cash flow statement with examples

TRANSCRIPT

CASH FLOW STATEMENT

Submitted to: Mr. N.K GuptaSubmitted by: Akshay Vohra

Donil ShijagurumayumGunjan Rastogi

Rahul IyerRajnees Singh

“THE FACT IS THAT ONE OF THE EARLIEST LESSONS I LEARNED IN BUSINESS WAS THAT BALANCE SHEETS AND INCOME STATEMENTS ARE FICTION, CASH FLOW IS REALITY.”

-Mr. Chris Chocola2

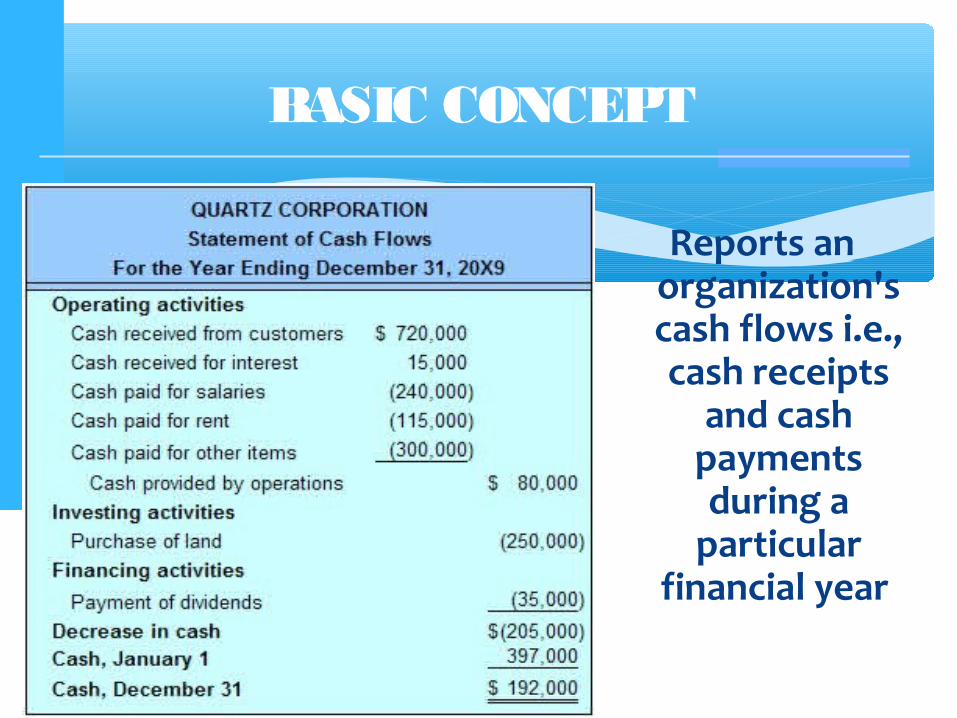

Reports an organization's cash flows i.e., cash receipts

and cash payments during a

particular financial year

BASIC CONCEPT

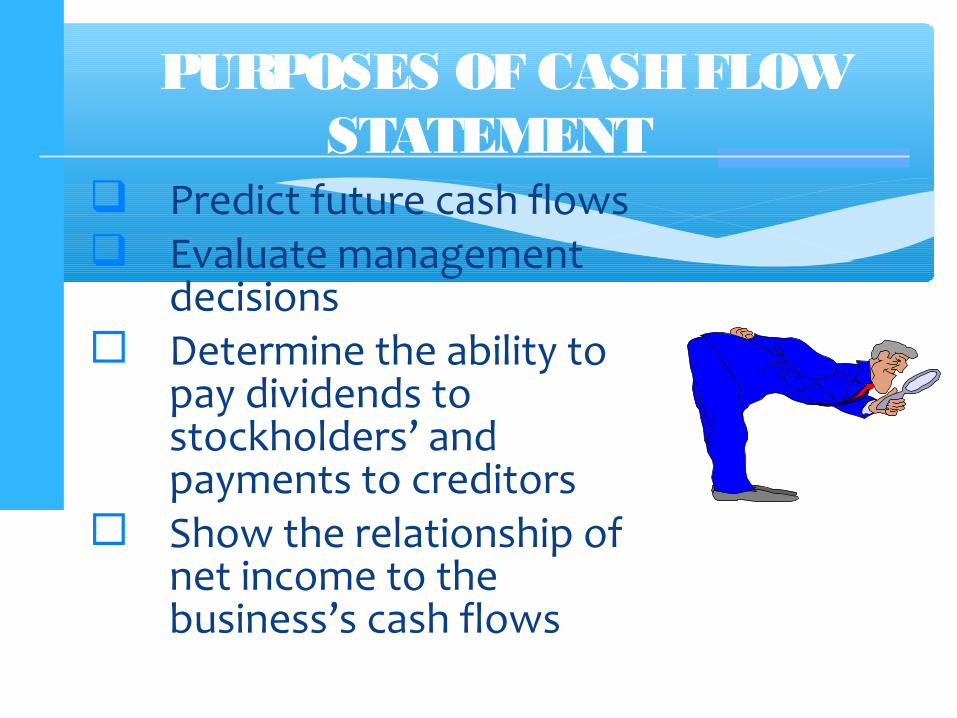

Predict future cash flows Evaluate management

decisions Determine the ability to

pay dividends to stockholders’ and payments to creditors

Show the relationship of net income to the business’s cash flows

PURPOSES OF CASH FLOW STATEMENT

To identify the sources from where cash inflows have arisen within a particular period and also shows the various activities where in the cash was utilized.

