csco q1fy10 presentation

TRANSCRIPT

8/14/2019 CSCO Q1FY10 Presentation

http://slidepdf.com/reader/full/csco-q1fy10-presentation 1/30

Conference Call

November 4, 2009

8/14/2019 CSCO Q1FY10 Presentation

http://slidepdf.com/reader/full/csco-q1fy10-presentation 2/30

GAAP RECONCILIATIONGAAP RECONCILIATIONDuring this presentation references to financial measures of Cisco w

references to non-GAAP financial measures. Cisco provides a recon

between GAAP and non-GAAP financial information on our website

www.cisco.com under “About Cisco” in the “Investor Relations” secti

http://investor.cisco.com/results.cfm

--This presentation contains projections and other forward-looking stat

regarding future events or the future financial performance of Cisco,

future operating results. These projections and statements are only

Actual events or results may differ materially from those in the proje

other forward-looking statements. Please see Cisco’s filings with the

including its most recent filing on Form 10-K, for a discussion of imp

factors that could cause actual events or results to differ materially fr

the projections or other forward-looking statements.

2

ill include

ciliation

t

n.

ements

including

redictions.

tions or

SEC,

rtant risk

om those in

8/14/2019 CSCO Q1FY10 Presentation

http://slidepdf.com/reader/full/csco-q1fy10-presentation 3/30

Opening Remarks

Financial Overvie

Business Overview

ra egy

Guidance

Summary Commen

3

nd

s

8/14/2019 CSCO Q1FY10 Presentation

http://slidepdf.com/reader/full/csco-q1fy10-presentation 4/30

Q1 FY’10 Highlight

Financial SummaryFinancial Summary Revenue of $9.0B (-13% vs -1

Non-GAAP EPS of $0.36

Solid expense management,

- Cash generated from operatio

Non-GAAP operating income

Product book to bill was abov

Services revenue up 7% y/y

5% to -17% guid

on-GAAP OpEx

ns of approx. $1.

ery strong at 29

1

8/14/2019 CSCO Q1FY10 Presentation

http://slidepdf.com/reader/full/csco-q1fy10-presentation 5/30

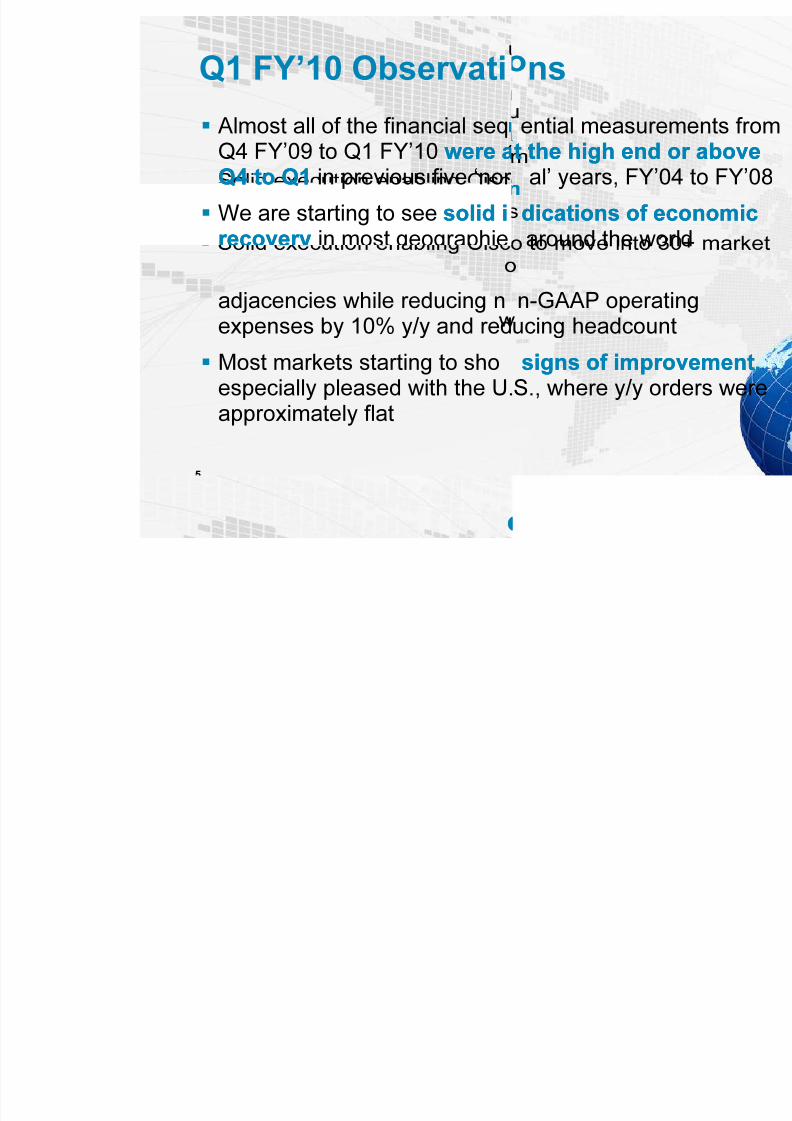

Q1 FY’10 Observati

Almost all of the financial seqQ4 FY’09 to Q1 FY’10 were awere aQ4 to Q1Q4 to Q1 in previous five ‘nor

We are starting to see solid isolid irecoveryrecovery in most geographie

adjacencies while reducing nexpenses by 10% y/y and red

Most markets starting to shoespecially pleased with the U.

