conference call august 13, 2004

DESCRIPTION

Consolidated Results. 1 st Half 2004. Conference Call August 13, 2004. Performance Indicators. R$ Million. 2Q04. 1Q04. 1H04. 1H03. Net Income. 305. 276. 581. 491. Earnings/1000 shares (R$). 2.21. 2.01. 4.22. 3.56. ROAE (%). 17.3%. 16.1%. 16.4%. 15.2%. BIS Ratio (%). - PowerPoint PPT PresentationTRANSCRIPT

1

Conference Call

August 13, 2004

Consolidated Results

1st Half 2004

2

Performance Indicators

R$ Million

2Q04 1Q04 1H04 1H03

Net Income 305 276 581 491

Earnings/1000 shares (R$) 2.21 2.01 4.22 3.56

ROAE (%) 17.3% 16.1% 16.4% 15.2%

BIS Ratio (%) 16.7% 18.1% 16.7% 16.7%

Total Assets 80,011 71,505 80,011 66,091

Total Loans 30,045 27,343 30,045 26,195

Deposits+Funds 59,831 56,738 59,831 47,003

Stockholders' Equity 7,704 7,358 7,704 6,847

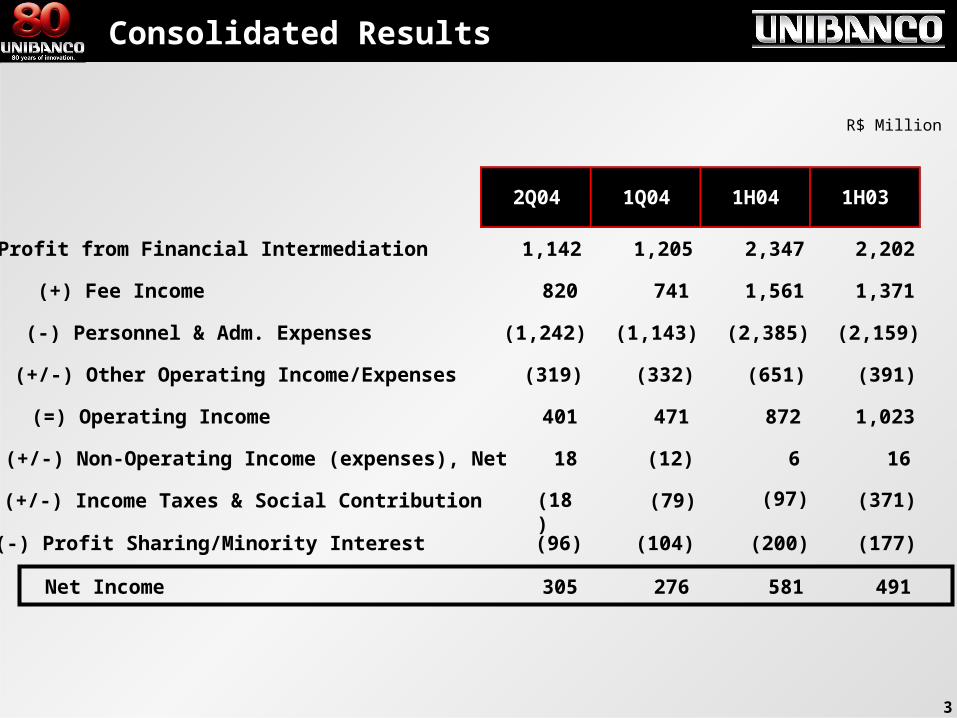

3

R$ Million

Consolidated Results

2Q04 1Q04 1H04 1H03

Profit from Financial Intermediation 1,142 1,205 2,347 2,202

(+) Fee Income 820 741 1,561 1,371

(-) Personnel & Adm. Expenses (1,242) (1,143) (2,385) (2,159)

(+/-) Other Operating Income/Expenses (319) (332) (651) (391)

(=) Operating Income 401 471 872 1,023

(+/-) Non-Operating Income (expenses), Net 18 (12) 6 16

(+/-) Income Taxes & Social Contribution (18)

(79)

(-) Profit Sharing/Minority Interest (96) (104) (200) (177)

Net Income 305 276 581 491

(97) (371)

