consolidated and other financial statements - eyjapan.jp · financial reporting developments a...

TRANSCRIPT

Financial reporting developments A comprehensive guide

Consolidated and other financial statements Noncontrolling interests, combined financial statements, and parent company financial statements

Revised October 2012

Financial reporting developments Consolidated and other financial statements

To our clients and other friends

This Financial reporting developments (―FRD‖) publication is designed to help you understand financial

reporting issues related to the accounting for noncontrolling interests. This publication also includes

interpretive guidance on consolidation procedure and on the presentation of combined and parent-only

financial statements. The publication reflects our current understanding of the provisions in ASC 810,

Consolidations, based on our experience with financial statement preparers and related discussions with

the FASB and SEC staffs.

The accounting for noncontrolling interests is based on the economic entity concept of consolidated

financial statements. Under the economic entity concept, all residual economic interest holders in an

entity have an equity interest in the consolidated entity, even if the residual interest is relative to only a

portion of the entity (that is, a residual interest in a subsidiary). Therefore, a noncontrolling interest is

required to be displayed in the consolidated statement of financial position as a separate component of

equity. Likewise, the consolidated net income or loss and comprehensive income or loss attributable to

both controlling and noncontrolling interests is separately presented on the consolidated statement of

comprehensive income.

Consistent with the economic entity concept, after control is obtained, increases or decreases in

ownership interests that do not result in a loss of control should be accounted for as equity transactions.

However, changes in ownership interests that result in a loss of control of a subsidiary or group of assets

generally result in corresponding gain or loss recognition upon deconsolidation. The decrease in

ownership guidance generally does not apply to transactions involving non-businesses, in-substance real

estate or oil and gas mineral rights conveyances.

The primary revisions made to this publication include the reorganization of certain content and the

removal of the discussion of the transition guidance in FASB Statement No. 160, Noncontrolling Interests

in Consolidated Financial Statements, an amendment of ARB No. 51 (primarily codified in ASC 810).

We also enhanced the interpretive guidance in Chapter 2 related to the presentation of noncontrolling

interests when derivatives are issued with or as part of those interests. We also added certain other

interpretive guidance (for example, to reflect the issuance of new guidance for deconsolidating in-

substance real estate). These important changes are summarized in Appendix C.

Practice and authoritative guidance interpreting the provisions of ASC 810 continue to evolve and

therefore readers should monitor developments in this area closely.

October 2012

Financial reporting developments Consolidated and other financial statements i

Contents

1 Consolidated financial statements .............................................................................. 1

1.1 Objectives and scope ............................................................................................................. 1

1.2 Consolidation procedure — time of acquisition.......................................................................... 4

1.2.1 Acquisition through single step ...................................................................................... 4

1.2.2 Acquisition through multiple steps ................................................................................. 4

1.3 Proportionate consolidation ................................................................................................... 5

1.4 Differing fiscal year-ends between parent and subsidiary ......................................................... 6

2 Nature and classification of the noncontrolling interest ................................................ 8

2.1 Noncontrolling interests ......................................................................................................... 8

2.2 Equity derivatives issued on the stock of a subsidiary ............................................................... 9

2.2.1 Is the equity derivative embedded in the noncontrolling interest or freestanding? .......... 10

2.2.1.1 Equity derivatives considered embedded ............................................................ 11

2.2.1.2 Equity derivatives considered freestanding ......................................................... 11

2.2.2 Equity derivatives deemed to be financing arrangements .............................................. 12

2.2.3 Application of the redeemable equity guidance ............................................................. 12

2.2.3.1 Measurement and reporting issues related to redeemable equity securities .......... 13

2.2.4 Earnings per share considerations................................................................................ 14

2.2.5 Examples of the presentation of noncontrolling interests with equity

derivatives issued on those interests ............................................................................ 14

2.2.6 Redeemable or convertible equity securities and UPREIT structures .............................. 19

2.2.7 Redeemable noncontrolling interest denominated in a foreign currency ......................... 20

3 Attribution of net income or loss and comprehensive income or loss ........................... 22

3.1 Attribution procedure .......................................................................................................... 22

3.1.1 Substantive profit sharing arrangements ...................................................................... 22

3.1.2 Attribution of losses .................................................................................................... 24

3.1.2.1 Distributions in excess of the noncontrolling interest’s carrying amount ............... 24

3.1.3 Attribution to noncontrolling interests held by preferred shareholders ........................... 25

3.1.4 Attribution of goodwill impairment ............................................................................... 25

3.1.5 Attributions related to business combinations effected before Statement

160 and Statement 141(R) were adopted .................................................................... 26

3.1.6 Effect on effective income tax rate ............................................................................... 26

4 Changes in a parent’s ownership interest in a subsidiary while control is retained ........ 28

4.1 Increases and decreases in a parent’s ownership of a subsidiary ............................................. 28

4.1.1 Increases in a parent’s ownership interest in a subsidiary .............................................. 29

4.1.1.1 Increases in a parent’s ownership interest in a consolidated VIE ........................... 30

4.1.2 Decreases in a parent’s ownership interest in a subsidiary without loss of control ........... 30

4.1.2.1 Accounting for a stock option of subsidiary stock ................................................ 32

4.1.2.2 Scope exception for in-substance real estate transactions ................................... 32

4.1.2.3 Scope exception for oil and gas conveyances ...................................................... 32

4.1.2.4 Decreases in ownership of a subsidiary that is not a business or

nonprofit activity ............................................................................................... 33

Contents

Financial reporting developments Consolidated and other financial statements ii

4.1.2.5 Issuance of preferred stock by a subsidiary ......................................................... 34

4.1.2.6 Decreases in ownership through issuance of partnership units that

have varying profit or liquidation preferences ..................................................... 34

4.1.3 Accumulated other comprehensive income considerations ............................................ 35

4.1.4 Accounting for foreign currency translation adjustments upon a change in

parent’s ownership interest without loss of control ....................................................... 36

4.1.5 Allocating goodwill upon change in parent’s ownership interest ..................................... 36

4.1.6 Accounting for transaction costs incurred in connection with changes in ownership........ 37

4.1.7 Chart summarizing accounting for changes in ownership .............................................. 37

4.2 Comprehensive example ...................................................................................................... 38

4.2.1 Consolidation at the acquisition date ............................................................................ 38

4.2.2 Consolidation in year of combination ............................................................................ 40

4.2.3 Consolidation after purchasing an additional interest .................................................... 42

4.2.4 Consolidation in year 2 ................................................................................................ 44

4.2.5 Consolidation after selling an interest without loss of control ......................................... 46

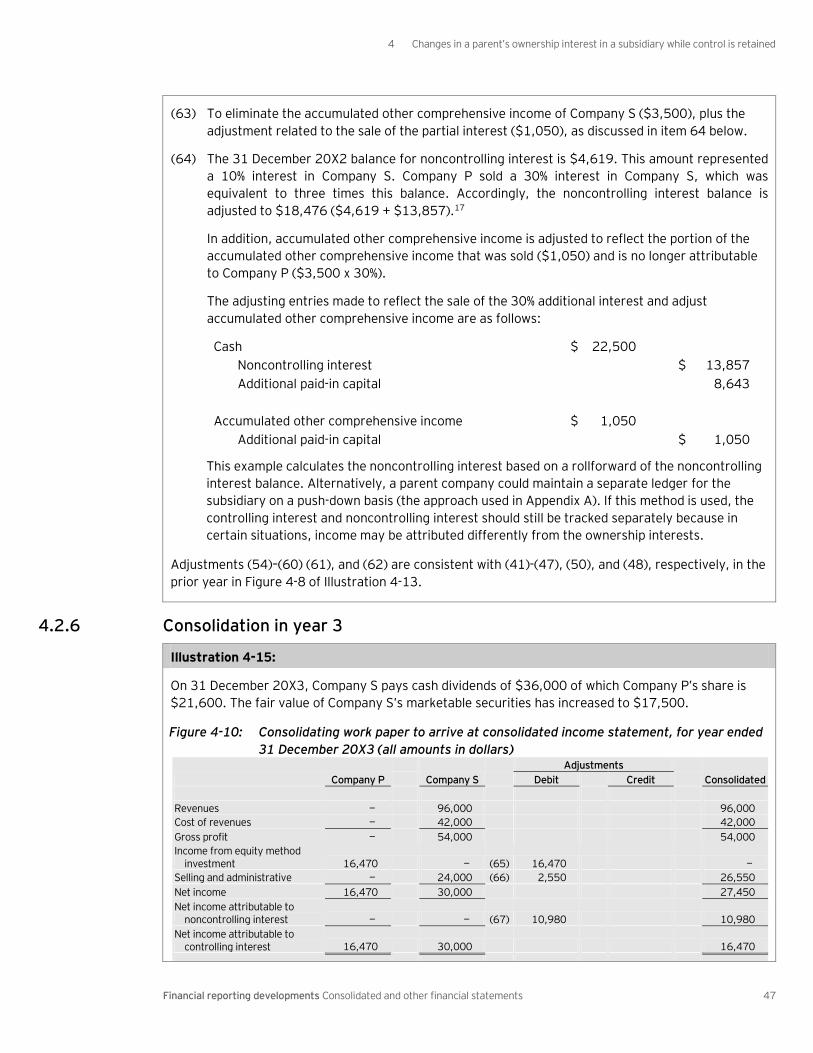

4.2.6 Consolidation in year 3 ................................................................................................ 47

