dagong europe proposed criteria for rating financial institutions

TRANSCRIPT

Dagong Europe Credit Rating - www.dagongeurope.com

Contacts

Carola Saldias

Senior Director

Financial Institutions

Christina Sterr

Director

Financial Institutions

Dagong Europe Proposed Criteria for Rating Financial Institutions 18 June 2013

Request for Comment

Financial Institutions

1 18 June 2013 Dagong Europe Proposed Criteria for Rating Financial Institutions

This request for comment details Dagong Europe’s Proposed Criteria for Rating Financial

Institutions. Market participants are invited to review and comment on the proposed criteria

to: [email protected] by 17th July 2013

TABLE OF CONTENTS

I SCOPE

II SUMMARY OF CRITERIA FOR RATING FINANCIAL INSTITUTIONS

III INDIVIDUAL FINANCIAL STRENGHT ASSESSMENT (IFSA)

Operation Environment

Corporate Governance and Development Strategy

Sustainability and Competition

Risk Management

Financial Analysis

Stress Testing and Scenario Analysis

IV EXTERNAL SUPPORT ASSESSMENT (ESA)

V OTHER CONSIDERATIONS FOR FINANCIAL INSTITUTIONS’ CREDIT RATINGS

Financial Institutions

2 18 June 2013 Dagong Europe Proposed Criteria for Rating Financial Institutions

I SCOPE

Dagong Europe has developed a comprehensive set of criteria for the process of assigning

Credit Ratings to Financial Institutions. The criteria set the framework for entities covered

under the Financial Institutions’ analytical team. It is applicable for institutions with different

business models, with and without banking license, as well for regulated and unregulated

entities. The definition of ‘bank’ is broad and includes the larger broker-dealers, mortgage

lenders, trust banks, credit unions, building societies, and custody banks.

The criteria do not apply to institutions, such as asset managers, exchanges, clearinghouses,

regional securities brokers or insurance companies. Procedures, criteria and models applied

by Dagong Europe in its credit rating process are developed in agreement with the Dagong

Europe Sector Heads and Credit Officers of the Committee for Credit Policies.

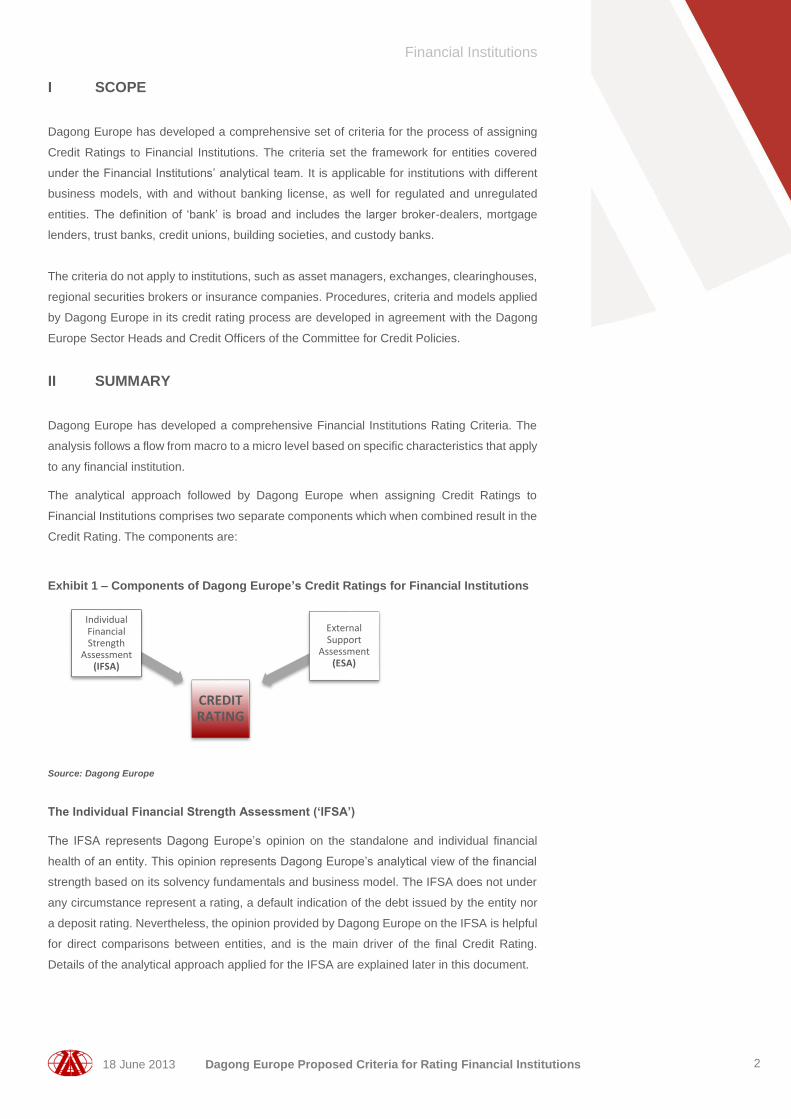

II SUMMARY

Dagong Europe has developed a comprehensive Financial Institutions Rating Criteria. The

analysis follows a flow from macro to a micro level based on specific characteristics that apply

to any financial institution.

The analytical approach followed by Dagong Europe when assigning Credit Ratings to

Financial Institutions comprises two separate components which when combined result in the

Credit Rating. The components are:

Exhibit 1 – Components of Dagong Europe’s Credit Ratings for Financial Institutions

Source: Dagong Europe

The Individual Financial Strength Assessment (‘IFSA’)

The IFSA represents Dagong Europe’s opinion on the standalone and individual financial

health of an entity. This opinion represents Dagong Europe’s analytical view of the financial

strength based on its solvency fundamentals and business model. The IFSA does not under

any circumstance represent a rating, a default indication of the debt issued by the entity nor

a deposit rating. Nevertheless, the opinion provided by Dagong Europe on the IFSA is helpful

for direct comparisons between entities, and is the main driver of the final Credit Rating.

