bridgend county borough council financial statements audit 2005/6 – presentation to audit...

TRANSCRIPT

Bridgend County Borough Council

Financial statements audit 2005/6 – Presentation to Audit Committee

26 October 2006

Public Sector

AUDIT

Gilbert LloydIan Pennington

2© 2006 KPMG LLP, the UK member firm of KPMG International, a Swiss cooperative. All rights reserved. This document is confidential and its circulation and use are restricted. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Contents

Analysis of Accounts

Audit Issues and adjustments

Statement on Internal Control

Use of Resources opinion

What next?

3© 2006 KPMG LLP, the UK member firm of KPMG International, a Swiss cooperative. All rights reserved. This document is confidential and its circulation and use are restricted. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Analysis of accounts

Balance sheet Assets and liabilities

Revenue reserves

Council tax and NNDR collection

Consolidated revenue account

4© 2006 KPMG LLP, the UK member firm of KPMG International, a Swiss cooperative. All rights reserved. This document is confidential and its circulation and use are restricted. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Assets and Liabilities

-500-400-300-200-100

0100200300400500

2003 2004 2005 2006£ m

illio

ns

Tangible fixed assets Long term debtors

Current assets Current liabilities

Long term borrowings Government Grants deferred

Capital contributions deferred Provisions and other deferred liabilities

Pension liabilities

Assets

Liabilities

5© 2006 KPMG LLP, the UK member firm of KPMG International, a Swiss cooperative. All rights reserved. This document is confidential and its circulation and use are restricted. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

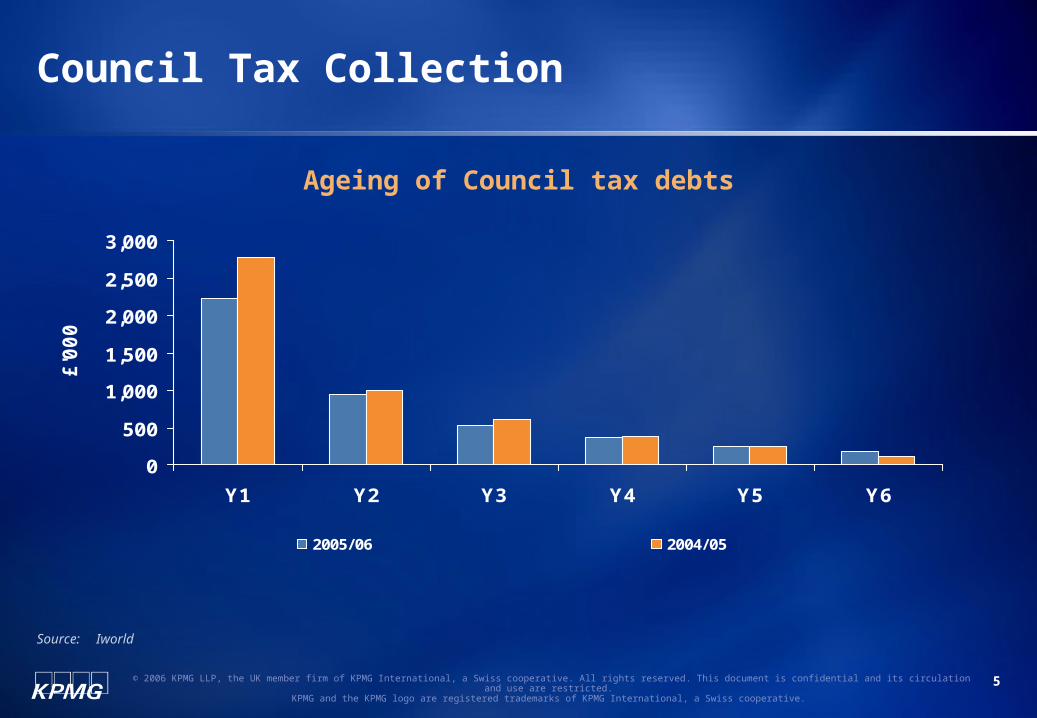

Council Tax Collection

0

500

1,000

1,500

2,000

2,500

3,000

Y1 Y2 Y3 Y4 Y5 Y6

£'0

00

2005/06 2004/05

Ageing of Council tax debts

Source: Iworld

6© 2006 KPMG LLP, the UK member firm of KPMG International, a Swiss cooperative. All rights reserved. This document is confidential and its circulation and use are restricted. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

NNDR Collection

0

500

1,000

1,500

2,000

2,500

3,000

Y1 Y2 Y3 Y4 Y5 Y6 Y7 Y8

£'0

00

2005/06 2004/05

Ageing of NNDR debts

Source: Iworld

7© 2006 KPMG LLP, the UK member firm of KPMG International, a Swiss cooperative. All rights reserved. This document is confidential and its circulation and use are restricted. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Revenue Reserves

-5,000

0

5,000

10,000

15,000

20,000

25,000

2003 2004 2005 2006

£'0

00

Council Fund Housing Revenue Account Delegated schools

Directorate reserves - surplus Directorate reserves - deficit Specific reserves

Source: Draft financial statements

8© 2006 KPMG LLP, the UK member firm of KPMG International, a Swiss cooperative. All rights reserved. This document is confidential and its circulation and use are restricted. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Consolidated Revenue Account

Detailed narrative in the accounts

Directorate deficit £1.5m as previously forecast

Offset by better than budgeted council tax collection

Management looking at ways of improving transparency

9© 2006 KPMG LLP, the UK member firm of KPMG International, a Swiss cooperative. All rights reserved. This document is confidential and its circulation and use are restricted. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Contents

Analysis of Accounts

Audit Issues and adjustments

Statement on Internal Control

Use of Resources opinion

What next?

