company insight brgr in equity september 26,...

TRANSCRIPT

Ambit Capital and / or its affiliates do and seek to do business including investment banking with companies covered in its research reports. As a result, investors should be aware that Ambit Capital may have a conflict of interest that could affect the objectivity of this report. Investors should not consider this report as the only factor in making their investment decision.

Challenge and change

Berger has made several changes across sales, HR, IT and marketing since 2011: a) connecting directly with painters rather than through dealers; b) leveraging marketing for Silk and ‘express painting’ for channel visibility; c) pioneering use of mobile app in sales/distribution; and d) renewed focus on talent hiring and incentivisation. These have not only helped challenge Asian Paints’ dominance in some areas but also create a highly positive work culture which improves the prospect of market share gains and operational efficiencies in future. We expect 28% EPS CAGR over FY16-21 with ROCE rising from 21% to 35%. Our DCF-based fair value of `296 implies 42x FY18E P/E.

Competitive position: STRONG Changes to this position: STABLE Improving channel connect through sales initiatives taken over FY10-16 In the economy segment, Berger has pioneered direct interaction with painters (SKU-specific coupon codes, Centralised Helpline to verify product purchase) rather than approaching them through dealers. In the premium segment, ‘Express Painting Service’, training academy for painters and ad campaigns for ‘Silk’ are helping Berger convince dealers and painters to generate leads and stock its products in the channel. The firm is also pioneering IT initiatives like a mobile app that not only helps improve account settlements for dealers but also improves the sales team’s performance measurement. Better HR processes and work culture will help deepen Berger’s moats Since 2011, Berger has made changes like streamlining sales hiring and performance measurement across the country, shaking out sales sluggishness by hiring younger, more agile personnel, and altering incentive structures. These, combined with a long list of operational initiatives pioneered by Berger, have helped significantly improve the organisation’s work culture. These initiatives should help improve market share and margins Through the above initiatives, we expect Berger to gain ~500bps market share from Kansai and Akzo Nobel over FY16-21. Whilst the firm’s gross margin differential against Asian Paints has already narrowed from >500bps until FY10 to <270bps in FY16, we expect EBITDA margins to expand by ~350bps over FY16-21 as investments in employees, marketing initiatives and operational efficiencies start yielding results. Reiterate BUY; deserves to trade at a premium to its historical averages We expect 19%/28% revenue/EPS CAGR over FY16-21, with RoCEs rising from 21% in FY16 to 35% in FY21E. Our DCF factors in longevity of Berger’s growth profile given market share gains amidst 13.5%/11% decorative paint industry revenue CAGR over FY15-25/FY25-35. Our upgraded fair value of `296 (previously `267) implies 11% upside and 42x FY18E P/E. We expect Berger to trade at no more than 5-10% discount to Asian Paints in future.

COMPANY INSIGHT BRGR IN EQUITY September 26, 2016

Berger PaintsBUY

Consumer Discretionary

Recommendation Mcap (bn): `258/US$3.8 6M ADV (mn): `128/US$1.9 CMP: `266 TP (12 mths): `296 Upside (%): 11

Flags Accounting: GREEN Predictability: GREEN Earnings Momentum: GREEN

Performance (%)

Source: Bloomberg, Ambit Capital Research

Berger’s forensic score analysis

Source: Ambit ‘HAWK’, Ambit Capital research

Berger’s greatness score analysis

Source: Ambit ‘HAWK’, Ambit Capital research

70

100

130

160

190

Sep

15

Nov

15

Jan

16

Mar

16

May

16

Jul 1

6

Sep

16

BRGR Sensex

Research Analysts

Rakshit Ranjan, CFA

+91 22 3043 3201 [email protected]

Dhiraj Mistry, CFA +91 22 3043 3264

Key financials Year to March FY14 FY15 FY16 FY17E FY18E

Net Revenues (` mn) 38,697 43,221 46,341 53,642 64,098

Operating Profits (` mn) 4,314 5,107 6,554 9,043 10,787

Net Profits (` mn) 2,494 2,647 3,698 5,532 6,778

Diluted EPS (`) 2.6 2.7 3.8 5.7 7.0

RoE (%) 24.1% 22.2% 27.0% 33.4% 33.4%

P/E (x) 103.6 97.6 69.8 46.7 38.1

P/B (x) 16.5 14.6 12.5 14.1 11.6

Source: Company, Ambit Capital research

Berger Paints

September 26, 2016 Ambit Capital Pvt. Ltd. Page 2

Transforming from a follower to a challenger to Asian Paints “Since 2010, every year Berger has appeared to be a new organisation, vastly different from what it was in the preceding year.” – One of the largest dealers of Berger in North India during our conversation with him in Aug’16.

“Over the past five years, Berger has emerged as the only company which has the focus, willingness and ability to challenge Asian Paints. Whilst we do not feel this challenge in South Mumbai, a dealer in a smaller town cannot ignore Berger anymore.” – a large exclusive dealer of Asian Paints in Mumbai during our conversation with him in Sept’16.

As highlighted in our ‘coffee-can’ note on Berger (Click here), until 2010, Berger spent its efforts in catching-up with Asian Paints, better than its peers like Akzo Nobel and Kansai Nerolac. As a result, Berger had successfully grown up the ranks in market share to become the second largest player in the decorative paints industry in India from being the eight largest player until the late 1970s. Despite this, in 2010, the firm still lacked basic operational infrastructure, e.g. a) ERP systems were sub-optimal; b) timely product replenishment in the channel was difficult; and c) whilst Berger was gaining share in the economy segment, it was incredibly difficult to do the same in the premium segment against Asian Paints and Dulux (by Akzo Nobel).

However, since 2010, Mr. Abhijit Roy has implemented several initiatives which have substantially improved the firm’s operational capabilities, to the extent that in many aspects Berger has been the pioneer in introducing new initiatives in the industry. Based on our recent channel checks, we have given some examples of these initiatives below.

Sales-oriented initiatives implemented over FY10-16 Focusing on the painter rather than the dealer – winning formula in the economy segment

The extent of end-customer involvement in the paint process is exceptionally low in rural areas and economy paint segment with the customer relying almost entirely on the painter for selection of the paint product. Under Abhijit Roy, Berger has been focusing on the painter (the key influencer in the paint project) in a big way over the past six year. This was achieved through a combination of the following initiatives:

Shorter-period painter schemes: While all companies have had annual incentive schemes for painters, Berger appears to have been the first company to start shorter-period (monthly or quarterly) schemes (albeit now this approach has been replicated by its peers as well).

Interacting directly with the painter, rather than through the dealer: In order to allocate incentives against various painters across the country, previously paint companies would rely on the dealers for collecting data on the quantum of paint purchased by each painter. Moreover, these incentives used to be distributed to the painters through the dealers. This process clearly led to a lot of inefficiencies in distribution of painter incentives. Some of these inefficiencies arose because the data reported by dealers was inaccurate, resulting in several eligible painters either not being aware of or not in receipt of the incentives they were entitled to. However, over the last 3-4 years, Berger has pioneered the implementation of a Centralised Helpline (toll free number for a call centre) which helps the painters to directly call the paint company and log a product purchase from the distribution network. In order to complete the information loop, this Centralised Helpline verifies the product purchase with the respective dealer. To further improve data collection accuracy for distribution of incentives, Berger has started offering a coupon code inside the paint container which is accessible only to the painter, who then calls the Centralised Helpline to log his product purchase. This process further empowers the painter in the whole process.

Berger Paints

September 26, 2016 Ambit Capital Pvt. Ltd. Page 3

Express Painting service – for breaking into the premium segment

Over the past 24 months, Berger has significantly scaled up the distribution and marketing of its ‘Express-Painting’ service. This concept involves enabling the painter to execute a paint project in a substantially quicker and cleaner manner. The firm is leveraging on the fast rising popularity of this concept amongst premium households to achieve the following outcomes:

Convincing a new dealer to stock Berger’s products for the first time as it helps such a dealer to remain relevant in an emerging trend.

