brookfield asset management/media/files/b/brookfield-bam-ir/ir day... · 1) represents total...

TRANSCRIPT

Brookfield Asset Management

INVESTOR DAY

SEPTEMBER 26 , 2018

2

Agenda

Strategic ReviewBruce Flatt, Senior Managing Partner & CEO

Focusing on Our People and CultureLori Pearson, Senior Managing Partner & COO

Financial ReviewBrian Lawson, Senior Managing Partner & CFO

Q&A

3

We continue to expand our franchise as one of the largest global alternative asset managers

4

$300B+ASSETS UNDER MANAGEMENT

80,000+EMPLOYEES

30+COUNTRIES

530+INSTITUTIONAL

INVESTORS

$129B+FEE BEARING

CAPITAL

5

Over the last year1 …

Raised $20 billion of capital in our public and private funds

Realized $13 billion of proceeds from asset sales

Notes/Assumptions:1) For the period September 1, 2017 – August 31, 2018

Deployed $33 billion of capital in high-quality assets, globally

6

Returns have been strong and this should continue

We expect interest rates to stay lowish

International trade is very topical

Currencies are volatile

Rising rates generally lead to growth in our cash flows

Our assets provide shelter

We earn high returns and hedge where we can

7

Irrespective of markets and politics, we continue to focus on:

Strengthening our balance sheets

Deploying capital for value

Recycling proceeds into higher yielding opportunities

Being patient, waiting for market breaks

8

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

BAM returns % S&P U.S. 10-year yields

Returns from value investing in real assets have been strong

7%1

Notes/Assumptions:1) Represents total return, compound with dividends reinvested2) Represents total return, compound with coupon reinvested

19%1

4%2

9

1Increasing real asset allocations

2Best-in-class

investor service

4Focusing

on our people and culture

There are four key factors to our growth strategy

3Identifying great

investment opportunities

10

Increasing Real Asset Allocations

1

11

Institutional allocations to real assets are below current targets …

Notes/Assumptions:1) Brookfield estimate

~$3 Trillion1 underweight

12

2008 2017 2030E

$52T2

$23T1

$100T3

Notes/Assumptions:1) Source: Willis Towers Watson Global Pension Assets Study, 2010; Preqin (in association with PwC) Sovereign Wealth Fund Report 2018 2) Source: Willis Towers Watson Global Pension Assets Study, 2018; Preqin (in association with PwC) Sovereign Wealth Fund Report 2018 3) Brookfield estimate

In addition, the universe of institutional capitalcontinues to grow

13

BondYields1

Target Real Asset

Yields3

Equity Yields2

1%-4%

6%-8%

7%-20%

Diversification

Less volatility

Predictable cash flows

Notes/Assumptions:1) Bloomberg as of June 30, 2018, U.S. 10-year treasury yield range over the past 10 years 2) Bloomberg as of June 30, 2018, total return of SPX, NASDAQ and DJI over the past 20 years, compounded with dividends reinvested3) Bloomberg as of June 30, 2018, real asset yield range is based on total returns earned by five publicly traded real asset managers over the past 10 years and the

S&P Real Asset Total Return Index

Why are investors choosing to invest their growing capital base in real assets?

Excess returns

14

POLLING QUESTION #1

What % of institutional investors plan on increasing allocations to alternative assets over the next 12 months?

a) >35%

b) 20-30%

c) <20%

15

A: According to a recent survey of over 100 institutional investors…

39%

Notes/Assumptions:Source: Coller Capital Global Private Equity Barometer – Summer 2018

plan to increase target allocations to alternative assetsover the next 12 months

16

Notes/Assumptions:1) Source: Coller Capital Global Private Equity Barometer – Summer 2018

Alternative Assets (Overall)

Private equity

Infrastructure

Real estate

29%

51%

27%

39%

4%

5%

5%

4%

Decrease Increase

% of respondents

17

We still believe target allocations will reach 40% in the long term and may be higher

Notes/Assumptions:1) Source: Willis Towers Watson Global Pension Assets Study, 2018 2) Brookfield estimate

20171 2030220001

Real Assets/AlternativesEquity/Fixed Income

5%95%75%

60%25%

40%+

18

Potential capture size?

$100T 40% $40T=Capture SizeMarket Size1

xAllocation1

Notes/Assumptions:1) Brookfield estimate

19

To sum up the opportunity

Institutions are increasing allocations to real assets

Plans are currently under-allocated even at current numbers

The capital to come is many trillions

Experienced managers will benefit from this

20

POLLING QUESTION #2

What % of total in-year fundraising do the top 20 firms (by size) represent?

a) >50%

b) 30-50%

c) 20-30%

d) <20%

21

A: According to market analysis…

~38%

Notes/Assumptions:Source: McKinsey & Company – The rise and rise of private markets; McKinsey Global Private Markets Review 2018

of 2017 fundraising went to the top 20 firms

22

We have four distinct advantages

We have established track records

We operate in multiple asset classes

We offer large global funds

We deliver exceptional investor experience

These advantages position us well

23

Best-in-Class Investor Service

2

24

We strive to provide best-in-class investor servicecentered around three key areas

3Investor

Reporting

2Investor

Communications

1Investor

Interactions

25

We have expanded our core investor service team

10

3 3

9

25

17

13

6

11

47

North America -Institutional

North America -Private Wealth

EMEA APAC Total

Q4 2016 Q2 2018

+2

+7+10

+3

+22

26

… and have dedicated resources to service new channels

Wirehouses

13PRIVATE WEALTH

RELATIONSHIP MANAGERS1

Family OfficesRegistered Investment Advisors

Notes/Assumptions:1) As at June 30, 2018

27

We surpassed 500 institutional investors this year

2013 2018 2023

530

200

~1,000

21

Notes/Assumptions:1) As at June 30, 20132) As at June 30, 2018

+165%

+89%

5-Year Target

28

Our existing investors are expanding their relationships with us

From 20131… … to 20181

1.6 2.0

Average # commitments per investor

Average commitment size per investor

+25%

+28%

Notes/Assumptions:1) As at June 30

$90M $115M

29

We are seeing more re-investment …

>60% of capital raised in the last 12 months is from existing investors

Notes/Assumptions:1) Includes co-investments and direct investments

30

…..and crossover

80% of our top 20 investorsinvest in multiple asset classes

Notes/Assumptions:1) Includes co-investments and direct investments

31

We are focused on innovative and broad product offerings

to meet investor demand

32

Over the years, our product offering has grown…

Notes/Assumptions: 1) Sample of select private and public strategies

Years

+115

17

14

12

9

2

2

1

2-10

29

Owner and Operator

Private Equity

Real Estate Credit

Real Estate

Infrastructure

Infrastructure Credit

Open End

Europe Credit

Listed Issuers

Other Public Securities

1900 2018

Priv

ate

Mar

kets

Publ

ic

Mar

kets

33

… and we will continue to expand in three key ways

Flagship Funds

Expanding the size of our

traditional funds

New Strategies

Launching new strategies adjacent to

existing strategies

Expanding our distribution channels for existing products

New Channels

34

Notes/Assumptions:1) Amounts raised include Brookfield’s commitment2) Actual timing and amounts raised may vary materially and are subject to market conditions and other factors and risks that are set out in our Notice to Recipients on Slides 116 to 1183) Raised to date as at September 25, 20184) Has not yet had a first close

