china real estate report 04 jan 2012

TRANSCRIPT

abc Global Research

Physical market to remain challenging against the backdrop of administrative measures, despite broader monetary easing

Divergent cost of capital will be a key differentiator in 2012, in addition to execution

Conviction calls on COLI, Longfor and CRL

Physical environment to remain challenging in 2012 despite signs of

monetary easing. Sector-specific administrative measures will continue

to rein in demand. We expect additional price cuts in early 2012 as

developers strive to maintain a decent sell-through rate. Hence we

advocate an investment focus on factors beyond the policy uncertainties.

Developers face increasingly divergent cost of debt financing, leading

to a wide range of cost of capital. Access to debt financing will depend

on a developer’s funding maturity profile, operational capability and

balance sheet strength. This will be a key differentiator as developers

move to a lower-margin and quick asset turn model.

Earnings and NAV estimate revisions are driven by changes in

assumptions for property price, contract sales and cost of debt. We

forecast residential prices to decline 20% in tier-1 cities and 10% in all

others. We expect lower contract sales in 2012-13 as a result. Increasing

differential in cost of debt will have a disproportionate impact on earnings.

We favour developers with superior execution, proven platform and

cost of capital advantage. These are the key factors underpinning our

conviction calls on COLI and Longfor, both of which have low cost of

capital and highest earnings visibility within their own SOE/non-SOE

peer group. We also favour CRL as it has improved its asset turn and has

good access to funding, while further asset injection risk has been

reduced. From a valuation perspective, we favour KWG given the large

discount to the liquidation value and its still manageable liquidity.

Financial Institutions Group China Real Estate

China Real Estate Looking beyond the policy conundrum

Valuation summary

Bbg Price HSBC TP (Disc)/prem __ Core PE __Company ticker 30-Dec rating to NAV FY12 FY13 (HKD) (HKD) (%) (x) (x)

Agile 3383 HK 7.0 OW(V) 8.4 (54) 4.1 3.7COLI 688 HK 13.0 OW(V) 21.0 (41) 6.4 5.6CRL 1109 HK 12.5 OW(V) 17.6 (40) 8.4 7.5Franshion 817 HK 1.5 OW 1.9 (69) 5.1 4.4GZ R&F 2777 HK 6.1 OW(V) 7.1 (66) 3.9 3.4KWG 1813 HK 2.6 OW(V) 4.5 (80) 3.2 2.7Longfor 960 HK 8.8 OW(V) 13.3 (54) 7.2 5.6Shimao 813 HK 6.6 N(V) 7.0 (62) 4.4 4.0Shui On Land 272 HK 2.4 OW 2.9 (68) 7.4 5.2SOHO 410 HK 5.2 N 5.4 (47) 5.9 3.9Yanlord* YLLG SP 1.0 N(V) 1.0 (61) 7.5 6.9

* in SGD. Please refer to summary table of changes in ratings, NAVs and target prices on page 4. Source: Bloomberg, HSBC estimates

4 January 2012

Disclaimer & Disclosures This report must be read with the disclosures and the analyst certifications in the Disclosure appendix, and with the Disclaimer, which forms part of it

Derek Kwong* Analyst The Hongkong and Shanghai Banking Corporation Limited +852 2996 6629 [email protected]

Michelle Kwok* Analyst The Hongkong and Shanghai Banking Corporation Limited +852 2996 6918 [email protected]

Philip Zhong* Analyst The Hongkong and Shanghai Banking Corporation Limited +852 2996 6535 [email protected]

Stanley Cheung* Associate The Hongkong and Shanghai Banking Corporation Limited +852 2822 4395 [email protected]

Qi Zhuang* Associate The Hongkong and Shanghai Banking Corporation Limited +852 2996 6590 [email protected]

Ganesh Siva* Associate, Bangalore View HSBC Global Research at: http://www.research.hsbc.com

*Employed by a non-US affiliate of HSBC Securities (USA) Inc, and is not registered /qualified pursuant to FINRA regulations.

Issuer of report: The Hongkong and Shanghai Banking Corporation Limited

渐飞研究报告 - http://bg.panlv.net

abc

2

Financial Institutions Group China Real Estate 4 January 2012

Looking beyond the policy conundrum 6

Cost of capital under the limelight 12

Earnings and NAV estimate revisions 16

Downside protection – theoretical liquidation value 23

Assessing the cash flow buffer 26

Be realistic on policy expectations 32

Key property market data 39

Company write-ups 51 Agile (3383 HK) 52

China Overseas Land (688 HK) 54

China Resources Land (1109 HK) 56

Franshion (817 HK) 58

Guangzhou R&F (2777 HK) 60

KWG Property (1813 HK) 62

Longfor (960 HK) 64

Shimao (813 HK) 66

Shui On Land (272 HK) 68

SOHO China (410 HK) 70

Yanlord Land (YLLG SP) 72

Disclosure appendix 74

Disclaimer 77

Contents

渐飞研究报告 - http://bg.panlv.net

abc

3

Financial Institutions Group China Real Estate 4 January 2012

Key charts

Market share of key developers (as of November 2011) Developers’ net gearing (ex-restricted cash) and cash level Weighted cost of debt (as of December 2011)

13.8%

11. 3%

8.9%8.9%

0

100

200

300

400

500

600

2008 2009 2010 2011

0%

5%

10%

15%

20%

Key dev elopers (LHS) Market Share (RHS

(RMBmn)

0

20

40

60

80

100

120

2005 2006 2007 2008 2009 2010 1H11

0%

20%

40%

60%

80%

100%

Cash -ex .restricted (LHS) Net Gearing (RHS)

(RMB bn) (%)

3%

6%

9%

12%

CO

LI

CR

L

Fra

nshi

on

SO

HO

Long

for

Yan

lord

Shu

i on

Land

R&

F

Agi

le

KW

G

Shi

mao

*Key developers include Agile, COLI, CRL, Country Garden, Evergrande, Gemdale, GZRF, KWG, Longfor, Poly (A share), Shimao, Vanke

Source: Company data. CEIC

Source: Company data, HSBC * Developers include COLI, CRL, Franshion, SOHO China, Longfor, Shui On Land, GZ R&F, Agile, KWG and Shimao

Source: HSBC estimates

NAV discount chart PB chart (x) PE chart (x)

-80%

-60%

-40%

-20%

0%

20%

40%

60%

2005 2006 2007 2008 2009 2010 2011

% to NAV +1 SD Mean-1 SD -2 SD

0

1

2

3

4

5

97 99 01 03 05 07 09 11

0

10

20

30

40

50

60

97 99 01 03 05 07 09 11

Source: Company data, HSBC estimates Source: Company data, HSBC estimates Source: Company data, HSBC estimates

渐飞研究报告 - http://bg.panlv.net

abc

4

Financial Institutions Group China Real Estate 4 January 2012

Changes in ratings, NAVs and target prices

______Rating______ __________ Forward NAV___________ _________Target discount__________ __________ Target price ___________ Potential ____Implied PE (x) ____ Old New Old New % Chg Old New % Chg Old New % Chg return* FY12e FY13e

Agile OW OW(V) 20.5 15.2 -26% -53% -45% 8% 9.6 8.4 -13% 26% 4.9 4.5 COLI OW OW(V) 24.2 22.1 -9% 0% -5% -5% 24.2 21.0 -13% 65% 10.4 9.1 CRL N OW(V) 24.4 20.7 -15% -55% -15% 40% 11.0 17.6 60% 44% 11.8 10.5 Franshion OW OW 5.4 4.8 -12% -55% -60% -5% 2.5 1.9 -24% 30% 6.4 5.5 R&F OW OW(V) 20.4 17.8 -12% -56% -60% -4% 8.9 7.1 -20% 26% 4.5 3.9 KWG OW OW(V) 15.5 13.0 -16% -45% -65% -20% 8.5 4.5 -47% 81% 5.6 4.7 Longfor OW OW(V) 21.5 19.0 -11% -20% -30% -10% 17.2 13.3 -22% 55% 10.9 8.5 Shimao OW N(V) 19.5 17.5 -11% -57% -60% -3% 8.4 7.0 -17% 12% 4.7 4.2 Shui On Land OW OW 8.8 7.3 -17% -55% -60% -5% 4.0 2.9 -27% 29% 9.2 6.5 SOHO OW N 11.6 9.8 -16% -45% -45% 0% 6.4 5.4 -16% 10% 6.1 4.0 Yanlord n/a N(V) n/a 2.4 n/a n/a -58% n/a n/a 1.0 n/a 7% 7.5 6.9Simple average -14% 0% -14% 7.5 6.3

* Potential return equals the percentage difference between the current share price (as of 30 December 2011) and the target price, plus the forecast dividend yield We initiated coverage of Yanlord stock in a separate note (Initiate N(V): In need of a strategic shift, 4 January 2012) Source: HSBC estimates

Changes in core EPS (RMB), 2011-13e

Company ______________________ 2011e _______________________ ______________________ 2012e _______________________ ______________________ 2013e _______________________ Old New % Chg Old New % Chg Old New % Chg

Agile 1.35 1.33 -1% 1.74 1.44 -17% 2.20 1.59 -28%COLI* 1.55 1.51 -3% 1.65 1.71 4% 2.33 1.97 -16%CRL* 0.99 1.02 3% 1.32 1.26 -4% 1.55 1.42 -9%Franshion* 0.22 0.22 -2% 0.27 0.25 -7% 0.29 0.29 1%GZ R&F 1.25 1.20 -4% 1.20 1.34 12% 1.49 1.55 4%KWG 0.64 0.60 -6% 0.79 0.69 -13% 1.06 0.82 -23%Longfor 0.84 0.84 0% 1.12 1.04 -7% 1.50 1.33 -12%Shimao 1.26 1.25 -1% 1.35 1.26 -6% 1.49 1.40 -6%Shui On Land 0.22 0.23 3% 0.32 0.27 -15% 0.41 0.38 -7%Soho 0.18 0.18 0% 0.80 0.75 -6% 1.16 1.14 -2%Yanlord n/a 0.59 n/a n/a 0.71 n/a n/a 0.76 n/aAverage -1% -6% -10%

*HKD Source: HSBC estimates

渐飞研究报告 - http://bg.panlv.net

abc

5

Financial Institutions Group China Real Estate 4 January 2012

Valuation summary: China Developers (share price as of 30 December 2011)