Building painter/contractor loyalty by offering training programs to painters for Express Painting service. The firm has set up a training academy called ‘iTrain’, which helps the painters get trained on upgraded technology like ‘Express-Painting’ tools.

Express Painting is being used as a good tool for both ATL and BTL marketing, alongside the ‘Silk’ campaign featuring Bollywood actress Katrina Kaif, which has been ongoing for the last 4 years.

Berger’s sales team is increasingly focusing on ‘lead-conversion’, rather than on ‘lead-generation’ because the awareness built with dealers, painters and customers, works towards generating leads about a new project.

Mobile App for dealers as well as the sales team

Berger has launched an Android mobile application which aims to help the dealers and firm’s sales team in the following manner:

Real-time update on dealer-level account settlement, which helps improve transparency for dealers

Improved platform for performance measurement and incentivisation of the sales team

Although Asian Paints already has a website to enable these functionalities for dealers, it does not yet have a mobile application in place.

Improved supply chain efficiencies

The speed of supply chain for Berger in its distribution channel has improved substantially over the past 3-4 years. This has been achieved through a combination of: a) CRM implementation in 2012 (albeit Berger was one of the last amongst the top four paint companies to make such an IT investment) and nurturing this platform for improved data analytics; b) investing in servicing demand from hitherto remote locations, much before the scale of demand from such locations was big enough; and c) bringing more agility in the sales team by hiring young talent, thereby reducing the average age of employees in the team.

As a result of these initiatives, in larger cities, Berger now fulfils demand in 4-5 hours (vs. 3-4 hours for Asian Paints) compared to previous timelines which were at least twice that of Asian Paints in such cities till 5-6 years ago.

“Now there are set timings for Berger’s lorry to leave the depot and we (dealers) know about these timings because we deal with the company regularly. So we place our orders accordingly.” – a large dealer of Berger in North India during our conversation with him in Aug’16.

Berger Paints

September 26, 2016 Ambit Capital Pvt. Ltd. Page 4

Improvements in HR process and work culture Over the past five years, Berger has streamlined its HR processes including the implementation of a system called ‘Human Resource Management System (HRMS)’. We understand that the following aspects of HR management have improved:

Previously, the recruitment of a sales officer used to be carried out by various branch managers. This led to a lack of consistency in the quality of people being hired across geographies and hence inter-branch transfers used to create problems. The firm has standardised these processes across the country.

Sluggishness in the sales team has been shaken out by the hiring of younger and more agile workforce.

Management trainees are being recruited from IIMs and hence recruiting quality has been improved along with increased focus on training these recruits.

Incentive structures of the sales team have been changed with infrastructure implemented to track performance granularly.

As a result of these changes, the work culture of the organisation has improved in the following manner:

Whilst several of the operational changes implemented were initially not very well accepted, having seen the successful outcome of these changes, employees are encouraged about the firm moving forward in the industry.

Virtuous cycle of positivity: Employees in the sales-team do NOT feel that they are the ‘Number 2’ player in every aspect of the business (Number 1 being Asian Paints). As a result, when they tell the dealers, they feel proud to call themselves as leaders in a few aspects of the business. As these dealers increase their association with Berger over time, it further improves the confidence and morale of the workforce.

Employees across the hierarchy, including those in junior managerial roles, have a clear vision about where their career and operational role are headed.

There is freedom to innovate and to make mistakes. Employees are not berated or scolded for having made mistakes whilst trying to innovate. This culture has helped cultivate an entrepreneurial feeling amongst employees.

Mr. Abhijit Roy, in a conversation with us last year, mentioned “We have a very open culture. Like anybody from field level to sales manager can walk into my room without appointment and talk to me to either give information or ask for my views. I sometimes call branch managers into a conference room and ask them to present their success story which we put up on SharePoint (a team collaboration software tool) for everyone else to understand and share. This encourages people to think differently and innovate.”

Berger Paints

September 26, 2016 Ambit Capital Pvt. Ltd. Page 5

Understanding sustainability of growth We expect 13.5%/11% sales CAGR for decorative paints industry over FY15-25/FY25-35 Exhibit 1: Decorative paints industry’s revenue CAGR and its growth drivers

Growth drivers FY05-15 FY15-25E FY25-35E

CAGR CAGR CAGR

Population Increase - increase in # of HHs 1.6% 1.1% 1.1%

More nuclear families - increase in # of HHs 1.2% 1.2% 0.8%

Decrease in Repainting Cycle 3.3% 3.1% 2.3%

‘Kaccha to Pucca’ shift in houses 1.5% 1.5% 1.5%

Like for like product price hikes 2.9% 2.9% 2.9%

Premiumisation of product portfolio 1.5% 1.5% 1.5%

Shift from Unorganised to Organised Market 2.9% 1.4% 0.5%

Total CAGR

15.9% 13.5% 11.0%

Source: Ambit Capital research; Industry

Despite being one of the oldest and one of the largest categories in the home building sector, the Indian paints industry is far from saturation point for most of its growth drivers. Our analysis suggests that revenue growth of the decorative paints industry in India is likely to moderate from 16.3% CAGR over FY05-15 to 13.5% CAGR over FY15-25 and 11% CAGR over FY25-35. Please refer to our previous note (click here) for details on the underlying demographic/industry-level data for each of these growth drivers.

We expect Berger to gain 100bps market share each year over FY16-21 The paints industry in India is a tough, ruthless and complex business. Unlike other FMCG industries, the paints business faces the following unique challenges:

Limited scope for product differentiation;

Low involvement of end-customers in deciding which paint product to choose, especially in economy and mid-priced paint products (less than `160 per litre);

Voluminous nature of the paint product (in terms of price per unit volume); and

Large number of stock-keeping units (SKUs) given varied paint preferences across geographies in terms of colours, type of paints and size of the SKUs.

Hence, competitive pressures in the paints industry are high and have resulted in:

Reduced trade margins of only 3-6% in the distribution channel for the paints industry as compared to 13-20% for consumer staples categories (for example: food, beverages, etc.), and 20-30% for most other discretionary consumer categories (for example: automobiles, durables, leisure, etc.).

Increased bargaining power of the channel (dealers and painters) as compared to other consumption categories given their ability to push a particular paint product to the end-consumers.

In such a tough business, with low margins for distributors, how does one gain leadership? What are the critical success factors to beat competition? The answers to these questions lie around: a) building efficiency of supply chain to ensure high inventory turnover for a dealer whilst maintaining tight control of the working capital cycle (especially inventory management); and b) building a strong connect with the influencer, i.e. the painters and dealers in order to generate demand. Since such supply chain efficiencies and channel connect cannot be built overnight, the focus of the management team in steadily improving its demand forecasting capabilities and distribution network efficiencies is the key driver of success of a paint company.

We expect industry revenue growth of 13.5% CAGR over FY15-25 and 11.0% CAGR over FY25-35

We expect 500bps market share gains for Berger from Kansai Nerolac and Akzo Nobel over FY16-21

Berger Paints

September 26, 2016 Ambit Capital Pvt. Ltd. Page 6

We identify five drivers of competitive advantages in the industry and compare the four leading players on these drivers, as shown in the exhibit below.

Exhibit 2: Comparison of top-4 paint players across drivers of competitive advantages

Asian Paints Berger Paints Kansai Nerolac ICI/Akzo Nobel

Supply chain management Relationships with dealers Relationships with painters

Marketing initiatives

Quality of management professionals

Overall

Source: Industry, Ambit Capital research; Note: is the strongest and is the weakest.

Under the leadership of Mr. Abhijit Roy over the past three years, Berger has implemented several initiatives around HR, raw material procurement, manufacturing processes, sales function, brand building and launch of new products/ services. Through these initiatives, we expect the firm to gain ~500bps market share over FY16-21 (from ~20% currently to ~25% in FY21). These market share gains are likely to come from peers like Kansai Nerolac and Akzo Nobel given a relative lack of focus of these peers in improving their sales, supply chain, and marketing capabilities at the ground level.

However, given the limited visibility of sustainability of such initiatives by the firm thereafter, we assume the revenues will increase only in line with the overall market beyond FY21.

