business sweden russia 2016 - business climate survey final report

TRANSCRIPT

CONFIDENTIAL

FOR INTERNAL USE WITHIN CLIENT COMPANY ONLY

BUSINESS

CLIMATE SURVEY

RUSSIA 2016

Andreas Giallourakis

Trade Commissioner Russia

I am glad to present this report on the business climate in Russia. We look back at a

dramatic 2015 with significant volatility, uncertainty, challenges, political turbulence and

few reasons for positive outlooks. The Rouble has had a dramatic year with sharp

changes. The oil price finished the year on a 10-year low. Most of you reading this report

are working with business in Russia. You all have your own impressions and opinions

about the current state and direction of the Russian economy.

What is presented in this report is an aggregated picture of the Russian market from the

point of view of the Swedish business community engaged in Russia. We often read

forecasts and reports based on statistics and macro indicators. I believe this report

constitutes in important complement in the decision-making process by offering insights

from those with boots on the ground.

There are currently more than 350 Swedish subsidiaries in Russia. Business Sweden has

been in Russia since 1994 and has in the meantime accumulated a substantial body of

knowledge about the Russian market. We engage in discussions with a multitude of

Swedish companies on a daily basis and advice on strategic issues concerning their

operations and approach to the market.

As a result of our experiences and interactions with the vast amount of Swedish

companies in Russia, we see the need for guidance and reliable input when deciding

upon matters concerning Russia. I hope you will gain new insights from this report and

that we can bring you some guidance in your decision-making processes.

BUSINESS SWEDEN 16 MAY 2016 2

Foreword

Method

Current status

Regulatory environment

Future plans

Conclusions and recommendations

Final Words

Appendix

4

5

9

14

17

23

24

BUSINESS SWEDEN 16 MAY, 2016 3

AGENDA

The survey was sent to 179 Swedish subsidiaries in Russia, representing all company

sizes and industries where Swedish companies are active. 103 participated in the

survey which implicates a response rate of 58 %. There are around 350 Swedish

subsidiaries on the Russian market. Some of the larger corporations have several

subsidiaries, many subsidiaries are holding companies and some real estate

companies have one subsidiary for each property. This renders it irrelevant to reach

out to all of them. Within the companies we reached to country managers, regional

managers and others in leading positions. The survey was open for the respondents

during 4 weeks in March 2016.

The survey took on a descriptive approach to identify major trends among Swedish

companies in Russia. The current state of business was covered in a number of

questions about internal factors such as turnover and other indicators. The companies

were asked to express their expectations of the near future to find out the current

sentiment on the development of the Russian business climate.

The companies were also asked to give their view on how external factors such as

politics, corruption and other societal factors affect their business in Russia. This year’s

survey was complemented with data from earlier years’ Business Climate Survey and,

where relevant by secondary sources.

BUSINESS SWEDEN 16 MAY 2016 4

METHOD

Response Rate

58%

103

respondents

GOOD COVERAGE AND RESPONSE

RATE IN SAMPLE

4

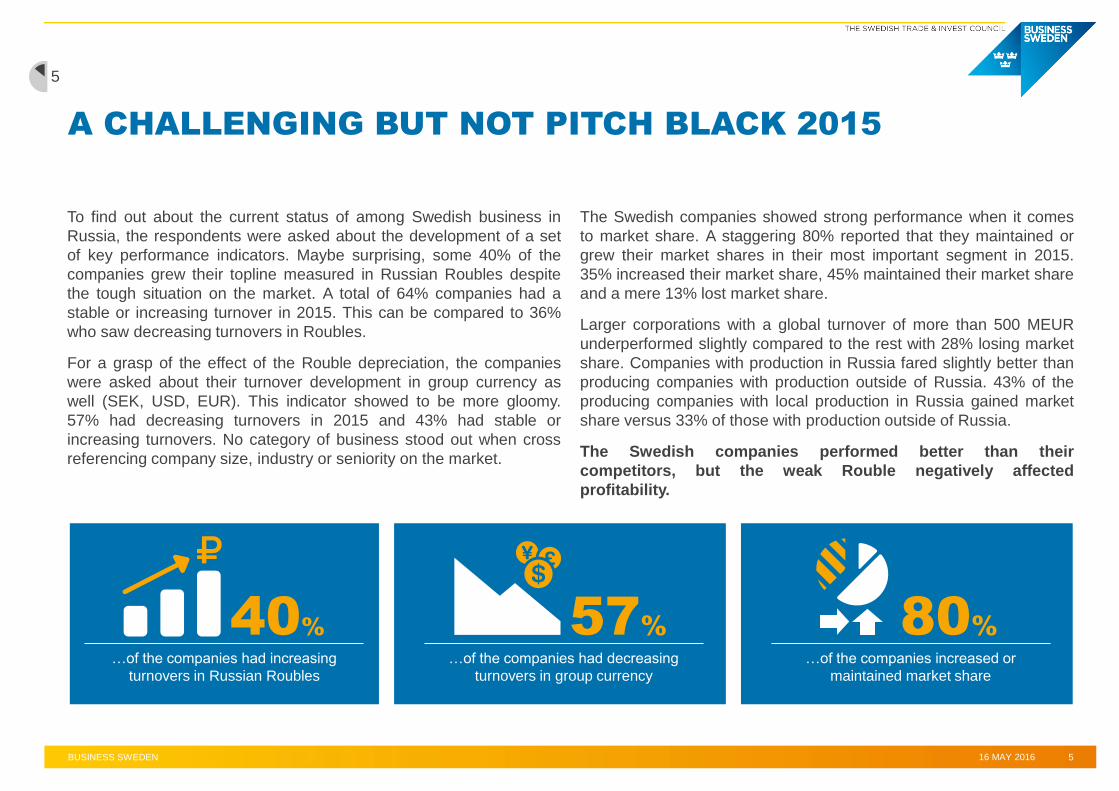

To find out about the current status of among Swedish business in

Russia, the respondents were asked about the development of a set

of key performance indicators. Maybe surprising, some 40% of the

companies grew their topline measured in Russian Roubles despite

the tough situation on the market. A total of 64% companies had a

stable or increasing turnover in 2015. This can be compared to 36%

who saw decreasing turnovers in Roubles.