4

Financial Margin

2Q04 1Q04 1H04 1H03

Revenue from financial intermediation 3,414 2,891 6,305 4,950 Expenses on financial intermediation (1,956) (1,373) (3,329) (2,051)

Financial margin before provision for loan losses (A) 1,458 1,518 2,976 2,899

Provision for loan losses (316) (313) (629) (697) Financial margin (after provision for loan losses) 1,142 1,205 2,347 2,202

Total Average Assets (-) Average Permanent Assets (B) 71,791 67,045 69,741 67,398

Net Financial Margin Annualized (%) (A/B) 8.4% 9.4% 8.7% 8.8%

R$ Million

5

Financial Margin 8.4% 9.4%

Domestic Treasury Losses 0.15%

-

0.15% -0.15%

0.20%

-

2Q04 1Q04

8.90% 9.25%

35 b.p.

8.55% 9.25%

Extraordinary Restatement on Insurance and Pension Plans

Increase in Interbank Investments

Financial Margin Simulation

Comparable Financial Margins

Financial Margin

6

Fiscal Effects

Income before Taxes and Profit Sharing 419 459

Profit Sharing (57) (69)

( A ) Income before Taxes and after Profit Sharing 362 390

Income Tax @ 25% and Social Contribution @ 9% (123) (132)

Adjustments to derive effective tax rate:

Interest on capital stock 42 49

Permanent differences (net) 30 (0)

Subtotal (51) (84)

Exchange rate fluctuation non taxable / (non deductible)and Equity Income 33 5

( B ) Income Tax & Social Contribution for the period (18) (79)

( B / A ) Effective Income Tax & Social Contribution Rate 5% 20%

878

(126)

752

(256)

91

30

(135)

38

(97)

13%

2Q04 1Q04 1H04

R$ Million

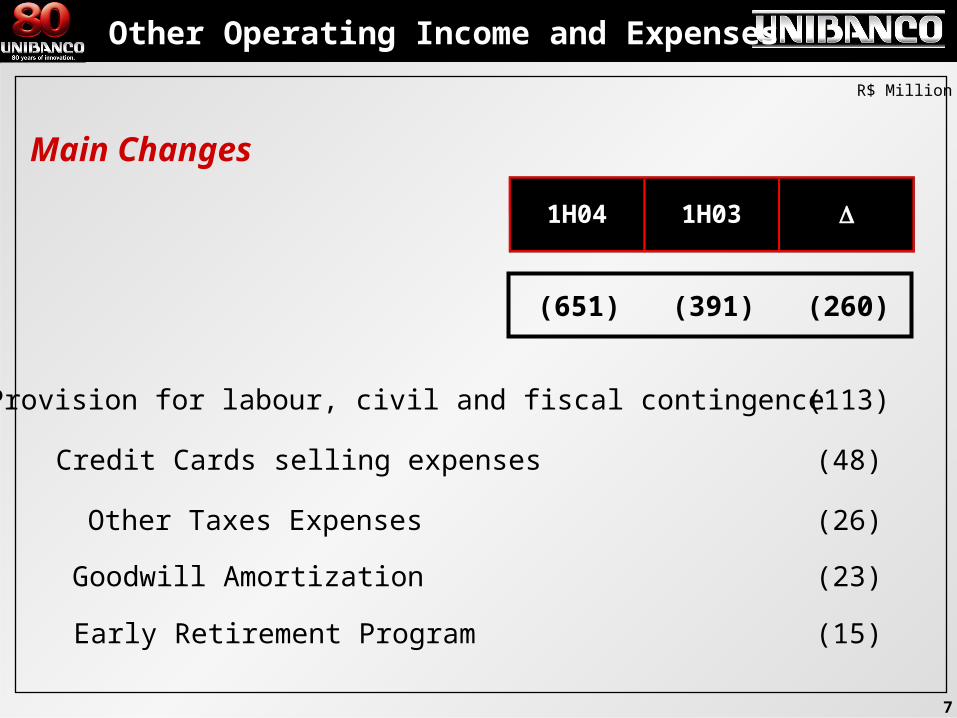

7

R$ Million

Main Changes

1H04 1H03

(651) (391) (260)

(113)

Credit Cards selling expenses (48)

Other Taxes Expenses (26)

Goodwill Amortization (23)

Early Retirement Program (15)