Details of the analytical approach applied for the IFSA are explained later in this document.

CREDIT RATING

Individual Financial Strength

Assessment (IFSA)

External Support

Assessment (ESA)

Financial Institutions

3 18 June 2013 Dagong Europe Proposed Criteria for Rating Financial Institutions

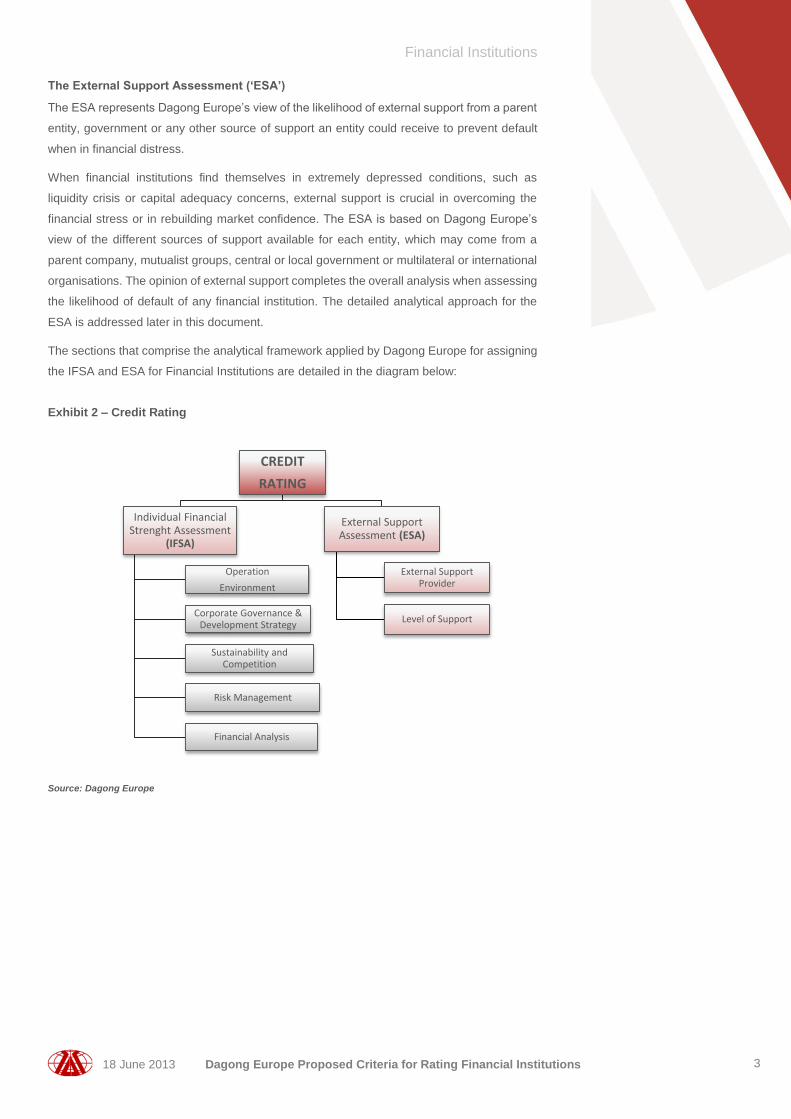

The External Support Assessment (‘ESA’)

The ESA represents Dagong Europe’s view of the likelihood of external support from a parent

entity, government or any other source of support an entity could receive to prevent default

when in financial distress.

When financial institutions find themselves in extremely depressed conditions, such as

liquidity crisis or capital adequacy concerns, external support is crucial in overcoming the

financial stress or in rebuilding market confidence. The ESA is based on Dagong Europe’s

view of the different sources of support available for each entity, which may come from a

parent company, mutualist groups, central or local government or multilateral or international

organisations. The opinion of external support completes the overall analysis when assessing

the likelihood of default of any financial institution. The detailed analytical approach for the

ESA is addressed later in this document.

The sections that comprise the analytical framework applied by Dagong Europe for assigning

the IFSA and ESA for Financial Institutions are detailed in the diagram below:

Exhibit 2 – Credit Rating

Source: Dagong Europe

CREDIT

RATING

Individual Financial Strenght Assessment

(IFSA)

Operation

Environment

Corporate Governance & Development Strategy

Sustainability and Competition

Risk Management

Financial Analysis

External Support Assessment (ESA)

External Support Provider

Level of Support

Financial Institutions

4 18 June 2013 Dagong Europe Proposed Criteria for Rating Financial Institutions

III INDIVIDUAL FINANCIAL STRENGTH ASSESSMENT (IFSA)

The IFSA reflects Dagong Europe’s evaluation of the stand-alone, intrinsic financial health of

an entity based solely on its financial fundamentals, business model and operating

environment. The IFSA is directly comparable with other entities within the financial industry

since it does not include any adjustments related to external support (government, parent

company or any other source).

The IFSA is mainly applicable to a business model of ‘traditional commercial banking’ (defined

as a combination of corporate and retail business as earnings generators) as it represents the

most traditional form that a financial institution would take to enter a market. Nevertheless,

the IFSA takes into consideration the differences in business models, evaluating the

complexity and target markets of each entity. Dagong Europe assesses whether the business

nature of the entity is accurately represented by standard metrics. If this is not the case,

adjustments can be made to reflect the financial profile and risks that otherwise may not be

identified.

