corp e&p m&a

TRANSCRIPT

Crude Oil Production, North America (BI OILSN)

The BLOOMBERG PROFESSIONAL service, BLOOMBERG Data and Bloomberg Intelligence (the "Services") are owned and distributed by Bloomberg Finance L.P. ("BFLP") in all jurisdictions other than Argentina, Bermuda, China, India, Japan and Korea (the "BLP Countries"). BFLP is a wholly ownedsubsidiary of Bloomberg L.P. ("BLP"). BLP provides BFLP with global marketing and operational support and service for the Services and distributes the Services either directly or through a non-BFLP subsidiary in the BLP Countries. Certain functionalities distributed via the Services are available only tosophisticated institutional investors and only where the necessary legal clearance has been obtained. BFLP, BLP and their affiliates do not guarantee the accuracy of prices or information in the Services. Nothing in the Services shall constitute or be construed as an offering of financial instruments by BFLP,BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of an investment strategy or whether or not to "buy", "sell" or "hold" an investment. Information available via the Services should not be considered as information sufficient upon which to base an investmentdecision. BLOOMBERG, BLOOMBERG PROFESSIONAL, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG ANYWHERE, BLOOMBERG TRADEBOOK, BLOOMBERG TELEVISION, BLOOMBERG RADIO, BLOOMBERG PRESS and BLOOMBERG.COM are trademarks and service marksof BFLP, a Delaware limited partnership, or its subsidiaries. © 2015 Bloomberg Finance L.P. All rights reserved. This document and its contents may not be forwarded or redistributed without the prior consent of Bloomberg.

Overview > Why The Corporate E&P M&A Fuss? It Doesn't Work Well >> Exhibit 1 of 13

E&P Corporate M&A Focus Ignores Key Fact: It May Not Add ValueAnalysts: Vincent G Piazza & Gurpal DosanjhMar 24, 2015The drop in benchmark crudeoil prices is raising expectationsof an increase in corporate M&Aamong exploration and productioncompanies. Yet E&P asset dealshave been more frequent, with fewcorporate transactions occurringin past commodity cycles. Thecorporate E&P acquisitions thathave occurred likely haven't yieldedthe expected benefits. Energyservices and equipment deals,and divestitures in other energysegments, may have producedbetter value for the investors andcompanies involved.

Key Points (5 of 13):* Corporate E&P Deals May Not Fulfill All Traditional M&A Goals* Hunt for Technology, Expertise Irrelevant in Corporate E&PDeals* Stock-Market Fallout of E&P Corporate Deals May Restrain M&A* Spinoffs, Asset Sales May Make More Sense Than CorporateE&P M&A* Energy Services M&A May Be More Likely Than E&P Deals in2015

Crude Oil Production TeamBloomberg Intelligence

Crude Oil Production, North America (BI OILSN)

The BLOOMBERG PROFESSIONAL service, BLOOMBERG Data and Bloomberg Intelligence (the "Services") are owned and distributed by Bloomberg Finance L.P. ("BFLP") in all jurisdictions other than Argentina, Bermuda, China, India, Japan and Korea (the "BLP Countries"). BFLP is a wholly ownedsubsidiary of Bloomberg L.P. ("BLP"). BLP provides BFLP with global marketing and operational support and service for the Services and distributes the Services either directly or through a non-BFLP subsidiary in the BLP Countries. Certain functionalities distributed via the Services are available only tosophisticated institutional investors and only where the necessary legal clearance has been obtained. BFLP, BLP and their affiliates do not guarantee the accuracy of prices or information in the Services. Nothing in the Services shall constitute or be construed as an offering of financial instruments by BFLP,BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of an investment strategy or whether or not to "buy", "sell" or "hold" an investment. Information available via the Services should not be considered as information sufficient upon which to base an investmentdecision. BLOOMBERG, BLOOMBERG PROFESSIONAL, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG ANYWHERE, BLOOMBERG TRADEBOOK, BLOOMBERG TELEVISION, BLOOMBERG RADIO, BLOOMBERG PRESS and BLOOMBERG.COM are trademarks and service marksof BFLP, a Delaware limited partnership, or its subsidiaries. © 2015 Bloomberg Finance L.P. All rights reserved. This document and its contents may not be forwarded or redistributed without the prior consent of Bloomberg.

Overview > Why The Corporate E&P M&A Fuss? It Doesn't Work Well >> Exhibit 2 of 13

Corporate E&P Deals May Not Fulfill All Traditional M&A GoalsAnalysts: Vincent G Piazza & Gurpal DosanjhMar 24, 2015M&A's goals usually includeacquiring a unique technologyor process, consolidating marketshare, growing geographically oradding capacity or product lines.Execution is aimed at raising equitymultiples by enhancing marginsand returns. Yet traditional M&Adrivers may not pertain to corporateE&P deals and history suggests thatunderlying core assets are the focusof acquisitions. Asset transactionsand joint ventures had become moreprevalent as acquirers gained directexposure to the underlying asset.

Crude Oil Production TeamBloomberg Intelligence

Crude Oil Production, North America (BI OILSN)

The BLOOMBERG PROFESSIONAL service, BLOOMBERG Data and Bloomberg Intelligence (the "Services") are owned and distributed by Bloomberg Finance L.P. ("BFLP") in all jurisdictions other than Argentina, Bermuda, China, India, Japan and Korea (the "BLP Countries"). BFLP is a wholly ownedsubsidiary of Bloomberg L.P. ("BLP"). BLP provides BFLP with global marketing and operational support and service for the Services and distributes the Services either directly or through a non-BFLP subsidiary in the BLP Countries. Certain functionalities distributed via the Services are available only tosophisticated institutional investors and only where the necessary legal clearance has been obtained. BFLP, BLP and their affiliates do not guarantee the accuracy of prices or information in the Services. Nothing in the Services shall constitute or be construed as an offering of financial instruments by BFLP,BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of an investment strategy or whether or not to "buy", "sell" or "hold" an investment. Information available via the Services should not be considered as information sufficient upon which to base an investmentdecision. BLOOMBERG, BLOOMBERG PROFESSIONAL, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG ANYWHERE, BLOOMBERG TRADEBOOK, BLOOMBERG TELEVISION, BLOOMBERG RADIO, BLOOMBERG PRESS and BLOOMBERG.COM are trademarks and service marksof BFLP, a Delaware limited partnership, or its subsidiaries. © 2015 Bloomberg Finance L.P. All rights reserved. This document and its contents may not be forwarded or redistributed without the prior consent of Bloomberg.

