moreinformation about tax on contributions, collection and

use of your Tax File Number (TFN), claiming tax deductionsfor your personal contributions, and tax on income within youraccount please see '4. How super is taxed' in the AdditionalInformation Booklet Part 1 - General.

4. How we invest yourmoney

When deciding how you want your super to be invested, youmust consider the likely investment return, risk and yourinvestment timeframe.

Option 1 – Asgard MySuper (Default)When Ernst & Young opens your Asgard Employee Superaccount and/or if you don't make an investment choice, anAsgard MySuper account will be opened for you.

Asgard MySuper is invested in the Asgard MySuper LifestageInvestment Option applicable to the year you were born. Itsatisfies the MySuper rules established by the government.

Your Asgard MySuper Lifestage Investment Option gives youaccess to a diversified portfolio of assets through the AsgardMySuper PST which holds units in a corresponding Lifestagemanaged investment.

Your Welcome Pack will confirm the Asgard MySuper LifestageInvestment Option applicable to you.

For example, Sarah was born in May 1986 - she's 33 years old.Based on her birth year, she'll be invested into the AsgardMySuper 1980's Lifestage Investment Option that's designedfor younger members like Sarah who are a long way offretirement. The investment mix for this age is currently moregrowth oriented to target a higher return over the long term.

For information about how your Asgard MySuperaccount is invested including the strategic asset

allocation and ranges, please see '3. Asgard MySuper(Default)' in the Additional Information Booklet Part 2 -Investment.

What is the investment strategy for theAsgard MySuper Lifestage InvestmentOptions?The Asgard MySuper Lifestage Investment Options are managedby Advance and aim to achieve an appropriate level of risk andreturn over time by automatically adjusting the mix of assetsthroughout your life, as you move closer to retirement.

Over time the Asgard MySuper Lifestage Investment Option willgradually shift to a more conservative asset mix. It does this byreducing the allocation to growth assets, such as shares andproperty, and increasing the allocation to defensive assets, suchas fixed income and cash.

The strategic asset allocation is the mix of growth and defensiveassets set with the aim of achieving the investment returnobjective.

There is a different Asgard MySuper Lifestage Investment Optionfor each decade, designed to suit members born within thatdecade, whose investment needs and approach to risk over timeis typical of investors around the same age. You can only investin the Asgard MySuper Lifestage Investment Option applicableto the year you were born.

6

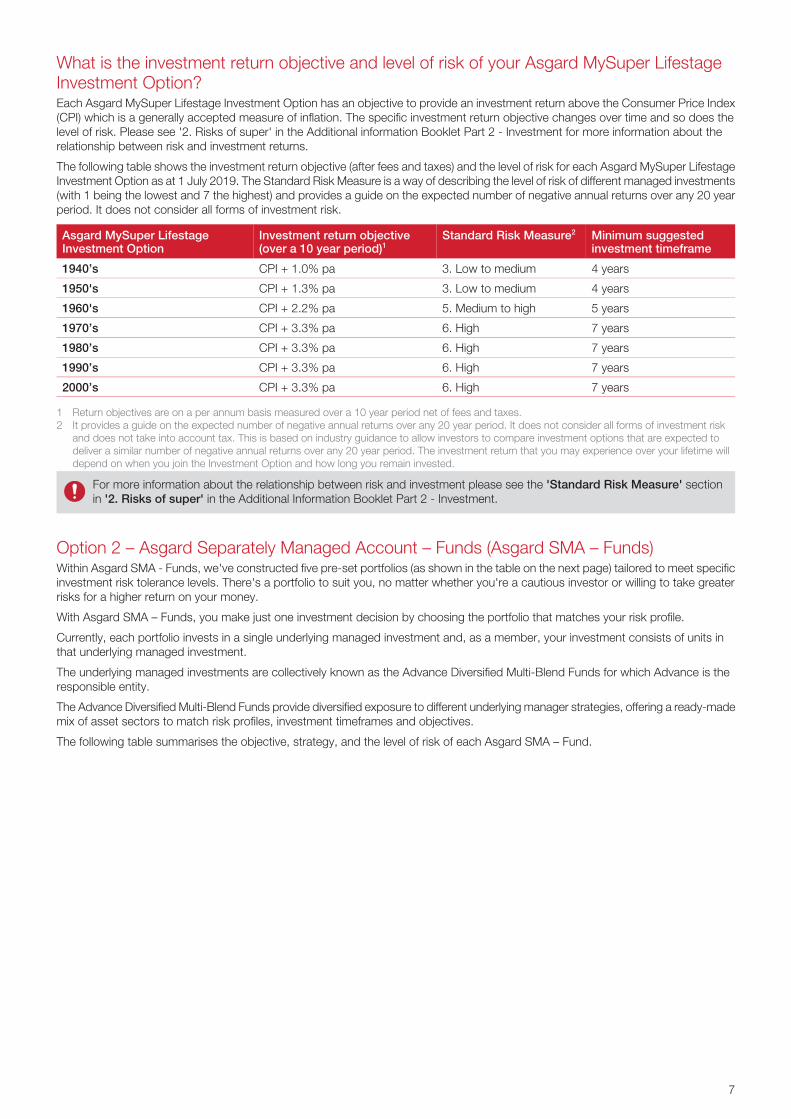

What is the investment return objective and level of risk of your Asgard MySuper LifestageInvestment Option?Each Asgard MySuper Lifestage Investment Option has an objective to provide an investment return above the Consumer Price Index(CPI) which is a generally accepted measure of inflation. The specific investment return objective changes over time and so does thelevel of risk. Please see '2. Risks of super' in the Additional information Booklet Part 2 - Investment for more information about therelationship between risk and investment returns.

The following table shows the investment return objective (after fees and taxes) and the level of risk for each Asgard MySuper LifestageInvestment Option as at 1 July 2019. The Standard Risk Measure is a way of describing the level of risk of different managed investments(with 1 being the lowest and 7 the highest) and provides a guide on the expected number of negative annual returns over any 20 yearperiod. It does not consider all forms of investment risk.

Minimum suggestedinvestment timeframe

Standard Risk Measure2Investment return objective(over a 10 year period)1

Asgard MySuper LifestageInvestment Option

4 years3. Low to mediumCPI + 1.0% pa1940’s

4 years3. Low to medium CPI + 1.3% pa1950's

5 years5. Medium to high CPI + 2.2% pa1960's

7 years6. HighCPI + 3.3% pa1970’s

7 years6. HighCPI + 3.3% pa1980’s

7 years6. HighCPI + 3.3% pa1990’s

7 years6. HighCPI + 3.3% pa2000’s

1 Return objectives are on a per annum basis measured over a 10 year period net of fees and taxes.2 It provides a guide on the expected number of negative annual returns over any 20 year period. It does not consider all forms of investment risk

and does not take into account tax. This is based on industry guidance to allow investors to compare investment options that are expected todeliver a similar number of negative annual returns over any 20 year period. The investment return that you may experience over your lifetime willdepend on when you join the Investment Option and how long you remain invested.

For more information about the relationship between risk and investment please see the 'Standard Risk Measure' sectionin '2. Risks of super' in the Additional Information Booklet Part 2 - Investment.

Option 2 – Asgard Separately Managed Account – Funds (Asgard SMA – Funds)Within Asgard SMA - Funds, we've constructed five pre-set portfolios (as shown in the table on the next page) tailored to meet specificinvestment risk tolerance levels. There's a portfolio to suit you, no matter whether you're a cautious investor or willing to take greaterrisks for a higher return on your money.

With Asgard SMA – Funds, you make just one investment decision by choosing the portfolio that matches your risk profile.

Currently, each portfolio invests in a single underlying managed investment and, as a member, your investment consists of units inthat underlying managed investment.

The underlying managed investments are collectively known as the Advance Diversified Multi-Blend Funds for which Advance is theresponsible entity.

The Advance Diversified Multi-Blend Funds provide diversified exposure to different underlying manager strategies, offering a ready-mademix of asset sectors to match risk profiles, investment timeframes and objectives.

The following table summarises the objective, strategy, and the level of risk of each Asgard SMA – Fund.