It is significant to management for proper cash planning and maintaining a proper matching between cash inflows and outflows.

Shows efficiency of a firm in generating cash inflows from its regular operations.5

IMPORTANCE OF CASH FLOW STATEMENT

Reports the amount of cash used during the period in various long-term investing activities, such as purchase of fixed assets.

Reports the amount of cash received during the period through various financing activities, such as issue of shares, debentures and raising long-term loan.

6

WHAT IS CASH?

∗ Cash in hand∗ Cash in bank∗ Cash equivalents - highly liquid, short-term investments

that can be converted into cash with little delay

FORMS OF CASH

THREE CASH FLOW ACTIVITIES

CASH FLOW FROM OPERATING ACTIVITIES

CASH FLOW FROM OPERATING ACTIVITIES

Operating activities are normal and core activities within a business that generate cash inflows and outflows. They include:

∗ Total sales of goods and services collected during a period;

∗ Payments made to suppliers of goods and services used in production settled during a period;

∗ Payments to employees or other expenses made during a period.

MORE ON OPERATING ACTIVITIES

12

∗ An accounting item indicating the money a company brings in from ongoing, regular business activities, such as manufacturing and selling goods or providing a service. Cash flow from operating activities does not include long-term capital or investment costs. It does include earnings before interest and taxes plus depreciation minus taxes.

13

DEFINITION OF OPERATING ACTIVITIES

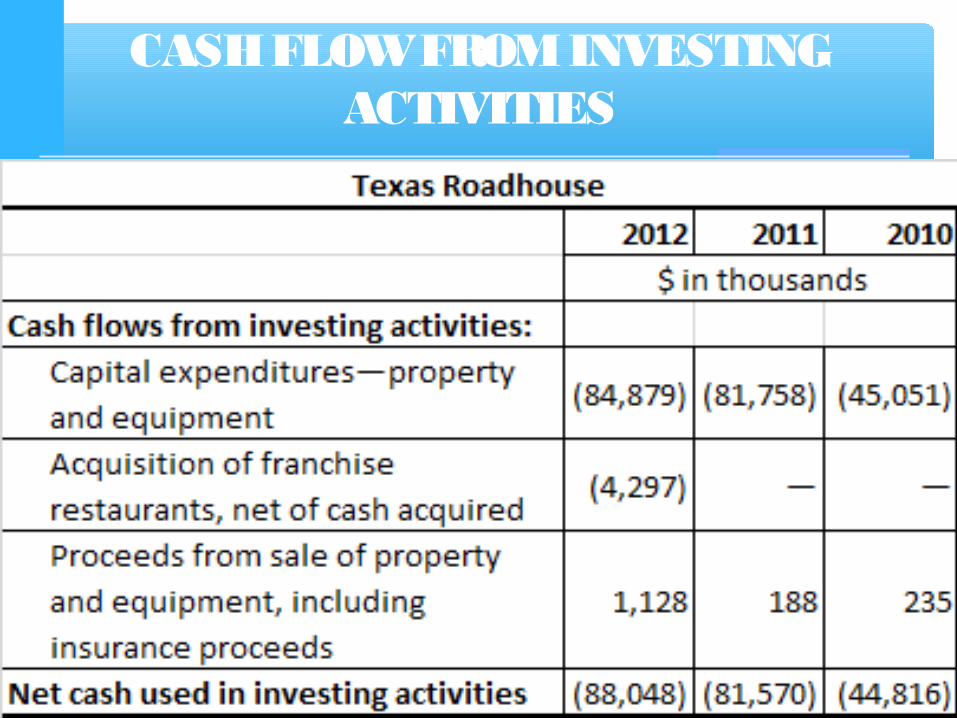

CASH FLOW FROM INVESTING ACTIVITIES

CASH FLOW FROM INVESTING ACTIVITIES

∗ An item on the cash flow statement that reports the aggregate change in a company's cash position resulting from any gains (or losses) from investments in the financial markets and operating subsidiaries, and changes resulting from amounts spent on investments in capital assets such as plant and equipment.

DEFINITION OF INVESTING ACTIVITIES

∗ Examples of Inflows: Proceeds from disposal of property, plant and

equipment Cash receipts from disposal of debt instruments of

other entities Receipts from sale of equity instruments of other

entities

INFLOW OR OUTFLOW OF CASH

17

∗ Examples of Outflows: Payments for acquisition of property, plant and

equipment Payments for purchase of debt instruments of

other entities Payments for purchase of equity instruments of

other entities Sales/maturities of investments Includes purchasing and selling long- term assets

and other investments.18

CASH FLOW FROM FINANCING ACTIVITIES

CASH FLOW FROM FINANCING ACTIVITIES

∗ A category in a company’s cash flow statement that accounts for external activities that allow a firm to raise capital and repay investors, such as issuing cash dividends, adding or changing loans or issuing more stock. Cash flow from financing activities shows investors the company’s financial strength. A company that frequently turns to new debt or equity for cash, for example, could have problems if the capital markets become less liquid.

∗ FORMULA: Cash received from issuing stock or debt - cash paid as dividends and Re-acquisition of debt/stock.

CASH FLOW FROM FINANCING ACTIVITIES

Two Formats forOperating Activities

Indirect method reconciles from net income to net cash provided by operating activities

23

INDIRECT METHOD

∗Direct method reports all cash receipts and cash payments from operating activities

24

DIRECT METHOD

” The only difference between the two methods is, how cash flows from

operating activities are calculated.”

