chapter iv results and discussion 4.1. results and...

TRANSCRIPT

74

CHAPTER IV

RESULTS AND DISCUSSION

4.1. Results and Discussion

This chapter will present the results of the design of the student loan

framework in Indonesia, which is focused on 3 parts, the objectives, student

loan scheme, and the repayment model of student loans. The results of this study

are based on the results of interviews conducted with 2 expert informants, Mr.

Angga E Hanafie who is given the initials AH as representatives of Mandiri

Bank and Mr. Dendi Permana who is given the initial DP as a representative of

CIMB Niaga Bank. This research is also supported by regulations issued by

Bank Indonesia and OJK, and scientific journals. So hopefully this research can

be resourceful and useful for further research.

The design of the results of this study refers to interview result and scientific

journals on student loans that have been implemented in other countries which

are focused on 5 Asian countries especially China, Hong Kong SAR, Republic

of Korea, The Philippines, and Thailand and in the process will be adjusted to

the situation in Indonesia so that the design can be feasible and applicable. The

schemes used by other countries become the main source of this research so that

the schemes are known the weakness and the strength.

This chapter will be discussed in 3 points, first, the purpose of student loans

which will discuss various program objectives and the application of objectives

in 5 Asian countries. Second, the student loan scheme will be discussed

75

regarding the scheme that can be used in Indonesia by taking into account the

banks and the students perspective, therefore, the scheme could be implemented

in Indonesia. Third, repayment models which will discuss models that can be

used by the public without bearing the banking risk.

4.2.The Objective of Student Loan

The purpose to form a program, of course, there is the ultimate goal of the

program. This goal is fundamental because it influences the design and

operation of the study in this student loan scheme. Student loans which are

currently not yet implemented in Indonesia must have clear objectives so that

the program can be made effectively and efficiently. Based on the experience

of other countries that have implemented student loans, there can be identified

5 objectives of making student loans, that are budgetary objectives, facilitating

higher education expansion, social objectives, manpower needs, and easing

student's financial burdens.

1. Budgetary Objectives

Public universities throughout the world and especially in

developing countries are under-financed. A tight government budget can

lead to under-financed general public universities. Based on A. Ziderman

(2004) this can be caused by several reasons. First, additional government

funding for universities may not be available so that universities do not have

the ability to maintain the level of enrolment and quality in the face of rising

costs. Second, cuts from government spending specifically to tertiary

76

education will put pressure on universities to seek alternative funding.

Third, many countries have adopted policies that support basic education

rather than tertiary education which leads to the reallocation of funding from

tertiary education to funds education which has a higher social rate of return.

Tightening the budget has caused public universities to shift to

greater cost recovery, in their efforts to utilize alternative funding sources.

This may require more realistic tuition fees for the services received.

Turning to the banking system in an effort to make routine loans so as to

ease the burden of payments may not be available because the banking

sector is very difficult to lend to education. In this case, the government can

encourage student loan programs through relief in terms of interest rates so

that these loans can be done by the public and can feel higher education.

2. Facilitating Higher Education Expansion

The government responds to increased social demand for higher

education through policies that lead to an increase in the number of students

participating in education; however, due to limited public budget, the

growth in the number of student participation cannot be followed by

proportionate additional government funding. Responding to increased

social demand for education expansion will require an increase in

expenditure on the public budget, especially in higher education which is

quite large.

The step that can be considered is to encourage the growth of private

higher education. Students pay full fees at private universities, by not putting

77

a heavy burden on the public budget. However, the cost of education in

private universities tends to be large and beyond the reach of society,

especially the lower middle class. Student loans may be the answer in easing

the burden of tuition fees at private universities, especially if private

universities can be open to all society classes.

3. Social Objectives

In many countries, the low participation of young people whose low

economic background in education, which is not compulsory such as

college, is a social problem; improving access to universities for this group

has become a concern in determining policies in the education and social

areas. There is a consensus that clear financial incentives need to be offered,

not only to overcome the burden of making payments and living expenses

but also to balance the ability of parents to reduce the risk of family income

and the risk that the benefits of the educational process may not be large

enough.

The traditional, and most effective, method of increasing access to

education for the underprivileged is through the provision of grants or

scholarships to cover school fees and usually living costs as well. However,

massive grants schemes are likely to be very expensive; the use of loans

rather than grants offers a method that increases access for the wider

disadvantaged group and reduces or uses less public budget expenditure in

the long run, along with increased loan payments. To be effective in

increasing access to education for disadvantaged groups, loans must be

78

made with attractive packaging. Therefore, justification is made for

subsidized loans, in the case of a grace period for payments, the interest

charged below the market interest rate, and payments will not be directly

related to inflation. Loan schemes intended to help disadvantaged groups

must be designed in such a way as to reach this group, otherwise, the main

purpose of the scheme will be lost.

4. Manpower Needs

Student loan schemes can be specifically aimed at providing support

for students who are willing to study in a department or special expertise

that is being prioritized by the state due to the need for expertise or work for

the benefit of the national or other social projects

5. Easing Students Financial Burdens

This goal is more directed towards developed countries. Although

the burden for tuition fees is minimal, it is not impossible that the student's

family faces another heavy financial burden. Such expenses may occur due

to potential income or even those that fixed income lost during the study

period, a large educational burden due to studying in locations far from

home both outside the region, islands, or abroad. Financial pressures, which

may have a negative effect on learning outcomes student, can be reduced by

the wide availability of student loans. Such a burden may be more on the

less capable group, but the point is that this loan can be available to all

students both for the able and disadvantaged groups. Even so, there needs

79

to be an adjustment between the able and disadvantaged groups so that the

use of subsidies to ease the financial burden will not be wrongly targeted.

A clear division can be made by dividing goals number 1 and 2 as well as

goals from numbers 3-5. The goals of the first group, number 1 and 2, prioritize

university income due to tight funding from the government and in order to

increase social demand in higher education. Whereas in the second group's goal

number 3-5 it is not specifically concerned in university funding, but a broader

approach that is social perspective.

“Kalau ada metode jaminan yang tadi (tahan ijazah dan deposit) benefitnya

apa buat kampus? Ini lower admin fee dan fresh money dengan syarat ada

jaminan.” -DP.

With the existence of fresh money as a result of the implementation of

student loans, the campus can use these funds for development purposes or to

increase the ability of the university to social demand from the society. So that

the society's need for universities will be more fulfilled let alone supported by

funding that helps students access tertiary education.

Most of the student loan schemes use high amounts of subsidies, especially

in developing countries. However, the existence of these subsidies cannot be

sufficiently justified because the purpose of the loan is full loan recovery. Loan

schemes aimed at people who cannot afford to be made an exception as a way

to facilitate particular manpower shortages. It is noted that for purposes number

1 and 2 must be limited to students enrolling in public universities unless this

80

loan is made specifically for private universities. However, to achieve goal

number 3-5, loans must be available to both public and private students in the

context of equality.