The IFSA is the first stage in Dagong Europe’s process of assigning a Credit Rating. It is worth

noting that the IFSA does not under any circumstance represent an ultimate indication of

default risk or severity of loss. The higher the IFSA score, the stronger the entity’s stand-alone

financial health and therefore ability to fulfill its financial commitments.

The IFSA is displayed by the following scale. With the exception of the IFSA of 'aaa' and

'cc/c/d', each IFSA can be modified by the addition of a plus or a minus, expressed as a (+)

or (-) respectively, indicating a higher or a lower IFSA within each category.

Exhibit 3: Definition of IFSA - Individual Financial Strength Assessment

aaa

“aaa” denotes the highest score in the individual financial strength

assessment, with excellent and strong indicators in all the factors that comprise the IFSA. Represents entities with solid and recognised successful business models supported by an excellent risk management framework. A sound capital base to support organic growth is also available. Entities are typically located in stable economic environments with highly efficient and predictable legal and regulatory frameworks.

aa

'aa' denotes very strong individual financial strength, with a combination of

excellent and sound indicators within the factors that comprise the IFSA. Represented by entities with solid and recognised successful business models supported by a very good risk management framework. A sound capital base to support organic growth is available. Entities in this category are typically located in stable economic environments with highly efficient and predictable legal and regulatory frameworks.

a

'a' denotes a strong individual financial strength assessment with a mixed

combination of good indicators within the factors that compose the IFSA. It represents entities with stable business models supported by good risk management frameworks. A healthy capital base to support organic growth is available. Entities are typically located in stable economic environments with efficient and fairly predictable legal and regulatory frameworks.

Financial Institutions

5 18 June 2013 Dagong Europe Proposed Criteria for Rating Financial Institutions

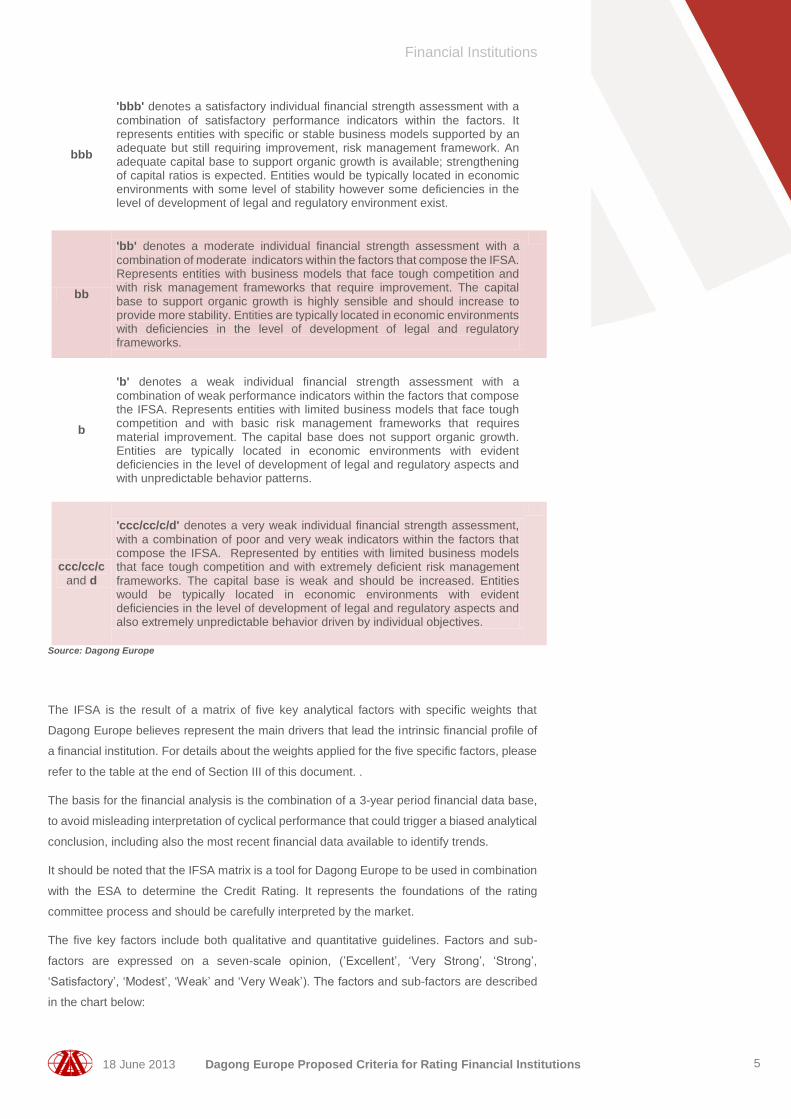

bbb

'bbb' denotes a satisfactory individual financial strength assessment with a

combination of satisfactory performance indicators within the factors. It represents entities with specific or stable business models supported by an adequate but still requiring improvement, risk management framework. An adequate capital base to support organic growth is available; strengthening of capital ratios is expected. Entities would be typically located in economic environments with some level of stability however some deficiencies in the level of development of legal and regulatory environment exist.

bb

'bb' denotes a moderate individual financial strength assessment with a

combination of moderate indicators within the factors that compose the IFSA. Represents entities with business models that face tough competition and with risk management frameworks that require improvement. The capital base to support organic growth is highly sensible and should increase to provide more stability. Entities are typically located in economic environments with deficiencies in the level of development of legal and regulatory frameworks.

b

'b' denotes a weak individual financial strength assessment with a

combination of weak performance indicators within the factors that compose the IFSA. Represents entities with limited business models that face tough competition and with basic risk management frameworks that requires material improvement. The capital base does not support organic growth. Entities are typically located in economic environments with evident deficiencies in the level of development of legal and regulatory aspects and with unpredictable behavior patterns.

ccc/cc/c and d

'ccc/cc/c/d' denotes a very weak individual financial strength assessment,

with a combination of poor and very weak indicators within the factors that compose the IFSA. Represented by entities with limited business models that face tough competition and with extremely deficient risk management frameworks. The capital base is weak and should be increased. Entities would be typically located in economic environments with evident deficiencies in the level of development of legal and regulatory aspects and also extremely unpredictable behavior driven by individual objectives.

