broadcast & enterprise connectivity solutions

TRANSCRIPT

Broadcast & Enterprise Connectivity SolutionsDenis Suggs

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 3© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 3

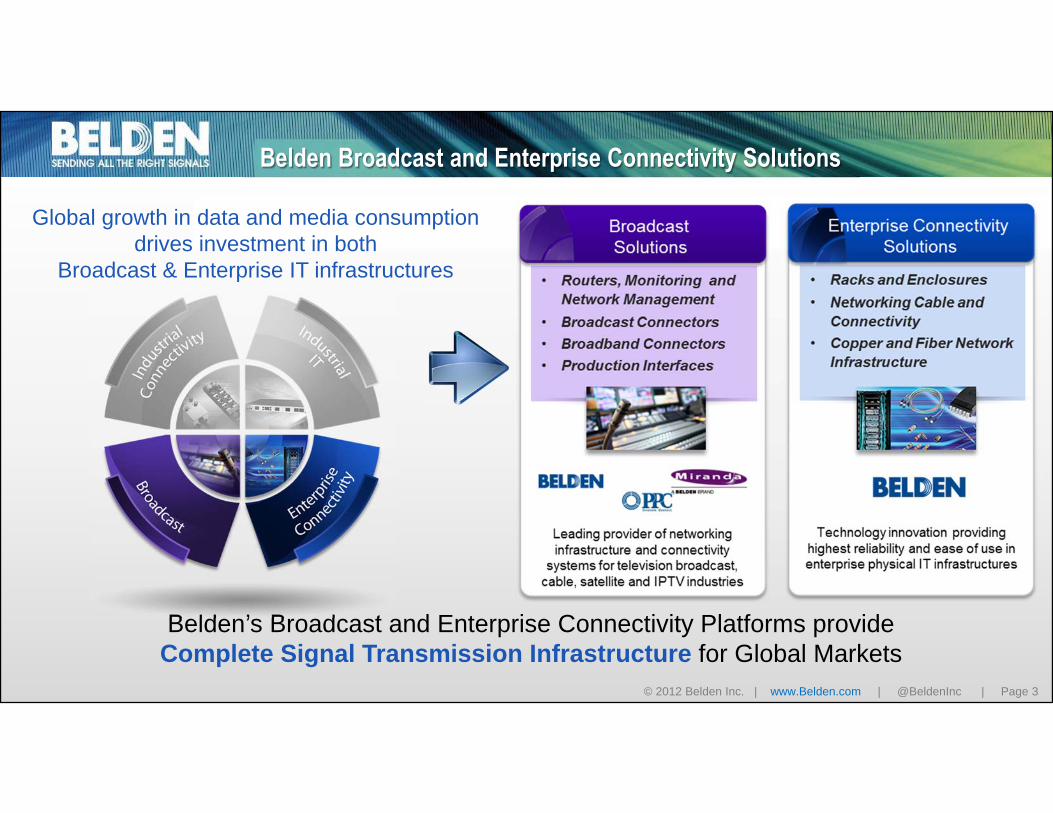

Belden Broadcast and Enterprise Connectivity Solutions

Global growth in data and media consumption drives investment in both

Broadcast & Enterprise IT infrastructures

Belden’s Broadcast and Enterprise Connectivity Platforms provide Complete Signal Transmission Infrastructure for Global Markets

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 4© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 4

Broadcast Solutions

1. Estimated 2012 results. Thermax and Raydex not shown.

IndustrialConnectivity Solutions

Industrial ITSolutions

Enterprise Connectivity Solutions

Revenue ≈ $640M1 | Gross Margins ≈ 24-26% | Operating Profit Margins ≈ 8-10%

Enterprise Connectivity Solutions

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 5© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 5