Company Bbg HSBC Share price Target price Diff to TP Mkt cap 12m NAV (Disc)/Prem ______Core PE (x)_______ Yield (%) PB (x) Ticker rating (HKD) (HKD) (%) (HKDbn) (HKD/sh) (%) FY12e FY13e FY12e FY12e China Developers Agile 3383 HK OW(V) 6.96 8.4 21 24 15.2 (54) 4.1 3.7 5.9 0.8 COLI 688 HK OW(V) 12.98 21.0 62 106 22.1 (41) 7.6 6.6 3.3 1.4 CR Land 1109 HK OW(V) 12.48 17.6 41 72 20.7 (40) 9.9 8.8 3.6 1.2 Franshion Properties 817 HK OW 1.50 1.9 27 14 4.8 (69) 6.0 5.1 3.1 0.5Guangzhou R&F 2777 HK OW(V) 6.14 7.1 16 20 17.8 (66) 3.9 3.4 10.3 0.7 KWG Property 1813 HK OW(V) 2.62 4.5 72 8 13.0 (80) 3.2 2.7 7.7 0.5 Longfor Properties 960 HK OW(V) 8.78 13.3 51 45 19.0 (54) 7.2 5.6 2.8 1.7 Shimao Property 813 HK N(V) 6.63 7.0 6 24 17.5 (62) 4.4 4.0 6.8 0.6 Shui On Land 272 HK OW 2.36 2.9 23 14 7.3 (68) 7.4 5.2 4.6 0.4 SOHO China 410 HK N 5.17 5.4 4 27 9.8 (47) 5.9 3.9 6.0 1.2 Yanlord (SGD) YLLG SP N(V) 0.96 1.0 7 2 2.4 (60) 7.5 6.9 1.2 0.7 Note: OW = Overweight; N = Neutral; UW = Underweight; V = volatile. Source: Bloomberg, HSBC estimates

Contracted sales analysis

November Change in Change in YT November Change in November November November 2011 Target 2011 Target 2011Company Sales value

RMB mSales value

m-o-m Sales value

y-o-ySales value

RMB mSales value

y-o-y vs. 1H monthly

average vs. 2H monthly

average vs. YT Oct or NovMonthly average

Sales value RMB m

Sales % achieved

as of

Agile* 2,800 -15% 0% 29,000 14% 7% 7% 7% 37,000 78% NovCOLI* 2,819 -51% -38% 67,398 36% -60% -49% -56% 68,500 98% NovCR Land* 2,740 -15% 4% 30,070 51% 22% -21% 0% 30,000 100% NovCountry Garden 2,500 -43% -29% 39,400 30% -30% -35% -32% 43,000 92% NovEvergrande 1,240 -86% -81% 79,120 66% -82% -86% -84% 70,000 113% NovFranshion* n/a n/a n/a 8,800 n/a n/a n/a n/a 10,000 88% NovGZ R&F* 2,810 37% -37% 26,320 -8% 26% 11% 20% 32,000 82% NovKWG* 806 -6% 61% 10,897 3% -26% -9% -20% 15,000 73% NovLongfor* 3,010 -31% -26% 35,640 29% -1% -16% -8% 40,000 89% NovSino Ocean 2,200 -19% 0% 23,900 31% 7% -6% 1% 28,000 85% NovShui On Land*^ n/a n/a n/a 6,500 116% n/a n/a n/a 10,000 65% OctShimao* 1,742 -22% -51% 28,457 5% -27% -44% -35% 36,000 79% NovSOHO China* n/a n/a n/a 10,630 n/a n/a n/a n/a 23,800 45% NovVanke 8,290 -20% -36% 115,720 16% -24% -22% -23% 140,000 83% NovAverage# 32% -21% -28% -24% 85%

* Company under coverage ^ Year to October # Average applicable only to the companies announced November 2011 numbers (shaded in grey) Source: Company data, HSBC estimates

渐飞研究报告 - http://bg.panlv.net

abc

6

Financial Institutions Group China Real Estate 4 January 2012

Policy easing or not, should this be the question? The surprise reserve requirement ratio (RRR) cut

in November 2011 sparked expectations of a

reversal of months of tightening, and on the

surface, this is a positive sign for the physical

market and equities alike. News on introduction

of tax incentives for home purchases across a

number of cities including Beijing also seems to

legitimize the belief that easing will have a

positive impact on the housing market. The

injection of liquidity in the system could see some

benefits for the housing market, albeit indirect.

However, we believe it is still early days as

administrative policies like the Home Purchase

Restriction (HPR) will continue to put a cap on

demand, and the operating environment in 2012

will remain challenging.

Trading at an average of more than 50% discount

to NAV and 5.8x 2012e PE, both more than one

standard deviation below their historical mean,

conventional valuation metrics have continued to

hover around trough levels seen during the 2008

market downturn. Despite the seemingly

constructive valuation for the sector overall, we

are reluctant to formulate a sector-wide bullish

outlook because the verdict is not out yet on the

policy front and there remain a multitude of

prevailing industry headwinds.

While the volatility in global markets and other

externalities could in part explain the absolute

share price weakness, this is nevertheless

outweighed by the slew of industry-specific

uncertainties on the horizon.

Continued tight credit conditions (both

onshore and offshore): There is a prolonged lag

in mortgage disbursements from banks which is

putting some pressure on developers’ cash flow.

Shrinkage in corporate lending is also putting

pressure on developers’ cost of credit via onshore

trust financing or offshore high yield issues. The

key implication is that pre-sales become a more

important funding channel for developers.

Game theory in the physical market: There are

expectations of larger price declines amid shrinking

transaction volumes. Price discounting by

developers has accelerated since last summer, and

there has been a noticeable decline in volume

trends since September. This has spread from tier-1

Looking beyond the policy conundrum Recent RRR cut sparked expectations of policy easing, but administrative measures will remain status

quo in our view; hence operating environment in 2012 should stay challenging

Proven execution ability, balance sheet strength and cost of capital advantage are key differentiating

factors for the winners. We expect to see continual market share gain by the leaders

Despite constructive sector valuation, we do not anticipate a sector-wide rerating. COLI and Longfor

remain our conviction Overweights — we are adding CRL to this list

渐飞研究报告 - http://bg.panlv.net

abc

7

Financial Institutions Group China Real Estate 4 January 2012

cities like Shanghai and Beijing into major tier-2

cities. We believe this will put more pressure on

home prices (see new assumptions), particularly

from now to end 1Q12.

The policy conundrum: The investment case for

the sector cannot be based on a policy reversal, as

in our opinion, its effect on the housing market

will be limited. While on the monetary side the

RRR cut could mean the beginning of multiple

cuts, that’s broad macro implication without

considering more sector-specific issues. We

believe the central government’s stance toward

the housing sector is likely to remain hawkish in

the foreseeable future. We see the broader

monetary easing and other lateral relief like tax

incentives as evidence that the core administrative

measure HPR will remain firmly in place.

From an equity perspective, we believe

investment strategy should be based on a base

case of policy status quo for the housing sector.

As such, we believe companies with proven

execution track records particularly under difficult

market conditions, strong balance sheets and

better access to capital at a lower cost will be in a

more advantageous position in 2012.

Property price assumption for 2012 More developers have jumped onto the price

discounting bandwagon since September. This is

partly in an effort to achieve respectable sales

results as they drift behind the required run rate to

hit targets. Contracted sales have become a key

source of funding the business in the current tight

credit environment. In the coming months and

particularly in the seasonally quiet 1Q, we believe

the price cuts will steepen and spread from tier-1

to tier-2 and then smaller cities around the

country.

We expect residential prices to fall by 20% in tier-

1 cities and by 10% in tier-2/3 cities over the next

12 months. To put this into perspective, our

projected price falls will bring property prices

back to levels seen in 2009.

In distinguishing our price outlook for different

tier cities, the key factor for consideration is the

difference in depth of the secondary markets. We

are expecting steeper price corrections in tier-1

cities due to the availability of competitive

products in the secondary market. As such, tier-1

cities are more susceptible to inventory build-up

and pricing pressure.

Property price assumption for the next 12 months

Previous assumption New assumption

Residential price Tier-1 city -15% -20% Tier-2 city -5% -10% Tier-3 city 0% -10%Retail/office price 0% 0%

Source: HSBC estimates

GAV breakdown by tier cities

(%) Tier 1 Tier 2 Tier 3 Total

Agile Properties 20 80 - 100China Overseas Land 20 73 7 100China Resources Land 22 65 13 100Franshion Properties 24 74 2 100Guangzhou R&F 37 53 10 100KWG Property 53 47 - 100Longfor properties 25 42 33 100Shimao Property 14 70 16 100Shui On Land 23 77 - 100SOHO China 100 - - 100Yanlord 42 55 3 100Simple average 35 57 8Weighted average* 30 60 10

Source: HSBC estimates *by market capitalisation

Residential price trend – Year-end monthly average

0

1,000

2,000

3,000

4,000

5,000

6,000

98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

(RMB/sqm)2012e: down 10-15%, back to 2009 level

Source: NDRC, CEIC

渐飞研究报告 - http://bg.panlv.net

abc

8

Financial Institutions Group China Real Estate 4 January 2012

Cost of capital will be in the limelight While the key priority for developers will still be

market share gain amid continued industry

consolidation, we believe the market will be

placing increasing emphasis on developers’

capital structure and access/cost of capital. On the

one hand, the capital intensive nature of the real

estate business highlights the importance of

prudent balance sheet management, specifically

developers’ ability to withstand unforeseen

contracted sales shortfall, given the cyclical and

policy sensitive nature of the business. On the

other hand, the need to achieve quick asset

turnover also implies a strong competitive edge

for developers with ready access to funding at a

competitive cost. In our view, the ability to secure

low cost debt will prove to be an increasingly

important investment attribute worth appreciation

in the China property sector, particularly as both

onshore and offshore credit markets remain tight.

Against this backdrop, we argue that we need to

account for and reflect a greater range of cost

capital in our financial models. For our coverage

universe, we have derived cost of capital of

between 9% and 15% based on a detailed

appraisal of the capital structure and cost. The

differing cost of capital will have a minor impact

on NAV calculation. Cost of debt will impact the

forward margin prospect.