Source: Dagong Europe

The IFSA is the result of a matrix of five key analytical factors with specific weights that

Dagong Europe believes represent the main drivers that lead the intrinsic financial profile of

a financial institution. For details about the weights applied for the five specific factors, please

refer to the table at the end of Section III of this document. .

The basis for the financial analysis is the combination of a 3-year period financial data base,

to avoid misleading interpretation of cyclical performance that could trigger a biased analytical

conclusion, including also the most recent financial data available to identify trends.

It should be noted that the IFSA matrix is a tool for Dagong Europe to be used in combination

with the ESA to determine the Credit Rating. It represents the foundations of the rating

committee process and should be carefully interpreted by the market.

The five key factors include both qualitative and quantitative guidelines. Factors and sub-

factors are expressed on a seven-scale opinion, (’Excellent’, ‘Very Strong’, ‘Strong’,

‘Satisfactory’, ‘Modest’, ‘Weak’ and ‘Very Weak’). The factors and sub-factors are described

in the chart below:

Financial Institutions

6 18 June 2013 Dagong Europe Proposed Criteria for Rating Financial Institutions

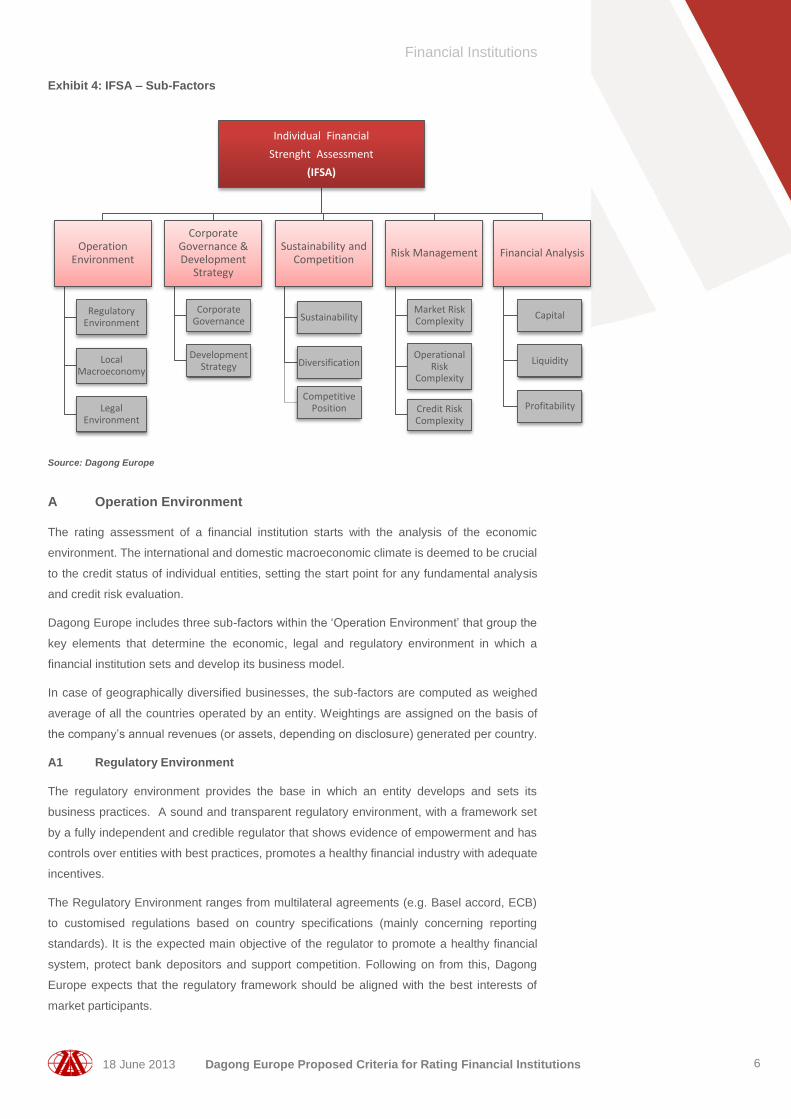

Exhibit 4: IFSA – Sub-Factors

Source: Dagong Europe

A Operation Environment

The rating assessment of a financial institution starts with the analysis of the economic

environment. The international and domestic macroeconomic climate is deemed to be crucial

to the credit status of individual entities, setting the start point for any fundamental analysis

and credit risk evaluation.

Dagong Europe includes three sub-factors within the ‘Operation Environment’ that group the

key elements that determine the economic, legal and regulatory environment in which a

financial institution sets and develop its business model.

In case of geographically diversified businesses, the sub-factors are computed as weighed

average of all the countries operated by an entity. Weightings are assigned on the basis of

the company’s annual revenues (or assets, depending on disclosure) generated per country.

A1 Regulatory Environment

The regulatory environment provides the base in which an entity develops and sets its

business practices. A sound and transparent regulatory environment, with a framework set

by a fully independent and credible regulator that shows evidence of empowerment and has

controls over entities with best practices, promotes a healthy financial industry with adequate

incentives.

The Regulatory Environment ranges from multilateral agreements (e.g. Basel accord, ECB)

to customised regulations based on country specifications (mainly concerning reporting

standards). It is the expected main objective of the regulator to promote a healthy financial

system, protect bank depositors and support competition. Following on from this, Dagong

Europe expects that the regulatory framework should be aligned with the best interests of

market participants.

