billboard valuation: an overview - transportation.org · billboard valuation: an overview •...

TRANSCRIPT

Billboard Valuation: An Overview

• De-mystify the billboard

• Discuss applicability of three approaches to value

• Discuss sources/methods of multipliers and cap rates

• Discuss site value attributes/features

• Discuss the perspective of the Billboard Company

• Case Study in Billboards

Today’s Objectives

Welcome to Indiana…

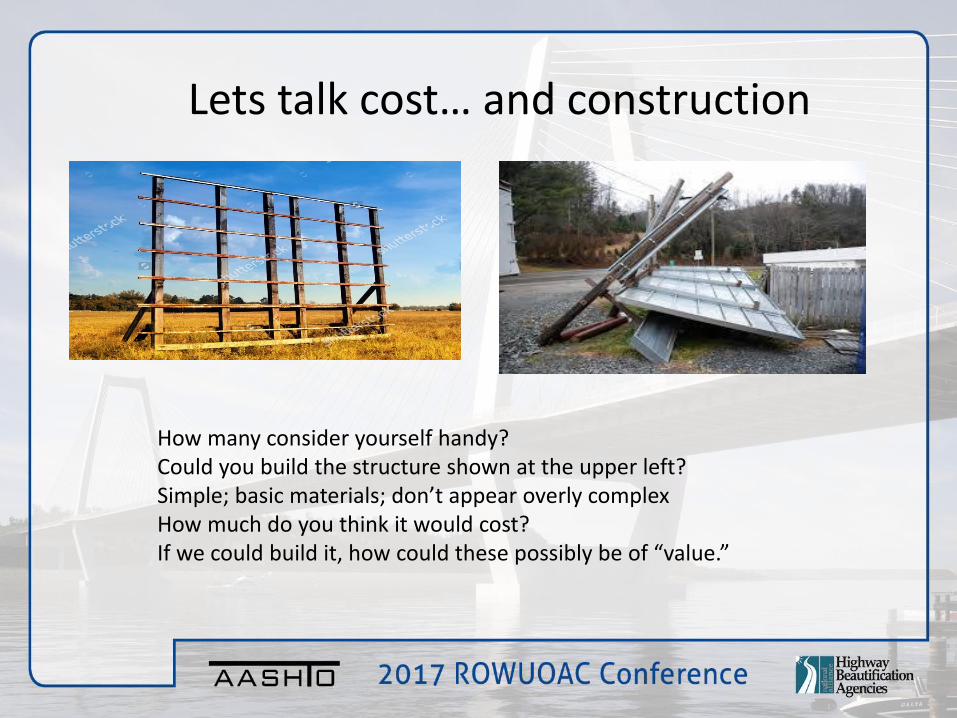

Lets talk cost… and construction

How many consider yourself handy? Could you build the structure shown at the upper left? Simple; basic materials; don’t appear overly complex How much do you think it would cost?If we could build it, how could these possibly be of “value.”