$14.0 Launch Q4 2018Infrastructure $2.7 $7.0

$9.0 $11B3Real Estate

$4.0 $7B4+$0.8Private Equity

$1.0 $4.4

$1.0

($ billions)Current2Previous Three Flagship Vintages

Flagship Funds1

The size of our flagship funds continue to grow

35

New Strategies

Notes/Assumptions:1) Source: McKinsey & Company – The rise and rise of private markets; McKinsey Global Private Markets Review 2018

1

PERPETUAL CORE CREDIT

2

CREDIT

Investors are looking for longer-term and lower risk investments1

36

We recently launched eight fundsunder these new strategies…

Perpetual Core

$2.3B1

4 Funds

Credit

$4.0B1

4 Funds

Notes/Assumptions:1) Committed as at June 30, 2018, includes Brookfield commitment2) Brookfield estimate; includes future funds not yet raised. Actual timing and amounts raised may vary materially and are subject to market conditions and other factors and

risks that are set out in our Notice to Recipients on Slides 116 through 118

Current

Long-Term Target2 $60B2 $100B2

37

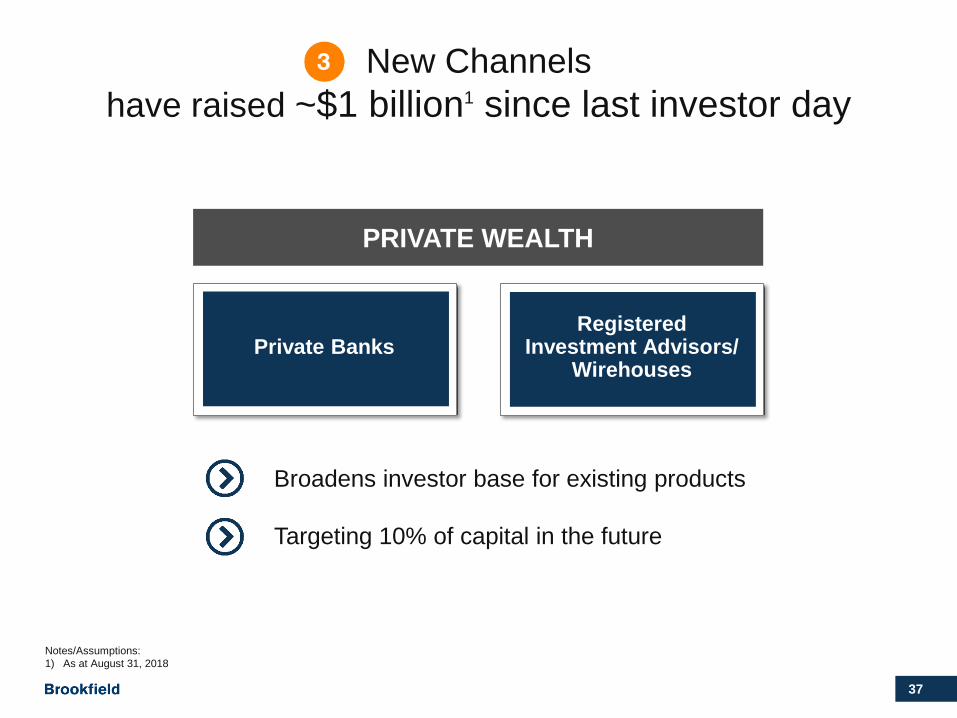

New Channels have raised ~$1 billion1 since last investor day

Broadens investor base for existing products

Targeting 10% of capital in the future

Private BanksRegistered

Investment Advisors/ Wirehouses

PRIVATE WEALTH

Notes/Assumptions:1) As at August 31, 2018

38

Notes/Assumptions:1) Source: Capgemini Financial Services Analysis, 20182) Brookfield estimate; includes future funds not yet raised. Actual timing and amounts raised may vary materially and are subject to market conditions and other factors

