climate change: strategic issues for management

TRANSCRIPT

Climate Change: Strategic Issues for Management AccountingManagement Accounting

ByProf. Janek Ratnatunga

Professor and Head of SchoolUniversity of South Australia

Research sponsored by:

The Greenhouse Effect

Sources Sinks

The Hockey Stick

• CO2 fromSiple Ice Core pvs. Age.

• However, there is much debate (especially amongstamongst politicians) if Human activity has caused this “Hockey Stick” effect.

Carbon-ethics

• Do We Need an Economic Solution (e.g. Kyoto)?– The Schumacherian ideal– Meta Economics

• We should reduce our carbon footprint purely on moral grounds

Intermediate Variable ConsequencesPreconditions

Behavioral Response by

Individuals and Business Entities

Reduction of Greenhouse Gas

Emissions

Change in Value of Business

Entity

Greenhouse Gas Emissions in

Nature

Greenhouse Gas Emissions by

Humans

Carbon-ethics: End of Pipe Solutions

• Good Carbon Behaviour (Ethical solutions)– Reducing Carbon Footprint

Problem

– Lifestyle changes (End-of-Pipe Solutions)

End of Pipe

Solution

Carbon-Ethics for Business

Change Lightbulbs to Low Emission Shut off Computers (no standby)Pay the Carbon Tax Switch off the Lights At Quitting TimeBuild a Skyscraper End the Paper ChaseBuild a Skyscraper End the Paper ChaseTurn Up the Geothermal Heat Play the MarketCapture the Carbon Think Outside the PackagingLet Employees Work Close to Home Trade Carbon for CapitalPay Your Bills Online Set an Organisational Carbon BudgetOpen a Window Pay For Your Carbon SinsAsk the Experts For An Energy Audit Make One Right Turn After AnotherBuy Green Power Plant a Tree in the TropicsRemove the tie (Everyday is Casual Friday)

Drive Green (Change company Vehicles to Bio fuels)

Fly Straight to Location If You Must Burn Coal, Do it RightCopy California’s State Emission Levels

Set a Higher Carbon Emission Standard

Turn Food Into Fuel (Bio Fuels) Illuminate Public Spaces with LEDs

Carbon-Ethics for Individuals

Get Blueprints for a Green House Fly Straight between LocationsChange Light bulbs to Low Emission Support your Local FarmerPay the Carbon Offsets when Buying Plant a Bamboo FenceM f th M i H G W ddi (i B L ll )Move from the Mansion Have a Green Wedding (i.e. Buy Locally)Hang Up a Clothes Line Remove the Tie (Casual Business Attire)Give New Life to Your Old Warm Clothes Drive Green on the using Bio-Fuel CarsUse More Geothermal Heat Just Say No to Plastic Bags Take Another Look at Vintage Clothes Switch off the Lights At Quitting TimeWork Close to Home Shut off your ComputerRide the Bus End the Paper ChaseMove to a High Rise Building Think Outside the PackagingPay Your Bills Online Trade Carbon for CapitalOpen a Window (natural cooling) Make Your Garden GrowOpen a Window (natural cooling) Make Your Garden GrowAsk the Experts For An Energy Audit of Your Home

Wear Green Eye Shadow (Made from Renewable Resources)

Buy Green Power, At Home or Away Fill Car Up With PassengersCheck the Label (cheap prices for overseas products because no Carbon costs are paid)

Rake in the Fall Colours (Rather than using Leaf Blowers)

Properly iInsulate Your Water Heater Check Your TiresAvoid the Meat Products Set a Personal Carbon BudgetBe Aggressive about Passive Houses Consume Less, Share More, Live Simply

• The Emerging Paradigm Of Carbonomics– 21st Century ‘Needs’ met with 18th Century ‘Power’

Carbonomics: Start of Pipe Solutions

– Economic incentives for the development of sustainable technologies that reduce CO2 emissions (Winners and Losers)

• Wind Farms• Geothermal• Water (Hydro and Ocean Waves)

N• Nuclear

Start of Pipe Solution

No Problem

• The Kyoto Protocol (ratified by over 150 countries)– Some have “caps” (e.g. European Countries)

Kyoto Mechanisms

– Some are “thinking” about it (e.g. Australia)– Some are “exempt”(e.g. China, India, Indonesia)

• International (Cross-Country) Mechanisms– Joint Implementation (JI)– Clean Development Mechanism (CDM): – International Emission Trading (IET)International Emission Trading (IET)

• All three mechanisms required the concept of a ‘carbon credit’ as a: – measurable and tradable instrument – that is acceptable across nations.