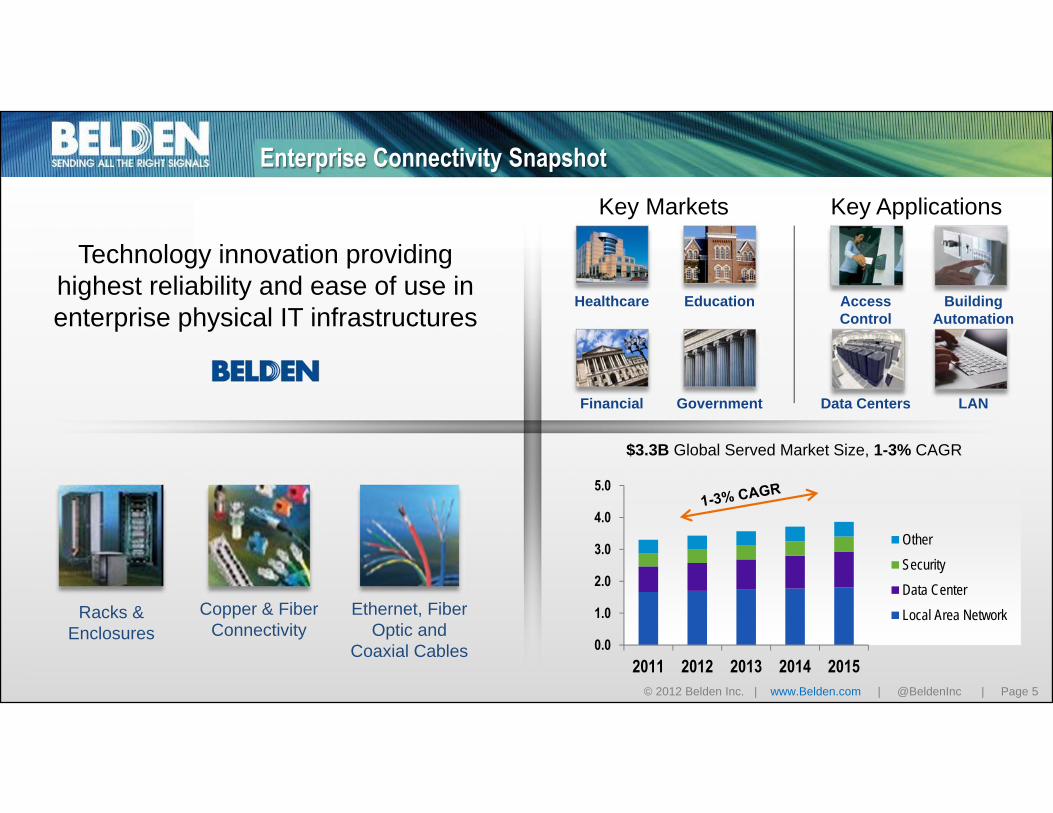

Enterprise Connectivity Snapshot

Technology innovation providing highest reliability and ease of use in enterprise physical IT infrastructures

$3.3B Global Served Market Size, 1-3% CAGR

Ethernet, Fiber Optic and

Coaxial Cables

Copper & Fiber Connectivity

Racks & Enclosures

Key Markets Key Applications

Healthcare

Government

Education

Financial

Access Control

LAN

Building Automation

Data Centers

0.0

1.0

2.0

3.0

4.0

5.0

2011 2012 2013 2014 2015

OtherSecurityData CenterLocal Area Network

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 6© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 6

Enterprise Connectivity Market Drivers

Customers demand reliable transmission of data intensive streaming video, which requires high bandwidth and high performance IT infrastructure

2007 2012

DVD only service

20 million visitors per month

23 million streaming video

subscribers

800 million visitors watching 4 billion hours each month

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 7© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 7

Enterprise Connectivity Market DriversGrowth in data consumption is occurring across all access types

Growth in both wired and wireless data access requires an underlying IT infrastructure to service the demand

Mobile Access92% CAGR

Fixed / WiFi Access39% CAGR

Fixed / Wired Access24% CAGR

in data consumption through 2015

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 8© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 8

Enterprise Connectivity Market DriversConsumption of data accelerating fastest in emerging markets

Belden’s global reach and relationships are positioned to convert this Enterprise Connectivity market growth into revenue

Latin America IP traffic will grow at 49% CAGR

Asia Pacific data consumption will reach

41.1 exabytes per month

By 2016,Middle East and Africa IP

traffic will grow at 57% CAGR

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 9© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 9

Enterprise Connectivity Growth Drivers

Accelerating growth in global data consumption drives investment in the IT infrastructure offered by Belden Enterprise Connectivity solutions

Business IT Investment in Data Centers and Local

Area Networks (LAN)

Data Traffic Jam

Global video streaming, social media, cloud

computing

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 10© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 10