For a grasp of the effect of the Rouble depreciation, the companies

were asked about their turnover development in group currency as

well (SEK, USD, EUR). This indicator showed to be more gloomy.

57% had decreasing turnovers in 2015 and 43% had stable or

increasing turnovers. No category of business stood out when cross

referencing company size, industry or seniority on the market.

The Swedish companies showed strong performance when it comes

to market share. A staggering 80% reported that they maintained or

grew their market shares in their most important segment in 2015.

35% increased their market share, 45% maintained their market share

and a mere 13% lost market share.

Larger corporations with a global turnover of more than 500 MEUR

underperformed slightly compared to the rest with 28% losing market

share. Companies with production in Russia fared slightly better than

producing companies with production outside of Russia. 43% of the

producing companies with local production in Russia gained market

share versus 33% of those with production outside of Russia.

The Swedish companies performed better than their

competitors, but the weak Rouble negatively affected

profitability.

BUSINESS SWEDEN 16 MAY 2016 5

A CHALLENGING BUT NOT PITCH BLACK 2015

40%

…of the companies had increasing

turnovers in Russian Roubles

57% 80%

…of the companies had decreasing

turnovers in group currency

…of the companies increased or

maintained market share

5

No one can have missed that the situation on the Russian market has been tough the

past two years. The official inflation landed on 12.9% for 2015. The Rouble’s

depreciation against the Swedish Krona and other foreign currencies hit importers.

Also producers who import components for assembly on the Russian market had to

fight high volatility. All this affected our Swedish companies as well. Many companies

had to either maintain prices, keep volumes but lose margins, or raise prices, loose

volumes and keep margins.

A majority, 55% of the companies raised their prices in 2015. This is considerably more

than in 2014 when 36% of our respondents raised prices. This previous cautiousness

is mainly the reason why many had to make harsher adjustments in 2015. 44%

maintained their prices in 2014 compared to 26% in 2015.

A smaller group of companies lowered their prices in 2015. 9% in 2015 and 11% in

2014. Broken down by industry, the companies connected to real-estate stands out

here. There is an over supply on the market of commercial and private properties and

market prices have been stable or even decreasing in local currency. The effect in

foreign currency is obviously even more negative. In the end this is positive for those

who rent and problematic for the companies letting property.

BUSINESS SWEDEN 16 MAY 2016 6

HOW ARE THE COMPANIES

DEALING WITH THE MARKET?

TOP LINE

55%

23%

13%

44%

4% 7% 9%

29% 26% 26%

8%

1%

10%

Raisedmorethan20%

Raisedby 0-20%

Nochange

Loweredby 0-20%

Loweredby more

than20%

I don’t know/not relevant

2014

2015

…of the companies raised prices in

2015

Company Pricing Policies 2014-2015

6

The companies have not only taken top-line action to counter the market. A lot is

happening on the cost side. Real wages are falling in Russia. For the first time since the

90’s real wages have decreased two years in a row. The purchasing power in Russia

diminishes and especially imported goods and travel abroad have become much more

expensive for the average wage worker.

Most companies have raised wages but less than inflation in 2015. Together with

unchanged wages, real wage decreases dominate with 86% of the respondents. The

same categories amounted to 71% in 2014. Only 10 % raised wages more than inflation in

comparison to 16% in 2014. The expectations for next year are mostly on further real

wage decreases. Nominal wage decreases are very rare and only occurred in one

company in 2015.

Staff decreased in 2015 both in total and with regards to foreign employees – expats. 38%

decreased their staff, almost twice as many as those who increased staff. Overall, larger

companies were overrepresented among those who cut staff and small and medium

companies led the way in staff hiring.

More expensive expats are being replaced by less expensive local talents. 16% of the

companies cut down on expats in 2015. Interviews with HR-related companies confirm

this observation. Large resources are spent to find and develop local managers to replace

foreign staff and management. This trend is most noticeable among the larger companies

where you also find the largest total presence of expats and the possibility to make such

adjustments.

The companies take decisive action both on top and bottom lines to counter the

tough situation on the market.