Carbon Credit:

Carbon Credit Definition

Each carbon credit represents one metric tonne of CO2

–either removed from the atmosphere or –saved from being emitted.

• Country Level Issues (Three principle Ways to ‘Manage’ Carbon Emission Targets):

Managing Carbon Emission Targets

– By Taxation. By imposing a straight tax on emissions.– By Allocating ‘permits’ or ‘ration cards’ to business

entities or individuals for a cap and trade system.– By Approving certain organisations as being able to issue

carbon credits (called ‘abatement certificates’)

• Carbon Emissions Trading (Requires a Cap-and-Trade system)

Carbon Emissions Trading

– Ideally be based on free-market principles– Each individual emission allowance has a ‘vintage year’

designation (that is, the year an allowance may be used)– Brokers and other non-participants typically buy and sell

emission allowances in (vibrant) secondary markets.The European Union Emission Trading Scheme (EU– The European Union Emission Trading Scheme (EU ETS) is the world’s largest multi-country cap and trade system.

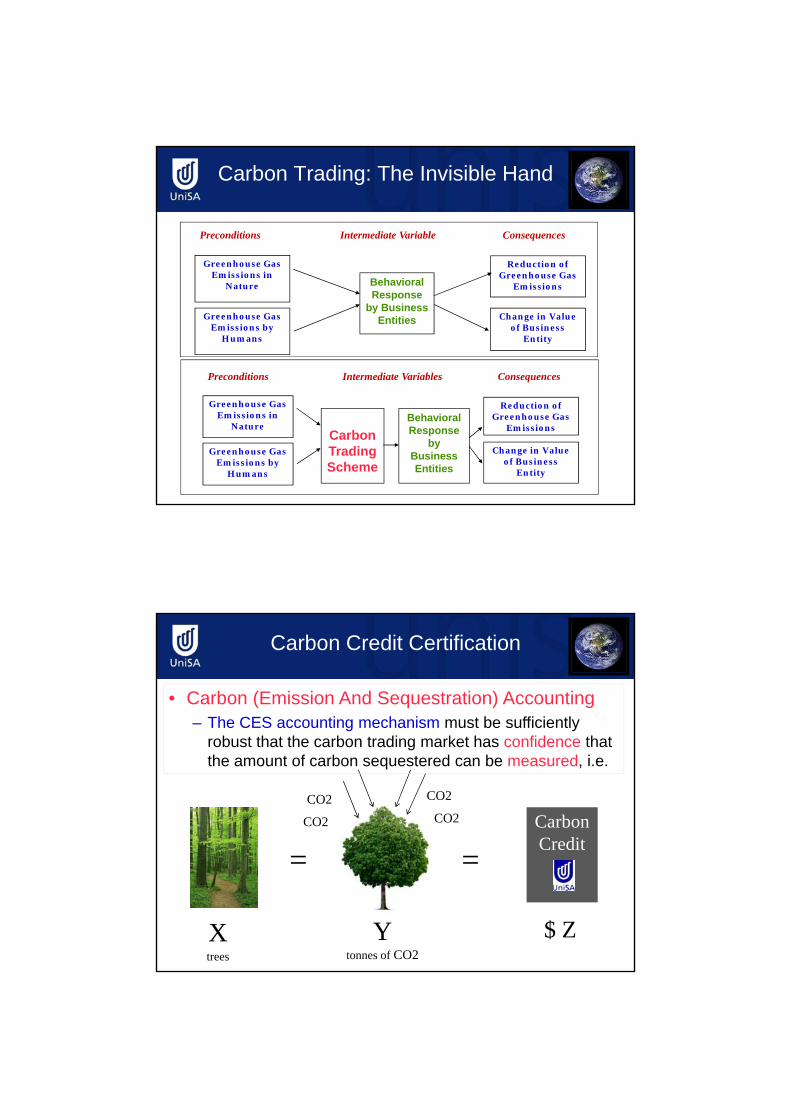

Carbon Trading: The Invisible Hand

Intermediate Variable ConsequencesPreconditions

Reduction of Greenhouse Gas

Behavioral Response

by Business Entities

Reduction of Greenhouse Gas

Emissions

Change in Value of Business

Entity

Greenhouse Gas Emissions in

Nature

Greenhouse Gas Emissions by

Humans

Intermediate Variables ConsequencesPreconditions

Behavioral Response

by Business Entities

Carbon Trading Scheme

Reduction of Greenhouse Gas

Emissions

Change in Value of Business

Entity

Greenhouse Gas Emissions in

Nature

Greenhouse Gas Emissions by

Humans

Carbon Credit Certification

• Carbon (Emission And Sequestration) Accounting– The CES accounting mechanism must be sufficiently

CarbonCredit

CO2 CO2

CO2 CO2

robust that the carbon trading market has confidence that the amount of carbon sequestered can be measured, i.e.

Xtrees

= =

Ytonnes of CO2

$ Z

• CES Accounting Standards– Any CES accounting standard developed by a country or

CES Accounting & Assurance

y g p y yNGO will need to be consistent with the Intergovernmental Panel on Climate Change (IPCC)principles.

– There are at least 21 organisations offering accreditation and auditing services, across the globe

– the new market is largely unregulated and lacksthe new market is largely unregulated and lacks transparency

Management Accounting Issue

• Firms operating in a carbon rationing jurisdiction:

Carbon Investment Appraisal

The options available to manage carbon emissions liability:carbon emissions liability:

• Do nothing and buy carbon credits• Undertake Carbonvestments:

– Undertake internal projects to lower carbon liability

– Invest in external projects to offsetInvest in external projects to offset carbon footprints

– A combination of both internal and external investments

Expected usage

Emissions Management: Alternative Strategy No.1

usage 100,000 MT CO 2 Equivalent

Buy CreditsWait till End of Reporting Period

Buy Credits in ETS Market (Max Price A$46)

Max Cost A$ 4.6 m

Exp. Usage 100,000 MT

Undertake Internal Abatement Projects(Cost: $0.3m); CO2 saving: 40,000 MT)

