b oeing c apital c orporation international conference on air transport, law and regulation abu...

Post on 20-Dec-2015

217 views

TRANSCRIPT

BOEING CAPITAL CORPORATIONBOEING CAPITAL CORPORATION

International Conference on Air Transport, Law and Regulation

Abu Dhabi, UAE

April 16, 2009

International Conference on Air Transport, Law and Regulation

Abu Dhabi, UAE

April 16, 2009

John Matthews

Managing DirectorMiddle East & Africa

John Matthews

Managing DirectorMiddle East & Africa

2

Aircraft Financing Environment

Capital ProvidersCapital Providers 20032003 20042004 20052005 20062006 20072007 20082008 TodayToday 20102010 20112011

Lessors R/Y Y G G G Y/R R/Y Y Y/G

Commercial Banks R/Y G G G G Y/R R/Y Y Y/G

Public Debt / Capital Markets

R R R/Y Y G/Y/G R R R/Y Y/G

Export CreditAgencies

G G G G G G/Y G/Y Y Y

Private Equity Hedge Funds

G G G G G R R R/Y Y

Tax Equity R R Y Y G G/Y G/Y Y/G G

Airframe and Engine Manufacturers

R R/Y G G G Y Y/R R/Y Y/G

New Sources of Funding

G G/Y G/Y Y G

Satisfactory Cautionary Major ConcernG Y R ChangeY/G

Difficult, volatile, fragileDifficult, volatile, fragileDifficult, volatile, fragileDifficult, volatile, fragile

3

Sources of Financing

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2002 2003 2004 2005 2006 2007 2008 2009

Export credit Export credit

Bank debt Bank debt

Manufacturer

Cash / otherCash / other

Leasing companiesLeasing companies

Public debt/capital markets

376 281 285 290 394 441 375 481

$26B $20B $19B $19B $25B $29B $23B $29B

17%

28%

28%

3.5%

3.5%

20%

4

U.S. Capital Markets Activity (2007 – 2008)

EETCsEETCs

1Q 2008 2Q 2008

DAL ($550M) Calyon /PK, New and refi

Portfolio ActivityPortfolio Activity

2Q 2007 3Q 2007 4Q 2007

ILFCCIT

AWASGECAS

CAL• $1.1B• New

(18) 737-900ER,(12) 737-800

• ‘A’ Pricing T+138 bps

UAL• $0.7B• Refinancing

(2) 767-300ER,(4) 777-200,(4) 777-200ER,(3) 747-400

• ‘A’ Pricing T+155 bps

SWA• $0.5B• New

(16) 737-700 with winglets

• ‘A’ Pricing T+160 bps

NWA• $0.5B• New

(27) EMB-175LR• ‘A’ Pricing T+250 bps

DAL• $1.4B• Refinancing

(11) 737-800, (4) 767-300ER,(14) 767-400ER, (7) 777-200ER

• ‘A’ Pricing T+230 bps

Genesis(Equity)

• $108M

HSH Nordbank

• Fund• $1.3B

AerCap (Equity)• $1.7B

AerCap (Equity)• $518M

RBS• Securitization• $1.09B

Babcock & Brown (IPO)

• $495M (equity) / $853M (scrtzn)

ACG • Bond• $250M

UAL• $0.35B• ‘A’ Tranche only• Anticipated pricing

12-13%• (5) A319s, (6) A320s,

(2) 767-300ERs,(2) 777-200A, and (2) 777-200ERs

3Q 2008

AerCap ($750M) Calyon/ refiMoved to the Banks

EETC market pricing makes it not viable today… portfolio activity shutdownEETC market pricing makes it not viable today… portfolio activity shutdownEETC market pricing makes it not viable today… portfolio activity shutdownEETC market pricing makes it not viable today… portfolio activity shutdown

5

Lessor Landscape

Traditional Capital New Money

Lessor funding under pressureLessor funding under pressureLessor funding under pressureLessor funding under pressure

6

Global Bank Debt

European aircraft banks− Majority of global aircraft debt financing− Major financiers of second tier lessors− 80 - 220 bps more expensive since August 2007− Now competitive with EETC market− Some signs of pull back to preserve capital

US banks− Primarily investment banking (use someone else’s balance sheet)− Crucial structuring expertise and syndication capability

Regional banks− Formerly a niche market that is achieving critical mass− China regional banks repositioning

Softening, on close watch due to sector challengesSoftening, on close watch due to sector challengesSoftening, on close watch due to sector challengesSoftening, on close watch due to sector challenges

7

Evolution of Aircraft Banking

The Next GenerationThe Next Generation

The 80sThe 80s

NISSHO IWAI

The 60s – 70sThe 60s – 70s

The 90s – TodayThe 90s – Today

PK AIR FINANCE

Aircraft finance continues to attract new debt providersAircraft finance continues to attract new debt providersAircraft finance continues to attract new debt providersAircraft finance continues to attract new debt providers

8

Ex-Im Bank is a Significant Financier ofBoeing Aircraft

0%

10%

20%

30%

40%

50%

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Ex-Im % of Boeing Exports Ex-Im % of Boeing Deliveries