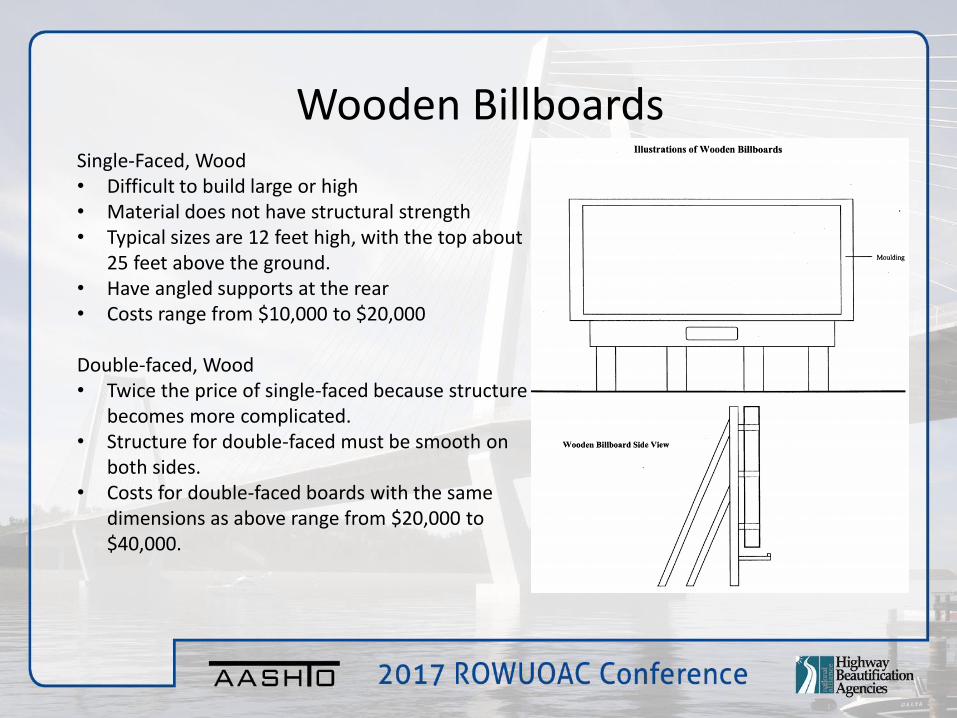

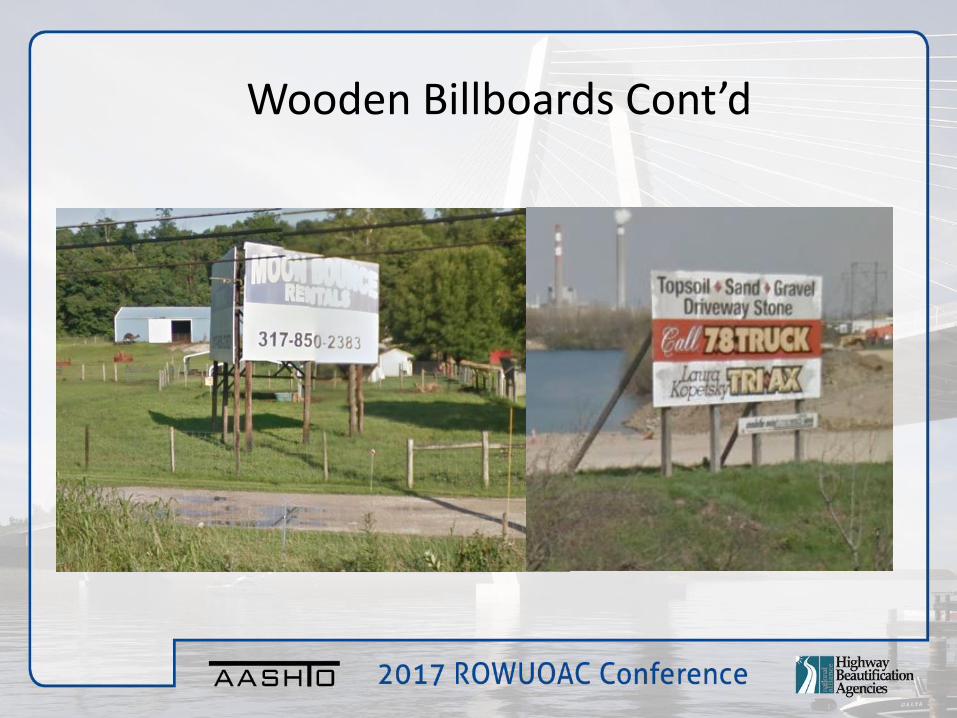

Wooden BillboardsSingle-Faced, Wood• Difficult to build large or high • Material does not have structural strength• Typical sizes are 12 feet high, with the top about

25 feet above the ground. • Have angled supports at the rear• Costs range from $10,000 to $20,000

Double-faced, Wood• Twice the price of single-faced because structure

becomes more complicated. • Structure for double-faced must be smooth on

both sides. • Costs for double-faced boards with the same

dimensions as above range from $20,000 to $40,000.

Wooden Billboards Cont’d

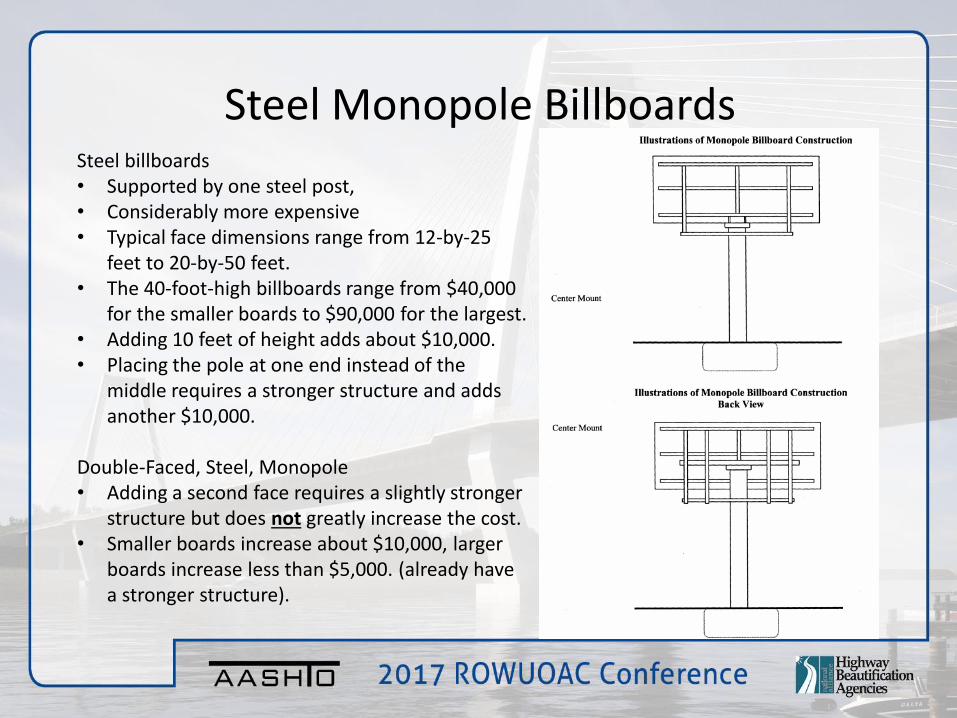

Steel Monopole BillboardsSteel billboards • Supported by one steel post, • Considerably more expensive • Typical face dimensions range from 12-by-25

feet to 20-by-50 feet. • The 40-foot-high billboards range from $40,000

for the smaller boards to $90,000 for the largest.• Adding 10 feet of height adds about $10,000.• Placing the pole at one end instead of the

middle requires a stronger structure and adds another $10,000.