5 Intercompany eliminations ....................................................................................... 50

5.1 Procedures for eliminating intercompany balances and transactions ...................................... 50

5.1.1 Effect of noncontrolling interest on elimination of intercompany amounts ...................... 51

6 Loss of control over a subsidiary or a group of assets ................................................ 63

6.1 Deconsolidation of a subsidiary or derecognition of certain groups of assets ........................... 63

6.1.1 Loss of control ............................................................................................................ 65

6.1.2 Nonreciprocal transfers to owners ............................................................................... 65

6.1.3 Gain/loss recognition................................................................................................... 66

6.1.4 Measuring the fair value of consideration received and any retained

noncontrolling investment ........................................................................................... 67

6.1.4.1 Accounting for contingent consideration in deconsolidation ................................. 68

6.1.4.2 Accounting for a retained creditor interest in deconsolidation .............................. 71

6.1.5 Accounting for accumulated other comprehensive income in deconsolidation ................ 71

6.1.6 Deconsolidation through multiple arrangements ........................................................... 71

6.1.7 Deconsolidation through a bankruptcy proceeding ........................................................ 72

6.1.8 Gain/loss classification and presentation ...................................................................... 73

6.1.9 Subsequent accounting for retained noncontrolling investment ..................................... 73

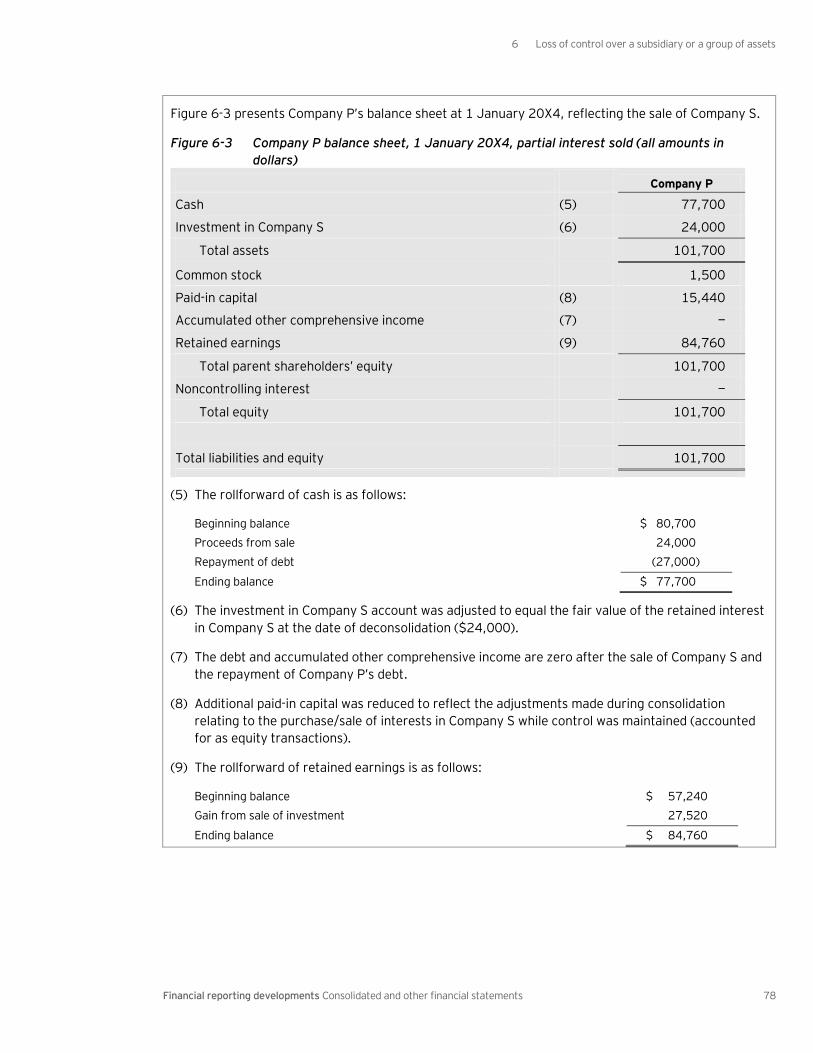

6.2 Comprehensive example ...................................................................................................... 74

6.2.1 Deconsolidation by selling entire interest ...................................................................... 75

6.2.2 Deconsolidation by selling a partial interest .................................................................. 77

7 Combined financial statements ................................................................................. 79

7.1 Purpose of and procedures for combined financial statements ............................................... 79

7.1.1 Common management ................................................................................................ 79

7.1.2 Procedures applied in combining entities for financial reporting ..................................... 80

8 Parent-company financial statements ....................................................................... 81

8.1 Purpose of and procedures for parent-company financial statements ..................................... 81

8.1.1 Investments in subsidiaries .......................................................................................... 81

8.1.2 Investments in non-controlled entities .......................................................................... 82

8.1.3 Disclosure requirements .............................................................................................. 82

Contents

Financial reporting developments Consolidated and other financial statements iii

9 Presentation and disclosures .................................................................................... 83

9.1 Certain presentation and disclosure requirements related to consolidation ............................. 83

9.1.1 Consolidated statement of comprehensive income presentation .................................... 84

9.1.2 Reconciliation of equity presentation ........................................................................... 84

9.1.2.1 Presentation of redeemable noncontrolling interests in equity reconciliation ........ 85

9.1.2.2 Interim reporting period requirements ................................................................ 85

9.1.3 Consolidated statement of financial position presentation ............................................. 86

9.1.4 Consolidated statement of cash flows presentation ....................................................... 86

9.1.4.1 Presentation of transaction costs in statement of cash flow ................................. 87

9.1.5 Disclosure ................................................................................................................... 87

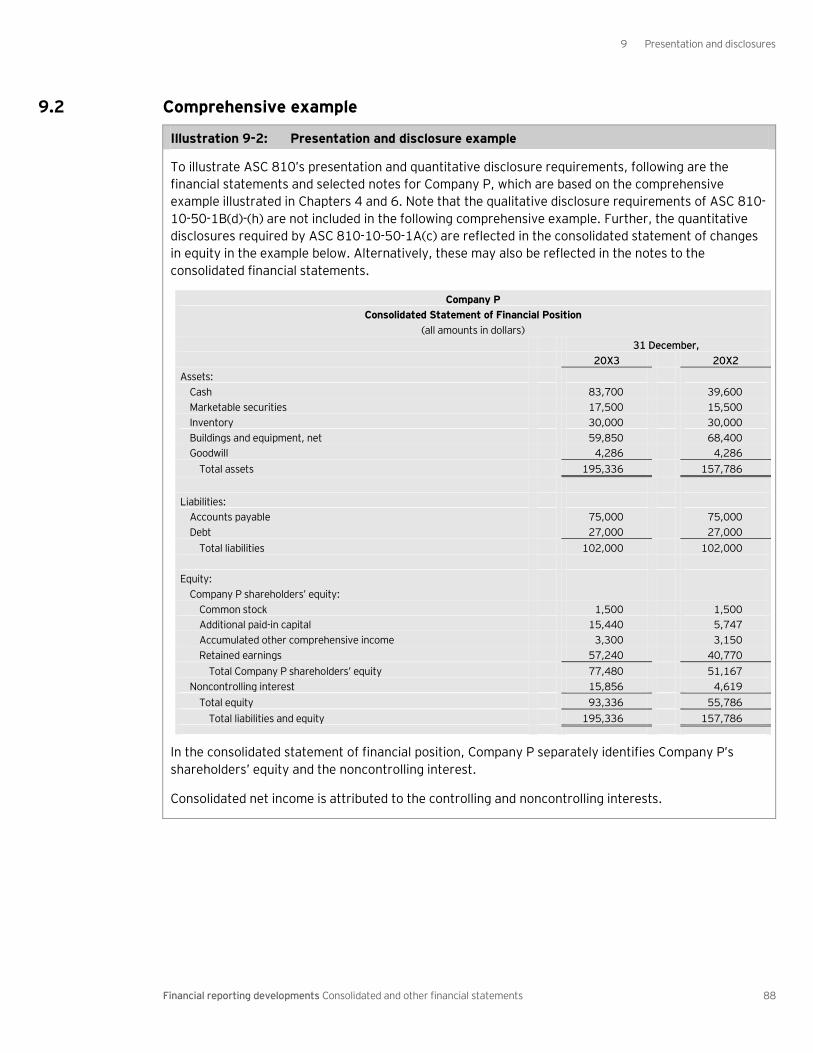

9.2 Comprehensive example ...................................................................................................... 88

A Comprehensive example .......................................................................................... A-1

B Comparison of ASC 810 to IAS 27(R) ....................................................................... B-1

C Summary of important changes ............................................................................... C-1

D Abbreviations used in this publication ...................................................................... D-1

E Index of ASC references in this publication ............................................................... E-1

Contents

Financial reporting developments Consolidated and other financial statements iv

Notice to readers:

This publication includes excerpts from and references to the FASB Accounting Standards Codification

(the Codification or ASC). The Codification uses a hierarchy that includes Topics, Subtopics, Sections

and Paragraphs. Each Topic includes an Overall Subtopic that generally includes pervasive guidance for

the topic and additional Subtopics, as needed, with incremental or unique guidance. Each Subtopic

includes Sections that in turn include numbered Paragraphs. Thus, a Codification reference includes the

Topic (XXX), Subtopic (YY), Section (ZZ) and Paragraph (PP).