The valuation considerations Current sector valuation has priced in a rather grim outlook

While risk aversion on a high beta sector persists,

we argue that current valuation is pricing in an

overly grim outlook of the physical market, with

NAV discounts and PE both trading on a par to

the “darkest months” of 2008. Our analysis

indicates that current share prices are implying an

unrealistic one-off ASP decline of 28-50% across

all asset classes and all cities, which we find

unrealistic. Further, we also find that current share

prices are implying a massive devaluation in land

banks, as stocks are trading at a 4-39% discount to

historical land cost, except developers with state-

owned enterprise (SOE) status. Last but not least,

the bond market is providing some basis for our

argument that the sell-off in equities is overdone.

While bond prices are down, the magnitude of

solvency risk implied is significantly lower than

that reflected in the equity pricing.

Theoretical floor value analysis

We have devised an alternate valuation analysis

which we believe is a sound “pessimistic”

scenario analysis, where we employed a step-up

discounting approach on capital employed. Note

our derived floor values are calculated on a cost-

basis by taking the summation of all sunk costs

that developers have incurred and then netting off

their respective net debt to arrive at the floor

value. In our view, this metric serves to provide a

better gauge to developers’ tangible net worth, as

we strip out all subjective assumptions embedded

in traditional NAV estimates such as ASP, timing

difference of cash flow and WACC.

While there isn’t a barrier in the way of continued

or further weakness in share prices given the

current state of global equity markets, our

assessment of stocks’ theoretical floor values does

indicate that shares are well protected on the

downside. Of the nine stocks in our analysis, five

are trading at or below their respective floor

value; thus, current share prices are well protected

on the downside from a fundamental standpoint.

Not revisiting 2009, no V-shape rebound

We do not believe signs of a policy reversal for

the housing sector are conclusive, although easing

for the broader monetary environment has started.

The cooling of housing prices and transactions is

the result of administrative measures and

monetary conditions, the magnitude of which are

unlikely to have put the central government in

enough of a comfort zone to unwind.

Out of the 121 cities that have publicly announced

administrative measures such as HPR and price

restrictions, over 40 cities still recorded gains in

2011, and these are mostly tier-2/3 cities. At the

same time, over 30 cities are likely to miss their

target housing price level. It is therefore not

渐飞研究报告 - http://bg.panlv.net

abc

9

Financial Institutions Group China Real Estate 4 January 2012

surprising that cities like Zhuhai and Zhongshan

placed temporary price restrictions on pre-sales in

order to dilute ASP for 2011. Recent media

reports suggest that the Ministry of Housing and

Construction had asked the cities with HPR

expiring at year-end 2011 to extend the measure

indefinitely, and many cities have complied so far.

As such, we believe investment in the sector in

2012 should be based on the assumption that

administrative measures will remain status quo. In

our view, there will be no “rising tide lifts all

boats” situation like in 2009. We favour

companies with strong balance sheets, superior

access to debt funding at competitive costs and

proven execution track records, in this order of

priority. Hence our conviction OW stocks for

the sector are COLI, CRL and Longfor.

Changes to stock valuation Stocks for which we have widened the target discounts:

KWG from -45% (+0.5 SD) to -65% (-0.5 SD) to

account for the company’s slow sales momentum

given the continuous delay in new launches.

KWG only achieved 73% of its full-year

contracted sales target as at November 2011. In

our view, the company is likely to miss its 2011

full-year target by about 20%.

Longfor from -20% (+1 SD) to -30% (+0.5 SD)

as we believe the company’s sales momentum

will be partially capped while the central

government’s stance toward the housing sector

remains hawkish. We have applied a +0.5 SD

target discount for all of our conviction stocks

(i.e. Longfor, COLI and CRL) which have proven

sales records. Longfor remains the leader of the

pack among the non-SOEs.

We have fine-tuned the target discount of the

following companies, due simply to the increase

in market volatility that has led to a wider

measure of standard deviation from mean.

COLI from 0% to -5% (maintain +0.5 SD)

Franshion from -55% to -60% (maintain -1 SD)

GZ R&F from -56% to -60% (maintain -1 SD)

Shimao from -57% to -60% (maintain -1 SD)

Shui On Land from -55% to -60% (maintain -1 SD)

Stock for which we have narrowed the target discount:

CRL from -55% to -15% to reflect the stronger-

than-expected pick-up in contracted sales

momentum in 2H11. Thanks to its SOE

background, we expect the absolute advantage in

cost of capital to remain intact despite the tight

credit environment. In terms of balance sheet

management, CRL has deleveraged following the

latest round of share issuances to fund the asset

injection from the parent company. Given the

sheer size of the remaining assets pending for

injection, we expect CRL to break the annual

asset injection mode in 2012, which should be

welcomed by investors.

渐飞研究报告 - http://bg.panlv.net

abc

10

Financial Institutions Group China Real Estate 4 January 2012

Where our conviction lies

With the view that administrative measures like

HPR will continue to suppress demand for

residential properties, we prefer companies with

proven sales records, competitive cost of capital

and strong balance sheet management.

COLI (688 HK; OW(V); TP HKD21)

COLI is the leader of the pack in terms of both

operations and balance sheet strength. The

company was a standout in sales delivery in 2011

amid the government’s persistently tight grip on

the policy front. With ready access to offshore

bank loans from Hong Kong, COLI has the lowest

cost of capital in the China property sector.

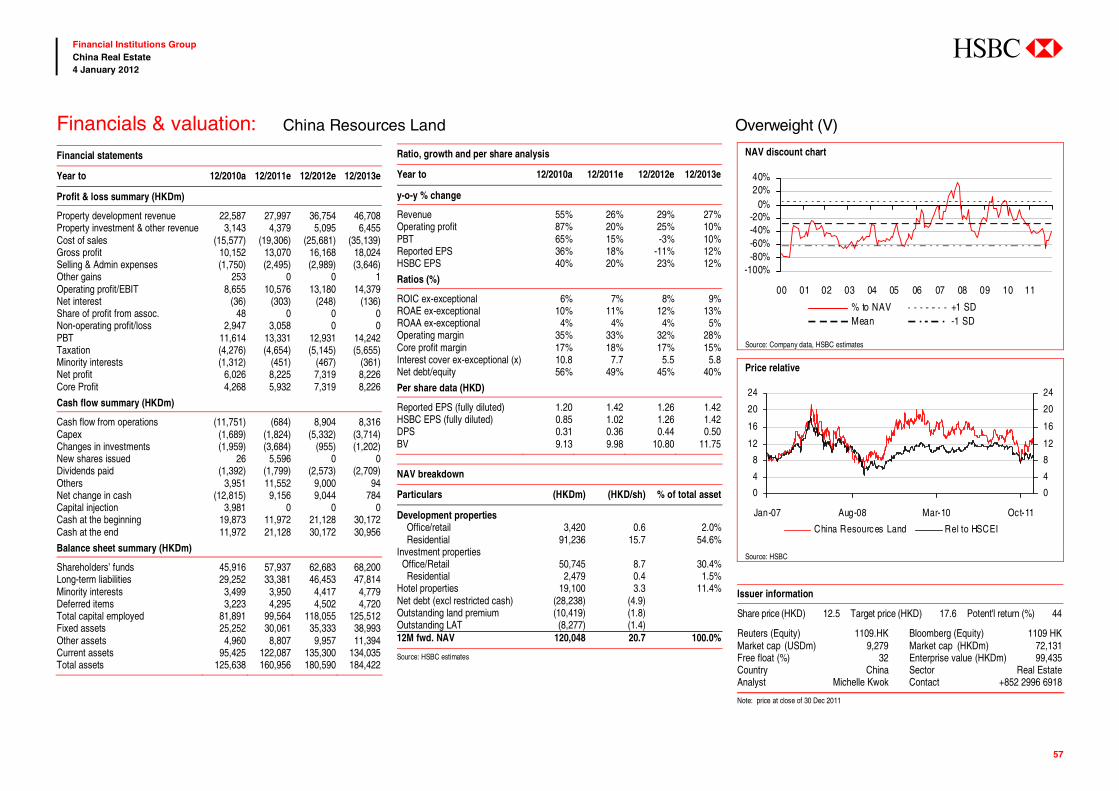

CRL (1109 HK; OW(V); TP HKD17.6)

CRL has radically improved its slow asset

turnover in 2011, by posting 51% y-o-y growth in

contracted sales through November 2011. While

cost of capital becomes a crucial differentiating

factor, we believe its SOE background will allow

CRL to enjoy low cost funding. CRL has also

deleveraged following the issuance of shares for

the latest asset injection. We expect CRL may

break its annual asset injection tradition in 2012,

given the sheer size of the remaining project,

Shenzhen Dachong, in the pipeline. That would be

a big positive for CRL, as we argue that the

“growth by injection” model is no longer

appropriate for a well-developed company. See

our note Viability of future asset injection a moot

point dated 20 September 2011 for further details.