and risks that are set out in our Notice to Recipients on Slides 116 through 118

2008 2017 2030

$70T1

$130T2

Retail capital growth is substantial…

$32T1

39

Identifying Great Investment Opportunities

3

40

Investing in real assets globally requires casting a wide net

41

Our large scale capital provides us with a competitive advantage …

Less competition for large transactions

42

We will always find a home for attractive investments

Private Funds

Co-investment

Listed Issuer

BAM

43

The assets we acquire vary but our investment approach is always the same

Acquire high-quality

assets

On a value basis

Enhance value through

operating expertise

44

We continue to find excellent opportunities to deploy capital globally,

leveraging our operating expertise

45

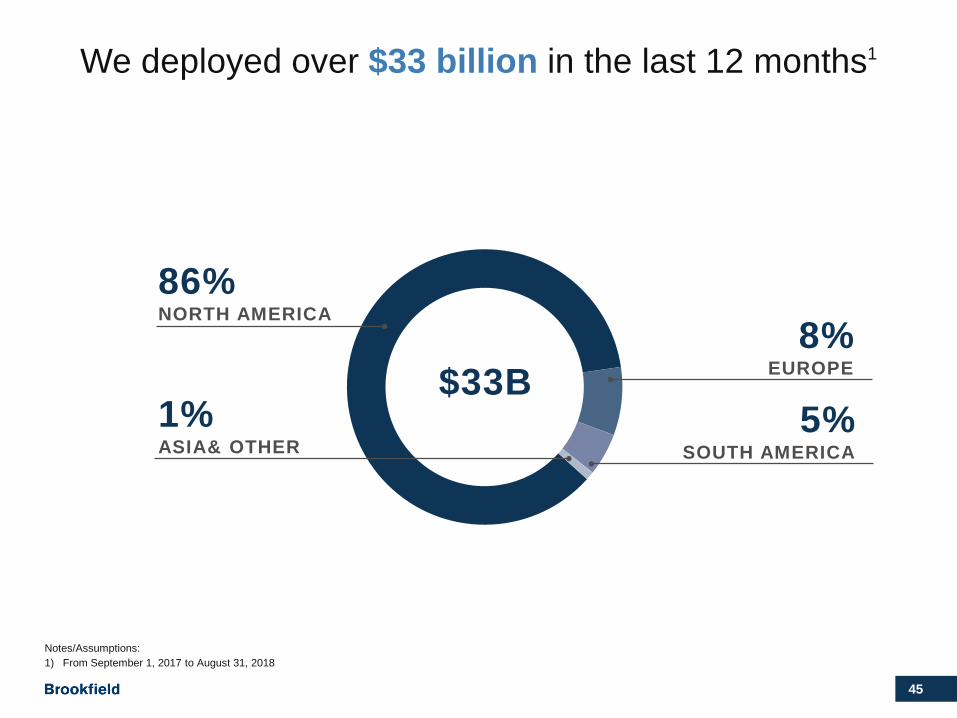

We deployed over $33 billion in the last 12 months1

5%SOUTH AMERICA

86%NORTH AMERICA

8%EUROPE

1% ASIA& OTHER

$33B

Notes/Assumptions:1) From September 1, 2017 to August 31, 2018

46

TerraForm Power and TerraForm Global

$1.5 billionLARGE SCALE CAPITAL

North & SouthAmerica and AsiaGLOBAL REACH

Renewable TeamOPERATING CAPABILITIES

2017 – Q4

47

Westinghouse Electric Corporation

$4 billionLARGE SCALE CAPITAL

U.S., Europe and AsiaGLOBAL REACH

Private Equity TeamOPERATING CAPABILITIES

2018 – Q3

48

Enercare

$3.3 billionLARGE SCALE CAPITAL

Canada and the U.S.GLOBAL REACH

Infrastructure TeamOPERATING CAPABILITIES

2018 – Q41

Notes/Assumptions:1) Transaction expected to close in Q4 2018

49

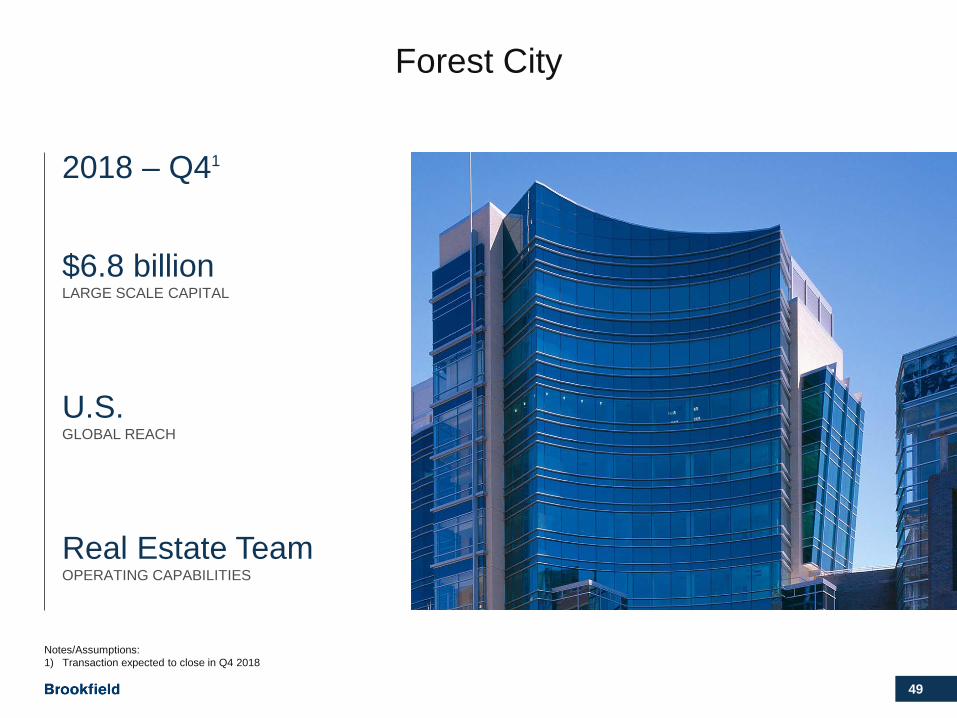

$6.8 billionLARGE SCALE CAPITAL

U.S.GLOBAL REACH

Real Estate TeamOPERATING CAPABILITIES

Forest City

2018 – Q41

Notes/Assumptions:1) Transaction expected to close in Q4 2018

50

Enbridge assets

$3.3 billionLARGE SCALE CAPITAL

CanadaGLOBAL REACH

Infrastructure TeamOPERATING CAPABILITIES

2019 – H11

Notes/Assumptions:1) Transaction expected to close in H1 2019

51

To sum up …

52

We want to leave you with five important points

Our franchise is still growing rapidly

We are well positioned to capture a larger piece of a growing market

We continue to deploy capital in high-quality real assets

Excellence in customer service is critical to success

We are structured for growth

53

Focusing on Our People and Culture | Lori Pearson

4

54

Maintaining our culture as we continue to grow supports value creation

Long-term Focus

Alignment of Interests Collaboration

PeopleVALUE

FOR SHAREHOLDERSAND INVESTORS

Operating Philosophy =+

55

Attract – Develop – Align

The Goal: achievement of potential

Compensate with a focus on alignment

Compensation

5

Provide them with stretch roles

Opportunities

4

Exposure

Operate a flat structure to provide exposure to

leadership

3

Develop

Succession planning effectively starting

on day one

2

Hire Right

Focus on people who can grow with the

organization

1

56

We hire people who have potential and the attributesof a Brookfield leader …

1

ENTREPRENEURIAL

2

COLLABORATIVE

3

DISCIPLINED

57

Recruit from within

Reinforces culture and knowledge sharing

Business Group Region Region

BusinessGroup

PortfolioCompanies

Business Group Region

Function Function

58

Our compensation strategies reinforce alignment

Emphasis on long-term compensation

All management receives some BAM equity based compensation

Management owns 20% of Brookfield

59

We have built an experienced and deep management team

60

Real Estate

Renewable Power Infrastructure Private

Equity

Public Securities

GroupCorporate

28 13 23 21 17 22

The Senior Executive Team has an average tenure of18 years working together

124 Managing Partners and Managing Directorsacross our geographies and business groups

61

INDIVIDUAL EXCELLENCEOPERATING PHILOSOPHY

Long-termfocus

To summarize…

Alignment of interests

Flat structure

Collaborative

Entrepreneurial

Disciplined

Brookfield culture

62

Financial Review| Brian Lawson

63

Agenda

Carried Interest

Balance Sheet Resilience

Value Creation

3

1

2

Financial Profile4

64

Our business is…

Straightforward Transparent Resilient Growing

65

Value Creation

1

66

Value creation at Brookfieldcomes from two primary sources

Invested Capital

BAM VALUE

Asset Manager

• Fee related earnings• Carried interest

• Value appreciation• Cash distributions

67

Our value creation process is straightforward and transparent

Raise Capital

Invest

Enhance Returns

Monetize

Business Cycle BAM Value Drivers

3

2

4

1

Base Fees

Performance Income1

Invested Capital Returns

Notes/Assumptions:1) Performance income includes incentive distributions, performance fees and carried interest