Enterprise Connectivity Growth Drivers

0.00.20.40.60.81.01.21.4

2008 2009 2010 2011 2012

Belden Enterprise Connectivity vs. Non-Residential Investment

2008 = 1.0

Belden Enterprise Connectivity Non-Res Investment

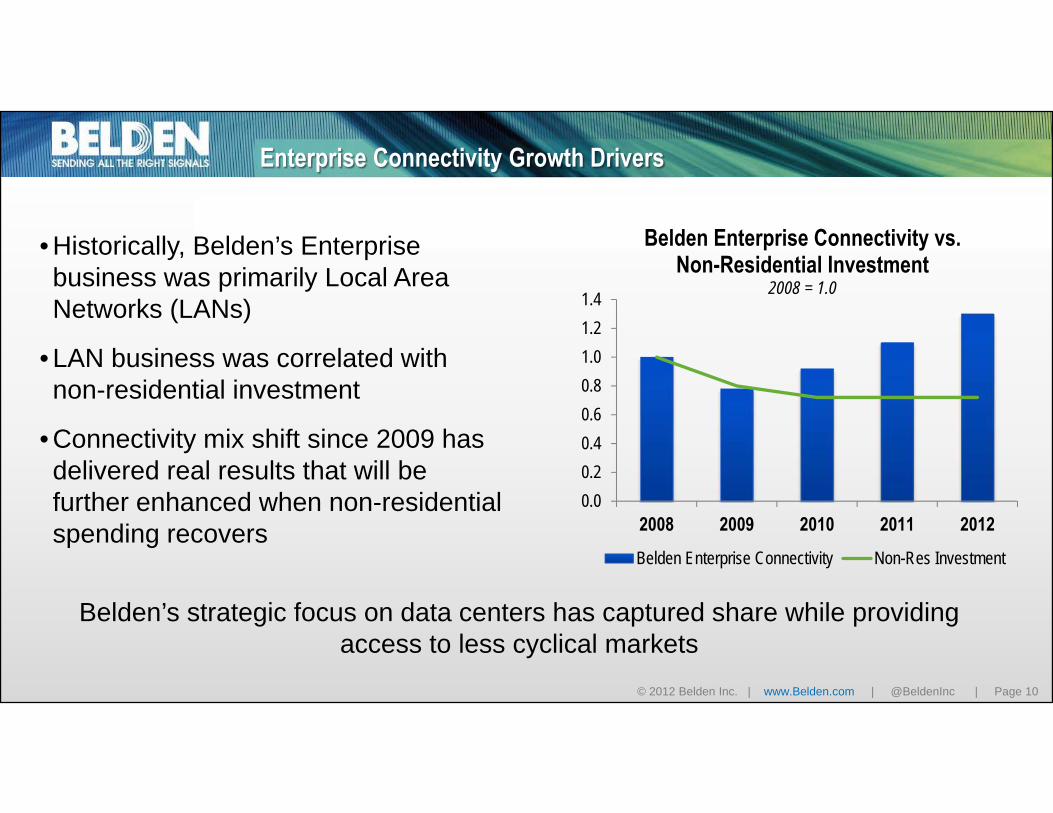

Belden’s strategic focus on data centers has captured share while providing access to less cyclical markets

• Historically, Belden’s Enterprise business was primarily Local Area Networks (LANs)

• LAN business was correlated with non-residential investment

• Connectivity mix shift since 2009 has delivered real results that will be further enhanced when non-residential spending recovers

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 11© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 11

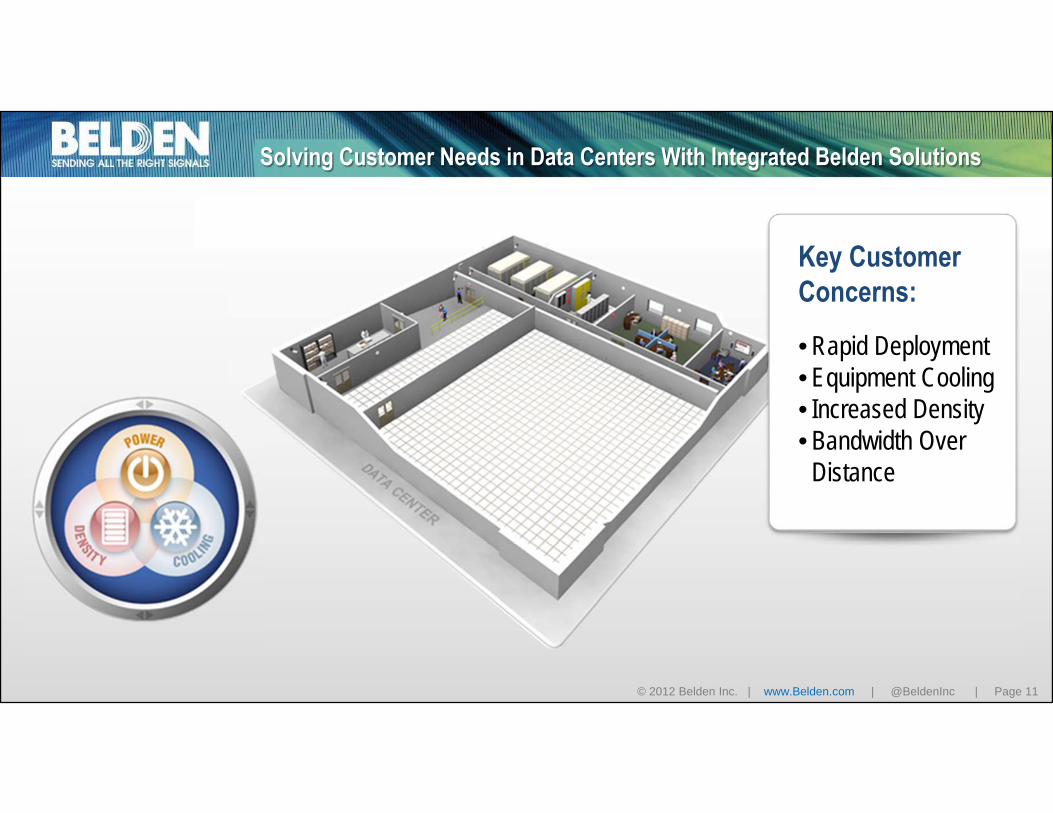

Solving Customer Needs in Data Centers With Integrated Belden Solutions

Key Customer Concerns:

• Rapid Deployment• Equipment Cooling• Increased Density• Bandwidth Over

Distance

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 12© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 12

Solving Customer Needs in Data Centers With Integrated Belden Solutions

Rapid Deployment/ Cable ManagementBelden Racks & Enclosures

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 13© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 13

Solving Customer Needs in Data Centers With Integrated Belden Solutions

Rapid Deployment/ Cable ManagementBelden Racks & Enclosures

Equipment Cooling/Lower Energy Costs

Belden AEHC System

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 14© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 14