7

Minimumsuggestedinvestmenttimeframe

StandardRiskMeasure

Investment Strategy ObjectiveAsgardSMA -Funds

3 years3. Low tomedium

The Fund invests in a diverse mix ofassets with a majority (about 70%) indefensive assets and a modestinvestment (about 30%) in growthassets.

To provide income with a low risk of capitalloss over the short to medium-term withsome capital growth over the long-term.

Defensive

4 years5. Medium tohigh

The Fund invests in a mix of defensiveassets (around 50%) and growth assets(around 50%).

To provide relatively stable total returns(before fees and taxes) over the short tomedium-term with some capital growthover the long-term through a diversified mixof growth and defensive assets.

Moderate

5 years5. Medium tohigh

The Fund invests in a diverse mix ofassets with both income-producingassets (around 30%) and growth assets(around 70%).

To provide moderate to high total returns(before fees and taxes) over themedium-term from a combination of capitalgrowth and income through a diversifiedmix of growth and defensive assets.

Balanced

6 years6. HighThe Fund invests in a diverse mix ofassets with an emphasis (about 85%)on growth-oriented assets andinvestment (about 15%) in defensiveassets.

To provide high returns (before fees andtaxes) over the long-term through capitalgrowth by investing predominantly ingrowth assets.

Growth

7 years6. HighThe Fund invests primarily in growthassets (about 100%).

To provide high total returns (before feesand taxes) over the long-term throughcapital growth by investing predominantlyin growth assets.

HighGrowth

For more information about the investment objectives and the investment process of the Advance Diversified Multi-BlendFunds and the key characteristics of each of the five Asgard SMA - Funds please see '4. Asgard SMA - Funds' in the

Additional Information Booklet Part 2 - Investment.

Option 3 – Asgard Managed ProfilesAsgard Managed Profiles enables you to design an investment profile from the extensive range of managed investments. Extensiveresearch is conducted by us to provide you with a list of managed investments you are able to invest in through Asgard EmployeeSuper. The list of managed investments you can invest in is available in the List of Available Investment Options Booklet. You, andyour financial adviser (if you have one), can establish an investment profile using one or more managed investments chosen from theextensive range of wholesale managed investments.

For more information about managed investments and what is involved in investing in them through Asgard Managed Profilesplease see '5. Asgard Managed Profiles' in the Additional Information Booklet Part 2 - Investment. For a list of available

investments and the Investment Selection form please see the List of Available Investment Options Booklet.

For more information about your initial investment in Asgard Employee Super, changing your investment, making an investmentchoice, changes to investment managers and managed investments and labour standards and environmental, social and ethicalconsiderations please see the 'Investing' section in '3. How your account works' in the Additional Information Booklet Part 1 -General and '1. About investing' in the Additional Information Booklet Part 2 - Investment.

8

5. Benefits and features of Asgard Employee Super

Ernst & Young (EY) has selected Asgard Employee Super as theirdefault corporate super fund. Here we highlight the key benefitsof Asgard Employee Super.

Asgard MySuperAsgard MySuper offers a simple super solution for members whoprefer not to play an active role with super. It automatically adjustsyour investment mix over time to achieve an appropriate level ofrisk and return for each lifestage.

Wide range of investment options andfeaturesWe offer a broad range of investment options to suit your financialsituation, goals and preference for risk. You can choose to leavethe investing to us, select a diversified portfolio or invest inmanaged investments.

For information about communications from investmentmanagers and voting rights, and what happens when

there are adverse changes to underlying managed investmentsplease see '7. Other information' in the Additional InformationBooklet Part 1 - General.

InsuranceEY has designed a default insurance package for its employees.This includes Life Protection and Total and PermanentDisablement (TPD) through Master Policies which are issued byOnePath. For permanent employees, EY pays an additional supercontribution to cover your insurance fees. For more information,please see the Additional Information Booklet Part 3 – Insurance.

Benefits of group-buying powerHaving your super in Asgard Employee Super may give youaccess to group discounts on fees and the cost of insurance.Even small discounts in fees and costs may have a big impacton your long-term returns.

Access to your account information at anytimeYou can monitor your account online via Investor Onlineat investoronline.info/. You can also find out if you have any lostsuper with SuperCheck.

Focused on your financial wellbeingYou'll have access to our unique wellbeing program, which isbuilt on our philosophy that financial wellbeing is closely linkedto your health, and your connection with family, community andwork.

Our program includes an array of benefits, including educationaround each aspect of wellbeing, interactive tools like WealthReview and exclusive offers through Benefits Now.

Benefits Now packageWe’ve negotiated great deals, offers and discounts with majorretailers and brands as part of our member benefits package –Benefits Now. For details of some of the many savings you canaccess with Benefits Now, please visit Investor Online.

When you change jobsWhen we’re told that you have left EY, you and your spouse andfamily member(s) (if applicable) will automatically become‘Personal members’ within Asgard Employee Super. This means

you can keep your Asgard Employee Super account and manyof its benefits regardless of where you work. If you and yourspouse and family member(s) (if applicable) become a ‘Personalmember’, any EY-related discounts on fees will ordinarily cease.Any employer-tiering discount on the Administration fee willgenerally cease and your insurance fees may change. Foremployee members, your insurance benefits may change or maycease when you become a ‘Personal member’.

For more information about what happens when youchange jobs please see the 'Changing jobs -

Becoming a Personal member with Asgard EmployeeSuper' section in '3. How your account works' in theAdditional Information Booklet Part 1 - General.

Keeping you informedWe keep you up-to-date with important changes to your AsgardEmployee Super account:

When you join – You’ll receive a Welcome Pack with youraccount details and access details for Investor Online,

Ongoing – You’ll receive half-yearly Investor Reports detailingyour account information for the period. You’ll also receiveconfirmation of certain transactions. The latest Axis magazineand Annual Report are available via Investor Online.

For more information about how you can keepup-to-date with your account please see '6. Keeping

you informed' in the Additional Information Booklet Part 1 -General.

Spouse and family accountsYour spouse and other family members can also open an accountin Asgard Employee Super, and will receive the same feediscounts as you. They can also apply for insurance through theBT Protection Plans.

For more information about spouse and family accountssee the 'Opening an account' section in '3. How your

account works' in the Additional Information Booklet Part 1- General.

When you retireYou can access your super benefits or you can transfer them tothe Asgard Allocated Pension Account, or another Asgardpension product without selling down your managed investments.The Asgard Allocated Pension Account is issued by us. You canobtain a copy of the PDS by calling us on 1800 155 235, or fromyour financial adviser. You should consider the PDS beforemaking a decision about the Asgard Allocated Pension Account.

For information about the features of your AsgardEmployee Super including accessing your super, what

will occur if you wish to close your account and how you cannominate who you like us to pay your death benefit to pleasesee the 'Accessing your Asgard Employee Super', 'Closingyour account' and 'What happens if you die?' sections in'3. How your account works' in the Additional InformationBooklet Part 1 - General.

9

6. Risks of superAll investments involve risk. Super funds may invest in a rangeof asset classes, including cash, fixed interest, property andshares, which have different levels of risk.

Asgard Employee Super offers a variety of investment options,containing different weightings of these asset classes. The likelyinvestment return, and the risk of losing money, is different foreach investment option depending on the underlying mix ofassets.

Generally, the higher the potential return of an investment overthe longer term, the greater the level of risk of loss in the shorterterm.

What are the risks involved?When considering your investment in super, it’s important tounderstand that:

investments will fluctuate in value

returns are not guaranteed and you may lose some, or all, ofyour money

depending on your investment profile, and the associatedliquidity risk, part or all of your assets may become illiquid

investment returns can be volatile and future returns may varyfrom past returns. Past performance is not a reliable indicatorof future performance

laws affecting your super may change in the future, and

the amount of your future super savings (including contributionsand returns) may not be enough to provide adequately for yourretirement.

Processing of transactions may be delayed in somecircumstances, for example, when an investment manager delaysissuing unit prices. Managed investments may also be closed,varied or terminated, or investment managers replaced withoutnotice.

There are particular risks associated with each investment option.These could include (among other things) risks specific to acertain security, market risk, currency risk, interest rate risk,derivatives and gearing risk, alternative investments risk, creditrisk, liquidity risk and legal and regulatory risk.

The appropriate level of risk for you will depend on your age,investment timeframe, where other parts of your wealth areinvested, and your risk tolerance.