% discount to NAV

-5%

-15%

-30%

-45% -45%

-55%-60% -60% -60% -60%

-65%-75%

-50%

-25%

0%

COLI CRL Longfor SOHO Agile Yanlord Franshion R&F Shimao Shui On KWG

Disccount to NAV

Source: HSBC estimates

Standard deviation below mean

Agile Franshion KWG

R&F Shimao Shui On Yanlord

SOHO

LongforCRLCOLI

(1.5)

(1.0)

(0.5)

-

0.5

1.0

Standard dev iation below mean

Deeper discount to

mean

Source: HSBC estimates

渐飞研究报告 - http://bg.panlv.net

abc

11

Financial Institutions Group China Real Estate 4 January 2012

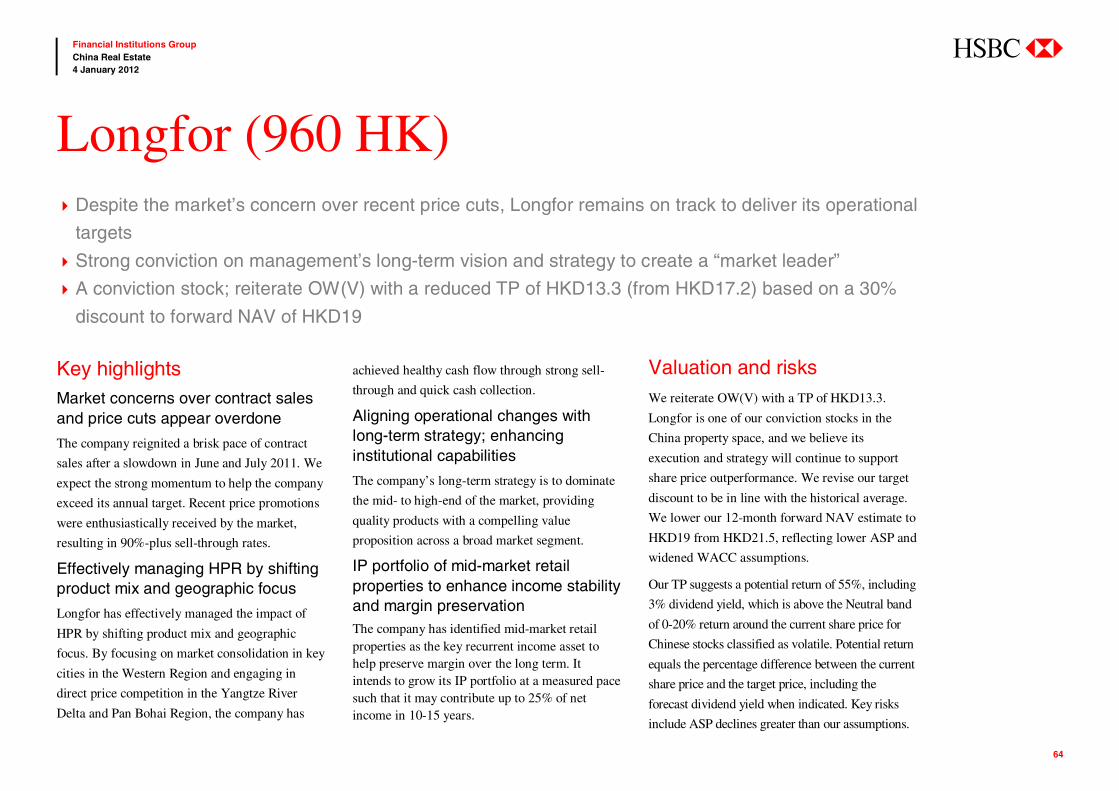

Longfor (960 HK; OW(V); TP HKD13.3)

Longfor’s contracted sales momentum has

outpaced the sector’s, particularly during the

summer months that defied the market slowdown.

Longfor leads the pack among the non-SOEs in

terms of borrowing cost advantage and contracted

sales momentum. These are the key reasons

behind our conviction.

渐飞研究报告 - http://bg.panlv.net

abc

12

Financial Institutions Group China Real Estate 4 January 2012

The importance of cost of capital advantage While consistency in operating cash flow, balance

sheet strength preservation and market share gains

will continue to be important benchmarks in 2012,

we believe the market will place increasing

emphasis on cost of capital amid challenging

equity markets and credit conditions, both onshore

and offshore. We see wide differential among

companies under our coverage and believe this

will emerge as a key investment consideration in

2012 for the following key reasons:

Real estate investment is a capital intensive

business

The sector’s cost of capital is structurally

trending north, as credit has gotten

incrementally tighter

Wide divergence in cost of capital should be

reflected in the value of the underlying assets

(NAV)

The structural step-up in debt cost will

become more apparent, to be reflected in

developers’ P&L

For these reasons, we believe developers’ ability

to secure low debt cost will prove to be an

increasingly important investment attribute worth

appreciation in the China property sector. That

said, despite the importance and relevance of

developers’ cost of funding in asset valuation, we

believe the market has to an extent neglected this

factor as a fundamental consideration in stock

selection so far.

Two considerations: NAV and margins

In terms of valuation, our NAV estimates are

directly affected as WACC is a key assumption in

DCF analysis which is the foundation of our NAV

calculation.

In terms of margin, our hypothetical margin

analysis highlights how the cost of debt can come

into play differently for high and low margin

companies. Low margin companies are harder hit

when finance cost increases, while the impact on

high margin companies is buffered by the

reduction in Land Appreciation Tax (LAT).

Cost of capital under the limelight The market should pay increasing attention to cost of capital for the sector, amid global equity market

volatility and tight credit conditions

We revise our WACC assumptions by 90-460bp to 9.1-15.3% to account for the sizable difference in

developers’ cost of capital

Difference in WACC will be reflected in our NAV calculation, and difference in cost of debt will have

forward margin implications

渐飞研究报告 - http://bg.panlv.net

abc

13

Financial Institutions Group China Real Estate 4 January 2012

WACC revision

Company Old New Change

Agile 10.7% 15.3% 4.6% COLI 8.8% 9.1% 0.3% CRL 9.0% 10.2% 1.2% Franshion 9.3% 10.2% 0.9% R&F 11.0% 14.4% 3.4% KWG 11.0% 14.2% 3.2% Longfor 9.0% 13.1% 4.1% Shimao 10.0% 14.1% 4.1% Shui on Land 9.5% 12.9% 3.5% SOHO 9.0% 10.3% 1.2% Yanlord* n/a 11.4% n/a Average 2.6%

Source: HSBC estimates We initiated coverage of Yanlord stock in a separate note (Initiate N(V): In need of a strategic shift, 4 January 2012)

Estimated weighted cost of debt

3%

6%

9%

12%

CO

LI

CR

L

Fra

nshi

on

SOH

O

Long

for

Yan

lord

Shui

on

Land

R&F

Agile

KW

G

Shim

ao

Source: HSBC estimates

Our adjustments to WACC

In anticipation of persistent scrutiny on

developers’ balance sheet strength preservation,

and increasing divergence in their respective cost

of borrowing, we see the need to adjust WACC to

appropriately capture the divergence in funding

costs following the wave of USD high yield

issuances over the past 18 months. We revise our

WACC assumptions by 90-460bp to 9.1-15.3%.

Agile, Longfor and Shimao are standouts with the

biggest WACC adjustments of 410-460bp,

affected by both higher beta (cost of equity) and

higher cost of debt (reliance on offshore high

yields on the debt front). We believe our revised

range of WACC assumptions is much wider than

what is currently adopted by the market with a

spread of 610bp between the lowest and highest

WACC for stocks in our coverage universe.

Key reasons behind our WACC revisions:

The market has simplistically assumed a

relatively tight and generalized WACC range,

which we deem as inappropriate as it fails to

account for the true costs of borrowing

against the rather un-accommodative lending

environment.

There were sizable differences in developers’

borrowing costs of some 1,000bp in 1H11 and

this spread is unlikely to be reversed. For

stocks within our coverage universe, COLI,

CRL, Franshion, SOHO and Longfor are

developers with significant cost of debt

advantage and this is owing to the strong

support of banks and the syndicated loan

market.

The equity market has become more volatile,

and hence the market adopted beta needs to

be adjusted accordingly in order to

appropriately calculate the cost of equity. WACC calculation methodology In our WACC calculation, we assume a target debt

structure of 40% and a corporate tax rate of 25%.

Estimating the cost of equity

This is calculated based on the CAPM formula:

)( RfRmRfKe −+= β

Key assumptions in our calculations include a

risk-free rate of 3.5% and equity risk premium of

10%. Company-specific betas are based on

weekly calculations of the past three years.

Estimating the cost of debt

In estimating developers’ cost of debt, we refer to

the last reported loan profile and our estimated

mark-to-market finance cost of each company.

Based on our analysis, we observe that the stocks

could be generally categorized into three groups,

given the sizable difference in the cost of debt.

渐飞研究报告 - http://bg.panlv.net

abc

14

Financial Institutions Group China Real Estate 4 January 2012

Category 1 stocks – (below 7.5%) key sources

of borrowing: Offshore HKD bank loans +

onshore bank loans at a small premium above the

benchmark rate

Stocks: COLI, CRL, Franshion

This group of developers has ready access to the

offshore syndicated loan market, as well as

onshore bank loans at a small premium above the

benchmark People’s Bank of China (PBOC) rate.

We observe that offshore low-cost borrowing

contributes more than 50% of COLI’s and CRL’s

debt profile as of the latest reporting date. Not

surprisingly, developers in this group are mainly

SOEs, whose parent backings have enhanced

credit accessibility with more flexible funding

channels. These developers enjoy the lowest cost

of borrowing among the three groups of stocks.

Category 2 stocks – (7.5% to 10%) key sources

of borrowing: Onshore construction loans at a

reasonable premium above the benchmark rate +

offshore syndicated loan + USD high yield bond

Stocks: Longfor, Soho China, Shui On Land,

Yanlord

This group of developers possesses healthy

balance sheets, or in the case of Shui On Land is

the subsidiary of a HK-based listed company.

Developers in this group are able to secure

onshore construction loans at reasonable rates, fair

access to offshore syndicated loans and sensible

issue cost in the offshore high yield bond market.

Category 3 stocks – (above 10%) key sources of

borrowing: Onshore construction loans at a

premium above the benchmark rate + offshore

syndicated loan + USD high yield bond

Stocks: Agile, GZ R&F, KWG, Shimao

Developers who have stretched balance sheets and

limited source of low-cost funding fall into this

category. We observe that these developers

generally relied more heavily on offshore high

yield bond as of their latest report date. We

believe their key sources of borrowing are

onshore construction loans, but at higher

premiums over the PBOC benchmark lending

rate.

Putting it together: WACC range of 9.1-15.3%

Our revised WACC range of 9.1-15.3% represents

a sizable spread of 610bp between the high end

and low end, based on the determined cost of

equity and debt. Note that we have assumed a

40% debt-to-asset ratio across the board. In this

exercise, we find that COLI has the lowest

WACC, while Agile is penalized for its

dependence on USD HY issuances and high beta.