Ex-Im SupportedDeliveries

54 52 18 22 34 62 72 56 49 72 68 53 52 88 91 63 105

AircraftExported

205 160 100 76 205 311 264 198 158 168 154 143 160 314 367 228 394

Total Aircraft Deliveries

330 270 206 218 375 563 620 489 527 381 281 285 290 395 440 375 482

9

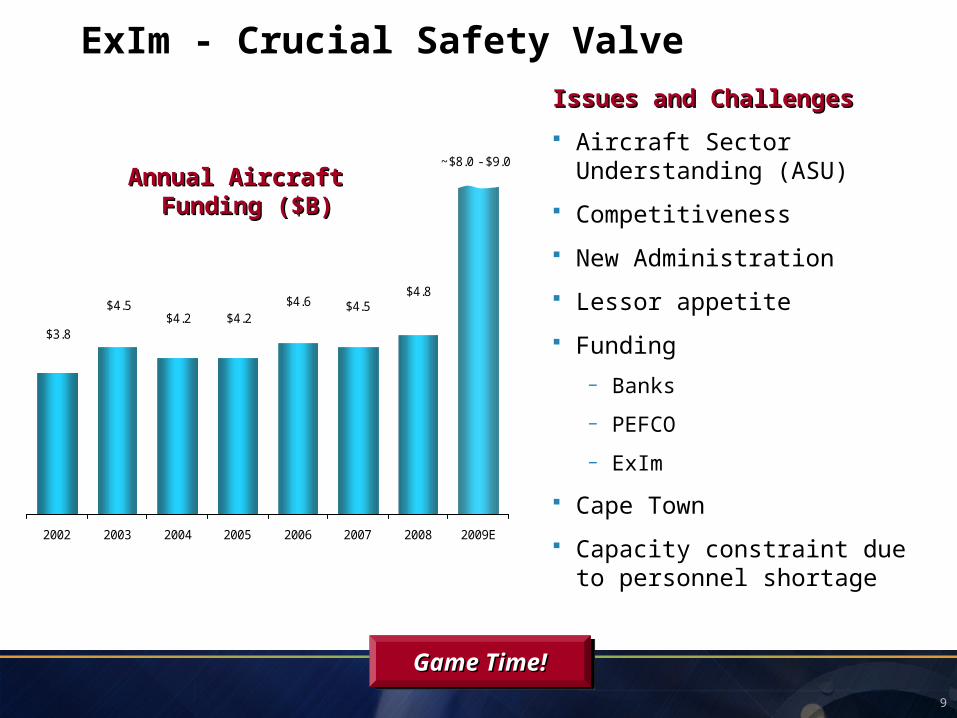

ExIm - Crucial Safety Valve

Issues and ChallengesIssues and Challenges

Aircraft Sector Understanding (ASU)

Competitiveness

New Administration

Lessor appetite

Funding

− Banks

− PEFCO

− ExIm

Cape Town

Capacity constraint due to personnel shortage

~$8.0 - $9.0

$4.8$4.5$4.6

$4.2$4.2$4.5

$3.8

2002 2003 2004 2005 2006 2007 2008 2009E

Annual Aircraft Funding Annual Aircraft Funding ($B)($B)

Game Time!Game Time!Game Time!Game Time!

10

Hedge Funds / Private Equity

Source of lessor equity and secondary liquidity (EETCs, mezzanine debt)

Severely impacted by sub-prime mortgage crisis

terra firmaterra firma

Post sub-prime access to capital significantly curtailedPost sub-prime access to capital significantly curtailedPost sub-prime access to capital significantly curtailedPost sub-prime access to capital significantly curtailed

11

Developing Sources of Capital

ChinaChina Middle EastMiddle East

Developing Regional BankingDeveloping Regional Banking Sovereign Wealth FundsSovereign Wealth Funds

• Qatar

• Kuwait

• Saudi Arabia

• UAE

• Bahrain

• Oman

12

Global syndication infrastructureGlobal syndication infrastructureGlobal syndication infrastructureGlobal syndication infrastructure

Panama Oman

Afghanistan

Indonesia

Ethiopia

Ireland Mongolia

Cape Verde

Nigeria

Malaysia

Kenya Mexico

Pakistan

Senegal

South Africa

Albania

USA

Angola

Colombia

India BangladeshUAE Luxembourg Saudi Arabia

TanzaniaCuba Singapore China

Cape Town Treaty Gaining MomentumJanuary 20, 2009

2009 Focus2009 Focus

European Union

Russia

Canada

Brazil

Japan

13

Cape Town Opportunities

Global EETCGlobal EETC SyndicationSyndication

US EETC SyndicationUS EETC Syndicationof Global Airlinesof Global Airlines

MinimumCapital

Requirements

SupervisoryReviewProcess

MarketDiscipline

Pillar 1Pillar 1 Pillar 2Pillar 2 Pillar 3Pillar 3

BASEL IIBASEL II

BASEL 2BASEL 2

The next generation of structured aircraft financeThe next generation of structured aircraft financeThe next generation of structured aircraft financeThe next generation of structured aircraft finance

14

AirlineCustomers

AirlineCustomers

OpinionMakersOpinionMakers

CapitalProviders

CapitalProviders

BoeingBoeing