Exhibit 3: Berger’s revenue growth vs paints industry over FY06-36E

FY05-15 CAGR FY16-26 CAGR FY26-36 CAGR

Industry revenue growth 15.9% 13.5% 11.0%

Berger’s revenue growth 16.5% 16.6% 10.5%

Source: Ambit Capital research

Manufacturing process efficiencies over FY10-16 yet to fully percolate to EBITDA As highlighted in the chart below, Berger has reported a significant improvement in: a) working capital cycle supported by a 26% increase in creditor days; and b) faster gross margin expansion compared to Asian Paints, of which only a small fraction can be attributed to premiumisation of the product portfolio.

Exhibit 4: Berger and Asian Paints’ gross margin over FY10-20

Source: Ambit Capital research

Exhibit 5: Berger and Asian Paints’ working capital days over FY10-20

Source: Ambit Capital research

30%

35%

40%

45%

50%

FY1

0

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

FY1

6

FY1

7E

FY1

8E

FY1

9E

FY2

0E

Berger Asian Paints

-

15

30

45

60

FY1

0

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

FY1

6

FY1

7E

FY1

8E

FY1

9E

FY2

0E

Berger Asian Paints

Berger Paints

September 26, 2016 Ambit Capital Pvt. Ltd. Page 7

These improvements have been possible due to a combination of the following initiatives:

Development of alternate raw materials, new sources for raw materials and improved formulations for better quality and lower costs and innovative procuring and application.

Implementation of a new Vendor Management System, which helped in informed and intelligent buying of raw materials and effective negotiation with vendors of raw materials.

Improvement of productivity at all plants by fine-tuning operations for savings in time and costs and are benchmarked against best practices across all plants and outside the company.

Whilst we forecast no further reduction in the differential between gross margin of Berger and Asian Paints, we expect Berger’s EBITDA margins to expand by ~340bps over FY15-20 (thereby reducing the differential against Asian Paints by 200bps) due to a combination of the following factors:

Reduction in ad-spend to sales ratio: Out of the 450bps gross margin expansion reported by Berger over FY10-15, as much as 210bps was invested in increased ad-spend. Whilst we expect the firm’s focus on ad-spend to continue, we forecast a 130bps reduction in ad-spend to sales ratio for the firm over FY16-21 as the benefits of these higher marketing investments start coming through in the form of market share gains.

Efficiencies around salaries and wages: We expect an ~100bps reduction in salaries and wages to sales ratio over FY16-21 due to the combination of two factors: (a) the firm will reap rewards of having upgraded the quality of middle management talent that it hired over the past three years; and (b) as the firm becomes a process-oriented organisation incrementally, there will be scale efficiencies on this cost item – for example, benefits of standardising the process for hiring its sales team.

Operating efficiencies (120bps): Due to scale-related benefits as also gains from increased use of IT, data analytics and process-driven operations, we expect operating efficiencies of 20-30bps each across various cost items like freight handling charges and other operating expenses.

As a result of the revenues and margin forecasts highlighted above, we expect Berger to report 18.6%/28% CAGR for sales/earnings over FY16-21 with ROCE rising from 21% in FY16 to 35% in FY21.

Berger Paints

September 26, 2016 Ambit Capital Pvt. Ltd. Page 8

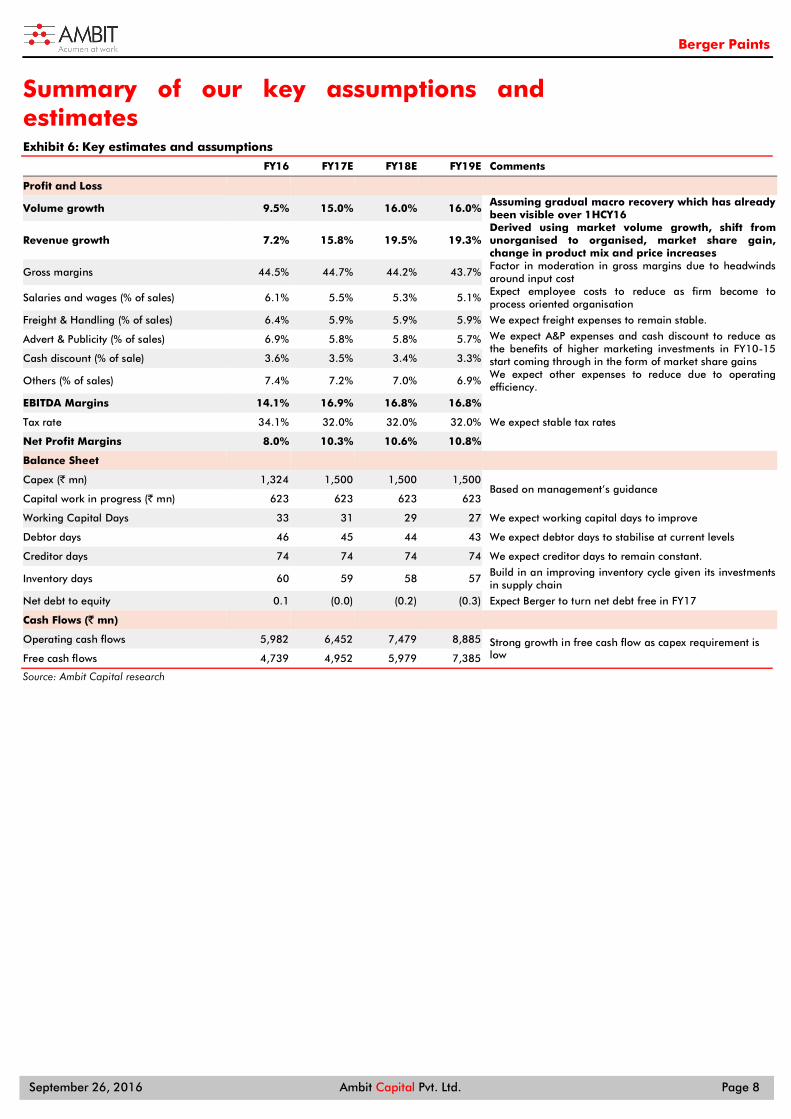

Summary of our key assumptions and estimates Exhibit 6: Key estimates and assumptions

FY16 FY17E FY18E FY19E Comments

Profit and Loss

Volume growth 9.5% 15.0% 16.0% 16.0% Assuming gradual macro recovery which has already been visible over 1HCY16

Revenue growth 7.2% 15.8% 19.5% 19.3% Derived using market volume growth, shift from unorganised to organised, market share gain, change in product mix and price increases

Gross margins 44.5% 44.7% 44.2% 43.7% Factor in moderation in gross margins due to headwinds around input cost

Salaries and wages (% of sales) 6.1% 5.5% 5.3% 5.1% Expect employee costs to reduce as firm become to process oriented organisation

Freight & Handling (% of sales) 6.4% 5.9% 5.9% 5.9% We expect freight expenses to remain stable.

Advert & Publicity (% of sales) 6.9% 5.8% 5.8% 5.7% We expect A&P expenses and cash discount to reduce as the benefits of higher marketing investments in FY10-15 start coming through in the form of market share gains Cash discount (% of sale) 3.6% 3.5% 3.4% 3.3%

Others (% of sales) 7.4% 7.2% 7.0% 6.9% We expect other expenses to reduce due to operating efficiency.

EBITDA Margins 14.1% 16.9% 16.8% 16.8%

Tax rate 34.1% 32.0% 32.0% 32.0% We expect stable tax rates

Net Profit Margins 8.0% 10.3% 10.6% 10.8%

Balance Sheet

Capex (` mn) 1,324 1,500 1,500 1,500 Based on management’s guidance

Capital work in progress (` mn) 623 623 623 623

Working Capital Days 33 31 29 27 We expect working capital days to improve

Debtor days 46 45 44 43 We expect debtor days to stabilise at current levels

Creditor days 74 74 74 74 We expect creditor days to remain constant.