Double-Faced, Steel, Monopole• Adding a second face requires a slightly stronger

structure but does not greatly increase the cost.• Smaller boards increase about $10,000, larger

boards increase less than $5,000. (already have a stronger structure).

Steel Monopole Billboards Cont’d

Steel Multi-post Billboards• Supporting with several steel posts increases the

cost, but decreases the cost of the board structure• Overall slightly less expensive than monopole • Boards range in cost from $30,00 to $70,000,

(slightly less than the corresponding monopole boards.)

• Double-faced boards also less expensive than monopole

• Can be arranged in a V-shaped format for better visibility from both directions and for more stability.

• Costs range from $60,000 to $90,000.

Steel Multi-post Billboards Cont’d

So the Cost is the Value, right?Wrong.

3 Broad Steps in the cost approach are:

• Estimate the replacement cost new of the improvements • Estimate the loss in value from all forms of depreciation, deduct

the total amount of depreciation from the replacement cost new (MISSING)

• Estimate the value of the land as if vacant and add the land value estimate to the depreciated cost value to arrive at the total property value (MISSING)

Depreciation estimates are difficult and often applied incorrectly. Most important aspect missing is LOCATION, LOCATION, LOCATION.

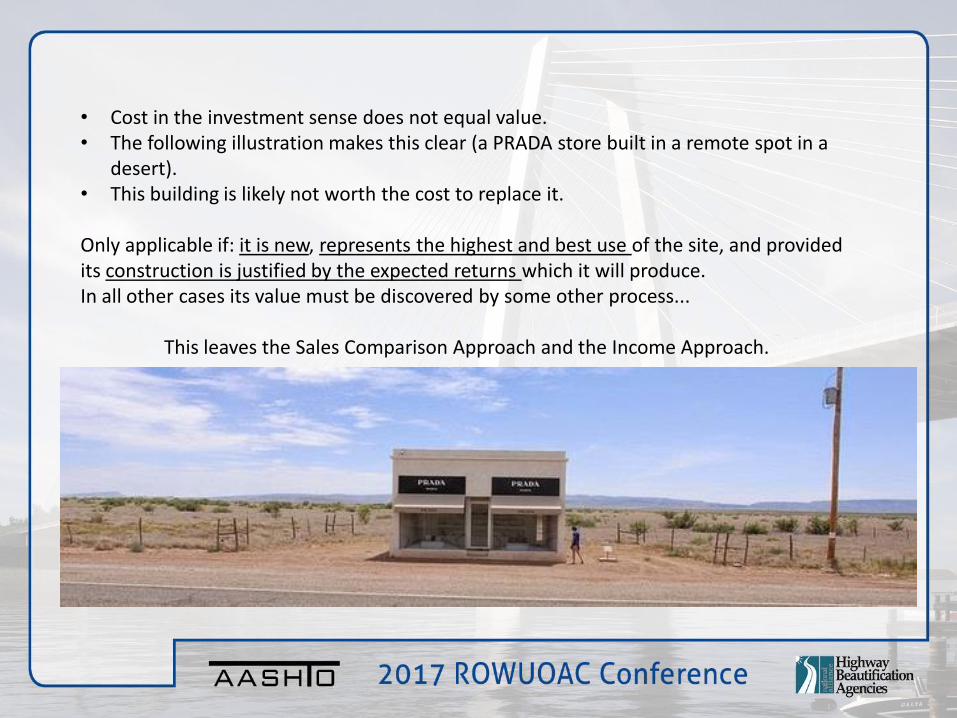

• Cost in the investment sense does not equal value. • The following illustration makes this clear (a PRADA store built in a remote spot in a

desert). • This building is likely not worth the cost to replace it.

Only applicable if: it is new, represents the highest and best use of the site, and provided its construction is justified by the expected returns which it will produce.In all other cases its value must be discovered by some other process...

This leaves the Sales Comparison Approach and the Income Approach.