Provision for labour, civil and fiscal contingence

Other Operating Income and Expenses

8

Impact on Investments Abroad

2Q04 1Q04 1H04 1H03

Investments Abroad (US$ Million) 606 674 606 953

Exchange Rate (R$/US$) 3.1075 2.9086 3.1075 2.8720

Exchange rate fluctuation on investments abroad 97 8 105 (642)

Hedge on investments abroad (63) 34 (28) 605

Net Accounting Impact before Income Tax and Social Contribution 34 42 77 (37)

Fiscal Effects 33 3 36 (218)

Net Impact after Income Tax and Social Contribution 67 45 113 (255)

R$ Million

9

R$ Million

Securities Portfolio

Market Value Adjustment

Securities Portfolio

Market Value

Adjustment06/30/2004

2Q04

Market Value

Adjustment03/31/2004

1Q04

Income Statement Impact 65 -46 111 7

Stockholders´ Equity Impact (165) 92 (257) 61

Jun-04 % Portfolio Jun-03 % Portfolio

Trading Securities 9,177 49% 5,582 35%

Securities Available for Sale 3,237 18% 5,051 32%

Securities Held to Maturity 6,174 33% 5,183 33%

Total Securities 18,588 15,816

10

Fees from Services Rendered

1,371

1,561

9.2%

16.7%

28.1%

13.9%

741 809

484565

146

187

1H03 1H04

Assets under Management

Credit Cards

Banking fees and other fees and comissions

R$ Million

11

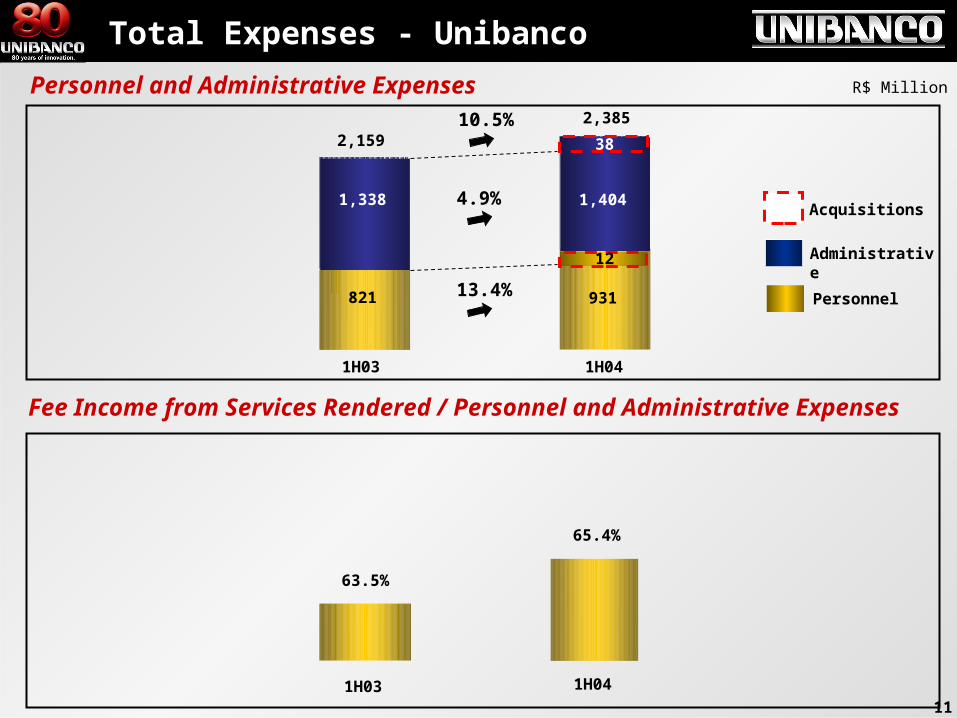

Total Expenses - Unibanco

Personnel and Administrative Expenses R$ Million

Fee Income from Services Rendered / Personnel and Administrative Expenses

1H04

63.5%

65.4%

1H03

Personnel

Administrative

Acquisitions

931

12

1,404

38

821

1,338

1H041H03

2,159

2,385

13.4%

4.9%

10.5%

12

Loan Portfolio Breakdown