渐飞研究报告 - http://bg.panlv.net

abc

15

Financial Institutions Group China Real Estate 4 January 2012

WACC calculations

Onshore RMB Premium above

PBOC

Offshore borrowing

cost

Bond / notes

interest

Weight of onshore RMB

Weight of offshore HKD

Weight of offshore HY

WA cost of debt Debt/ Asset

Revised beta

Risk free rate

Market risk premium

Equity/ Assets

Tax WACC

(a) (b) (c) (d) (e) (f) (g) = PBOC rate*(1+a)*(d) + (b)*(e)+ (c)*(f)

(h) (i) (j) (k) (l) (m) (^)

Agile 40% 9% 13% 55% 10% 35% 10.84% 40% 1.65 3.5% 10% 60% 25% 15.3%COLI 0% 3% n/a 20% 80% 0% 3.40% 40% 1.00 3.5% 10% 60% 25% 9.1%CRL 10% 4% n/a 30% 70% 0% 5.11% 40% 1.10 3.5% 10% 60% 25% 10.2%Franshion 10% 7% n/a 70% 30% 0% 7.49% 40% 0.95 3.5% 10% 60% 25% 10.2%R&F 40% 9% 15% 70% 10% 20% 10.76% 40% 1.50 3.5% 10% 60% 25% 14.4%KWG 40% 9% 15% 60% 10% 30% 11.28% 40% 1.45 3.5% 10% 60% 25% 14.2%Longfor 20% 7% 11% 65% 15% 20% 8.71% 40% 1.40 3.5% 10% 60% 25% 13.1%Shimao 40% 9% 15% 60% 10% 30% 11.28% 40% 1.45 3.5% 10% 60% 25% 14.1%Shui On Land 30% 9% 12% 60% 10% 30% 9.96% 40% 1.30 3.5% 10% 60% 25% 12.9%SOHO 20% 8% 10% 70% 30% 0% 8.28% 40% 0.95 3.5% 10% 60% 25% 10.3%Yanlord 15% 7% 13% 50% 15% 35% 9.60% 40% 1.08 3.5% 10% 60% 25% 11.4%

Source: HSBC estimates ^ WACC = (h) * (g) * [1-( m)] + [(j) +(i) * (k)] * (l)

Summary of credit rating and access to offshore loans

Company Name

S&P corporate credit rating

Moody's corporate credit

rating

Access to offshore

syndication loans

Agile BB/Stable/-- Ba2/Stable YesCOLI BBB/Stable/-- Baa2/Stable YesCR Land BBB/Stable/-- Baa2/Stable YesFranshion BB+/Stable/-- Baa3/Stable YesGZ R&F na. na. YesKWG BB-/Stable/-- Ba3/B1/Stable YesLongfor BB+/Stable/-- Ba2/Ba3/Stable YesShimao BB/Negative/-- Ba3/Stable YesShui On na. na. YesSoho China na. na. YesYanlord BB/Negative/-- Ba2/Negative Yes

Source: S&P, Moody’s, Company data, HSBC estimates

China Developers’ source of funding

15.4%

22.7%

17.3%

19.5%

19.8 %

22.7%

4 1.2 %

34.8%

36.8 %

36.8 %

48 .1%

34.8%

42 .3%

41.5%

44.8 %

43 .0%

3 1.3 %

41.5%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

FY11*

1H11

FY10

1H10

FY09

1H09

Bank Loan Foreign Investment Equity Pre-sale proceeds and Mortgage receipt

Source: CEIC *As at October-2011

渐飞研究报告 - http://bg.panlv.net

abc

16

Financial Institutions Group China Real Estate 4 January 2012

Changes in earnings estimates We lower our 2011-13 EPS forecasts by an

average -1%, -6% and -10%, respectively.

Two reasons behind our earnings revisions

Incorporation of our revised property

price assumptions: In the coming 12 months,

we look for residential prices to decline 20%

in tier-1 cities, and decline 10% in both tier-2

and below cites, respectively.

Revisions in contracted sales forecasts:

Slower-than-expected contracted sales through

November 2011 will see selective developers

succumb to the reality of a sales shortfall for

2011. As a result, we adjust our 2011 sales

forecast to reflect developers’ current pace of

sales as well as their lack of incentive to

overachieve in property sales based on the

current state of equity markets. Thus, we also

adjust contracted sales for 2012-13 based on

more reasonable y-o-y growth rates.

Note the muted impact on 2011e EPS is mainly

attributable to the strong revenue lock-in ratio,

which came on the back of sales secured through

November 2011 and in 2010. While we estimate

70% of property development revenue has been

secured as at November 2011, we do not rule out

the possibility that developers push some

deliveries into 2012, if both the physical and stock

markets continue to weaken from this point.

Earnings and NAV estimate revisions We lower our 2011-13 EPS estimates by an average of -1%, -6 and -10%, respectively, to reflect

scaled-back contracted sales forecasts and revisions in ASP

Accordingly, we lower our NAV estimate on average by 14%

We have adjusted our target NAV discounts for COLI, CRL, Franshion, KWG, Longfor and SOL

EPS revisions (RMB), 2011-13e

Company ____________ 2011e _____________ ____________ 2012e _____________ ____________ 2013e _____________ Old New % Chg Old New % Chg Old New % Chg

Agile 1.35 1.33 -1% 1.74 1.44 -17% 2.20 1.59 -28%COLI* 1.55 1.51 -3% 1.65 1.71 4% 2.33 1.97 -16%CRL* 0.99 1.02 3% 1.32 1.26 -4% 1.55 1.42 -9%Franshion* 0.22 0.22 -2% 0.27 0.25 -7% 0.29 0.29 1%R&F 1.25 1.20 -4% 1.20 1.34 12% 1.49 1.55 4%KWG 0.64 0.60 -6% 0.79 0.69 -13% 1.06 0.82 -23%Longfor 0.84 0.84 0% 1.12 1.04 -7% 1.50 1.33 -12%Shimao 1.26 1.25 -1% 1.35 1.26 -6% 1.49 1.40 -6%Shui On Land 0.22 0.23 3% 0.32 0.27 -15% 0.41 0.38 -7%SOHO 0.18 0.18 0% 0.80 0.75 -6% 1.16 1.14 -2%Yanlord n/a 0.59 n/a n/a 0.71 n/a n/a 0.76 n/aAverage -1% -6% -10%

Source: HSBC estimates *in HKD

Property price assumption for the next 12 months

Previous assumption New assumption

Residential price Tier-1 city -15% -20% Tier-2 city -5% -10% Tier-3 city 0% -10% Retail/office price 0% 0%

Source: HSBC estimates

渐飞研究报告 - http://bg.panlv.net

abc

17

Financial Institutions Group China Real Estate 4 January 2012

Therefore, we fine-tune our 2011 EPS estimate by

-1% on average for stocks under our coverage.

Higher -6% and -10% EPS revisions are seen in

2012-13, respectively, as we scale back

developers’ contracted sales forecasts. Theoretical revenue lock-in ratio for 2011-12

Company Carry-fwd unbooked

revenue 2010 (RMBm)

Contracted sales thru Nov 2011 (RMBm)

2011 Rev Lock-in

ratio

2012 Rev Lock-in

ratio*

Agile 20,000 28,000 100% 60% COLI 32,300 67,398 100% 100% CR Land 21,037 30,070 100% 84% GZ R&F 16,672 26,320 100% 75% Franshion n/a 8,800 100% 27% KWG 7,367 10,897 100% 92% Longfor 33,800 35,640 100% 100% Shimao 17,000 28,457 100% 51% Shui On Land^ 2,825 6,500 100% 42% SOHO China 4,500 10,630 100% 69% Average 70%

Source: Company data, HSBC estimates * as of November 2011 ^ as of October 2011

Cost of debt implication on profitability

While cost of capital advantage is the key theme

in 2012, we also highlight that profitability, as

measured by net profit margin, is a function of

finance cost. Hence, developers with significant

cost of debt advantage are better placed to achieve

higher profit margins.

Note, however, that cost of debt and net margin

do not exhibit a linear relationship, as the LAT

provisions increase as net profit margin grows.

Indeed, our net margin sensitivity analysis

indicates that low margin companies are generally

Contracted sales revisions

(RMBm) FY11 Revision(%)

FY12 Revision(%)

Implied y-o-y growth (%)

FY13 Revision(%)

Implied y-o-y growth (%)

Agile 34,900 -6% 40,323 -11% 16% 45,762 -12% 13%COLI 75,000 9% 89,177 0% 19% 106,284 5% 19%CRL 31,500 5% 34,624 6% 10% 38,432 -10% 11%Franshion 8,148 0% 6,748 -9% -17% 8,749 19% 30%R&F 30,500 -5% 32,274 -10% 13% 40,389 0% 25%KWG 11,400 -4% 11,455 -8% -4% 12,393 -4% 8%Longfor 40,000 -0% 45,300 -4% 13% 50,388 -7% 11%Shimao 31,800 -8% 31,177 -15% -2% 34,922 -19% 12%Shui on Land 7,550 -10% 9,966 -20% 32% 13,446 -24% 35%SOHO 14,500 0% 17,193 -3% 19% 19,182 -1% 12%Yanlord 8,484 n/a 9,741 n/a 15% 11,970 n/a 23%Average n/a -2% n/a -7% 10% n/a -5% 21%Total 293,782 327,977 12% 381,917 17%Total (adjusted*) 147,282 158,876 8% 186,812 18%

Source: HSBC estimates *Excluding the consistent players: COLI, CRL and Longfor

Net margin sensitivity analysis on different finance costs

Low margin company Typical company High margin company

Average ASP 16,000 Average construction cost 5,000 Average land cost 4,000 Average capitalised interest* 675Gross Profit Margin 30% 40% 50%Average SG&A to ASP ratio 7% 7% 5%Average LAT to ASP ratio 4% 7% 12%Income tax 25% 25% 25%Net profit margin 14.5% 18.9% 24.8%Sensitivity analysis Assumed 500bp increase in finance cost Change Change ChangeGP margin 25.3% -4.9% 35.3% -4.2% 46.4% -3.5%LAT to ASP ratio 2.0% -2.0% 5.7% -1.3% 9.9% -1.9%NP margin 12.2% -2.3% 16.9% -2.0% 23.6% -1.2% Assumed 1,000bp increase in finance cost Change Change ChangeGP margin 20.4% -9.8% 31.1% -8.4% 42.9% -7.0%LAT to ASP ratio 0.1% -3.9% 4.2% -2.8% 8.6% -3.2%NP margin 9.9% -4.6% 15.0% -4.0% 22.0% -2.8%

Source: HSBC estimates *Based on 75% interest capitalisation rate and 24 months of construction loans, interest cost of 5%

Every 1% increase in finance cost

Low margin Typical company High margin

GP margin -0.98% -0.80% -0.70% NP margin -0.46% -0.40% -0.23%

Source: HSBC estimates

Every 1% reduction in ASP

Low margin Typical company High margin

GP margin -0.81% -0.70% -0.56%NP margin -0.19% -0.33% -0.27%

Source: HSBC estimates

渐飞研究报告 - http://bg.panlv.net

abc

18

Financial Institutions Group China Real Estate 4 January 2012

harder hit when finance cost increases, while the

negative impact on high margin companies is

relatively muted as margins are buffered by a

reduction in LAT.