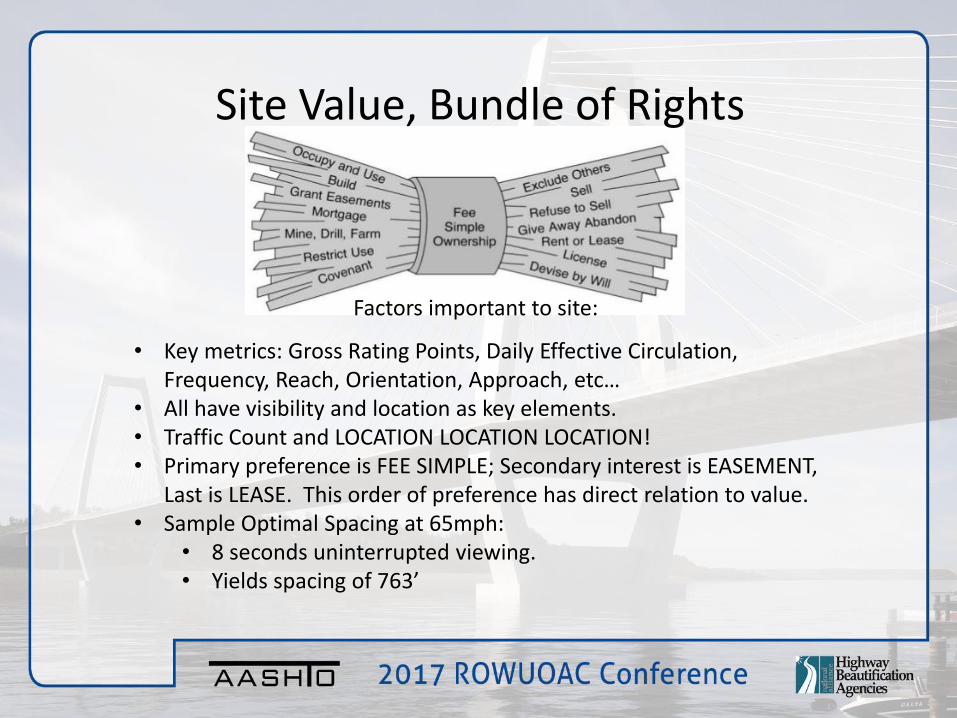

Site Value, Bundle of Rights

Factors important to site:

• Key metrics: Gross Rating Points, Daily Effective Circulation, Frequency, Reach, Orientation, Approach, etc…

• All have visibility and location as key elements.• Traffic Count and LOCATION LOCATION LOCATION!• Primary preference is FEE SIMPLE; Secondary interest is EASEMENT,

Last is LEASE. This order of preference has direct relation to value.• Sample Optimal Spacing at 65mph:

• 8 seconds uninterrupted viewing.• Yields spacing of 763’

More on INDY…

Sales Comparison Approach

• Reliability of the Sales Comparison Approach is greatly diminished if substitute properties are NOT available – Scarcity of Asset.

• Motivations of transactions• Geographic Diversification• Spatial Monopoly• Operating Efficiencies

• Many appraisers use a GRM in a Sales Comparison Approach, this should be cautioned as this is an Income based comparison and if not properly adjusted quantitatively, should be left to the Income Approach.

• Quantitative vs. Qualitative Analysis.

• Application of approach should ALWAYS mirror that of the market participant. Where does that leave us?

The INCOME APPROACH

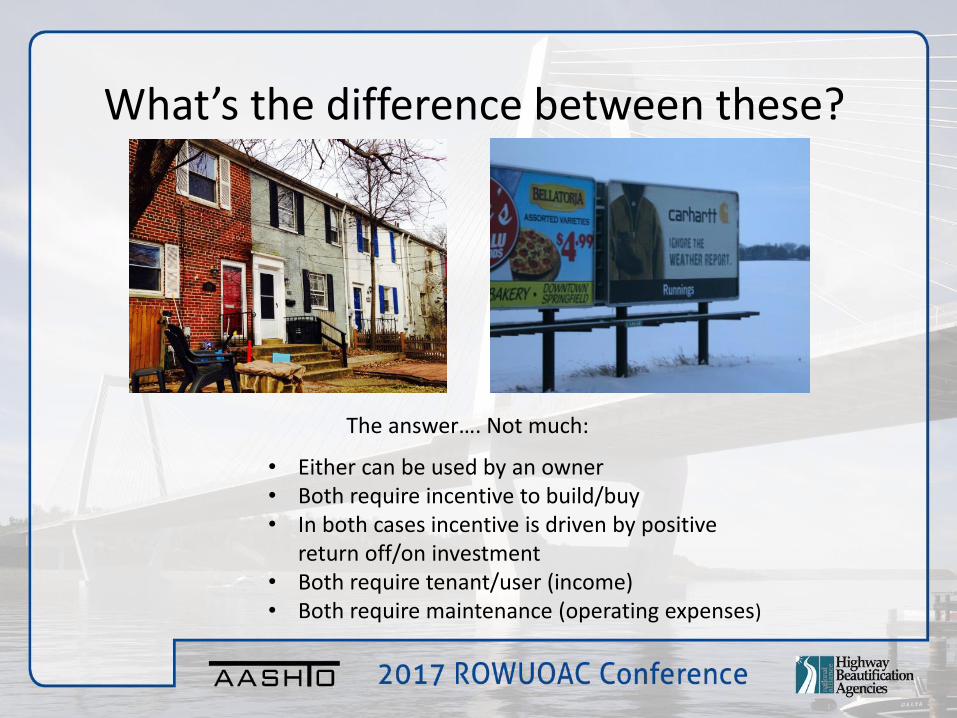

What’s the difference between these?