BUSINESS SWEDEN 16 MAY 2016 7

CUT OFF THE FINGER TO SAVE

THE HAND

BOTTOM LINE

86%

…of the companies lowered real wages

in 2015

38%

…of the companies cut down on staff in

2015

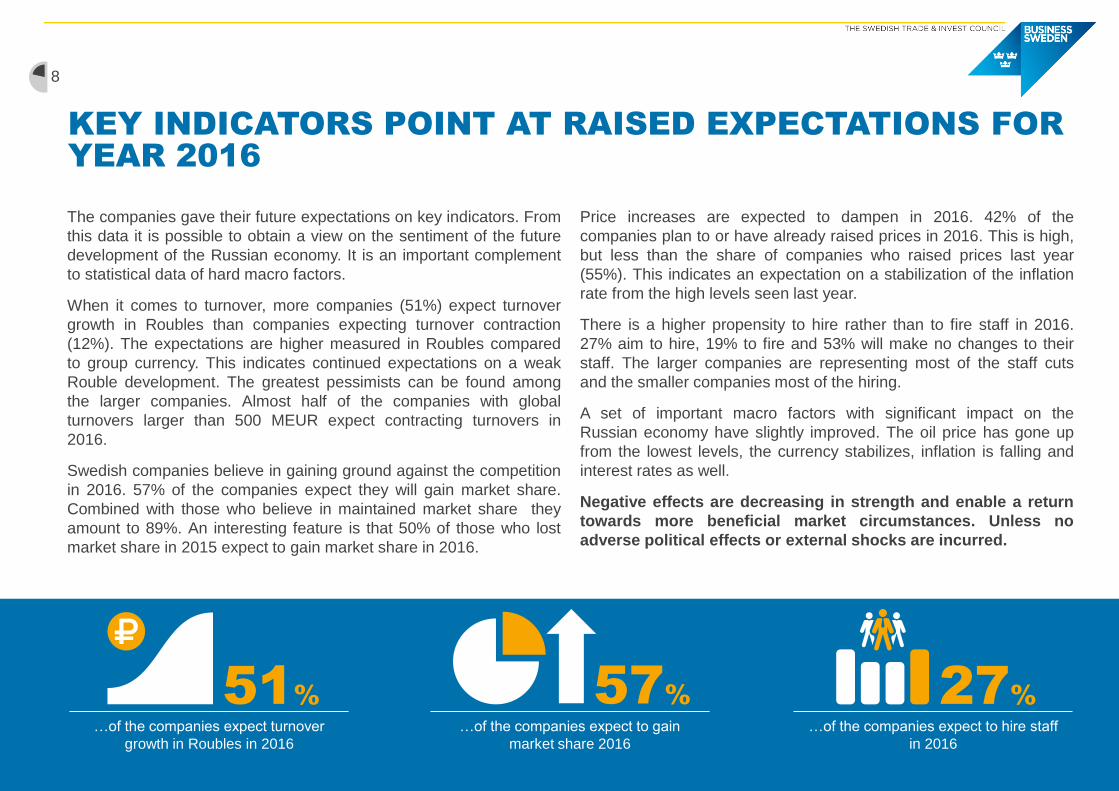

The companies gave their future expectations on key indicators. From

this data it is possible to obtain a view on the sentiment of the future

development of the Russian economy. It is an important complement

to statistical data of hard macro factors.

When it comes to turnover, more companies (51%) expect turnover

growth in Roubles than companies expecting turnover contraction

(12%). The expectations are higher measured in Roubles compared

to group currency. This indicates continued expectations on a weak

Rouble development. The greatest pessimists can be found among

the larger companies. Almost half of the companies with global

turnovers larger than 500 MEUR expect contracting turnovers in

2016.

Swedish companies believe in gaining ground against the competition

in 2016. 57% of the companies expect they will gain market share.

Combined with those who believe in maintained market share they

amount to 89%. An interesting feature is that 50% of those who lost

market share in 2015 expect to gain market share in 2016.

Price increases are expected to dampen in 2016. 42% of the

companies plan to or have already raised prices in 2016. This is high,

but less than the share of companies who raised prices last year

(55%). This indicates an expectation on a stabilization of the inflation

rate from the high levels seen last year.

There is a higher propensity to hire rather than to fire staff in 2016.

27% aim to hire, 19% to fire and 53% will make no changes to their

staff. The larger companies are representing most of the staff cuts

and the smaller companies most of the hiring.

A set of important macro factors with significant impact on the

Russian economy have slightly improved. The oil price has gone up

from the lowest levels, the currency stabilizes, inflation is falling and

interest rates as well.

Negative effects are decreasing in strength and enable a return

towards more beneficial market circumstances. Unless no

adverse political effects or external shocks are incurred.

BUSINESS SWEDEN 16 MAY 2016 8

KEY INDICATORS POINT AT RAISED EXPECTATIONS FOR

YEAR 2016

51%

…of the companies expect turnover

growth in Roubles in 2016

…of the companies expect to gain

market share 2016

57%

…of the companies expect to hire staff

in 2016

27%

8

Corruption is a frequent topic in discussions concerning business in Russia.

Transparency International ranks Russia at place number 119 out of 168 in their

corruption perception index in 2015.

The Swedish companies in the survey are not unaffected by corruption. The survey

shows that 9% of the companies have encountered corruption and criminal behavior

such as bribery and fraud in their business operations in 2015.

The most frequent area of such exposure is in connection to private external

counterparts where 8% indicate occurrence of activities such as kickbacks and bribes

among competitors to win orders.

Corruption in connection to authorities and public bodies is recognized by 7% of the

respondents. Examples given are blackmailing by tax authorities, questionable fire

inspections, harassment by traffic police.

Internal fraud is less frequent, but still 3% of the companies indicate cases of theft and

fraudulent behavior by own staff.

BUSINESS SWEDEN 16 MAY 2016 9

CORRUPTION CONTINUES

TO BE A PROBLEM

*IN THE MEANING OF CRIMINAL BEHAVIOR SUCH AS BRIBERY OR FRAUD

9%

…of the companies reported exposure

to some kind of corruption in 2015

7% 8% 3%

76% 74% 82%

18% 18% 15%

...public bodiessuch as customs

and otherauthorities

...privatecounterparts such

as customers,suppliers and

others

...internalcounterparts such

as employees

Exposure No exposure I don't know

Company Exposure to Corruption* in 2015 in

Connection With...

EXPOSURE

9

The general trend in corruption seems to be moving in a positive

direction. A larger share of companies (22%) noticing a decrease in

the extent of corruption the past 5 years, however this can be

compared to respondents perceiving an increase in the level of

corruption (16%). This tendency seems to be valid also for future

expectations, where 24% expect a decrease and 12% expect an

increase in the overall level of corruption in their field of business in

Russia.

Our estimation is that corruption remains a challenge in business in

Russia. However some positive tendencies can be spotted.

Court processes seem to be increasingly possible to win on

proper merits, also in processes against public representatives

Several high profile corruption cases against public figures have

caused officials and politicians to act more carefully

Business Sweden clearly opposes corrupt business behavior

and recommends to never engage in questionable business

setups. Beside the legal and ethical aspects, companies

engaging in corrupt activities take a large risk not only on the

local markets, but expose the brand and reputation to

considerable risks on a global scale.