approximately flat

ns

ential measuremt the high end ot the high end o

al’ years, FY’04

dications of ecdications of ecaround the wor

n-GAAP operatiucing headcount

signs of improsigns of improS., where y/y ord

8/14/2019 CSCO Q1FY10 Presentation

http://slidepdf.com/reader/full/csco-q1fy10-presentation 6/30

Q1 FY’10 Observati

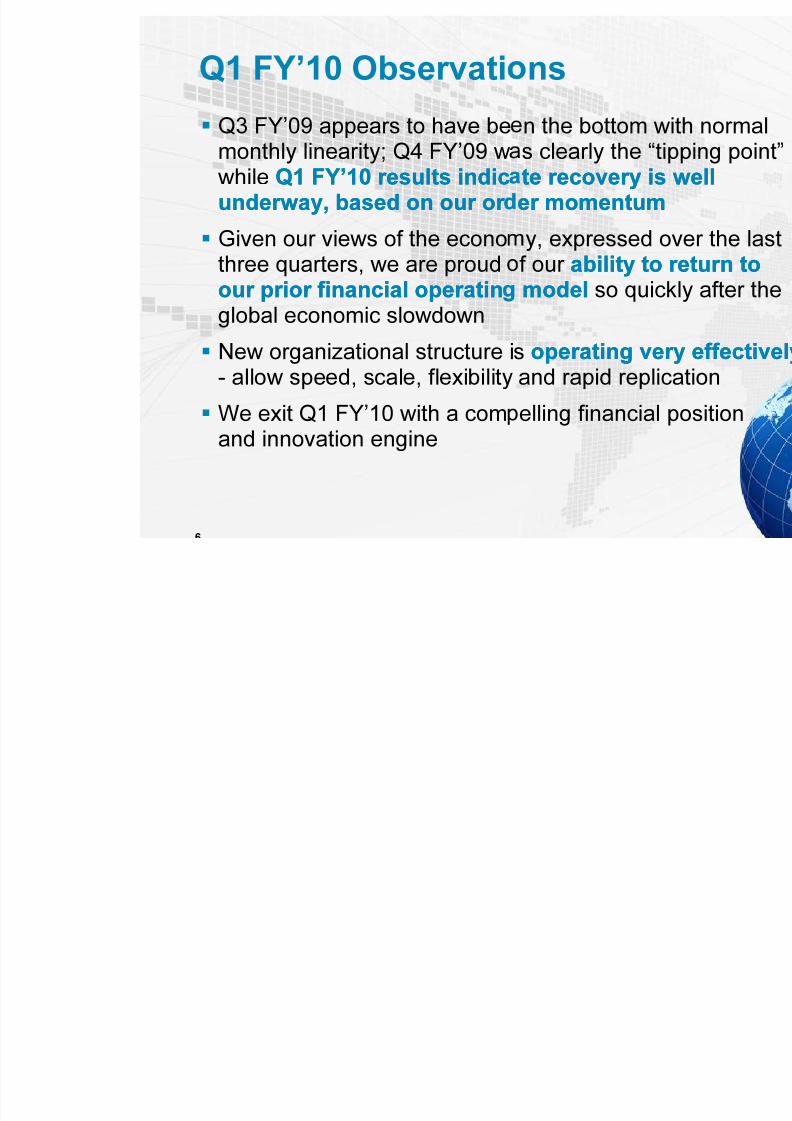

Q3 FY’09 appears to have bemonthly linearity; Q4 FY’09 wwhile Q1 FY’10 results indicQ1 FY’10 results indicunderway, based on our or underway, based on our or

Given our views of the econo

three quarters, we are proudour prior financial operatinour prior financial operatinglobal economic slowdown

New organizational structure i- allow speed, scale, flexibility

We exit Q1 FY’10 with a comand innovation engine

ns

n the bottom wis clearly the “tipte recovery is wte recovery is wer momentumer momentum

y, expressed ov

f our ability to rability to rmodelmodel so quick

s operating veryoperating veryand rapid replica

elling financial p

8/14/2019 CSCO Q1FY10 Presentation

http://slidepdf.com/reader/full/csco-q1fy10-presentation 7/30

Q1 FY’10 Observati

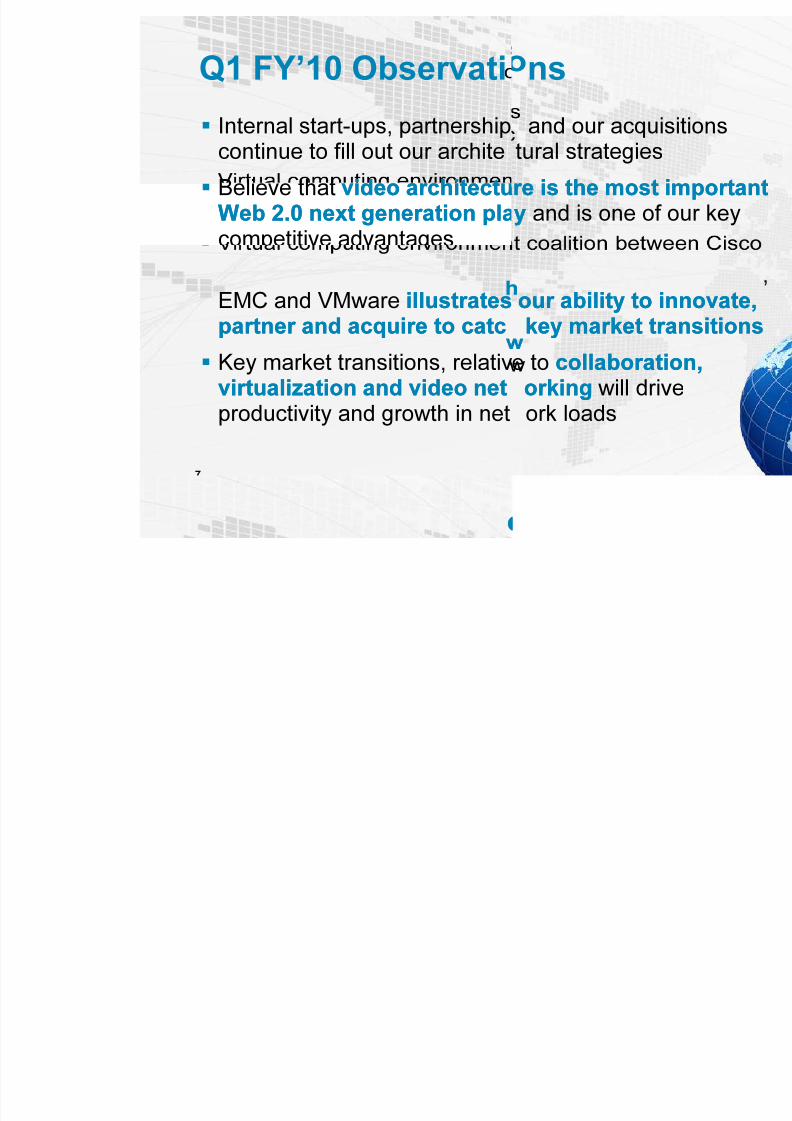

Internal start-ups, partnershipcontinue to fill out our archite

Believe that video architectuvideo architectuWeb 2.0 next generation plaWeb 2.0 next generation placompetitive advantages

EMC and VMware illustratesillustratespartner and acquire to catcpartner and acquire to catc

Key market transitions, relativvirtualization and video netvirtualization and video net