Solving Customer Needs in Data Centers With Integrated Belden Solutions

Rapid Deployment/ Cable ManagementBelden Racks & Enclosures

Equipment Cooling/Lower Energy Costs

Belden AEHC System

Density / Reduced Alien Cross TalkBelden connectivity,pre-terminated cables

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 15© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 15

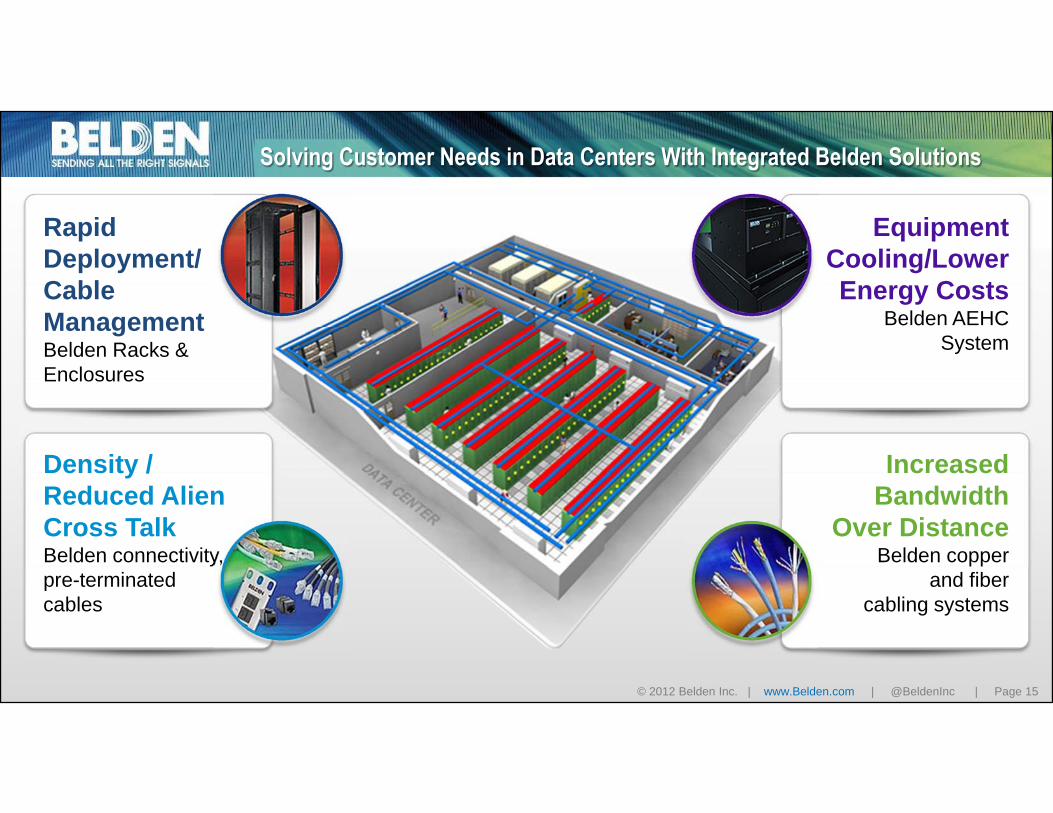

Solving Customer Needs in Data Centers With Integrated Belden Solutions

Rapid Deployment/ Cable ManagementBelden Racks & Enclosures

Equipment Cooling/Lower Energy Costs

Belden AEHC System

Density / Reduced Alien Cross TalkBelden connectivity,pre-terminated cables

Increased Bandwidth

Over DistanceBelden copper

and fiber cabling systems

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 16© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 16

Expanding Margins with Integrated Enterprise Connectivity Solutions

Fully-Optimized, Integrated Solutions

Air Flow Solutions

Copper & Fiber Cable Systems

Connectivity

Racks and Enclosures

Pre-configured Racks

Pre-terminated Solutions

LOW HIGHValue Add, Margin

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 17© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 17

Driving Growth Through Integrated Solutions and Belden MDS

Fully-Optimized, Integrated Solutions

Belden Market Delivery System Organic

Growth

Margin Expansion

Our customers look to us as a trusted advisor to deliver the solutions they need

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 18© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 18

Broadcast

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 19© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 19

Broadcast Solutions

Enterprise Connectivity Solutions

1. Estimated 2012 results.

IndustrialConnectivity Solutions

Industrial ITSolutions

Broadcast Solutions

Revenue ≈ $590M1 | Gross Margins ≈ 38-40% | Operating Profit Margins ≈ 13-15%

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 20© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 20

Broadcast Overview

Leading provider of networking infrastructure and connectivity systems for television broadcast, cable, satellite and IPTV industries

$3.5B Global Served Market, 3-5% CAGRBrands & Product Portfolio

Interfaces, Routers, &

Playout

Camera Mounted Fiber

Solutions

Precision A/V Cable &

Connectivity

0.0

1.0

2.0

3.0

4.0

5.0

2011 2012 2013 2014 2015

ConnectivityIT Playout & MonitoringHardwareCable

Miranda TechnologiesStrath Goodship

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 23© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 23

Miranda

world leader in hardwareand software solutionsthat enable television

broadcasters, cable, satellite and IPTV operators to

competitively deliver more content with higher quality

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 24© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 24