Throughout this publication references to guidance in the codification are shown using these reference

numbers. References are also made to certain pre-codification standards (and specific sections or

paragraphs of pre-Codification standards) in situations in which the content being discussed is excluded

from the Codification.

This publication has been carefully prepared but it necessarily contains information in summary form and

is therefore intended for general guidance only; it is not intended to be a substitute for detailed research

or the exercise of professional judgment. The information presented in this publication should not be

construed as legal, tax, accounting, or any other professional advice or service. Ernst & Young LLP can

accept no responsibility for loss occasioned to any person acting or refraining from action as a result of

any material in this publication. You should consult with Ernst & Young LLP or other professional

advisors familiar with your particular factual situation for advice concerning specific audit, tax or other

matters before making any decisions.

Portions of FASB publications reprinted with permission. Copyright Financial Accounting Standards Board, 401 Merritt 7, P.O. Box 5116, Norwalk, CT 06856-5116, U.S.A. Portions of AICPA Statements of Position, Technical Practice Aids, and other AICPA publications reprinted with permission. Copyright American Institute of Certified Public Accountants, 1211 Avenue of the Americas, New York, NY 10036-8875, USA. Copies of complete documents are available from the FASB and the AICPA.

Financial reporting developments Consolidated and other financial statements 1

1 Consolidated financial statements

1.1 Objectives and scope

Excerpt from Accounting Standards Codification Consolidation — Overall

Objectives

General

810-10-10-1

The purpose of consolidated financial statements is to present, primarily for the benefit of the owners

and creditors of the parent, the results of operations and the financial position of a parent and all its

subsidiaries as if the consolidated group were a single economic entity. There is a presumption that

consolidated financial statements are more meaningful than separate financial statements and that

they are usually necessary for a fair presentation when one of the entities in the consolidated group

directly or indirectly has a controlling financial interest in the other entities.

Scope and Scope Exceptions

Entities

810-10-15-8

The usual condition for a controlling financial interest is ownership of a majority voting interest, and,

therefore, as a general rule ownership by one reporting entity, directly or indirectly, of more than 50

percent of the outstanding voting shares of another entity is a condition pointing toward consolidation.

The power to control may also exist with a lesser percentage of ownership, for example, by contract,

lease, agreement with other stockholders, or by court decree.

810-10-15-10

A reporting entity shall apply consolidation guidance for entities that are not in the scope of the Variable

Interest Entities Subsections (see the Variable Interest Entities Subsection of this Section) as follows:

a. All majority-owned subsidiaries — all entities in which a parent has a controlling financial interest —

shall be consolidated. However, there are exceptions to this general rule.

1. A majority-owned subsidiary shall not be consolidated if control does not rest with the

majority owner — for instance, if any of the following are present:

i. The subsidiary is in legal reorganization

ii. The subsidiary is in bankruptcy

iii. The subsidiary operates under foreign exchange restrictions, controls, or other

governmentally imposed uncertainties so severe that they cast significant doubt on the

parent's ability to control the subsidiary.

iv. In some instances, the powers of a shareholder with a majority voting interest to control

the operations or assets of the investee are restricted in certain respects by approval or

veto rights granted to noncontrolling shareholder (hereafter referred to as

noncontrolling rights). In paragraphs 810-10-25-2 through 25-14, the term

noncontrolling shareholder refers to one or more noncontrolling shareholders. Those

noncontrolling rights may have little or no impact on the ability of a shareholder with a

1 Consolidated financial statements

Financial reporting developments Consolidated and other financial statements 2

majority voting interest to control the investee's operations or assets, or, alternatively,

those rights may be so restrictive as to call into question whether control rests with the

majority owner.

v. Control exists through means other than through ownership of a majority voting

interest, for example as described in (b) through (e).

2. A majority-owned subsidiary in which a parent has a controlling financial interest shall not be

consolidated if the parent is a broker-dealer within the scope of Topic 940 and control is

likely to be temporary.

3. Except as discussed in paragraph 946-810-45-3, consolidation by an investment company

within the scope of Topic 946 of a non-investment-company investee is not appropriate.

b. Subtopic 810-20 shall be applied to determine whether the rights of the limited partners in a

limited partnership overcome the presumption that the general partner controls, and therefore

should consolidate, the partnership.

c. Subtopic 810-30 shall be applied to determine the consolidation status of a research and

development arrangement.

d. The Consolidation of Entities Controlled by Contract Subsections of this Subtopic shall be applied

to determine whether a contractual management relationship represents a controlling financial

interest.

e. Paragraph 710-10-45-1 addresses the circumstances in which the accounts of a rabbi trust that

is not a VIE (see the Variable Interest Entities Subsections for guidance on VIEs) shall be

consolidated with the accounts of the employer in the financial statements of the employer.

ASC 810 defines a subsidiary as an entity in which a parent has a controlling financial interest, whether

that controlling interest comes through voting interests or other means (for example, variable interests).

While consolidation policy is not the subject of this publication, in general, the first step in determining

whether an entity has a controlling financial interest in a subsidiary is to establish the basis on which the

investee is to be evaluated for control (that is, whether the consolidation determination should be based

on ownership of the investee’s outstanding voting interests or its variable interests). Accordingly, the

provisions of ASC 810-10’s variable interest model1 should first be applied to determine whether the

investee is a variable interest entity (VIE). Only if the entity is determined not to be a VIE should the

consolidation guidance for voting interest entities within ASC 810-10 be applied.

Once it is determined a parent has a controlling financial interest in an entity, the assets, liabilities and

any noncontrolling interests of that entity are accounted for in the parent’s consolidated financial

statements in accordance with the consolidation principles in ASC 810-10-45. These principles are

generally the same for entities consolidated under the voting interest and variable interest models.

Illustration 1-1 summarizes how ASC 810’s control framework should generally be applied to interests in

an entity.

1 Generally ASC 810-10 includes guidance with respect to the consolidation considerations for voting interest entities and variable

interest entities for each of ASC 810-10’s sections. In each of ASC 810-10’s sections there is a General subsection with respect to the consolidation model. This guidance applies to voting interest entities and also may apply to variable interest entities in certain circumstances. The Variable Interest Entities subsection within each of ASC 810-10’s sections contains considerations

with respect to variable interest entities. In referring to the Variable Interest Model in ASC 810-10, we are referring to the guidance applicable to variable interest entities in each of ASC 810-10’s sections.

1 Consolidated financial statements

Financial reporting developments Consolidated and other financial statements 3

Illustration 1-1: ASC 810, Consolidation Decision Tree

1 See our Financial reporting developments publication, Consolidation of variable interest entities, for guidance on silos and specified assets.

No Yes

Related party or de facto

agent consolidates entity

Does the enterprise,

including its related parties and de facto agents,

collectively have power and benefits?

Yes

Variable Interest Model

Is the entity being evaluated for consolidation a legal entity?

No

Yes

No

Yes

Yes

No

Does a scope exception to consolidation guidance (ASC 810) apply?

• Employee benefit plans

• Governmental organizations

• Certain investment companies

Does a scope exception to the Variable Interest Model apply?

• Not-for-profit organizations

• Separate accounts of life insurance companies

• Lack of information

• Certain businesses

Does the enterprise have a variable

interest in a legal entity?

Consider whether fees paid to a decision maker or a

service provider represent a variable interest

Apply other GAAP

Is the legal entity a variable interest entity?

• Does the entity have sufficient equity to finance its activities without additional subordinated financial support?

• Do the equity holders, as a group, lack the characteristics

of a controlling financial interest?

• Is the legal entity structured with non-substantive voting

rights (i.e., anti-abuse clause)?

Apply other GAAP

Consider whether silos exist or whether the interests or

other contractual arrangements of the entity (excluding

interests in silos) qualify as variable interests in the entity

as a whole1

Yes No

Is the enterprise the primary beneficiary (i.e., Does the enterprise individually have both

power and benefits)?