The answer…. Not much:

• Either can be used by an owner• Both require incentive to build/buy• In both cases incentive is driven by positive

return off/on investment• Both require tenant/user (income)• Both require maintenance (operating expenses)

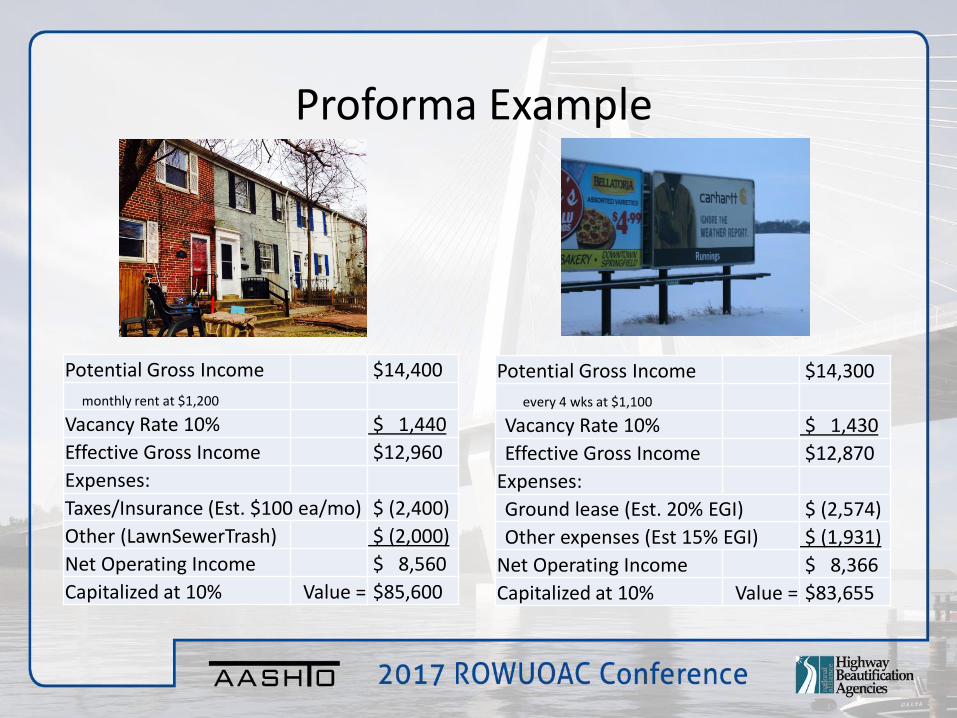

Proforma Example

Potential Gross Income $14,300

every 4 wks at $1,100

Vacancy Rate 10% $ 1,430

Effective Gross Income $12,870

Expenses:

Ground lease (Est. 20% EGI) $ (2,574)

Other expenses (Est 15% EGI) $ (1,931)

Net Operating Income $ 8,366

Capitalized at 10% Value = $83,655

Potential Gross Income $14,400

monthly rent at $1,200

Vacancy Rate 10% $ 1,440

Effective Gross Income $12,960

Expenses:

Taxes/Insurance (Est. $100 ea/mo) $ (2,400)

Other (LawnSewerTrash) $ (2,000)

Net Operating Income $ 8,560

Capitalized at 10% Value = $85,600

Sources of Rates/Multipliers

• Two common multiples in this industry apply to Revenue and to Earnings.• The multiple of revenue is known as the EGIM, (Effective Gross Income

Multiplier). • The multiple of earnings is simply an EBITDA multiple, as typically seen in

business valuation.• So how do we determine and apply the appropriate Rate or Multiplier?

• Comparable Sale Extraction• 10K Data• Cap Rate surveys for similar investments• Multiples in the past few years have tended to be 8X to 12X. • The average multiple of forward EBITDA is about 10X by Lamar.

• Ultimately the use of a rate/multiplier MUST be extracted from the BILLBOARD market.

Factors driving Rates/Multipliers• The appropriate multiple relates more to:

• The company’s fit into its existing portfolio. • Signs in or near major markets with premium sites. • Regions with strong economic fundamentals.• Where there is restrictions on new permits/high barriers to entry.• High traffic counts, good visibility of sign faces, and low competition

from other companies.

Case Study – 16 Billboards

The following is presents a summary of 16 billboards.

Lets assume the following fictional scenario:

• All signs owned by one sign company

• All signs are to be acquired by State Department of Transportation for new interstate along an existing state highway corridor with expanded r/w limits.