BUSINESS SWEDEN 16 MAY 2016 10

RUSSIA HAS A LONG WAY TO GO, BUT IS MOVING

FORWARD WITH A TURTLE’S PACE

22%

36%

16%

25% 24%

33%

12%

31%

Decreased / Willdecrease

No change Increased / Willincrease

I don’t know

Development last 5 years

Expectation of coming 5 years

The development is going in the right direction but

It will take a long time to get significant results

Development and expectation of the Extent of

Corruption

10

BUSINESS SWEDEN 16 MAY 2016 11

THE POLITICAL TURBULENCE IS SHAPING THE RULES

OF THE GAME

The relations between Russia and EU, USA and other individual

countries have been tense since 2014. Earlier cooperation and

common agendas have been changed into conflict and political

standoffs.

Sanctions imposed by the EU and USA on Russia have limited the

possible areas of cooperation and trade in a number of fields.

41% of the companies in the survey have been affected negatively by

sanctions and embargoes. Commenting on what specific effects they

encountered, sanctions in the whole range of measures are found:

Sanctions related to Crimea

Sector specific sanctions such as the oil industry

Increased control of goods with dual use

Counterparts being on the sanctions lists

Lack of financing among counterparts

An interesting result of the survey is that 7% of the respondents claim

to have benefited by the sanctions regimes. They comment that

competitors have left the market, that the Russian government is

supporting their local activities.

The political risk in Russia is always a factor to take into account. This

has been accentuated over the past two years. However the direct

effects are not always negative for all players on the market.

Geopolitics is rocking the boat… …of the companies were negatively

affected by sanctions in 2015

…of the companies were positively

affected by the sanctions in 2015

41% 7%

11

The Russian government is actively pushing for shifting the domestic demand from

imported products to locally produced goods. New trade barriers have appeared that are

affecting foreign companies.

The import embargo on food products gives the most visible effect. Since 2014 dairy, meat,

fruit and vegetables are not permitted for imports from the EU and USA. This has a large

impact on specific companies in this sector where they have been compelled to either

establish local production or see the market go lost.

On a larger scale the import substitution activities have been concentrated in public

procurement. Where locally produced alternatives exist, companies offering foreign

products have been restricted in participating in public tenders. Domestic producers enjoy

a significant advantage in many spheres, not only when dealing with public counterparties,

but also where there is governmental financing or where there might be a public

counterpart in a second or third step away from the deal as such.

As an effect we see that a radically smaller share of the companies define B2G (business

to government) as their main line of business. The share of companies with government as

their most important customer group has decreased from 12% to 4% from last year’s

survey.

Legislation and regulations are being adapted to define and classify products based on

origin. Narrow and exact criteria are being developed, defining exactly what procedures

that have to be undertaken on Russian soil for goods to be recognized as locally produced.

This process is still ongoing and further development can be expected.

Protectionist measures demand localization of production for companies to keep

access to market

BUSINESS SWEDEN 16 MAY 2016 12

PUSH FOR LOCAL PRODUCTION IS

AFFECTING EXPORTERS

IMPORT

SUBSTITUTION

Protectionist moves raise market

thresholds for foreign companies

The share of companies with

government as their most important

customer group has dropped

12% 4%

2015

2016 B

2

G

BUSINESS SWEDEN 16 MAY 2016 13

INVESTMENTS ARE LAGGING, BUT SOME KEEP

STRENGTHENING THE LOCAL FACILITIES

For Russia as a whole, the level of investments is down radically the

past two years, especially in Foreign Direct Investments.

According to the Russian Central Bank, net flow of FDI into Russia

amounts to 52 MUSD in Q3 2015. This is a drastic difference with the

quarterly flows from about two years ago ranging between 8 700 –

11 800 MUSD.

Among the companies in the survey a third has local production, 19%

don’t produce at all and 48% don’t have local production in Russia.

Out of the companies with production in Russia 63% consider

investing more in it and only 1 company look at divesting the existing

production. Out of the producing companies, that don’t produce in

Russia, 1/5 consider localization of production within 3 years time.

The overall share of companies investing in their Russian operations

is down from 41% in 2014 to 31% in 2015. This number stays stable

in expectations on further investments in 2016

The most popular areas of investment is in:

Facilities and land

Production equipment and other machinery

IT infrastructure

Staff

A small share of the companies have used Russian federal and

regional incentive programs such as

Tax breaks

State guarantees

Special investment contracts

Public Private Partnership

8% of the respondents have used similar investment incentive

schemes. All but one company claim that these measures have been

beneficial for the company.

1/3 …of the companies have local

production in Russia

…of the companies made investments

in 2015

…of the companies have used some

kind of governmental support

31% 8%

13

BUSINESS SWEDEN 16 MAY 2016 14

COMPANIES ARE STAYING AND

EXPANDING IN RUSSIA

As a general trend on the long term ambition the statement is clear: The Swedish

companies are in Russia to stay and expand in the long run. The largest share of

companies, 74% are looking at long term expansion and a further 20% intend to

maintain the current level of business in Russia. A handful of companies plan on

reducing their presence or leaving the market.

The largest companies are the most expansionist in this regard. 19 out of 20

companies with a global turnover of >5 000 MEUR indicate an intention to grow long

term.

Looking at the short term intention to grow the local footprint, a tip over into growth

mode is spotted. 18% of the companies intend to increase their local footprint,

measured in number of offices, outlets, stores, production sites etc. Contrasted by 2%

intending to decrease the same footprint.

In the previous two years the expanding and contracting sides have been closer in

share, with an overweight to growth in 2014 (16% growth and 9 % contraction) and to

contraction in 2015 (12% growth and 14% contraction).

The regions drawing most of the attention is Far East and the Pacific Coast, and

Southern Russia. The “Millioniki” cities with >1m inhabitants are also attracting new

expansion.