productivity and growth in net

ns

and our acquistural strategies

re is the most imre is the most imyy and is one of o

our ability to inour ability to inkey market trakey market tra

e to collaboratiocollaboratioorkingorking will drive

ork loads

8/14/2019 CSCO Q1FY10 Presentation

http://slidepdf.com/reader/full/csco-q1fy10-presentation 8/30

Opening Remarks

Financial Overvie

Business Overview

ra egy

Guidance

Summary Commen

nd

s

8/14/2019 CSCO Q1FY10 Presentation

http://slidepdf.com/reader/full/csco-q1fy10-presentation 9/30

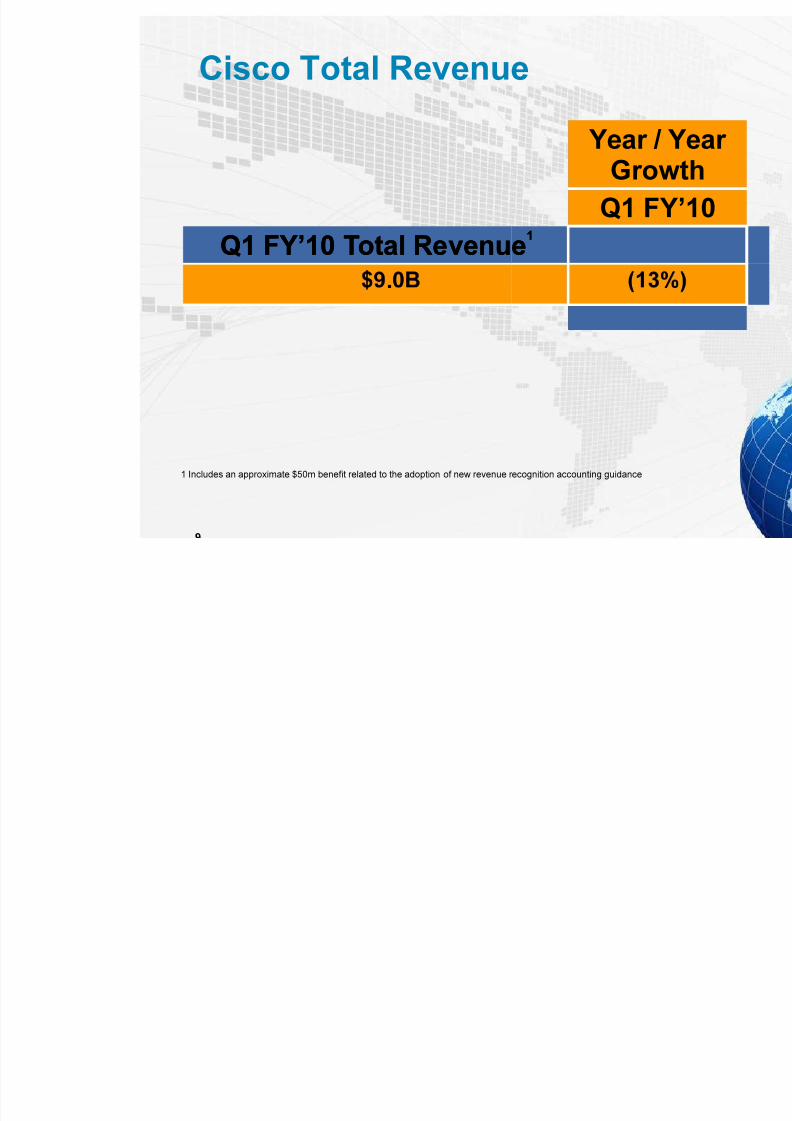

Cisco Total Revenu

Q1 FY’10 Total RevenuQ1 FY’10 Total Revenu

.