• All signs are subject to Eminent Domain

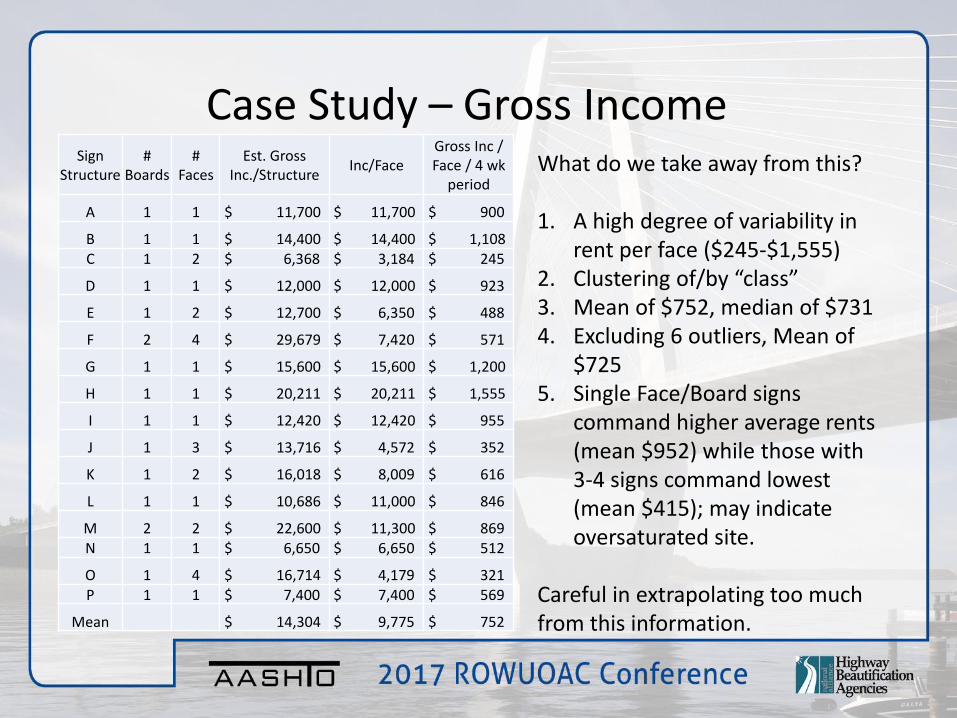

Case Study – Gross IncomeWhat do we take away from this?

1. A high degree of variability in rent per face ($245-$1,555)

2. Clustering of/by “class”3. Mean of $752, median of $7314. Excluding 6 outliers, Mean of

$7255. Single Face/Board signs

command higher average rents (mean $952) while those with 3-4 signs command lowest (mean $415); may indicate oversaturated site.

Careful in extrapolating too much from this information.

Sign Structure

# Boards

# Faces

Est. Gross Inc./Structure

Inc/FaceGross Inc / Face / 4 wk

period

A 1 1 $ 11,700 $ 11,700 $ 900

B 1 1 $ 14,400 $ 14,400 $ 1,108 C 1 2 $ 6,368 $ 3,184 $ 245

D 1 1 $ 12,000 $ 12,000 $ 923

E 1 2 $ 12,700 $ 6,350 $ 488

F 2 4 $ 29,679 $ 7,420 $ 571

G 1 1 $ 15,600 $ 15,600 $ 1,200

H 1 1 $ 20,211 $ 20,211 $ 1,555

I 1 1 $ 12,420 $ 12,420 $ 955

J 1 3 $ 13,716 $ 4,572 $ 352

K 1 2 $ 16,018 $ 8,009 $ 616

L 1 1 $ 10,686 $ 11,000 $ 846

M 2 2 $ 22,600 $ 11,300 $ 869 N 1 1 $ 6,650 $ 6,650 $ 512

O 1 4 $ 16,714 $ 4,179 $ 321 P 1 1 $ 7,400 $ 7,400 $ 569

Mean $ 14,304 $ 9,775 $ 752

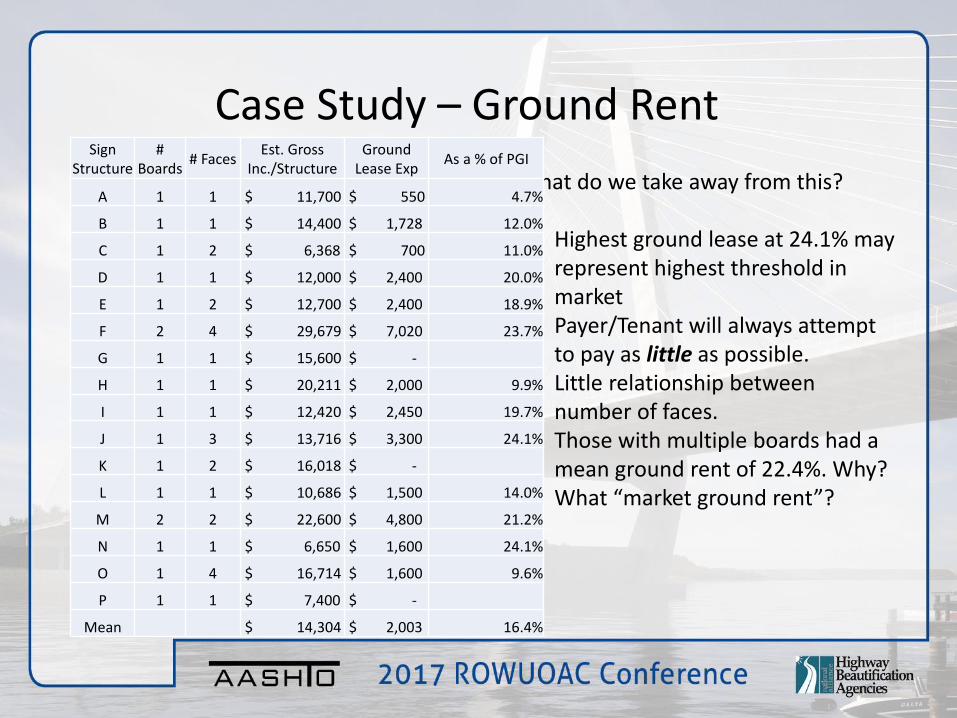

Case Study – Ground Rent

What do we take away from this?