Television Value Chain is Evolving

Creation Aggregation Delivery Consumers

Over the Top (OTT)

Television Service

ProvidersBroadcastersStudios

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 25© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 25

Market Drivers Influencing Broadcast

More HD and Live TV Driving Traditional Viewing

Channel Count Increasing

Increasing Over the Top & VOD Content Delivery

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 26© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 26

Market Drivers Influencing Broadcast

Channel Count Increasing

Increasing Over the Top & VOD Content Delivery

More HD and Live TV Driving Traditional Viewing

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 27© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 27

HD Still Has a Long Way to Go

Technology Used by TV BroadcastersCURRENT TV Operations TV Operations IN 2-3 YEARS

Source: Devoncroft – Big Broadcast Survey

Standard & Definitions

HD Analog Standard & Definitions

HD Analog

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 28© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 28

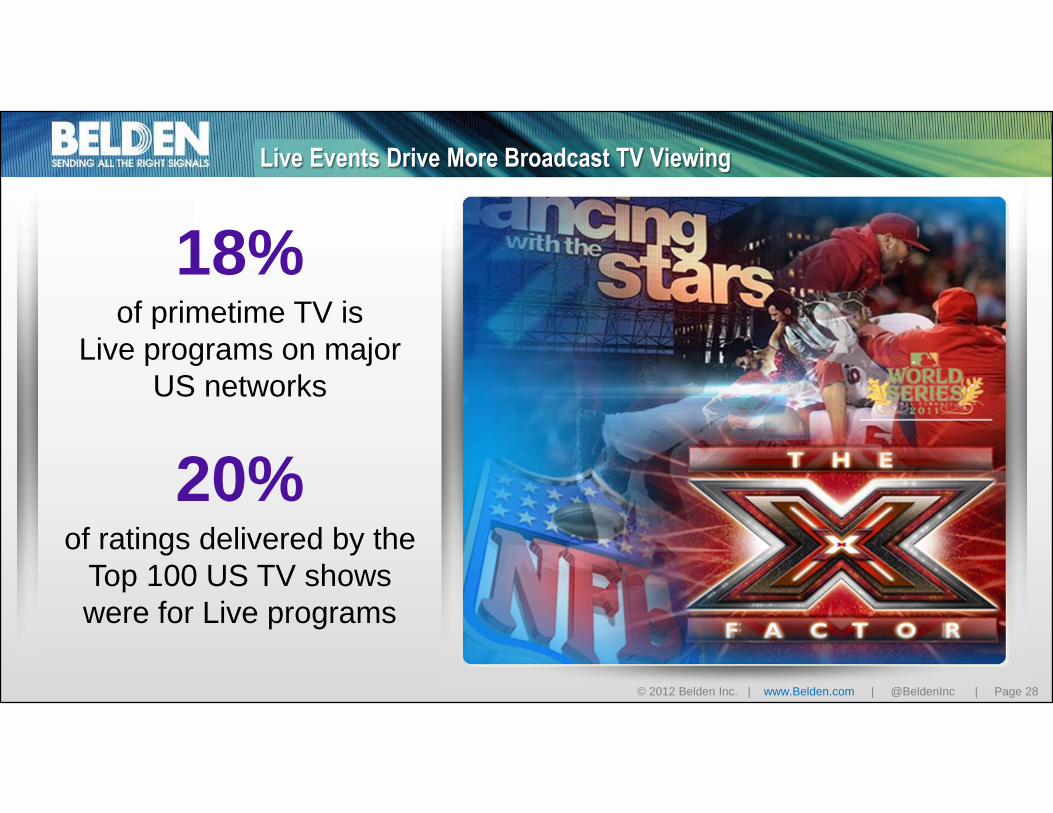

Live Events Drive More Broadcast TV Viewing

18%of primetime TV is

Live programs on major US networks

20%of ratings delivered by the

Top 100 US TV shows were for Live programs

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 29© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 29

Broadcasters Need More Complex Infrastructure to Support Live HD

More complex studio productions with more

cameras and more remote feeds

More demand for Miranda infrastructure

and monitoring solutionsCentral Switching Center

ABC Network Operation Center, New York

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 30© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 30

Miranda Infrastructure Products Benefiting from Live HD Momentum

Integration of Miranda’s infrastructure products simplifies complex live operations

Densite Interfacing Products

Enterprise Class Routers

Kaleido –XMulti-Viewers

TelecastFiber Interfaces

Broadcasters: HD Digital | Live TV

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 31© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 31

Market Drivers Influencing Broadcast

Channel Count Increasing

Increasing Over the Top & VOD Content Delivery

More HD and Live TV Driving Traditional Viewing

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 32© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 32