1 Includes an approximate $50m benefit related to the adoption of new revenue r

e

Year / YGrow

Q1 FY

ee11

ecognition accounting guidance

8/14/2019 CSCO Q1FY10 Presentation

http://slidepdf.com/reader/full/csco-q1fy10-presentation 10/30

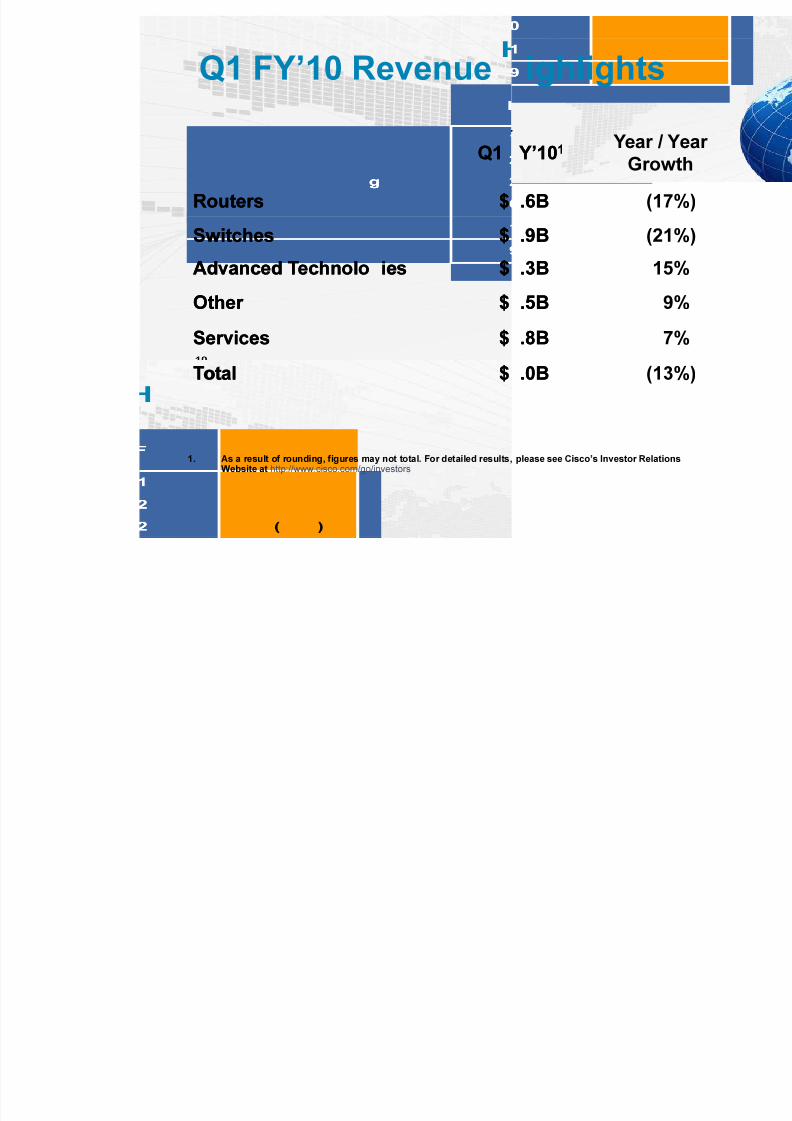

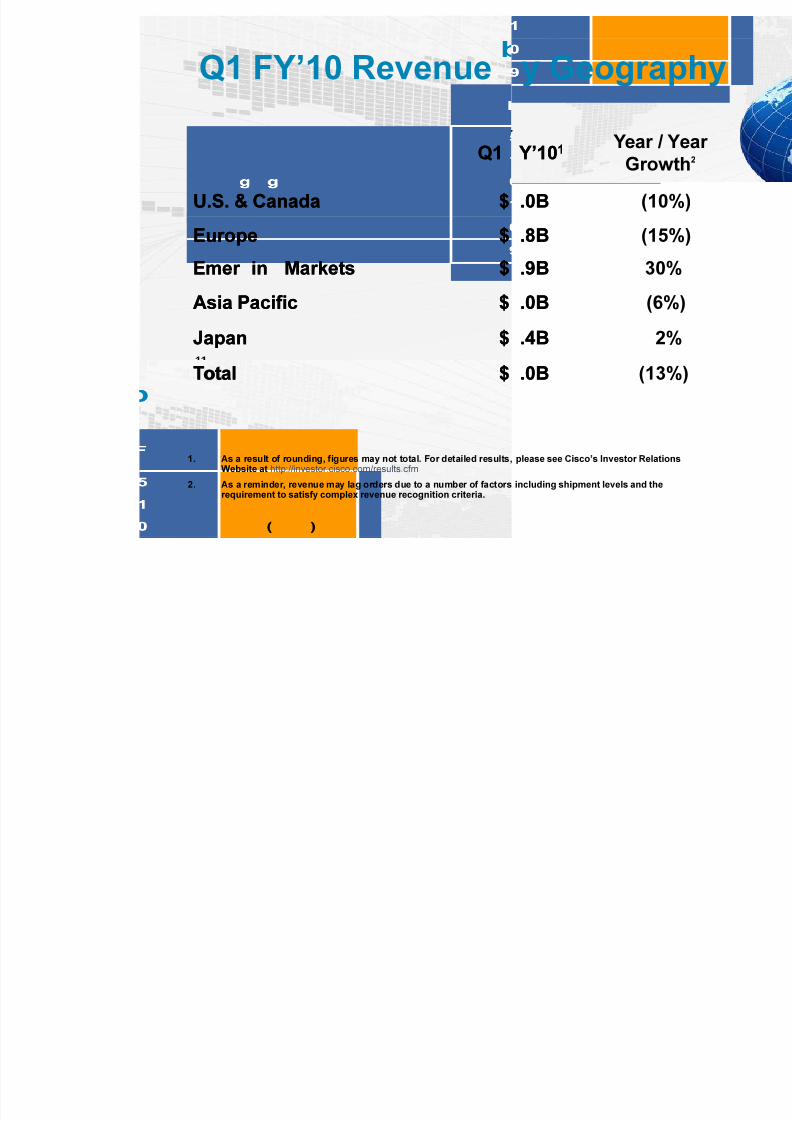

Q1 FY’10 Revenue

Q1Q1

RoutersRouters $$

SwitchesSwitches $$

Advanced Technolo iesAdvanced Technolo ies $$Other Other $$

ServicesServices $$

TotalTotal $$

1. As a result of rounding, figures may not total. For detailed results,Website at http://www.cisco.com/go/investors

ighlights

Y’10Y’1011 Year / YGrow

.6B.6B (17

.9B.9B (21

.3B.3B 15

.5B.5B 9

.8B.8B 7

.0B.0B (13

please see Cisco’s Investor Relation

8/14/2019 CSCO Q1FY10 Presentation

http://slidepdf.com/reader/full/csco-q1fy10-presentation 11/30

8/14/2019 CSCO Q1FY10 Presentation

http://slidepdf.com/reader/full/csco-q1fy10-presentation 12/30

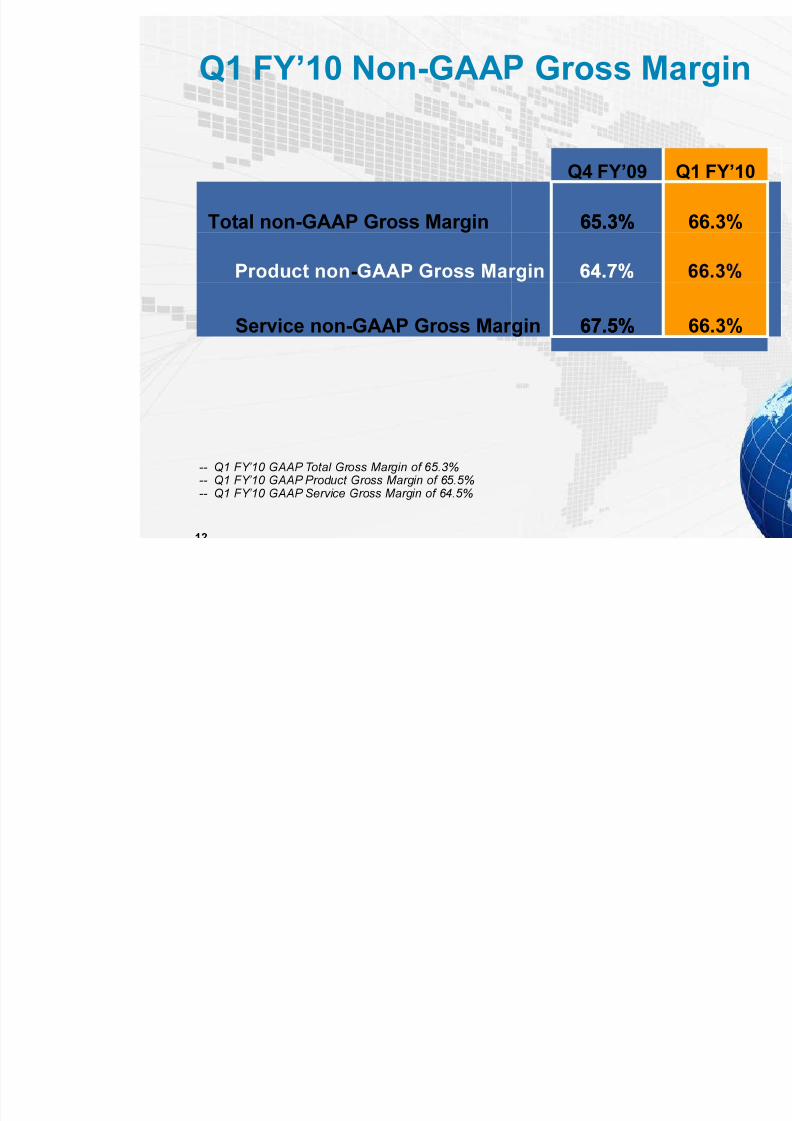

Q1 FY’10 Non-GAA

Total non-GAAP Gross Margin

-

Service non-GAAP Gross Mar

-- Q1 FY’10 GAAP Total Gross Margin of 65.3%-- Q1 FY’10 GAAP Product Gross Margin of 65.5%-- Q1 FY’10 GAAP Service Gross Margin of 64.5%

Gross Ma

Q4 FY’09

65.3%65.3%

gin 67.5%67.5%

8/14/2019 CSCO Q1FY10 Presentation

http://slidepdf.com/reader/full/csco-q1fy10-presentation 13/30

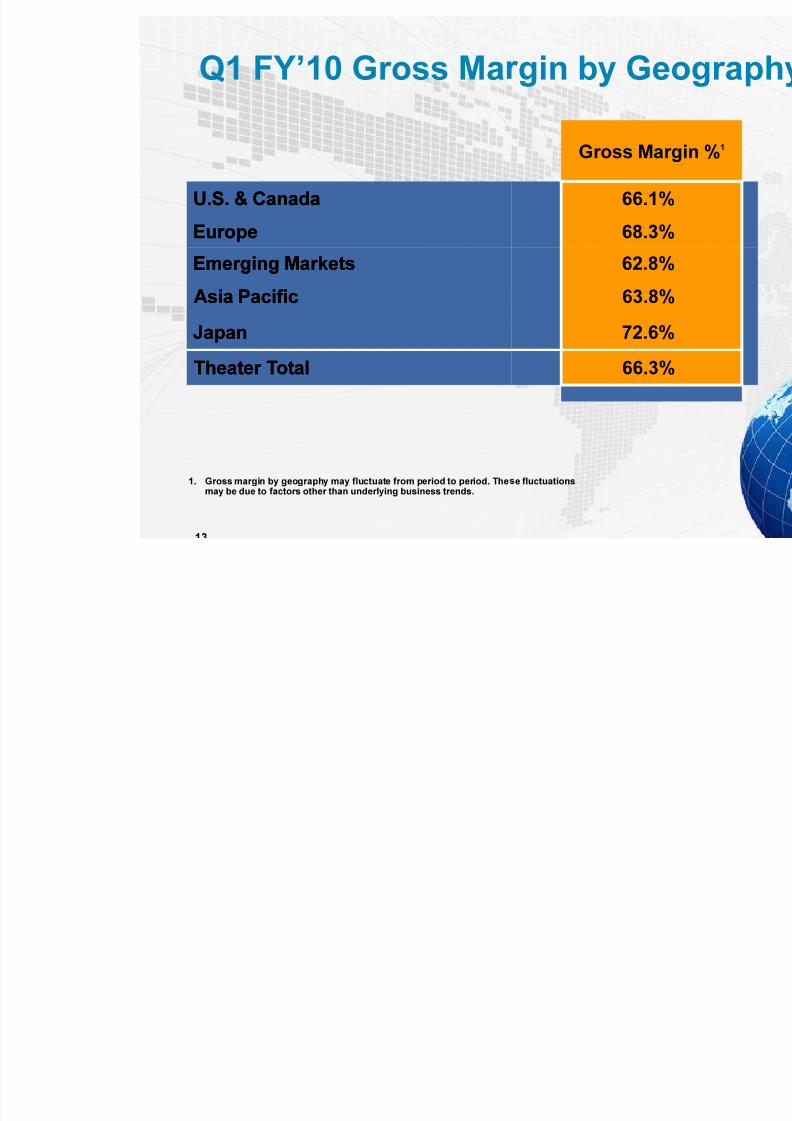

Q1 FY’10 Gross Ma

U.S. & CanadaU.S. & Canada

EuropeEurope

Emerging MarketsEmerging Markets

Asia PacificAsia Pacific

JapanJapan

Theater TotalTheater Total

1. Gross margin by geography may fluctuate from period to period. Themay be due to factors other than underlying business trends.