68

The sum of the parts is ~$56 billion…

Notes/Assumptions:1) Information presented is illustrative only. Actual results may vary materially and are subject to market conditions and other factors and risks that are set out in our Notice to

Recipients on Slides 116 through 118. Assumes a 60% margin on annualized fee revenues and a 70% margin on gross target carried interest. Reflects Brookfield’s estimates of appropriate multiples applied to fee related earnings and carried interest in the alternative asset management industry based on, among other things, industry reports. These multiples are used to measure performance for business planning purposes

2) Annualized as at June 30, 20183) Represents blended value, which is the quoted value of listed investments and IFRS value of unlisted investments, subject to two adjustments. First, we reflect BPY at its

IFRS value as we believe that this best reflects the fair value of the underlying properties. Second, we reflect Brookfield Residential at its privatization value

Plan Value1

AS AT JUNE 30($ millions) Multiple1 Ann.2 2018 2017

Asset manager

Annualized fee related earnings 20x $ 861 $ 17,220 $ 15,480

Net target carried interest 10x 808 8,080 6,020

25,300 21,500

Invested capital3 31,122 29,413

Total $ 56,422 $ 50,913

$6B

69

…which means BAM is trading at a 25% discount

($ millions) Total Per Share3

Asset manager plus invested capital (plan value)1,2 $ 56,422 $ 56.21

Implied equity market capitalization4 42,477 42.32

Discount to plan value $ 13,945 25%

Notes/Assumptions:1) As at June 30, 2018. Information presented is illustrative only. Actual results may vary materially and are subject to market conditions and other factors and risks that are set

out in our Notice to Recipients on Slides 116 through 1182) Illustrative stock price analysis is not intended to forecast or predict future events, but rather to provide information utilized by Brookfield in measuring performance for

business planning purposes, based on the specific assumptions and other factors described herein and in our Notice to Recipients on Slides 116 through 118. Actual results and share price performance may differ materially and are subject to market conditions

3) Per share amount calculated using total diluted shares as at June 30, 20184) Based on September 14, 2018 public pricing

70

Our activities add value in other ways….

High-quality critical assets and services

Positive contributionto communities

and employee base

Protect financial future for investors

1 2 3

71

We put a high priority on ESG principles

Consistent with owning and operating long-term sustainable assets

Important to our investors, employees and other stakeholders

72

ESG in action

Built into our investment approval process

One of world’s largest pure-play renewable energy portfolios

90% of our core office portfolio is green building certified

90% reduction in energy usage from our infrastructure district energy business

73

Balance Sheet Resilience

2

74

Maintaining a resilient balance sheet is a core part of our strategy

Strong liquidity

• $11 billion of core liquidity• $22 billion of dry powder

Notes/Assumptions:1) As at and annualized June 30, 2018

Non-recourse asset level debt

• Non-recourse, limited cross-collateralization or parental guarantees

• Duration matching with the underlying assets

Stable capital structure

• Long-term debt, perpetual shares • Investment grade model with limited

covenants• Self-sufficient listed entities

Strong cash flow generation

• $1.8 billion annual free cash flow• Contractual fee revenues• Stable distributions

75

Our net invested capital totals $31 billion

Notes/Assumptions:1) Quoted amounts based on June 29, 2018 public pricing2) Represents the quoted value of listed investments and IFRS value of unlisted investments as at June 30, 2018, subject to two adjustments. First, we reflect BPY at its IFRS value

as we believe that this best reflects the fair value of the underlying properties. Second, we reflect Brookfield Residential at its privatization value3) Calculated as multiplying units held at June 30, 2018 by distributions per unit, except for distributed cash flow on our financial assets which is estimated to be an 8% total return on

the weighted average balance of the last four quarters4) Includes other listed investments and financial assets. Financial assets cash flow estimated 8% annualized total return on the weighted average balance over the last four quarters.

As at June 30, 2018, the financial assets balance was $3.4 billion

Our invested capital is transparent, flexible and generates substantial cash flow

AS AT JUNE 30($ millions) Quoted1 IFRS Blended2

Distributed Cash Flow3

BPY $ 10,547 $ 16,907 $ 16,907 $ 691

BEP 5,661 3,801 5,661 369

BIP 4,519 1,920 4,519 221

BBU 3,362 1,921 3,362 22

Other listed4 5,536 5,483 5,536 281

Total listed investments $ 29,625 30,032 35,985 $ 1,584

Unlisted investments 4,463 5,585

Corporate capitalization and working capital (10,448) (10,448)

Net invested capital $ 24,047 $ 31,122

76

Our capital structure is resilientand long term in nature

$56B Common equity (at plan value)

$6BLong-term investment

grade debt (10-year average term)

$4BPerpetual preferred

shares

Notes/Assumptions:1) As at June 30, 2018

77

We generate over $1.8 billion of cash available fordistribution / reinvestment on an annualized basis,

with no carried interest

AS AT JUNE 30($ millions) 20181

Fee related earnings $ 861

Distributions from listed investments 1,584

2,445

Corporate activities

Corporate costs, cash taxes and other (156)

Corporate interest expense (320)

Preferred share dividends (152)

Cash available for distribution / reinvestment $ 1,817

Notes/Assumptions:1) Annualized

78

… and distribute ~ 30% to shareholders

AS AT JUNE 30($ millions) 20181

Cash available for distribution / reinvestment $ 1,817

Common share dividends (576)

Cash available for distribution / reinvestment, net $ 1,241

Percent distributed to shareholders 32%

Notes/Assumptions:1) Annualized

79

How are we using this cash to enhance shareholder return?