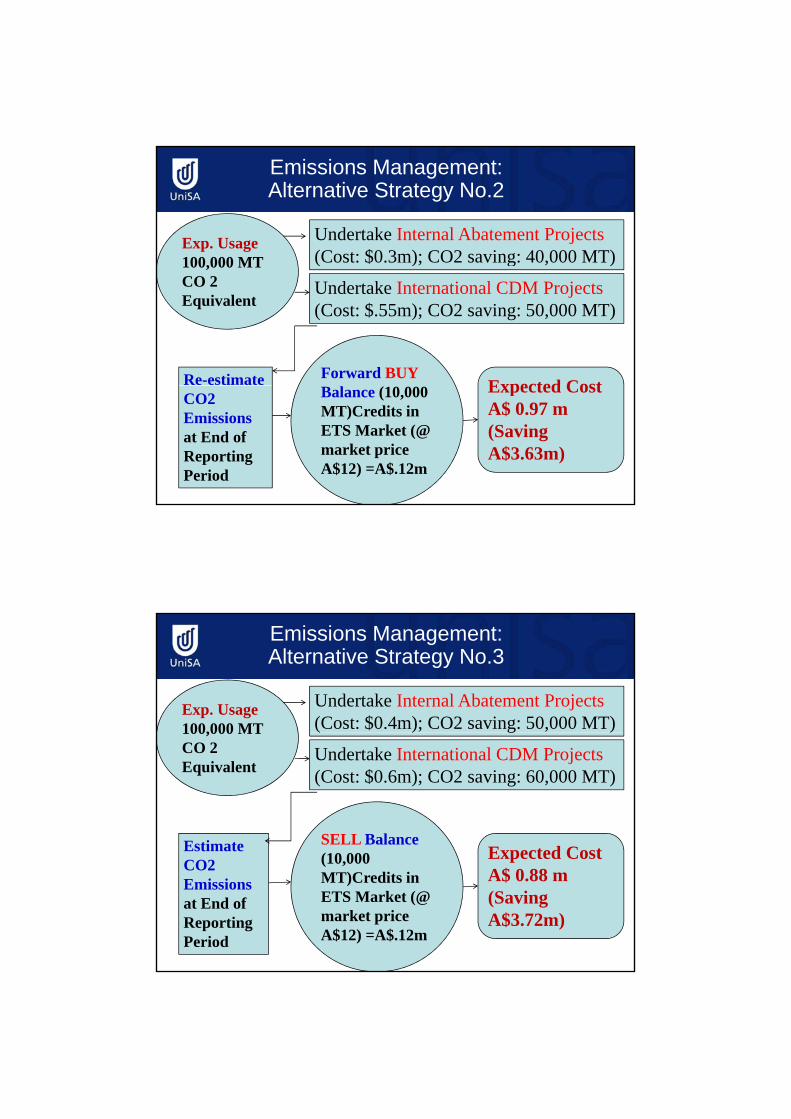

Emissions Management: Alternative Strategy No.2

100,000 MT CO 2 Equivalent

Re-estimate Forward BUYExpected Cost

( ) g )

Undertake International CDM Projects(Cost: $.55m); CO2 saving: 50,000 MT)

CO2 Emissions at End of Reporting Period

Balance (10,000 MT)Credits in ETS Market (@ market price A$12) =A$.12m

Expected Cost A$ 0.97 m (Saving A$3.63m)

Exp. Usage 100,000 MT

Undertake Internal Abatement Projects(Cost: $0.4m); CO2 saving: 50,000 MT)

Emissions Management: Alternative Strategy No.3

SELL Balance Expected Cost

100,000 MT CO 2 Equivalent

Estimate

( ) g )

Undertake International CDM Projects(Cost: $0.6m); CO2 saving: 60,000 MT)

(10,000 MT)Credits in ETS Market (@ market price A$12) =A$.12m

Expected Cost A$ 0.88 m (Saving A$3.72m)