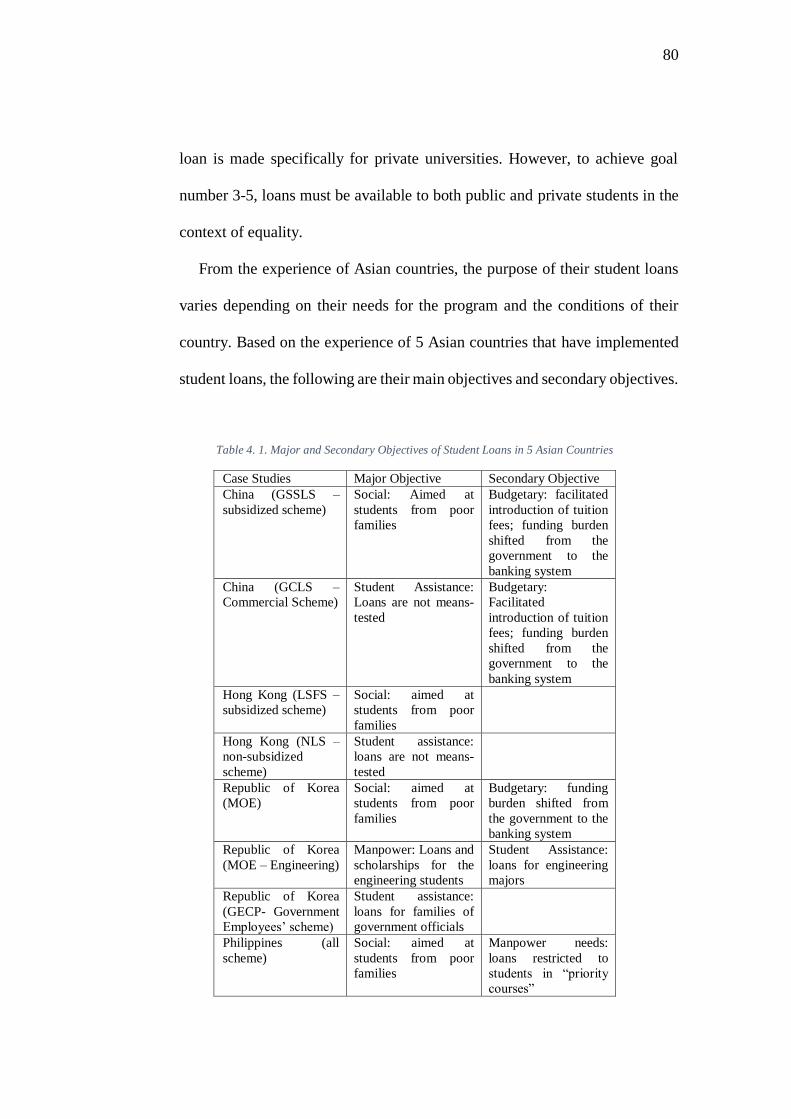

From the experience of Asian countries, the purpose of their student loans

varies depending on their needs for the program and the conditions of their

country. Based on the experience of 5 Asian countries that have implemented

student loans, the following are their main objectives and secondary objectives.

Table 4. 1. Major and Secondary Objectives of Student Loans in 5 Asian Countries

Case Studies Major Objective Secondary Objective

China (GSSLS –

subsidized scheme)

Social: Aimed at

students from poor

families

Budgetary: facilitated

introduction of tuition

fees; funding burden

shifted from the

government to the

banking system

China (GCLS –

Commercial Scheme)

Student Assistance:

Loans are not means-

tested

Budgetary:

Facilitated

introduction of tuition

fees; funding burden

shifted from the

government to the

banking system

Hong Kong (LSFS –

subsidized scheme)

Social: aimed at

students from poor

families

Hong Kong (NLS –

non-subsidized

scheme)

Student assistance:

loans are not means-

tested

Republic of Korea

(MOE)

Social: aimed at

students from poor

families

Budgetary: funding

burden shifted from

the government to the

banking system

Republic of Korea

(MOE – Engineering)

Manpower: Loans and

scholarships for the

engineering students

Student Assistance:

loans for engineering

majors

Republic of Korea

(GECP- Government

Employees’ scheme)

Student assistance:

loans for families of

government officials

Philippines (all

scheme)

Social: aimed at

students from poor

families

Manpower needs:

loans restricted to

students in “priority

courses”

81

Thailand Social: aimed at

students from poor

families

University expansion:

subsidized students in

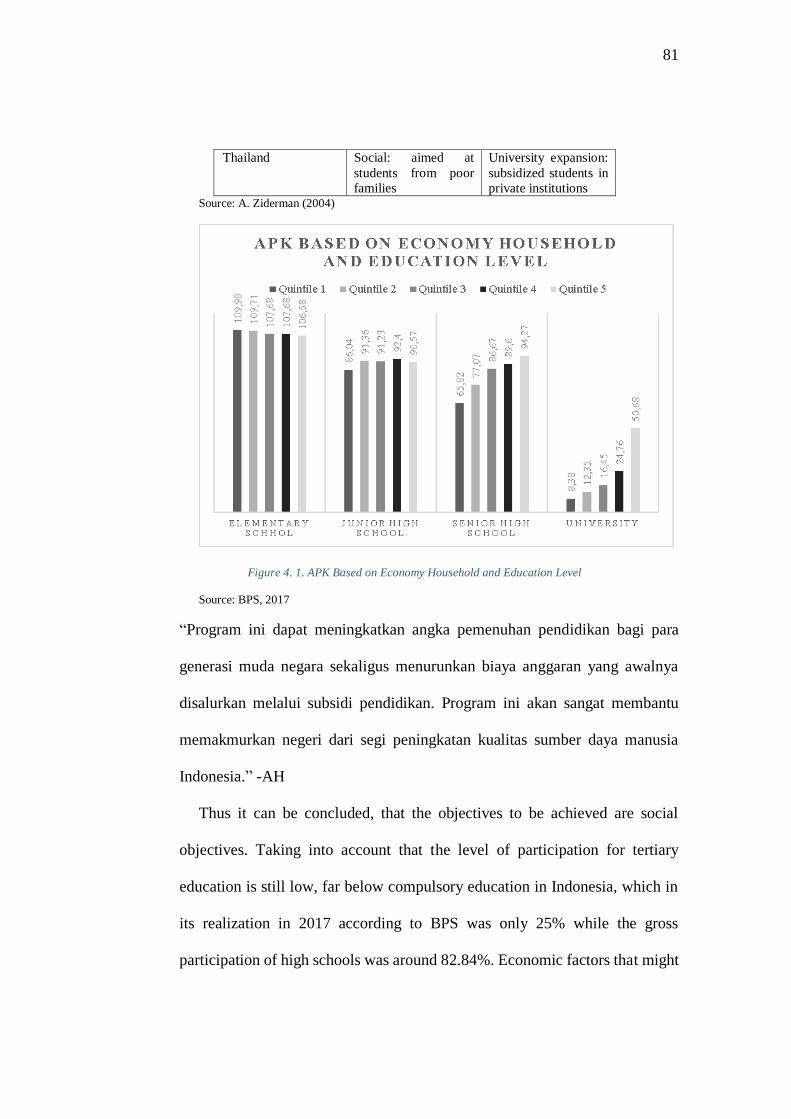

private institutions Source: A. Ziderman (2004)

Figure 4. 1. APK Based on Economy Household and Education Level

Source: BPS, 2017

“Program ini dapat meningkatkan angka pemenuhan pendidikan bagi para

generasi muda negara sekaligus menurunkan biaya anggaran yang awalnya

disalurkan melalui subsidi pendidikan. Program ini akan sangat membantu

memakmurkan negeri dari segi peningkatan kualitas sumber daya manusia

Indonesia.” -AH

Thus it can be concluded, that the objectives to be achieved are social

objectives. Taking into account that the level of participation for tertiary

education is still low, far below compulsory education in Indonesia, which in

its realization in 2017 according to BPS was only 25% while the gross

participation of high schools was around 82.84%. Economic factors that might

82

be a barrier for prospective students are evidenced through low participation

from the lower middle class which is explained through figure 9 above.