Individual Financial

Strenght Assessment

(IFSA)

Operation Environment

Regulatory Environment

Local Macroeconomy

Legal Environment

Corporate Governance & Development

Strategy

Corporate Governance

Development Strategy

Sustainability and Competition

Sustainability

Diversification

Competitive Position

Risk Management

Market Risk Complexity

Operational Risk

Complexity

Credit Risk Complexity

Financial Analysis

Capital

Liquidity

Profitability

Financial Institutions

7 18 June 2013 Dagong Europe Proposed Criteria for Rating Financial Institutions

As a consequence of the recent financial crisis, Dagong Europe strongly focus on the

regulatory standards for liquidity management and the minimum standards applied. Dagong

Europe places a high value on the implementation of close liquidity controls within the

regulatory framework.

Financial institutions with an approved ‘Banking License’, are subject to more specific

regulatory standards and ongoing supervision. Ready access to central bank lending or

refinancing facilities provides a certain level of protection to creditors. Nevertheless, financial

institutions without a ‘Banking License’ can have similar control mechanisms and advantages

depending on their regulatory status and country-specific enforcement, which are been

considered within the analysis.

For financial institutions that have operations or business lines in more than one country, the

regulatory framework that applies for the purpose of analysis is taken from the country in

which the entity has its home operations. If operations in other countries are relevant (in terms

of earnings contribution, or assets, depending on disclosure), the analysis includes an

assessment of the regulatory framework of the secondary country as well. Dagong Europe

notes that for certain financial institutions (typically large and systemically important

institutions) a more and more consolidated analysis on the regulatory framework can be

applied.

The Regulatory Environment is determined by a seven-point qualitative opinion from

’Excellent’ to ‘Very Weak’.

A2 Local and Macro-Economy

The importance of local and macro-economic conditions is directly correlated to the

performance of the financial industry. Due to the nature of the financial industry, the state of

the local and macro economy has direct effects on the demand for financial services and thus

the ability of market players to generate earnings.

The analysis and assessment of a country’s economy is a key driver for the expected

performance of a financial institution. In addition, economic cycles can have strong effect on

asset evaluation, with an impact on the valuation of financial institutions valuation balance

sheets. The economic flexibility of a country determines how easily it can navigate through

potential imbalances but it is also important in terms of the tools it can use to mitigate any

external economic turmoil or crisis that could affect the local economy. Dagong Europe

evaluates the health of the economy through the following macro indicators:

GDP change (last full year or most recent data related to analysed results), which

represents the market attractiveness in terms of economic growth and potential.

CPI average last year (or most recent year average related to analysed results), which

represents price of money and provides an indication of the stability of costs.

Unemployment rate (last full year or most recent data related to analysed results), which

indicates the prospective strength of the economy in terms of potential purchasing power

and size of the population with real disposable income.

A3 Legal Environment

The Legal Environment is a key factor in setting the operational framework of financial

markets. A well-established and proven legal framework, with clear legal procedures, ability

Financial Institutions

8 18 June 2013 Dagong Europe Proposed Criteria for Rating Financial Institutions

to enforce contracts and predictable foreclosure times is vital to allow for a smooth operating

environment for financial market participants. Especially when assets are non-performing,

each country’s legal framework affects directly an institution’s business model and therefore

the standard for credit risk related expenses and losses for non-performing assets.

Dagong Europe evaluates and compares the strengths and weaknesses of the legal

framework of each country along the above described characteristics. The score on Legal

Environment is determined by a seven-point scale based on a qualitative opinion ranging from

’Excellent’ to ‘Very Weak’.

B Corporate Governance and Development Strategy

B1 Corporate Governance

The assessment of a financial institution’s governance framework is an important factor in

determining the quality of management, the fulfillment and predictability of the strategic plan

and long term performance. It therefore effects the financial stability of an entity. Since the

approach to Corporate Governance can be very different depending on the ownership

structure of an entity, the qualitative judgment made by Dagong Europe takes into account

also the complexity of the ownership structure.

The assessment includes an opinion on how the entity manages its relationship with all

stakeholders including shareholders, financial markets, regulatory entities, employees and

any other relevant parties. A review of the entity’s own definition, procedures, internal policies

and business practices is key to understanding and identifying potential risks from lack of

governability or management weaknesses.

Dagong Europe’s opinion on Corporate Governance is defined as a qualitative score that is

‘Neutral’, ‘Weak’ or ‘Very Weak’. The rationale behind this qualitative opinion is based on the

fact that Corporate Governance should be a minimum standard of best practices in every

financial institution. Dagong Europe gives no credit to strong Corporate Governance

frameworks, since it represents a minimum level of professionalism and responsibility for each

analysed entity. There is a negative stance for those frameworks that in Dagong Europe’s

opinion are not compliant with minimum industry standards and therefore represent a flaw

that could lead to potential governance risks. A comprehensive list of questions and topics

that are usually discussed when evaluating Corporate Governance are:

Composition of the board of directors/supervisory board and background.

Concentration of power for decision making processes.

How are strategy and objectives communicated within the organisation and how

aligned are they within the organisational structure.

Is risk tolerance appetite clearly determined and communicated?

How is the risk management function structured and managed?

How experienced is senior management?

Are internal procedures and practices clearly defined, communicated and applied?

What has been the outcome of the last inspection by the regulator/central bank?

Complexity of the ownership structure.

Financial Institutions

9 18 June 2013 Dagong Europe Proposed Criteria for Rating Financial Institutions

Structure of the management compensation packages. Are the incentives for

management compensation aligned with a sustainable long-term perspective of the

institution?

Quality of reporting, controls and monitoring from the board to management level.

Detailed explanation for any legal or regulatory disputes.