74%

20%

1%

2%

3%

6%

Expand Maintain Decrease Leave Other

Long-term plans for Russia

LOCAL PRESENCE

…of the companies are planning to

expand their geofootprint in 2016

18%

14

BUSINESS SWEDEN 16 MAY 2016 15

FREE RESOURCES ON THE MARKET AMID ONGOING

REGRESSION

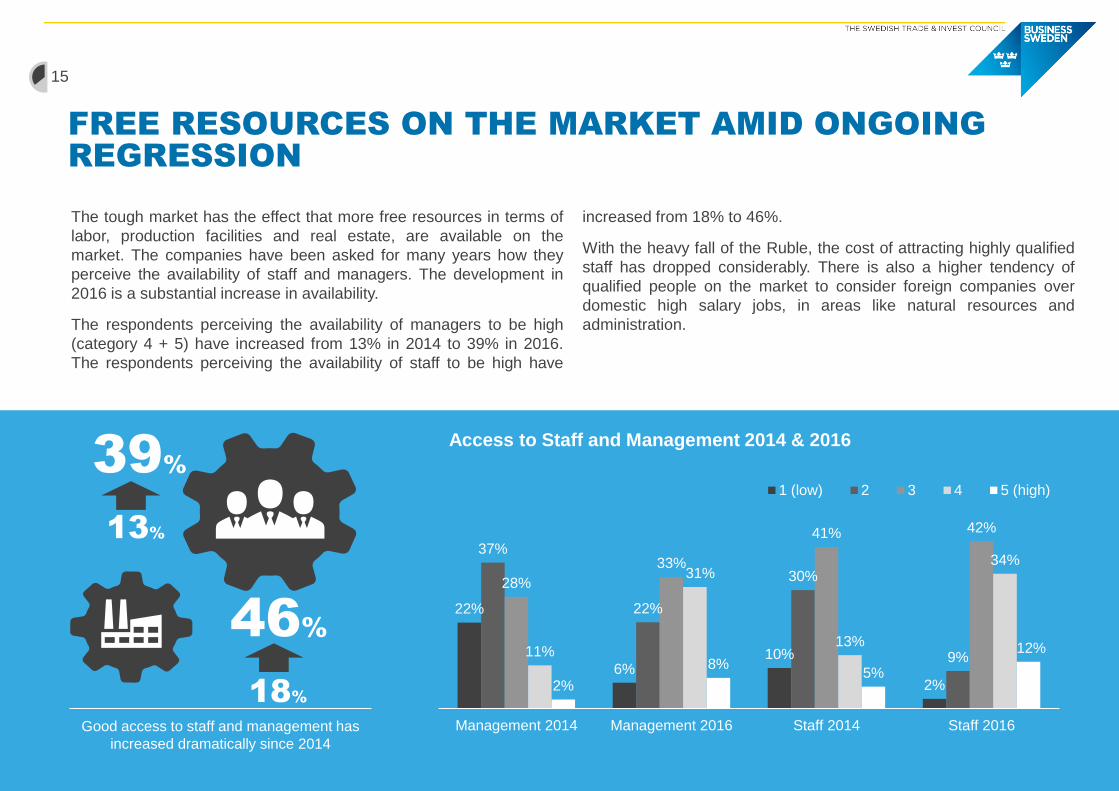

The tough market has the effect that more free resources in terms of

labor, production facilities and real estate, are available on the

market. The companies have been asked for many years how they

perceive the availability of staff and managers. The development in

2016 is a substantial increase in availability.

The respondents perceiving the availability of managers to be high

(category 4 + 5) have increased from 13% in 2014 to 39% in 2016.

The respondents perceiving the availability of staff to be high have

increased from 18% to 46%.

With the heavy fall of the Ruble, the cost of attracting highly qualified

staff has dropped considerably. There is also a higher tendency of

qualified people on the market to consider foreign companies over

domestic high salary jobs, in areas like natural resources and

administration.

22%

6% 10%

2%

37%

22%

30%

9%

28%

33%

41% 42%

11%

31%

13%

34%

2%

8% 5%

12%

Management 2014 Management 2016 Staff 2014 Staff 2016

1 (low) 2 3 4 5 (high)

Access to Staff and Management 2014 & 2016

46%

39%

13%

18%

Good access to staff and management has

increased dramatically since 2014

15

BUSINESS SWEDEN 16 MAY 2016 16

WHY STAY IN RUSSIA?

What are the main drivers to remain doing business on the Russian

market?

The sentiment for the Russian market is challenging, going into the

third year of recession with political sanctions on top of it. Despite this

fact, 84% of the respondents estimate their long term profitability on

the Russian market being moderate to very high. The long term

profitability seems to talk in favor of the Russian market despite the

low tide in the economy.

A growing share of the respondents believe in the Russian market as

a whole. 70% expect that the Russian market as a whole recovers

and returns to growth within 3 years. Still, 7% don’t foresee any

positive scenario, but that number has fallen from 20% last year. In

general the expectations on the market have consolidated to more

moderate expectations.

The Swedish brand is strong. A reassuring 88% of the respondents

claim that the image of Sweden among its counterparts is positive or

very positive. Only one respondent indicated that the image would be

negative. All companies profiling themselves as Swedish claim that

the association with Sweden impacts their business in a positive way.

Some 15% of the companies don’t profile themselves as Swedish

companies.

These impressions from the Swedish companies active in Russia can

be complemented with external research by the Levada institute,

measuring the sentiment among Russians on Sweden. Year after year

Sweden scores high in these polls compared to nearby countries and

to the EU as a whole.