For more information about the risks involved withinvesting please see '2. Risks of super' in the Additional

Information Booklet Part 2 - Investment.

7. Fees and other costs

DID YOU KNOW?

Small differences in both investment performance and fees and costs can have a substantial impact on your long-termreturns.

For example, total annual fees and costs of 2% of your account balance rather than 1% could reduce your final return byup to 20% over a 30 year period (for example, reduce it from $100,000 to $80,000).

You should consider whether features such as superior investment performance or the provision of better member servicesjustify higher fees and costs.

You or your employer, as applicable, may be able to negotiate to pay lower fees.Ask the fund or your financial adviser.1

TO FIND OUT MORE

If you would like to find out more, or see the impact of the fees based on your own circumstances, the Australian Securitiesand Investments Commission (ASIC) website (www.moneysmart.gov.au) has a superannuation calculator to help you check

out different fee options.

This document shows fees and other costs that you may be charged. These fees and costs may be deducted from your money, fromthe returns on your investment or from the assets of the superannuation entity as a whole.

Other fees, such as activity fees, advice fees for personal advice and insurance fees, may also be charged, but these will depend onthe nature of the activity, advice or insurance chosen by you.

Taxes, insurance fees and other costs relating to insurance are set out in another part of this document and in the Additional InformationBooklet.

You should read all the information about fees and other costs because it’s important to understand their impact on your investment.

The fees and other costs for the MySuper product offered by the superannuation entity, and each option offered by the entity are setout in the table on the following pages.

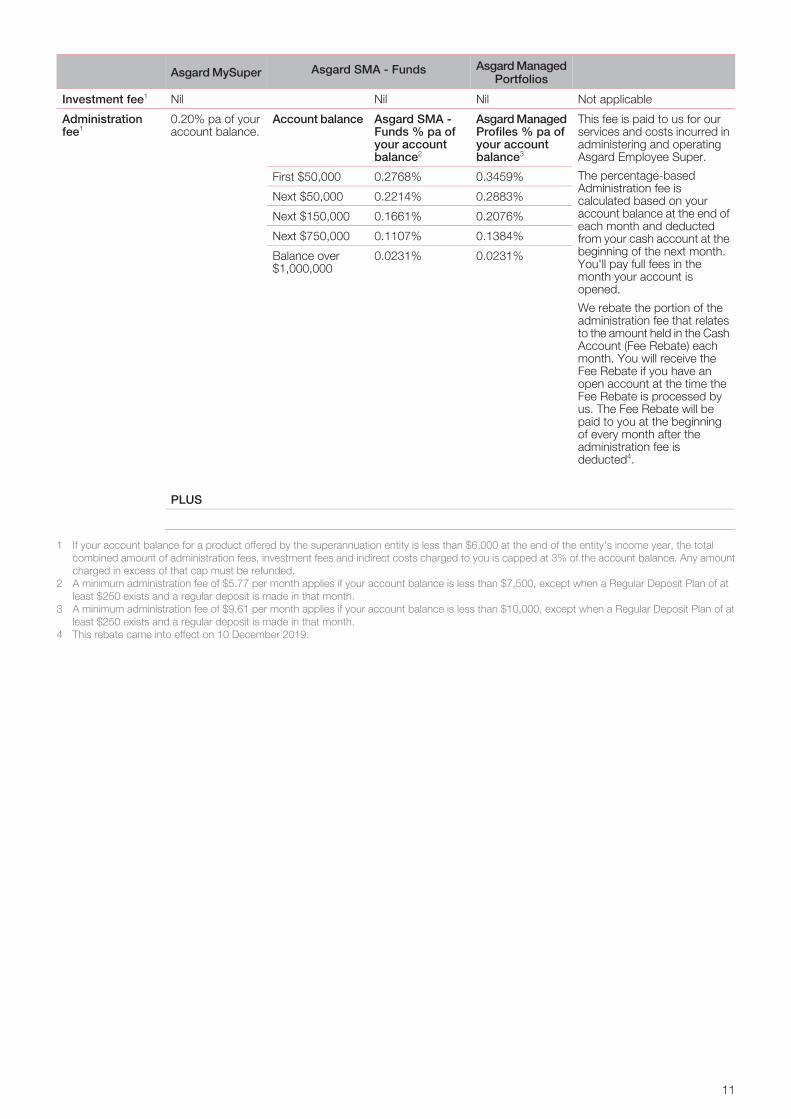

Asgard Employee Super Account - Ernst & Young - For EY employees and their spouse and family

How and when paidAmountType of fee

1 This warning is prescribed by law. Fees in Asgard Employee Super Account are only negotiable with your employer.

10

Asgard ManagedPortfolios

Asgard SMA - FundsAsgard MySuper

Not applicableNilNilNilInvestment fee1

This fee is paid to us for ourservices and costs incurred inadministering and operatingAsgard Employee Super.

Asgard ManagedProfiles % pa ofyour accountbalance3

Asgard SMA -Funds % pa ofyour accountbalance2

Account balance0.20% pa of youraccount balance.

Administrationfee1

0.3459%0.2768%First $50,000 The percentage-basedAdministration fee iscalculated based on your0.2883%0.2214%Next $50,000

0.2076%0.1661%Next $150,000 account balance at the end ofeach month and deducted

0.1384%0.1107%Next $750,000 from your cash account at the0.0231%0.0231%Balance over

$1,000,000beginning of the next month.You'll pay full fees in themonth your account isopened.

We rebate the portion of theadministration fee that relatesto the amount held in the CashAccount (Fee Rebate) eachmonth. You will receive theFee Rebate if you have anopen account at the time theFee Rebate is processed byus. The Fee Rebate will bepaid to you at the beginningof every month after theadministration fee isdeducted4.

PLUS

1 If your account balance for a product offered by the superannuation entity is less than $6,000 at the end of the entity's income year, the totalcombined amount of administration fees, investment fees and indirect costs charged to you is capped at 3% of the account balance. Any amountcharged in excess of that cap must be refunded.

2 A minimum administration fee of $5.77 per month applies if your account balance is less than $7,500, except when a Regular Deposit Plan of atleast $250 exists and a regular deposit is made in that month.

3 A minimum administration fee of $9.61 per month applies if your account balance is less than $10,000, except when a Regular Deposit Plan of atleast $250 exists and a regular deposit is made in that month.