Implementation of student loan may help to boost the participation rate for

tertiary education in particular for who are facing difficulities in economy.

4.3.Design of Student Loan Scheme

After the goal has been made, the next step is how the student loan system

is used. The system in question such as loan requirements and the amount or

scope to be used and questions that arise such as whether students pay the

burden of education while studying, whether private universities are allowed

into the scheme, whether financial assistance in reducing financial burdens for

university access is available both publicly and private sector, etc. This can be

answered if the design for student loans has been made. To make a good design,

of course, it must be adjusted to the conditions of Indonesia as well as taking

into account feasibility and applicable for Indonesia.

The combination of institutions to divide responsibility for different

administrative functions might leverage the outcome of the program.

University/colleges/other educational institutions may be given responsibility

for selection of borrowers and commercial banks may actually provide the

loans and collect repayments. The justification for those roles is that

commercial banks may have considered as institution who expertise in the

management of loan and collection of repayment, but little knowledge of

education system, while education institution may well have equipped to make

83

academic judgments, but less experienced in judging financial need, and not at

all experienced in administering and controlling loans.

In discussing this design, it will be divided into several perspectives,

especially banking and students.

4.3.1. Student Loan Perspective for Banking

OJK and BI regulations as a guide of bank performance are binding

regulations on banks and must be obeyed. This regulation is important

because financial institutions are known as highly regulated institutions

because the risks faced can cause turbulence in one country to an economic

crisis. Therefore, clear rules regarding financial institutions are needed so

that preventive and coercive measures can be made if there are indicators

that have crossed the threshold.

In the student loan program, banks become important as one of the

institutions that can disburse funds for educational loan needs, although

not all countries use banks as a source of funds because there are countries

that use the government as a source of funds. Assuming the scheme to be

used will become a mass program, great funds are needed that can

guarantee the bank can provide money to borrow but has the ability to pay

its obligations (interest rates for savings and deposits).

The use of banks instead of autonomous bodies or government

institutions is because the banks are more efficient. According to Albrecht

(1993), there are 3 good reasons to rely on the private sector to run student

loan program:

84

1. The government doesn’t have to make initial capital outlays

2. Private sector efficiencies may reduce the cost of loan program

3. The government doesn’t have to create a potentially costly

administrative apparatus to operate the program

The capital which is provided by banks is coming from private investors

rather than the government. With this current system, it will reduce the

financial burden on the public budget. The government doesn’t finance the

program directly, but they try to provide the cost of guaranteeing the loans

against the default and subsidizing the borrowers and lenders. In the USA

students borrowed over $9 billion in 1985-6, but the total cost to the

Federal Government was only one-third of this, at $3.2 billion

(Woodhall,1987).

Loans are also closely related to the risk. The risk faced by the bank

besides being unable to provide funds due to a lack of funding may be the

risk of default on the loan. These risks must be mitigated by banks in

collaboration with OJK as supervisors so that these risks do not affect the

bank. The following is a student loan financial scheme both in terms of

function and institution from 5 Asian Countries

Table 4. 2. Student Loan Financial Scheme from 5 Asian Countries

Case Study Capital

Provision

Loan Subsidies

(Interest rates,

etc.)

Risk-Bearing

China (GSSLS-

Subsidized

Scheme)

State-owned

Commercial

Banks

Government Banks

China (GCLS-

Commercial

Scheme)

Commercial

Banks

None Parental Asset

(Collateral)

85

Hong Kong

(LSFS-

Subsidized

Scheme)

Government

Budget

Government Government,

Parents

Hong Kong

(NLS-Non-

Subsidized

Scheme)

Government

Budget

None None: Risk factor is

incorporated in the

interest rate

Republic of

Korea (MOE)

Commercial

Banks

Government Government,

Students/Parents

Republic of

Korea (GECP-

Government

Employees’

Scheme)

Government

(previously,

government

employees

pension scheme)

Government Government,

Parents

Philippines

(Study Now Pay

Later)

Government

budget

(previously,

government

financing

institution)

Government Government

Philippines

(Region 5)

Government

Budget

Government Government

Philippines

(Centres of

Excellences)

Government

Budget

Government Government, Co-

Signatory

Thailand Government

Budget

Government Government,

Parents Source: A. Ziderman (2004)

Thus in this point, there will be some discussion on the perspective of

student loans for banks including, the first, function of OJK supervision of

banks which will be discussed about OJK supervision and regulation of

banking activities, especially in the health level of bank and risk

management. Second, the banking cash flow scheme which will be

discussed regarding the system of cash inflow and outflow from a banking

perspective.

4.3.1.1. OJK Supervision Function on Banks

The Financial Services Authority (OJK) is an institution

that functions as a provider of an integrated regulation and

86

supervision system for all activities in the financial services sector.

One of the financial services sectors that are regulated and

supervised by OJK is banking. This task was initially under the

authority of BI but after the issuance of Undang-Undang number

21 /2011 the authority was transferred to OJK while BI was more

focused on the monetary sector.

According to Kasmir (2014), as an institution that carries

out regulation and supervision in one of them, especially banking,

OJK has several authorities, especially

1. Regulations and supervision of bank institutions

which include

a. Permits for the establishment of banks, opening

bank offices, statute, work plans, ownership,

management, and human resources, mergers,

consolidations and acquisitions of banks, and

revocation of bank business licenses

b. Bank business activities, including sources of

funds, provision of funds, hybrid products, and

activities in the service sector

2. Regulations and supervision regarding bank health

including

87

a. Liquidity, profitability, solvency, asset quality,

minimum capital adequacy ratio, maximum lending

limit, loan to deposit ratio, and bank reserves

b. Bank statements related to bank health and

performance

c. Debtor information system

d. Credit testing

e. Bank accounting standards

3. Regulations and supervision regarding bank

prudential aspects, including:

a. Risk management

b. Bank governance

c. “Know your customer” principle and anti-money

laundering

d. Prevention of financing terrorism and banking

crime

4. Bank inspection

In its authority, OJK issued several regulations concerning

bank health that must be followed by banks as stated in POJK No.4

/ POJK.03 / 2016 concerning the evaluation of the health of

commercial banks and described in more detail in OJK Circular

Letter Number 14 / SEOJK.03 / 2017 along with the attachments.