70%

…of the companies lowered real wages

in 2015 3 years

84%

…of the companies think the Russian

market is moderately to highly profitable

…of the companies expect the market

will turnaround within 3 years

…say the Swedish brand is perceived

positively or very positively in Russia

70% 88%

16

BUSINESS SWEDEN 16 MAY 2016 17

DIVERSE FACTORS AFFECT

STRATEGIC CHOICES IN RUSSIA

The Russian market faces great challenges in the turbulence that has been ongoing

since 2014. The past few years have been tough for many, but the expectations on

2016 and beyond are filled with more confidence than anticipated.

The Swedish companies undertake significant action on top and bottom lines to

counter the new normal, they seem to beat the competition. They take market share

and the long term profitability appear to be satisfactory.

The corruption remains a problem, in contact with public counterparts and authorities,

as well as private external and internal counterparts. The trend is assumed to be

somewhat positive going forward.

Protectionist measures and a strong focus on local production pressures the

companies to action to keep their access to the market.

The Swedish companies have a strong position with strong brands and a potential to

develop the operations in a favorable and profitable direction. And to remain winners in

the tough competition.

Because there is a shake out going on in the market. Many weak players are leaving,

closing or going bankrupt. It is important to remember that the tough times in the

Russian market are valid for all companies. The competitors of the Swedish

companies fight the same challenges. The strongest players survive and have good

chances to gain market share and a stronger position.

FOOD FOR

THOUGHT

There is a shakeout going on and the

strongest will prevail

Russia is complex and many factors

need strategic analysis

17

BUSINESS SWEDEN 16 MAY 2016 18

THE FUTURE IS UNPREDICTABLE AND RUSSIA DEMANDS

CLOSE MONITORING OF DEVELOPMENTS

The future is uncertain, the political risk remains high, and we don’t

know what we can expect going forward.

The first part of 2016 has shown a lower level of conflict in the

political landscape and a respite in the dramatic events seen since

2014. How this will develop further, is impossible to foresee.

Single major events can have large consequences. The downed

Russian fighter jet in Syria changed the relation between Russia and

Turkey overnight with dramatic consequences for Turkish companies

and Russian consumers.

We see no reason to worry in the specific relation between Russia

and Sweden, but the speed in policy change in dramatic events

makes the political risk utterly hard to predict.

Energy and commodity prices are still of vital importance for the

Russian economy. The currency rate and the Moscow stock

exchange show high correlation with the oil price. An increase in the

oil price might take Russia out of recession sooner, a decrease can

rapidly make the future prospects more gloomy.

It is important to maintain a close monitoring of the Russian market,

and to spot events that can affect the business activities in Russia.

This is not least valid for the regulatory affairs, where new laws and

regulations come frequently and often change the preconditions for

business. Sometimes in a favorable direction, sometimes in ways

that demand big adjustments or even disables a continued concern.

There is high business potential in Russia, also after the events

of 2014 and 2015. The risk level is high and a robust, yet flexible

strategy is recommended to deal with unexpected changes.

?

Uncertainty is something everyone has to deal with in

Russia. No one knows what will happen in the future

18

BUSINESS SWEDEN 16 MAY 2016 19

CHOOSE YOUR STRATEGY BASED ON RISK APPETITE,

TIME HORIZON AND RESOURCES

Russia is and will remain a large nearby market, with opportunities for

a high reward and with a significant risk to consider. Many strategic

considerations need to be done, some of which are covered in this

report, based on the impressions of Swedish companies on the

Russian market.

What strategy to choose is mainly depending on the company’s

Resources, Risk Appetite and Time Horizon.

The three last pages of this report will go through three scenarios

based on high, medium and low level of these three main factors.

High Low

Risk/Reward

3 MAIN STRATEGIES FOR THE RUSSIAN MARKET

19

BUSINESS SWEDEN 16 MAY 2016 20

HIGH RISK / HIGH REWARD – THE AGGRESSIVE

APPROACH

If the three factors Resources, Risk Appetite and Time Horizon

are in abundance, there is a good opportunity to fight the bearish

market. Take the initiative and establish a heavy local presence in

Russia as a local player for the Russian market and the surrounding

countries. By establishing or increasing local production, own

distribution and sales channels, the company can act aggressively

and take market share from competitors. Competitors can be

beaten or bought, asset prices have a lower valuation than in a long

time.

Use competitive advantages that the foreign ownership provides.

Financing is scarce on the market. By taking up financing offshore

and funnel it to Russia, opportunities may appear that competitors

will find hard to compete with. Be proactive in governmental

relations and influence the debate where the rules of the market are

being shaped.

Being successful in a strong scenario can enable a dominant

position on the market, but with significant risk, high demand for

resources and possibly many years before a stable profit can be

reached.

Fight the bearish market!

20

BUSINESS SWEDEN 16 MAY 2016 21

THE MIDDLE WAY – LAY LOW

In the mid range of the strategy scenario we find the “wait and see”

mode. This has been the main option for most companies the past

few years. Costs have been cut, the cost base has been adjusted

for weaker sales and lower margins.

Remain on the market but lose the lead.

Keep a possibility to scale up when the market returns to a more

favorable direction.

Develop cooperation with collaborative partners and find alternative

markets for existing products.

Monitor the development on the market and react fast to changes.