Variable Interest Model (cont.)

No Yes

Consolidate entity Does a related party or de facto agent

individually have power and benefits?

No

No Yes

Party most

closely associated with

VIE consolidates

Do not

consolidate

Do the minority shareholders

hold substantive participating rights or do certain other

conditions exist (e.g., legal subsidiary is in bankruptcy)?

No Yes

Do not consolidate

No Yes

Do not consolidate Consolidate entity

Voting model

The general partner (GP) is presumed to

have control unless that presumption can be overcome by one the following conditions:

• Can a simple majority vote of limited partners remove a general partner without cause and there are no barriers to the exercise that removal right?

• Do limited partners have substantive participating rights?

Consolidation of partnerships and

similar entities

Consolidation of corporations and

other legal entities

Does a majority shareholder, directly or

indirectly, have greater than 50% of the outstanding voting shares?

No Yes

GP does not consolidate the entity. In limited

circumstances a limited partner may consolidate

(e.g., a single limited partner that has the ability to liquidate

the limited partnership or kick out the general partner

without cause).

GP consolidates entity

1 Consolidated financial statements

Financial reporting developments Consolidated and other financial statements 4

Note:

The FASB currently has a consolidation project on its agenda to amend ASC 810. The FASB’s tentative

decisions would modify the provisions for evaluating an enterprise as a principal or an agent and the

provisions for evaluating the substance of kick-out rights and participating rights, among other things.

Additionally, the tentative decisions would modify the literature in ASC 810-20 used to reach

consolidation conclusions for limited partnerships and similar entities. Readers should monitor

developments in this area closely.

1.2 Consolidation procedure — time of acquisition

An entity may acquire a controlling financial interest in a subsidiary through a single step or through

multiple steps over time.

1.2.1 Acquisition through single step

ASC 805 provides guidance when an acquirer obtains control of an acquiree through a single investment,

often referred to as a ―single-step acquisition.‖ Single step acquisitions are perhaps the most

recognizable form of business combination. ASC 805 requires an acquirer to recognize the assets

acquired, the liabilities assumed, and any noncontrolling interest in the acquiree, generally measured at

their fair values as of the acquisition date. These concepts are discussed further in our FRD, Business

combinations. The comprehensive example in Chapter 4 includes an example of the accounting for a

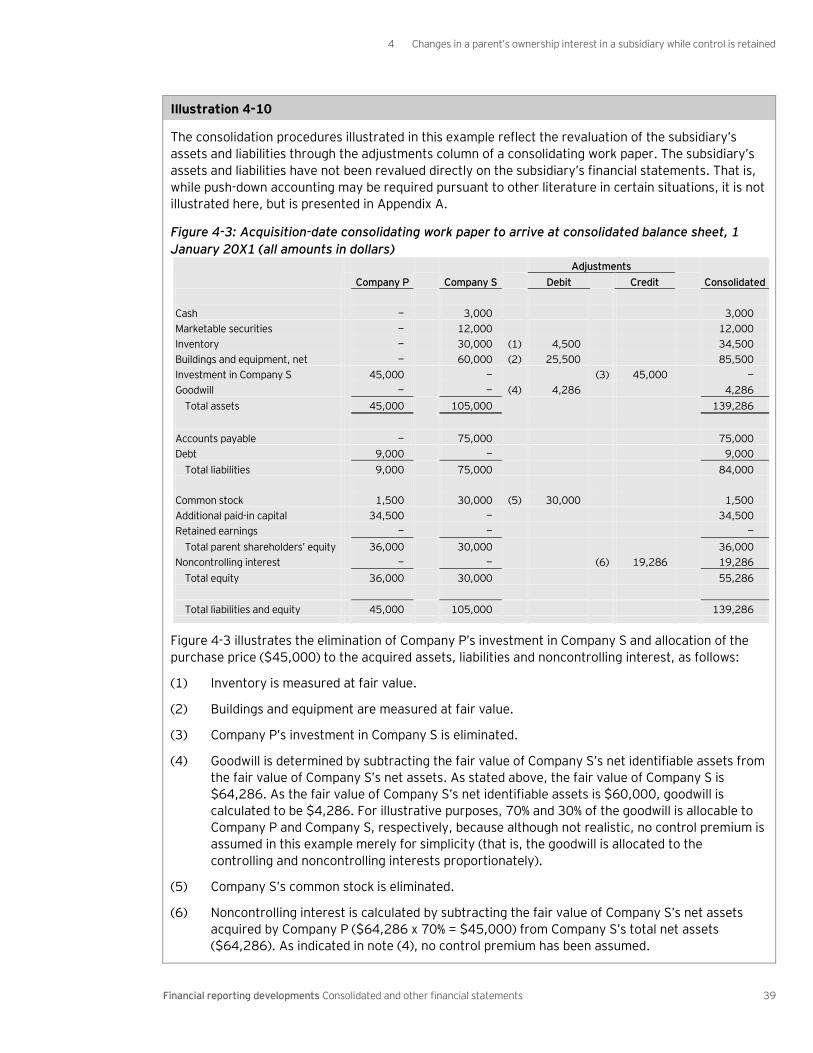

single-step acquisition. See Section 4.2, Illustration 4-9; Section 4.2.1, Illustration 4-10; and Section

4.2.2, Illustration 4-11.

1.2.2 Acquisition through multiple steps

An acquirer may obtain control of an acquiree through a series of two or more investments, which is

commonly referred to as a ―step acquisition.‖ or, in ASC 805, as a ―business combination achieved in

stages.‖ Under ASC 805, if the acquirer holds a noncontrolling equity investment in the acquiree

immediately before obtaining control, the acquirer should first remeasure that investment to fair value as

of the acquisition date and recognize any remeasurement gain or loss in earnings. If, before obtaining

control, an acquirer recognized changes in the value of its noncontrolling investment in the target in

other comprehensive income (that is, the investment was classified as available-for-sale in accordance

with ASC 320), the amount recognized in other comprehensive income as of the acquisition date should

be reclassified from other comprehensive income and included in the recognized remeasurement gain or

loss as of the acquisition date. The acquirer then should apply ASC 805’s business combination guidance,

as discussed in our FRD, Business combinations.

After taking control of a target company, further acquisitions of ownership interests (i.e., acquisitions of

noncontrolling ownership interests with no changes in control) are accounted for as transactions among

shareholders within equity pursuant to the guidance in ASC 810 (refer to Chapter 4).

Illustration 1-2 summarizes these concepts.

1 Consolidated financial statements

Financial reporting developments Consolidated and other financial statements 5

Illustration 1-2: Summary of guidance applied for acquisitions of an interest in an entity

Acquisition of an

interest prior to

obtaining control

Apply other GAAP (ASC 320, ASC 323 and ASC 815, among others).

Acquisition of an

additional interest,

which provides control

First, remeasure the previously held interest (i.e., the interest held before

obtaining control, if any) at fair value, recognizing any gain or loss in

earnings. Next, measure and consolidate (generally at fair value) the net

assets acquired and any noncontrolling interests, in accordance with ASC

805. (Refer to our FRD, Business combinations, for further interpretive

guidance).

Acquisition of an

additional interest,

after control has

already been obtained*

Reduce the carrying amount of the noncontrolling interest. Recognize any

difference between the consideration paid and the reduction to the

noncontrolling interest in equity attributable to the controlling interest.

(See Chapter 4 for further interpretive guidance).

* See Section 4.1.2 for further discussion of this accounting.

1.3 Proportionate consolidation

Excerpt from Accounting Standards Codification Consolidation — Overall

Other Presentation Matters

810-10-45-14

If the investor-venturer owns an undivided interest in each asset and is proportionately liable for its

share of each liability, the provisions of paragraph 323-10-45-1 may not apply in some industries. For

example, in certain industries the investor-venturer may account in its financial statements for its pro

rata share of the assets, liabilities, revenues, and expenses of the venture. Specifically, a

proportionate gross financial statement presentation is not appropriate for an investment in an

unincorporated legal entity accounted for by the equity method of accounting unless the investee is in

either the construction industry (see paragraph 910-810-45-1) or an extractive industry (see

paragraphs 930-810-45-1 and 932-810-45-1). An entity is in an extractive industry only if its

activities are limited to the extraction of mineral resources (such as oil and gas exploration and

production) and not if its activities involve related activities such as refining, marketing, or

transporting extracted mineral resources.

Real Estate — General — Investments — Equity Method and Joint Ventures

Recognition

970-323-25-12

If real property owned by undivided interests is subject to joint control by the owners, the investor-

venturers shall not present their investments by accounting for their pro rata share of the assets,

liabilities, revenues, and expenses of the ventures. Most real estate ventures with ownership in the

form of undivided interests are subject to some level of joint control. Accordingly, such investments

shall be presented in the same manner as investments in noncontrolled partnerships.