25

DIFFERENCE BETWEEN INDIRECT & DIRECT METHOD

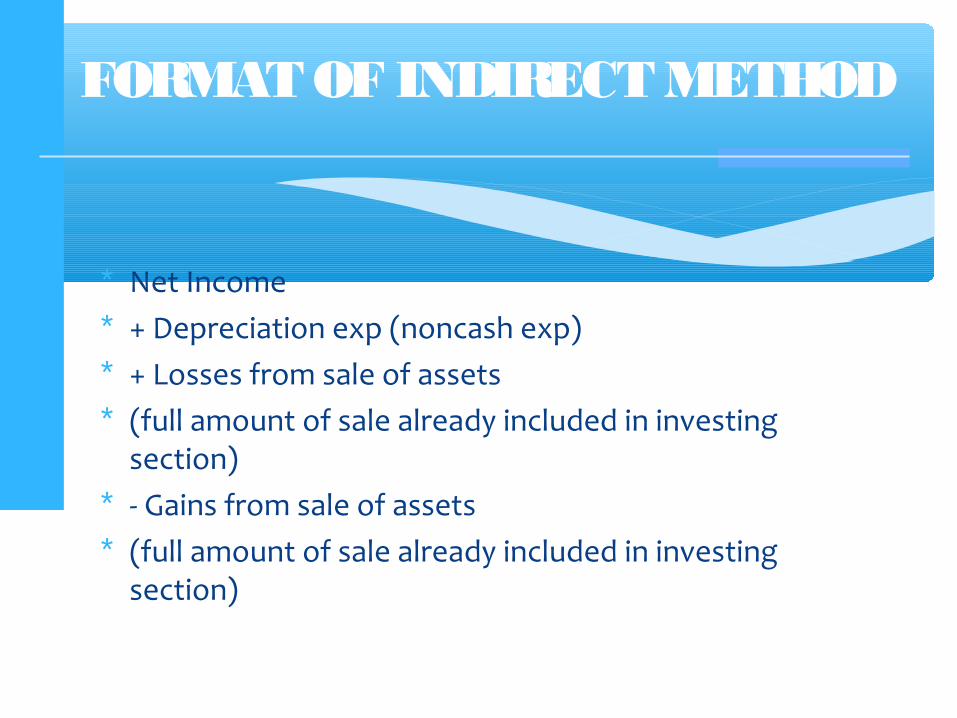

FORMAT OF INDIRECT METHOD

∗ Net Income∗ + Depreciation exp (noncash exp)∗ + Losses from sale of assets ∗ (full amount of sale already included in investing

section)∗ - Gains from sale of assets∗ (full amount of sale already included in investing

section)

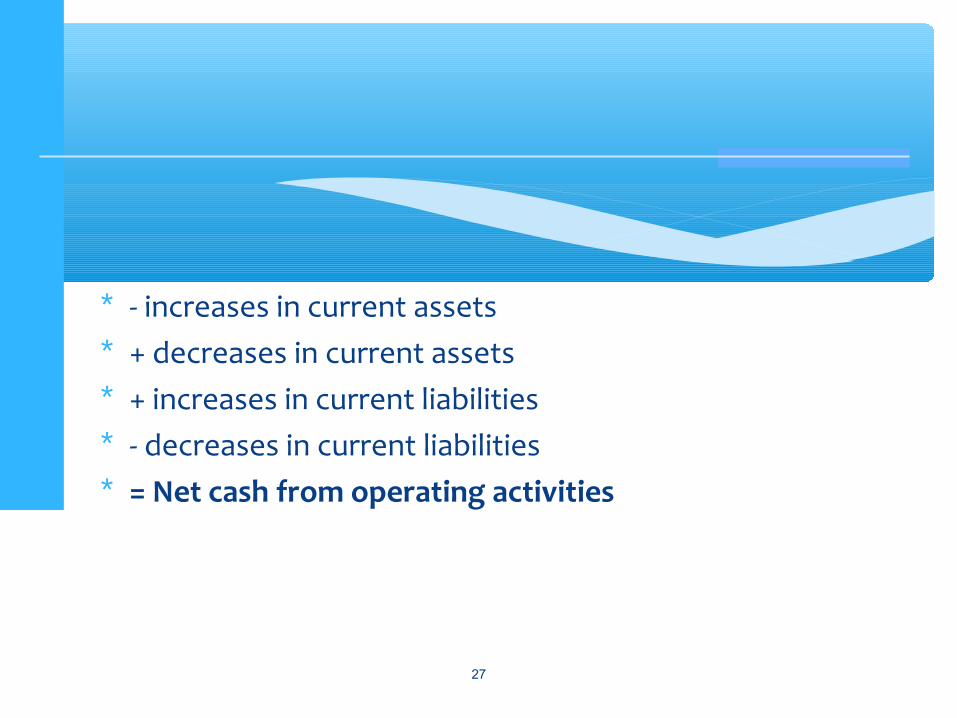

∗ - increases in current assets∗ + decreases in current assets∗ + increases in current liabilities∗ - decreases in current liabilities∗ = Net cash from operating activities