21

Lay low and wait for summer

BUSINESS SWEDEN 16 MAY 2016 22

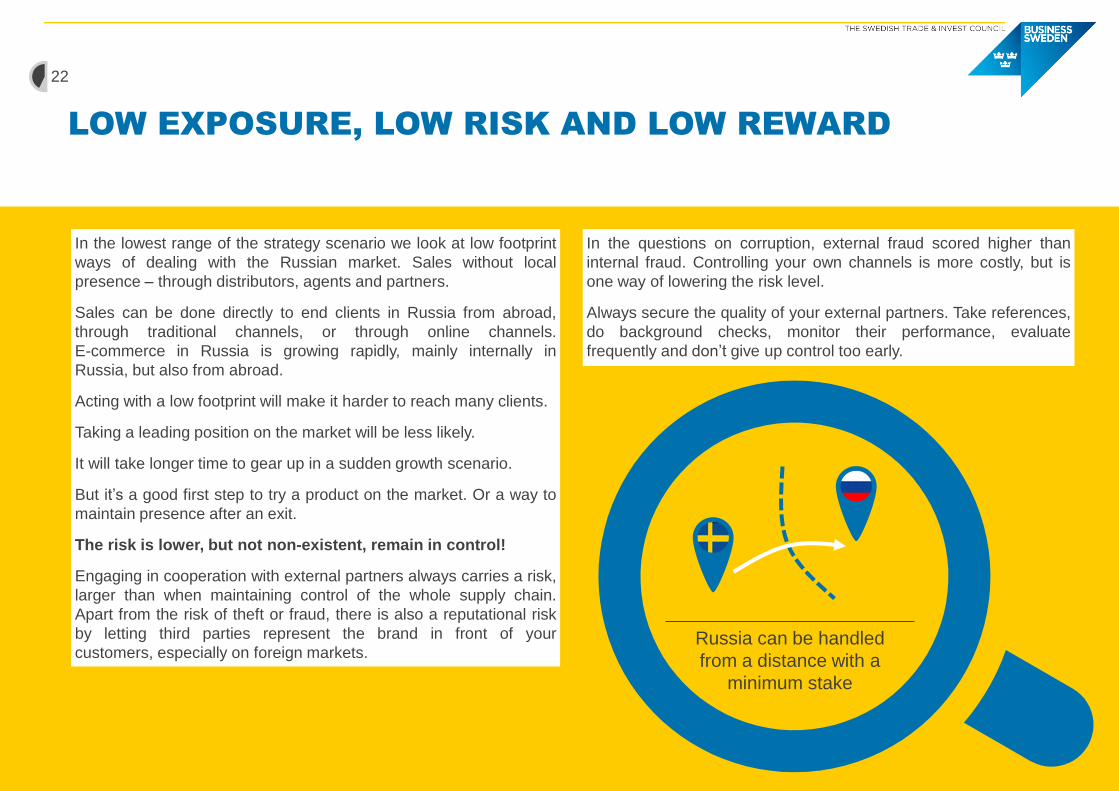

LOW EXPOSURE, LOW RISK AND LOW REWARD

In the lowest range of the strategy scenario we look at low footprint

ways of dealing with the Russian market. Sales without local

presence – through distributors, agents and partners.

Sales can be done directly to end clients in Russia from abroad,

through traditional channels, or through online channels.

E-commerce in Russia is growing rapidly, mainly internally in

Russia, but also from abroad.

Acting with a low footprint will make it harder to reach many clients.

Taking a leading position on the market will be less likely.

It will take longer time to gear up in a sudden growth scenario.

But it’s a good first step to try a product on the market. Or a way to

maintain presence after an exit.

The risk is lower, but not non-existent, remain in control!

Engaging in cooperation with external partners always carries a risk,

larger than when maintaining control of the whole supply chain.

Apart from the risk of theft or fraud, there is also a reputational risk

by letting third parties represent the brand in front of your

customers, especially on foreign markets.

Russia can be handled

from a distance with a

minimum stake

22

In the questions on corruption, external fraud scored higher than

internal fraud. Controlling your own channels is more costly, but is

one way of lowering the risk level.

Always secure the quality of your external partners. Take references,

do background checks, monitor their performance, evaluate

frequently and don’t give up control too early.

BUSINESS SWEDEN 16 MAY 2016 23

Thank you for taking your time to read this report on the Business Climate in

Russia. Russia is a country and a market that has always triggered strong

emotions. Sometimes big and frightening, sometimes incomprehensible and

unpredictable. But remember that it is more similar than we sometimes

assume it to be. Business in Russia is like business in most places, every

country is unique in its own way.

Don’t hesitate to reach out to me or my team in Moscow, Stockholm or any of

the other 50+ locations where we are represented in the world. We have seen

a lot and know the local aspects of business.

We discuss strategies and plans on a daily basis. We advice our clients, from

the smallest startups to the global corporations in all steps of their international

endeavors. We have the networks and can complement your internal

resources in an efficient way, worldwide.

All the very best, vi hörs!