4 This rebate came into effect on 10 December 2019.

11

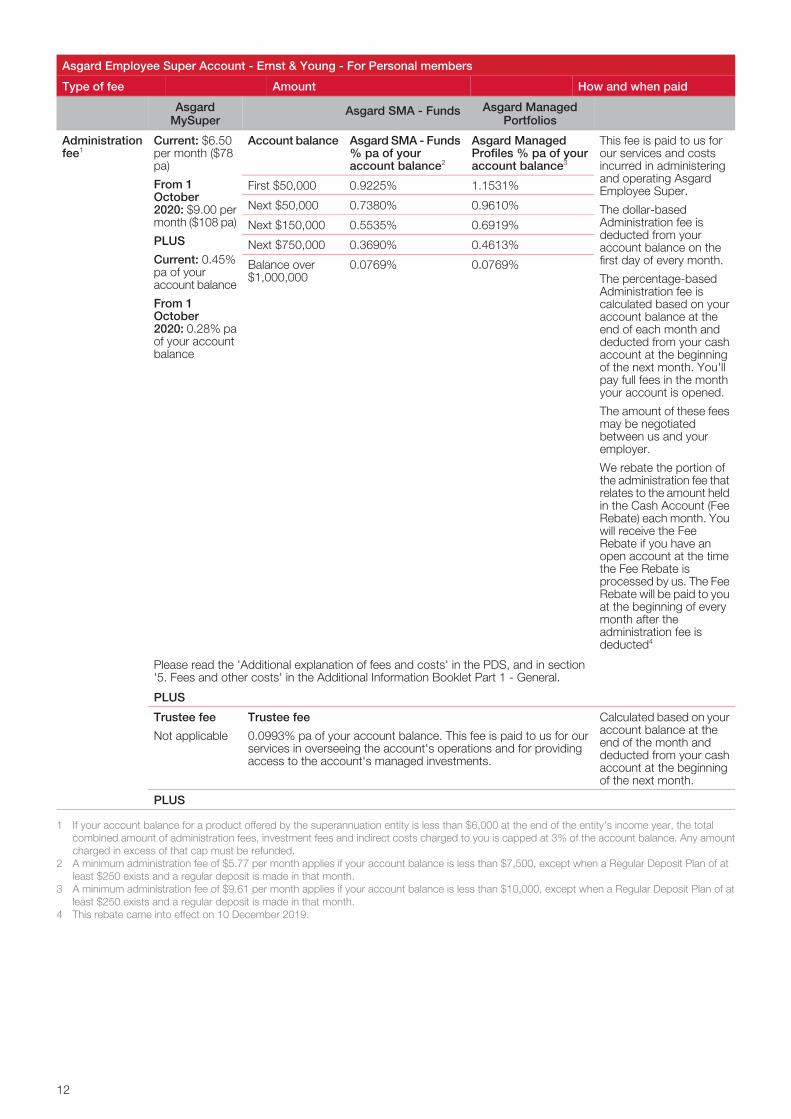

Asgard Employee Super Account - Ernst & Young - For Personal members

How and when paidAmountType of fee

Asgard ManagedPortfolios

Asgard SMA - FundsAsgardMySuper

This fee is paid to us forour services and costsincurred in administeringand operating AsgardEmployee Super.

Asgard ManagedProfiles % pa of youraccount balance3

Asgard SMA - Funds% pa of youraccount balance2

Account balanceCurrent: $6.50per month ($78pa)

From 1October2020: $9.00 permonth ($108 pa)

PLUS

Administrationfee1

1.1531%0.9225%First $50,000

0.9610%0.7380%Next $50,000 The dollar-basedAdministration fee isdeducted from youraccount balance on thefirst day of every month.

0.6919%0.5535%Next $150,000

0.4613%0.3690%Next $750,000Current: 0.45%pa of youraccount balance

0.0769%0.0769%Balance over$1,000,000 The percentage-based

Administration fee iscalculated based on yourFrom 1

October2020: 0.28% paof your accountbalance

account balance at theend of each month anddeducted from your cashaccount at the beginningof the next month. You'llpay full fees in the monthyour account is opened.

The amount of these feesmay be negotiatedbetween us and youremployer.

We rebate the portion ofthe administration fee thatrelates to the amount heldin the Cash Account (FeeRebate) each month. Youwill receive the FeeRebate if you have anopen account at the timethe Fee Rebate isprocessed by us. The FeeRebate will be paid to youat the beginning of everymonth after theadministration fee isdeducted4

Please read the 'Additional explanation of fees and costs' in the PDS, and in section'5. Fees and other costs' in the Additional Information Booklet Part 1 - General.

PLUS

Calculated based on youraccount balance at theend of the month and

Trustee fee

0.0993% pa of your account balance. This fee is paid to us for ourservices in overseeing the account's operations and for providingaccess to the account's managed investments.

Trustee fee

Not applicable

deducted from your cashaccount at the beginningof the next month.

PLUS

1 If your account balance for a product offered by the superannuation entity is less than $6,000 at the end of the entity's income year, the totalcombined amount of administration fees, investment fees and indirect costs charged to you is capped at 3% of the account balance. Any amountcharged in excess of that cap must be refunded.

2 A minimum administration fee of $5.77 per month applies if your account balance is less than $7,500, except when a Regular Deposit Plan of atleast $250 exists and a regular deposit is made in that month.

3 A minimum administration fee of $9.61 per month applies if your account balance is less than $10,000, except when a Regular Deposit Plan of atleast $250 exists and a regular deposit is made in that month.

4 This rebate came into effect on 10 December 2019.

12

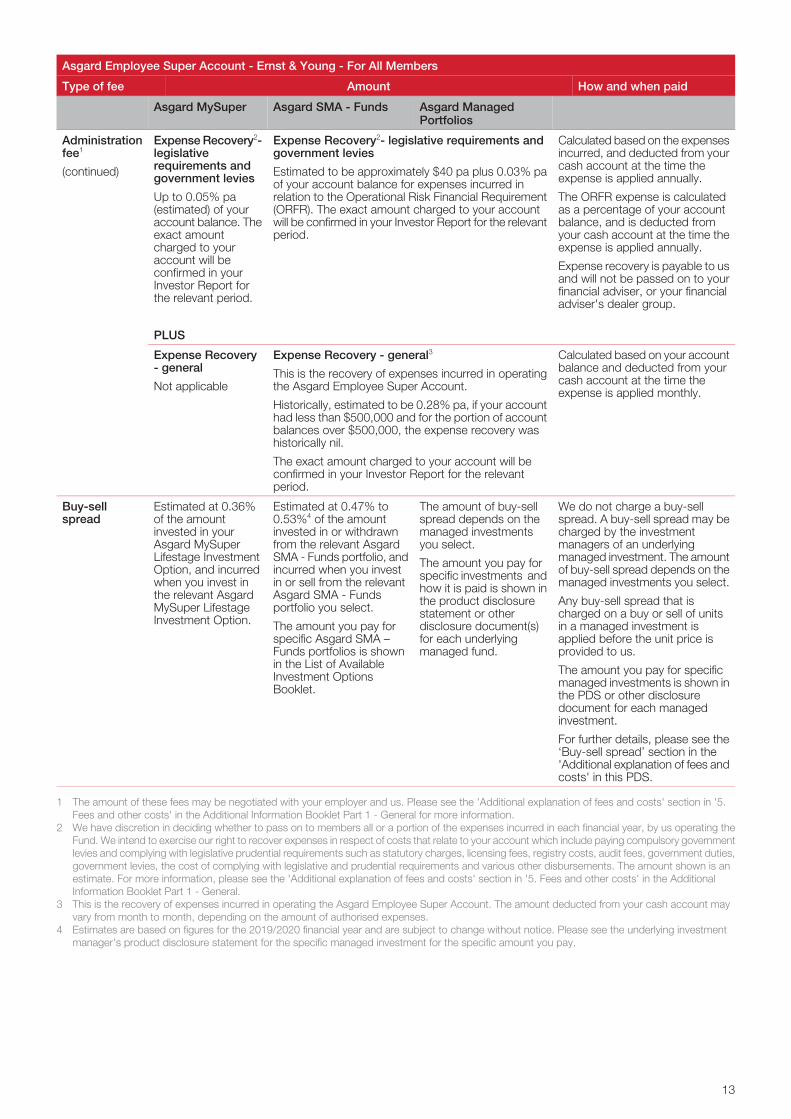

Asgard Employee Super Account - Ernst & Young - For All Members

How and when paidAmountType of fee

Asgard ManagedPortfolios

Asgard SMA - FundsAsgard MySuper

Calculated based on the expensesincurred, and deducted from yourcash account at the time theexpense is applied annually.

Expense Recovery2- legislative requirements andgovernment levies

Estimated to be approximately $40 pa plus 0.03% paof your account balance for expenses incurred inrelation to the Operational Risk Financial Requirement

Expense Recovery2-legislativerequirements andgovernment levies

Up to 0.05% pa(estimated) of youraccount balance. The

Administrationfee1

(continued)

The ORFR expense is calculatedas a percentage of your accountbalance, and is deducted fromyour cash account at the time theexpense is applied annually.

(ORFR). The exact amount charged to your accountwill be confirmed in your Investor Report for the relevantperiod.exact amount

charged to youraccount will be Expense recovery is payable to us

and will not be passed on to yourfinancial adviser, or your financialadviser's dealer group.

confirmed in yourInvestor Report forthe relevant period.

PLUS

Calculated based on your accountbalance and deducted from your

Expense Recovery - general3

This is the recovery of expenses incurred in operatingthe Asgard Employee Super Account.

Expense Recovery- general

Not applicable cash account at the time theexpense is applied monthly.

Historically, estimated to be 0.28% pa, if your accounthad less than $500,000 and for the portion of accountbalances over $500,000, the expense recovery washistorically nil.

The exact amount charged to your account will beconfirmed in your Investor Report for the relevantperiod.

We do not charge a buy-sellspread. A buy-sell spread may becharged by the investment

The amount of buy-sellspread depends on themanaged investmentsyou select.