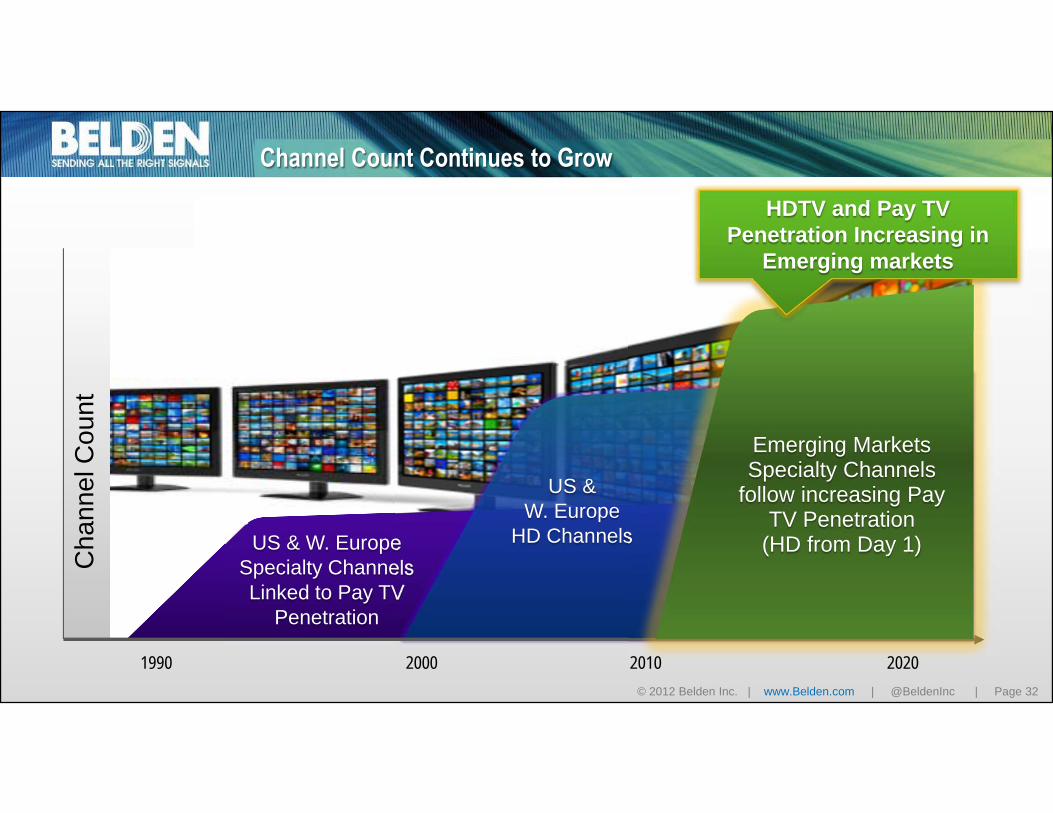

Channel Count Continues to Grow

US & W. Europe Specialty ChannelsLinked to Pay TV

Penetration

US & W. Europe

HD Channels

Emerging MarketsSpecialty Channels

follow increasing Pay TV Penetration

(HD from Day 1)

Cha

nnel

Cou

nt

HDTV and Pay TV Penetration Increasing in

Emerging markets

1990 2000 2010 2020

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 33© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 33

Growth Opportunity for Miranda Infrastructure and Playout Products

Miranda Infrastructure Products Playout

Densite Interfacing Products

Enterprise Class Routers

Kaleido –XMulti-Viewers

TelecastFiber

Interfaces

iTX IT Based Playout

Master Ctl/Branding

Broadcasters: Increasing Channel Count

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 34© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 34

A Changing Business Presence

Wins accelerating sales in Emerging Markets

Miranda Revenue

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 35© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 35

Market Drivers Influencing Broadcast

Channel Count Increasing

Increasing Over the Top & VOD Content Delivery

More HD and Live TV Driving Traditional Viewing

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 36© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 36

Any Content to Any Device Creates Opportunity for Us

Watch Anytime…and Anywhere

Over 33% of Americans have watched TV on an “alternative platform”

Internet video to TV doubled in 2011

HD VoD surpassed standard defby end of 2011

VoD traffic to triple by 2016

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 37© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 37

Consumers

Video Distribution

Broadcasters distributing content through Traditional and Over the Top methods

Creation Aggregation Delivery

Television Service

ProvidersBroadcastersStudios

Over the Top (OTT)

LINEAR (TV By Appointment)

Over the Top

NON LINEAR (Catch Up TV) Video on Demand

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 38© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 38

iTX Based Playout and Publishing Supports Linear and Non-Linear Delivery

iTX Based Playoutand

Content Publishing

enterprisesuiteVOD Publishing

Broadcasters

LINEAR (TV By Appointment)

Over the Top

NON LINEAR (Catch Up TV) Video on Demand

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 39© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 39

Miranda’s Go To Market

Best-in-class by creating customer value

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 40© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 40

What Makes the Combination of Belden and Miranda So Compelling?