/Andreas

Final words

+46 703 909 473

www.business-sweden.se

@BusinessSweCEE

Business Sweden’s purpose is to help every Swedish

company to reach their full international potential

BUSINESS SWEDEN 16 MAY 2016 24

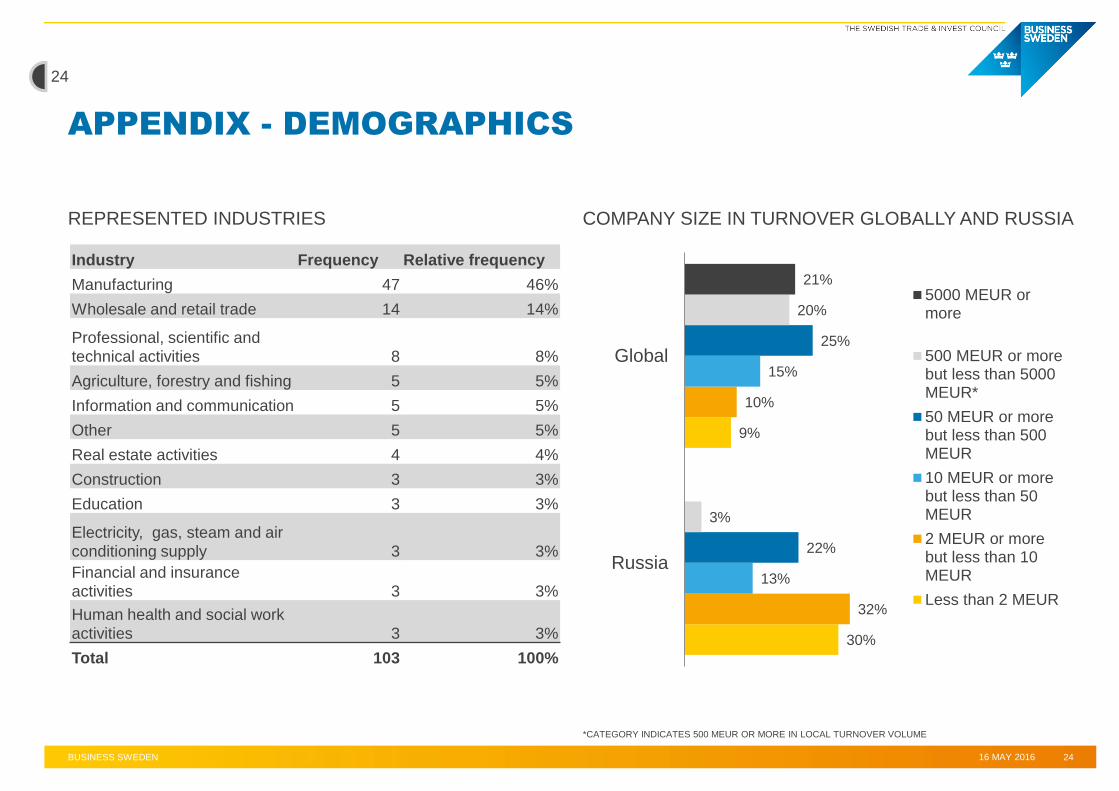

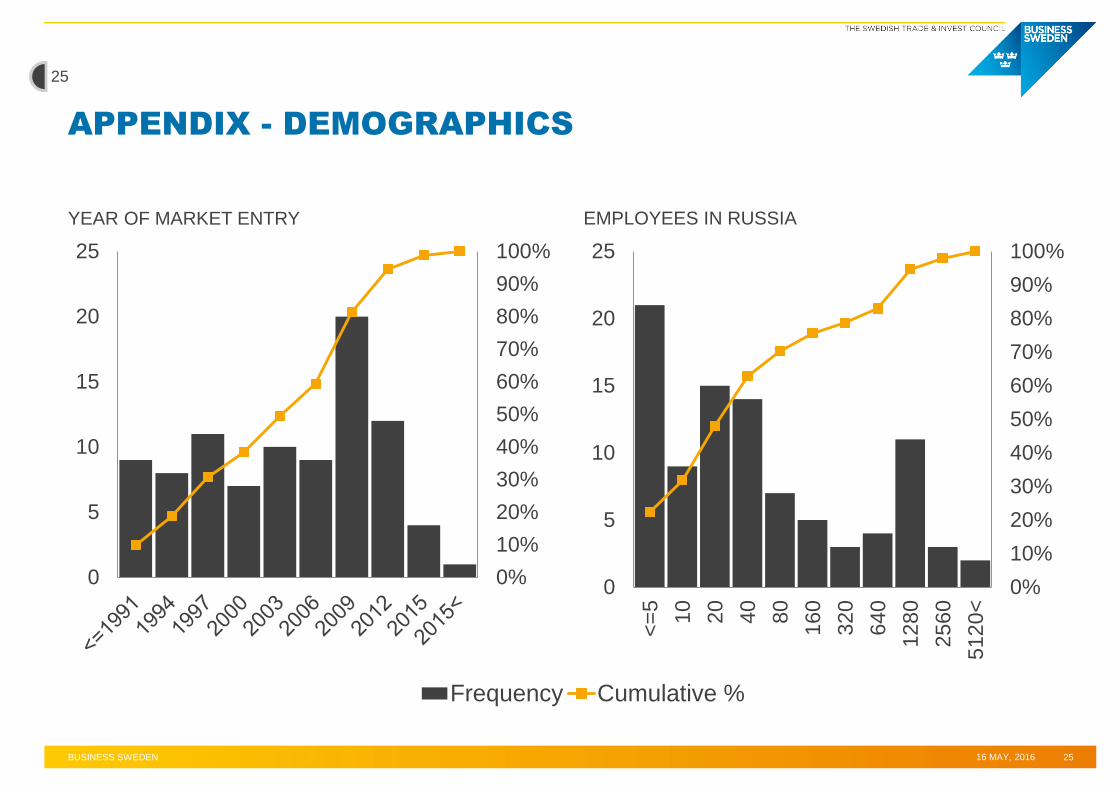

APPENDIX - DEMOGRAPHICS

30%

9%

32%

10%

13%

15%

22%

25%

3%

20%

21%

Russia

Global

5000 MEUR ormore

500 MEUR or morebut less than 5000MEUR*

50 MEUR or morebut less than 500MEUR

10 MEUR or morebut less than 50MEUR

2 MEUR or morebut less than 10MEUR

Less than 2 MEUR

REPRESENTED INDUSTRIES COMPANY SIZE IN TURNOVER GLOBALLY AND RUSSIA

*CATEGORY INDICATES 500 MEUR OR MORE IN LOCAL TURNOVER VOLUME

Industry Frequency Relative frequency

Manufacturing 47 46%

Wholesale and retail trade 14 14%

Professional, scientific and

technical activities 8 8%

Agriculture, forestry and fishing 5 5%

Information and communication 5 5%

Other 5 5%

Real estate activities 4 4%

Construction 3 3%

Education 3 3%

Electricity, gas, steam and air

conditioning supply 3 3%

Financial and insurance

activities 3 3%

Human health and social work

activities 3 3%

Total 103 100%

24

YEAR OF MARKET ENTRY

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

5

10

15

20

25

EMPLOYEES IN RUSSIA

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

5

10

15

20

25

<=

5

10

20

40

80

16

0

32

0

64

0

128

0

256

0

512

0<

16 MAY, 2016 BUSINESS SWEDEN 25

APPENDIX - DEMOGRAPHICS

Frequency Cumulative %

25