This regulation explains that banks and OJK are required to

88

conduct bank health assessments both consolidated and

individually. The assessment of bank health uses a risk-based bank

rating approach with the following coverage:

1. Risk Profile

2. Good Corporate Governance

3. Earnings

4. Capital

If in the assessment conducted by the OJK, in this case,

the OJK assessment will be used if there is a difference with the

results of the health assessment by the bank, the bank is required to

submit an action plan in accordance with applicable regulations.

Banks that violate rules, there are already written regulation

regarding sanctions to be taken from written sanctions to the

suspension of certain business activities.

4.3.1.2.Banking Cash Flow Scheme

One of the country's economic movements is driven by credit

growth through banks. The growth of bank credit cannot be separated

from the contribution of the growth of third party funds as the main

source of bank funding. The importance of the presence of bank credit

in moving the national economy requires funds obtained through funds

from the public collected through demand deposits, savings, and

deposits. Banks as financial institutions that have operations in the sale

and purchase of money that has the meaning of buying, especially

89

collecting funds and selling, providing loans, but before it is sold, of

course, what is needed is to buy money (raise funds) first. Sources of

bank income according to Dr. Kasmir (2014) includes

1. Funds sourced from the bank itself

The source of these funds from their own capital. The

definition of own capital is the capital of its shareholders. Broadly

speaking, it can be concluded that the fundraising itself consists of:

a. Capital contribution from shareholders

b. Bank reserves, which means the reserves of profit last year that

are not shared with shareholders. This reserve is intentionally

provided to anticipate future profit

c. Bank profit that has not been shared is the profit that has not been

distributed in the year concerned so that it can be used as capital

for a while

2. Funds coming from society

This source of funds is the most important source of funds

for bank operations and is a parameter of the success of the bank if

it is able to finance its operations through this source. This funding

source is the easiest to do and is the dominant source of funds with

the condition that interest and attractive facilities for the society.

Nevertheless, this funding source is a relatively expensive source

of funds compared to other funding sources. The source of funds is

coming from:

90

a. Current account (demand deposits)

b. Savings (saving deposit)

c. Deposits (time deposits)

The division of types of deposits into several types is

designed so that the depositors have choices in accordance with

their respective goals. Types of deposits such as demand deposits

are designed to facilitate payment, especially consumers who are

business people even though the interest generated is not as large

as other deposits. Savings deposits and deposits can generate large

interest. Although deposits (time desposits) have some limitation

in withdrawing funds, it generates greater interest.

3. Funds sourced from other institutions

This third source of funding is additional if the bank faces

difficulties in finding the first and second sources of funds. Sources

of funds through fundraising other institutions are relatively more

expensive and are only temporary. The funds provided are also

only used to finance or pay certain transactions. Obtaining funds

from this source can be obtained from:

a. Liquidity credit from Bank Indonesia is credit given by Bank

Indonesia to banks who are experiencing liquidity problems. This

liquidity credit is also given to financing certain sectors

91

b. Interbank loans are usually given to banks that have lost clearing

within the clearinghouse. This loan is short term and relatively

expensive

c. Loans from foreign banks are loans obtained by banks from

foreign parties

d. Money Market Securities (SBPU) in this case the banks' issue

SBPU and then traded to interested parties, both financial and non-

financial companies.

After the process of collecting funds has been completed, the next

step is to distribute the funds back to the people who need them. This

activity is known as fund allocation. Allocating funds other than in the

form of loans can also be in the purchase of assets that are considered

beneficial to the bank.

Bank profits come from the difference, the difference between the

interest given from the funds received and the interest received from the

allocation of funds. So that the determination of the source of funds is

a very influential interest in the allocation of funds to be charged.

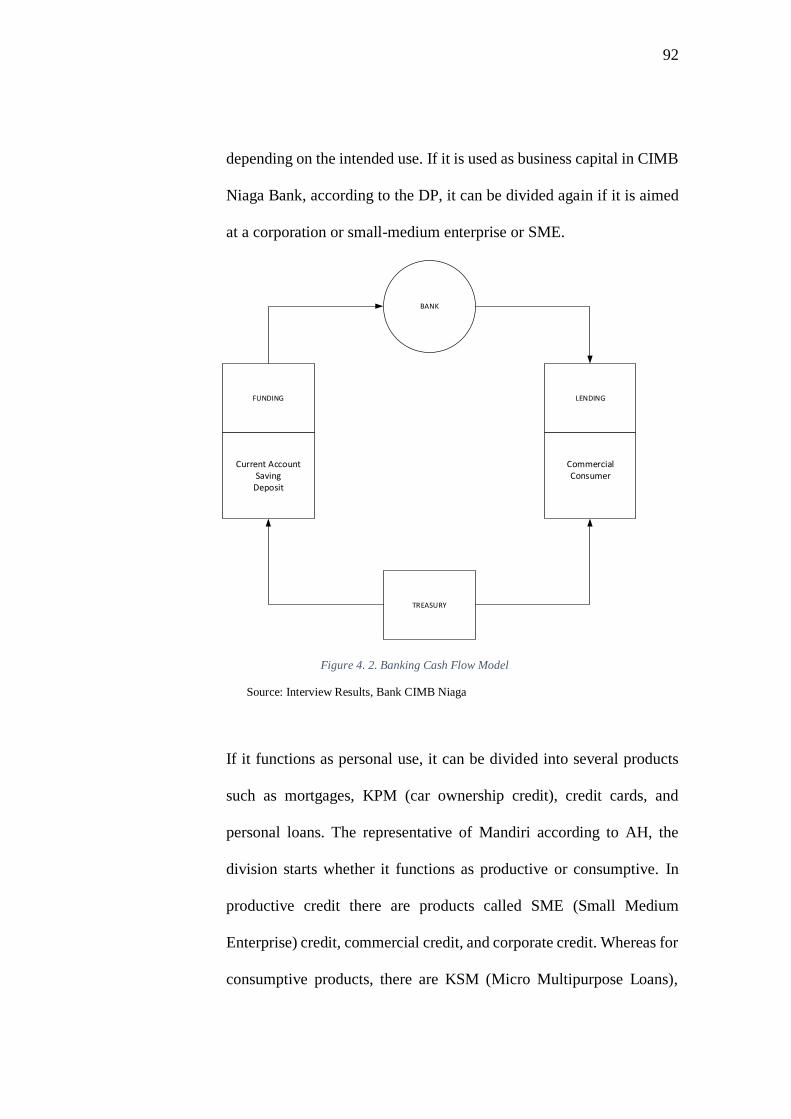

Based on the explanation above with interview results, it can be

concluded that the banking cash flow model can be drawn in figure 10

Sources of funds (funding) from the public consisting of current

accounts, savings, and deposits into the bank, then the funds will be

allocated to the form of credit or asset purchases. In the form of credit

(lending) will take the form of loans to commercial and consumer

92

depending on the intended use. If it is used as business capital in CIMB

Niaga Bank, according to the DP, it can be divided again if it is aimed

at a corporation or small-medium enterprise or SME.