Inventory days 60 59 58 57 Build in an improving inventory cycle given its investments in supply chain

Net debt to equity 0.1 (0.0) (0.2) (0.3) Expect Berger to turn net debt free in FY17

Cash Flows (` mn)

Operating cash flows 5,982 6,452 7,479 8,885 Strong growth in free cash flow as capex requirement is low Free cash flows 4,739 4,952 5,979 7,385

Source: Ambit Capital research

Berger Paints

September 26, 2016 Ambit Capital Pvt. Ltd. Page 9

Valuations: Retain BUY, deserves high P/E We expect ~19% revenue CAGR and ~28% EPS CAGR over FY16-21E with RoCEs rising from 21% in FY16 to 35% in FY21E. Our DCF factors in longevity of Berger’s healthy growth profiles derived from improving values around: (a) quality talent hiring; (b) strong organisational culture; (c) increasingly process-oriented operations; (d) impactful marketing; and (e) controlled capital allocation. As a result, we use terminal growth in our DCF from FY40. Our three-stage DCF gives a fair value of `296 (11% upside), implying an FY18E P/E of 42x. We reiterate BUY.

We prefer DCF over a multiples-based approach Given the steady and cash-generative nature of the business, we use a DCF approach to arrive at a fair value for Berger. Moreover, we believe that a relative valuation based approach around say P/E or EV/EBITDA multiples does NOT adequately capture the fair value of Berger. This is because, given the way Berger has cemented its second rank position in the industry over the past decade, and given the various initiatives implemented around personnel management, marketing and operational efficiencies by Mr. Abhijit Roy over the past five years, Berger’s historical relative valuation band-charts (see the exhibits below) are incorrect benchmarks for the current implied P/E multiple. Berger’s P/E and EV/EBITDA multiples have justifiably re-rated upwards over the past three years.

Our DCF valuation model on Berger includes the following three stages:

Stage 1: Five-year growth phase – FY16-21 We forecast 18.6% revenue CAGR for Berger led by an industry growth rate of ~14% and market share gains of ~500bps. As highlighted above, we expect EBITDA margin expansion of 350bps over FY16-21E and hence forecast 28% EPS CAGR. We expect a reduction in inventory days from 60 days in FY16 to 55 days in FY21E through improving efficiency of working capital cycle management and incremental investments in improved data analytics for finished goods inventory management and Vendor Management System for improved raw material procurement efficiencies. This would lead to a reduction in working capital cycle days from 40 days in FY16 to 24 days in FY21E. This is likely to lead to an improvement in asset turnover from 2.2x in FY15 to 2.7x in FY21E.

As a result of margin expansion and improved asset turns, RoEs are likely to improve from 27% in FY16 to ~34% in FY21E.

Exhibit 7: Berger’s earnings profile over FY11-21

Source: Ambit Capital research

Exhibit 8: Asset turnover and RoCE

Source: Ambit Capital research

10%

15%

20%

25%

30%

35%

40%

0%

10%

20%

30%

40%

50%

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

FY1

6

FY1

7E

FY1

8E

FY1

9E

FY2

0E

FY2

1E

Revenue growth (LHS) EPS growth (LHS)

RoCE (RHS) EBITDA Margin (RHS)

15%

20%

25%

30%

35%

40%

1.5

1.7

1.9

2.1

2.3

2.5

2.7

2.9

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

FY1

6

FY1

7E

FY1

8E

FY1

9E

FY2

0E

FY2

1E

Asset turnover ROCE (RHS)

We change our recommendation from SELL to BUY.

Berger Paints

September 26, 2016 Ambit Capital Pvt. Ltd. Page 10

Stage 2: Fade period over FY22-40 This stage of our DCF model forecasts a gradual moderation in revenue growth rates from 19% in FY21 to 6% in FY40 (an overall CAGR of ~12%). PBIT margins in this stage are likely to remain steady as the firm sustains its market dominance as the second-largest player.

Exhibit 9: Our assumption on operating metrics in the fade period of our DCF-based valuation (` mn)

Source: Ambit Capital research

Stage 3: Growth to perpetuity From FY40, we forecast growth in revenues, earnings and cash flows at 5%, broadly in line with the long-term GDP growth forecasts for India.

WACC used for discounting of cash flows Our DCF model uses a WACC of 13% for the company which is based on the computation shown in the table on the right.

Cross cycle valuation evolution There are three key conclusions worth noticing from the cross cycle valuations charts below: a) Asian Paints as well as Berger have witnessed a 30-35% re-rating in their valuation multiples over the past five years; b) the gap between valuation multiples of Asian Paints and Berger has reduced from 30-40% five years ago to 10-15% now; and c) whilst five years ago these paint companies used to trade at a 15-20% discount to the FMCG sector average, currently they trade at a premium to the FMCG sector average. We see all three of these trends being justified by a combination of the following factors:

Consumption of ‘home building material’ as a broad category has seen significant traction. Households are increasingly willing to spend on organised and aspirational brands with shortening replacement cycles.

Decorative paints’ volume growth rates have shown greater resilience compared to any other discretionary consumption or staples consumer category over the past 15 years despite the cyclicality of consumer spending over this period.

Nature of competitive advantages in decorative paints (speed of supply chain and relationships with channel partners) are significantly more sustainable than those in the staples categories (like marketing, distribution reach etc.). As a result, although there have been several sources of disruption in consumption over the past 15 years – modern retail expansion, ecommerce channel expansion, Patanjali type of new entrants, influx of MNCs like Sherwin Williams, Mondelez etc – Asian Paints and Berger Paints have NOT been affected.

Due to the series of initiatives taken by Berger under the leadership of Mr. Abhijit Roy, the firm has caught up with Asian Paints on both revenue growth rates as well as margins, in a sustainable manner.

0%

10%

20%

30%

40%

020,00040,00060,00080,000

100,000120,000

FY2

1

FY2

2

FY2

3

FY2

4

FY2

5

FY2

6

FY2

7

FY2

8

FY2

9

FY3

0

FY3

1

FY3

2

FY3

3

FY3

4

FY3

5

FY3

6

FY3

7

FY3

8

FY3

9

FY4

0

FCFF (LHS) Revenue growth (RHS)

PBIT Margin (RHS) ROCE (RHS)

WACC computation

Item %

Risk free rate of return 8.2

Beta (2 Year monthly) 0.85

Risk Premium 7

Cost of Equity 14.2

Cost of Debt 12

Debt/Equity 20

Corporate Tax Rate 30

WACC 13.0

Source: Ambit Capital Research

Berger Paints

September 26, 2016 Ambit Capital Pvt. Ltd. Page 11

Exhibit 10: EV/EBITDA band of Berger and Asian Paints

Source: Ambit Capital research

Exhibit 11: P/E band of Berger and Asian Paints

Source: Ambit Capital research

Relative valuation – deserves a rich P/E Despite paints companies being classified as chemicals companies globally and despite paints being linked to the home building sector, we believe that the business models and growth prospects of paints companies in India are akin to the consumer staples/entry-level consumer discretionary companies because the paint companies are highly cash-generative B2C businesses in India with drivers of competitive advantages including supply chain efficiencies, quality of distribution and brand recall.

Within the consumer sector, we believe FMCG is a more appropriate peer group for decorative paints companies because: a) decorative paints category size is large (over $6bn currently); b) runway for category growth is long given demand is largely replacement-driven with shrinking replacement cycles; c) capex and working capital cycle requirements are similar to that of the staples companies; d) distribution network is solely through the widespread mom-n-pop dealer network rather than through select few retail shops or ecommerce; and e) demand is highly resilient across strong and weak consumption environments unlike most discretionary consumer categories.

Berger Paints is currently trading at a 3% premium to peers like Kansai Nerolac, and at a 5% discount to the market leader, Asian Paints. We believe that the premium against Kansai and Akzo is clearly justified due to the superior competitive advantages that were highlighted in Exhibit 2 on page 6. We believe the firm deserves to trade at a slight discount of 5% as against Asian Paints since the market leader continues to demonstrate superior capabilities around velocity of its supply chain, efficient working capital cycles and greater capital efficiency underpinned by a high-quality talent pool at the middle and senior management level, which helps it successfully drive category evolution over time.