• Access to the venue/outside broadcast market through Telecast products

• Ability to offer unique combinations with Belden’s connectivity products

• Deeper access to emerging markets, such as Brazil

• Belden’s business systems to enhance Miranda’s efficiencies, quality and growth

• Premium brands of the broadcast industry

• Strong relationships with Broadcasters for key functionality

• A unique skillset and track record in product development

Together, strongly positioned with scale, breadth and uniqueness of solutions

Customer Panel

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 42© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 42

Customer Bios

Joe MardiniVice President - Data Centre Solutions & Mid MarketBell Business Markets

Ed MueskesVice President Connectivity SolutionsSchneider Electric

Financial OverviewHenk Derksen

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 45© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 45

Consistent Financial Performance

Organic Revenue Growth: 4 – 6%

Operating Profit Margin: 14 – 16%

Free Cash Flow: Exceed Net Income

Return on Invested Capital: 13 – 15%

3-Year Financial Goals

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 46© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 46

Organic Revenue Growth

Revenues ($Million) and Organic Growth (%)

Market provided a challenging environment for growth in 2012

Organic Growth Goal:4% - 6%

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 47© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 47

Operating Profit Margin

Operating Profit ($Million)

Accelerated transformation drives higher margin goal

Operating Profit Margin Goal:

14% - 16%

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 48© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 48

Operating Profit Margin Bridge

Operating Profit Margin, 2011-2012E

Improving business model

10.5%

11.7%80 bps

50 bps (40) bps 30 bps

8%

9%

10%

11%

12%

13%

14%

FY 2011 Mix Productivity Leverage on Growth

Acquisitions FY 2012E1

1. Based on management’s best estimates.

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 49© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 49

Quality of Earnings: Free Cash Flow Generation

Since 2005, Belden has delivered free cash flow in excess of net income

110%

173%

126%114%

208%

124% 126%101%

$0.50

$0.75

$1.00

$1.25

$1.50

$1.75

$2.00

$2.25

$2.50

$2.75

$3.00

$3.25

$3.50

$3.75

0%

50%

100%

150%

200%

250%

2005 2006 2007 2008 2009 2010 2011 2012EFCF Per Share FCF, % of NI

1

1. Based on management’s best estimates.

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 50© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 50

Dry Powder

Estimated Available Funds (Year-end 12/31/2012)

Belden is well-capitalized and strategically advantaged

Excess Cash$200 million

Committed Deal Capacity

$200 million

Result into$400 million in dry powder

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 51© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 51

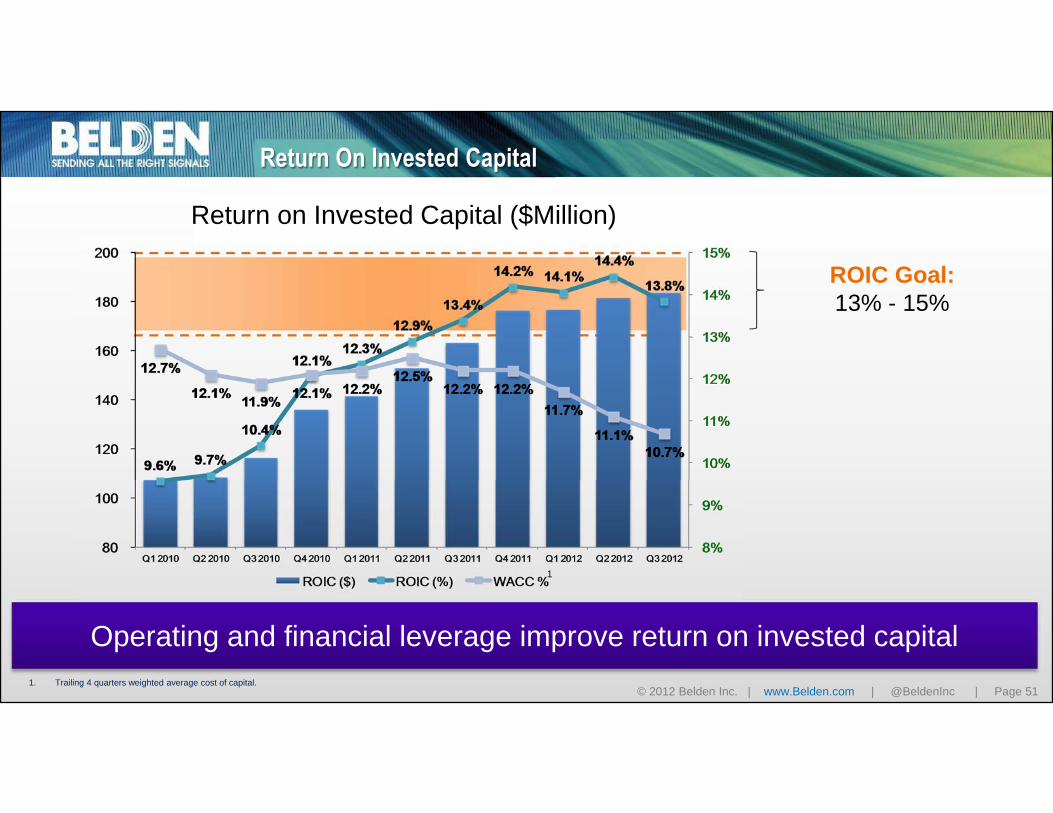

Return On Invested Capital

Operating and financial leverage improve return on invested capital

Return on Invested Capital ($Million)

ROIC Goal:13% - 15%

1. Trailing 4 quarters weighted average cost of capital.

1

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 52© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 52

Return On Invested Capital

Operating and financial leverage improve return on invested capital

Return on Invested Capital ($Million)

ROIC Goal:13% - 15%

1. Trailing 4 quarters weighted average cost of capital.

1

ValueCreation

Q&A

2012 Investor and Analyst Meeting

2012 Investor and Analyst Meeting

Thank You.