Non-Accrual Portfolio / Total Portfolio

AA-C Loan Portfolio

D-H

A

C

AA

B Net Write-Off / Total Portfolio

90.5%

91.9% 91.9% 110.0%108.6%

102.8%

Coverage Ratio of Non-Accrual Portfolio

12.2%7.5% 6.9%

9.9%

9.9% 8.1%

33.9%37.4% 37.7%

34.5% 37.1% 39.2%

9.5% 8.1% 8.1%

Jun-03 Mar-04 Jun-04

26,195 27,343 30,045

AA

A

B

C

D-H

R$ milion

5.5%

4.7% 4.7%

Jun-03 Mar-04 Jun-04

1.1%

1.5%

0.8%

2Q03 1Q04 2Q04

13

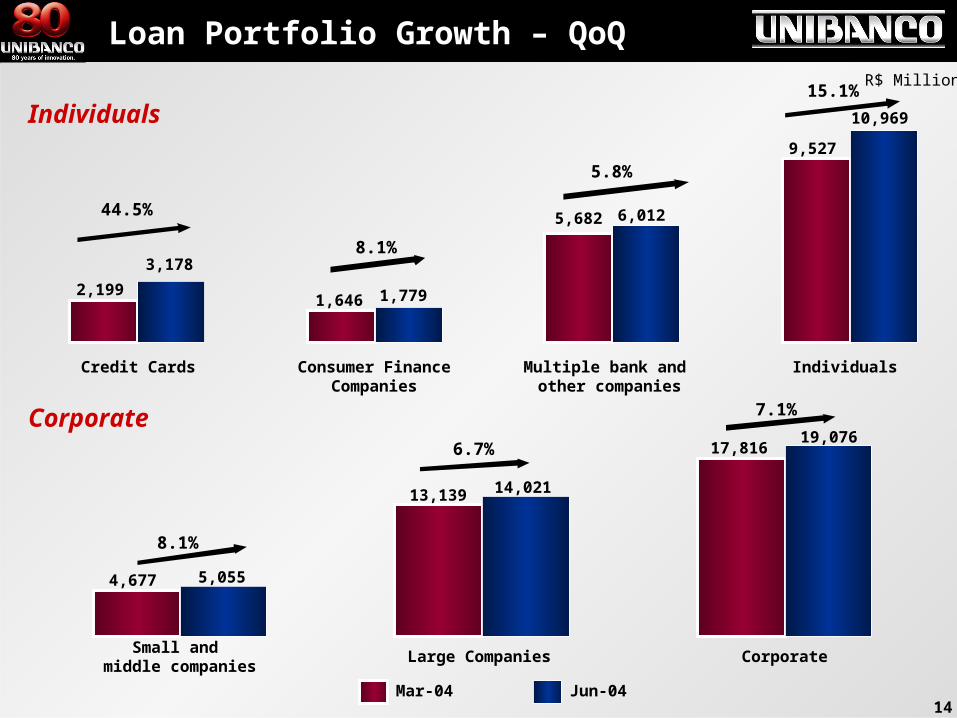

Loan Portfolio Growth

R$ Million

3.0%

7.1%15.1%

7.1%

4.4%9.9%

26,195 27,34330,045

14.7%

Individuals

Corporate

% Jun-04/Jun-03

+23.3%

% Jun-04/Jun-03

+10.3%

17,297 17,816 19,076

8,898 9,52710,969

Jun-03 Mar-04 Jun-04

14

44.5%

5.8%

15.1%

8.1%3,178

10,969

1,779

6,012

2,1991,646

5,682

9,527

7.1%

8.1%

6.7%

Mar-04 Jun-04

19,076

14,021

5,055

17,816

13,139

4,677

Corporate

Individuals

R$ Million

Credit Cards Consumer FinanceCompanies

Multiple bank and other companies

Individuals

Small and middle companies

Large Companies Corporate

Loan Portfolio Growth – QoQ

15

R$ Million

Jun-03 Jun-04

17,297

13,045

4,252

19,076

14,021

5,055

Small and middle companies

Large Companies Corporate

18.9%

7.5%Corporate

10.3%

2,104

8,898

3,178

1,500

5,294

10,969

1,779

6,012

Credit Cards Consumer FinanceCompanies

Multiple bank and other companies

Individuals

51.0%

13.6%

23.3%

Individuals

18.6%

Loan Portfolio Growth - YoY

16

R$ Million

Consumer Companies

Consumer Companies: Fininvest, Unicard, 50% LuizaCred, 50% PontoCred, 33.3% Credicar and HiperCard.