27

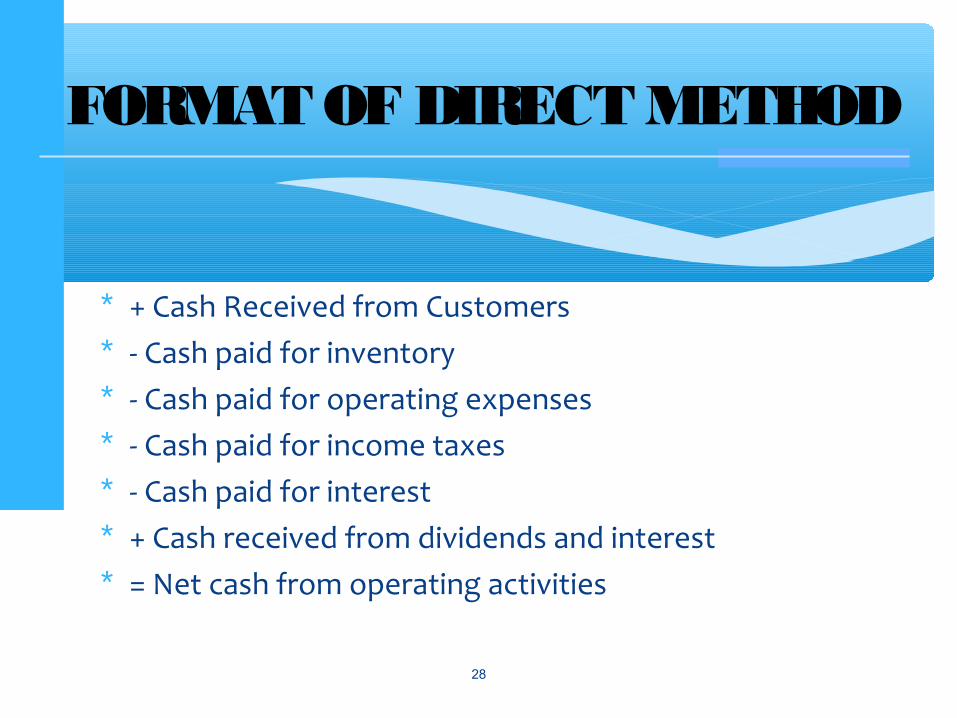

∗ + Cash Received from Customers∗ - Cash paid for inventory ∗ - Cash paid for operating expenses∗ - Cash paid for income taxes∗ - Cash paid for interest∗ + Cash received from dividends and interest∗ = Net cash from operating activities

28

FORMAT OF DIRECT METHOD

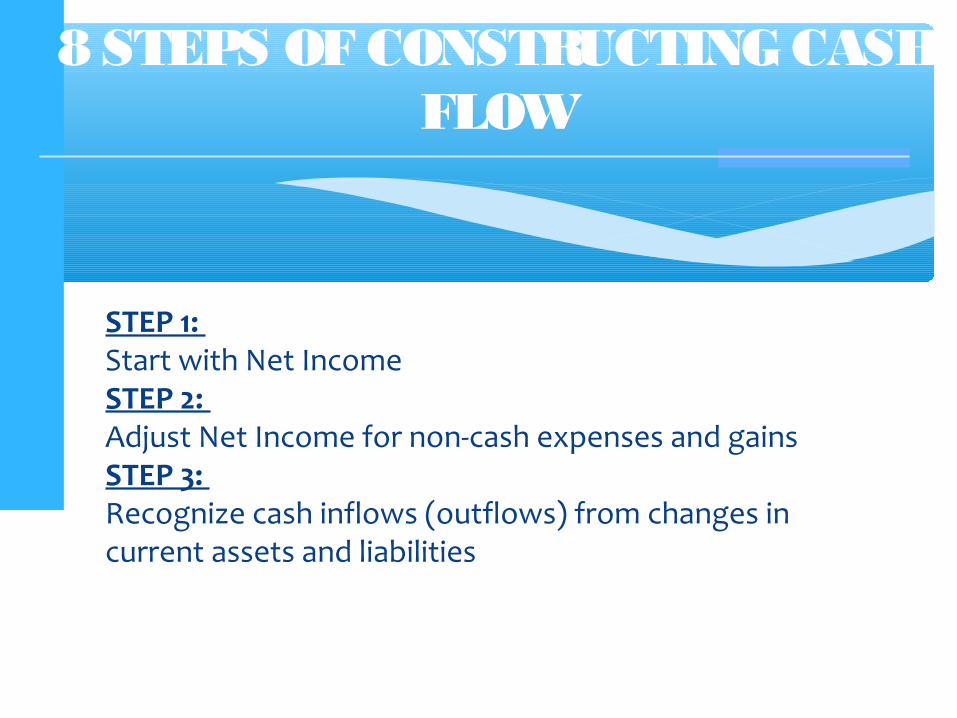

8 STEPS OF CONSTRUCTING CASH FLOW

STEP 1: Start with Net IncomeSTEP 2: Adjust Net Income for non-cash expenses and gainsSTEP 3: Recognize cash inflows (outflows) from changes in current assets and liabilities