EPS revisions by company Below we discuss key changes to our EPS

estimates by company, noting that all of our

revised estimates have incorporated our latest

ASP forecasts.

Agile (3383 HK; OW(V); TP HKD8.4)

With contracted sales continuing to track behind

schedule at a 76% run rate through November,

Agile will struggle to meet its 2011 full-year

target, leading us to lower our 2011 contracted

sales forecast by 6% to RMB35bn from

RMB37bn. Accordingly, we have scaled down

contracted sales for 2012 and 2013 by 11% and

12%, respectively. This is mainly attributable to

lower ASP assumptions as the company has

reiterated its strategy of value pricing its product

to ensure strong sell-through. In addition, its

Hainan project will contribute less to the bottom

line as the company builds out the comprehensive

commercial phase. Hence, we lower our 2012 and

2013 EPS by 17% and 28%, respectively, while

leaving 2011 EPS largely unchanged as the

bookings have largely been secured.

COLI (688 HK; OW(V); TP HKD21)

Being the leader of the pack in terms of both sales

progress and earnings visibility, COLI is on track

to meet our EPS forecasts. We revise our 2012

and 2013 EPS forecasts by +4% and -16%, while

fine tuning our 2011 EPS forecast by -3%. Larger

magnitude of revision in 2013 is mainly due to

our ASP revision, given that most of the

upcoming sales will be recognised in 2013.

CRL (1109 HK; OW(V); TP HKD17.6)

Similar to COLI, CRL should have no difficulties

in achieving the 2011 full-year sales target.

Core profit margin trends

2008 2009 2010 2011e 2012e 2013e

Agile 59% 14% 17% 16% 17% 15% COLI 21% 17% 22% 23% 20% 21% CRL 18% 18% 17% 18% 17% 15% Franshion 21% 17% 17% 25% 17% 13% R&F 13% 13% 14% 17% 13% 12% KWG 25% 16% 17% 18% 23% 23% Longfor 5% 13% 17% 17% 16% 12% Shimao 15% 16% 16% 16% 13% 11% Shui on Land 73% 25% 15% 18% 20% 15% SOHO 13% 23% 19% 16% 24% 24% Yanlord 14% 14% 17% 12% 12% 11% Simple avg 25% 17% 17% 18% 18% 16% Wtg avg* 21% 17% 18% 19% 18% 17%

Source: HSBC estimates *By market capitalization

Development margins trends

2008 2009 2010 2011e 2012e 2013e

Agile 37% 37% 46% 49% 45% 41% COLI 44% 32% 40% 36% 33% 32% CRL 38% 38% 42% 40% 38% 32% Franshion 51% 46% 45% 55% 42% 41% R&F 38% 35% 41% 43% 33% 31% KWG 51% 37% 42% 43% 37% 33% Longfor 25% 28% 32% 36% 33% 27% Shimao 49% 39% 40% 46% 40% 38% Shui on Land 40% 51% 38% 41% 47% 36% SOHO 49% 52% 51% 33% 49% 46% Yanlord 56% 56% 55% 40% 44% 38% Simple avg 43% 41% 43% 42% 40% 36% Wtg avg* 41% 37% 41% 39% 37% 34%

Source: HSBC estimates *By market capitalization

渐飞研究报告 - http://bg.panlv.net

abc

19

Financial Institutions Group China Real Estate 4 January 2012

Hence, our EPS revisions are mainly reflective of

push-back in completion schedule and changes in

ASP. The company also has a growing investment

property (IP) portfolio expected to contribute

about 7% of total revenue in 2011, the highest

proportion among large developers. As IP

generally carry a higher margin than development

properties, they can have a disproportionate

impact on the bottom line. Our analysis shows

each dollar of the company’s property

development revenue contributes RMB0.17 to net

income, while a dollar of rental revenue can

contribute RMB0.43 to the bottom line. Hence we

expect the company’s IP portfolio to provide

some degree of earning resilience. We cut our

2012 and 2013 EPS by 4% and 9% on the back of

lower GFA delivery by 5-10% during these

periods, respectively.

Franshion (817 HK; OW; TP HKD1.9)

Our 2011 EPS is largely unchanged as our forecast

captures the latest sales progress following our

revision in Patience beginning to bear fruit (20

October 2011). In 2012, we lower our EPS

modestly by 7%, as the majority of the 2012

revenue has already been secured, implying

minimal impact from our ASP revisions. Our 2013

EPS is largely unchanged, as the effect of the ASP

decline is offset by higher contracted sales, mainly

from the Qingdao Lanhai Xingang City project.

GZ R&F (2777 HK; OW(V); TP HKD7.1)

Although the company remains confident of

achieving its 2011 full-year contracted sales target

of RMB32bn (revised down from RMB40bn in

September), we expect the company to achieve

95% by year-end 2011, i.e. RMB30.5bn, down

5% from our previous estimate. Accordingly, we

revise our 2011 EPS down by 4%. We also lower

2012 contracted sales by 10% due to the current

sales momentum. As we believe that our 2012e

EPS reduction was too conservative (see 28

September note OW: Reality bites, but guidance

cut manageable), we raise 2012 EPS by 12% to

RMB1.34 from RMB1.20. Coming from a low

base of contracted sales, we believe GZ R&F

could see a rebound in sales in 2013 (w estimate

25% growth). As a result, we raise our 2013 EPS

by 4%, despite a reduction in contracted sales in

the previous two years.

KWG (1813 HK; OW(V); TP HKD4.5)

We lower our 2011 EPS by 6%, the most of

stocks in our coverage universe, given that sales

through November 2011 are significantly behind

schedule. Continuous delays in project launches

should see 2011 full-year sales fall short of target

by about 20%. Coupled with the company’s large

exposure in higher tier cities (53% in tier-1, the

highest among all developers excluding SOHO),

we expect contracted sales to remain flat in 2012

and to log only moderate growth of 8% y-o-y in

2013. We lower our 2012-13 EPS by 13% and

23%, respectively.

Longfor (960 HK; OW(V); TP HKD13.3)

Longfor is firmly on track to meet its 2011

contracted sales target based on the company’s

sales progress through November. Our 2011 EPS

is largely unchanged as Longfor offers the highest

theoretical revenue lock-in ratio through 2012.

Despite this, we scale down Longfor’s contracted

sales forecasts in both 2012 and 2013 along with

other developers in the sector. The revised y-o-y

sales growth forecasts of 11-13% are only

marginally lower than previous forecasts of 15%.

We believe this is justified given the company’s

demonstrated practice of aggressive price cutting

and the resultant 90%+ sell-through rate. Hence,

we cut our 2012-13 EPS by 7% and 12%,

accordingly.

Shimao (813 HK; N(V); TP HKD7)

Following our latest round of estimate revisions

(see Upgrade to OW: But deleveraging will drain

growth, 11 October 2011) we leave our 2011 EPS

unchanged, but further lower our 2012-13 EPS by

6% and 6%, respectively. These changes are

mainly attributable to our 15-20% reduction in

contracted sales estimates for 2012-13, as well as

changes in ASP.

渐飞研究报告 - http://bg.panlv.net

abc

20

Financial Institutions Group China Real Estate 4 January 2012

Shui On Land (272 HK; OW; TP HKD2.9)

We lift our 2011 EPS modestly by 3% to reflect

the disposal of IP in KIC, which is partially offset

by the share issuances from the recent acquisition

of Shui On Plaza and Langham Xintiandi. The

larger magnitude of EPS cuts in both 2012 (-15%)

and 2013 (-7%) mainly reflects the full dilution

effect from the issuances. As a reminder, SOL

will be issuing 614m shares to fund the

acquisitions in October 2011, representing 12% of

the pre-issuance share base.

SOHO (410 HK; N; TP HKD5.4)

With less than 50% sales target achieved as of

November, we believe the company will see a

slower sales schedule and possibly lower ASP in

the coming two years. We therefore reduce our

2012 and 2013 earnings estimates by 6% and 2%,

respectively, following our latest update (28

October 2011), OW: Hiccup in commercial sales,

but balance sheet strength is a boon).

Changes in NAV estimates We revise our 12-month forward NAV estimates

by 14% on average for stocks in our coverage

universe.

Key reasons behind our NAV revisions:

Incorporation of our revised property

price assumptions. In the coming 12 months,

we look for residential prices to decline 20%

in tier-1 cities, and decline 10% in both tier-2

and below cites.

Push back in sales proceeds, as a result the

scaled back contracted sales forecasts

discussed above.

Adaptation of a wider WACC range to more

accurately reflect the sizable differences in

the cost of debt, especially when comparisons

are made between SOEs and non-SOEs.

Note that the magnitude of our NAV revisions is

small, as more than 70% of most developers’

GAV estimates are derived from projects in tier-2

and below cities.

Adjustments in target NAV discounts We are widening our target NAV discounts for

COLI, Franshion, GZ R&F, KWG, Longfor,

Shimao and SOL, while narrowing the discount

level for Agile and CRL. Our adjustments are

based on developers’ sales achievement as of

November 2011, financial strength assessment,

risks associated with general operations, as well

as the state of the global economy. We are

otherwise maintaining target NAV discounts of

other stocks in our coverage universe, given that

the qualitative aspects of developers are

unchanged since our last sector report published

on 10 June 2011 Price cuts may be a blessing in

disguise.

Note that our target discounts range from half a

standard deviation above the mean to one standard

deviation below the historical average, which are

reflective of the uncertain and slowing residential

sales outlook, as well as company-specific factors

such as contracted sales progress and financial

flexibility. Within our coverage universe, we

attach the smallest target discounts to COLI, CRL

and Longfor, owing to their superior execution,

earnings visibility and cost of capital advantage.

渐飞研究报告 - http://bg.panlv.net

abc

21

Financial Institutions Group China Real Estate 4 January 2012

Earnings and NAV sensitivity ASP sensitivity of our earnings and NAV

estimates depends on developers’ geographic

landbank exposure. As we have assumed a larger

magnitude of price decline in tier-1 cities,

developers with higher exposure these regions

will be harder hit.