Overview > Why The Corporate E&P M&A Fuss? It Doesn't Work Well >> Exhibit 3 of 13

Hunt for Technology, Expertise Irrelevant in Corporate E&P DealsAnalysts: Vincent G Piazza & Gurpal DosanjhMar 24, 2015Corporate E&P acquisitions aren'tdriven by the hunt for technologyor human expertise. Technologybecomes ubiquitous in the oil patchas rapid adoption by producersquickly dilutes the short-termbenefits of initial deployment.Unconventional drilling techniquesand completion designs quicklybecome universal across plays.Speed is the differentiator. As theindustry moves from explorationto resource exploitation throughpervasive technological evolution,acquiring human expertise is not themain driver of M&A.

Crude Oil Production Team For interactive exhibit on Bloomberg, run:Bloomberg Intelligence MA T:5998489902745387120<GO>

Crude Oil Production, North America (BI OILSN)

The BLOOMBERG PROFESSIONAL service, BLOOMBERG Data and Bloomberg Intelligence (the "Services") are owned and distributed by Bloomberg Finance L.P. ("BFLP") in all jurisdictions other than Argentina, Bermuda, China, India, Japan and Korea (the "BLP Countries"). BFLP is a wholly ownedsubsidiary of Bloomberg L.P. ("BLP"). BLP provides BFLP with global marketing and operational support and service for the Services and distributes the Services either directly or through a non-BFLP subsidiary in the BLP Countries. Certain functionalities distributed via the Services are available only tosophisticated institutional investors and only where the necessary legal clearance has been obtained. BFLP, BLP and their affiliates do not guarantee the accuracy of prices or information in the Services. Nothing in the Services shall constitute or be construed as an offering of financial instruments by BFLP,BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of an investment strategy or whether or not to "buy", "sell" or "hold" an investment. Information available via the Services should not be considered as information sufficient upon which to base an investmentdecision. BLOOMBERG, BLOOMBERG PROFESSIONAL, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG ANYWHERE, BLOOMBERG TRADEBOOK, BLOOMBERG TELEVISION, BLOOMBERG RADIO, BLOOMBERG PRESS and BLOOMBERG.COM are trademarks and service marksof BFLP, a Delaware limited partnership, or its subsidiaries. © 2015 Bloomberg Finance L.P. All rights reserved. This document and its contents may not be forwarded or redistributed without the prior consent of Bloomberg.

Overview > Why The Corporate E&P M&A Fuss? It Doesn't Work Well >> Exhibit 4 of 13

Stock-Market Fallout of E&P Corporate Deals May Restrain M&AAnalysts: Vincent G Piazza & Gurpal DosanjhMar 24, 2015M&A among publicly traded E&Psmay be more restrained thanexpected because of the poorstock performance that followedprevious corporate transactions.In particular, market reaction toExxon Mobil's $41.4 billion 2009purchase of XTO Energy mayhave discouraged other would-beacquirers. Large foreign majorshave written down their interests inU.S. onshore unconventional jointventures, potentially deterring deals.While smaller corporate M&A mayhave provided geographic footholds,growth has been disorderly.

Crude Oil Production Team For interactive exhibit on Bloomberg, run:Bloomberg Intelligence G BI3 334<GO>

Crude Oil Production, North America (BI OILSN)

The BLOOMBERG PROFESSIONAL service, BLOOMBERG Data and Bloomberg Intelligence (the "Services") are owned and distributed by Bloomberg Finance L.P. ("BFLP") in all jurisdictions other than Argentina, Bermuda, China, India, Japan and Korea (the "BLP Countries"). BFLP is a wholly ownedsubsidiary of Bloomberg L.P. ("BLP"). BLP provides BFLP with global marketing and operational support and service for the Services and distributes the Services either directly or through a non-BFLP subsidiary in the BLP Countries. Certain functionalities distributed via the Services are available only tosophisticated institutional investors and only where the necessary legal clearance has been obtained. BFLP, BLP and their affiliates do not guarantee the accuracy of prices or information in the Services. Nothing in the Services shall constitute or be construed as an offering of financial instruments by BFLP,BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of an investment strategy or whether or not to "buy", "sell" or "hold" an investment. Information available via the Services should not be considered as information sufficient upon which to base an investmentdecision. BLOOMBERG, BLOOMBERG PROFESSIONAL, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG ANYWHERE, BLOOMBERG TRADEBOOK, BLOOMBERG TELEVISION, BLOOMBERG RADIO, BLOOMBERG PRESS and BLOOMBERG.COM are trademarks and service marksof BFLP, a Delaware limited partnership, or its subsidiaries. © 2015 Bloomberg Finance L.P. All rights reserved. This document and its contents may not be forwarded or redistributed without the prior consent of Bloomberg.

Overview > Why The Corporate E&P M&A Fuss? It Doesn't Work Well >> Exhibit 5 of 13

Spinoffs, Asset Sales May Make More Sense Than Corporate E&P M&AAnalysts: Vincent G Piazza & Gurpal DosanjhMar 24, 2015Reducing complexity throughdivesting assets may prove tobe a better strategy for energycompanies compared with corporateM&A. Equities of independentsand companies that havestreamlined through divestitureshave outperformed integratedcompanies, which combine E&P andrefining businesses. IndependentE&Ps may provide the desiredconcentrated geographic andcommodity exposures, rather thanholding shares of more diversifiedintegrated peers.

