chapter 16 efficient and equitable taxation copyright © 2010 by the mcgraw-hill companies, inc. all...

TRANSCRIPT

CHAPTER 16

Efficient and Equitable Taxation

Copyright © 2010 by the McGraw-Hill Companies, Inc. All rights reserved.McGraw-Hill/Irwin

16-2

Optimal Commodity Taxation

w(T – l) = PXX + PYY

wT = PXX + PYY + wl

wT = (1 + t)PXX + (1 + t)PYY + (1 + t)wl

1 wT = PXX + PYY + wl 1 + t

16-3

The Ramsey Rule

X per year

PX

DX

P0

X0

c

P0 + uXb

X1

∆X

a

ExcessBurden

P0 + (uX + 1) f

X2

i

∆x

ej

h

g

MarginalExcessBurden

marginal excess burden = area fbae = 1/2∆x[uX + (uX + 1)] = ∆X

16-4

The Ramsey Rule Continued

change in tax revenues = area gfih – area ibae = X2 – (X1 – X2)uX

marginal tax revenue = X1 ∆X

marginal tax revenue per additional dollar of tax revenue = ∆X/(X1 - ∆X)

marginal tax revenue per additional dollar of tax revenue for good Y = ∆Y/(Y1 - ∆Y)

To minimize overall excess burden = ∆X/(X1 - ∆X) = ∆Y/(Y1 - ∆Y)

therefore X

X

Y

Y1 1

16-5

A Reinterpretation of the Ramsey Rule

t

tX

Y

Y

X

inverse elasticity rule

t tX X Y Y

16-6

The Corlett-Hague Rule

• In the case of two commodities, efficient taxation requires taxing commodity complementary to leisure at a relatively high rate

16-7

Equity Considerations

• Equity implications of inverse elasticity rule

• Vertical equity

• Optimal departure from Ramsey Rule

16-8

Application: Taxation of the Family

• Under federal income tax law, fundamental unit of income taxation is family

• Is excess burden minimized by taxing each spouse’s income at same rate?

• Should husbands face higher marginal tax rates than wives?

16-9

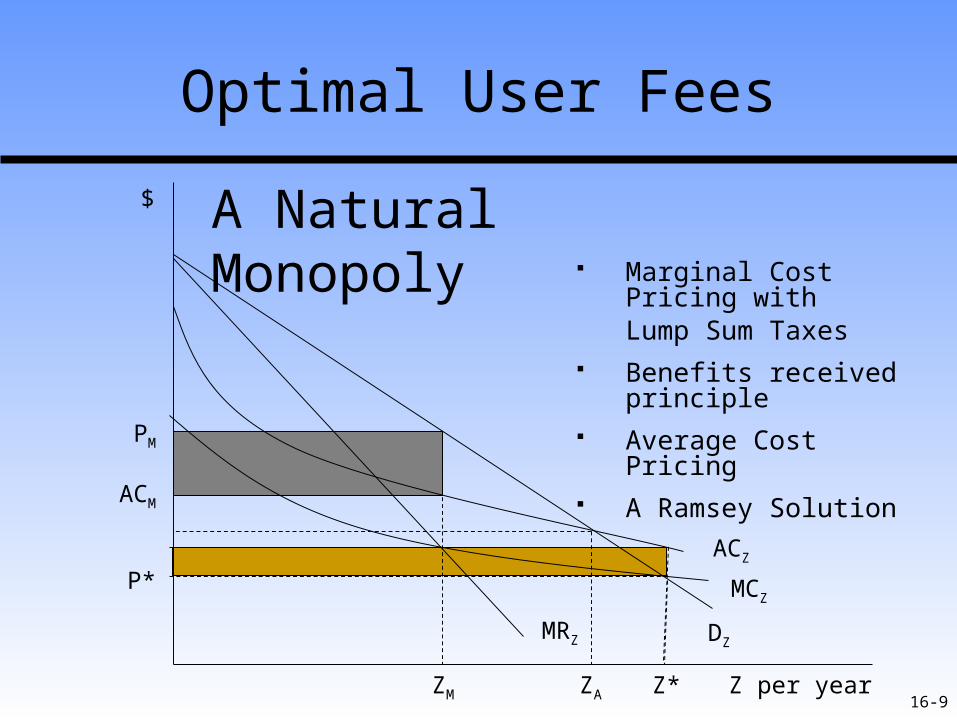

Optimal User Fees

Z per year

$ A Natural Monopoly

DZMRZ

ACZ

MCZ

ZM

PM

ACM

Z*

P*

ZA

Marginal Cost Pricing withLump Sum Taxes

Benefits received principle Average Cost Pricing A Ramsey Solution

16-10

Optimal Income Taxation-Edgeworth’s Model

• W = U1 + U2 + … + Un

• Individuals have identical utility functions that depend only on their incomes

• Total amount of income fixed

• Implications of model for income tax

16-11

Optimal Income Taxation-Modern Studies

• Supply-side responses to taxation

• Linear income tax model (flat income tax)

– Revenues = -α + t * Income

• Stern [1987]

• Gruber and Saez [2002]

IncomeT

ax R

even

ue

α = lump sumgrant

t = marginaltax rate

16-12

Politics and the Time Inconsistency Problem

• Public choice analysis of tax policy

• Time inconsistency of optimal policy

16-13

Other Criteria for Tax Design

• Horizontal equity– Utility definition of horizontal equity

• Transitional equity– Rule definition of horizontal equity

16-14

Costs of Running the Tax System

• Costs of administering the income tax in the U.S.

• Types of costs– Compliance– Administration

16-15

Tax Evasion

• Evasion versus Avoidance

• Policy Perspective: Architectural Tax Avoidance

• Methods of tax evasion– Keeping two sets of books– Moonlight for cash– Barter– Deal in cash

16-16

Positive Analysis of Tax Evasion

(Dollars of underreporting)(Dollars of underreporting)

$ $MC = p * marginalpenalty

MC = p * marginalpenalty

MB = tMB = t

R* R* = 0

16-17

Costs of Cheating

• Psychic costs of cheating

• Risk aversion

• Work choices– Underground economy

• Changing Probabilities of Audit

16-18

Normative Analysis of Tax Evasion

• Tax evaders given weight in the social welfare function

• Tax evaders given no weight in the social welfare function– Expected marginal cost of cheating = penalty rate

* probability of detection– Probability of detection = f (resources devoted to

tax administration)– Draconian vs. just retribution penalties