chapter 12 lecture: advanced micro-level valuation

TRANSCRIPT

Chapter 12 Lecture:Chapter 12 Lecture:

Advanced Micro-Level Valuation

Advanced Micro-Level Advanced Micro-Level ValuationValuation

Due to unique features of real estate, compared either to typical corporate capital budgeting, or to typical securities investments…

1. Investment Value (vs Market Value)

2. Asset market inefficiency (“noise” & inertia in prices)

3. Two parallel asset markets (private & public).

TWO CONCEPTS OF TWO CONCEPTS OF "VALUE""VALUE"1) "MARKET VALUE" (MV) = The Price at

which the property is most likely to sell in the current market (expected transaction price in current property market).

2) "INVESTMENT VALUE" (IV) = The present value of the long-run value of the property to a specified owner, assuming it is held by that owner for a long time without selling it. (Aka: “usage value”, “inherent value”.)

Usually these two are the same thing.

However, However, 3 conditions where 3 conditions where they may differ:they may differ:1) Owner is user and unique fit in real

production:– e.g., prop=restaurant w golden arches,

owner=McDonalds…– Corp. real estate?– Some REITs?

Conditions (cont’d):Conditions (cont’d):

2) Owner has a different tax status than that of the more typical investor/owner of the type of property in question:– MV determined by type of investors

actively buying and selling in the property market.

Conditions (cont’d):Conditions (cont’d):

Can IV MV market-wide?…

3) Informational inefficiency in the real estate market (e.g., "sluggishness", "bubbles") MV no longer well reflects fundamental long-run equilibrium value: You can predict which way it will change?

CAVEAT #1: CAVEAT #1:

Watch out for IV: A great “sales pitch”! IV usually more subjective than MV. People have a tendency to exaggerate frequency and significance of the conditions which can cause IV MV, to argue for their interest.Be skeptical of claims that IV MV.

CAVEAT #2:CAVEAT #2:

Do not pay > MV,just because IV > MV. Do not sell for < MV,just because IV < MV. “You get what you negotiate.”

Aside:Aside:

Often in corporate capital budgeting, there is no market for the underlying productive assets. Therefore, there is no MV. So IV is all there is. So distinction between IV vs MV (and therefore between NPV judged from a MV perspective vs NPV judged from an IV perspective) is often ignored in corporate environment. (But see Brealey-Myers Ch.11…)

General Rule for Condition General Rule for Condition in which: IV in which: IV MV MV

Investor(s) on at least one side of deal must be "intra-marginal"...