Crude Oil Production Team For interactive exhibit on Bloomberg, run:Bloomberg Intelligence G BI2 6075<GO>

Crude Oil Production, North America (BI OILSN)

The BLOOMBERG PROFESSIONAL service, BLOOMBERG Data and Bloomberg Intelligence (the "Services") are owned and distributed by Bloomberg Finance L.P. ("BFLP") in all jurisdictions other than Argentina, Bermuda, China, India, Japan and Korea (the "BLP Countries"). BFLP is a wholly ownedsubsidiary of Bloomberg L.P. ("BLP"). BLP provides BFLP with global marketing and operational support and service for the Services and distributes the Services either directly or through a non-BFLP subsidiary in the BLP Countries. Certain functionalities distributed via the Services are available only tosophisticated institutional investors and only where the necessary legal clearance has been obtained. BFLP, BLP and their affiliates do not guarantee the accuracy of prices or information in the Services. Nothing in the Services shall constitute or be construed as an offering of financial instruments by BFLP,BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of an investment strategy or whether or not to "buy", "sell" or "hold" an investment. Information available via the Services should not be considered as information sufficient upon which to base an investmentdecision. BLOOMBERG, BLOOMBERG PROFESSIONAL, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG ANYWHERE, BLOOMBERG TRADEBOOK, BLOOMBERG TELEVISION, BLOOMBERG RADIO, BLOOMBERG PRESS and BLOOMBERG.COM are trademarks and service marksof BFLP, a Delaware limited partnership, or its subsidiaries. © 2015 Bloomberg Finance L.P. All rights reserved. This document and its contents may not be forwarded or redistributed without the prior consent of Bloomberg.

Overview > Why The Corporate E&P M&A Fuss? It Doesn't Work Well >> Exhibit 6 of 13

Energy Services M&A May Be More Likely Than E&P Deals in 2015Analysts: Vincent G Piazza & Andrew CosgroveMar 24, 2015Energy M&A in 2015 may befocused on oil services andequipment companies, in contrastto investor expectations that oiland gas E&P transactions willbe more prevalent. There were247 oil services deals worth $32billion completed from early 2009 tomid-2010, the year and a half thatfollowed oil's last decline. During thesame period, 51 E&P deals, totaling$6.6 billion, were consummated.Servicers with available capital mayopportunistically seek market-sharegains from weaker competitors amidthe decline.

Crude Oil Production TeamBloomberg Intelligence

Crude Oil Production, North America (BI OILSN)

The BLOOMBERG PROFESSIONAL service, BLOOMBERG Data and Bloomberg Intelligence (the "Services") are owned and distributed by Bloomberg Finance L.P. ("BFLP") in all jurisdictions other than Argentina, Bermuda, China, India, Japan and Korea (the "BLP Countries"). BFLP is a wholly ownedsubsidiary of Bloomberg L.P. ("BLP"). BLP provides BFLP with global marketing and operational support and service for the Services and distributes the Services either directly or through a non-BFLP subsidiary in the BLP Countries. Certain functionalities distributed via the Services are available only tosophisticated institutional investors and only where the necessary legal clearance has been obtained. BFLP, BLP and their affiliates do not guarantee the accuracy of prices or information in the Services. Nothing in the Services shall constitute or be construed as an offering of financial instruments by BFLP,BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of an investment strategy or whether or not to "buy", "sell" or "hold" an investment. Information available via the Services should not be considered as information sufficient upon which to base an investmentdecision. BLOOMBERG, BLOOMBERG PROFESSIONAL, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG ANYWHERE, BLOOMBERG TRADEBOOK, BLOOMBERG TELEVISION, BLOOMBERG RADIO, BLOOMBERG PRESS and BLOOMBERG.COM are trademarks and service marksof BFLP, a Delaware limited partnership, or its subsidiaries. © 2015 Bloomberg Finance L.P. All rights reserved. This document and its contents may not be forwarded or redistributed without the prior consent of Bloomberg.

Overview > Why The Corporate E&P M&A Fuss? It Doesn't Work Well >> Exhibit 7 of 13