1 Consolidated financial statements

Financial reporting developments Consolidated and other financial statements 6

The use of the proportionate gross financial statement presentation method (that is, proportionate

consolidation, as described in ASC 810-10-45-14) is permitted only in the following circumstances: a)

investments in certain unincorporated legal entities in the extractive or construction industry that

otherwise would be accounted for under the equity method of accounting (i.e., a controlling interest does

not exist), and b) ownership of an undivided interest in real property when each owner is entitled only to

its pro rata share of income and expenses and is proportionately (i.e., severally) liable for its share of

each liability, and the real property owned is not subject to joint control by the owners.

1.4 Differing fiscal year-ends between parent and subsidiary

Excerpt from Accounting Standards Codification Consolidation — Overall

Objectives

General

Differing Fiscal Year-Ends Between Parent and Subsidiary

810-10-15-11

A difference in fiscal periods of a parent and a subsidiary does not justify the exclusion of the

subsidiary from consolidation.

Other Presentation Matters

Differing Fiscal Year-Ends Between Parent and Subsidiary

810-10-45-12

It ordinarily is feasible for the subsidiary to prepare, for consolidation purposes, financial statements

for a period that corresponds with or closely approaches the fiscal period of the parent. However, if

the difference is not more than about three months, it usually is acceptable to use, for consolidation

purposes, the subsidiary's financial statements for its fiscal period; if this is done, recognition should

be given by disclosure or otherwise to the effect of intervening events that materially affect the

financial position or results of operations

810-10-45-13

A parent or an investor should report a change to (or the elimination of) a previously existing

difference between the parent's reporting period and the reporting period of a consolidated entity or

between the reporting period of an investor and the reporting period of an equity method investee in

the parent's or investor's consolidated financial statements as a change in accounting principle in

accordance with the provisions of Topic 250. While that Topic generally requires voluntary changes in

accounting principles to be reported retrospectively, retrospective application is not required if it is

impracticable to apply the effects of the change pursuant to paragraphs 250-10-45-9 through 45-10.

The change or elimination of a lag period represents a change in accounting principle as defined in

Topic 250. The scope of this paragraph applies to all entities that change (or eliminate) a previously

existing difference between the reporting periods of a parent and a consolidated entity or an investor

and an equity method investee. That change may include a change in or the elimination of the

previously existing difference (lag period) due to the parent's or investor's ability to obtain financial

results from a reporting period that is more consistent with, or the same as, that of the parent or

investor. This paragraph does not apply in situations in which a parent entity or an investor changes its

fiscal year-end.

1 Consolidated financial statements

Financial reporting developments Consolidated and other financial statements 7

Disclosure

810-10-50-2

An entity should make the disclosures required pursuant to Topic 250. This paragraph applies to all

entities that change (or eliminate) a previously existing difference between the reporting periods of a

parent and a consolidated entity or an investor and an equity method investee. This paragraph does

not apply in situations in which a parent entity or an investor changes its fiscal year-end.

If there is a difference between a parent’s fiscal year end and a subsidiary’s fiscal year end, the parent

may use the subsidiary’s financial statements for consolidation purposes, provided the difference is not

more than about three months (i.e., 93 days per Rule 3A-02(b) of Regulation S-X). When the fiscal year

ends do differ, a parent should disclose the effect of intervening events that, if recognized, would

materially affect the consolidated financial position or results of operations.

If a parent elects to change or eliminate an existing difference in fiscal periods, the parent would report

this as a change in accounting principle in accordance with the provisions of ASC 250. This guidance

does not apply, however, in situations in which a parent entity changes its fiscal year-end.

Financial reporting developments Consolidated and other financial statements 8

2 Nature and classification of the noncontrolling interest

2.1 Noncontrolling interests

Excerpt from Accounting Standards Codification Consolidation — Overall

Glossary

810-10-20

Noncontrolling Interest

The portion of equity (net assets) in a subsidiary not attributable, directly or indirectly, to a parent. A

noncontrolling interest is sometimes called a minority interest.

Other Presentation Matters

Nature and Classification of the Noncontrolling Interest in the Consolidated Statement of Financial

Position

810-10-45-15

The ownership interests in the subsidiary that are held by owners other than the parent is a

noncontrolling interest. The noncontrolling interest in a subsidiary is part of the equity of the

consolidated group.

810-10-45-16

The noncontrolling interest shall be reported in the consolidated statement of financial position within

equity, separately from the parent’s equity. That amount shall be clearly identified and labeled, for

example, as noncontrolling interest in subsidiaries (see paragraph 810-10-55-41). An entity with

noncontrolling interests in more than one subsidiary may present those interests in aggregate in the

consolidated financial statements.

810-10-45-16A

Only either of the following can be a noncontrolling interest in the consolidated financial statements:

a. A financial instrument (or an embedded feature) issued by a subsidiary that is classified as equity

in the subsidiary’s financial statements

b. A financial instrument (or an embedded feature) issued by a parent or a subsidiary for which the

payoff to the counterparty is based, in whole or in part, on the stock of a consolidated subsidiary,

that is considered indexed to the entity’s own stock in the consolidated financial statements of the

parent and that is classified as equity.

810-10-45-17

A financial instrument issued by a subsidiary that is classified as a liability in the subsidiary’s financial

statements based on the guidance in other Subtopics is not a noncontrolling interest because it is not

an ownership interest. For example, Topic 480 provides guidance for classifying certain financial

instruments issued by a subsidiary.

2 Nature and classification of the noncontrolling interest

Financial reporting developments Consolidated and other financial statements 9

810-10-45-17A

An equity-classified instrument (including an embedded feature that is separately recorded in equity

under applicable GAAP) within the scope of the guidance in paragraph 815-40-15-5C shall be

presented as a component of noncontrolling interest in the consolidated financial statements whether

the instrument was entered into by the parent or the subsidiary. However, if such an equity-classified

instrument was entered into by the parent and expires unexercised, the carrying amount of the

instrument shall be reclassified from the noncontrolling interest to the controlling interest.

Note:

This chapter introduces certain concepts related to the accounting for financial instruments that may

have embedded features. Given the complexity of the relevant authoritative literature and the

significant judgment required to apply that literature, it may be important to consult additional

guidance when accounting for these instruments and their related features.

ASC 810-10 indicates that a noncontrolling interest in an entity is any equity interest in a consolidated

entity that is not attributable to the parent. ASC 810-10 requires that the noncontrolling interest be

classified as a separate component of consolidated equity.

In ASC 810-10, the FASB concluded that a noncontrolling interest in an entity meets the definition of

equity in Concepts Statement 6, which defines equity (or net assets) as, ―the residual interest in the

assets of an entity that remains after deducting its liabilities.‖ A noncontrolling interest represents a

residual interest in the assets of a subsidiary within a consolidated group and is, therefore, consistent

with the definition of equity in Concepts Statement 6. The noncontrolling interest is presented separately

from the equity of the parent so that users of the consolidated financial statements can distinguish the

parent’s equity from the equity attributable to the noncontrolling interest (that is, equity of the

subsidiary held by owners other than the parent).

To be classified as equity in the consolidated financial statements, the instrument issued by the

subsidiary should be classified as equity by the subsidiary based on other authoritative literature. If the

instrument is classified as a liability in the subsidiary’s financial statements (e.g., under any of the

guidance in ASC 480), it cannot be presented as noncontrolling interest in the consolidated entity’s

financial statements because that instrument does not represent an ownership interest in the

consolidated entity under US GAAP.

For example, mandatorily redeemable preferred shares issued by a subsidiary would be classified as a

liability in the subsidiary’s financial statements pursuant to ASC 480. The preferred shares would not be

classified as noncontrolling interest in the consolidated financial statements.

2.2 Equity derivatives issued on the stock of a subsidiary

It is common for a parent and the noncontrolling interest holders of a subsidiary to enter into

arrangements whereby they may do one or more of the following:

• Grant the noncontrolling interest holders an option to sell their equity interests in the subsidiary to

the parent

• Grant the parent an option to acquire the equity interests in the subsidiary held by the noncontrolling

holders

• Obligate the parent to acquire and the noncontrolling holders to sell their equity interests in the

subsidiary

2 Nature and classification of the noncontrolling interest

Financial reporting developments Consolidated and other financial statements 10

Those arrangements can take the form of options (written or purchased, puts or calls), forwards (date-

certain or contingent) or even swap-like contracts. In some cases, the arrangements may be papered

between the parent and the noncontrolling interest holders, and in other cases between the subsidiary

and the noncontrolling interest holders.

The various options and forwards described above are contracts on the shares (common or preferred) of

a subsidiary. If the underlying share is classified in equity (as noncontrolling interest), the equity

derivatives2 on the noncontrolling interest should be separately evaluated to determine their

classification.

The accounting in this area can be complex because of the variety of authoritative guidance that should

be considered and the terms of the transaction. For example, (1) the equity derivative may be entered

into contemporaneously with the creation of the noncontrolling interest or subsequent to its creation, (2)

the form of the equity derivative (that is, whether it is embedded or freestanding) can be determinative

and (3) the strike price of the equity derivative may be set at either a fixed or variable (formulaic) price or

at fair value. Each of those variations can affect the accounting.