CO2 Emissions at End of Reporting Period

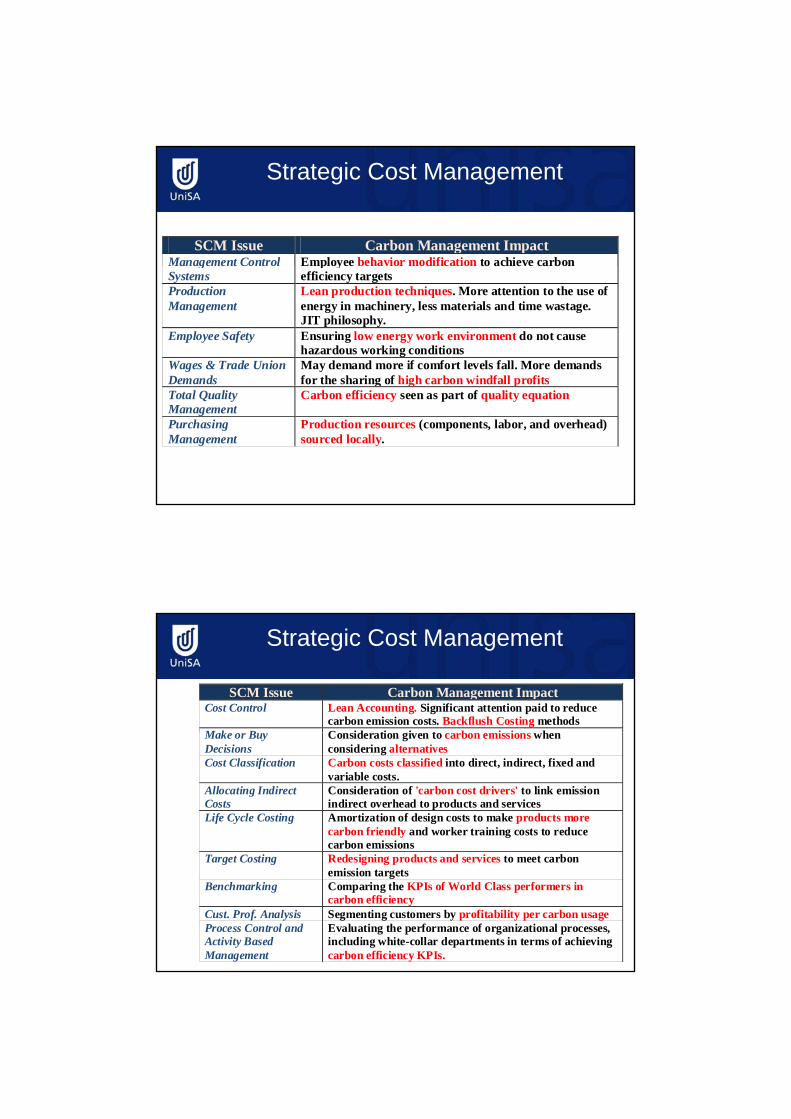

Strategic Cost Management

SCM Issue Carbon Management ImpactManagement Control Employee behavior modification to achieve carbon Management Control Systems

Employee behavior modification to achieve carbon efficiency targets

Production Management

Lean production techniques. More attention to the use of energy in machinery, less materials and time wastage. JIT philosophy.

Employee Safety Ensuring low energy work environment do not cause hazardous working conditions

Wages & Trade Union Demands

May demand more if comfort levels fall. More demands for the sharing of high carbon windfall profitsg g p

Total Quality Management

Carbon efficiency seen as part of quality equation

Purchasing Management

Production resources (components, labor, and overhead) sourced locally.

Strategic Cost Management

SCM Issue Carbon Management ImpactCost Control Lean Accounting. Significant attention paid to reduce

carbon emission costs. Backflush Costing methods M k B C id ti i t b i i hMake or Buy Decisions

Consideration given to carbon emissions when considering alternatives

Cost Classification Carbon costs classified into direct, indirect, fixed and variable costs.

Allocating Indirect Costs

Consideration of 'carbon cost drivers' to link emission indirect overhead to products and services

Life Cycle Costing Amortization of design costs to make products more carbon friendly and worker training costs to reduce carbon emissions

Target Costing Redesigning products and services to meet carbon emission targets

Benchmarking Comparing the KPIs of World Class performers in carbon efficiency

Cust. Prof. Analysis Segmenting customers by profitability per carbon usage Process Control and Activity Based Management

Evaluating the performance of organizational processes, including white-collar departments in terms of achieving carbon efficiency KPIs.

Strategic Cost Management

SCM Issue Carbon Management ImpactEfficiency or Productivity

Consideration given not only to economic efficiency, but also carbon usage efficiency.