gin by Geo

Gross Marg

66.1%

68.3%

62.8%

63.8%

72.6%

66.3%

e fluctuations

8/14/2019 CSCO Q1FY10 Presentation

http://slidepdf.com/reader/full/csco-q1fy10-presentation 14/30

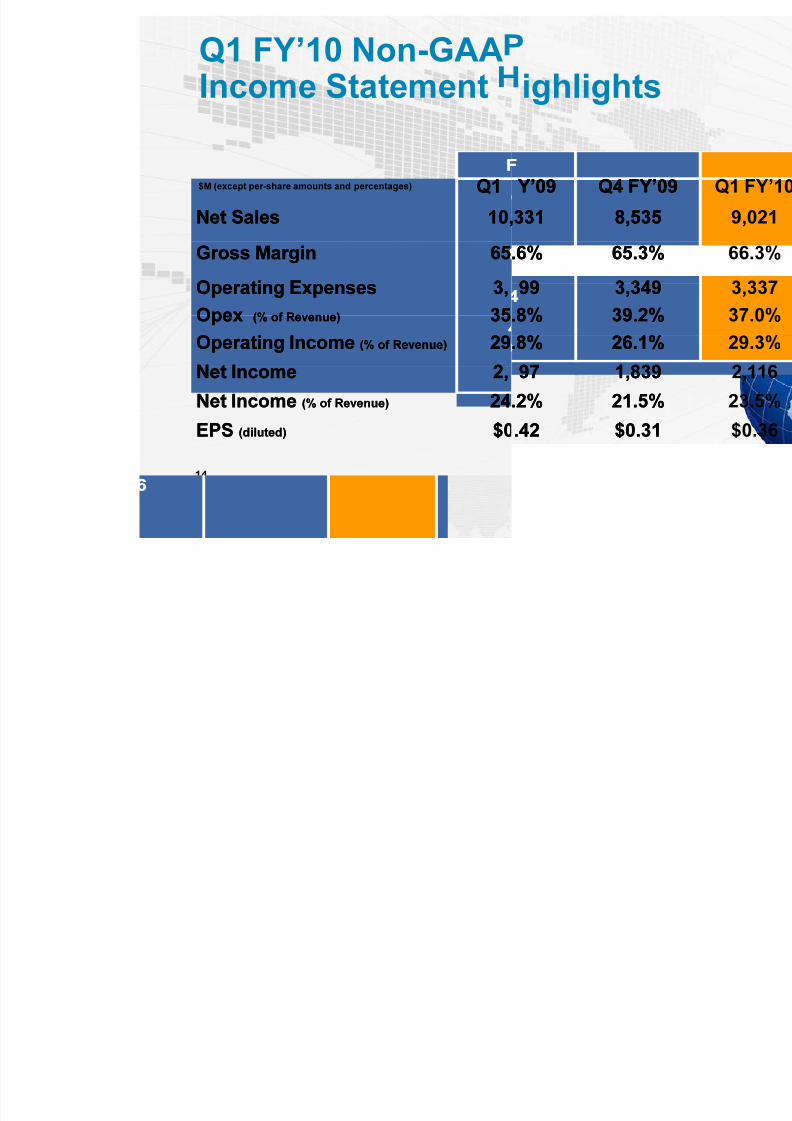

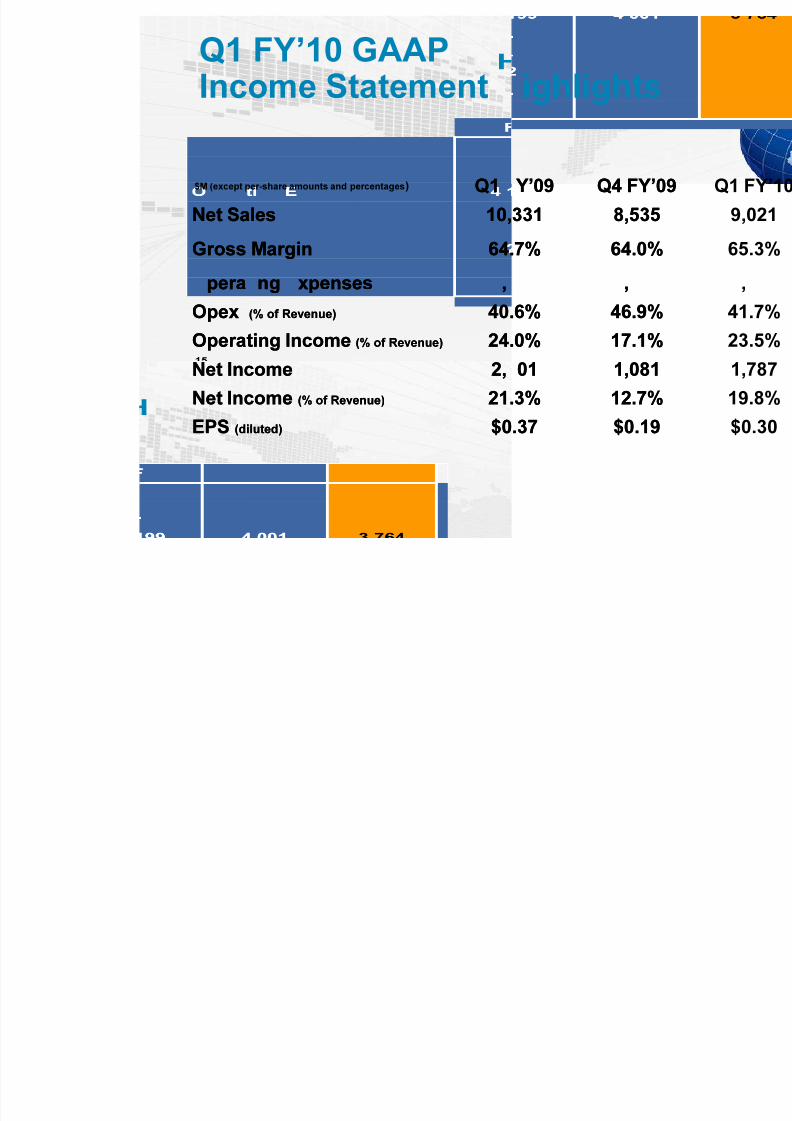

Q1 FY’10 Non-GAAIncome Statement

$M (except per-share amounts and percentages) Q1Q1

Net SalesNet Sales 10,10,

Gross MarginGross Margin 6565

Operating ExpensesOperating Expenses 3,3,

OpexOpex (% of Revenue)(% of Revenue) 3535

Operating IncomeOperating Income (% of Revenue)(% of Revenue) 2929

Net IncomeNet Income 2,2,

Net IncomeNet Income (% of Revenue)(% of Revenue) 2424

EPSEPS (diluted)(diluted) $0$0

ighlights

Y’09Y’09 Q4 FY’09Q4 FY’09

331331 8,5358,535

.6%.6% 65.3%65.3%

9999 3,3493,349

.8%.8% 39.2%39.2%

.8%.8% 26.1%26.1%

9797 1,8391,839

.2%.2% 21.5%21.5%

.42.42 $0.31$0.31

8/14/2019 CSCO Q1FY10 Presentation

http://slidepdf.com/reader/full/csco-q1fy10-presentation 15/30

Q1 FY’10 GAAPIncome Statement

$M (except per-share amounts and percentages) Q1Q1

Net SalesNet Sales 10,10,

Gross MarginGross Margin 64.64.