BANK

FUNDING LENDING

TREASURY

Current AccountSaving

Deposit

CommercialConsumer

Figure 4. 2. Banking Cash Flow Model

Source: Interview Results, Bank CIMB Niaga

If it functions as personal use, it can be divided into several products

such as mortgages, KPM (car ownership credit), credit cards, and

personal loans. The representative of Mandiri according to AH, the

division starts whether it functions as productive or consumptive. In

productive credit there are products called SME (Small Medium

Enterprise) credit, commercial credit, and corporate credit. Whereas for

consumptive products, there are KSM (Micro Multipurpose Loans),

93

KPR (Mortgages), Multipurpose Mortgages, and KKB (Motorized

Vehicle Loans). According to the DP, inflows and outflows of funds are

regulated by treasury whereby if the funds collected and allocated have

reached the LFR (Loan to Funding Ratio) then if there is a request for

allocation of large funds that come in, a request to the Funding division

is needed to find ways to increase the pool of funds from the public.

Based on Bank Indonesia regulation PBI number 19/06 / PBI / 2017

regarding Fifth Amendment to “Bank Indonesia Regulation number

15/15 / PBI / 2013 regarding Statutory Reserves for Commercial Banks

in Rupiahs and Foreign Currencies for Conventional Commercial

Banks” that LFR (Loan to Funding Ratio) designate that the amount in

the LFR statutory reserve calculation is with the lower limit of the target

LFR of 78% and the upper limit of the target LFR of 92% and the upper

limit of the Target LFR of 94% with conditions set by BI so that the

treasury of each bank must ensure that the LFR is still within safe

threshold.

94

Figure 4. 3. Credit Types in CIMB Niaga Bank

Source: Interview Results, CIMB Niaga Bank

Figure 4. 4. Credit Types in Mandiri Bank

Source: Interview Results, Mandiri Bank

Credit

CorporateMedium Small

EnterpriseConsumer

KPR

KPM

Credit Card

Personal Loan

Credit

Productive

SME

Corporate

Commercial

Consumptive

KSM

KPR

Multifunction KPR

KKB

95

Thus it can be concluded that if the student loan program will be

implemented in Indonesia with the bank as a source of funding, the bank

needs to assess the ability to raise funds before giving loans to large

amounts of students. Banks need to pay attention to the provisions

written in OJK and BI regulations as standard regulations that

absolutely must be followed. Banks must be prepared in addition to

preparing funds, must also be ready in terms of scoring and payment

mechanisms that will be discussed later. BUMN banks as agents of

changes are demanded to support government programs but do not

forget that bank stability must be prioritized so that economic activity

runs well. Although according to AH and DP, both are agreed that

student loan only requires a fragment of credit, significant number of

default rate could lead to a failure program or put heavy burden on

banks.

4.3.2. Student Loan Perspectives for Students

Credit is a facility needed by the society where the society can apply

for credit because it requires additional funds for their needs. In the

previous discussion, it was explained that banks have several credit

services that can be used by the public for various purposes. But what

about students who still don't have jobs who want to apply for credit for

education? At this point, several things will be discussed, first the

provision of credit where credit applications have several conditions that

must be met. Second, loan guarantees which will be discussed regarding

96

loan guarantees so that students can apply for credit without providing a

great risk to the bank. Third, the loan amount will be discussed how much

the loan can be given to student loan applicants.

4.3.2.1. Terms of Credit Provision

Before giving credit to society, there are conditions that must

be met by society. These requirements are required by the bank so

that the bank can find out whether the applicant is eligible to be

given credit or not. Requests for student loans will be different

compare other countries, especially in developing countries wherein

for example Indonesia, there is uncertainty that university graduates

can immediately hired so there need to be adjustments that can be

met by the public and the risk borne by banks is not large. Following

are the experiences of 5 Asian countries regarding student loan

arrangements in the income ceiling for eligibility in loans which is

described in figure 13.

According to the DP, the requirements that must be met in a

personal loan which is almost the same as a student loan are, the first

they should be Indonesian citizens, then aged 21 - 55 years when the

applicant registering is the student's parent or the party responsible

for the student, then the student's parents or guardians are working

or self-employed, after that the requirement is either, a CIMB Niaga

customer or non CIMB Niaga customer. For CIMB Niaga

97

customers, they must have a payroll which means the transferred

income must be to a CIMB Niaga account

Table 4. 3. Student Loan Arrangements in The Income Ceiling for Eligibility in Loans for 5 Asian Countries

Case Study (Loans

Scheme)

Eligibility How is the eligibility

income ceiling fixed

Who provides

certification of

declared family

income

China (GSSLS-

Subsidized Scheme)

Poor Students Local Government

Poverty Line

Local Authority

Hong Kong (LSFS-

Subsidized Scheme)

Poor Students Amount of loan

offered is in inverse

proportion to family

income and assets

The applicant provides

documentation such as

salary statement,

profit-and-loss

account, etc

Hong Kong (NLS-

Non-Subsidized

Scheme)

All Students n.a n.a

Republic of Korea

(MOE)

Poor Students Ministry of Education

(Eligibility ceiling is

above the poverty

line)

Educational

Institutions; Banks

Republic of Korea

(GECP-Government

Employees’ Scheme)

Government

employees and their

children

n.a n.a

Philippines (All

Schemes)

Poor Students Official Poverty Line Parents’ employer

Thailand Poor Students Loans Scheme Office

(Eligibility ceiling is

above the poverty

line)

Government official

(Level 4 and above);

village head

Source: A. Ziderman, (2004)

“Punya payroll, payroll itu adalah misalkan kalau kamu sudah kerja

rekening gajian kamu itu ditransfer sama perusahaan ke rekening

CIMB Niaga itu namanya pakai payroll.”-DP

Then the average daily balance savings of at least 10 million

rupiah means that even though they already have a CIMB Niaga

account, customers must also have an average of at least 10 million.

98

“tabungan ini harus saldo rata-rata harian minimum 10 juta jadi

meskipun sudah punya rekening CIMB Niaga tapi tiap bulannya

hanya satu juta tetap saja tidak bisa”-DP

Then there is a credit card. If it comes from another bank

customer, then the requirement is to have a bank credit card. If

applicant only have a payslip, then the application cannot be

processed because it is prone to fraud. After going through these

requirements, the application will be checked from internal checking

whether there has ever been a history of fraud and money laundering

through AML. Second, conduct an external checking which will

check financial transactions through the SLIK (Financial

Information Service System) owned by the OJK and verify the status

of the house and employment status. Third, do a loan assignment

where CIMB Niaga regulations apply a DBR of 65%, which means

that the total income per month is only allowed a maximum loan

installment of 65% of income. These criteria are described in figure

14.

“Hal ini memang menjadi tantangan terbesar untuk Bank. Namun

dapat disiasati dengan manajemen risiko dengan baik yaitu:

memberikan persyaratan tertentu kepada mahasiswa: misalnya

mensyaratkan minimum nilai dan IPK.

99

Indonesia Citizen

21 – 55 years old

Employee /

Entrepreneur

CIMB Niaga

Customer

Non-CIMB Niaga

Customer

- Payroll

- Minimum Average

Daily Balance

Savings at least 10

million

- CIMB Niaga Credit

Card

- Other Banks Credit

Card

Figure 4. 5. Requirements To Apply For Credit .