Price Relationship or Reductions in purchase prices considered via the sale of pRecovery

p pcarbon efficiency credits

Overall Effectiveness This profitability of the bottom-line figure given in terms of both economic and environmental effectiveness.

Value-Adding/Non-Value Adding Work

All reworks, recoveries, errors etc. considered to be avoidable carbon emitting activities

Executive Information Systems (EIS)

The drill-down facilities to be extended to financial and non-financial carbon emitting measures.

Corporate Governance Accountability and transparency issues extended reporting on carbon management initiativesreporting on carbon management initiatives

Enforcement and Compliance

Voluntary and mandatory enforcement of carbon emission targets

The Strategic Audit Extended to cover the expected future carbon footprint of the organization due to its production, marketing, logistics, capital investment and HRM practices

Corporate Reputation Audit

The evaluation of the organization’s image and brand with regards to being a responsible carbon citizen of the world.

Strategic Management AccountingSMA Issue Carbon Management Impact

Business Policy Primary Objective Sustainable Value Creation

C titi Carbon efficienc seen as a marketing mi ariable inCompetitive Advantage

Carbon efficiency seen as a marketing mix variable in product differentiation. An Efficient Carbon Management (ECM) focus also taken in cost leadership strategies.

Line-of-Business ECM seen as a potential line-of-business Competition and Industry Structures

Adding a sixth force to Porter's Five Forces Model - the impact on the Industry of Carbon regulation (Porter, 1980 and 1983).

Gap Analysis Strategies considered to close gap between current emission levels and future emission targets

Environmental Externalities

Considered 'internalities' in product-market decision making and HRM

Risk Management Consideration of the impact on cash flows and reputation of the company as a result of the carbon strategy positioning of the company. Risk vs. Reward outcomes (e.g. cash flow at risk) should be considered.

