cost-volume-profit relationship chapter 5. cvp formula cvp formula sx = vcx + fc + p s= selling...

TRANSCRIPT

COST-VOLUME-PROFIT COST-VOLUME-PROFIT RELATIONSHIPRELATIONSHIPCHAPTER 5

CVP FormulaCVP FormulaSx = VCx + FC + PS= Selling PriceX= Sales VolumeVC = Variable Cost per unitFC = Fixed CostP= ProfitVery powerful equationIf all else fails just work the

equation

Things you can find out using CVP Things you can find out using CVP formulaformulaBreakeven pointsUnits to sell to get a certain profitHow many more to sell if Fixed

Cost increasedSelling Price

Apply CVP FormulaApply CVP FormulaSelling Price $36Variable Cost $24 per unitFixed Costs $12,000Units 2,000Profit= ?Put in CVP formula

CONTRIBUTION MARGINCONTRIBUTION MARGINThe amount that contributes to fixed

costs and profits i.e ContributionCalculated In per unit, $ and in %

$100 Sales 60 VC$ 40 CM 40% Ratio

($40/$100= .40) 35 FC $ 5 NI

CONTRIBUTION MARGIN CONTRIBUTION MARGIN FORMATFORMAT Income Income StatementStatementSALES

-VARIABLE COST=CONTRIBUTION MARGIN- FIXED EXPENSESNET OPERATING INCOME

Exercise 5-1 page 213

Application of CVP Application of CVP DataDataExercise 5-5 page 2141- Increase advertising budget2- Increase quality of product

BREAK EVEN (BE) IN UNITS & BREAK EVEN (BE) IN UNITS & $$The units or $ that will cover the

fixed costs with no profit.

Sx – VCx= FC BE in equation method

FC/CM% = BE$ CM MethodYou can determine: BE in units,

BE in $Exercise 5-7 pg 214

PROFIT PLANNINGPROFIT PLANNINGAnswers these questions:How many do I need to sell to

make $100,000 profitFor example: If I reduce my fixed

costs by $2,000 and increase my sales in units by 100 how will my profit change?

Target Profit Target Profit AnalysisAnalysis Formula for units to make a $

profit FC + Profit Unit CM

X sales price = Sales to attain target profit

Exercise 5-6 pg 2141- equation method2- CM approach

Margin of Safety Margin of Safety (MS)(MS) Amount you can drop before losses

are incurredHow much can our sales drop

before we start losing moneyEvery company has a different %

because each is structured differently

How much excess you have over break even.

How much you have after you cover your fixed costs.

Margin of Safety formulaMargin of Safety formulaBudgeted Sales – BE$ = MS$MS$/Budgeted Sales=MS%Example:Sales $100,000BE$ 87,500MS$ $ 12,500 / 100,000 =

12.5%Exercise 5-8 page 214

Operating Leverage (OL) pg Operating Leverage (OL) pg 202202How sensitive income is to a %

change in Sales $How a % change in Sales volume

will affect profits.It is a MultiplierIf OL is high a small % change in

Sales will reuslt in a higher change in NI

Operating Leverage Operating Leverage FormulaFormulaContribution Margin $Net Income in $

It OL is 2 and sales increased by 5% then net income will increase by 10%

Exercise 5-9 pg 215

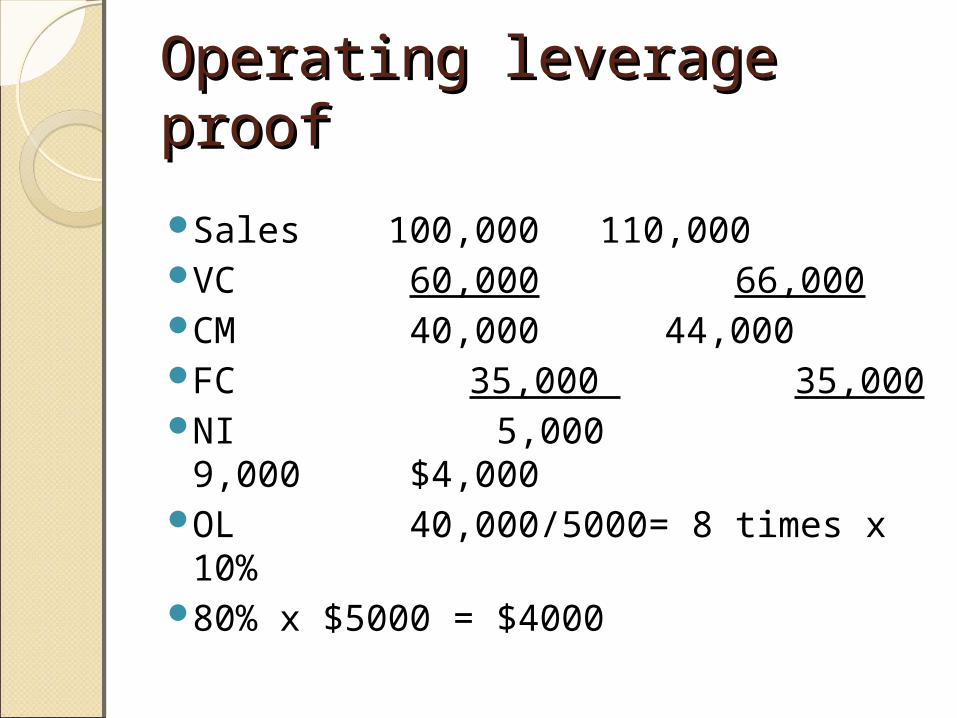

Operating leverage proofOperating leverage proof

Sales 100,000 110,000VC 60,000 66,000CM 40,000 44,000FC 35,000 35,000NI 5,000 9,000

$4,000OL 40,000/5000= 8 times x 10%80% x $5000 = $4000

CM Ratio CM Ratio Another way to determine effect on net

incomeChange in Net Income with the change in

Total Sales

If we sell 10,000 more units, how would our net income increase?

10,000 X25%CM= 2500 change in units X $24 per unit = $60,000 increase in NI

How much would our net income increase if our sales increase by $240,000

$240,000 X 25% = $60,000

Sales Mix Sales Mix Multi Product CM Multi Product CMProportions in which a company’s products

are soldMix that will yield the greatest profitSteps to determine1- Total all sales2- VC % for each product and total sales3- = CM% for all sales4- Determine total BE$ FC/CM%5- Each product % of total sales X BE$6- Use VC% for each product for VC7- =CM for each product = total fixed costs Page 206 Exhibit 5-4Exercise 5-10, pg 215