Estimated at 0.47% to0.53%4 of the amountinvested in or withdrawnfrom the relevant Asgard

Estimated at 0.36%of the amountinvested in yourAsgard MySuper

Buy-sellspread

managers of an underlyingSMA - Funds portfolio, andLifestage Investment managed investment. The amount

of buy-sell spread depends on themanaged investments you select.

The amount you pay forspecific investments andhow it is paid is shown in

incurred when you investin or sell from the relevantAsgard SMA - Fundsportfolio you select.

Option, and incurredwhen you invest inthe relevant AsgardMySuper LifestageInvestment Option.

Any buy-sell spread that ischarged on a buy or sell of unitsin a managed investment isapplied before the unit price isprovided to us.

the product disclosurestatement or otherdisclosure document(s)for each underlyingmanaged fund.

The amount you pay forspecific Asgard SMA –Funds portfolios is shownin the List of AvailableInvestment OptionsBooklet.

The amount you pay for specificmanaged investments is shown inthe PDS or other disclosuredocument for each managedinvestment.

For further details, please see the‘Buy-sell spread’ section in the'Additional explanation of fees andcosts' in this PDS.

1 The amount of these fees may be negotiated with your employer and us. Please see the 'Additional explanation of fees and costs' section in '5.Fees and other costs' in the Additional Information Booklet Part 1 - General for more information.

2 We have discretion in deciding whether to pass on to members all or a portion of the expenses incurred in each financial year, by us operating theFund. We intend to exercise our right to recover expenses in respect of costs that relate to your account which include paying compulsory governmentlevies and complying with legislative prudential requirements such as statutory charges, licensing fees, registry costs, audit fees, government duties,government levies, the cost of complying with legislative and prudential requirements and various other disbursements. The amount shown is anestimate. For more information, please see the 'Additional explanation of fees and costs' section in '5. Fees and other costs' in the AdditionalInformation Booklet Part 1 - General.

3 This is the recovery of expenses incurred in operating the Asgard Employee Super Account. The amount deducted from your cash account mayvary from month to month, depending on the amount of authorised expenses.

4 Estimates are based on figures for the 2019/2020 financial year and are subject to change without notice. Please see the underlying investmentmanager's product disclosure statement for the specific managed investment for the specific amount you pay.

13

Asgard Employee Super Account - Ernst & Young - For all members

How and when paid AmountType of fee

Asgard Managed Portfolios

Asgard SMA - FundsAsgard MySuper

Not applicableNil Nil NilSwitching fee

Not applicableNil Nil Nil Advice feerelating to allmembersinvesting in a

We do not charge Advicefees. However, you mayagree to pay Adviser fees toparticular your financial adviser. PleaseMySuper product

or InvestmentOption

see ‘Personal advice fees’ inthis PDS and in section '5.Fees and other costs' in theAdditional InformationBooklet Part 1 – General.

Personal advice fees paid toyour financial adviser foradvice and related services

Personal advice fees, as negotiated and agreed with your financial adviser.The amount of any Personal advice fee may vary. Please see the 'Additionalexplanation of fees and costs' in this PDS and in the Additional Information BookletPart 1 - General for details of how Personal advice fees are calculated.

Other fees andcosts1

are deducted from your cashaccount monthly in arrears(or at the time your accountis closed, if applicable).

PLUS

This fee is paid to us forinsurance premiums paid tothe Insurer and costs

Insurance fees - if you have insurance in Asgard Employee Super.

The amount of any Insurance fees may vary. Please see the 'Additional explanationof fees and costs' in this PDS and the Additional Information Booklet Part 3 -Insurance for details of how Insurance fees are calculated. incurred in relation to the

provision of insurance. It isdeducted from your cashaccount monthly in advance.See the AdditionalInformation Booklet Part 3 -Insurance for the applicableInsurance fees.

Please see the 'Additional explanation of fees and costs' section in this PDS and the Additional Information Booklet Part 1 - General forfurther information about these fees and costs, such as Activity fees, Personal advice fees, and insurance fees.

1

14

Asgard Employee Super Account

How and when paidAmountType of fee

Asgard ManagedPortfolios

Asgard SMA - FundsAsgard MySuper

Investment managerfees,performance-relatedfees and other indirectcosts

Investment managerfees,performance-relatedfees and other indirectcosts

Investment managerfees,performance-relatedfees and other indirectcosts

Indirect cost ratio

Investment manager feeis deducted from theassets of the Asgard My

Not applicable1Not applicable1Investment manager feesof 0.50% pa of the AsgardMySuper Lifestage

Super LifestageInvestment Option's assetInvestment Option andreflected in the daily unitprice.

value. For a temporaryperiod from 1 April to 30September 2020 theinvestment manager feefor members in the AsgardLifestage investmentoption will be 0.40% pa.

PLUS

Performance-related feesare deducted from theassets of the relevant

Estimatedperformance-related feeof 0.01% to 0.02%2 pa of

Asgard MySuper Lifestagethe Asgard My SuperLifestage InvestmentOption's asset value.

Investment Option andreflected in the daily unitprice when investmentperformance targets aremet.

PLUS

Other indirect costs areincurred in managing theunderlying investment

Estimated other indirectcosts of 0.07% to0.12%3 pa of the Asgard

assets of the AsgardMySuper LifestageInvestment Option's assetvalue.

Estimated total indirectcost ratio of 0.58% to0.64% pa of the Asgard

MySuper LifestageInvestment Option and arereflected in the daily unitprice.

MySuper LifestageInvestment Option'sasset value.

1 Fees and costs are also payable in relation to the underlying investments. For more information on the fees and costs relating to your underlyinginvestments, please see the 'Additional explanation of fees and costs' section in '5. Fees and other costs' in the Additional Information Booklet Part1 - General and the List of Additional Investment Options Booklet.

2 The amount of performance-related fees is an estimate in relation to the 12 months to 30 June 2019. The performance-related fees shown are notrepresentative of likely future performance. Please see the ‘Additional explanation of fees and costs’ section in '5. Fees and other costs' in theAdditional Information Booklet Part 1 – General for more information.

3 The amount of other indirect costs is an estimate of the additional costs incurred in managing the underlying assets of the investment option inrelation to the 12 months to 30 June 2020. Please see the 'Additional explanation of fees and costs' section in '5. Fees and other costs' in theAdditional Information Booklet Part 1 - General for more information.

15

Asgard Employee Super Account

How and when paidAmountType of fee

Asgard Managed Portfolios

Asgard SMA - FundsAsgard MySuper

PLUS

This fee is charged by theCash AccountAdministrator1 for the

Cash account fee (for the cash account only)

This is the amount the Administrator earns for managing theamount held in your cash account.

Cash account fee

Not applicable

Indirect costratio (continued)

administration of yourIt is equal to the amount we earn in relation to the funds heldin your cash account, less the interest amount that we creditto your cash account.

Asgard SMA - Funds andAsgard Managed Profilescash account.

The declared interest rate may change from time to time butwill be greater than 0%. For the current interest rate declaredon your cash account, speak with your financial adviser, go toInvestor Online or call us.

The Cash account feeaccrues daily. It isdeducted on a monthlybasis from the interestearned by the CashWe estimate the Cash account fee to be approximately 1.33%

pa, although the actual fee may vary from time to time. Theestimate is based on the average fee for the financial yearended 30 June 2019. For the latest Cash account fee, pleasecontact our Customer Relations team.

Account Administrator onthe underlying bankaccounts maintained withthe Westpac Group.

For Asgard MySuperLifestage InvestmentOption, the cash accountis cleared at the end ofeach business day. Nointerest is earned and noCash account fee ischarged.

1 The Cash Account Administrator is BT Portfolio Services Limited ABN 73 095 055 208 (BTPS). BTPS is a related body corporate of BTFM.

You can use the information set out in the table on the following page to compare the fees and costs with those for other superproducts. The calculator referred to in the Consumer Advisory Warning in the ‘Fees and other costs’ section of this PDS can be usedto calculate the effect of fees and costs on account balances.