SMA Issue Carbon Management Impact

Strategic Management Accounting

Human Resource Management Corporate Culture A carbon lifestyle culture from grass roots level upwards.

Low carbon footprint activities encouraged. Excellence sought in seeking continuous improvement in ECM

Empowerment Employees given resources and responsibility to participate in ECM in lowering the organization’s carbon footprint

SMA Issue Carbon Management Impact Marketing Strategy P d t d M k t C b i t id ti id d t ti ll i

Strategic Management Accounting

Products and Markets Carbon impact considerations considered systematically in all product-market strategies

Marketing Research Undertaken to determine the needs of customers in terms of participating in reducing carbon emissions and the incremental price they are willing to pay for this (carbon consciousness)

Market Segmentation Separating customers geographically, demographically and psychographically in terms of their carbon p y g p yconsciousness.

Positioning Strategy Consideration of taking an 'active or 'passive' positioning in terms of ECM as a source of competitive advantage.

The Product Life Cycle (P.L.C.)

Consideration of the carbon footprint left by product throughout its life cycle, especially in the decline and obsolescence stages.

SMA Issue Carbon Management Impact Marketing Strategy (Cont) Market Penetration Strategies

Using carbon efficiency of existing products as an attribute to sell more to existing carbon conscious customers

k l i ffi i f i i

Strategic Management Accounting

Market Development Strategies

Using carbon efficiency of existing products as an attribute to sell new carbon conscious customers in new segments

Product Development Strategies

Incorporating carbon efficiency as an attribute in new product designs to keep existing carbon conscious customers loyal to the brand

Diversification Strategies

Leaving industries having products and markets seen as high carbon emitting to new industries better long-term

b t i bl t (i l d i t t i JIcarbon sustainable prospects (includes investments in JIs, and CDMs under Kyoto).

Experience Curves Organizations with high experience in ECM products and services should have lower costs.

Budgeting for Marketing Activities

Budgets will incorporate ECM activities as potential revenues and cost savings. Carbon trading activities could be considered a separate line of business.

SMA Issue Carbon Management Impact Product Marketing Strategies The Product Portfolio (BCG) Matrix

Star products will have high market share and high

Strategic Management Accounting

(BCG) Matrix Star products will have high market share and high market growth opportunities in industries with better long-term carbon sustainable prospects.

New Product Development (NPD)

Designing products and services to meet carbon emission targets and marketing them as such

Product Abandonment

Product Review Teams to consider carbon footprint in addition to profitability targets

Inflation The passing on of mandatory carbon costs and taxes as hi h i ill i fl ihigher prices to consumers will cause inflation.

Packaging Consideration given to carbon footprint of packaging, in terms of functionalism, convenience, recyclability and also image.

After-Sales Service The carbon emission in terms of materials, labor and overhead of undertaking work due to meeting warranties and other after sales services should be costed into the product

SMA Issue Carbon Management Impact Pricing Strategy

Strategic Management Accounting

Pricing Analysis Carbon costs, carbon related competitor activity and the value of low-carbon footprint products to carbon conscious customers should be considered in such analyses

Elasticity of Demand The impact on demand due to changes in prices if carbon costs are incorporated.

Skimming Selling to high carbon conscious customers willing to pay a price well above costs

Penetration Absorbing carbon costs of products and services sold toPenetration Absorbing carbon costs of products and services sold to low carbon conscious customers to develop brand awareness. Productivity improvements can only be obtained either by lowering costs via ECM or changing customer carbon consciousness levels.

SMA Issue Carbon Management Impact

Strategic Management Accounting

International Business Strategy Exporting vs. International Operations

Carbon costs can be reduced via Joint Implementation (JI) and Clean Development Mechanism (CDM) investments as per the Kyoto protocol

Price Differentials and Carbon Dumping

Competing with countries that do not have carbon costs. Influencing government policy to impose countervailing carbon taxes.

Hedging Policies Ensuring that carbon credits in the overseas country is not edgi g olicies su g c bo c ed s e ove se s cou y s odevalued in terms of the parent country carbon credit pricing.

SMA Issue Carbon Management Impact Promotional Strategy

Strategic Management Accounting

Promotional "Pull" Strategy (via Advertising etc.)