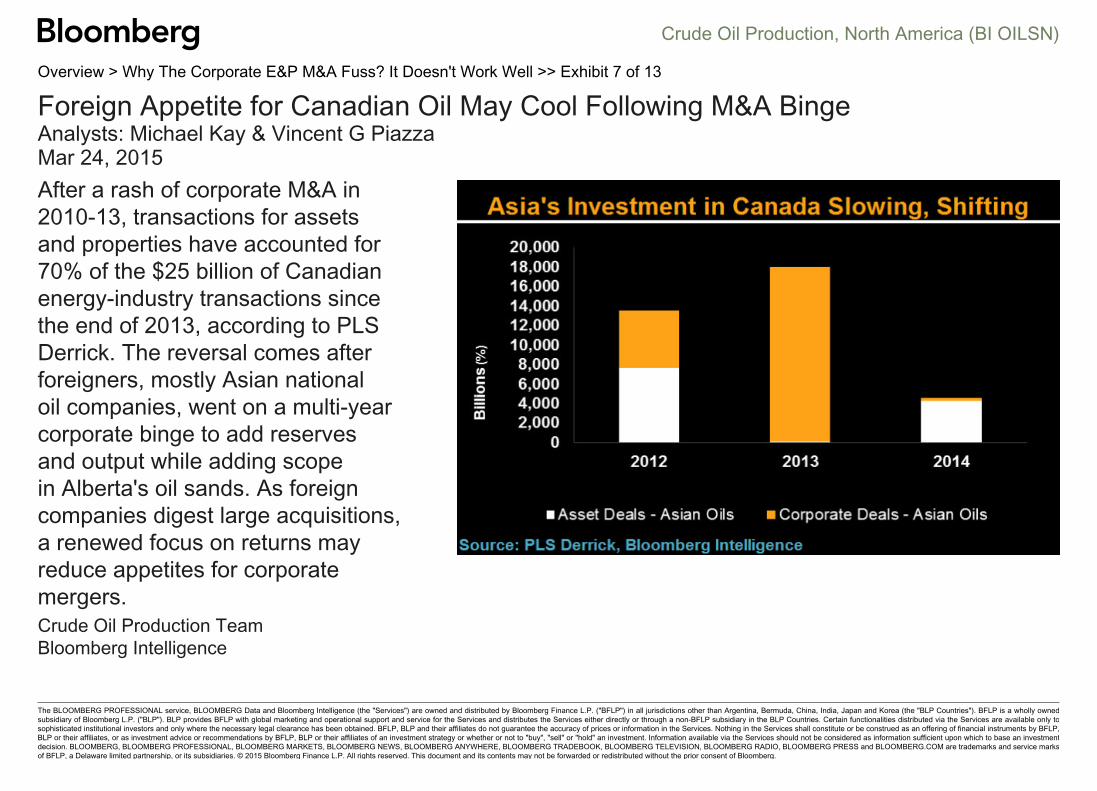

Foreign Appetite for Canadian Oil May Cool Following M&A BingeAnalysts: Michael Kay & Vincent G PiazzaMar 24, 2015After a rash of corporate M&A in2010-13, transactions for assetsand properties have accounted for70% of the $25 billion of Canadianenergy-industry transactions sincethe end of 2013, according to PLSDerrick. The reversal comes afterforeigners, mostly Asian nationaloil companies, went on a multi-yearcorporate binge to add reservesand output while adding scopein Alberta's oil sands. As foreigncompanies digest large acquisitions,a renewed focus on returns mayreduce appetites for corporatemergers.

Crude Oil Production TeamBloomberg Intelligence

Crude Oil Production, North America (BI OILSN)

The BLOOMBERG PROFESSIONAL service, BLOOMBERG Data and Bloomberg Intelligence (the "Services") are owned and distributed by Bloomberg Finance L.P. ("BFLP") in all jurisdictions other than Argentina, Bermuda, China, India, Japan and Korea (the "BLP Countries"). BFLP is a wholly ownedsubsidiary of Bloomberg L.P. ("BLP"). BLP provides BFLP with global marketing and operational support and service for the Services and distributes the Services either directly or through a non-BFLP subsidiary in the BLP Countries. Certain functionalities distributed via the Services are available only tosophisticated institutional investors and only where the necessary legal clearance has been obtained. BFLP, BLP and their affiliates do not guarantee the accuracy of prices or information in the Services. Nothing in the Services shall constitute or be construed as an offering of financial instruments by BFLP,BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of an investment strategy or whether or not to "buy", "sell" or "hold" an investment. Information available via the Services should not be considered as information sufficient upon which to base an investmentdecision. BLOOMBERG, BLOOMBERG PROFESSIONAL, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG ANYWHERE, BLOOMBERG TRADEBOOK, BLOOMBERG TELEVISION, BLOOMBERG RADIO, BLOOMBERG PRESS and BLOOMBERG.COM are trademarks and service marksof BFLP, a Delaware limited partnership, or its subsidiaries. © 2015 Bloomberg Finance L.P. All rights reserved. This document and its contents may not be forwarded or redistributed without the prior consent of Bloomberg.

Overview > Why The Corporate E&P M&A Fuss? It Doesn't Work Well >> Exhibit 8 of 13

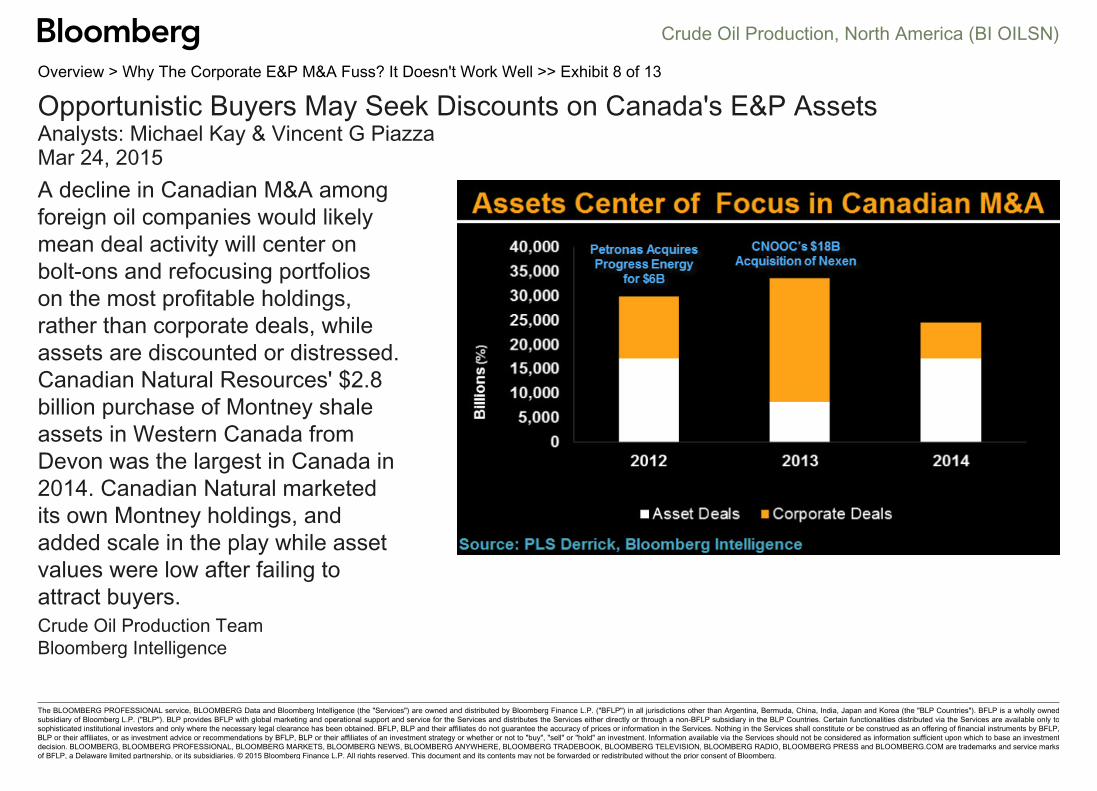

Opportunistic Buyers May Seek Discounts on Canada's E&P AssetsAnalysts: Michael Kay & Vincent G PiazzaMar 24, 2015A decline in Canadian M&A amongforeign oil companies would likelymean deal activity will center onbolt-ons and refocusing portfolioson the most profitable holdings,rather than corporate deals, whileassets are discounted or distressed.Canadian Natural Resources' $2.8billion purchase of Montney shaleassets in Western Canada fromDevon was the largest in Canada in2014. Canadian Natural marketedits own Montney holdings, andadded scale in the play while assetvalues were low after failing toattract buyers.