pera ng xpensespera ng xpenses ,,

OpexOpex (% of Revenue)(% of Revenue) 40.40.

Operating IncomeOperating Income (% of Revenue)(% of Revenue) 24.24.

Net IncomeNet Income 2,2,

Net IncomeNet Income (% of Revenue)(% of Revenue) 21.21.

EPSEPS (diluted)(diluted) $0$0

ighlights

Y’09Y’09 Q4 FY’09Q4 FY’09

331331 8,5358,535

7%7% 64.0%64.0%

,,

6%6% 46.9%46.9%

0%0% 17.1%17.1%

0101 1,0811,081

3%3% 12.7%12.7%

.37.37 $0.19$0.19

8/14/2019 CSCO Q1FY10 Presentation

http://slidepdf.com/reader/full/csco-q1fy10-presentation 16/30

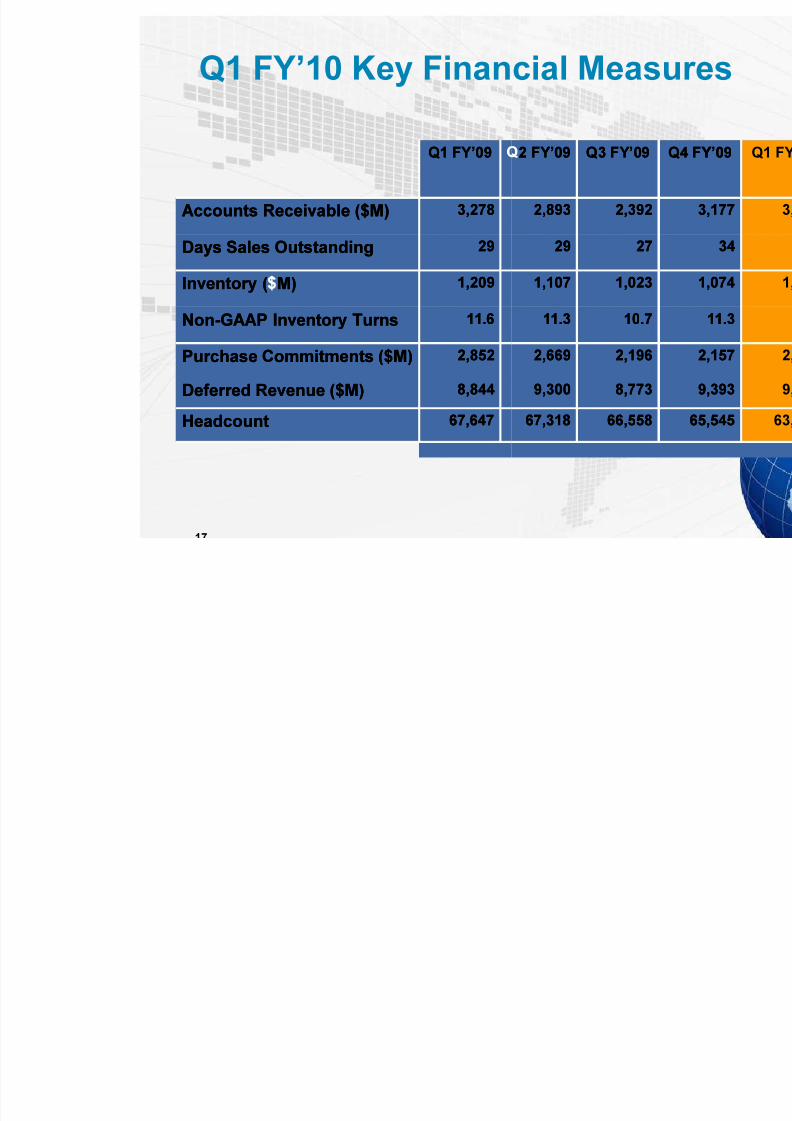

Q1 FY’10 Key Finan

Q1 FY’09Q1 FY’09

Cash and Cash EquivalentsCash and Cash Equivalentsand Investments ($M)and Investments ($M)

26,76326,763

Operating Cash Flow ($M)Operating Cash Flow ($M) 2,7182,718

Share Repurchase ProgramAmAm

PurchaPurcha

Q1 FY’10 Purchases $1

Cumulative Program Purchases*Cumulative Program Purchases* $58$58

*Since program inception in FY’02

Approx. $13.1B remaining authorized fundprogram, including $10B additional author on November 4 2009 by Cisco Board of Dir

cial Measu

2 FY’092 FY’09 Q3 FY’09Q3 FY’09

29,53129,531 33,55133,551

3,1983,198 1,9961,996

untunteded ($M)($M)

Number of Number of SharesShares (M)(M)

AvgAvg

,753 76

,932,932 2,8782,878

in repurchaseization approvedectors.