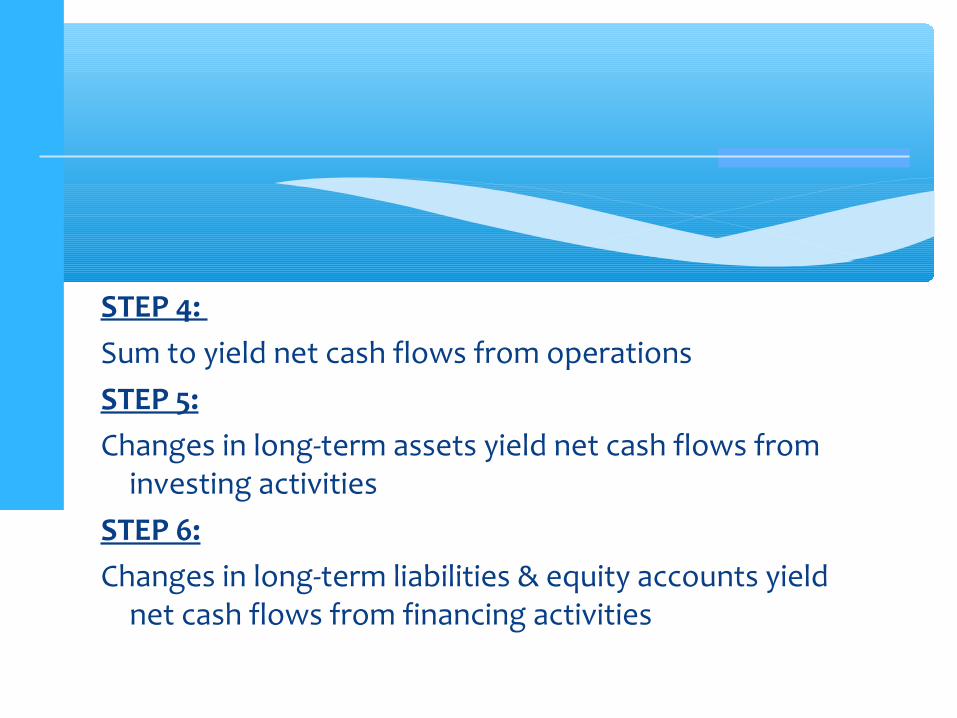

STEP 4: Sum to yield net cash flows from operationsSTEP 5:Changes in long-term assets yield net cash flows from

investing activitiesSTEP 6:Changes in long-term liabilities & equity accounts yield

net cash flows from financing activities

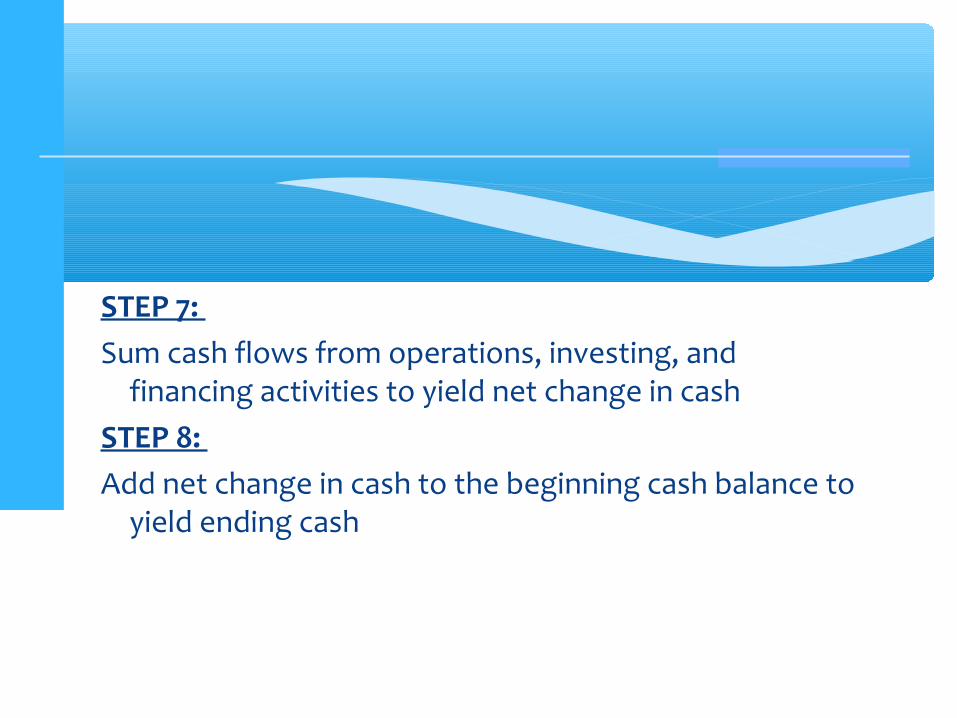

STEP 7: Sum cash flows from operations, investing, and

financing activities to yield net change in cashSTEP 8: Add net change in cash to the beginning cash balance to