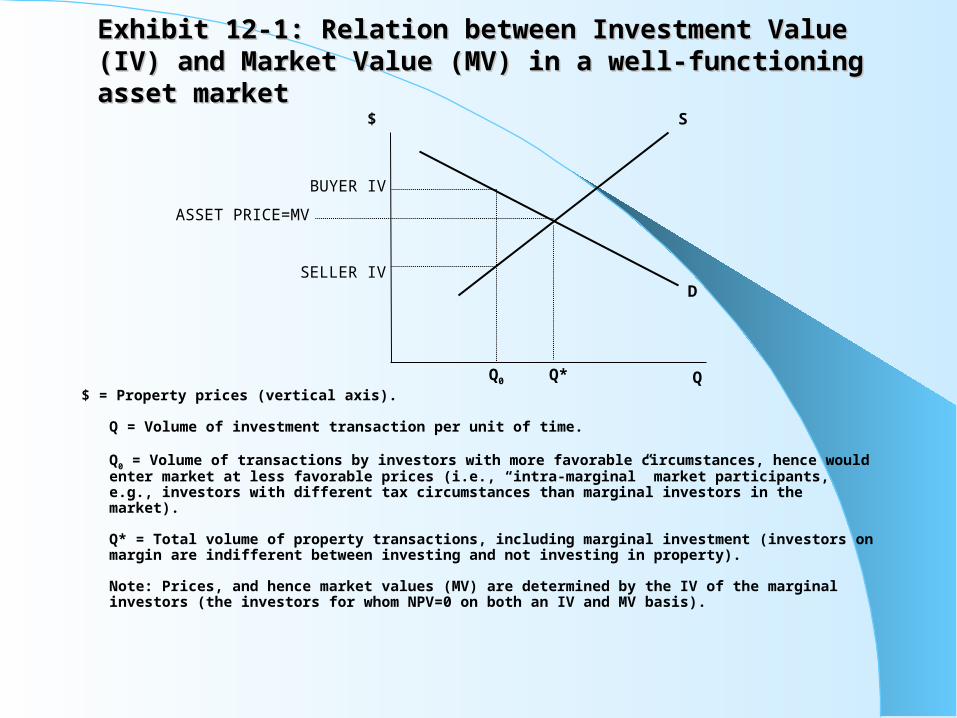

Exhibit 12-1: Relation between Investment Value Exhibit 12-1: Relation between Investment Value (IV) and Market Value (MV) in a well-functioning (IV) and Market Value (MV) in a well-functioning asset marketasset market

$ = Property prices (vertical axis). Q = Volume of investment transaction per unit of time. Q0 = Volume of transactions by investors with more favorable circumstances, hence would enter market at less favorable prices (i.e., “intra-marginal” market participants, e.g., investors with different tax circumstances than marginal investors in the market). Q* = Total volume of property transactions, including marginal investment (investors on margin are indifferent between investing and not investing in property). Note: Prices, and hence market values (MV) are determined by the IV of the marginal investors (the investors for whom NPV=0 on both an IV and MV basis).

BUYER IV

SELLER IV

ASSET PRICE=MV

D

S

Q

$

Q*Q0

Thus, General Condition to Thus, General Condition to allow NPV>0 …allow NPV>0 …It’s based on IV, not MV, and

It requires “uniqueness” (“intra-marginalness”)... For marginal investors: IV=MV.

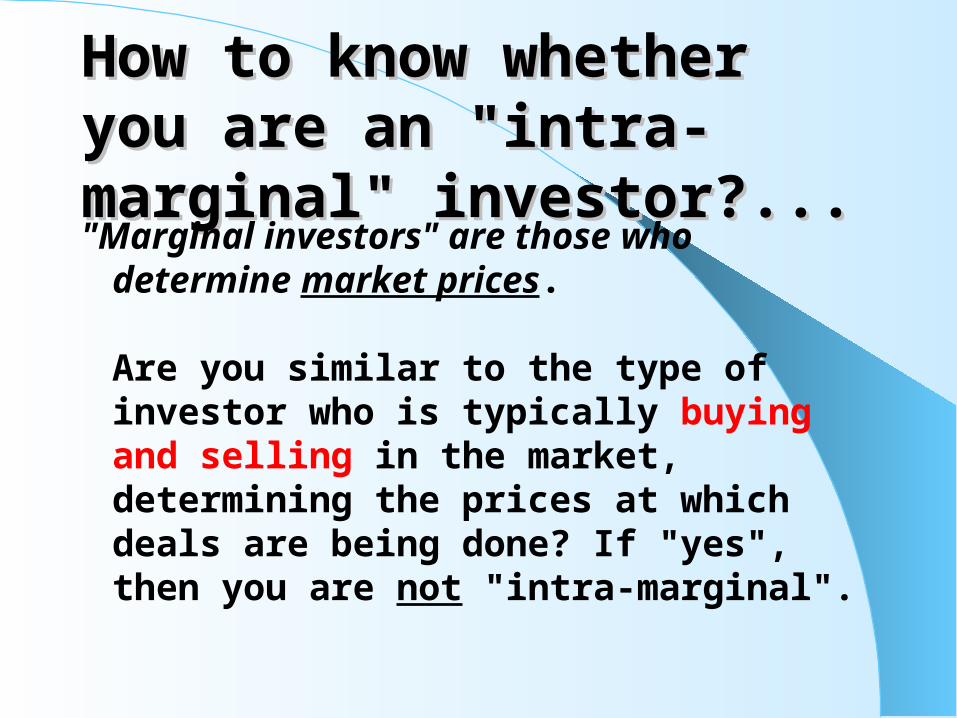

How to know whether you How to know whether you are an "intra-marginal" are an "intra-marginal" investor?...investor?..."Marginal investors" are those who

determine market prices. Are you similar to the type of investor who is typically buying and selling in the market, determining the prices at which deals are being done? If "yes", then you are not "intra-marginal".