Participate in capital raises by our listed partnerships

Seed new investment strategies

Help facilitate large fund transactions

BAM share repurchases, which have been a lower priority in recent years

80

Carried Interest

3

81

How we measure carried interest

The carried interest we expect to earn on

third-party capital, assuming the fund achieves the target

return, annualized on a straight-line basis

EarningsPotential

Carried interest generated and based on fund

performance to date, assuming funds are

liquidated at current values

CurrentPerformance

Carried interest earned, excluding amounts subject

to clawback; basis for financial statement and

FFO recognition

Final Results

Target Carried Interest Realized Carried InterestUnrealized Carried Interest

1 2 3

82

Carried interest profile for a typical fund

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10Target carry Generated carry Realized carry

Notes/Assumptions:1) Illustrative of carried interest generated and realized over the 10-year life of a fund

83

Common carry misconception

Carry is earned on total profits provided that the preferred return is met

Carry is earned only on profit above the preferred return

Misconception Fact

84

Carry is earned on total fund profits

Opportunistic

Gross target return 20.0%

Base fee (2.0)%

Total fund profit 18.0%

Carry at 20% of total fund profit1,2 3.6%

Return to investor 14.4%

Typical preferred return 8%

Notes/Assumptions:1) Carried interest is generated once a private fund exceeds its preferred return. It will typically go through a catch-up period until the manager and limited partner (LP)

are earning carry at their respective percentages2) Average carried interest rate on opportunistic funds

85

The majority of our funds are tracking tomeet or exceed their target returns1

AS AT JUNE 30, 2018($ millions) Vintage2 Total CEC

Unrealized Carried Interest

GrossIRR3,4,5

Target Gross

IRR5

Opportunistic 2006 – 2018 $ 21,692 $ 1,655 23% – 28% 20%

Value add 2008 – 2016 16,685 715 15% 13% – 15%

Credit and core plus 2005 – 2018 8,483 157 13% 12% – 15%

Total $ 46,860 $ 2,527

Notes/Assumptions:1) See Q2 2018 Supplemental Information for further disaggregation by investment strategy 2) Year of final close3) On existing carry eligible funds, excluding open-ended funds and funds categorized as “Other” in the Supplemental Information 4) Unrealized fund returns reflected. The actual realized returns on current unrealized investments may vary materially and are subject to market conditions and other factors and risks

that are set out in our Notice to Recipients on Slides 116 to 1185) Gross IRR reflects performance before fund expenses, management fees (or equivalent fees) and carried interest

Which means they are well over the preferred return and will earn carry on each dollar of profit

86

In the last twelve months, we generated $1 billion of net carried interest, exceeding our target of $808 million

($ millions) 2018 2017

Carry eligible capital1 $ 46,860 $ 40,426

Invested 25,769 22,901

Uncalled fund commitments 21,091 17,525

Target carry, net1,2 808 602

Generated carry, net3 1,007 372

Notes/Assumptions:1) As at June 302) Assumes 70% margin on gross target carried interest3) Last twelve months ended June 30

87

Our generation expectations have grown and shifted forward since last year…

$0.0

$2.0

$4.0

$6.0

$8.0

$10.0

$12.0

2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027

Generated - 2017 IR Day Generated - 2018 IR Day

($ billions)

Existing Funds Only1

Notes/Assumptions:1) As at June 30. Information presented, including gross carried interest on existing funds, is illustrative only. Actual results may vary materially and are subject to market

conditions and other factors and risks that are set out in our Notice to Recipients on Slides 116 through 118

2017 IR Day

Generated

Generated

2018 IR Day

88

…and realizations are now expected to be $10 billion

$0.0

$2.0

$4.0

$6.0

$8.0

$10.0

$12.0

2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027

Realized - 2018 IR Day

($ billions)

Existing Funds Only1

2018 IR Day

Realized

Notes/Assumptions:1) As at June 30. Information presented, including gross carried interest on existing funds, is illustrative only. Actual results may vary materially and are subject to market

conditions and other factors and risks that are set out in our Notice to Recipients on Slides 116 through 118

89

On an annualized basis realizations should look like this…

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

$3.5

$4.0

2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027

Realized - Existing Funds

($ billions)

30% 70%

Notes/Assumptions:1) As at June 30. Information presented, including gross carried interest on existing funds, is illustrative only. Actual results may vary materially and are subject to market

conditions and other factors and risks that are set out in our Notice to Recipients on Slides 116 through 118

90

… and will be supplemented by carry on future funds

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

$3.5

$4.0

2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027

Generated - Existing Funds Generated - Future Funds Realized - Existing Funds Realized - Future Funds

($ billions)

Notes/Assumptions:1) As at June 30. Information presented, including gross carried interest on existing funds and future funds, is illustrative only. Actual results may vary materially and are subject

to market conditions and other factors and risks that are set out in our Notice to Recipients on Slides 116 through 118

91

How do we value this carry?

92

Notes/Assumptions:1) Information presented is illustrative only. Actual results may vary materially and are subject to market conditions and other factors and risks that are set

out in our Notice to Recipients on Slides 116 through 118. Assumes a 70% margin on gross target carried interest. Reflects Brookfield’s estimates of an appropriate multiple applied to carried interest in the alternative asset management industry based on, among other things, industry reports. This multiple is used to measure performance for business planning purposes

Expect to generate net target carry of $808 millionif we meet target returns on existing funds

We value carry as a multiple of net target carry

10Multiple1

$8BValue created1

$808MNet target carry

93

This $8 billion of value is supported by our DCF model1

$4.3B $8.0B

Terminal Value

$3.7B

Existing Funds

Notes/Assumptions:1) To value carried interest we use discounted cash flow values for expected carried interest assuming gross target returns, before fund expenses, management fees

(or equivalent fees) and carried interest of 20% for opportunistic funds and 13% for value add, credit and core plus funds are achieved. We apply a terminal multiple of 5x on expected carried interest at the end of 10 years to account for future funds. The aggregate amount is then discounted at 10% and we assume a 70% margin

94

Net terminal value represents value of future funds1

Notes/Assumptions:1) Net terminal value is the estimated value of carried interest on future funds. It is calculated based on a range of gross target returns implying a range of future carried interest

to which we then apply an assumed 5x multiple to. This value is then discounted using a range of discount rates. Net terminal value is presented on a net basis assuming a 70% margin

2) Gross target return reflects performance before fund expenses, management fees (or equivalent fees) and carried interest

Our net terminal value of carried interest is $4.3 billion

Gross Target Return2

18% 19% 20% 21% 22% OpportunisticAS AT JUNE 30, 2018($ milions) 11% 12% 13% 14% 15% Value Add, Credit & Core Plus