Consumer Companies Under Management: Fininvest, Unicard, 50% PontoCred, 50% PontoCred and HiperCard.

1H04 1H03 1H04 1H03

Equity Income 287 195 186 111

Billings 9,898 7,507 6,913 4,727

Volume of Transactions (million) 132 93 93 57

Credit Portfolio 4,943 3,622 3,647 2,488

Loan Losses 370 344 312 283

Loan Losses / Credit Portfolio 7.5% 9.5% 8.6% 11.4%

ROAE % 56.4% 69.7% 42.0% 50.9%

Consumer CompaniesConsumer Companies

under Management

17

R$ Million

Consumer Companies

Net Income

Number of Transactions (million)

31.8%

82.0%

+

50

91

1H03 1H04

22

29

1H03 1H04

Credit Portfolio

14.1%

1,360

1,552

Jun-03 Jun-04

Billings

12.6%

1,965

2,213

1H03 1H04

18

Consumer Companies

Credit Portfolio Financed Volume

R$ Million

17.1%

16.7%

19.5%

8.1%

7.0%

54

63

1H03 1H04

9671,045

400 428

1H03 1H04

35

41

1H03 1H04

2,516

3,006

1H03 1H04

Net Income Credit Portfolio and Financed Volume

Number of Transactions (million)Billings

19

R$ Million

Consumer Companies

From March 1st to June 30th, 2004.