Any compliance breach, exception, or fine from a regulatory institution.

Sizable related-party lending.

As part of the Corporate Governance assessment, Dagong Europe also highlights the

importance of financial reporting in terms of quality, transparency and timing. The disclosure

of financial information of poor quality that lacks transparency or is published late is viewed

by Dagong Europe as a weak form of Corporate Governance.

Dagong Europe applies a -1 notch adjustment for ‘Weak’ Corporate Governance structures

and a -3 notch adjustment on ‘Very Weak’ Corporate Governance structures on the final IFSA

level. As mentioned above, a ‘Neutral’ assessment does not alter the IFSA.

B2 Development Strategy

The analysis of the development strategy of any financial institution ranges from a basic

review of the organisational structure to a more in depth analysis of the management skills

and ability to fulfill the strategic plan and focus on the long-term sustainability of the business

model.

In any business model, the business philosophy and strategy plays a key role in determining

the long term objectives and risks that the management is willing to undertake in order to

achieve the strategic goals. It is important that the management’s philosophy and actions

provide realistic strategies that reflect the real competitive advantages and disadvantages of

an entity. Unrealistic expansionary strategies may lead to pressure, relaxing credit risk

controls and unnecessarily increasing the entity’s overall risk appetite, misaligning the real

performance from approved policies. On the other hand, an overly conservative management

strategy may result in missed business opportunities and reduced competitive strength in the

long term.

A comprehensive analysis of management’s ability to implement the business strategy and

its competency in achieving it are fundamental to Dagong Europe. As a key tool to analyse

the quality of management, Dagong Europe will request access to the entity’s specific

management reporting system and reports to address the soundness of the information and

data shared for decision-making purposes.

The analysis of the growth strategy also includes any merger and acquisition (M&A) process

put in place. It is well known that M&A involve risks that are sometimes difficult to identify. The

success and value creation through M&A depends heavily on an adequate strategic fit of the

merging entities.

Management's business decisions and plans for poorly performing business units or those

that no longer make strategic sense represent another relevant area for analysis. Objective

appraisals of businesses units and disciplined approaches in dealing with underperformers

(divestiture, restructuring, discontinuation etc.) are reviewed.

Financial Institutions

10 18 June 2013 Dagong Europe Proposed Criteria for Rating Financial Institutions

The score on Development Strategy is determined by a seven-point qualitative opinion scale

ranging from ’Excellent’ to ‘Very Weak’.

C Sustainability and Competition

Sustainability and Competition factors are material to help an entity to position itself within the

competitive environment and develop a successful business strategy. The ability of an entity

to scale its operation and gain a stable market share provides a basis for long-term earnings

and therefore financial sustainability.

Additionally, Sustainability and Competition factors includes a quantitative evaluation that

helps to support and confirm the ability of an entity to maintain its long-term solvency and

competitive position. For Sustainability and Competition, Dagong Europe analyses the

following sub-factors:

C1 Sustainability

The sustainability of the business model sets a base for any projection and predictability of

performance. The ability of an entity to overcome market distresses is based on its

sustainability and stability of earnings generated through a healthy business model. It is noted

that traditional banking models have proven to be more stable, with a more predictable

performance throughout cycles. They have demonstrated to be better preserved from event

risk and large one-off extraordinary expenses. Dagong Europe's values the 'simple' or so

called ‘traditional banking’ model, with e.g. high net interest earnings proportion and loan and

deposit dominant balance sheets. In Dagong Europe’s view a sustainable and traditional

banking model could provide a higher level of protection to creditors in the long-term.

The quantitative measures used to identify an entity’s business model sustainability are:

Revenues Structure: Net Interest Income to Total Revenues – 3 year average

including year-to-date data

Balance Sheet Structure 1: Stable Funding1 to Total Funding – 3 year average

including year-to-date data

Balance Sheet Structure 2: Gross Loans to Total Assets – 3 year average including

year-to-date data

C2 Diversification

Diversification is an important factor to be considered in the analysis of any financial institution.

Regional, industry and income diversification can decrease dependence on the performance

of a specific market and improve the ability of an entity to face any distressed conditions on

isolated markets or business segments.

Diversification can add more stability and therefore be viewed as a strength or add volatility

and be viewed as a weakness. This is related to the nature of the diversification, the ability of

1 Stable funding includes typically deposit and long-term market funding facilities (with more

than 7 years residual maturity). Dagong Europe in certain instances adjusts the composition of stable funding. However, this adjustment is clearly specified and analysed accordingly.

Financial Institutions

11 18 June 2013 Dagong Europe Proposed Criteria for Rating Financial Institutions

the entity to manage that diversification and finally, the overall contribution of that

diversification to the entity’s consolidated business model.

The development of business segments that are not of the expertise of an entity, or that are

in markets that require high investment or large business intelligence to be successfully

developed, could be viewed as a potential weakness instead of a business opportunity.

On the other hand, a reasonable or strong diversification rationale and model would be one

in which an entity is able to either develop a franchise simultaneously and successfully in a

different country (or countries), or develop different business lines. This is proven as a factor

of mitigation in terms of financial performance helping to overcome different economic cycles

or specific business risks.

Dagong Europe analyses and reviews in detail the nature of the diversification and the

expertise of the entity in terms of market and business model, to fairly assess the

diversification effect.

In order to analyse an entity’s ‘Diversification’, Dagong Europe sets a qualitative opinion that

is be ‘Neutral’, ‘Weak’ or ‘Very Weak’. The rationale behind this qualitative opinion is based

on the fact that, despite that diversification can be very positive for some entities, it is more

reasonable to adjust the IFSA for the lack of diversification than give benefit from it.