-

5

10

15

20

25

30

35

Sep-

11

Jan-

12

May

-12

Sep-

12

Jan-

13

May

-13

Sep-

13

Jan-

14

May

-14

Sep-

14

Jan-

15

May

-15

Sep-

15

Jan-

16

May

-16

Sep-

16

Berger Paints Asian Paints

-

10

20

30

40

50

60

Sep-

11

Jan-

12

May

-12

Sep-

12

Jan-

13

May

-13

Sep-

13

Jan-

14

May

-14

Sep-

14

Jan-

15

May

-15

Sep-

15

Jan-

16

May

-16

Sep-

16

Berger Paints Asian Paints

Berger Paints

September 26, 2016 Ambit Capital Pvt. Ltd. Page 12

Exhibit 12: Relative valuations for Berger and its peers

Company name CMP (LC)

Mcap (US$mn)

EPS CAGR

FY16-18

P/E EBITDA

CAGR EV/EBITDA

Sales CAGR

EV/SALES ROE FY17

(%) FY17E FY18E FY16-18 FY17E FY18E FY16-18 FY17E FY18E

Indian paint/ adhesive companies

Asian Paints 1,177 16,886 25% 51 41 23% 32 26 17% 6.2 5.1 36

Berger Paints 263 3,821 35% 46 38 28% 28 23 18% 4.7 3.9 33

Pidilite Industries Ltd 707 5,422 18% 43 34 17% 27 22 15% 5.8 4.8 27

Akzo Nobel India Ltd 1,610 1,155 17% 32 28 18% NA NA 12% NA NA 29

Kansai Nerolac Paints Ltd 376 3,032 -22% 43 37 19% 28 24 14% 4.5 3.9 19

Median for paint/ adhesive companies 18% 43 37 19% 28 23 15% 5.3 4.3 27

Indian FMCG companies HUL 909 29,422 22% 40 33 18% 28 23 14% 5.2 4.5 123

Dabur 286 7,514 15% 36 30 16% 27 23 16% 4.9 4.1 31

Godrej Cons 1,622 8,258 12% 41 38 15% 30 26 16% 5.3 4.6 25

Marico Inds 286 5,519 29% 40 31 26% 27 21 17% 5.1 4.2 40

Britannia Inds 3,387 6,078 18% 42 36 18% 27 23 16% 3.9 3.4 48

Nestle India 6,379 9,198 23% 50 38 32% 29 22 20% 6.1 5.0 41

GSK Cons 6,186 3,891 9% 36 32 14% 33 27 13% 5.0 4.3 27

Colgate 969 3,942 15% 39 33 17% 24 20 14% 5.5 4.7 61

Median for FMCG companies 17% 40 33 17% 28 23 16% 5.2 4.4 41

Global paint companies

Akzo Nobel 61 17,129 4% 15 14 1% 8 7 0% 1.2 1.1 15

PPG Industries Inc 102 27,283 15% 17 15 10% 11 10 1% 2.0 2.0 33

Du Pont (E.I.) De Nemours 67 58,580 31% 21 18 17% 12 10 3% 2.6 2.3 30

Kansai Paint Co Ltd 2,203 5,991 11% 23 23 5% 12 12 -3% 1.7 1.8 9 Nippon Paint Holdings Co Ltd

3,480 11,296 -58% 37 30 61% 12 10 44% 2.2 1.8 6

Duluxgroup Ltd 6 1,920 8% 19 19 9% 12 12 3% 1.7 1.6 35

Sherwin-Williams Co/The 278 25,673 11% 22 20 11% 13 12 5% 2.3 2.2 89

Median for global paint companies 11% 21 19 10% 12 10 3% 2.0 1.8 30

Source: Bloomberg, Ambit Capital research

Ambit vs consensus As highlighted in the table below, our earnings estimates are 8-9% ahead of consensus forecasts partly led by a higher revenue growth and partly by a higher margin forecast. This, we believe, is likely to be a result of: a) no market share gains expected by consensus for Berger possibly due to underappreciation of the firm’s competitive advantages amidst recent operational initiatives; and b) greater reversal of crude oil price softening related gross margin tailwind by consensus for the sector.

Exhibit 13: Ambit vs consensus (` mn)

Ambit Consensus

Divergence from Consensus

FY17E

Sales 53,642 51,677 4%

EBITDA 9,043 8,379 8%

PAT 5,532 5,107 8%

FY18E

Sales 64,098 60,682 6%

EBITDA 10,787 9,952 8%

PAT 6,778 6,222 9%

Source: Ambit capital research

Berger Paints

September 26, 2016 Ambit Capital Pvt. Ltd. Page 13

Changes to our estimates and valuations Exhibit 14: Change in our estimates (` mn)

Particulars New Estimates Old Estimates Divergence Comments

FY17E FY18E FY19E FY17E FY18E FY19E FY17E FY18E FY19E

Sales 53,642 64,098 76,447 53,642 64,098 76,447 0% 0% 0%

EBITDA 9,043 10,787 12,865 9,043 10,421 12,276 0% 4% 5% We expect EBITDA margin expansion due to lower employee and A&P cost and increasing operating efficiency EBITDA margin 16.9% 16.8% 16.8% 16.9% 16.3% 16.1% - 57 77

PAT 5,532 6,778 8,259 5,532 6,530 7,858 0% 4% 5% EBITDA margin expansion flows down to EPS EPS 5.7 7.0 8.5 5.7 6.7 8.1 0% 4% 5%

Source Ambit capital research

Risks to our BUY stance Sluggish economic growth for a prolonged period of time can result in a

moderation in our FY17 revenue growth forecasts for Berger vs our current expectation of a revival in YoY revenue growth rates from 7% in FY16 to 16% in FY17E.

Capital misallocation in future? As highlighted previously, one of the biggest factors driving consistency of returns for Berger in the past has been the firm’s prudent approach towards capital allocation. Any changes to this approach, especially outside the paints business for the firm could result in a reduction in focus and financial return profiles for the firm thereafter.

Catalysts Improvements in margins, working capital cycle and market share: As

highlighted previously, several initiatives are underway at Berger which are likely to sustain the momentum of improving EBITDA margins, working capital cycle days and market share gains. The extent of these benefits is NOT fully appreciated in consensus forecasts and current valuations.

Updates around GST rollout: Any clarity around timelines and structure of GST rollout from the Government is likely to result in increased expectations around: a) accelerated shift from the unorganised to organised market; b) quantum of benefits from lower tax liability for Berger vs the current levels of 25-26%; and c) improved supply chain efficiencies following GST rollout.

Exhibit 15: Explanation for our accounting score

Segment Score Comments

Accounting GREEN Berger scores well on cash conversion, related party advances and return on surplus cash; however, its working capital cycle is average; RoEs and provisions for debtors outstanding for more than six months are better than peers.

Predictability GREEN Predictability of earnings remains high for Berger given: (a) high correlation of industry volume growth rates with GDP; (b) strong correlation of raw material costs with crude and foreign exchange rates; and (c) market share changes across various players in the industry.

Earnings Momentum GREEN On the back of higher-than-expected volume growth, Berger’s consensus EPS estimates have been upgraded by 4% for FY17 and FY18 over the past six months.

Source: Ambit Capital research

Berger Paints

September 26, 2016 Ambit Capital Pvt. Ltd. Page 14

Exhibit 16: Berger forensic score evolution

Source: Ambit ‘HAWK’, Ambit Capital research, Note: Using our ‘accounting framework’, we categorise the market into deciles on the basis of their accounting quality with ‘D1’ indicating the best decile and ‘D10’ indicating the worst decile. Our analysis points towards a strong link between accounting quality and share price performance.