16

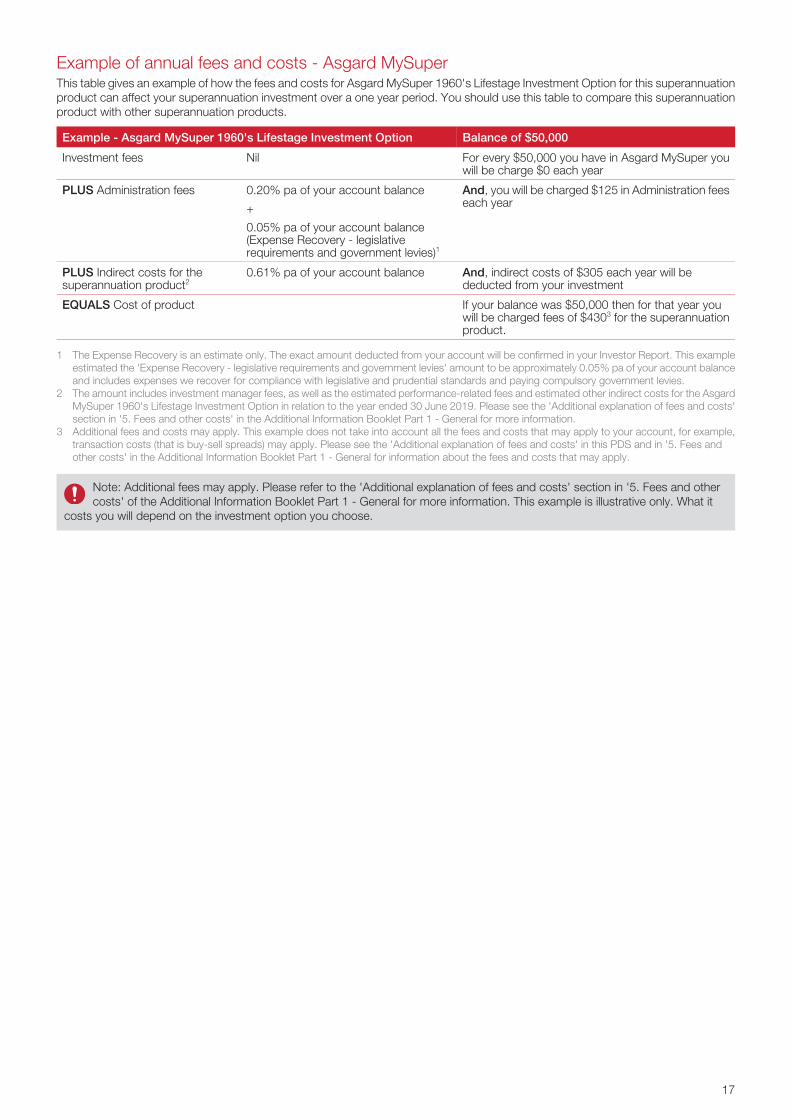

Example of annual fees and costs - Asgard MySuperThis table gives an example of how the fees and costs for Asgard MySuper 1960's Lifestage Investment Option for this superannuationproduct can affect your superannuation investment over a one year period. You should use this table to compare this superannuationproduct with other superannuation products.

Balance of $50,000Example - Asgard MySuper 1960's Lifestage Investment Option

For every $50,000 you have in Asgard MySuper youwill be charge $0 each year

NilInvestment fees

And, you will be charged $125 in Administration feeseach year

0.20% pa of your account balance

+

PLUS Administration fees

0.05% pa of your account balance(Expense Recovery - legislativerequirements and government levies)1

And, indirect costs of $305 each year will bededucted from your investment

0.61% pa of your account balancePLUS Indirect costs for thesuperannuation product2

If your balance was $50,000 then for that year youwill be charged fees of $4303 for the superannuationproduct.

EQUALS Cost of product

1 The Expense Recovery is an estimate only. The exact amount deducted from your account will be confirmed in your Investor Report. This exampleestimated the 'Expense Recovery - legislative requirements and government levies' amount to be approximately 0.05% pa of your account balanceand includes expenses we recover for compliance with legislative and prudential standards and paying compulsory government levies.

2 The amount includes investment manager fees, as well as the estimated performance-related fees and estimated other indirect costs for the AsgardMySuper 1960's Lifestage Investment Option in relation to the year ended 30 June 2019. Please see the 'Additional explanation of fees and costs'section in '5. Fees and other costs' in the Additional Information Booklet Part 1 - General for more information.

3 Additional fees and costs may apply. This example does not take into account all the fees and costs that may apply to your account, for example,transaction costs (that is buy-sell spreads) may apply. Please see the 'Additional explanation of fees and costs' in this PDS and in '5. Fees andother costs' in the Additional Information Booklet Part 1 - General for information about the fees and costs that may apply.

Note: Additional fees may apply. Please refer to the 'Additional explanation of fees and costs' section in '5. Fees and othercosts' of the Additional Information Booklet Part 1 - General for more information. This example is illustrative only. What it

costs you will depend on the investment option you choose.

17

Example of annual fees and costs - Asgard SMA - FundsThis table gives an example of how the fees and costs for accessing the Asgard SMA - Funds Balanced Portfolio through thesuperannuation product can affect your superannuation investment over a one year period. You should use this table to compare thissuperannuation product with other superannuation products.

Balance of $50,0001Example - Asgard SMA - Funds Balanced Portfolio

For every $50,0001 you have in the superannuationproduct you will be charge $0 each year

NilInvestment fees

And, you will be charged $201.07 in administrationfees each year

0.2768% pa of your account balance

+

PLUS Administration fees1

$40 + 0.03% pa of your account balance(Expense Recovery - legislativerequirements and government levies)2

And, indirect costs of $33.25 each year will bededucted from your investment

1.33% of your cash account balance(Cash account fee)3

PLUS Indirect costs for thesuperannuation product

If your balance was $50,0001 then for that year youwill be charged fees of $234.324 for thesuperannuation product.

EQUALS Cost of product

1 In this example it is assumed that $50,000 is invested in the Asgard SMA - Funds Balanced Portfolio (with an additional $2,500 held in the cashaccount).

2 The Expense Recovery is an estimate only. The exact amount deducted from your account will be confirmed in your Investor Report. This exampleestimated the 'Expense Recovery - legislative requirements and government levies' amount to be approximately $40 + 0.03% pa of your accountbalance and includes expenses we recover for compliance with legislative and prudential standards and paying compulsory government levies.

3 The amount of the Cash account fee is based on the assumption that $2,500 is held in the cash account. The amount of the Cash account fee willvary depending on the amount you hold in your cash account.

4 Additional fees and costs may apply. This example does not take into account all the fees and costs that may apply to your account, for example,transaction costs may apply. Please see the 'Additional explanation of fees and costs' in the PDS and in the Additional Information Booklet Part 1- General for information about the fees and other costs that may apply.

This example is illustrative only and fees and costs may vary for your actual investment. The example only shows the fees and coststhat relate to accessing investments through the superannuation product and not the fees and costs of the underlying managedinvestments. Additional costs will be charged by the issuers of those underlying managed investments that you decide to invest in.Please refer to the following example that illustrates the combined effect of the fees and costs.