8/14/2019 CSCO Q1FY10 Presentation

http://slidepdf.com/reader/full/csco-q1fy10-presentation 17/30

Q1 FY’10 Key Finan

Q1 FY’09Q1 FY’09

Accounts Receivable ($M)Accounts Receivable ($M) 3,2783,278

Days Sales OutstandingDays Sales Outstanding 2929

Inventory ( M)Inventory ( M) 1,2091,209

NonNon--GAAP Inventory TurnsGAAP Inventory Turns 11.611.6

Purchase Commitments ($M)Purchase Commitments ($M) 2,8522,852

Deferred Revenue ($M)Deferred Revenue ($M) 8,8448,844

HeadcountHeadcount 67,64767,647

cial Measu

2 FY’092 FY’09 Q3 FY’09Q3 FY’09 QQ

2,8932,893 2,3922,392

2929 2727

1,1071,107 1,0231,023

11.311.3 10.710.7

2,6692,669 2,1962,196

9,3009,300 8,7738,773

67,31867,318 66,55866,558

8/14/2019 CSCO Q1FY10 Presentation

http://slidepdf.com/reader/full/csco-q1fy10-presentation 18/30

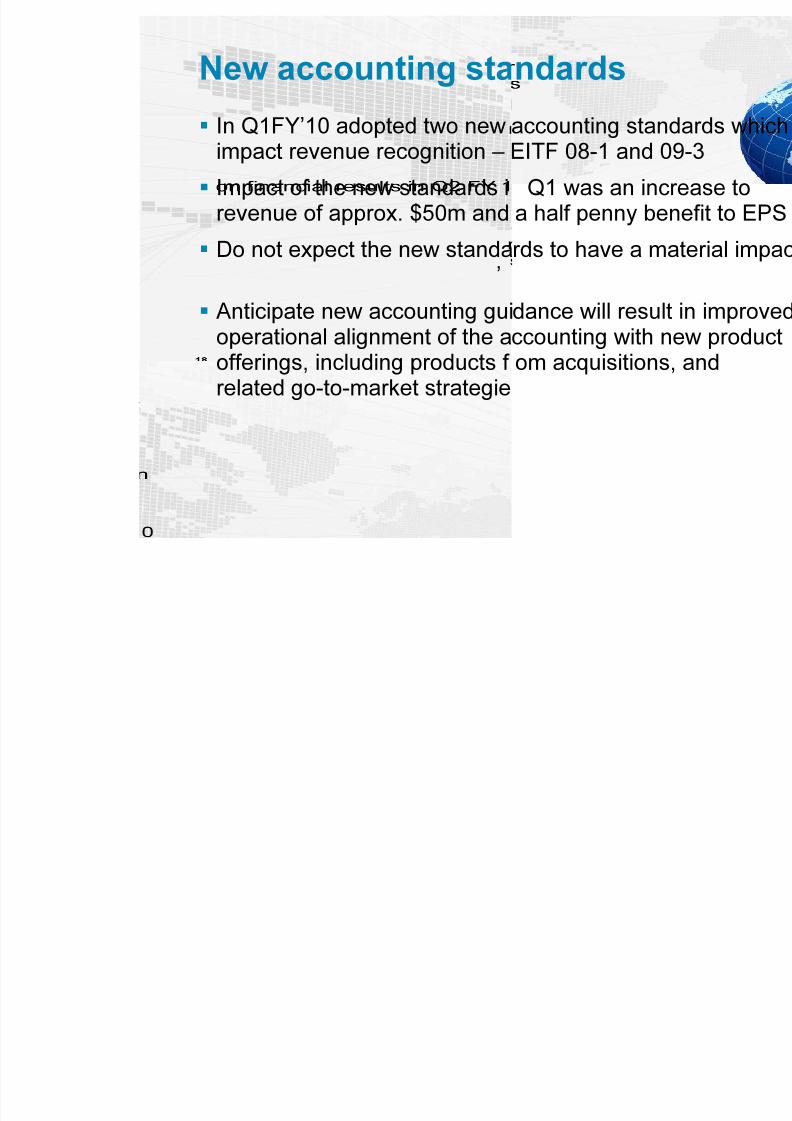

New accounting sta

In Q1FY’10 adopted two newimpact revenue recognition –

Impact of the new standards irevenue of approx. $50m and

Do not expect the new standa

’ Anticipate new accounting gui

operational alignment of the aofferings, including products f related go-to-market strategie

ndards

accounting standEITF 08-1 and 09

Q1 was an incra half penny ben

rds to have a ma

dance will result ccounting with neom acquisitions,

8/14/2019 CSCO Q1FY10 Presentation

http://slidepdf.com/reader/full/csco-q1fy10-presentation 19/30

Financial summary

Pleased with our Q1 results awhich we can continue to focfocmarket transitionsmarket transitions

Ongoing efforts to improve eff allowed us to deliver strong p

make investments in innovmake investments in innovand our key growth opportuand our key growth opportu

d the strong fous on growth ans on growth an

iciency and prodrformance; we w

tion, operationation, operationanitiesnities

8/14/2019 CSCO Q1FY10 Presentation

http://slidepdf.com/reader/full/csco-q1fy10-presentation 20/30

Opening Remarks

Financial Overvie

Business Overview

ra egy

Guidance

Summary Commen

nd

s

8/14/2019 CSCO Q1FY10 Presentation

http://slidepdf.com/reader/full/csco-q1fy10-presentation 21/30

Strategy Review

Q1 continued the trend of baland operational effectiveness

The major results and commitvideovideo and collaborationcollaboration wer phases of our focus on marke