Exhibit 17: Berger greatness score evolution

Source: Ambit ‘HAWK’, Ambit Capital research, Note: On our ‘greatness framework’, on a scale of 0 to 100, a small minority of outstanding companies tend to score above 67 whilst most companies tend to have scores below 50

Berger Paints

September 26, 2016 Ambit Capital Pvt. Ltd. Page 15

Balance Sheet

Year to March (` mn) FY15 FY16 FY17E FY18E FY19E

Shareholders' equity 693 694 971 971 971

Reserves & surpluses 11,913 14,098 17,358 21,296 26,034

Total networth 12,606 14,792 18,329 22,267 27,005

Minority Interest 0 0 0 0 0

Preference share capital 0 0 0 0 0

Debt 6,089 3,243 2,243 1,243 243

Deferred tax liability 579 687 687 687 687

Total liabilities 19,273 18,722 21,259 24,197 27,934

Gross block 14,613 15,938 17,438 18,938 20,438

Net block 9,307 9,764 10,197 10,590 10,948

CWIP 1,004 623 623 623 623

Investments 1,345 2,992 2,992 2,992 2,992

Cash & equivalents 1,698 1,095 2,825 4,820 7,622

Debtors 5,352 5,806 6,574 7,680 8,950

Inventory 7,195 7,582 8,629 10,135 11,879

Loans & advances 1,070 1,202 1,391 1,662 1,983

Other current assets 188 128 147 176 209

Total current assets 15,503 15,813 19,566 24,473 30,642

Current liabilities 7,121 9,375 10,852 12,967 15,466

Provisions 765 1,095 1,267 1,514 1,806

Total current liabilities 7,886 10,470 12,119 14,481 17,271

Net current assets 7,617 5,343 7,447 9,992 13,371

Miscellaneous 0 0 0 0 0

Total assets 19,273 18,722 21,259 24,197 27,934

Source: Company, Ambit Capital research

Income statement

Year to March (` mn) FY15 FY16 FY17E FY18E FY19E

Operating income 43,221 46,341 53,642 64,098 76,447

% growth 11.7% 7.2% 15.8% 19.5% 19.3%

Operating expenditure 38,113 39,787 44,599 53,311 63,582

Operating profit 5,107 6,554 9,043 10,787 12,865

% growth 18.4% 28.3% 38.0% 19.3% 19.3%

Depreciation 925 1,000 1,067 1,106 1,142

EBIT 4,182 5,554 7,976 9,680 11,723

Interest expenditure 501 290 228 145 62

Non-operating income 360 345 386 432 484

Adjusted PBT 4,041 5,609 8,135 9,968 12,145

Tax 1,394 1,911 2,603 3,190 3,886

Adjusted PAT/ Net profit 2,647 3,698 5,532 6,778 8,259

% growth 6% 40% 50% 23% 22%

Prior Period Items - - - - -

Reported PAT / Net profit 2,647 3,698 5,532 6,778 8,259

Minority Interest 0 0 0 0 0

Share of associates 0 0 0 0 0

Adjusted Consolidated net profit 2,647 3,698 5,532 6,778 8,259

Reported Consolidated net profit 2,647 3,698 5,532 6,778 8,259

Source: Company, Ambit Capital research

Berger Paints

September 26, 2016 Ambit Capital Pvt. Ltd. Page 16

Cash flow statement

Year to March (` mn) FY15 FY16 FY17E FY18E FY19E

EBIT 4,542 5,899 8,362 10,112 12,207

Depreciation 925 1,000 1,067 1,106 1,142

Others (142) (315) (0) 0 -

Tax (1,437) (1,812) (2,603) (3,190) (3,886)

(Incr) / decr in net working capital (434) 1,211 (374) (550) (578)

Cash flow from operations 3,454 5,982 6,452 7,479 8,885

Capex (1,615) (1,243) (1,500) (1,500) (1,500)

(Incr) / decr in investments (361) (1,451) - - -

Other income (expenditure) 148 122 - - -

Others - - - - -

Cash flow from investments (1,829) (2,572) (1,500) (1,500) (1,500)

Net borrowings (149) (2,387) (1,000) (1,000) (1,000)

Issuance of equity - 0 277 - -

Interest paid (451) (257) (228) (145) (62)

Dividend paid (1,169) (1,080) (2,272) (2,840) (3,521)

Others - - - - -

Cash flow from financing (1,769) (3,724) (3,222) (3,984) (4,583)

Net change in cash (144) (314) 1,730 1,995 2,802

Closing cash balance 1,697 480 2,825 4,820 7,622

Free cash flow 1,839 4,739 4,952 5,979 7,385

Source: Company, Ambit Capital research

Ratio analysis

Year to March (%) FY15 FY16 FY17E FY18E FY19E

EBITDA margin (%) 11.8% 14.1% 16.9% 16.8% 16.8%

EBIT margin (%) 10.5% 12.7% 15.6% 15.8% 16.0%

Net profit margin (%) 6.1% 8.0% 10.3% 10.6% 10.8%

Dividend payout ratio (%) 36.2% 37.2% 41.1% 41.9% 42.6%

Net debt: equity (x) 0.3 0.1 (0.0) (0.2) (0.3)

Working capital turnover (x) 5.7 8.7 7.2 6.4 5.7

Gross block turnover (x) 3.0 2.9 3.1 3.4 3.7

RoCE (%) 16.5% 21.2% 29.5% 31.2% 32.7%

RoIC (%) 19.0% 23.2% 32.7% 37.6% 43.2%

RoE (%) 22.2% 27.0% 33.4% 33.4% 33.5%

Source: Company, Ambit Capital research

Valuation parameters

Year to March (` mn) FY15 FY16 FY17E FY18E FY19E

EPS (`) 2.7 3.8 5.7 7.0 8.5

Diluted EPS (`) 2.7 3.8 5.7 7.0 8.5

Book value per share (`) 18.2 21.3 18.9 22.9 27.8

Dividend per share (`) 0.9 1.2 2.0 2.5 3.1

P/E (x) 97.6 69.8 46.7 38.1 31.3

P/BV (x) 14.6 12.5 14.1 11.6 9.6

EV/EBITDA (x) 48.3 37.9 27.6 23.1 19.4

EV/EBIT (x) 58.2 44.3 31.2 25.7 21.2

Source: Company, Ambit Capital research

Berger Paints

September 26, 2016 Ambit Capital Pvt. Ltd. Page 17

Institutional Equities Team Saurabh Mukherjea, CFA CEO, Institutional Equities (022) 30433174 [email protected]

Research Analysts

Name Industry Sectors Desk-Phone E-mail

Nitin Bhasin - Head of Research E&C / Infra / Cement / Industrials (022) 30433241 [email protected]

Aadesh Mehta, CFA Banking / Financial Services (022) 30433239 [email protected]

Abhishek Ranganathan, CFA Retail (022) 30433085 [email protected]

Achint Bhagat, CFA Cement / Home Building (022) 30433178 [email protected]

Anuj Bansal Mid-caps (022) 30433122 [email protected]

Aditi Singh Economy / Strategy (022) 30433284 [email protected] Ashvin Shetty, CFA Automobile (022) 30433285 [email protected]

Bhargav Buddhadev Power Utilities / Capital Goods (022) 30433252 [email protected]

Deepesh Agarwal, CFA Power Utilities / Capital Goods (022) 30433275 [email protected]

Dhiraj Mistry, CFA Consumer (022) 30433264 [email protected]

Gaurav Khandelwal, CFA Automobile (022) 30433132 [email protected] Girisha Saraf Mid-caps / Small-caps (022) 30433211 [email protected]

Karan Khanna, CFA Strategy (022) 30433251 [email protected]

Pankaj Agarwal, CFA Banking / Financial Services (022) 30433206 [email protected]

Paresh Dave, CFA Healthcare (022) 30433212 [email protected]

Parita Ashar, CFA Metals & Mining / Aviation (022) 30433223 [email protected]

Prashant Mittal, CFA Strategy / Derivatives (022) 30433218 [email protected]

Rahil Shah Banking / Financial Services (022) 30433217 [email protected]

Rakshit Ranjan, CFA Consumer (022) 30433201 [email protected]

Ravi Singh Banking / Financial Services (022) 30433181 [email protected]

Ritesh Gupta, CFA Oil & Gas / Chemicals / Agri Inputs (022) 30433242 [email protected]

Ritesh Vaidya, CFA Consumer (022) 30433246 [email protected]