Crude Oil Production TeamBloomberg Intelligence

Crude Oil Production, North America (BI OILSN)

The BLOOMBERG PROFESSIONAL service, BLOOMBERG Data and Bloomberg Intelligence (the "Services") are owned and distributed by Bloomberg Finance L.P. ("BFLP") in all jurisdictions other than Argentina, Bermuda, China, India, Japan and Korea (the "BLP Countries"). BFLP is a wholly ownedsubsidiary of Bloomberg L.P. ("BLP"). BLP provides BFLP with global marketing and operational support and service for the Services and distributes the Services either directly or through a non-BFLP subsidiary in the BLP Countries. Certain functionalities distributed via the Services are available only tosophisticated institutional investors and only where the necessary legal clearance has been obtained. BFLP, BLP and their affiliates do not guarantee the accuracy of prices or information in the Services. Nothing in the Services shall constitute or be construed as an offering of financial instruments by BFLP,BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of an investment strategy or whether or not to "buy", "sell" or "hold" an investment. Information available via the Services should not be considered as information sufficient upon which to base an investmentdecision. BLOOMBERG, BLOOMBERG PROFESSIONAL, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG ANYWHERE, BLOOMBERG TRADEBOOK, BLOOMBERG TELEVISION, BLOOMBERG RADIO, BLOOMBERG PRESS and BLOOMBERG.COM are trademarks and service marksof BFLP, a Delaware limited partnership, or its subsidiaries. © 2015 Bloomberg Finance L.P. All rights reserved. This document and its contents may not be forwarded or redistributed without the prior consent of Bloomberg.

Overview > Why The Corporate E&P M&A Fuss? It Doesn't Work Well >> Exhibit 9 of 13

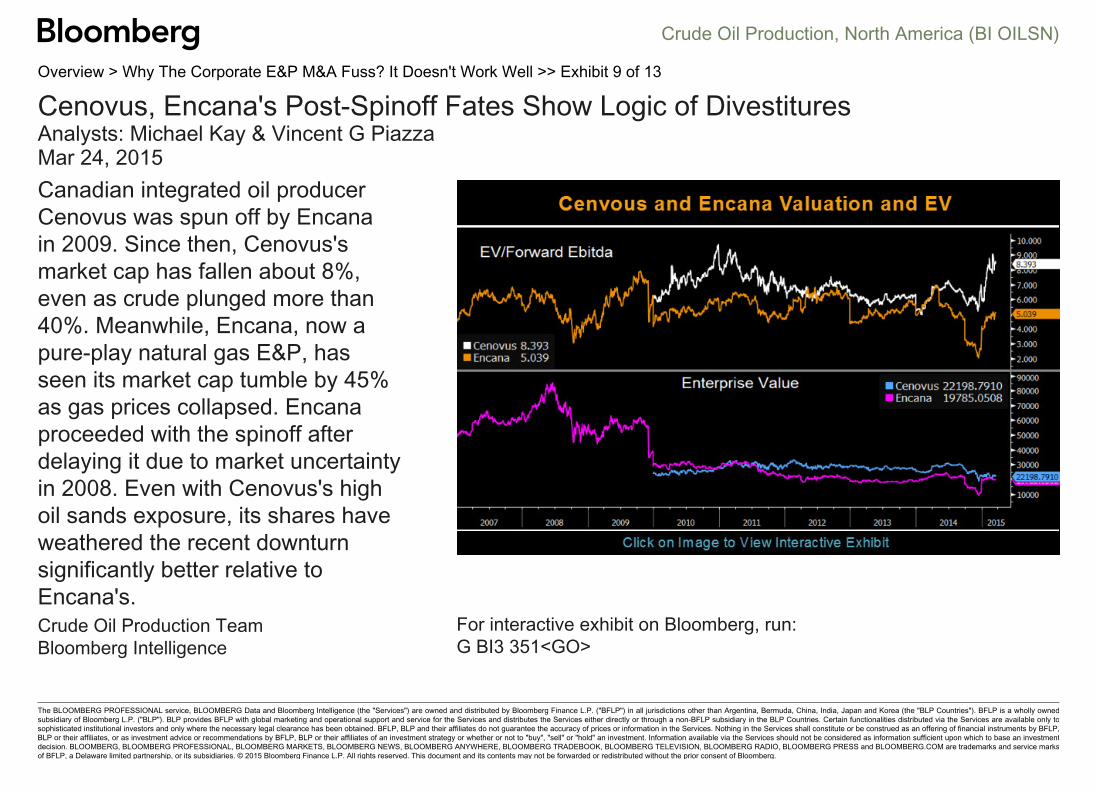

Cenovus, Encana's Post-Spinoff Fates Show Logic of DivestituresAnalysts: Michael Kay & Vincent G PiazzaMar 24, 2015Canadian integrated oil producerCenovus was spun off by Encanain 2009. Since then, Cenovus'smarket cap has fallen about 8%,even as crude plunged more than40%. Meanwhile, Encana, now apure-play natural gas E&P, hasseen its market cap tumble by 45%as gas prices collapsed. Encanaproceeded with the spinoff afterdelaying it due to market uncertaintyin 2008. Even with Cenovus's highoil sands exposure, its shares haveweathered the recent downturnsignificantly better relative toEncana's.