communications and IT

nce between inn

ents to virtualivirtualievident in almoadjacencies as

8/14/2019 CSCO Q1FY10 Presentation

http://slidepdf.com/reader/full/csco-q1fy10-presentation 22/30

Strategy Review

Virtualization

– Solid momentum driven by Nex

– UCS experiencing solid market

– VCE Coalition announcementrepresents an unprecedented l

Video – TelePresence revenues grew i

– TANDBERG, DVN and Pure Di

– Medianet architectural solution

Collaboration

– Collaboration driving the next winnovation and productivity

– TANDBERG also about integrabroader $30B+ collaboration m

– Intent to acquire Starent focuss

us 5000 and 7000 fa

reception

ith EMC and VMwavel of collaboration

excess of 100% y/y

ital announcements

ave of business gro

ion of video into therket

d on mobile subscr

8/14/2019 CSCO Q1FY10 Presentation

http://slidepdf.com/reader/full/csco-q1fy10-presentation 23/30

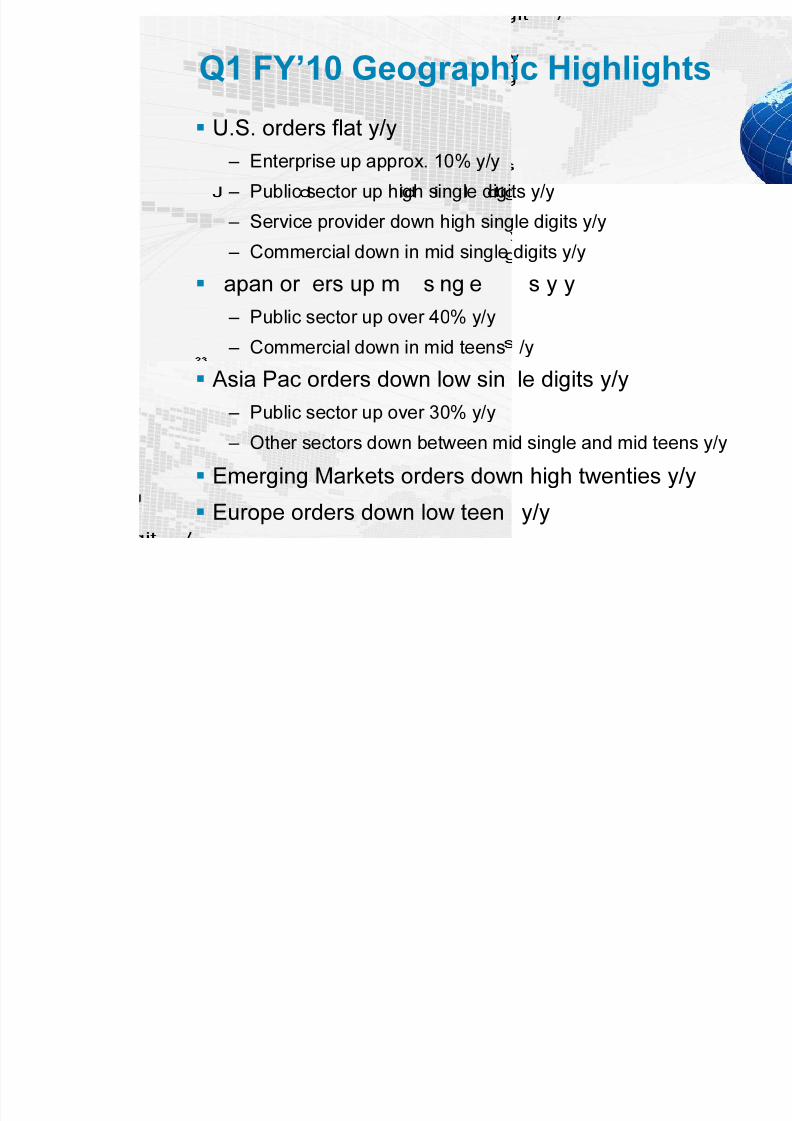

Q1 FY’10 Geograph

U.S. orders flat y/y– Enterprise up approx. 10% y/y

– Public sector up high single digi

– Service provider down high sing

– Commercial down in mid single

apan or ers up m s ng e

– Public sector up over 40% y/y

– Commercial down in mid teens

Asia Pac orders down low sin

– Public sector up over 30% y/y– Other sectors down between mi

Emerging Markets orders dow

Europe orders down low teen

ic Highligh

ts y/y

le digits y/y

digits y/y

s y y

/y

le digits y/y

d single and mid tee

n high twenties y

y/y

8/14/2019 CSCO Q1FY10 Presentation

http://slidepdf.com/reader/full/csco-q1fy10-presentation 24/30

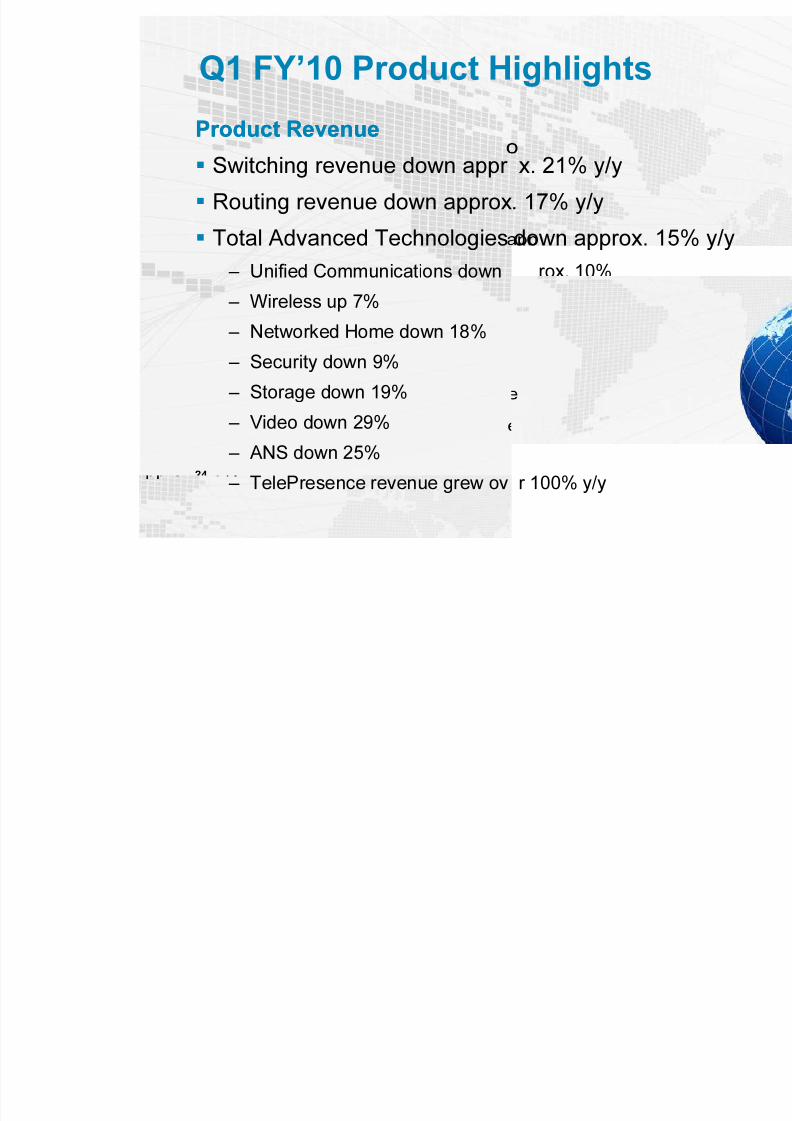

Q1 FY’10 Product H

Product RevenueProduct Revenue Switching revenue down appr

Routing revenue down approx

Total Advanced Technologies

– Unified Communications down– Wireless up 7%

– Networked Home down 18%

– Security down 9%

– Storage down 19%

– Video down 29%

– ANS down 25%

– TelePresence revenue grew ov

ighlights

x. 21% y/y

. 17% y/y

down approx. 15

rox. 10%

r 100% y/y

8/14/2019 CSCO Q1FY10 Presentation

http://slidepdf.com/reader/full/csco-q1fy10-presentation 25/30

Vision, Strategy an

VisionVision of how the industry evvery much as we expected

Our differentiated strategydifferentiated strategy iCisco and our customers that

a customer partnership perspof our customers’ total comm

Execution

lving appears to

achieving the bwe thought were

ctive, market shnications and IT

8/14/2019 CSCO Q1FY10 Presentation

http://slidepdf.com/reader/full/csco-q1fy10-presentation 26/30

Opening Remarks

Financial Overvie

Business Overview

ra egy

Guidance

Summary Commen

nd

s

8/14/2019 CSCO Q1FY10 Presentation

http://slidepdf.com/reader/full/csco-q1fy10-presentation 27/30

Summary Commen

While no one knows for sure t

recovery, job creation opportuof another downturn, we will swe will sexecution assuming an optiexecution assuming an opti

Our customers are rapidly expCisco can help them achieve t

peers

In Q2 FY’10 we plan to aggreaggreand adjacent marketsand adjacent markets for the

On a global and U.S. basis we

we also continue to see somcontinue to see somuncertaintiesuncertainties from an econospending perspective

s

e strength of the

ities and the poset our strategy et our strategy istic viewistic view

anding their viewheir own producproduc

sively invest insively invest inlonger term

saw improveme

challenges anchallenges anic, political and c

8/14/2019 CSCO Q1FY10 Presentation

http://slidepdf.com/reader/full/csco-q1fy10-presentation 28/30

Summary Commen Clearly we saw a tipping poitipping poi

was very strong sequentiallwas very strong sequentially/y growth confirm that the ma

Still too early to know what thextent of job creation,extent of job creation, whichsustainability, will look like in 2

Expect a continued recovery iexpectat ons o not get a eexpectat ons o not get a e

Position Cisco to gain momenwhether they are industry coindustry cotransitions, market adjacentransitions, market adjaceneconomiceconomic

We believe our vision, stratevision, strateare in great shape and produprodu

s

t in Q4 FY’09, at in Q4 FY’09, a

, our expectationrket is recovering

rate of recoverrate of recoveris required for 010

to next year, impo mar et reao mar et rea

um in market trasolidation, prodsolidation, prody opportunitiesy opportunities

y, and executioy, and executioing resultsing results

8/14/2019 CSCO Q1FY10 Presentation

http://slidepdf.com/reader/full/csco-q1fy10-presentation 29/30

8/14/2019 CSCO Q1FY10 Presentation

http://slidepdf.com/reader/full/csco-q1fy10-presentation 30/30