Ritika Mankar Mukherjee, CFA Economy / Strategy (022) 30433175 [email protected]

Ritu Modi Automobile (022) 30433292 [email protected]

Sagar Rastogi Technology (022) 30433291 [email protected]

Sudheer Guntupalli Technology (022) 30433203 [email protected]

Sumit Shekhar Economy / Strategy (022) 30433229 [email protected]

Utsav Mehta, CFA E&C / Industrials (022) 30433209 [email protected]

Vivekanand Subbaraman, CFA Media (022) 30433261 [email protected]

Sales

Name Regions Desk-Phone E-mail

Sarojini Ramachandran - Head of Sales UK +44 (0) 20 7886 2740 [email protected]

Dharmen Shah India / Asia (022) 30433289 [email protected]

Dipti Mehta India / USA (022) 30433053 [email protected]

Hitakshi Mehra India (022) 30433204 [email protected]

Krishnan V India / Asia (022) 30433295 [email protected]

Nityam Shah, CFA USA / Europe (022) 30433259 [email protected] Parees Purohit, CFA UK / USA (022) 30433169 [email protected]

Praveena Pattabiraman India / Asia (022) 30433268 [email protected]

Shaleen Silori India (022) 30433256 [email protected]

Vishal Mehta India / Asia (022) 30433198 [email protected]

Singapore

Pramod Gubbi, CFA – Director Singapore +65 8606 6476 [email protected]

Shashank Abhisheik Singapore +65 6536 1935 [email protected]

USA / Canada

Ravilochan Pola - CEO Americas +1(646) 361 3107 [email protected]

Production

Sajid Merchant Production (022) 30433247 [email protected]

Sharoz G Hussain Production (022) 30433183 [email protected]

Jestin George Editor (022) 30433272 [email protected]

Nikhil Pillai Database (022) 30433265 [email protected]

Berger Paints

September 26, 2016 Ambit Capital Pvt. Ltd. Page 18

Berger Paints India Ltd (BRGR IN, BUY)

Source: Bloomberg, Ambit Capital research

0

50

100

150

200

250

300

Sep-

13

Nov

-13

Jan-

14

Mar

-14

May

-14

Jul-

14

Sep-

14

Nov

-14

Jan-

15

Mar

-15

May

-15

Jul-

15

Sep-

15

Nov

-15

Jan-

16

Mar

-16

May

-16

Jul-

16

Sep-

16

Berger Paints India Ltd

Berger Paints

September 26, 2016 Ambit Capital Pvt. Ltd. Page 19

Explanation of Investment Rating

Investment Rating Expected return (over 12-month)

BUY >10%

SELL <10%

NO STANCE We have forward looking estimates for the stock but we refrain from assigning valuation and recommendation

UNDER REVIEW We will revisit our recommendation, valuation and estimates on the stock following recent events

NOT RATED We do not have any forward looking estimates, valuation or recommendation for the stock POSITIVE We have a positive view on the sector and most of stocks under our coverage in the sector are BUYs

NEGATIVE We have a negative view on the sector and most of stocks under our coverage in the sector are SELLs

Disclaimer This report or any portion hereof may not be reprinted, sold or redistributed without the written consent of Ambit Capital. AMBIT Capital Research is disseminated and available primarily electronically, and, in some cases, in printed form.

Additional information on recommended securities is available on request.

Disclaimer

1. AMBIT Capital Private Limited (“AMBIT Capital”) and its affiliates are a full service, integrated investment banking, investment advisory and brokerage group. AMBIT Capital is a Stock Broker, Portfolio Manager and Depository Participant registered with Securities and Exchange Board of India Limited (SEBI) and is regulated by SEBI

2. AMBIT Capital makes best endeavours to ensure that the research analyst(s) use current, reliable, comprehensive information and obtain such information from sources which the analyst(s) believes to be reliable. However, such information has not been independently verified by AMBIT Capital and/or the analyst(s) and no representation or warranty, express or implied, is made as to the accuracy or completeness of any information obtained from third parties. The information, opinions, views expressed in this Research Report are those of the research analyst as at the date of this Research Report which are subject to change and do not represent to be an authority on the subject. AMBIT Capital may or may not subscribe to any and/ or all the views expressed herein.

3. This Research Report should be read and relied upon at the sole discretion and risk of the recipient. If you are dissatisfied with the contents of this complimentary Research Report or with the terms of this Disclaimer, your sole and exclusive remedy is to stop using this Research Report and AMBIT Capital or its affiliates shall not be responsible and/ or liable for any direct/consequential loss howsoever directly or indirectly, from any use of this Research Report.

4. If this Research Report is received by any client of AMBIT Capital or its affiliate, the relationship of AMBIT Capital/its affiliate with such client will continue to be governed by the terms and conditions in place between AMBIT Capital/ such affiliate and the client.

5. This Research Report is issued for information only and the 'Buy', 'Sell', or ‘Other Recommendation’ made in this Research Report such should not be construed as an investment advice to any recipient to acquire, subscribe, purchase, sell, dispose of, retain any securities and should not be intended or treated as a substitute for necessary review or validation or any professional advice. Recipients should consider this Research Report as only a single factor in making any investment decisions. This Research Report is not an offer to sell or the solicitation of an offer to purchase or subscribe for any investment or as an official endorsement of any investment.

6. This Research Report is being supplied to you solely for your information and may not be reproduced, redistributed or passed on, directly or indirectly, to any other person or published, copied in whole or in part, for any purpose. Neither this Research Report nor any copy of it may be taken or transmitted or distributed, directly or indirectly within India or into any other country including United States (to US Persons), Canada or Japan or to any resident thereof. The distribution of this Research Report in other jurisdictions may be strictly restricted and/ or prohibited by law or contract, and persons into whose possession this Research Report comes should inform themselves about such restriction and/ or prohibition, and observe any such restrictions and/ or prohibition.

7. Ambit Capital Private Limited is registered as a Research Entity under the SEBI (Research Analysts) Regulations, 2014. SEBI Reg.No.- INH000000313.

Conflict of Interests

8. In the normal course of AMBIT Capital’s business circumstances may arise that could result in the interests of AMBIT Capital conflicting with the interests of clients or one client’s interests conflicting with the interest of another client. AMBIT Capital makes best efforts to ensure that conflicts are identified and managed and that clients’ interests are protected. AMBIT Capital has policies and procedures in place to control the flow and use of non-public, price sensitive information and employees’ personal account trading. Where appropriate and reasonably achievable, AMBIT Capital segregates the activities of staff working in areas where conflicts of interest may arise. However, clients/potential clients of AMBIT Capital should be aware of these possible conflicts of interests and should make informed decisions in relation to AMBIT Capital’s services.

9. AMBIT Capital and/or its affiliates may from time to time have or solicit investment banking, investment advisory and other business relationships with companies covered in this Research Report and may receive compensation for the same.

Additional Disclaimer for U.S. Persons

10. The research report is solely a product of AMBIT Capital

11. AMBIT Capital is the employer of the research analyst(s) who has prepared the research report

12. Any subsequent transactions in securities discussed in the research reports should be effected through Enclave Capital LLC. (“Enclave”).

13. Enclave does not accept or receive any compensation of any kind for the dissemination of the AMBIT Capital research reports.

14. The research analyst(s) preparing the email / Research Report/ attachment is resident outside the United States and is/are not associated persons of any U.S. regulated broker-dealer and that therefore the analyst(s) is/are not subject to supervision by a U.S. broker-dealer, and is/are not required to satisfy the regulatory licensing requirements of FINRA or required to otherwise comply with U.S. rules or regulations regarding, among other things, communications with a subject company, public appearances and trading securities held by a research analyst account.