18

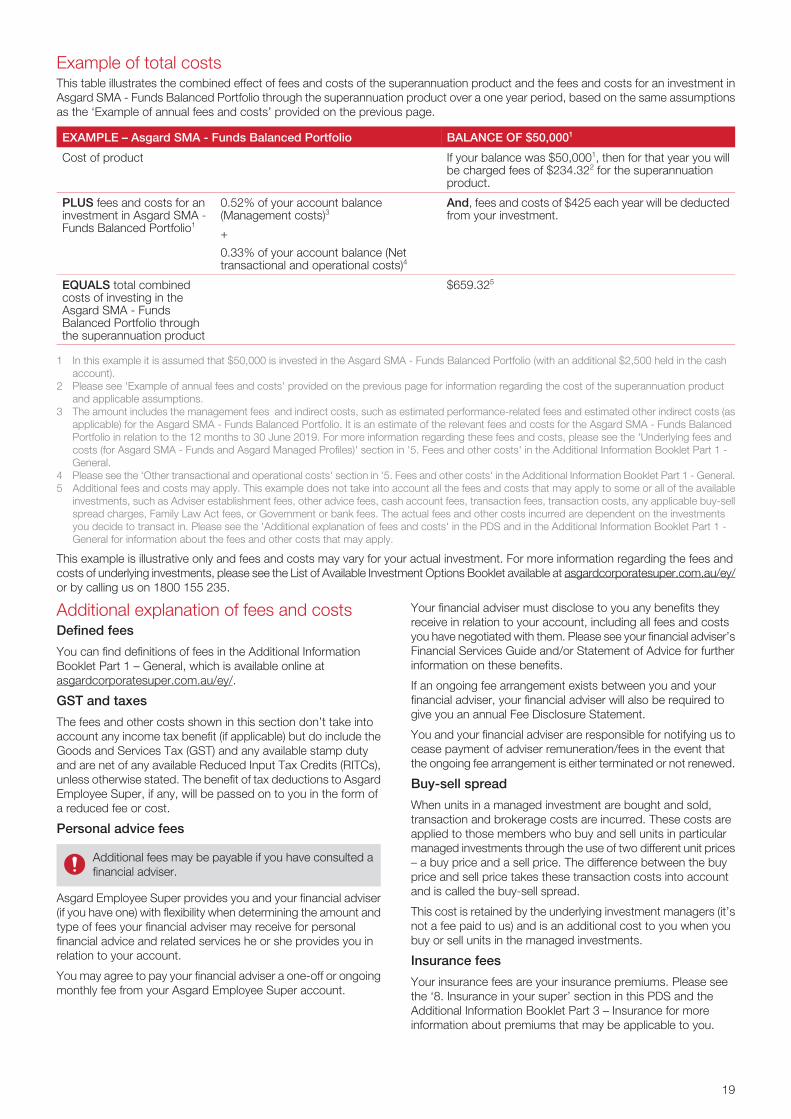

Example of total costsThis table illustrates the combined effect of fees and costs of the superannuation product and the fees and costs for an investment inAsgard SMA - Funds Balanced Portfolio through the superannuation product over a one year period, based on the same assumptionsas the ‘Example of annual fees and costs’ provided on the previous page.

BALANCE OF $50,0001EXAMPLE – Asgard SMA - Funds Balanced Portfolio

If your balance was $50,0001, then for that year you willbe charged fees of $234.322 for the superannuationproduct.

Cost of product

And, fees and costs of $425 each year will be deductedfrom your investment.

0.52% of your account balance(Management costs)3

PLUS fees and costs for aninvestment in Asgard SMA -Funds Balanced Portfolio1

+

0.33% of your account balance (Nettransactional and operational costs)4

$659.325EQUALS total combinedcosts of investing in theAsgard SMA - FundsBalanced Portfolio throughthe superannuation product

1 In this example it is assumed that $50,000 is invested in the Asgard SMA - Funds Balanced Portfolio (with an additional $2,500 held in the cashaccount).

2 Please see 'Example of annual fees and costs' provided on the previous page for information regarding the cost of the superannuation productand applicable assumptions.

3 The amount includes the management fees and indirect costs, such as estimated performance-related fees and estimated other indirect costs (asapplicable) for the Asgard SMA - Funds Balanced Portfolio. It is an estimate of the relevant fees and costs for the Asgard SMA - Funds BalancedPortfolio in relation to the 12 months to 30 June 2019. For more information regarding these fees and costs, please see the 'Underlying fees andcosts (for Asgard SMA - Funds and Asgard Managed Profiles)' section in '5. Fees and other costs' in the Additional Information Booklet Part 1 -General.

4 Please see the 'Other transactional and operational costs' section in '5. Fees and other costs' in the Additional Information Booklet Part 1 - General.5 Additional fees and costs may apply. This example does not take into account all the fees and costs that may apply to some or all of the available

investments, such as Adviser establishment fees, other advice fees, cash account fees, transaction fees, transaction costs, any applicable buy-sellspread charges, Family Law Act fees, or Government or bank fees. The actual fees and other costs incurred are dependent on the investmentsyou decide to transact in. Please see the 'Additional explanation of fees and costs' in the PDS and in the Additional Information Booklet Part 1 -General for information about the fees and other costs that may apply.

This example is illustrative only and fees and costs may vary for your actual investment. For more information regarding the fees andcosts of underlying investments, please see the List of Available Investment Options Booklet available at asgardcorporatesuper.com.au/ey/or by calling us on 1800 155 235.

Additional explanation of fees and costsDefined fees

You can find definitions of fees in the Additional InformationBooklet Part 1 – General, which is available online atasgardcorporatesuper.com.au/ey/.

GST and taxes

The fees and other costs shown in this section don’t take intoaccount any income tax benefit (if applicable) but do include theGoods and Services Tax (GST) and any available stamp dutyand are net of any available Reduced Input Tax Credits (RITCs),unless otherwise stated. The benefit of tax deductions to AsgardEmployee Super, if any, will be passed on to you in the form ofa reduced fee or cost.

Personal advice fees

Additional fees may be payable if you have consulted afinancial adviser.

Asgard Employee Super provides you and your financial adviser(if you have one) with flexibility when determining the amount andtype of fees your financial adviser may receive for personalfinancial advice and related services he or she provides you inrelation to your account.

You may agree to pay your financial adviser a one-off or ongoingmonthly fee from your Asgard Employee Super account.

Your financial adviser must disclose to you any benefits theyreceive in relation to your account, including all fees and costsyou have negotiated with them. Please see your financial adviser’sFinancial Services Guide and/or Statement of Advice for furtherinformation on these benefits.

If an ongoing fee arrangement exists between you and yourfinancial adviser, your financial adviser will also be required togive you an annual Fee Disclosure Statement.

You and your financial adviser are responsible for notifying us tocease payment of adviser remuneration/fees in the event thatthe ongoing fee arrangement is either terminated or not renewed.

Buy-sell spread

When units in a managed investment are bought and sold,transaction and brokerage costs are incurred. These costs areapplied to those members who buy and sell units in particularmanaged investments through the use of two different unit prices– a buy price and a sell price. The difference between the buyprice and sell price takes these transaction costs into accountand is called the buy-sell spread.

This cost is retained by the underlying investment managers (it’snot a fee paid to us) and is an additional cost to you when youbuy or sell units in the managed investments.

Insurance fees

Your insurance fees are your insurance premiums. Please seethe ‘8. Insurance in your super’ section in this PDS and theAdditional Information Booklet Part 3 – Insurance for moreinformation about premiums that may be applicable to you.

19

Changes in fees and costs

We may alter any of the fees and other costs, or introduce newfees and other costs without your consent. You’ll receive at least30 days written notice of any proposal to introduce new fees andother costs, or to increase current fees and costs (other thanincreases as a result of indexation). If you nominate an ongoingflat dollar amount Personal advice fee, this fee may be increasedannually in line with the Consumer Price Index.

When we’re told that you have left EY, you and your spouse andfamily member(s) (if applicable) will automatically become‘Personal members’ within Asgard Employee Super Account.Any EY-related discounts on fees and insurance fees will ordinarilycease, unless your former employer has negotiated otherwise.Any employer-tiering discount on the Administration fee willgenerally cease and your insurance fees may change when youbecome a ‘Personal member’.

For more detailed information about fees and other costsplease see '5. Fees and other costs' in the Additional

Information Booklet Part 1 - General.

20

8. Insurance in your super

What insurance is included in Asgard Employee Super?Asgard Employee Super offers Life Protection, or Life and Total and Permanent Disablement (TPD) Protection subject to eligibilityconditions such as age, occupation and employment status (please see the ‘Terms and Conditions’ section of the Additional InformationBooklet Part 3 – Insurance for further details of the eligibility criteria).

The types of insurance cover available include:

Life Protection – pays a lump sum if you die or are diagnosed with a terminal illness,

TPD Protection – pays a lump sum if you become totally and permanently disabled. TPD Protection can only be taken out with LifeProtection.

Please note: there’s no Salary Continuance Insurance within your Asgard Employee Super Account. EY holds a separate Group SalaryContinuance Insurance policy outside of superannuation.