Crude Oil Production Team For interactive exhibit on Bloomberg, run:Bloomberg Intelligence G BI3 351<GO>

Crude Oil Production, North America (BI OILSN)

The BLOOMBERG PROFESSIONAL service, BLOOMBERG Data and Bloomberg Intelligence (the "Services") are owned and distributed by Bloomberg Finance L.P. ("BFLP") in all jurisdictions other than Argentina, Bermuda, China, India, Japan and Korea (the "BLP Countries"). BFLP is a wholly ownedsubsidiary of Bloomberg L.P. ("BLP"). BLP provides BFLP with global marketing and operational support and service for the Services and distributes the Services either directly or through a non-BFLP subsidiary in the BLP Countries. Certain functionalities distributed via the Services are available only tosophisticated institutional investors and only where the necessary legal clearance has been obtained. BFLP, BLP and their affiliates do not guarantee the accuracy of prices or information in the Services. Nothing in the Services shall constitute or be construed as an offering of financial instruments by BFLP,BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of an investment strategy or whether or not to "buy", "sell" or "hold" an investment. Information available via the Services should not be considered as information sufficient upon which to base an investmentdecision. BLOOMBERG, BLOOMBERG PROFESSIONAL, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG ANYWHERE, BLOOMBERG TRADEBOOK, BLOOMBERG TELEVISION, BLOOMBERG RADIO, BLOOMBERG PRESS and BLOOMBERG.COM are trademarks and service marksof BFLP, a Delaware limited partnership, or its subsidiaries. © 2015 Bloomberg Finance L.P. All rights reserved. This document and its contents may not be forwarded or redistributed without the prior consent of Bloomberg.

Overview > Why The Corporate E&P M&A Fuss? It Doesn't Work Well >> Exhibit 10 of 13

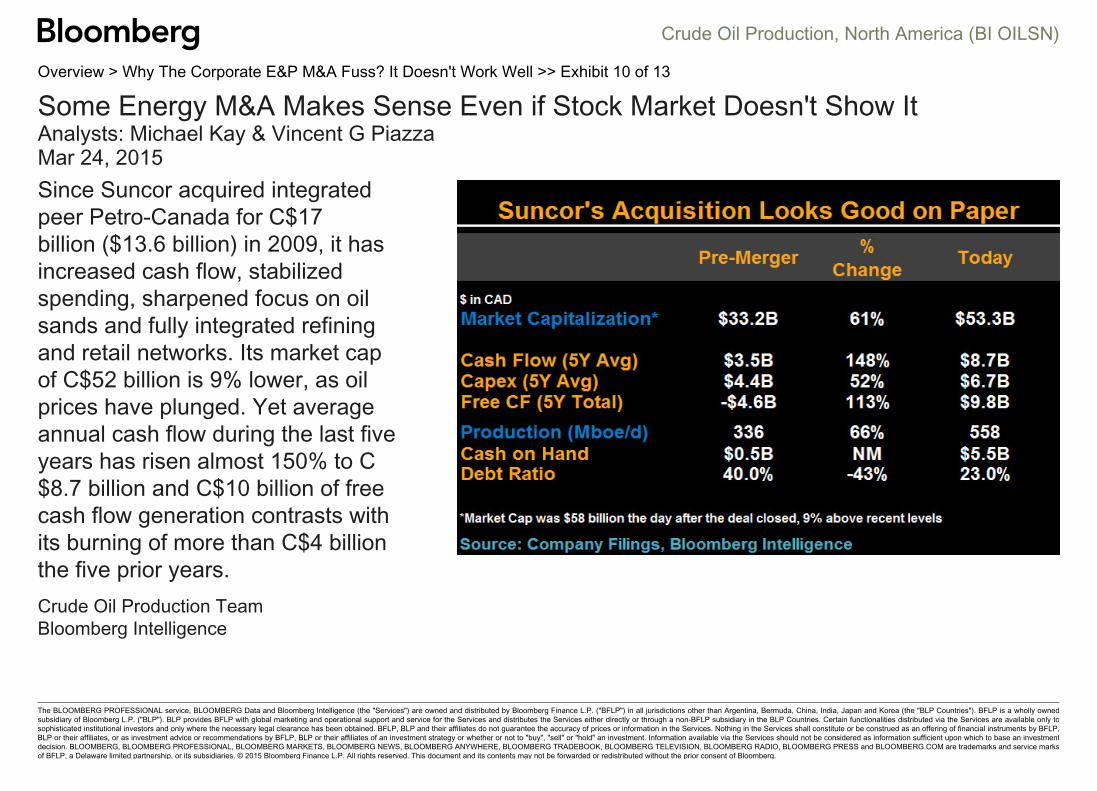

Some Energy M&A Makes Sense Even if Stock Market Doesn't Show ItAnalysts: Michael Kay & Vincent G PiazzaMar 24, 2015Since Suncor acquired integratedpeer Petro-Canada for C$17billion ($13.6 billion) in 2009, it hasincreased cash flow, stabilizedspending, sharpened focus on oilsands and fully integrated refiningand retail networks. Its market capof C$52 billion is 9% lower, as oilprices have plunged. Yet averageannual cash flow during the last fiveyears has risen almost 150% to C$8.7 billion and C$10 billion of freecash flow generation contrasts withits burning of more than C$4 billionthe five prior years.

Crude Oil Production TeamBloomberg Intelligence

Crude Oil Production, North America (BI OILSN)

The BLOOMBERG PROFESSIONAL service, BLOOMBERG Data and Bloomberg Intelligence (the "Services") are owned and distributed by Bloomberg Finance L.P. ("BFLP") in all jurisdictions other than Argentina, Bermuda, China, India, Japan and Korea (the "BLP Countries"). BFLP is a wholly ownedsubsidiary of Bloomberg L.P. ("BLP"). BLP provides BFLP with global marketing and operational support and service for the Services and distributes the Services either directly or through a non-BFLP subsidiary in the BLP Countries. Certain functionalities distributed via the Services are available only tosophisticated institutional investors and only where the necessary legal clearance has been obtained. BFLP, BLP and their affiliates do not guarantee the accuracy of prices or information in the Services. Nothing in the Services shall constitute or be construed as an offering of financial instruments by BFLP,BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of an investment strategy or whether or not to "buy", "sell" or "hold" an investment. Information available via the Services should not be considered as information sufficient upon which to base an investmentdecision. BLOOMBERG, BLOOMBERG PROFESSIONAL, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG ANYWHERE, BLOOMBERG TRADEBOOK, BLOOMBERG TELEVISION, BLOOMBERG RADIO, BLOOMBERG PRESS and BLOOMBERG.COM are trademarks and service marksof BFLP, a Delaware limited partnership, or its subsidiaries. © 2015 Bloomberg Finance L.P. All rights reserved. This document and its contents may not be forwarded or redistributed without the prior consent of Bloomberg.