The following summarizes, at a high level, the relevant accounting considerations applicable to equity

derivatives associated with noncontrolling interest.

2.2.1 Is the equity derivative embedded in the noncontrolling interest or freestanding?

The first step in accounting for an equity derivative associated with a noncontrolling interest is to

determine whether the equity derivative is an embedded feature in the noncontrolling interest or a

freestanding financial instrument, because the accounting can be significantly different. For example, the

accounting for a freestanding written put on a subsidiary’s shares is different than that for puttable

shares issued by the subsidiary. While ASC 480 provides little interpretive guidance on the definition of a

―freestanding‖ financial instrument, we believe that the substance of a transaction should be considered

in making this determination.

The determination of whether an instrument is embedded or freestanding involves understanding both

the form and substance of the transaction, and may involve substantial judgment. In this regard,

documenting an instrument in a separate contract is not necessarily determinative that it is freestanding,

particularly when a contract is entered into in conjunction with another transaction. If the transactions

are between the same parties and involve the same underlying (in this context, the issuer’s shares), it is

important to assess whether the instruments are (1) legally detachable and (2) separately exercisable.

Those concepts can be further described as follows:

• Legally detachable — Generally, whether two instruments can be legally separated and transferred

such that the two components may be held by different parties.

• Separately exercisable — Generally, whether one instrument can be exercised without terminating

the other instrument (e.g., through redemption, simultaneous exercise, or expiration).

If the exercise of one instrument must result in the termination of the other, the instruments would

generally not be considered freestanding pursuant to ASC 480. On the other hand, if one instrument can

be exercised while the other instrument continues to be outstanding, the instruments would be

considered freestanding under ASC 480.

2 This chapter refers to ―derivatives‖ in the common use of the word, not just instruments that meet the definition of a derivative in ASC 815-10-15.

2 Nature and classification of the noncontrolling interest

Financial reporting developments Consolidated and other financial statements 11

For example, if a parent enters into a contract with the only minority shareholder of its privately held

subsidiary that permits the shareholder to put its shares in the subsidiary to the parent at a fixed price,

that put option generally would be considered to be embedded in the related shares. In contrast, if the

same parent enters into a put option on publicly traded common stock of a different subsidiary, and that

put option permits the counterparty to put any common shares of the subsidiary to the parent at a fixed

price (e.g., the counterparty could put shares of the subsidiary already owned or buy shares in the

market), that written put option would be considered freestanding, provided that it is also legally

detachable from the shares.

2.2.1.1 Equity derivatives considered embedded

If the equity derivative is considered a feature embedded in the subsidiary’s shares, that embedded

feature should be analyzed to determine whether the shares should be a mandatorily redeemable financial

instrument subject to ASC 480 or, if the shares are not a liability, whether the feature should be bifurcated.

To determine whether the embedded feature should be bifurcated, the hybrid instrument (the

subsidiary’s shares and embedded feature) should be evaluated under ASC 815-15. In many cases,

unless the subsidiary itself is a publicly traded entity, the feature will not meet the definition of a

derivative pursuant to ASC 815-10-15 because those features usually require gross physical settlement

or the transfer of the full amount of consideration payable in exchange for the full number of underlying

nonpublic subsidiary shares. As the underlying nonpublic shares are not readily convertible to cash, this

gross physical settlement does not meet any of the forms of net settlement pursuant to ASC 815-10-15-

99. However, if the instrument meets the definition of a derivative, it should be evaluated under

ASC 815-10-15-74(a) to determine if an exception from bifurcation is available.3

The exception in ASC 815-10-15-74(a) is applicable if the feature is considered indexed to the issuer’s

own stock and would be classified in equity. ASC 815-40 includes guidance that should be considered in

making this determination. There are special considerations as to whether the feature is considered

indexed to the issuer’s own stock when subsidiary shares are involved, as discussed in ASC 815-40-15-5C.

If an equity derivative is (1) deemed to be embedded and (2) the entire instrument is not a liability, the

redeemable equity guidance should be considered (see Section 2.2.3 below).

2.2.1.2 Equity derivatives considered freestanding

An equity derivative that is considered a freestanding financial instrument should be evaluated pursuant

to ASC 480 to determine whether liability classification is required as, for the purposes of ASC 480, an

issuer’s equity share includes the equity shares of any entity whose financial statements are included in

the consolidated financial statements. Instruments that may require the issuer to transfer cash or other

assets in exchange for its own shares are among those classified as liabilities pursuant to ASC 480. For

example, a physically settled forward contract that requires the parent to pay cash in exchange for the

subsidiary’s shares is within the scope of ASC 480. Further, a freestanding written put option on the

subsidiary’s shares is also a liability under ASC 480 regardless of whether it settled gross or net.

If the equity derivative is not a liability pursuant to ASC 480, the instrument should be evaluated to

determine whether it is a derivative pursuant to ASC 815. Similar to the analysis of an embedded feature

in the subsidiary’s shares, frequently, it will not meet the definition of a derivative because it lacks net

settlement. Even if the contract meets the definition of a derivative, it may still qualify for a scope

exception from derivative accounting pursuant to ASC 815-10-15-74(a), which considers the guidance in

ASC 815-40. If the equity derivative does not meet the definition of a derivative, that same guidance in

ASC 815-40 is applied to determine the contract’s classification.

3 The embedded feature would be considered a derivative if the underlying shares were publicly traded. If the feature meets the net settlement criterion by way of a required or alternative settlement in net cash or net shares, the conclusion that the feature

was embedded should be revisited.

2 Nature and classification of the noncontrolling interest

Financial reporting developments Consolidated and other financial statements 12

2.2.2 Equity derivatives deemed to be financing arrangements

In limited situations, a parent may enter into an equity derivative to acquire a subsidiary’s shares that

should be accounted for as a financing of the parent’s purchase of the minority interest. In those

situations, equity derivatives are entered into between the parent and minority interest holder at the

inception of noncontrolling interest that require physical settlement. The contracts may be either (1) a

fixed-priced forward to buy the remaining interest in the subsidiary at a stated future date and the

forward is considered freestanding or (2) combination of a purchased call option and written put option

with same (or not significantly different) fixed strike price and same fixed exercise date that are

embedded in the shares.4

Essentially, the parent consolidates 100% of the subsidiary and does not recognize the noncontrolling

interest at the consolidated entity level, but rather a liability for the financing (i.e., the future purchase of

the noncontrolling interest). In those circumstances, the risks and rewards of owning the noncontrolling

interest have been obtained by the parent during the period of the equity derivative, even though the

legal ownership of the noncontrolling interest is still retained by the noncontrolling interest holders.

Essentially, combining the equity derivative and the noncontrolling interest reflects the substance of the

transaction; that is, the noncontrolling interest holder is financing the noncontrolling interest.

ASC 480-10-55-54 states that the forward contract should be recognized as a liability, initially measured

at the present value of the fixed forward price. Subsequently, the liability is accreted to the fixed forward

price over the term of the forward contract with the resulting expense recognized as interest cost.

Similar accounting and measurement would be applied to the combined noncontrolling interest and

embedded options.

The initial measurement guidance in ASC 480-10-55-54 is not consistent with the general initial

measurement requirement of ASC 480 for physically settled forward purchase contracts. The general

measurement guidance in ASC 480-10-30-3 states that a freestanding physically settled forward

contract should be measured initially at the fair value of the underlying shares at inception, adjusted for

any consideration or unstated rights or privileges. While the methods are different, we generally believe

that they should result in approximately the same initial measurement. Any significant differences would

require additional analysis to determine if there are additional rights or privileges in the transaction.

2.2.3 Application of the redeemable equity guidance

Generally, an embedded feature, whether or not bifurcated, that permits or requires the noncontrolling

interest holder to deliver the subsidiary’s interests in exchange for cash or other assets from the controlling

entity (or the subsidiary itself) will result in the noncontrolling interest being considered redeemable equity.

Public entities should consider the SEC staff’s guidance (included in codification at ASC 480-10-S99-3A) on

redeemable equity securities when classifying redeemable noncontrolling interest. Those interests should

first follow the accounting and measurement guidance in ASC 810-10 (including allocation of earnings,

adjustments for dividends, etc.). The SEC’s guidance should then be considered, which could affect the

classification (presented in the mezzanine rather than in equity), and if so, may also adjust the

measurement of any noncontrolling interest and the related earnings per share calculations.