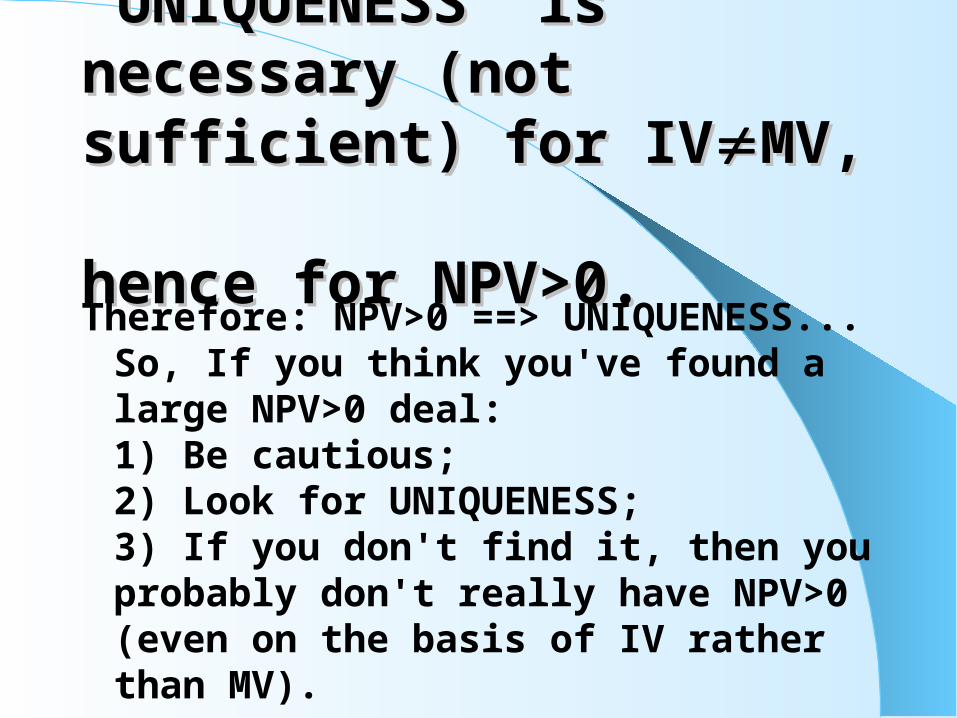

"UNIQUENESS" is "UNIQUENESS" is necessary (not sufficient) necessary (not sufficient) for IVfor IVMV, MV, hence for NPV>0.hence for NPV>0.Therefore: NPV>0 ==> UNIQUENESS...

So, If you think you've found a large NPV>0 deal:1) Be cautious;2) Look for UNIQUENESS;3) If you don't find it, then you probably don't really have NPV>0 (even on the basis of IV rather than MV).

How to measure Investment How to measure Investment Value:Value:Use long-horizon DCF

With “personalized” cash flows (e.g., after-tax), But discounted @ market-based discount rate, derived from observation of the capital market (because that is the OCC).