2012 Investor and Analyst Meeting

Appendix

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 56

GAAP-to-Non-GAAP ReconciliationQ1 Q2 Q3 Q4

GAAP revenues 384,424$ 410,563$ 396,927$ 425,176$ Revenues from acquisitions - - - (6,544) Purchase accounting effects related to acquisitions - - - - Discontinued operations GAAP revenues 15,924 15,578 14,545 - Deferred revenue adjustments (5,885) (5,377) (3,509) - Non-GAAP revenues 394,463$ 420,764$ 407,963$ 418,632$

GAAP operating income 31,295$ 39,610$ 41,586$ 16,698$ Amortization of intangibles 2,713 2,587 2,600 3,289 Asset impairment - - - 16,574 Accelerated depreciation 1,108 1,108 - - Purchase accounting effects related to acquisitions 988 635 635 7,149 Deferred gross profit adjustments (3,346) (3,019) (1,927) - Discontinued operations GAAP operating loss (3,169) (2,666) (3,176) - Severance and other restructuring costs 4,084 3,785 1,663 509 Total operating income adjustments 2,378 2,430 (205) 27,521 Non-GAAP operating income 33,673$ 42,040$ 41,381$ 44,219$ Non-GAAP operating income as a percent of revenues 8.5% 10.0% 10.1% 10.6%

Q1 Q2 Q3 Q4

GAAP revenues 461,628$ 536,251$ 519,713$ 464,361$ Revenues from acquisitions - - - - Purchase accounting effects related to acquisitions - - - - Discontinued operations GAAP revenues - - - - Deferred revenue adjustments - - - - Non-GAAP revenues 461,628$ 536,251$ 519,713$ 464,361$

GAAP operating income 42,073$ 58,212$ 51,863$ 34,858$ Amortization of intangibles 3,679 3,347 3,371 3,375 Asset impairment - - - 2,549 Purchase accounting effects related to acquisitions - - - - Deferred gross profit adjustments - - - - Severance and other restructuring costs - - - 4,938 Total operating income adjustments 3,679 3,347 3,371 10,862 Non-GAAP operating income 45,752$ 61,559$ 55,234$ 45,720$ Non-GAAP operating income as a percent of revenues 9.9% 11.5% 10.6% 9.8%

Q1 Q2 Q3

GAAP revenues 464,291$ 484,042$ 490,367$ Revenues from acquisitions - - - Purchase accounting effects related to acquisitions - - 1,710 Discontinued operations GAAP revenues - - - Deferred revenue adjustments - - 1,080 Non-GAAP revenues 464,291$ 484,042$ 493,157$

GAAP operating income (loss) 43,965$ 58,351$ (7,609)$ Amortization of intangibles 3,235 2,570 7,798 Asset impairment - - 29,998 Purchase accounting effects related to acquisitions - - 11,219 Deferred gross profit adjustments - - 864 Severance and other restructuring costs - - 17,427 Total operating income adjustments 3,235 2,570 67,306 Non-GAAP operating income 47,200$ 60,921$ 59,697$ Non-GAAP operating income as a percent of revenues 10.2% 12.6% 12.1%

(In tho us ands , except pe rcentages )

2010

(In tho us ands , except pe rcentages )

(In tho us ands , except pe rcentages )

2011

2012

© 2012 Belden Inc. | www.Belden.com | @BeldenInc | Page 57

GAAP-to-Non-GAAP Reconciliation

Free Cash Flow

We define free cash flow, which is a non-GAAP financial measure, as net cash provided by operating activities less capital expenditures, net of proceeds from the disposal of tangibleassets. We believe free cash flow provides useful information to investors regarding our ability to generate cash from business operations that is available for acquisitions and otherinvestments, service of debt principal, dividends and share repurchases. We use free cash flow, as defined, as one financial measure to monitor and evaluate performance andliquidity. Non-GAAP financial measures should be considered only in conjunction with financial measures reported according to accounting principles generally accepted in theUnited States. Our definition of free cash flow may differ from definitions used by other companies.

2011 2010 2009 2008 2007 2006 2005

GAAP net cash provided by operating activities 184,563$ 111,549$ 151,810$ 173,874$ 205,556$ 141,156$ 49,149$

Capital expenditures, net of proceeds from

the disposal of tangible assets (38,840) (25,769) (38,725) (28,434) (34,452) (17,105) (12,157)

Non-GAAP free cash flow 145,723$ 85,780$ 113,085$ 145,440$ 171,104$ 124,051$ 36,992$

GAAP diluted weighted average shares 47,415 47,783 46,594 44,692 50,615 50,276 52,122

Adjustment for anti-dilutive shares that are dilutive under non-GAAP measures - - 405 2,740 - - -

Non-GAAP diluted weighted average shares 47,415 47,783 46,999 47,432 50,615 50,276 52,122

Non-GAAP free cash flow per share 3.07$ 1.80$ 2.41$ 3.07$ 3.38$ 2.47$ 0.71$

(In tho us ands , except per s hare amo unts )