2012e earnings sensitivity to ASP changes 2013e earnings sensitivity to ASP changes NAV sensitivity to ASP changes (as of December 2011)

-50%

-40%

-30%

-20%

-10%

0%

Agi

le

CO

LI

CR

L

Fra

nshi

on

GZ

R&

F

KW

G

Long

for

Shi

mao

SO

L

Soh

o

ASP dow n 10% ASP dow n 20%

-50%

-40%

-30%

-20%

-10%

0%

Agi

le

CO

LI

CR

L

Fra

nshi

on

GZ

R&

F

KW

G

Long

for

Shi

mao

Shu

i On

Soh

o

ASP dow n 10% ASP dow n 20%

-50%

-40%

-30%

-20%

-10%

0%

Agi

le

CO

LI

CR

L

Fra

nshi

on

GZ

R&

F

KW

G

Long

for

Shi

mao

Shu

i On

Soh

o

ASP dow n 10% ASP dow n 20%

Source: HSBC estimates Source: HSBC estimates Source: HSBC estimates

渐飞研究报告 - http://bg.panlv.net

abc

22

Financial Institutions Group China Real Estate 4 January 2012

Changes in ratings, NAVs and target prices

Company _____ Rating _____ _______Forward NAV (HKD) _______ _______ Target discount (%) ________ ______ Target price (HKD)________ Potential ___ Implied PE by our TP ___Name Old New Old New % Chg Old New % Chg Old New % Chg return* FY12e FY13e

Agile OW OW(V) 20.5 15.2 -26% -53% -45% 8% 9.6 8.4 -13% 26% 4.9 4.5 COLI OW OW(V) 24.2 22.1 -9% 0% -5% -5% 24.2 21.0 -13% 65% 10.4 9.1 CRL N OW(V) 24.4 20.7 -15% -55% -15% 40% 11.0 17.6 60% 44% 11.8 10.5 Franshion OW OW 5.4 4.8 -12% -55% -60% -5% 2.5 1.9 -24% 30% 6.4 5.5 R&F OW OW(V) 20.4 17.8 -12% -56% -60% -4% 8.9 7.1 -20% 26% 4.5 3.9 KWG OW OW(V) 15.5 13.0 -16% -45% -65% -20% 8.5 4.5 -47% 81% 5.6 4.7 Longfor OW OW(V) 21.5 19.0 -11% -20% -30% -10% 17.2 13.3 -22% 55% 10.9 8.5 Shimao OW N(V) 19.5 17.5 -11% -57% -60% -3% 8.4 7.0 -17% 12% 4.7 4.2 Shui On Land OW OW 8.8 7.3 -17% -55% -60% -5% 4.0 2.9 -27% 29% 9.2 6.5 SOHO OW N 11.6 9.8 -16% -45% -45% 0% 6.4 5.4 -16% 10% 6.1 4.0 Yanlord n/a N(V) n/a 2.4 n/a n/a -58% n/a n/a 1.0 n/a 7% 7.5 6.9Simple average -14% 0% -14% 7.5 6.3

* Potential return equals the percentage difference between the current share price (as of 30 December 2011) and the target price, plus the forecast dividend yield

We initiated coverage of Yanlord stock in a separate note (Initiate N(V): In need of a strategic shift, 4 January 2012) Source: HSBC estimates

渐飞研究报告 - http://bg.panlv.net

abc

23

Financial Institutions Group China Real Estate 4 January 2012

Conventional valuation metrics signal “buys” The sector’s average NAV discount currently stands

at above 50%, based on our revised NAV estimates

which employ the revised set of WACC determined

in the section - Cost of capital under the limelight

(pg 12). While the current NAV discount level,

together with PE, appear constructive from a

historical standpoint, there exists the counter

argument of NAV estimates being subjective given

the sensitivity to different assumptions such as ASP

levels and discount rates, although our estimates

already incorporate price cuts nationwide. At the

same time, earnings estimates are also susceptible to

varying degrees of adjustments given developers’

flexibility to shift completion schedules. Hence, we

believe it is relevant to gauge potential share price

downside from the current level, and we do so

Downside protection – theoretical liquidation value

Traditional valuation metrics are indicating “buy” signals for most stocks in our coverage universe

While we are not bullish on a sector-wide basis, we argue that stocks are well protected on the

downside based on our liquidation value analysis which gives a theoretical floor for share prices

The degree of relative downside protection is dependent on developers’ landbank geographic

distribution; developers with higher exposure to top-tier cities are better protected

Floor value calculation for stocks under coverage

(RMBm) COLI CRL Franshion GZ R&F KWG Longfor Shimao SOL SOHO

DP-cost (a) 85,511 42,518 11,662 31,452 17,800 38,227 21,781 19,073 15,235 IP-cost (b) 420 13,045 1,600 339 1,268 581 1,227 1,341 3,697 IP-completed (c) 10,934 24,836 14,768 11,532 4,132 4,047 14,332 6,788 7,070 Net debt (d) (20,587) (25,141) (13,596) (26,332) (12,185) (11,324) (23,131) (16,468) 1,386 Floor value (e) = (a+b+c+d) 76,278 55,259 14,435 16,991 11,016 31,530 14,210 10,734 27,388 No. of shares (f) 8,173 5,804 9,161 3,222 2,894 5,155 3,545 5,212 5,185 Floor value per share (HKD) (g) = (e)/(f) 11.0 11.2 1.9 6.2 4.5 7.2 4.7 2.4 6.2 Current share price* (h) 13.0 12.5 1.5 6.1 2.6 8.8 6.6 2.4 5.2Share price above or (below) floor value (g)/(h)-1 18% 11% -19% -1% -41% 22% 41% -3% -17%

Source: DataStream, HSBC estimates

渐飞研究报告 - http://bg.panlv.net

abc

24

Financial Institutions Group China Real Estate 4 January 2012

through a cost-based valuation method akin to a

liquidation analysis.

Deriving theoretical liquidation value Our liquidation analysis uses a cost-based

valuation metric to minimize assumptions used in

typical NAV estimates. This can also be

interpreted as the bear-case NAV, or floor value

for the stocks.

Our calculated floor values are largely reflective of

the sunk costs that developers have incurred, which

provides a tangible way of measuring a company’s

net worth. After summation of sunk cost

components, we subtract net debt from the

aggregate sunk cost to arrive at the final floor value.

Key assumptions and remarks:

Sunk costs include both land and construction

costs.

The sunk costs that we incorporate in the

calculation of a developers’ net worth is

dependent on the completion timeline on a

project-by-project basis, adjusted by an

accountability factor.

The accountability factor adjusts for the

difference in pre-sales timeline, as value

should not be attributed to projects that have

commenced pre-sale whereby the proceeds

have been captured on the balance sheet.

For development properties, the rule of thumb

is to account for costs that have been incurred

for projects which are currently on sale or

pending for pre-sale, as the sales proceeds

have yet to be recognized.

For IP under construction, sunk costs are

accounted for in a similar manner, based on

the projects’ all-in costs.

For completed IP, we value the assets based

on an income capitalization approach using

gross cap rates of 5-12%.

Having identified the cost-based valuation for

each of the property components discussed,

we apply a “haircut” to account for the

perception that the incremental costs of

acquiring new sites have fallen, and that

capital values of the completed IP have

declined, as market sentiment has

deteriorated.

The haircuts we apply are 30% and 50% for

values attributed to tier-1 and tier-2 cities,

respectively, while prospective values for

lower-tier cities have been omitted. This is

based on the premise that market clearance

prices for top-tier cities are more visible and

justifiable based on actual market

transactions, while price discovery in lower-

tier cities will become more difficult as

transaction volume drops

After summation of all sunk cost components,

we deduct the net debt (as at end-2011) to

arrive at the floor value, which should be

interpreted as the bear-case NAV.

As a side note, we use attributable values for our

floor value calculation as we do not believe

balance sheet items, presented on a consolidated

basis, are appropriate for this exercise.

GAV breakdown by tier cities

(%) Tier 1 Tier 2 Tier 3 Total

Agile Properties 20 80 - 100China Overseas Land 20 73 7 100China Resources Land 22 65 13 100Franshion Properties 24 74 2 100Guangzhou R&F 37 53 10 100KWG Property 53 47 - 100Longfor properties 25 42 33 100Shimao Property 14 70 16 100Shui On Land 23 77 - 100SOHO China 100 - - 100Yanlord 42 55 3 100Simple average 35 57 8Weighted average* 30 60 10

Source: HSBC estimates *by market capitalisation

渐飞研究报告 - http://bg.panlv.net

abc

25

Financial Institutions Group China Real Estate 4 January 2012

Differentiation among developers Our methodology favours developers with higher

exposure to top-tier cities, due to higher visibility

on market clearing prices (of both properties and

raw sites), given the availability of more frequent

and transparent comparable transactions.

Visibility deteriorates in the lower-tier cities,

which makes it more difficult to grasp the

underlying true value.

Hence, we expect developers with mostly

exposure in higher-tier cities to offer a higher

degree of downside protection. Not surprisingly,

within our coverage universe, we find four stocks

are better placed: namely Franshion, KWG, Shui

On Land and Soho China, with current share

prices at or below our estimated floor values.

Development properties sunk cost analysis

_______________ Key assumptions ______________ __________ Key components in floor value calculation _________Project completion schedule

Period for which construction cost will be

incurred

Contracted sales period

Sunk cost Adjustment factor in sunk cost

Remarks

FY11 FY09-11 FY11 & FY10 None 0% Since these projects are substantially sold, none of the cost incurred will be accounted for in our floor value as sales have been converted into cash captured on the balance sheet

FY12 FY10-12 FY11 & FY12 (incurred construction & land cost)*

adj factor 50% Assuming that half of the projects are sold in FY11 and FY12,

respectively, we only incorporate 50% of the incurred costs in our calculation

FY13 FY11-13 FY12 & FY13 (incurred construction & land cost)*adj factor

100% With these projects expected to commence presale in FY12 onwards, construction costs incurred and to be incurred will be fully accounted for in our floor value, given that sales have yet been materialized and recognized

Source: HSBC

渐飞研究报告 - http://bg.panlv.net

abc

26

Financial Institutions Group China Real Estate 4 January 2012

Cash is king In the early evolution of the sector (2004-07)

much of the market’s focus was on a developer’s

ability to expand its landbank based on the

premise of “the bigger the better”. Hence, the

market attached a premium to developers with the

strongest purchasing power, resulting in the land

acquisition frenzy seen in 2007. During the credit

crisis of 2008, developers struggled to recapitalize

their balance sheets amid a backdrop of domestic

property tightening measures.