4 ASC 480-10-55-53 through 55-56 describe three different derivative instruments indexed to the stock of a consolidated subsidiary. One instrument includes a written put and purchased call. ASC 480-10-55-55 provides for three different ways to account for the written put and purchased call, based on how the instruments were issued relative to the noncontrolling interest

(i.e., freestanding from or embedded in the noncontrolling interest). ASC 480-10-55-59 suggests that when the written put/purchased call are freestanding, they should be combined with the noncontrolling interest and accounted for as a financing. This accounting is not one of the three ways described in ASC 480-10-55-55. We believe the guidance in ASC 480-10-55-59 is

inconsistent with the guidance formerly in EITF 00-4, ―Majority Owner's Accounting for a Transaction in the Shares of a Consolidated Subsidiary and a Derivative Indexed to the Minority Interest in That Subsidiary.‖ As the Codification was not intended to change GAAP, we believe ASC 480-10-55-55 should be followed unless ASC 815 requires the options to be combined

with the noncontrolling interest, in which case the accounting described in ASC 480-10-55-60 through 55-62 should be followed.

2 Nature and classification of the noncontrolling interest

Financial reporting developments Consolidated and other financial statements 13

In certain instances, the issuer may be required, or may have a choice, to exchange the subsidiary’s

interests by delivery of its own shares, rather than cash or other assets. In those instances, the SEC

staff’s guidance requires the issuer to consider the guidance in ASC 815-40-25-7 through 25-35 to

determine whether it can deliver the shares that could be required under the settlement of the exchange.

If the issuer does not completely control settlement by delivery of its own shares (i.e., it cannot satisfy

the settlement in shares), cash settlement would be presumed and temporary classification may be

required for the noncontrolling interest.

2.2.3.1 Measurement and reporting issues related to redeemable equity securities

Redeemable noncontrolling interest is required to be initially measured at the initial carrying amount of

the noncontrolling interest pursuant to the guidance in ASC 805-20-30. While that will generally be fair

value, the guidance in ASC 805-20-30 should be considered.

For all companies, both public and nonpublic, noncontrolling interest is first accounted for pursuant to

ASC 810. If the noncontrolling interest is considered redeemable pursuant to ASC 480-10-S99-3A, the

redeemable noncontrolling interest is presented in temporary equity. The measurement guidance is not

applied in lieu of the accounting for noncontrolling interest under ASC 810. Rather, it is an incremental

measurement that starts with the carrying amount pursuant to ASC 810 and adjusts for any increase

(but not decrease) to the carrying amount of temporary equity.

As a result, a parent should first attribute net income or loss of the subsidiary and related dividends to the

noncontrolling interest pursuant to ASC 810. After that attribution, the issuer should consider the

provisions of ASC 480-10-S99-3A to determine whether any further adjustments are necessary to

increase the carrying value of redeemable noncontrolling interest. The amount presented in temporary

equity should be the greater of the noncontrolling interest balance determined pursuant to ASC 810 or

the amount determined pursuant to ASC 480-10-S99-3A.

Pursuant to ASC 480-10-S99-3A, a security (including noncontrolling interest) that is currently

redeemable is measured at the current redemption amount. For a security that is not redeemable

currently, but will become redeemable in the future, the SEC guidance permits the following two methods

of adjusting the carrying amount of the redeemable security:

• Method 1 — Adjust the carrying amount of the redeemable security to what would be the redemption

amount assuming the security was redeemable at the balance sheet date.

• Method 2 — Accrete the carrying amount of the redeemable security to the redemption amount over

time, to the date it is probable5 it will become redeemable, using an appropriate method (e.g., the

interest method).

The SEC guidance does not specify which method is required. We generally believe issuers should

evaluate the specific facts and circumstances of the applicable redemption feature and the level of

subjectivity and assumptions necessary and apply the method that best presents the economics of the

redeemable noncontrolling interest. Once the method is selected, it should be consistently applied.

Paragraph 16e of ASC 480-10-S99-3A states that the amount in temporary equity should not be less

than the redeemable instrument’s initial amount reported in temporary equity. It further states that

reductions in the carrying amount of a temporary equity instrument are appropriate only to the extent of

increases in the redeemable instrument’s carrying amount from the application of the SEC guidance. We

generally believe only the incremental measurement pursuant to the SEC staff’s guidance is subject to

this requirement. An issuer could potentially adjust a redeemable noncontrolling interest’s balance below

its initial carrying amount when applying ASC 810.

5 The ASC master glossary defines probable as: ―the future event or events are likely to occur.‖

2 Nature and classification of the noncontrolling interest

Financial reporting developments Consolidated and other financial statements 14

2.2.4 Earnings per share considerations

As noted in ASC 480-10-S99-3A paragraph 22, adjustments to the carrying amount of redeemable

noncontrolling interest from the application of the SEC guidance do not affect net income or comprehensive

income in the consolidated financial statements. However, the adjustments may affect earnings per share

(EPS). The effect, if any, will depend on (1) whether the noncontrolling interest is represented by the

subsidiary’s common shares or preferred shares and (2) if common shares, whether the redemption amount

is at the then-current fair value or some other value (e.g., a formulaic value or fixed amount).

Refer to Section 3.2.2 of our FRD, Earnings per share, for further discussion of the EPS effects of

redeemable equity instruments (including redeemable noncontrolling interest).

2.2.5 Examples of the presentation of noncontrolling interests with equity derivatives issued on those interests

The following table summarizes the accounting for certain common equity derivatives used to acquire

interests in a subsidiary. This table assumes the equity derivatives are issued on all of the outstanding

noncontrolling interest (i.e., for the fixed number of shares not held by the parent) and are entered into by

the controlling interest.

This table should be applied only after determining (1) when the equity derivative was entered into

relative to the creation of the noncontrolling interest 6 (2) whether its price is fixed, variable or at fair

value and (3) whether the instrument is embedded or freestanding. It should be used as a starting point

in applying the literature. Parenthetical references cite the relevant literature. Application of ASC 480-

10-S99-3A is not specifically provided in the table, but references are made where the SEC staff’s

guidance would be an additional consideration.

This table, necessarily, does not contemplate all possible instruments and assumes subsidiaries represent

substantive entities as contemplated in ASC 815-40-15-5C. Careful consideration of the individual facts

and circumstances will be necessary to determine the appropriate accounting for any instrument issued

on noncontrolling interest.

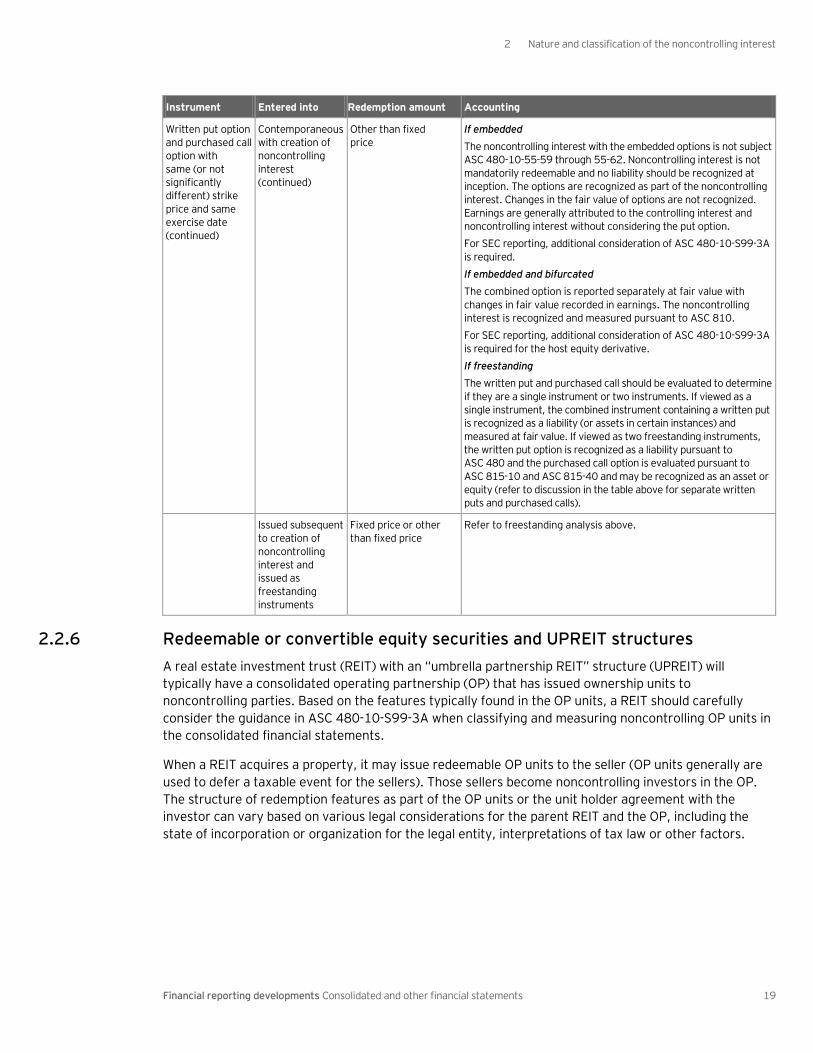

Instrument Entered into Redemption amount Accounting

Written put option permitting the

noncontrolling interest holder to put its interest to

the controlling interest

Contemporaneous with creation of

noncontrolling interest

Fixed, fair value or variable

If embedded

If the embedded written put option does not require bifurcation

pursuant to ASC 815-15, the put option is recognized as part of the noncontrolling interest. Changes in the fair value of the option over its life are not recognized. Earnings are generally attributed

to the controlling interest and noncontrolling interests without considering the put option.