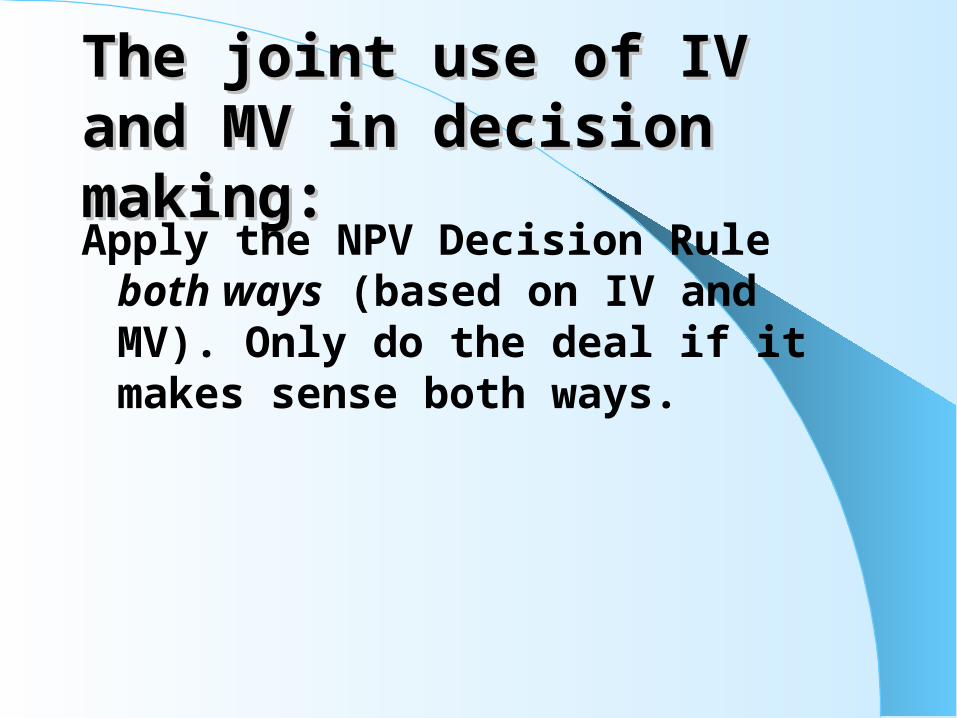

The joint use of IV and MV The joint use of IV and MV in decision making:in decision making:Apply the NPV Decision Rule both ways

(based on IV and MV). Only do the deal if it makes sense both ways.

Danger and Opportunity in Danger and Opportunity in Market Inefficiency...Market Inefficiency...Private real estate asset markets are less

“informationally efficient” than public securities markets. “Noisy prices” & inertia in asset market values.

DangersDangers::

IN REAL ESTATE INVESTMENT IN THE DIRECT (PRIVATE) PROPERTY MARKET, IT IS POSSIBLE TO DO DEALS WITH SUBSTANTIALLY POSITIVE, OR NEGATIVE, NPVs, MEASURED ON THE BASIS OF MARKET VALUE. REAL ESTATE MARKETS MAY TEND TO BE “BUBBLY” OR “CYCLICAL”. YOU CAN GET STUCK BUYING HIGH AND BEING FORCED TO SELL LOW.

OpportunitiesOpportunities::

DO YOUR “HOMEWORK” WELL, NEGOTIATE SMARTLY, YOU MAY GET A DEAL AT POSITIVE NPV. ANALYZE THE MARKET TO USE ITS PREDICTABILITY TO BUY LOW & SELL HIGH, BY AVOIDING FORCED SALES, E.G., BY RETAINING LIQUIDITY (HOW?).

Noise & Values in Private Noise & Values in Private R.E. Asset Mkts: R.E. Asset Mkts: Basic Valuation Theory…Basic Valuation Theory…

Exhibit 12-3a:Exhibit 12-3a:

Inherent Values

Fre

qu

en

cy

Buyers Sellers

A B C D E

Exhibit 12-3b:Exhibit 12-3b:

Fre

qu

en

cy

Buyers Sellers

Dualing Asset Markets Dualing Asset Markets (Public & Private):(Public & Private):The REIT Mkt vs the Private Direct Mkt

for Property…

The exhibit displays the NAREIT share price level index and NCREIF appreciation level index, both de-trended and normalized to have average value of zero and standard deviation of one.

-2

-1

0

1

2

3

78 80 82 84 86 88 90 92 94 96 98

NCREIF NAREIT

Exhibit 12-2: NAREIT vs NCREIF Asset Exhibit 12-2: NAREIT vs NCREIF Asset Values & Cash Flows (All indices set to Values & Cash Flows (All indices set to average value = 1)average value = 1)

Exhibit 12-2:NAREIT vs NCREIF Asset Values & Cash Flows

(All indices set to average value = 1)

0.6

0.8

1.0

1.2

1.4

1.6

81 83 85 87 89 91 93 95 97

NCREIF Value (unsmoothed) NAREIT Value (unlevered)

NCREIF CF (NOI) NAREIT CF(unlevered div.)Source: Authors’ estimates based on NAREIT Index and NCREIF Index. (NCREIF cash flows are based on NOI, NAREIT cash flows are based on dividends paid out.)

Chart 3:History of REIT "Growth Opportunities":

"Accretion Potential" measured by: (Publ.Val-Priv.Val) / Priv.Val, Based on Chart 2

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

74 76 78 80 82 84 86 88 90 92 94 96 98