Overview > Why The Corporate E&P M&A Fuss? It Doesn't Work Well >> Exhibit 11 of 13

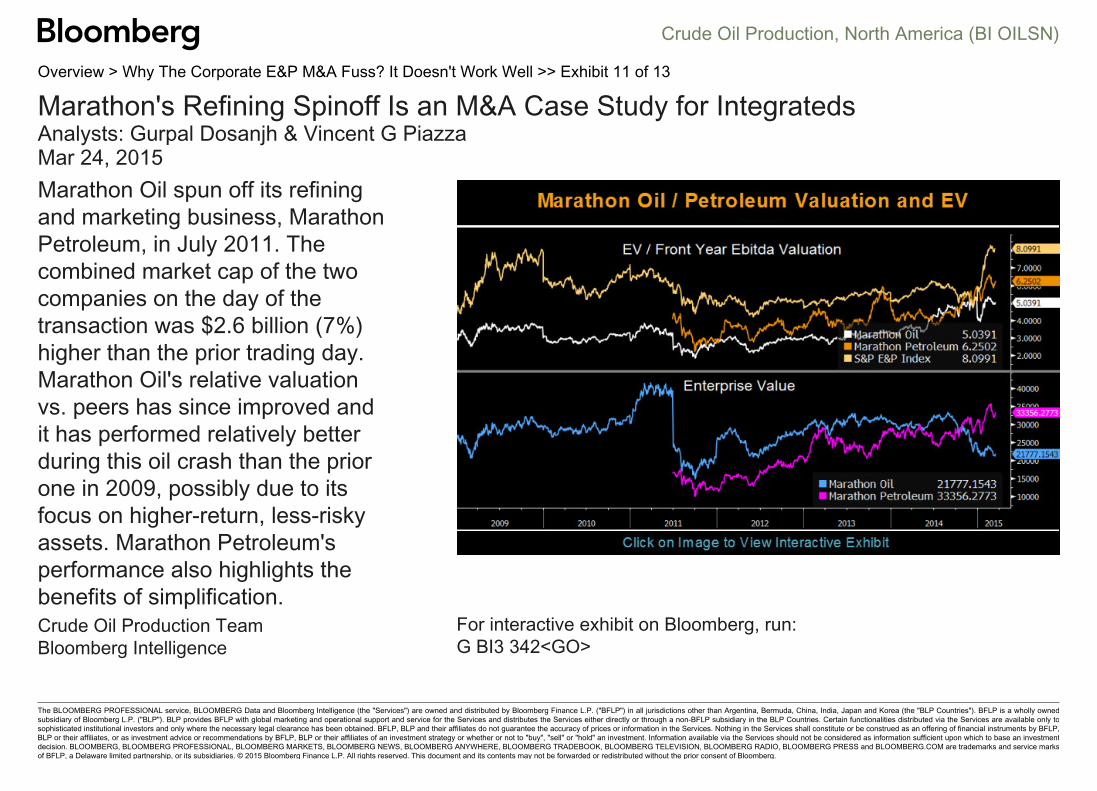

Marathon's Refining Spinoff Is an M&A Case Study for IntegratedsAnalysts: Gurpal Dosanjh & Vincent G PiazzaMar 24, 2015Marathon Oil spun off its refiningand marketing business, MarathonPetroleum, in July 2011. Thecombined market cap of the twocompanies on the day of thetransaction was $2.6 billion (7%)higher than the prior trading day.Marathon Oil's relative valuationvs. peers has since improved andit has performed relatively betterduring this oil crash than the priorone in 2009, possibly due to itsfocus on higher-return, less-riskyassets. Marathon Petroleum'sperformance also highlights thebenefits of simplification.

Crude Oil Production Team For interactive exhibit on Bloomberg, run:Bloomberg Intelligence G BI3 342<GO>

Crude Oil Production, North America (BI OILSN)

The BLOOMBERG PROFESSIONAL service, BLOOMBERG Data and Bloomberg Intelligence (the "Services") are owned and distributed by Bloomberg Finance L.P. ("BFLP") in all jurisdictions other than Argentina, Bermuda, China, India, Japan and Korea (the "BLP Countries"). BFLP is a wholly ownedsubsidiary of Bloomberg L.P. ("BLP"). BLP provides BFLP with global marketing and operational support and service for the Services and distributes the Services either directly or through a non-BFLP subsidiary in the BLP Countries. Certain functionalities distributed via the Services are available only tosophisticated institutional investors and only where the necessary legal clearance has been obtained. BFLP, BLP and their affiliates do not guarantee the accuracy of prices or information in the Services. Nothing in the Services shall constitute or be construed as an offering of financial instruments by BFLP,BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of an investment strategy or whether or not to "buy", "sell" or "hold" an investment. Information available via the Services should not be considered as information sufficient upon which to base an investmentdecision. BLOOMBERG, BLOOMBERG PROFESSIONAL, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG ANYWHERE, BLOOMBERG TRADEBOOK, BLOOMBERG TELEVISION, BLOOMBERG RADIO, BLOOMBERG PRESS and BLOOMBERG.COM are trademarks and service marksof BFLP, a Delaware limited partnership, or its subsidiaries. © 2015 Bloomberg Finance L.P. All rights reserved. This document and its contents may not be forwarded or redistributed without the prior consent of Bloomberg.