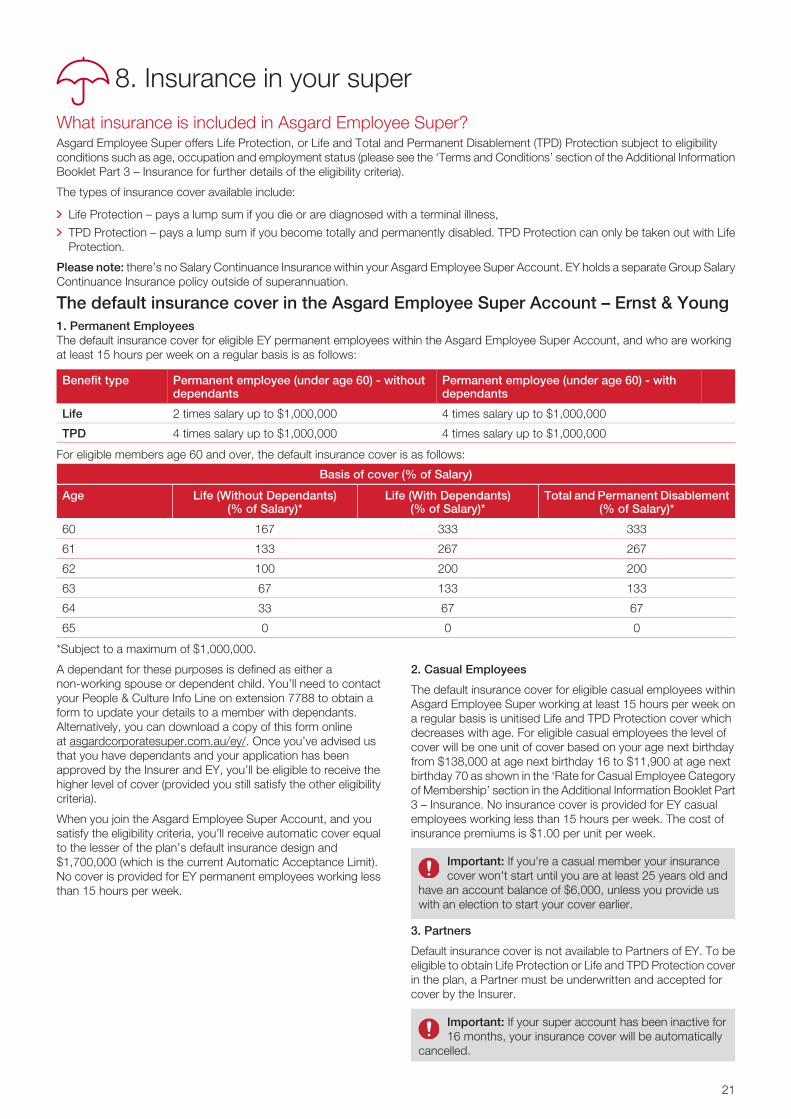

The default insurance cover in the Asgard Employee Super Account – Ernst & Young1. Permanent EmployeesThe default insurance cover for eligible EY permanent employees within the Asgard Employee Super Account, and who are workingat least 15 hours per week on a regular basis is as follows:

Permanent employee (under age 60) - withdependants

Permanent employee (under age 60) - withoutdependants

Benefit type

4 times salary up to $1,000,0002 times salary up to $1,000,000Life

4 times salary up to $1,000,0004 times salary up to $1,000,000TPD

For eligible members age 60 and over, the default insurance cover is as follows:

Basis of cover (% of Salary)

Total and Permanent Disablement(% of Salary)*

Life (With Dependants)(% of Salary)*

Life (Without Dependants)(% of Salary)*

Age

33333316760

26726713361

20020010062

1331336763

67673364

00065

*Subject to a maximum of $1,000,000.

A dependant for these purposes is defined as either anon-working spouse or dependent child. You’ll need to contactyour People & Culture Info Line on extension 7788 to obtain aform to update your details to a member with dependants.Alternatively, you can download a copy of this form onlineat asgardcorporatesuper.com.au/ey/. Once you’ve advised usthat you have dependants and your application has beenapproved by the Insurer and EY, you’ll be eligible to receive thehigher level of cover (provided you still satisfy the other eligibilitycriteria).

When you join the Asgard Employee Super Account, and yousatisfy the eligibility criteria, you’ll receive automatic cover equalto the lesser of the plan’s default insurance design and$1,700,000 (which is the current Automatic Acceptance Limit).No cover is provided for EY permanent employees working lessthan 15 hours per week.

2. Casual Employees

The default insurance cover for eligible casual employees withinAsgard Employee Super working at least 15 hours per week ona regular basis is unitised Life and TPD Protection cover whichdecreases with age. For eligible casual employees the level ofcover will be one unit of cover based on your age next birthdayfrom $138,000 at age next birthday 16 to $11,900 at age nextbirthday 70 as shown in the ‘Rate for Casual Employee Categoryof Membership’ section in the Additional Information Booklet Part3 – Insurance. No insurance cover is provided for EY casualemployees working less than 15 hours per week. The cost ofinsurance premiums is $1.00 per unit per week.

Important: If you're a casual member your insurancecover won't start until you are at least 25 years old and

have an account balance of $6,000, unless you provide uswith an election to start your cover earlier.

3. Partners

Default insurance cover is not available to Partners of EY. To beeligible to obtain Life Protection or Life and TPD Protection coverin the plan, a Partner must be underwritten and accepted forcover by the Insurer.

Important: If your super account has been inactive for16 months, your insurance cover will be automatically

cancelled.

21

What happens to my insurance when I leaveErnst & Young?Permanent employees:

If you are eligible for Automatic Acceptance Cover and youare over the age of 25 and reached an account balance of$6,000 when you leave your employer, your cover willautomatically transfer to the personal division when we arenotified you have ceased employment.

If you are eligible for Automatic Acceptance Cover but you areunder age 25 or have not reached an account balance of$6,000 when you leave your employer, you will be providedthe option to continue cover within 60 days from the date theemployer notifies us you have ceased employment.

Casual employees

If you are eligible for Automatic Acceptance Cover but you areunder the age 25 or have not reached an account balance of$6,000 when you leave your employer, your insurance cover willstart.

You will be provided with Standard Insurance when you turn 25and you have an account balance of $6,000. Any restrictions (forexample, New Events Cover) or exclusions will continue to apply.The occupation class recorded in your former Employer's planwill continue to apply, but you can ask us to change it.

Costs of coverThe amount you pay for insurance is called an ‘insurance fee’ or‘insurance premium’. Insurance fees are based on the type andamount of cover you or your employer has chosen along withvarious factors such as your age, gender and occupation.

Your insurance fee and amount of cover, if applicable, arecalculated when your insurance commences, when we’re notifiedof certain changes to your membership details (eg occupation),when your cover changes, or when your insurance is recalculatedannually on the date nominated by your employer based uponyour age.

For permanent employees only, EY pays for your default coverinsurance fees by making additional contributions into your superaccount to cover the cost of the insurance fees of your defaultlevel of insurance cover under the default insurance cover. Theseadditional contributions can be identified as ‘Employer preservedcontributions’ in your half-yearly Investor Reports.

If you choose to increase your level of insurance cover abovethe level prescribed by the default insurance cover, the additionalInsurance fee will be at your own cost. Please see the 'VoluntaryCover' in the Additional Information Booklet Part 3 - Insurance.

Please note: If you're a casual employee, you're required to payfor your insurance cover and the insurance fee for this will bededucted by us monthly from your cash account.

Changing coverEY provides a benefit to its permanent employees, however, itcannot take the circumstances of each individual employee intoaccount to determine whether the default insurance cover is theright cover for you. We suggest you speak to a financial adviserwho can advise you if you have adequate insurance cover.

If you would like to change your level of cover, please go toasgardcorporatesuper.com.au/ey/, or call us to speak to arepresentative who will guide you through the process.

Cover for spouse and family membersSpouse and family members of an EY member of AsgardEmployee Super can apply for insurance cover. Spouse andfamily members can apply for insurance cover through BTProtection Plans (BTPP), which is issued by us. You should

consider the BTPP Product Disclosure Statement before makinga decision about BTPP. To obtain a copy of the BTPP ProductDisclosure Statement, please speak to your financial adviser (ifyou have one), or call us on 1800 155 235. All cover is subjectto the assessment of medical evidence and acceptance of thecover by Westpac Life Insurance Services LimitedABN 31 003 149 157, the insurer of BTPP. Default insurancecover and automatic acceptance of cover are not available forspouse or family members.

For more information about eligibility for, and cancellationof insurance, conditions and exclusions applicable to