Investors have since placed increasing emphasis

on contracted sales and cash collection, as they

are key determinants of developers’ cash flow

management ability and will be of paramount

importance to “weather the storm”.

Balance sheets constrained, but no liquidity issue Against the backdrop of shrinking transaction

volumes, delayed cash receipts upon contracted

sales and a generally difficult financing

environment, balance sheet management will be

of rising importance for developers in 2012.

However, we deduce that the overall liquidity

position for the sector will remain manageable.

Our core cash flow analysis reveals that COLI,

Longfor and Agile are financially well equipped

to withstand unforeseen contracted sales shortfall,

while Shui On Land and Yanlord are under more

balance sheet strain. In this exercise, we have

assumed no cash outlay on new site acquisitions

Assessing the cash flow buffer Developers’ balance sheets are constrained amid shrinking transaction volumes and delayed cash

receipts, but the overall liquidity position is still manageable

COLI, Longfor and Agile are financially well equipped to withstand unforeseen contracted sales

shortfall, while SOL and Yanlord are under more balance sheet strain

China Developers’ key performance benchmarks

Key benchmarks Remarks

Contracted sales delivery Contracted sales delivery has become a prerequisite for success, given that contracted sales provides the single most important source of cash inflow. Furthermore, contracted sales also help gauge underlying demand of the physical property market

Market share gain In an environment where the size of the pie is constrained by shrinking transaction volume, developers' performance hinges on their ability to gain market share. In our view, the current policy and credit environment both indicate the likelihood of continual market consolidation, pushing towards to the favour of bigger developers

Consistency in operating cash flow Consistency in operating cash flow ultimately determines developers' ability to withstand unforeseen contracted sales shortfall, and hence a key benchmark to judge financial liquidity

Balance sheet preservation While balance sheet preservation is a function of consistency in operating cash flow, year-end gearing levels are also dependent on other factors such as capital outlay spent on acquisition of new projects, which is within the control of developers. This means that prudent balance sheet managers will scale back on acquisition outlays when times are challenging

Cash collection ratio This is a new found metric that only become relevant in recent months owing to delayed mortgage disbursements from banks upon contracted sales. In light of continual tightness in credit, the metric will be under the spot light in 2012

Source: HSBC

渐飞研究报告 - http://bg.panlv.net

abc

27

Financial Institutions Group China Real Estate 4 January 2012

beyond that already committed. In addition, we

assume no significant long-term debt repayment

as the sector’s bond maturity profile is heavily

concentrated in 2014 and beyond.

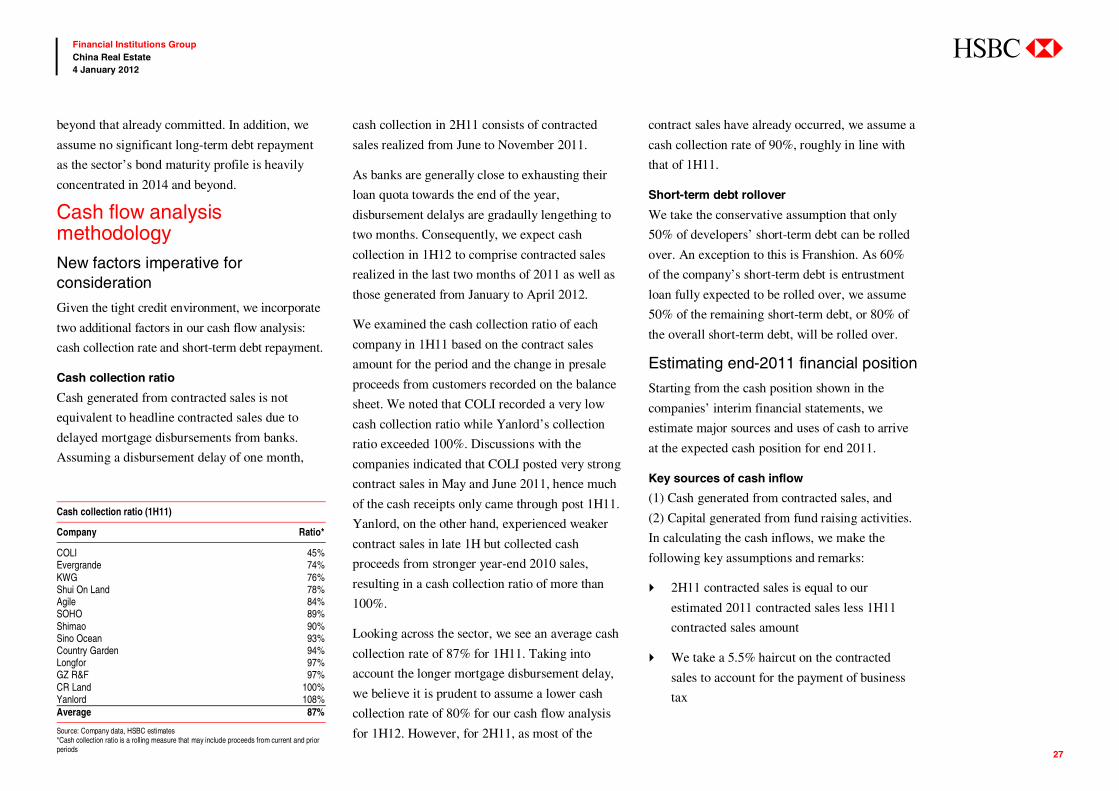

Cash flow analysis methodology New factors imperative for consideration

Given the tight credit environment, we incorporate

two additional factors in our cash flow analysis:

cash collection rate and short-term debt repayment.

Cash collection ratio

Cash generated from contracted sales is not

equivalent to headline contracted sales due to

delayed mortgage disbursements from banks.

Assuming a disbursement delay of one month,

cash collection in 2H11 consists of contracted

sales realized from June to November 2011.

As banks are generally close to exhausting their

loan quota towards the end of the year,

disbursement delalys are gradaully lengething to

two months. Consequently, we expect cash

collection in 1H12 to comprise contracted sales

realized in the last two months of 2011 as well as

those generated from January to April 2012.

We examined the cash collection ratio of each

company in 1H11 based on the contract sales

amount for the period and the change in presale

proceeds from customers recorded on the balance

sheet. We noted that COLI recorded a very low

cash collection ratio while Yanlord’s collection

ratio exceeded 100%. Discussions with the

companies indicated that COLI posted very strong

contract sales in May and June 2011, hence much

of the cash receipts only came through post 1H11.

Yanlord, on the other hand, experienced weaker

contract sales in late 1H but collected cash

proceeds from stronger year-end 2010 sales,

resulting in a cash collection ratio of more than

100%.

Looking across the sector, we see an average cash

collection rate of 87% for 1H11. Taking into

account the longer mortgage disbursement delay,

we believe it is prudent to assume a lower cash

collection rate of 80% for our cash flow analysis

for 1H12. However, for 2H11, as most of the

contract sales have already occurred, we assume a

cash collection rate of 90%, roughly in line with

that of 1H11.

Short-term debt rollover

We take the conservative assumption that only

50% of developers’ short-term debt can be rolled

over. An exception to this is Franshion. As 60%

of the company’s short-term debt is entrustment

loan fully expected to be rolled over, we assume

50% of the remaining short-term debt, or 80% of

the overall short-term debt, will be rolled over.

Estimating end-2011 financial position

Starting from the cash position shown in the

companies’ interim financial statements, we

estimate major sources and uses of cash to arrive

at the expected cash position for end 2011.

Key sources of cash inflow

(1) Cash generated from contracted sales, and

(2) Capital generated from fund raising activities.

In calculating the cash inflows, we make the

following key assumptions and remarks:

2H11 contracted sales is equal to our

estimated 2011 contracted sales less 1H11

contracted sales amount

We take a 5.5% haircut on the contracted

sales to account for the payment of business

tax

Cash collection ratio (1H11)

Company Ratio*

COLI 45% Evergrande 74% KWG 76% Shui On Land 78% Agile 84% SOHO 89% Shimao 90% Sino Ocean 93% Country Garden 94% Longfor 97% GZ R&F 97% CR Land 100% Yanlord 108% Average 87%

Source: Company data, HSBC estimates *Cash collection ratio is a rolling measure that may include proceeds from current and prior periods

渐飞研究报告 - http://bg.panlv.net

abc

28

Financial Institutions Group China Real Estate 4 January 2012

2H11 cash collection of 90% across the

board, to reflect slow mortgage disbursement

from banks, except COLI due to its back-end

loaded sales in 1H

Decline in contracted sales proceeds in the

range of 10-20% in 1H12

50% of construction cost is funded through

drawdown of construction loans

The other key source of cash inflow is cash

generated from fund raising activities, which

is based on financing transactions announced.

Key sources of cash outflow

Major uses of cash include construction cost, land

premium payment, finance cost, SG&A expenses,

income tax and LAT, debt repayment, dividend

payment and other. Each item is derived based on

either company guidance or projections based on

historical data. In calculating cash outflows, we

make the following key assumptions and remarks:

Land premium payments are based on

committed amount as of June 2011. We

assume no additional land acquisitions in our

cash flow analysis.

Construction cost is based on the projected

value from our proprietary model. We also

assume 50% of the construction cost is

funded via construction loan drawdown.

SG&A, income tax, finance cost and LAT are

based on project value from our proprietary

model. Finance cost is taken as the cash

interest expense, inclusive of capitalization.

LAT is taken as recognized LAT expense

from two years prior, reflecting the timing of

actual LAT payment.

For debt repayment, we assume the cash

outflow is equal to 50% of the debt amount

under the short-term liability. This assumes

the company will be able to roll over the

remaining 50% of its short-term bank loans.

For dividend payment, we assume the interim

dividend announced in 1H will be paid out in

2H. We also assume any dividend payable

(declared from prior periods) to be settled in

2H11.

Accounting for each of the aforementioned cash

components, we arrive at the expected cash

position for 2H11. Most developers have a