15. This report is prepared, approved, published and distributed by the Ambit Capital located outside of the United States (a non-US Group Company”). This report is distributed in the U.S.by Enclave Capital LLC, a U.S. registered broker dealer, on behalf of Ambit Capital only to major U.S. institutional investors (as defined in Rule 15a-6 under the U.S. Securities Exchange Act of 1934 (the “Exchange Act”)) pursuant to the exemption in Rule 15a-6 and any transaction effected by a U.S. customer in the securities described in this report must be effected through Enclave Capital LLC (19 West 44th Street, suite 1700, New York, NY 10036). In order to receive any additional information about or to effect a transaction in any security or financial instrument mentioned herein, please contact a registered representative of Enclave Capital LLC., by phone at 646 361 3107.

16. As of the publication of this report Enclave Capital LLC, does not make a market in the subject securities.

17. This document does not constitute an offer of, or an invitation by or on behalf of Ambit Capital or its affiliates or any other company to any person, to buy or sell any security. The information contained herein has been obtained from published information and other sources, which Ambit Capital or its Affiliates consider to be reliable. None of Ambit Capital accepts any liability or responsibility whatsoever for the accuracy or completeness of any such information. All estimates, expressions of opinion and other subjective judgments contained herein are made as of the date of this document. Emerging securities markets may be subject to risks significantly higher than more established markets. In particular, the political and economic environment, company practices and market prices and volumes may be subject to significant variations. The ability to assess such risks may also be limited due to significantly lower information quantity and quality. By accepting this document, you agree to be bound by all the foregoing provisions.

Additional Disclaimer for Canadian Persons

18. AMBIT Capital is not registered in the Province of Ontario and /or Province of Québec to trade in securities and/or to provide advice with respect to securities.

19. AMBIT Capital's head office or principal place of business is located in India.

20. All or substantially all of AMBIT Capital's assets may be situated outside of Canada.

21. It may be difficult for enforcing legal rights against AMBIT Capital because of the above.

22. Name and address of AMBIT Capital's agent for service of process in the Province of Ontario is: Torys LLP, 79 Wellington St. W., 30th Floor, Box 270, TD South Tower, Toronto, Ontario M5K 1N2 Canada.

23. Name and address of AMBIT Capital's agent for service of process in the Province of Montréal is Torys Law Firm LLP, 1 Place Ville Marie, Suite 1919 Montréal, Québec H3B 2C3 Canada.

Additional Disclaimer for Singapore Persons

24. This Report is prepared and distributed by Ambit Capital Private Limited and distributed as per the approved arrangement under Paragraph 9 of Third Schedule of Securities and Futures Act (CAP 289) and Paragraph 11 of the First Schedule to the Financial Advisors Act (CAP 110) provided to Ambit Singapore Pte. Limited by Monetary Authority of Singapore.

25. This Report is only available to persons in Singapore who are institutional investors (as defined in section 4A of the Securities and Futures Act (Cap. 289) of Singapore (the “SFA”).” Accordingly, if a Singapore Person is not or ceases to be such an institutional investor, such Singapore Person must immediately discontinue any use of this Report and inform Ambit Singapore Pte. Limited.

Berger Paints

September 26, 2016 Ambit Capital Pvt. Ltd. Page 20

Additional Disclaimer for UK Persons

26. All of the recommendations and views about the securities and companies in this report accurately reflect the personal views of the research analyst named on the cover. No part of this research analyst’s compensation was, is, or will be directly or indirectly related to the specific recommendations or views expressed by the research analyst in this research report. This report may not be reproduced, redistributed or copied in whole or in part for any purpose.

27. This report is a marketing communication and has been prepared by Ambit Capital Pvt Ltd of Mumbai, India (“Ambit”) and has been approved in the UK by Ambit Capital (UK) Limited (“ACUK”) solely for the purposes of section 21 of the Financial Services and Markets Act 2000. Ambit is regulated by the Securities and Exchange Board of India and is registered as a Research Entity under the SEBI (Research Analysts) Regulations, 2014. ACUK is regulated by the UK Financial Services Authority and has registered office at C/o Panmure Gordon & Co PL, One New Change, London, EC4M9AF.

28. In the UK, this report is directed at and is for distribution only to persons who (i) fall within Article 19(1) (persons who have professional experience in matters relating to investments) or Article 49(2)(a) to (d) (high net worth companies, unincorporated associations etc) of the Financial Services and Markets Act 2000 (Financial Promotions) Order 2005 (as amended) or (ii) are professional customers or eligible counterparties of ACUK (all such persons together being referred to as "relevant persons"). This report must not be acted on or relied upon by persons in the UK who are not relevant persons.

29. Neither Ambit nor ACUK is a US registered broker-dealer. Transactions undertaken in the US in any security mentioned herein must be effected through a US-registered broker-dealer, in conformity with SEC Rule 15a-6.

30. Neither this report nor any copy or part thereof may be distributed in any other jurisdictions where its distribution may be restricted by law and persons into whose possession this report comes should inform themselves about, and observe, any such restrictions. Distribution of this report in any such other jurisdictions may constitute a violation of UK or US securities laws, or the law of any such other jurisdictions.

31. This report does not constitute an offer or solicitation to buy or sell any securities referred to herein. It should not be so construed, nor should it or any part of it form the basis of, or be relied on in connection with, any contract or commitment whatsoever. The information in this report, or on which this report is based, has been obtained from publicly available sources that Ambit believes to be reliable and accurate. However, it has not been prepared in accordance with legal requirements designed to promote the independence of investment research. It has also not been independently verified and no representation or warranty, express or implied, is made as to the accuracy or completeness of any information obtained from third parties.

32. The information or opinions are provided as at the date of this report and are subject to change without notice. The information and opinions provided in this report take no account of the investors’ individual circumstances and should not be taken as specific advice on the merits of any investment decision. Investors should consider this report as only a single factor in making any investment decisions. Further information is available upon request. No member or employee of Ambit or ACUK accepts any liability whatsoever for any direct or consequential loss howsoever arising, directly or indirectly, from any use of this report or its contents.

33. The value of any investment made at your discretion based on this Report, or income therefrom, maybe affected by changes in economic, financial and/or political factors and may go down as well as go up and you may not get back the original amount invested. Some securities and/or investments involve substantial risk and are not suitable for all investors.

34. Ambit and its affiliates and their respective officers directors and employees may hold positions in any securities mentioned in this Report (or in any related investment) and may from time to time add to or dispose of any such securities (or investment). Ambit and ACUK may from time to time render advisory and other services to companies referred to in this Report and may receive compensation for the same.

35. Ambit and its affiliates may act as a market maker or risk arbitrator or liquidity provider or may have assumed an underwriting commitment in the securities of companies discussed in this Report (or in related investments) or may sell them or buy them from clients on a principal to principal basis or may be involved in proprietary trading and may also perform or seek to perform investment banking or underwriting services for or relating to those companies.

36. Ambit and ACUK may sell or buy any securities or make any investment which may be contrary to or inconsistent with this Report and are not subject to any prohibition on dealing. By accepting this report you agree to be bound by the foregoing limitations. In the normal course of Ambit and its affiliates’ business, circumstances may arise that could result in the interests of Ambit conflicting with the interests of clients or one client’s interests conflicting with the interest of another client. Ambit makes best efforts to ensure that conflicts are identified, managed and clients’ interests are protected. However, clients/potential clients of Ambit should be aware of these possible conflicts of interests and should make informed decisions in relation to Ambit services.

Disclosures

37. The analyst (s) has/have not served as an officer, director or employee of the subject company.

38. There is no material disciplinary action that has been taken by any regulatory authority impacting equity research analysis activities. 39. All market data included in this report are dated as at the previous stock market closing day from the date of this report.

Analyst Certification

Each of the analysts identified in this report certifies, with respect to the companies or securities that the individual analyses, that (1) the views expressed in this report reflect his or her personal views about all of the subject companies and securities and (2) no part of his or her compensation was, is or will be directly or indirectly dependent on the specific recommendations or views expressed in this report. © Copyright 2015 AMBIT Capital Private Limited. All rights reserved.

Ambit Capital Pvt. Ltd. Ambit House, 3rd Floor. 449, Senapati Bapat Marg, Lower Parel, Mumbai 400 013, India. Phone: +91-22-3043 3000 | Fax: +91-22-3043 3100 CIN: U74140MH1997PTC107598 www.ambitcapital.com