Dagong Europe applies a -1 notch adjustment for ‘Weak’ Diversification and a -3 notch

adjustment on ‘Very Weak’ Diversification on the final IFSA. As mentioned above, a ‘Neutral’

assessment does not alter the IFSA.

C3 Competitive Position

The ability of a financial institution to develop a competitive advantage provides a basis to

generate stable profits and above average returns. In that context, an entity should carefully

manage and monitor the competitive environment to foresee the effects that any competitive

change would have on its business model and therefore, competitive position. The competitive

advantages can be a result of an internal strength or an external factor that allows the entity

to provide a distinctive product or service. A sound and recognised franchise is more stable

in times of financial stress, due to some benefit from the loyalty and preference of customers

and debt counterparties. However, this is dependent on the level of financial or economic

stress that affects the market or the entity in particular.

The score on Competitive Position is determined by a seven-point qualitative opinion scale

ranging from ’Excellent’ to ‘Very Weak’.

D Risk Management

For Dagong Europe, ability, expertise and a proven record of successful risk management is

a key qualitative factor for the IFSA. The ability of a financial institution to generate revenues

under a solid risk management framework is analysed and challenged. The business model

that financial institutions undertake carry credit, market and operational risks that need to be

managed well in order to provide profitability which needs to be properly adjusted based on

the identified risk appetite. Since the overall profitability that financial institutions achieve is

Financial Institutions

12 18 June 2013 Dagong Europe Proposed Criteria for Rating Financial Institutions

mostly determined by the level of risks accepted and rejected, the management of risks is

expected to be economically profitable and controlled accordingly.

The analysis of the management framework to monitor and control risks is assessed in the

business context the entity is set for. The coherence of the risk management framework with

the business model is the starting point for the analytical opinion. In this context, Dagong

Europe assesses the complexity of risk components managed by financial institutions

separately based on its nature: Market, Operational and Credit.

D1 Market Risk Complexity

The potential consequences of poor market risk management on an institution’s balance sheet

and financial profile of an entity can be significant. Dagong Europe follows a comprehensive

approach to understand and analyse each specific market risk framework from a qualitative

to a quantitative perspective.

The importance of the assessment of risk appetite, incentives and review of the practical

application of the framework are vital in assessing the complexity of market risks. In addition,

returns obtained from activities with market risk is a driver in determining the importance of

these risks on the entity’s overall IFSA.

The entity’s reporting of market risk, sensitivity analysis, stress testing tools and results is data

upon which the market risk complexity is assessed. The opinion is based on a qualitative

score of seven categories from ‘Excellent’ to ‘Very Weak’. There is no quantitative ratios

applied to market risk due to the vast diversity of models and tools used by entities depending

upon their complexity levels.

D2 Operational Risk Complexity

Due to the complexity of services provided by financial institutions and the volume and amount

of transactions involved, operational risk can cause great damage to the financial profile, in

both monetary and non-monetary terms. Operational risks could not only lead to unexpected

losses in financial statements but also regulatory fines, credibility loss, legal litigations or other

intangible brand damage. These could in turn result in a decrease in customer base and also

debt counterparties being reluctant to provide funding, dramatically affecting the scale of

operation of an entity.

There is no quantitative ratios applied to Operational Risk due to the vast diversity of models

and tools used by entities depending on their complexity levels, regulatory frameworks and

specific needs. Nevertheless, the approach takes into account the amount of capital available

(buffer) to cover any unexpected losses from Operational Risk and any other internal measure

that the management uses for that topic. In addition, Operational Risk assessment is

evaluated in the context of the business model complexity.

Dagong Europe’s opinion on Operational Risk complexity is based on a qualitative score of

seven categories from ‘Excellent’ to ‘Very Weak’.

D3 Credit Risk Complexity

For financial institutions, the key driver for recurrent earnings comes primarily from lending

activities, which commonly represent the largest portion of assets. The large size of loan

portfolios gather a variety of credit counterparties in nature, industries, loan specifications etc.

Financial Institutions

13 18 June 2013 Dagong Europe Proposed Criteria for Rating Financial Institutions

In that context, the quality of the loan portfolio represents a key driver on the financial profile

and earnings prospect of any entity.

An entity’s credit risk appetite represents the starting point of the analysis. Dagong Europe

discusses and reviews an entity’s credit risk policies in order to obtain an understanding and

the rationale for any lending decision. The analysis of credit operations and risk management

processes provides a basis for comparison with peer and industry benchmarks. This allows

Dagong Europe to identify whether an entity is aligned with best practices, regulation or any

other business approach in its development of credit activities.

The analysis includes a review of the entity’s credit policies and standards, collaterals,

management of recoveries and other related matters on loan write-offs policies.

Recent events in several European countries have shown how high borrower or industry

concentration can cause large charge-offs, and finally a deterioration of capital. Therefore, an

adequately diversified and granular credit portfolio is an indicator of reasonable credit risk

management that can help to reduce and mitigate credit losses. This is also related to large

exposures on specific industries, countries or any other niche heavily dependent on market

trends or economic conditions.

It is worth noting that although credit risk diversification can reduce the effect of a deterioration

of specific counterparties on the loan portfolio, in cases of economic downturn, typically the

loan portfolio as a whole is adversely affected. In those cases, it is necessary to carefully

analyse the macro-context and the ability of each entity to successfully overcome the

economic scenario with limited shocks on asset quality. Understanding the cause of credit

losses is a powerful tool in evaluating the expected performance of an entity’s asset quality.

Benchmarking and peer comparison allows Dagong Europe to identify the complexity and

specific characteristics that apply for each entity and therefore the expected asset quality

stresses under different economic scenarios.