Dis

coun

t Rat

e 8% 3,700 4,600 5,100 5,700 6,200

9% 3,400 4,200 4,700 5,200 5,700

10% 3,100 3,900 4,300 4,800 5,200

11% 2,800 3,600 3,900 4,400 4,800

12% 2,600 3,300 3,600 4,000 4,400

95

Takeaways

Carry is earned on every dollar of profits, as long as the preferred return is met

We value our carry at $8 billion, net of costs, discounted

Our carry is growing rapidly

96

Financial Profile

4

97

Five years ago we projected where we could be in 2018…

98

2013 2018P 2018

Fee related earnings1($ millions)

$ 302 $ 675 $ 861

Target carried interest, net2($ millions)

$ 263 $ 427 $ 808

We surpassed our growth projections

Notes/Assumptions:1) Annualized as at June 302) As at June 30

99

2013 2018P 2018

Fee bearing capital1($ billions)

$ 78 $ 126 $ 129

Listed partnerships 31 49 56

Private funds 29 47 57

Public securities2 18 30 16

Strong private fund inflows offset the saleof lower margin public securities businesses

Notes/Assumptions:1) As at June 30 2) Within the Public Securities Group, we sold a portion of our fixed income business in April 2014 and sold our securitized credit business in June 2016

100

Looking ahead…

101

Private fund fee bearing capital should more than double to $121 billion

$57B1

Outflows

Flagship Funds 2019 - 2021

Flagship Funds 2021 - 2023

Credit, Core & Other

$121B

Notes/Assumptions:1) Opening private fund fee bearing capital as at June 30, 20182) Information presented, including growth in fee bearing capital over the period, is illustrative only. Actual results may vary materially and are subject to market

conditions and other factors and risks that are set out in our Notice to Recipients on Slides 116 through 118

16%CAGR

Private Funds – Fee Bearing Capital($ billions)

102

and listed partnerships’ capitalizationshould increase to over $100 billion

Notes/Assumptions:1) Opening listed partnership fee bearing capital as at June 30, 20182) Information presented, including distribution growth, market valuation and issuances relating to listed partnerships, is illustrative only. Actual results may vary materially and are

subject to market conditions and other factors and risks that are set out in our Notice to Recipients on Slides 116 through 118

$56B1

$101B

Distribution growth (BEP, BIP, TERP)

Market value growth (BPY, BBU)

Issuances

Listed Partnership – Fee Bearing Capital($ billions)

13%CAGR

103

AS AT JUNE 30($ billions) 2018 ~5 Years1

Listed partnership $ 56 $ 101

Private funds 57 121

Public securities 16 23

Fee bearing capital $ 129 $ 245

In aggregate, we expect to increase our fee bearing capital to $245 billion in the next five years

+14%CAGR

Notes/Assumptions:1) Information presented, including growth in fee bearing capital over the period, is illustrative only. Actual results may vary materially and are subject to market conditions and

other factors and risks that are set out in our Notice to Recipients on Slides 116 through 118

104

AS AT JUNE 30($ millions) 20181 ~5 Years2

Base fees $ 1,153 $ 2,500

IDRs 198 550

Other fees 84 150

Fee revenues 1,435 3,200

Direct costs (574) (1,280)

Fee related earnings $ 861 $ 1,920

The increase in fee bearing capital should generate strong growth in fee related earnings

+18%CAGR

Notes/Assumptions:1) Annualized as at June 302) Information presented, including growth in fee related earnings, is illustrative only. Actual results may vary materially and are subject to market conditions and other factors

and risks that are set out in our Notice to Recipients on Slides 116 through 118

105

AS AT AND FOR THE LTM ENDED JUNE 30($ millions) 2018 ~5 Years

Carry eligible capital $ 46,860 $ 111,000

Generated carry, gross1 $ 1,429 $ 2,500

Generated carry, net1 $ 1,007 $ 1,750

And increase our potential to earn carried interest

19%

12%

12%

Notes/Assumptions:1) Information presented, including gross and net generated carried interest on existing and future funds, is illustrative only. Actual results may vary materially and are subject to

market conditions and other factors and risks that are set out in our Notice to Recipients on Slides 116 through 118

106

Growing cash flows significantly increase our invested capital

Notes/Assumptions:1) Opening “Blended” invested capital value as at June 30, 20182) Information presented, including distribution growth, market valuation and issuances relating to listed partnerships, is illustrative only. Actual results may vary materially and are

subject to market conditions and other factors and risks that are set out in our Notice to Recipients on Slides 116 through 118 3) Cash retained includes fee related earnings, invested capital cash flow and dispositions of directly held assets. Accumulated balances are reinvested at 8%4) Capitalization and dividends assumes a constant capitalization level and 7% annual growth in BAM dividends

Invested Capital($ billions)

$42B1

$66B

Capitalization and dividends4

Cash retained –distributions from invested capital3

Cash retained –fee related earnings3Value

appreciation (BPY, BBU)2Distribution

increase (BEP, BIP)2

2018 ~5 years

46

8

13 -7

107

Putting it all together

108

Plan value results in $118 per shareover the next five years…

Notes/Assumptions:1) Information presented is illustrative only. Actual results may vary materially and are subject to market conditions and other

factors and risks that are set out in our Notice to Recipients on Slides 116 through 118. Assumes a 60% margin on fee related revenues and a 70% margin on gross carried interest

2) Illustrative stock price analysis is not intended to forecast or predict future events, but rather to provide information utilized by Brookfield in measuring performance for business planning purposes, based on the specific assumptions and other factors described herein and in our Notice to Recipients on Slides 116 through 118. Actual results and share price performance may differ materially and are subject to market conditions

3) Per share amount calculated using total diluted shares as at June 30, 20184) Includes dividends; total return calculated as compared to public pricing ($42.32 per share as at September 14, 2018)

~5 Years Multiple ~5 Years ($ millions) ($ billions, except

per share amounts)

Asset managerFee related earnings1 $ 1,920 20x $ 38

Generated carried interest, net1 1,750 10x 18

Accumulated carried interest, net 7

63

Asset ownerInvested capital 66

Leverage (10)

56

Total plan value $ 119Plan value per share2,3 $ 118

24%Total

Return4

109

Notes/Assumptions:1) All figures on a per share basis. Calculated using total diluted shares as at June 30, 20182) Current discount to plan value per Slide 693) Information presented, including (i) distribution growth, (ii) market valuation, (iii) issuances relating to listed partnerships, (iv) future fundraising, (v) fee related earnings and (vi)

carried interest estimates, is illustrative only. Actual results may vary materially and are subject to market conditions and other factors and risks that are set out in our Notice to Recipients on Slides 116 through 118