An Integrated Marketing Communication (IMC) approach should be taken to promote how the product or service is reducing carbon footprint, e.g. via purchasing carbon offsets.

Promotional "Push" Strategy( via Sales Force)

Sales Force budgets, targets and incentive schemes geared towards extolling the attributes and pushing low carbon impact products. Traveling times on sales calls minimized to reduce carbon emissions. Bio-fuel cars used as sales

hi lvehicles.Sales Response Functions

Response of sales volume to carbon related promotions tracked.

Media Selection Strategies

Electronic media given higher priority to print media in order to reduce paper usage

SMA Issue Carbon Management Impact Supply Chain Strategies Product-Distance Carbon emission measurements in terms of Product-

Strategic Management Accounting

Distance. The longer the distance and the more players in the channels of distribution the higher is the carbon costs.

The Level of Service The Service - Cost Trade-off ( for the right product gets to the right place at the right time, should consider the carbon emissions required to provide this level of service.

Distribution Cost Accounting

Computation of carbon related costs in order processing, warehousing, transportation, and inventory control.

Transportation and Simplex Models

The use of these models to reduce transportation time and resulting reduction in carbon emissionsSimplex Models. resulting reduction in carbon emissions.

Channel Control Consideration of the motivation, relationships and conflict issues that arise when channels are asked to on-sell products and services using ECM approaches themselves

Channel Adaptability Consideration of the adaptability of channels to changes in product-markets as a result of reducing carbon footprint.

Distribution Cost Control

Using ratio analysis to ensure that economic analysis, and ECM in supply chain activities are both evaluated.

SMA Issue Carbon Management Impact Performance Evaluation Strategic Financial Structures (Gearing)

Consideration if carbon related investments should be financed via debt or equity. Ability to obtain shareholder and debt holder funding at favorable rates due to the use of such financing in ECM activities.

Strategic Management Accounting

g

Weighted Average Cost of Capital (WACC)

Calculating an organization’s carbon related Cost of Equity and Debt to calculate its overall Carbon-WACC. The equity and debt markets may value discount carbon intensive businesses (causing high financing costs) and place a value-premium on low carbon emitting businesses (causing low financing costs).

Corporate Performance

ROI used to evaluate ECM performance. If carbon related revenues and costs can be isolated as a separate line of

Perspectives business, this will enhance the evaluation.

Strategic Value Analysis

Calculation of value enhancement (or diminution) due to strategies relating to carbon related investments and operations

Valuing Strategic Investments

Valuation premium given to investments in ECM, such as investments in alternative energy assets and abatement activities (e.g.wind, biomass, solar, geothermal, nuclear)

SMA Issue Carbon Management Impact Performance Evaluation (Cont). Valuing Strategic Operations

These include operational adjustments to incumbent assets, changes to energy prices efficiencies in waste management

Strategic Management Accounting

Operations changes to energy prices, efficiencies in waste management, purchasing and sale of carbon credits and carbon related taxation.

Free Cash Flows Net Cash flows generated by carbon related activities less investments in carbon related non-current and current assets

The Business Value

The Net Present Value of expected future cash flows generated by strategic investments and operations in carbon related business.

The Balanced Corporate Report Card to incorporate financial and non-Scorecard

p p pfinancial KPIs with carbon focus. This could in addition to, or incorporated within the customer, innovation, internal business processes and financial focus.

Economic Value Added (EVA)

A charge against revenue is made for the cost of investments in carbon efficient assets. A separate Carbon-EVA can be calculated if carbon related net-income, investments and cost of capital can be isolated.

– An Australian Department of Climate Change (2008)policy paper states that properly qualified external

Professional Qualifications

auditors are needed, and must possess educational or professional qualifications in a relevant discipline.

– What is a ‘relevant discipline’ is not defined in the policy paper, and could cover specialist knowledge in a wide range of disciplines including:

• environmental law, ,• environmental science• bio-chemistry and • financial statement auditing (most likely)

– Clearly, therefore, the use of experts is encouraged in the policy paper (Department of Climate Change, 2008).

The ICCAA

– One of the reasons for setting up the ICCAA is to provide an integrated education program to Train and Certify such Experts.