Equity Income 20

Loan Portfolio 836

Fees 44

Provisions for Loan Losses 19

Portfolio (number of cards - million) 2.5

Billings 1,400

Volume of Transactions (million) 23.5

Average Ticket (R$) 59.60

Financial Information

Business Information

Annualized ROAE % 31%

Provisions for Loan Losses / Credit Portfolio 2.3%

20

Funding

R$ Million

47,003

56,73859,831

14.3%

27.4%

20.7%

% Jun-04-Jun-03

+32.5%

% Jun-04-Jun-03

+22.3%

4.0%

7.0%

5.5%

27.3%

Deposits

Assets under Management

23,978 27,414 29,328

23,02529,324 30,503

Jun-03 Mar-04 Jun-04

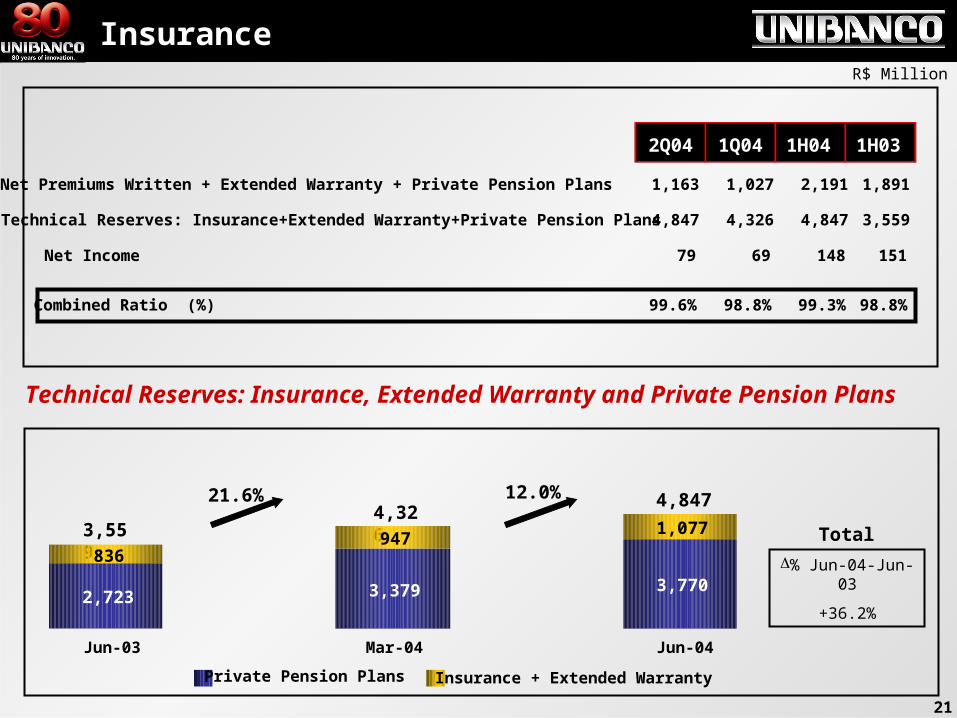

21

Technical Reserves: Insurance, Extended Warranty and Private Pension Plans

R$ Million

Insurance

3,5594,326

4,84712.0%21.6%

2,723 3,379 3,770

836947

1,077

Jun-03 Mar-04 Jun-04

Private Pension Plans Insurance + Extended Warranty

Net Premiums Written + Extended Warranty + Private Pension Plans 1,163 1,027 2,191 1,891

Technical Reserves: Insurance+Extended Warranty+Private Pension Plans 4,847 4,326 4,847 3,559

Net Income 79 69 148 151

Combined Ratio (%) 99.6% 98.8% 99.3% 98.8%

2Q04 1Q04 1H04 1H03

% Jun-04-Jun-03

+36.2%

Total

22

Claims Ratio

Administrative Expenses / Net Premiums Written

Insurance

51.7%51.9%

50.5%

2Q03 1Q04 2Q04

14.3%

11.7% 11.3%

2Q03 1Q04 2Q04

23

BNL Brasil Acquisition

Banca Nazionale del Lavoro (BNL) received 1,000,000,000 of Units (one billion of Units) from Unibanco and Unibanco Holdings. After the

conclusion of the transaction, BNL will own, directly and indirectly, 1.43% of Unibanco’s capital.

BNL Brasil (acquisition information):

Credit Portfolio of R$698.5 million

107 thousand clients

96 thousand cards issued

400 corporate clients, majority of Italian and European companies

will establish the Italian Desk.

24

Aumento de Liquidez na BovespaStocks Liquidity

Stocks Liquidity Increase (UBBR11)

Daily Average Volume

Trades

1Q03 2Q03 3Q03 4Q03 1Q04 2Q04

46

31

44

94

121

102

30,37128,757

39,219

22,674

25,157

16,835

3Q04*

290

31,453

* Until August 08th, 2004.

25

Reverse Stock Split

Unit R$ 127.10 / 1,000 Units

GDS US$ 21.01 / 500 Units

Unit R$ 12.71 / Units

GDS US$ 21.01 / 5 Units

BEFORE AFTERREVERSE

STOCK SPLIT Price on Aug.12,2004

As of August 30, 2004 every

100 shares will become 1 share.

26

Macroeconomic Perspectives 2004

GDP 3.5% 3.7%

Exchange Rate (R$ / US$) 3.05 3.10

SELIC (end of the year) 13.0% 15.5%

IPC-A 6.8% 7.2%

On May 13, 2004 On Aug 13, 2004

27

Guidelines onMay 13, 2004

1H04 vs.1H03

Guidelines onAug 13, 2004

Loan Portfolio 20% 15% 18%

Corporate 13% 10% 9%Large 10% 7% 5%Small and Medium 23% 20% 22%

Individuals 32% 23% 30%Multiple bank and other companies 25% 14% 22%Consumer Companies 25% 19% 23%Credit Cards

Administrative Expenses 7% 10% 9%

Fee Income 10-15% 14% 12-16%

Unibanco Guidelines 2004

HiperCard: (1) 30% (2) 40% (3) 41%

55%(1) 51%(2) 54%(3)

28

For further information contact our Investor Relations Area at

phone: 5511-3097-1626 / 1313fax: 5511-3813-6182

email: [email protected]: www.ir.unibanco.com

This presentation contains forward-looking statements regarding Unibanco. its subsidiaries and affiliates - anticipated synergies. growth plans. projected results and future strategies. Although these forward-looking statements reflect management’s good faith beliefs. they involve known and unknown risks and uncertainties that may cause the Company’s actual results or outcomes to be materially different from those anticipated and discussed herein. These risks and uncertainties include. but are not limited to. our ability to realize the amount of the projected synergies and the timetable projected. as well as economic. competitive. governmental and technological factors affecting Unibanco’s operations. markets. products and prices. and other factors detailed in Unibanco’s filings with the Securities and Exchange Commission which readers are urged to read carefully in assessing the forward-looking statements contained herein. Unibanco undertakes no duty to update any of the projections contained herein.