Source: Interview Results, CIMB Niaga Bank

Karena dapat menjadi salah satu parameter keseriusan mahasiswa

untuk belajar dan dapat berpengaruh dalam seberapa kompetitifnya

dia untuk mencari pekerjaan nantinya. Hal ini juga dapat menekan

angka peminjam yang terlalu besar dan sulit untuk dihandle. Selain

itu, mahasiswa harus berkomitmen untuk menyelesaikan studinya

maksimum selama 4 tahun, sehingga tidak memperpanjang tenor

kredit. Ini merupakan pendapat dari kita jika produk student loan

akan dijalankan, salah satu untuk do diligence adalah ada base figure

100

nya. Sehingga melalui IPK bisa dijadikan parameter untuk penilaian

pembiayaan. Salah satu do diligence adalah membiayai orang yang

memiliki prospektif baik salah satunya IPK, sama halnya dalam

perusahaan yang harus berdiri minimal 2 tahun, punya neraca dan

punya kinerja 2 tahun karena kalau belum 2 tahun, belum terlihat

apakah perusahaan tersebut bisa menghasilkan profit atau hanya

perusahaan yang mencoba-coba. “-AH

According to AH, to be able to apply student loans, it needs

good credit management and might be tricked with their academics

in terms of GPA and enrollment period, and their commitment on

the loan. These may help in making parameter for the financing

assessment.

4.3.2.2. Loan Collateral

Credit before being given to the applicant, the bank must be

confident that the credit given will really be returned. This belief can

be obtained through a credit rating before the credit is given. One of

the criteria in a credit rating is collateral.

Credit according to Dr. Cashmere (2014) can be provided

with or without collateral. Unsecured loans are relatively very

dangerous to the bank's position, considering that if the customer

experiences a traffic jam, it will be difficult to cover losses on the

101

credit extended. In contrast, a credit guarantee is relatively more

secure, given that any bad credit will be covered by the guarantee.

The emergence of collateral in loans such as student loans

will certainly be burdensome for students where the target of student

loans is to help students to be able to continue to tertiary educational

background. Families whose backgrounds are not able will certainly

find it difficult to provide collateral to banks because with large

amounts of loans there is no collateral owned to have a value that

can be used as collateral by the bank even if there will make the

family's position more difficult.

According to DP, the student loan program can run with

guarantees that must be met by the government, related universities,

and students.

“Ada dua misalnya pemerintah mengeluarkan deposit untuk

perguruan tinggi bisa menaruh deposito juga beserta dengan ijazah

SMA dan ijazah perguruan tinggi jika sudah lulus.”-DP

According to the DP, because guarantees cannot be

requested to families who are less able or there are no guarantees

whose value is the same as the amount of credit requested, students,

must submit their high school diploma to the university as a

guarantee that the student will attend the lecture process from start

to finish and reduce the risk of switching universities. While their

university diploma will be held until the obligation to repay credit

102

has been made all. The government and universities need to send

deposits to banks as collateral so that if there are students who do

not pay, the bank has the authority to take deposits deposited to the

bank.

“Jaminan yang rasional menurut saya adalah adanya reference

minimal tiga orang dari orang tua, guru, keluarga atau kerabat dari

yang bersangkutan untuk menjamin karakter dan komitmen

mahasiswa tersebut. Sehingga dapat menambah keyakinan Bank

untuk memberikan student loan.”-AH

According to AH, a guarantee which according to him is

rational is the recommendation from the closest person to guarantee

that the student will pay. It could add confidence for the banks to

provide the loans.

4.3.2.3. Loan Amount

The number of loans for credit varies depending on the

intended use. According to the DP, the number of loans used for

corporations will vary.

“Biasanya TBK (perusahaan terbuka) pinjamnya ratusan miliar

kalau perusahaan biasa biasanya lebih dari 1 miliar tergantung size

nya saja.”-DP

103

If it intends for consumers, it depends on their needs such as

buying a house, car, education, health, and others. Similar to student

loans, the number of loans will depend on their educational needs.

According to AH, the amount of student loan should be

limited according to tuition and books.

“Plafon kredit diberikan maksimum hanya berupa tuition fee dan

biaya buku saja. Melihat biaya SPP di beberapa universitas negeri di

Indonesia yang relative rendah, maka limitnya harus diberikan batas

maksimum untuk mengurangi risiko.”-AH

The amount of the loan will depend on the applicant's credit

background that applies to personal loans. With the calculation of

DBR (Debt Burden Ratio) tracing up to other banks, banks can find

out the burden of credit installments borne by that person. According

to DP, the number of loans can be from 5 million to 300 million, but

the DBR must be considered. DP divides the DBR according to

credit risk from credit scoring ranging from 65% low risk to 45%

high risk. Apart from the calculation of DBR, there are also other

factors such as SLIK (Financial Information Services System), and

others (the type of work, area (place of residence), workplace).

Limitation of the amount of the loan based on the bank's assessment

certainly cannot be a barrier in the student loan scheme so that the

use of the loan can be used to pay full tuition fees.

104

Thus it can be concluded that to withdraw loans from banks, in general,

must go through a fairly rigorous process because there are risks faced by banks

let alone large amounts of loans. But this is where the role of the government

is to be able to collaborate between the government, universities, banking, and

students. The collaboration is needed, in particular for state-owned banks must

be ready to support this student loan program after raising funds from the

society, students need to guarantee their diplomas to the relevant university

until graduation and their college diplomas will be held until paid in full, then

the government can deposit a number of deposits to the bank as collateral if

there is indicating in default or facing repayment difficulities from the customer

so the risk of the bank will be kept to a minimum. Using IDX checking as a

tracing tool is also needed so that it can be known who is borrowing student

loans and can be a preventive measure for applying for new loans.

4.4.Repayment Scheme on Student Loan

Loans that have been agreed by both parties mean that the borrower has

accepted that there are obligations that must be fulfilled. The obligation is to

repay the loan with an agreed nominal until a predetermined period. Payment

of credit loans generally pays the principal debt that has been added to the

interest. Similar to a student loan, the applicant must pay a sum of money to

cover the principal debt along with the interest. At this point two things will be

discussed, especially, the first is about the student loan payment scheme for

Indonesia. And secondly, how to minimize defaults.

105

4.4.1. Student Loan Payment Scheme Model

In student loans, the position is the same as personal credit, in which

the credit pyramid according to the DP occupies the top position, which

means it is in the lowest priority so that it has a large risk. Other loans have

collateral that makes the debtor has more obligations such as home loans

and car collateral, home certificates and BPKB. Then, credit card, if not

paid, can make debtors unable to withdraw new loans with their cards.

While on personal loan, there is no collateral to be held by banks.

Figure 4. 6. Credit Triangle Based on The Risk

Source: Interview Results, CIMB Niaga Bank

Payment of student loans must be calculated carefully because the

target of student loans is from a family background who can not afford. Thus

a payment scheme is needed that does not burden the family but at the same

time does not provide a great risk to the banking sector as a source of funds.