If the embedded put option is exercised, the noncontrolling

interest is reduced and APIC is adjusted for any difference between the noncontrolling interest’s carrying value and the consideration paid.7

For SEC reporting, additional consideration of ASC 480-10-S99-3A is required for the noncontrolling interest.

6 This table assumes that equity derivatives issued subsequent to the creation of the noncontrolling interest are freestanding.

Depending on individual facts and circumstances, certain equity derivatives issued subsequent to the creation of the noncontrolling interest could be considered embedded. If the instrument is considered to be embedded, the guidance on equity derivatives embedded in the noncontrolling interest should be applied, and the guidance in ASC 480-10-S99-3A should be considered.

7 ASC 810-10 requires transactions between the controlling interest and noncontrolling interest that do not result in consolidation

or deconsolidation to be recognized in equity.

2 Nature and classification of the noncontrolling interest

Financial reporting developments Consolidated and other financial statements 15

Instrument Entered into Redemption amount Accounting

If freestanding

ASC 480 requires it to be classified as a liability and measured at fair value with the changes in value recognized in earnings.

The exercise of the option results in the acquisition of noncontrolling interest and any difference between the cash paid and the combined value of the freestanding instrument and

noncontrolling interest’s carrying value would be recorded to APIC.

If embedded and bifurcated

The written put option is bifurcated and reported separately at

fair value with changes in fair value recorded in earnings. The noncontrolling interest is recognized and measured pursuant to ASC 810.

For SEC reporting, additional consideration of ASC 480-10-S99-3A is required for the host equity derivative.

Subsequent to creation of noncontrolling

interest

Fixed, fair value or variable

The written put option is recognized as a liability that is initially and subsequently measured at fair value pursuant to ASC 480. The noncontrolling interest is recognized and measured in

accordance with ASC 810.

Purchased call option permitting

the controlling interest to acquire the noncontrolling

interest

Contemporaneous with creation of

noncontrolling interest

Fixed, fair value or variable

If embedded

If the embedded purchased call option does not require bifurcation

pursuant to ASC 815-15, the call option is recognized as part of the noncontrolling interest. Changes in the fair value of the option over its life are not recognized. Earnings are generally attributed

to the controlling interest and noncontrolling interests without considering the call option.

If the embedded call option is exercised, the noncontrolling

interest is reduced and APIC is adjusted for any difference between the noncontrolling interest’s carrying value and the consideration paid.

If (1) freestanding and in the scope of ASC 815-10 or (2) bifurcated

The purchased call option is reported separately and measured at

fair value with changes in value recognized in earnings. The noncontrolling interest is recognized and measured pursuant to ASC 810.

If freestanding and not in the scope of ASC 815-10

Follow ASC 815-40 to determine the appropriate classification and subsequent measurement of the instruments as an asset or equity.

(ASC 815-40-25-1 through 25-43)

The noncontrolling interest continues to be recognized pursuant to ASC 810.

For a freestanding call option classified as equity pursuant to ASC 815-40, if the call option is not exercised and were entered into by the parent, the carrying amount of the instrument should

be reclassified from the noncontrolling interest to the controlling interest. If it is not exercised and were entered into by the subsidiary, there is no reclassification to be made.

The 1986 AICPA Options Paper provides potential measurement alternatives to be evaluated if it were determined that neither ASC 815-10 nor ASC 815-40 applied.

2 Nature and classification of the noncontrolling interest

Financial reporting developments Consolidated and other financial statements 16

Instrument Entered into Redemption amount Accounting

Subsequent to creation of noncontrolling

interest

Fixed, fair value or variable

If freestanding and in the scope of ASC 815-10

The freestanding purchased call option is reported separately and measured at fair value with changes in value recognized in

earnings. The noncontrolling interest is recognized and measured pursuant to ASC 810.

If freestanding and not in the scope of ASC 815-10

Follow ASC 815-40 to determine the appropriate classification and subsequent measurement of the instruments as an asset or equity. (ASC 815-40-25-1 through 25-43 )

The noncontrolling interest continues to be recognized pursuant to ASC 810.

For a freestanding call option classified as equity pursuant to

ASC 815-40, if the call option is not exercised and were entered into by the parent, the carrying amount of the instrument should be reclassified from the noncontrolling interest to the controlling

interest. If it is not exercised and were entered into by the subsidiary, there is no reclassification to be made.

The 1986 AICPA Options Paper provides potential measurement

alternatives to be evaluated if it were determined that neither ASC 815-10 nor ASC 815-40 applied.

Forward contract to acquire the noncontrolling

interest

Contemporaneous with creation of noncontrolling

interest

Payment amount and settlement date are fixed

If embedded

The noncontrolling interest would be a mandatorily redeemable financial instrument classified as a liability pursuant to ASC 480-10-

30-1 and measured initially at fair value.8 Noncontrolling interest is not recognized and no earnings are allocated to the noncontrolling interest. The parent accounts for this transaction as a financing and

recognizes 100% of the subsidiary’s assets and liabilities.

If freestanding

The forward contract is classified as a liability and initially measured

at an appropriate value.9 The liability is accreted to the settlement amount over the term of the forward contract with the resulting expense recognized as interest cost. Noncontrolling interest is not

recognized and no earnings are allocated to the noncontrolling interest.. The parent accounts for this transaction as a financing and recognizes 100% of the subsidiary’s assets and liabilities.

(ASC 480-10-30-3 and ASC 480-10-55-53 through 55-54)

When the forward contract is settled, the liability is derecognized.

8 Subsequently, whether the measurement requirements of ASC 480-10 or ASC 480-10-S99 would be required depends on the application of the transition guidance in ASC 480-10-65-1(b). If the measurement guidance under ASC480-10 is applicable, the liability is measured at the present value of the amount to be paid at settlement, accruing interest cost using the rate implicit at

inception based on the initial measurement. 9 When addressing the initial measurement of a forward contract on shares of a subsidiary, there are three conflicting

measurement models. A freestanding forward contract under ASC 480-10-30-3 is initially measured at the fair value of the shares to be repurchased, adjusted for any consideration or unstated rights or privileges. A freestanding forward contract under

ASC 480-10-55-54 is initially measured at the present value of the contract amount, which we believe should be discounted using a market-based rate reflecting the issuer’s own credit risk. A mandatorily redeemable noncontrolling interest is measured at fair value under ASC 480-10-30-1. We generally believe that these methods should result in approximately the same initial

measurement. Any significant differences would require additional analysis to determine if there were additional rights or privileges granted in the transaction.

2 Nature and classification of the noncontrolling interest

Financial reporting developments Consolidated and other financial statements 17

Instrument Entered into Redemption amount Accounting

Contemporaneous with creation of noncontrolling

interest

Payment amount or settlement date vary based on certain

conditions

If embedded

The resulting mandatorily redeemable financial instrument is a liability pursuant to ASC 480 and measured initially at fair value.10

Noncontrolling interest is not recognized and no earnings are allocated to the noncontrolling interest. The parent accounts for this transaction as a financing and recognizes 100% of the

subsidiary’s assets and liabilities.

If freestanding

The forward contract is not subject to ASC 480-10-55-54 as the

settlement price is not fixed. Pursuant to other sections of ASC 480, a liability should be recognized at the fair value of the shares at inception, adjusted for any consideration or unstated

rights or privileges. The liability is subsequently measured at the amount that would be paid on the reporting date with any change in value from the previous reporting date recognized as interest

cost. Noncontrolling interest is not recognized and no earnings are allocated to the noncontrolling interest. The parent accounts for this transaction as a financing and recognizes 100% of the

subsidiary’s assets and liabilities.

Forward contract

to acquire the noncontrolling interest

(continued)

Subsequent to

creation of noncontrolling interest

Payment amount and

settlement date are fixed

Pursuant to ASC 480, the freestanding forward contract is

recognized as a liability at the date on which the forward contract was entered into. The liability is initially measured at the fair value of the shares at inception adjusted for any consideration or

unstated rights or privileges. Subsequent measurement is at the present value of the amount to be paid at settlement, accruing interest cost using the rate implicit at inception based on the initial

measurement. The previously recognized noncontrolling interest is derecognized and any difference between the amount of the liability and the noncontrolling interest’s carrying amount is

recognized in APIC. No further attribution of earnings is necessary because there is no noncontrolling interest.

Either payment

amount or settlement date varies based on certain conditions

Same as the accounting if the settlement date is fixed except that

the liability is subsequently measured at the amount that would be paid on the reporting date with any change in value from the previous reporting date recognized as interest cost. No further

attribution of earnings is necessary because there is no noncontrolling interest.