yield ending cash

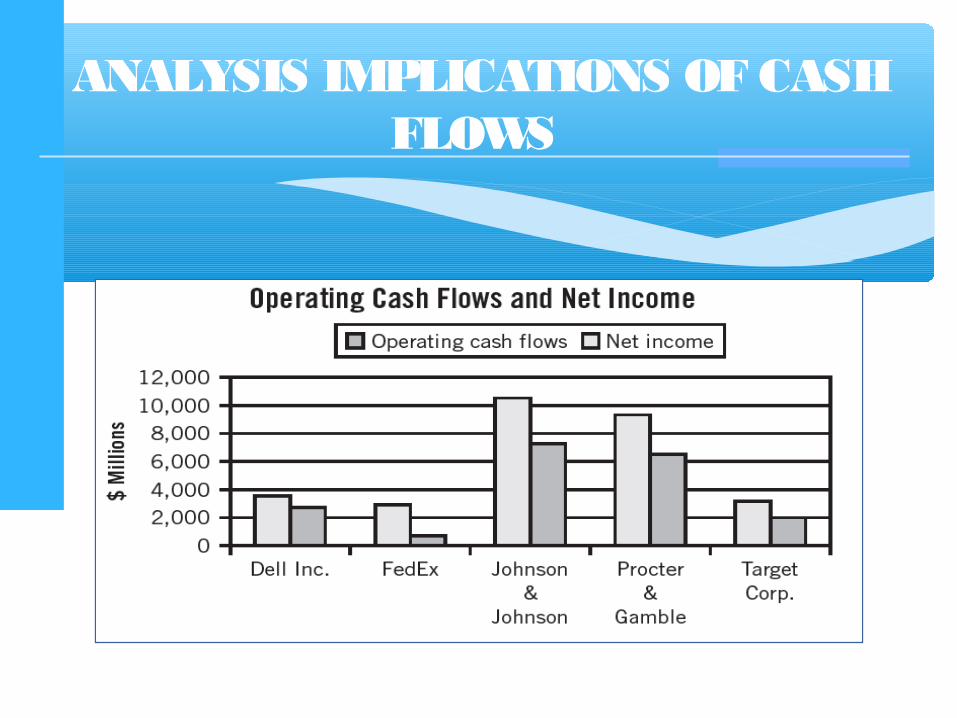

ANALYSIS IMPLICATIONS OF CASH FLOWS

A healthy cash flow is an essential part of any successful business. Some business people claim that a healthy cash flow is even more important than your business's ability to deliver its goods or services. Maintaining a viable cash flow system relies on SIX IMPORTANT ASPECTS discussed further :

33

MANAGING YOUR FIRM’S CASH FLOW

1. Understanding cash flow is the first step in effectively managing your cash flow. There's more to it than just a fancy term for the movement of money into, and out of, your business checking account.

2. Analyzing your cash flow will help you spot some of the

problem areas in the cash flow cycle of your business. As in any good analysis, you need to look individually at each of the important components that make up the cash flow cycle to determine if it's a problem area or not.

34

3. Developing a cash flow budget provides a good way of predicting your business's cash flow for the next month, six months or even the next year.

4. Improving your cash flow will, without a doubt, make your business more successful. Accelerating your cash inflows and delaying your cash outflows are key factors for improving and managing your cash flow. The cash flow budget is also a handy tool to use in the improvement and management of your cash flow.

35

5. Filling your cash flow gaps: from time to time, almost every business experiences the need for more cash than it has. If you find yourself in this position, you may have to borrow money to fill the gap.

6. Handling any cash surplus is just as important as the management of money into and out of your cash flow cycle. With the proper management of your cash flow, you might find yourself with a little extra cash, on which you can earn investment income.

36

EXAMPLES OF CASH FLOW STATEMENTS OF SOME

FAMOUS BRANDS

37

COMPARATIVE CASH FLOW STATEMENT

OF COCA-COLA

38

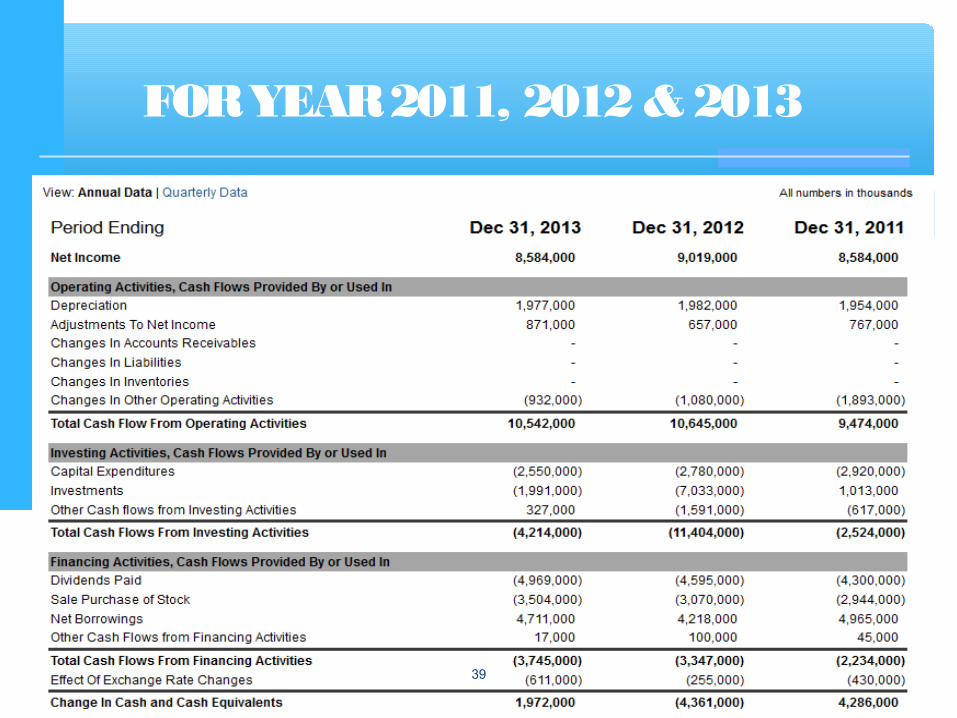

FOR YEAR 2011, 2012 & 2013

39

`

JOHNSON AND

JOHNSON’S CASH FLOW STATEMENT (in 3 Parts)