Overview > Why The Corporate E&P M&A Fuss? It Doesn't Work Well >> Exhibit 12 of 13

E&Ps May Find Simplicity Not Consolidation Drives Better ResultsAnalysts: Vincent G Piazza & Gurpal DosanjhMar 24, 2015Returning capital to shareholders,spinning off assets, or droppinginfrastructure assets intomaster limited partnershipsoffers transparency and mayenhance value for investors. YetE&Ps seeking inorganic growthopportunities may signal lessconfidence in existing assets. E&Pcompanies with simplified corporatestructures may perform betterthan diversified companies thatparticipate in corporate acquisitions.

Crude Oil Production Team For interactive exhibit on Bloomberg, run:Bloomberg Intelligence G BI3 349<GO>

Crude Oil Production, North America (BI OILSN)

The BLOOMBERG PROFESSIONAL service, BLOOMBERG Data and Bloomberg Intelligence (the "Services") are owned and distributed by Bloomberg Finance L.P. ("BFLP") in all jurisdictions other than Argentina, Bermuda, China, India, Japan and Korea (the "BLP Countries"). BFLP is a wholly ownedsubsidiary of Bloomberg L.P. ("BLP"). BLP provides BFLP with global marketing and operational support and service for the Services and distributes the Services either directly or through a non-BFLP subsidiary in the BLP Countries. Certain functionalities distributed via the Services are available only tosophisticated institutional investors and only where the necessary legal clearance has been obtained. BFLP, BLP and their affiliates do not guarantee the accuracy of prices or information in the Services. Nothing in the Services shall constitute or be construed as an offering of financial instruments by BFLP,BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of an investment strategy or whether or not to "buy", "sell" or "hold" an investment. Information available via the Services should not be considered as information sufficient upon which to base an investmentdecision. BLOOMBERG, BLOOMBERG PROFESSIONAL, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG ANYWHERE, BLOOMBERG TRADEBOOK, BLOOMBERG TELEVISION, BLOOMBERG RADIO, BLOOMBERG PRESS and BLOOMBERG.COM are trademarks and service marksof BFLP, a Delaware limited partnership, or its subsidiaries. © 2015 Bloomberg Finance L.P. All rights reserved. This document and its contents may not be forwarded or redistributed without the prior consent of Bloomberg.

Overview > Why The Corporate E&P M&A Fuss? It Doesn't Work Well >> Exhibit 13 of 13

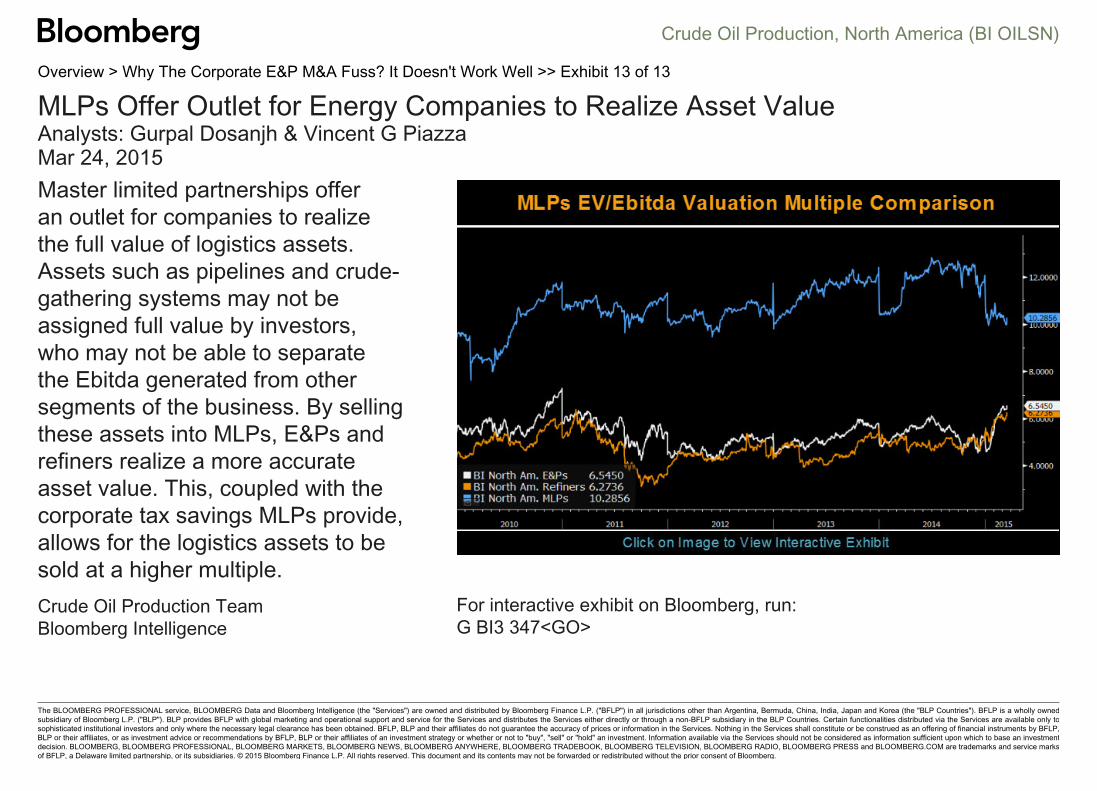

MLPs Offer Outlet for Energy Companies to Realize Asset ValueAnalysts: Gurpal Dosanjh & Vincent G PiazzaMar 24, 2015Master limited partnerships offeran outlet for companies to realizethe full value of logistics assets.Assets such as pipelines and crude-gathering systems may not beassigned full value by investors,who may not be able to separatethe Ebitda generated from othersegments of the business. By sellingthese assets into MLPs, E&Ps andrefiners realize a more accurateasset value. This, coupled with thecorporate tax savings MLPs provide,allows for the logistics assets to besold at a higher multiple.

Crude Oil Production Team For interactive exhibit on Bloomberg, run:Bloomberg Intelligence G BI3 347<GO>