10© 2006 KPMG LLP, the UK member firm of KPMG International, a Swiss cooperative. All rights reserved. This document is confidential and its circulation and use are restricted. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Audit issues and Adjustments

Audit adjustments – Revenue Account

Audit adjustments – Balance Sheet

Representation letter

Post balance sheet events

11© 2006 KPMG LLP, the UK member firm of KPMG International, a Swiss cooperative. All rights reserved. This document is confidential and its circulation and use are restricted. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Audit adjustments – Revenue Account

Reconciliation of Surplus reported to Council and final accounts

£’000

Accounts year end surplus as previously reported 47

Write off of old balances no longer due (91)

Correction of bad debt provision calculation 280

189

Surplus for the year 236

Source: Audit working papers and draft accounts

12© 2006 KPMG LLP, the UK member firm of KPMG International, a Swiss cooperative. All rights reserved. This document is confidential and its circulation and use are restricted. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Audit Adjustments – Balance Sheet

Summary of Audit differences

Amounts £’000 Balance sheet

Draft Total assets less liabilities as previously reported 90,760

Consolidated revenue Account (as per previous slide) 189

Reclassification of Insurance provision 1,209

Reconciliation between Housing benefit grant claim and year end debtor 136

Maesteg Washeries cost of works in year incorrectly capitalised (347)

Assets valued in the year not adjusted to reflect the movement in the asset value (91)

Ynysawdre Swimming pool, building impairment not recognised (1,850)

Total assets less liabilities as at 31 March 2006 90,006

13© 2006 KPMG LLP, the UK member firm of KPMG International, a Swiss cooperative. All rights reserved. This document is confidential and its circulation and use are restricted. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Audit issues and Adjustments

Representation letter

Post balance sheet events

No unadjusted audit differences to report

14© 2006 KPMG LLP, the UK member firm of KPMG International, a Swiss cooperative. All rights reserved. This document is confidential and its circulation and use are restricted. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Contents

Analysis of Accounts

Audit Issues and adjustments

Statement on Internal Control

Use of Resources opinion

What next?

15© 2006 KPMG LLP, the UK member firm of KPMG International, a Swiss cooperative. All rights reserved. This document is confidential and its circulation and use are restricted. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Statement on Internal Control

New statement prepared for 2005/06

Process has been well performed

Bought into at the highest level (Cabinet, CMB and Audit Committee)

SIC reported in the first draft of the accounts amended to reflect Internal Audit’s “unsatisfactory” opinion

Detailed action plans taken out of final draft

The statement is very personalised to Bridgend, and interesting and informative

Authority should continue to review the process for 2006/7

16© 2006 KPMG LLP, the UK member firm of KPMG International, a Swiss cooperative. All rights reserved. This document is confidential and its circulation and use are restricted. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Statement on Internal Control - continued

Audit Committee’s role is to:

Review SIC

Consider it in context of your work over the last 12 months Reports read

Presentations given and

Questions answered

Make recommendations to the signatories

Audit Committee has considered the draft of the SIC as previously reported and recommended it to signatories subject to an amendment to Internal Audit year end opinion

17© 2006 KPMG LLP, the UK member firm of KPMG International, a Swiss cooperative. All rights reserved. This document is confidential and its circulation and use are restricted. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Contents

Analysis of Accounts

Audit Issues and adjustments

Statement on Internal Control

Use of Resources opinion

What next?

18© 2006 KPMG LLP, the UK member firm of KPMG International, a Swiss cooperative. All rights reserved. This document is confidential and its circulation and use are restricted. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Use of Resources

Background

Use of resources opinion – types

Use of resources opinion 2005/6

19© 2006 KPMG LLP, the UK member firm of KPMG International, a Swiss cooperative. All rights reserved. This document is confidential and its circulation and use are restricted. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Use of Resources opinion

New code of audit practice

More formalised opinion

Eventually opinion will be incorporated into the financial statements

2005/06 reported via the Relationship Manager’s audit letter – which will include detailed comments and issues

National moderation process

20© 2006 KPMG LLP, the UK member firm of KPMG International, a Swiss cooperative. All rights reserved. This document is confidential and its circulation and use are restricted. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Use of Resources opinion

Links to Authority’s responsibilities

Not a “yes/no” opinion

Details will be in the RMAL

21© 2006 KPMG LLP, the UK member firm of KPMG International, a Swiss cooperative. All rights reserved. This document is confidential and its circulation and use are restricted. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Use of Resources Opinion 2005/6

Key matters

Performance management of services and staff (being dealt with by performance management flagship project and HR flagship project

System of internal control (as evidence by Chief Internal Auditor’s annual report)

Arrangements to maximise use of corporate asset base

Issues arising in year (primarily children’s services, and corporate culture review)

There are a number of other issues which will be reported in the RMAL

22© 2006 KPMG LLP, the UK member firm of KPMG International, a Swiss cooperative. All rights reserved. This document is confidential and its circulation and use are restricted. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Contents

Analysis of Accounts

Audit Issues and adjustments

Statement on Internal Control

Use of Resources opinion

What next?

23© 2006 KPMG LLP, the UK member firm of KPMG International, a Swiss cooperative. All rights reserved. This document is confidential and its circulation and use are restricted. KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

What next?

Relationship Manager’s Annual Letter

Regulatory plan for 2006/07

Accounts signing process