4) Cash retained includes fee related earnings, invested capital cash flow and dispositions of directly held assets. Accumulated balances are reinvested at 8%5) Illustrative stock price analysis is not intended to forecast or predict future events, but rather to provide information utilized by Brookfield in measuring performance for business

planning purposes, based on the specific assumptions and other factors described herein and in our Notice to Recipients on Slides 116 through 118. Actual results and share price performance may differ materially and are subject to market conditions

$1185Cash retained4

Discount to plan value2

…driven by fundraising and investing

Value creation –invested capital3

2018 Market Price

~5 years

Value creation –asset manager3

$42 14

10

31

21

24%Total

Return

110

($ millions) ~5 Years

Fee related earnings1 $ 1,920

Distributions from listed investments2 2,750

Corporate activities3

Corporate costs, cash taxes and other (200)

Corporate interest expense (320)

Preferred share dividends (150)

Cash available for distribution / reinvestment $ 4,000

The cash available for distribution, before carried interest,should more than double in ~5 years

Notes/Assumptions:1) Information presented, including growth in fee related earnings, is illustrative only. Actual results may vary materially and are subject to market conditions and other factors

and risks that are set out in our Notice to Recipients on Slides 116 through 118 2) Distributions from listed investments assumes dividend growth at mid-point of target distribution growth rates3) Corporate activities based on current capitalization per plan and growth in corporate costs of 5%

111

And including realized carried interest, distributable cash should increase to over $5 billion in ~5 years

2018 2019 2020 2021 2022 2023

Cash available for distribution Realized carried interest, net

$4.0$3.3

$2.9$2.5

$1.9

$5.1

1.82.3

2.63.1

3.64.0

Notes/Assumptions:1) Information presented, including net realized carried interest on existing funds, is illustrative only. Actual results may vary materially and are subject to market

conditions and other factors and risks that are set out in our Notice to Recipients on Slides 116 through 118

($ billions)

112

Looking out 10 years…

($ millions)Cumulative~10 Years1

Net cash from:

Fee related earnings $ 20,000

Net invested capital 25,000

Realized carried interest, net 15,000

$ 60,000

Notes/Assumptions:1) Per Brookfield plan, consistent with 5-year plan assumptions

113

This gives us flexibility toreturn substantial capital to shareholders

($ millions)Cumulative~10 Years1

Potential cash generation $ 60,000

Cash investment into listed partnerships (10,000)

Return of capital through dividends2 (10,000)

Available for share repurchases $ 40,000

Notes/Assumptions:1) Per Brookfield plan, consistent with 5-year plan assumptions2) Based on BAM annual dividend growth of 7%

114

We want to leave you with four important points

Our balance sheet is resilient

We are generating almost $2 billion, heading to over $5 billion of annual cash flows

Carry is growing rapidly and is very meaningful

These together should generate $60 billion of cash flow over the next 10 years with few identified uses

115

Q & A

116

Notice to RecipientsBrookfield is not making any offer or invitation of any kind by communication of this document to the recipient and under no circumstances is it to be construed as aprospectus or an advertisement.

Except where otherwise indicated herein, the information provided herein is based on matters as they exist as of the date of preparation and not as of any futuredate, is subject to change, and will not be updated or otherwise revised to reflect information that subsequently becomes available or circumstances existing orchanges occurring after the date hereof.

Unless otherwise noted, all references to “$” or “Dollars” are to U.S. Dollars.

CAUTIONARY STATEMENTS REGARDING FORWARD-LOOKING STATEMENTS AND INFORMATION

This presentation contains “forward-looking information” within the meaning of Canadian and United States securities laws, including United States Private SecuritiesLitigation Reform Act of 1995. Forward-looking statements include statements that are predictive in nature, depend upon or refer to future events or conditions, andinclude statements regarding our and our subsidiaries’ operations, business, financial condition, expected financial results, performance, prospects, opportunities,priorities, targets, goals, ongoing objectives, strategies and outlook, as well as the outlook for North American and international economies for the current fiscal yearand subsequent periods, and include, but are not limited to, statements regarding our asset management. In some cases, forward-looking statements can beidentified by terms such as “expects,” “anticipates,” “plans,” “believes,” “estimates,” “seeks,” “intends,” “targets,” “projects,” “forecasts” or negative versions thereofand other similar expressions such as “Brookfield plan” or “Brookfield estimate,” or future or conditional verbs such as “may,” “will,” “should,” “would” and “could.”

Below are certain of the forward-looking statements that are contained in this presentation and a number of assumptions underlying them.

Where this presentation refers to “gross carried interest” or “carried interest,” carried interest for existing funds is based on June 30, 2018 carry eligible capital andcarried interest for future funds is based on Brookfield’s estimates of future fundraising as at June 30, 2018, as described below. In addition, this presentationassumes that existing and future funds meet their target gross return. Target gross returns are typically 20+% for opportunistic funds; 13% to 15% for value addfunds; 12% to 15% for credit and core plus funds. Fee terms vary by investment strategy (carried interest is approximately 15% to 20% subject to a preferred returnand catch-up) and may change over time. This presentation assumes that capital is deployed evenly over a four-year investment period and realized evenly overthree years of sales. The year in which such sales commence varies by investment strategy and ranges from year 6 to year 10.

Where this presentation refers to “future fundraising,” or “growth in fee bearing capital” we assume that flagship funds are raised every two to three years basedon historical fund series and non-flagship funds are raised annually within certain strategies, and in other strategies every two years. Fund series’ sizes remainconstant and consistent with target funds from period-to-period. This presentation also assumes that distributions are based on fund realizations evenly over threeyears of sales. The year in which such sales commence varies by investment strategy and ranges from year 6 to year 10.

References to “distribution, growth, market valuation, and issuances relating to listed partnerships,” include the following assumptions: (i) BIP, BEP, andTERP grow at a rate equal to the mid-point of their target distribution growth rate, assuming current yield; (ii) the market price to IFRS discount on BPY (see Slide 75)is eliminated; (iii) BBU share price grows at a 10% annual rate; and (iv) total listed partnership capitalization includes issuances related to debt and preferred equityfor BPY, BIP and BEP, based on a debt to total capitalization ratio of 20-30%.