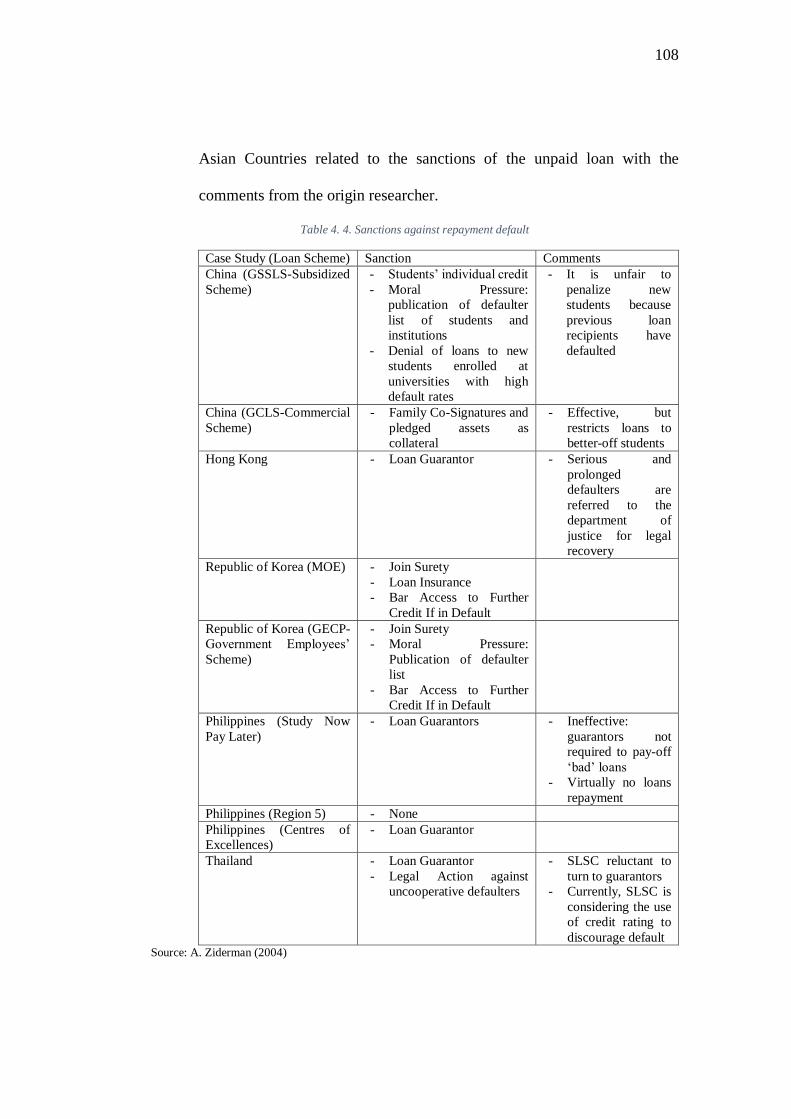

According to AH, student loans like abroad have never existed in Indonesia,

similar loans exist but payments are made by balloon payment where

Personal Loan

Credit Card

KPM

KPR

106

payments will begin when taking studies but the nominal is small, then after

graduation will enlarge proportionally until the loan is repaid. This balloon

payment has been carried out by Mandiri Bank as a financial institution in

collaboration with the Garuda Indonesia pilot academy where pilots who

take their studies at the academy will be given loans due to expensive study

fees, even though the prospective pilot has been given an income which

have not been high but can already make a minimum installment payment.

After becoming a pilot and having a flight time, the nominal payment will

increase proportionally until the loan is repaid. But AH gave an opinion if

this method is feasible because there is already a guarantee that all Garuda

Indonesia pilots would definitely work for the airline. This certainty is what

makes Mandiri Bank sure to fund pilot studies.

According to DP, the payment will be the same as AH already said. DP

believes that the payment when studying allows students to pay installments

to cover the interest first and will continue with principal debt after

graduated. Government intervention can be through interest subsidies and

deposits that initially should be 30% interest for personal loans (likened to

the category of student loans) can be reduced to around 13% because there

is certainty of government guarantees through deposits, not including the

reduction back through the interest subsidy program, the actual payments

tuition can ease the burden compared to the expected cost. According to the

DP, it is very important for payments to be made during enrollment as well

as to shorten the loan tenor so that the upcoming risk will also decrease.

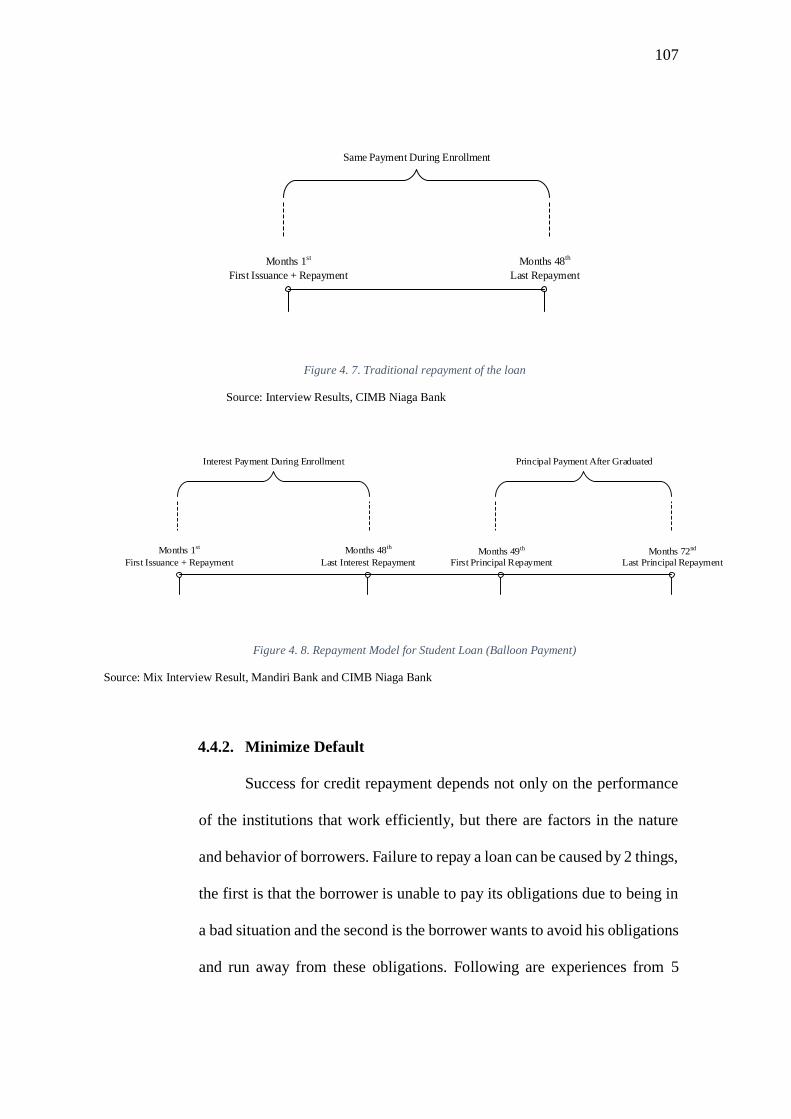

107

Months 1st

First Issuance + Repayment

Months 48th

Last Repayment

Same Payment During Enrollment

Figure 4. 7. Traditional repayment of the loan

Source: Interview Results, CIMB Niaga Bank

Months 1st

First Issuance + Repayment

Months 48th

Last Interest Repayment

Interest Payment During Enrollment

Months 49th

First Principal Repayment

Months 72nd

Last Principal Repayment

Principal Payment After Graduated

Figure 4. 8. Repayment Model for Student Loan (Balloon Payment)