1. Highest ground lease at 24.1% may represent highest threshold in market

2. Payer/Tenant will always attempt to pay as little as possible.

3. Little relationship between number of faces.

4. Those with multiple boards had a mean ground rent of 22.4%. Why?

5. What “market ground rent”?

Sign Structure

# Boards

# FacesEst. Gross

Inc./StructureGround

Lease ExpAs a % of PGI

A 1 1 $ 11,700 $ 550 4.7%

B 1 1 $ 14,400 $ 1,728 12.0%

C 1 2 $ 6,368 $ 700 11.0%

D 1 1 $ 12,000 $ 2,400 20.0%

E 1 2 $ 12,700 $ 2,400 18.9%

F 2 4 $ 29,679 $ 7,020 23.7%

G 1 1 $ 15,600 $ -

H 1 1 $ 20,211 $ 2,000 9.9%

I 1 1 $ 12,420 $ 2,450 19.7%

J 1 3 $ 13,716 $ 3,300 24.1%

K 1 2 $ 16,018 $ -

L 1 1 $ 10,686 $ 1,500 14.0%

M 2 2 $ 22,600 $ 4,800 21.2%

N 1 1 $ 6,650 $ 1,600 24.1%

O 1 4 $ 16,714 $ 1,600 9.6%

P 1 1 $ 7,400 $ -

Mean $ 14,304 $ 2,003 16.4%

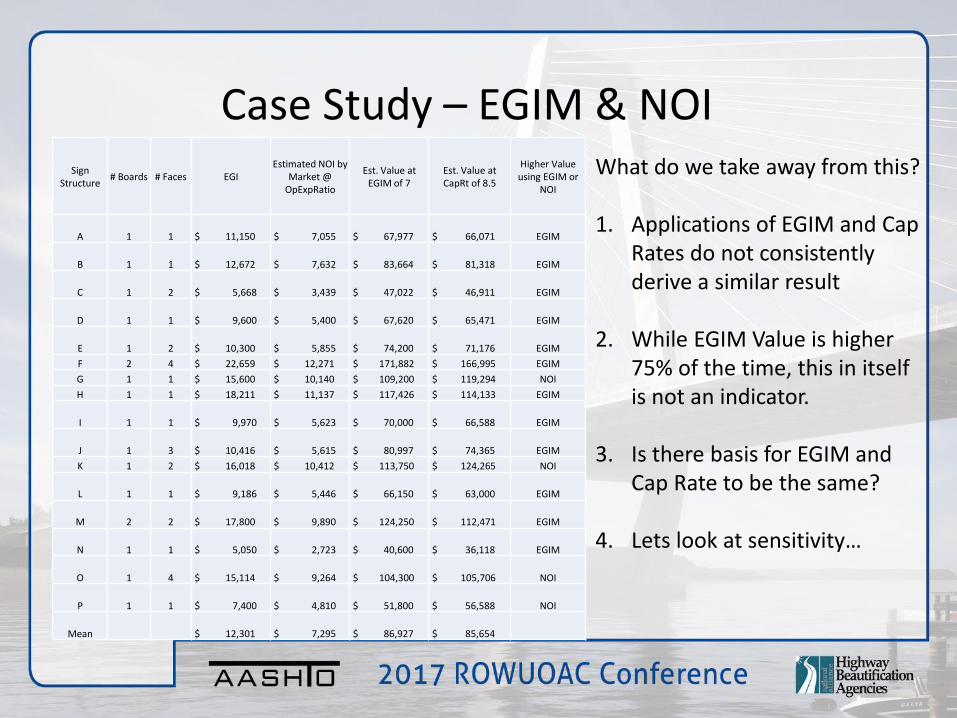

Case Study – EGIM & NOIWhat do we take away from this?