Where this presentation refers to “fee related earnings,” fee related earnings from listed partnerships and private funds are based on fee bearing capital increasingin accordance with Slide 103. The listed partnership management fees for BPY, BEP and TERP are fixed fees on initial capitalization and an additional fee of 1.25%on the amount in excess of initial capitalization. Management fees for BIP and BBU are 1.25% of total capitalization. Fee terms for private funds vary by investmentstrategy (generally, within a range of approximately 1-2%). The incentive distribution rights of the listed partnerships are based on a mid-point of the applicable listedpartnership’s distribution growth rate as described above. Other fees include the BBU performance fee assuming a 10% BBU annual share price growth. Fee relatedearnings assumes a margin of 60%.

117

Notice to Recipients cont’d

Although we believe that our anticipated future results, performance or achievements expressed or implied by the forward-looking statements and information arebased upon reasonable assumptions and expectations, the reader should not place undue reliance on forward- looking statements and information because theyinvolve known and unknown risks, uncertainties and other factors, many of which are beyond our control, which may cause our and our subsidiaries’ actual results,performance or achievements to differ materially from anticipated future results, performance or achievements expressed or implied by such forward-lookingstatements and information.

Factors that could cause actual results (including, among other things, carried interest; future fundraising; growth in fee bearing capital; growth in distribution, marketvaluation, and issuances relating to listed partnerships; and fee revenues and earnings) to differ materially from those contemplated or implied by forward-lookingstatements include, but are not limited to: lower than target investment returns; the impact or unanticipated impact of general economic, political and market factorsin the countries in which we do business; the fact that our success depends on market demand for our products; the behavior of financial markets, includingfluctuations in interest rates and foreign exchanges rates; changes in inflation rates in North America and international markets; the performance of global equity andcapital markets and the availability of equity and debt financing and refinancing within these markets; strategic actions including dispositions; the competitive marketfor acquisitions and other growth opportunities; our ability to satisfy conditions precedent required to complete such acquisitions; our ability to effectively integrateacquisitions into existing operations and attain expected benefits; the outcome and timing of various regulatory, legal and contractual issues; changes inaccounting policies and methods used to report financial condition (including uncertainties associated with critical accounting assumptions and estimates); the effectof applying future accounting changes; business competition; operational and reputational risks; technological change; changes in government regulation andlegislation within the countries in which we operate; changes in tax laws; catastrophic events, such as earthquakes and hurricanes; the possible impact ofinternational conflicts and other developments including terrorist acts and cyberterrorism; and other risks and factors detailed from time to time in our documents filedwith the securities regulators in Canada and the United States.

We caution that the foregoing list of important factors that may affect future results is not exhaustive. When relying on our forward-looking statements, investors andothers should carefully consider the foregoing factors and other uncertainties and potential events. Except as required by law, we undertake no obligation to publiclyupdate or revise any forward-looking statements or information in this presentation, whether as a result of new information, future events or otherwise.

CAUTIONARY STATEMENT REGARDING INVESTMENT PERFORMANCE

Past performance is not necessarily indicative of future results and there can be no assurance that comparable results will be achieved, that an investment will besimilar to the historic investments presented herein (because of economic conditions, the availability of investment opportunities or otherwise), that targeted returns,diversification or asset allocations will be met or that an investment strategy or investment objectives will be achieved. Any information regarding prior investmentactivities and returns contained herein has not been calculated using generally accepted accounting principles and may not have been audited or verified by anauditor or any independent party. Unless otherwise indicated, internal rates of return (including targeted rates of return) are presented on a “gross” basis (i.e., theydo not reflect management fees (or equivalent fees), carried interest (or incentive allocation), taxes, transaction costs and other expenses to be borne by investors,which in the aggregate are expected to be substantial).

Any changes to assumptions could have a material impact on projections and actual returns. Actual returns on unrealized investments will depend on, among otherfactors, future operating results, the value of the assets and market conditions at the time of disposition, legal and contractual restrictions on transfer that may limitliquidity, any related transaction costs and the timing and manner of sale, all of which may differ from the assumptions and circumstances on which the valuationsused in the prior performance data contained herein are based. Accordingly, the actual realized returns on unrealized investments may differ materially from thereturns indicated herein.

118

Notice to Recipients cont’d

TARGET RETURNS

The target returns set forth herein are for illustrative and informational purposes only and have been presented based on various assumptions made by Brookfield inrelation to the investment strategies being pursued by the funds, any of which may prove to be incorrect. Target gross returns do not reflect fund expenses,management fees (or equivalent fees) and carried interest. Target net returns take into account these items. Due to various risks, uncertainties and changes(including changes in economic, operational, political or other circumstances) beyond Brookfield’s control, the actual performance of the funds could differ materiallyfrom the target returns set forth herein. In addition, industry experts may disagree with the assumptions used in presenting the target returns. No assurance,representation or warranty is made by any person that the target returns will be achieved, and undue reliance should not be put on them. Prior performance is notindicative of future results and there can be no guarantee that the funds will achieve the target returns or be able to avoid losses.

CAUTIONARY STATEMENT REGARDING USE OF NON-IFRS MEASURES

This presentation contains references to financial metrics that are not calculated in accordance with, and do not have any standardized meaning prescribed by,International Financial Reporting Standards (“IFRS”). We believe such non-IFRS measures including, but not limited to, funds from operations (“FFO”) and investedcapital, are useful supplemental measures that may assist investors and others in assessing our financial performance and the financial performance of oursubsidiaries. As these non-IFRS measures are not generally accepted accounting measures under IFRS, references to FFO and invested capital, as examples, aretherefore unlikely to be comparable to similar measures presented by other issuers and entities. These non-IFRS measures have limitations as analytical tools. Theyshould not be considered as the sole measure of our performance and should not be considered in isolation from, or as a substitute for, analysis of our financialstatements prepared in accordance with IFRS. For a more fulsome discussion regarding our use of non-IFRS measures and their reconciliation to the most directlycomparable IFRS measures refer to our documents filed with the securities regulators in Canada and the United States.

OTHER CAUTIONARY STATEMENTS

Certain of the information contained herein is based on or derived from information provided by independent third-party sources. While Brookfield believes that suchinformation is accurate as of the date it was produced and that the sources from which such information has been obtained are reliable, Brookfield does notguarantee the accuracy or completeness of such information and has not independently verified such information or the assumptions on which such information isbased. This document is subject to the assumptions (if any) and notes contained herein.

The information in this document does not take into account your investment objectives, financial situation or particular needs and nothing contained herein shouldbe construed as legal, business or tax advice. Each prospective investor should consult its own attorney, business adviser and tax advisor as to legal, business, taxand related matters concerning the information contained herein.

Brookfield Asset Management

INVESTOR DAY

SEPTEMBER 26 , 2018