40

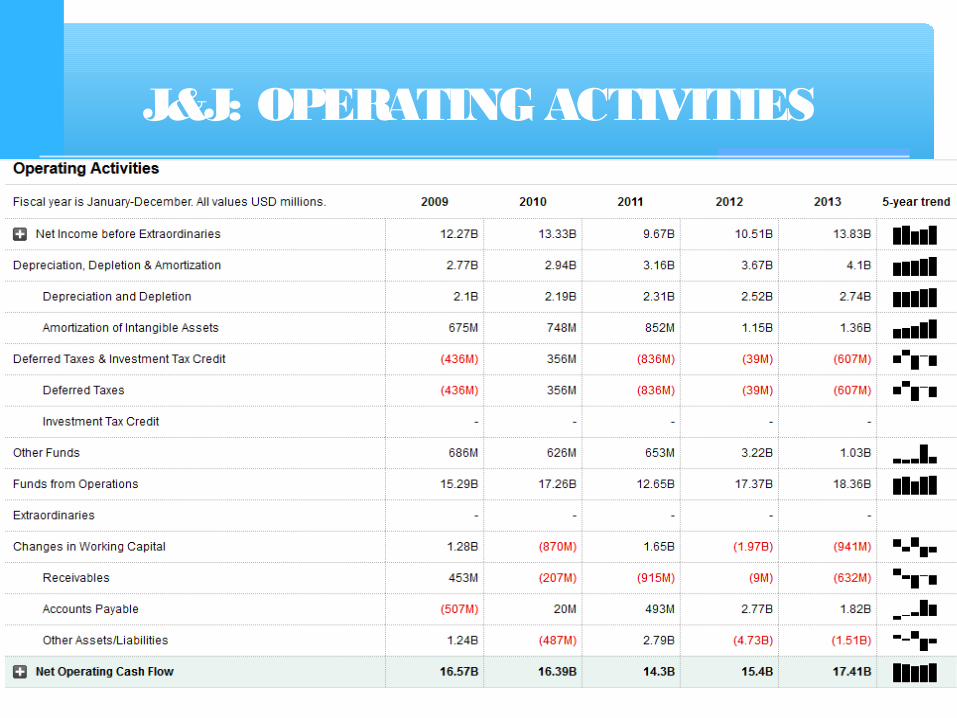

J&J: OPERATING ACTIVITIES

41

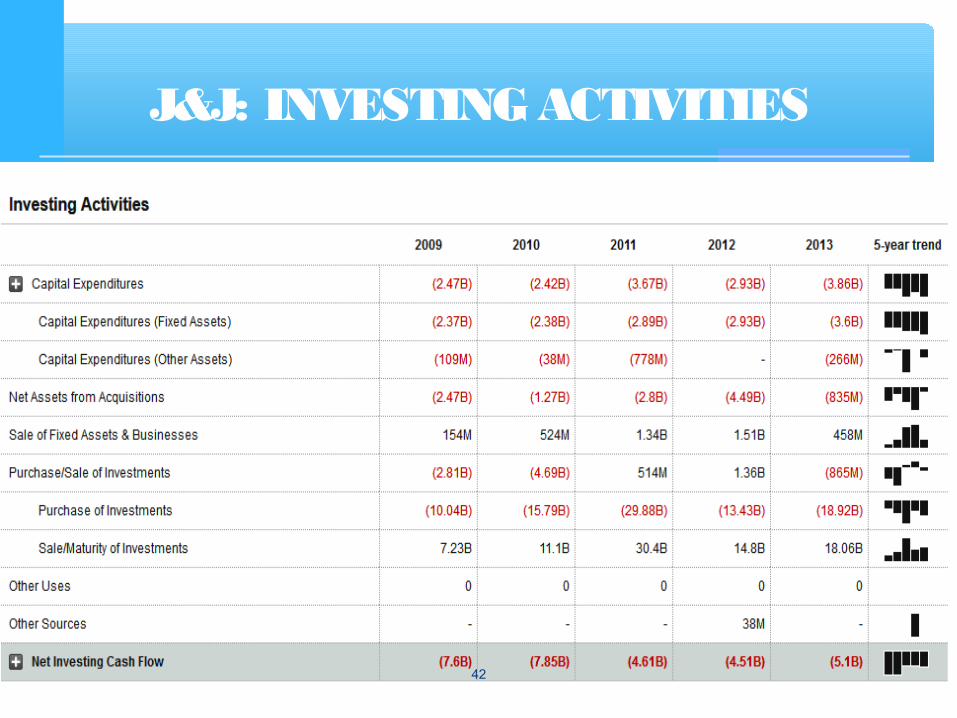

J&J: INVESTING ACTIVITIES

42

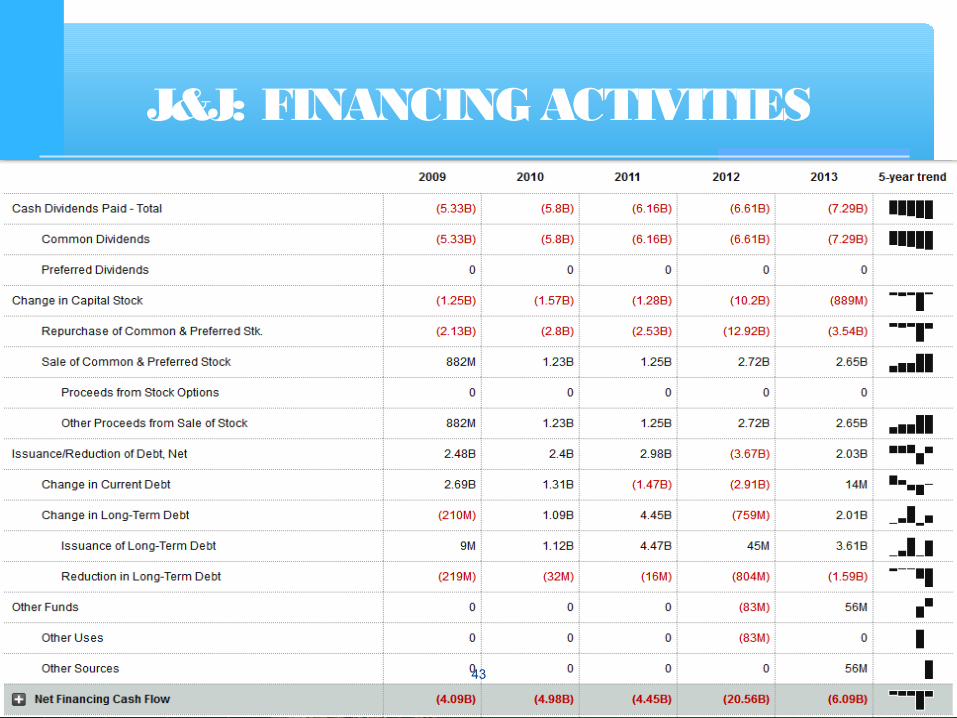

J&J: FINANCING ACTIVITIES

43

RELIANCE’S CASH FLOW STATEMENT

44

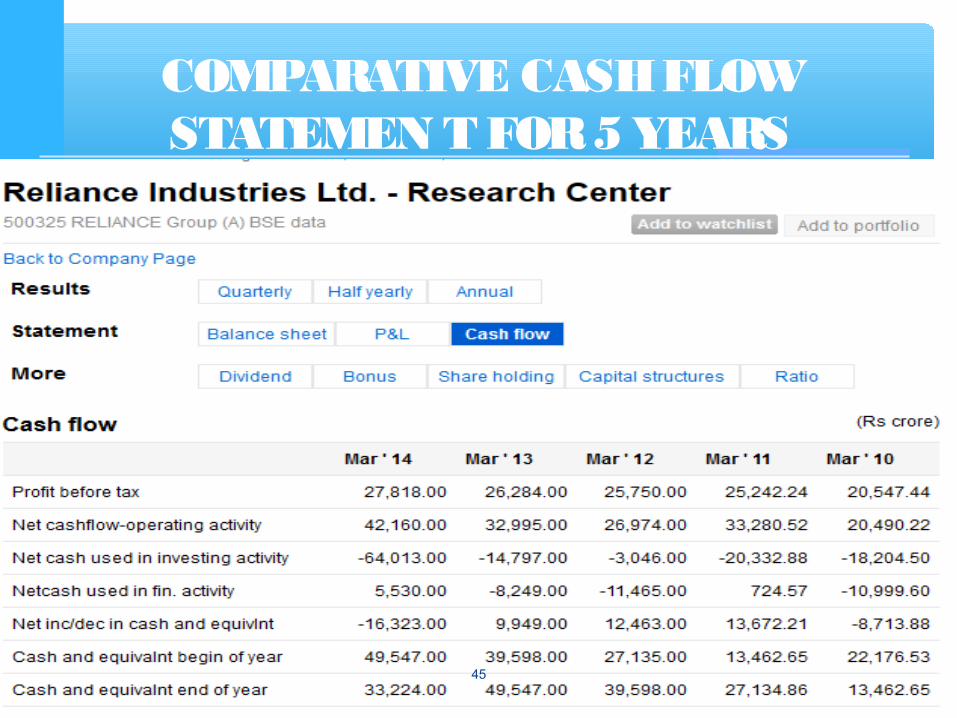

COMPARATIVE CASH FLOW STATEMEN T FOR 5 YEARS

45

DISADVANTAGES OF CASH FLOW STATEMENT

46

1. One of the potential disadvantages of the cash flow statement is that it does not take into consideration any future growth. When looking at the statement of cash flows, you are essentially looking at information from the past business operations.

Limitations of Cash Flow Statement

47

For example: If the company is in the process of developing a ground-breaking piece of technology, it could be about to generate a large amount of cash. If you just look at the cash flow statement, you may not evaluate the future potential of the company correctly.

48

49

2. Another potential problem with the statement of cash flows is that interpreting data may be difficult. The information on a cash flow statement is not necessarily easy to interpret. You can see where all of the cash flow is going, but you may not know if it should be going there.

50

For example, it may be difficult to gauge whether the company should be investing more in a plant or paying off debt. You have to take all of the information presented and make the best assumptions you can make.

3. Cash flow statements are not suitable for judging the profitability of a firm, as non-cash charges are ignored while calculating cash flows from operating activities.

51

4. As a cash flow statement is based on a cash basis of accounting, it ignores the basic accounting concept of accrual.

WHAT IS ACCURAL-BASED ACCOUNTING? A method that records income items when they are

earned and records deductions when expenses are incurred.

52

5. Business owners who experience cash flow difficulties are likely to make late payments for business supplies and other expenses. An honest and creative business owner who is on good terms with his suppliers will likely develop strategies for managing these situations.

53

For Example: A restaurant owner who offers his produce vendor a free meal while explaining that his payment will be late. A cash flow statement cannot capture these negotiations and agreements, but they are nonetheless a very real part of doing business.

54

A cash flow statement is a document depicting a company's liquidity, or its ability to meet current expenses using currently available resources. Cash flow statements are useful for providing a business with a general idea of how it will make ends meet in the short term. But cash flow statements do not show the full complexity of a business' strategies and resources for staying afloat or growing, and they depend on assumptions that are not always accurate.

AT THE END...

55

ACKNOWLEDGMENTS

Prof. Ramola KumarProf. N.K Gupta

Sony Ma’am

56

THANK YOU!

57