1. Applications of EGIM and Cap Rates do not consistently derive a similar result

2. While EGIM Value is higher 75% of the time, this in itself is not an indicator.

3. Is there basis for EGIM and Cap Rate to be the same?

4. Lets look at sensitivity…

Sign Structure

# Boards # Faces EGIEstimated NOI by

Market @ OpExpRatio

Est. Value at EGIM of 7

Est. Value at CapRt of 8.5

Higher Value using EGIM or

NOI

A 1 1 $ 11,150 $ 7,055 $ 67,977 $ 66,071 EGIM

B 1 1 $ 12,672 $ 7,632 $ 83,664 $ 81,318 EGIM

C 1 2 $ 5,668 $ 3,439 $ 47,022 $ 46,911 EGIM

D 1 1 $ 9,600 $ 5,400 $ 67,620 $ 65,471 EGIM

E 1 2 $ 10,300 $ 5,855 $ 74,200 $ 71,176 EGIM

F 2 4 $ 22,659 $ 12,271 $ 171,882 $ 166,995 EGIM

G 1 1 $ 15,600 $ 10,140 $ 109,200 $ 119,294 NOI

H 1 1 $ 18,211 $ 11,137 $ 117,426 $ 114,133 EGIM

I 1 1 $ 9,970 $ 5,623 $ 70,000 $ 66,588 EGIM

J 1 3 $ 10,416 $ 5,615 $ 80,997 $ 74,365 EGIM

K 1 2 $ 16,018 $ 10,412 $ 113,750 $ 124,265 NOI

L 1 1 $ 9,186 $ 5,446 $ 66,150 $ 63,000 EGIM

M 2 2 $ 17,800 $ 9,890 $ 124,250 $ 112,471 EGIM

N 1 1 $ 5,050 $ 2,723 $ 40,600 $ 36,118 EGIM

O 1 4 $ 15,114 $ 9,264 $ 104,300 $ 105,706 NOI

P 1 1 $ 7,400 $ 4,810 $ 51,800 $ 56,588 NOI

Mean $ 12,301 $ 7,295 $ 86,927 $ 85,654

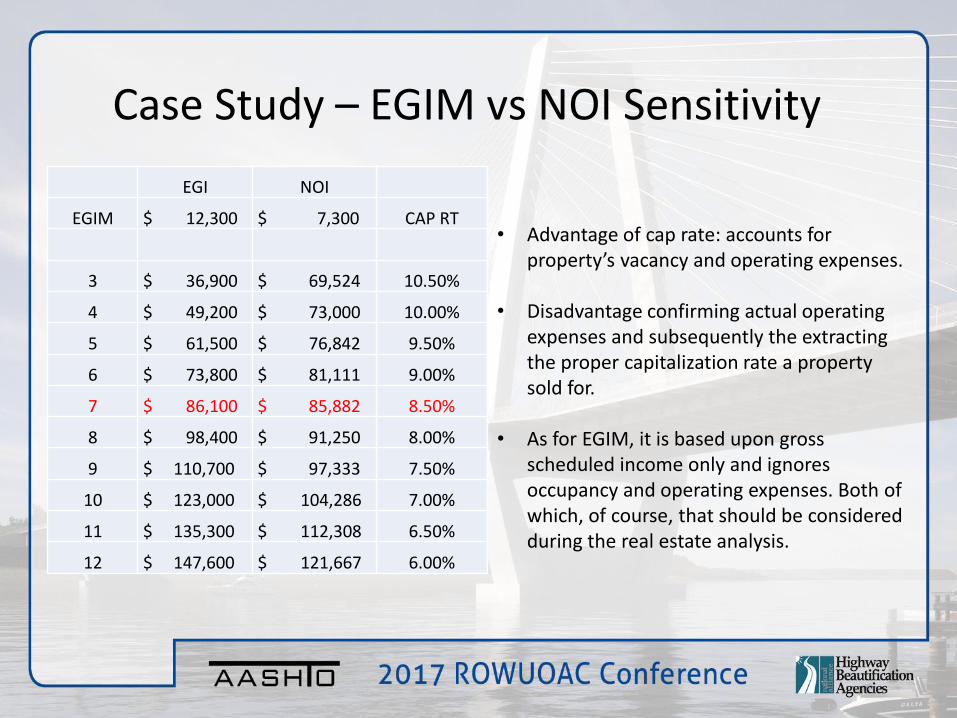

Case Study – EGIM vs NOI Sensitivity

EGI NOI

EGIM $ 12,300 $ 7,300 CAP RT

3 $ 36,900 $ 69,524 10.50%

4 $ 49,200 $ 73,000 10.00%

5 $ 61,500 $ 76,842 9.50%

6 $ 73,800 $ 81,111 9.00%

7 $ 86,100 $ 85,882 8.50%

8 $ 98,400 $ 91,250 8.00%

9 $ 110,700 $ 97,333 7.50%

10 $ 123,000 $ 104,286 7.00%

11 $ 135,300 $ 112,308 6.50%

12 $ 147,600 $ 121,667 6.00%

• Advantage of cap rate: accounts for property’s vacancy and operating expenses.

• Disadvantage confirming actual operating expenses and subsequently the extracting the proper capitalization rate a property sold for.

• As for EGIM, it is based upon gross scheduled income only and ignores occupancy and operating expenses. Both of which, of course, that should be considered during the real estate analysis.

Case Study – Cont’d YET again…

Generic Steps of a R/W Appraiser

• Obtain permit; determine legitimacy• Interview owner; request income & expenses• Survey market for competing signs• Obtain rack rate cards• Interview sign owners• Interview advertisers• Seek comparable sales• Determine market rent• Determine effective gross income• Select income method (EGIM, NOI/CapRt)• Apply methodologies to determine value• Support and defend.

Discussion Topics1. Do we NEED billboards?

2. Does a dilapidated sign have any value?

3. How has technology changed the industry • (phones, regulations, self-driving cars)

4. How has technology OF the industry changed? • (rotating billboards, digital billboards, guerilla marketing)

5. What are the options for relocation of billboards?

6. How does a grandfathered location effect value • (ie: sign not permitted in town limits)

7. Is there Intangible Business Value in billboards? If so, how do we extract it?

Thank you. Questions?