Source: Mix Interview Result, Mandiri Bank and CIMB Niaga Bank

4.4.2. Minimize Default

Success for credit repayment depends not only on the performance

of the institutions that work efficiently, but there are factors in the nature

and behavior of borrowers. Failure to repay a loan can be caused by 2 things,

the first is that the borrower is unable to pay its obligations due to being in

a bad situation and the second is the borrower wants to avoid his obligations

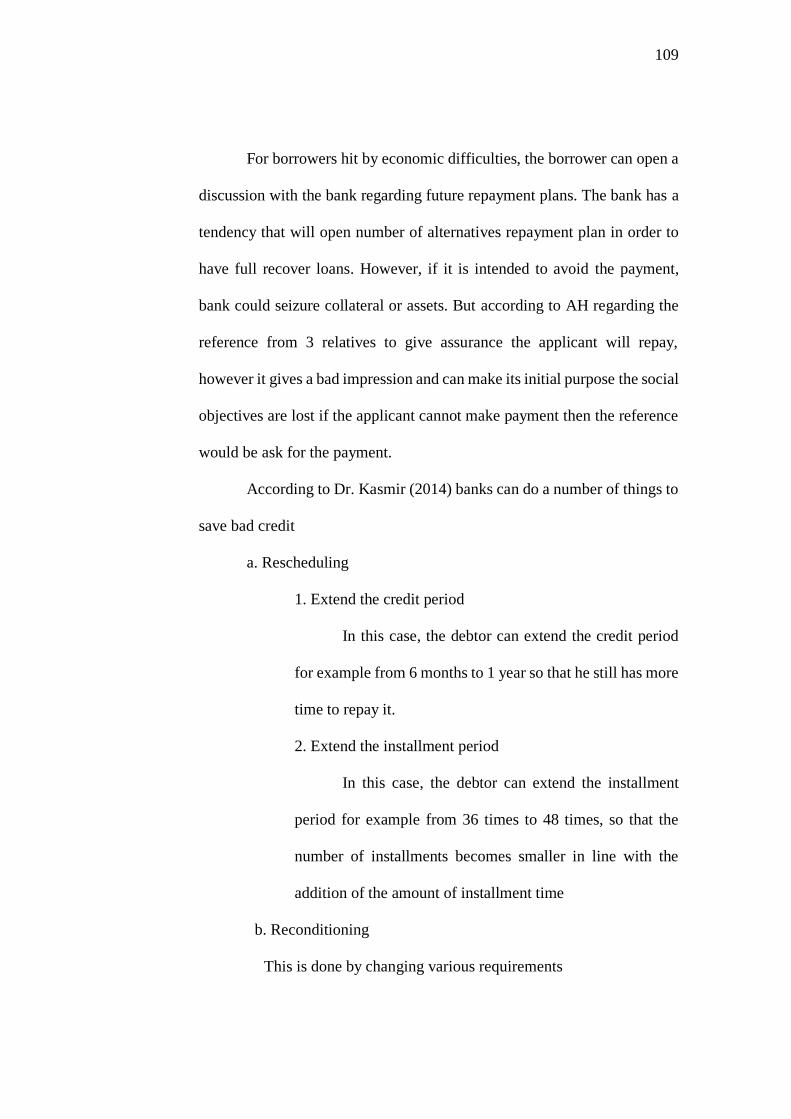

and run away from these obligations. Following are experiences from 5

108

Asian Countries related to the sanctions of the unpaid loan with the

comments from the origin researcher.

Table 4. 4. Sanctions against repayment default

Case Study (Loan Scheme) Sanction Comments

China (GSSLS-Subsidized

Scheme)

- Students’ individual credit

- Moral Pressure:

publication of defaulter

list of students and

institutions

- Denial of loans to new

students enrolled at

universities with high

default rates

- It is unfair to

penalize new

students because

previous loan

recipients have

defaulted

China (GCLS-Commercial

Scheme)

- Family Co-Signatures and

pledged assets as

collateral

- Effective, but

restricts loans to

better-off students

Hong Kong - Loan Guarantor - Serious and

prolonged

defaulters are

referred to the

department of

justice for legal

recovery

Republic of Korea (MOE) - Join Surety

- Loan Insurance

- Bar Access to Further

Credit If in Default

Republic of Korea (GECP-

Government Employees’

Scheme)

- Join Surety

- Moral Pressure:

Publication of defaulter

list

- Bar Access to Further

Credit If in Default

Philippines (Study Now

Pay Later)

- Loan Guarantors - Ineffective:

guarantors not

required to pay-off

‘bad’ loans

- Virtually no loans

repayment

Philippines (Region 5) - None

Philippines (Centres of

Excellences)

- Loan Guarantor

Thailand - Loan Guarantor

- Legal Action against

uncooperative defaulters

- SLSC reluctant to

turn to guarantors

- Currently, SLSC is

considering the use

of credit rating to

discourage default Source: A. Ziderman (2004)

109

For borrowers hit by economic difficulties, the borrower can open a

discussion with the bank regarding future repayment plans. The bank has a

tendency that will open number of alternatives repayment plan in order to

have full recover loans. However, if it is intended to avoid the payment,

bank could seizure collateral or assets. But according to AH regarding the

reference from 3 relatives to give assurance the applicant will repay,

however it gives a bad impression and can make its initial purpose the social

objectives are lost if the applicant cannot make payment then the reference

would be ask for the payment.

According to Dr. Kasmir (2014) banks can do a number of things to

save bad credit

a. Rescheduling

1. Extend the credit period

In this case, the debtor can extend the credit period

for example from 6 months to 1 year so that he still has more

time to repay it.

2. Extend the installment period

In this case, the debtor can extend the installment

period for example from 36 times to 48 times, so that the

number of installments becomes smaller in line with the

addition of the amount of installment time

b. Reconditioning

This is done by changing various requirements

110

1. Interest capitalization, interest is used as the principal

debt

2. Postponement of interest payments until a certain time

The point is that only interest is delayed, but the principal

debt payment must continue

3. The decrease in interest rates

The reduction in interest rates is intended to ease the burden

on customers depending on the consideration concerned.

The reduction in interest rates is expected to help ease the

customer's financial burden

c. Restructuring

1. Increase the amount of credit

2. Adding equity (cash or additional deposits from the owner)

d. Combination

Combined from the 3 things above

e. Seizure of collateral

The seizure is the last thing if the customer does not have good

intentions and is unable to pay all of his debts.

So it can be concluded that student loan payments can be made using the

balloon payment method and it is hoped that there will be government

intervention in providing deposits as collateral and providing interest

subsidies that can ease the financial burden. Repayment plan is also needed

if, at one time during the repayment period, the debtor is experiencing

111

economic difficulties so that he cannot make payments, other things that have

the intention not to pay can be resolved through the party responsible for the

student and through BEI checking and SLIK the student together with his

family unable to apply for credit again because there are still outstanding

credit obligations and any necessary sanctions with consideration of the

primary objectives.