In order to evaluate the composition of the loan book in more detail, Dagong Europe requires

detailed information on the most relevant large credit exposures (or borrowers) including

ratings, guarantees (and some transaction specific conditions if applicable), data on industry

exposure, concentration by lending products and any other additional data the agency

considers relevant for analytical purposes.

The opinion regarding credit risk complexity is based on a qualitative score of seven

categories ranging from ‘Excellent’ to ‘Very Weak’. Quantitative ratios enhance comparability

and complete Dagong Europe’s view on Credit Risk Complexity. The ratios used to measure

credit risk are:

Non-Performing Loans to Total Gross Loans2 - most recent year or year-to-date

data

Loan Loss Coverage (Loan Loss Reserves to Non-Performing Loans) - most recent

year or year-to-date data

2 Only includes on balance data of the loan portfolio, any information on off-balance data is

analysed and included in the stress test.

Financial Institutions

14 18 June 2013 Dagong Europe Proposed Criteria for Rating Financial Institutions

E Financial Analysis

The last component of the IFSA is focused solely on financial analysis, and includes a detailed

view on Capital, Liquidity and Profitability. This analysis provides a set of ratios to assess the

financial soundness of each entity, which is then used also for peer comparison.

A sound financial profile which can withstand also economic cycles is the basis for an entity’s

healthy and sustainable overall profile. The assessment of operating performance, balance

sheet strengths and weaknesses, capital and liquidity positions represent key drivers for long

term solvency prospects. Thus, Dagong Europe has divided the analysis into three sections:

Capital, Liquidity and Profitability.

E1 Capital

Capital is fundamental for the financial stability of any financial institution. It is the most certain

source of funds to absorb potential and unexpected losses when earnings are weak or

nonexistent, independently of their origins (credit, market and operational). It represents the

sole source of funding which is completely reliable in supporting any organic growth

expansion.

Dagong Europe reviews the composition of an entity’s capital base, the tools the management

has in place to control and review capital needs and the internal limits and minimum capital

levels that it tolerates within its business cycles. Dagong Europe regards an entity’s minimum

internal capital limits as an important indication of risk tolerance and ability to manage the

capital adequacy under tight financial scenarios.

Dagong Europe analyses capitalisation in the context of an entity’s risk profile. As such, when

assessing an entity’s capitalisation level, Dagong Europe distinguishes between Group 1,

Group 2, and Group 3 financial institutions. Group 1 includes financial institutions which qualify

for high or very high National Systemic or Supranational Support expectations under Dagong

Europe ESA framework (details under Section IV - External Support Assessment). Financial

institutions in Group 2 have a highly sustainable and stable business model (as described

under ‘Sustainability’) and Group 3 includes all other financial institutions. Dagong Europe

requests Group 1 entities to have higher capitalisation than Groups 2 and 3. In line with

regulators and market participants, Dagong Europe endorses systemically important financial

institutions to carry higher capital ratios. For Group 2 institutions - with traditional business

models which have proven to be more resilient to the multiple challenges of the financial crisis

– a less conservative capital assessment is applied than for Group 1 and Group 3 entities.

In addition to the common Tier 1 ratio to assess an institution’s capitalisation, Dagong Europe

analyses the so-called ‘Leverage’ ratio (Shareholder’s Equity to Total Assets). The risk-

weighting of assets can vary significantly, even between institutions with similar risk and asset

profile. This can be due to different regulatory frameworks on risk-weighting applications, or

for example variation in business sophistication of the institution. In order to compare

institutions true capital base – available to cover for losses – the Leverage ratio appears for

Dagong Europe as an effective measure.

Capital is an immediate buffer to mitigate financially distressed scenarios but if management

does not prospectively identify the risks held in the balance sheet, no matter the capital level

kept by an entity, the effect on the financial profile can be material.

Financial Institutions

15 18 June 2013 Dagong Europe Proposed Criteria for Rating Financial Institutions

On the other hand, in periods of economic growth and subsequent expansion of assets,

financial institutions are usually tempted to finance this growth through debt, increasing

leverage. In that context, the analysis of balance sheet growth in terms of quality, stability and

funding mix is be addressed carefully.

In terms of capital adequacy analysis, the ability that financial institutions have to obtain

additional capital if necessary, it is also important. In general, financial institutions have two

sources to obtain capital: (a) earnings generation, and (b) external capital injections.

a. The ability of an entity to generate positive and consistently growing earnings and retain

them in the balance sheet, through dividend payout ratios that allow sound and stable

capital growth, is the most valuable source of capital. Adequate management of risk-

adjusted returns, which is aligned with stakeholder expectations facilitates earnings

retention. If profitability is weak and risk-adjusted return levels are not in alignment with

the expected financial profile of an entity, stakeholders could demand additional

compensations and therefore reduce the internal capital growth level with high dividend

payouts.

b. In terms of external capital injections, the ability to raise capital could come from external

and new stakeholders through stock issuances or from current stakeholders through

capital injections.

Financial institutions can choose any alternative based on their own needs and specifications.

The timing and ability to obtain capital when needed without adding extra distress to the

financial profile should be the key factor in the choice of the source of capital. The ratios that

Dagong Europe uses to assess Capital strength of any financial institution are:

Tier I Capital Ratio - most recent year or year-to-date data

Leverage Ratio (Shareholder’s Equity to Total Assets) - most recent year or year-to

date data

E2 Liquidity

Solvency is highly correlated with liquidity issues, including the concept of ‘market contagion’

that could result from the financial instability of even a small and isolated entity, affecting to

the largest and more solid franchise. Dagong Europe requires entities to demonstrate their

ability to manage liquidity shortfalls under stressed economic scenarios.

Dagong Europe gives special attention to the Liquidity Management framework (promoted by

Basel III), including not only a qualitative analysis of liquidity plans (under contingency and

normal scenarios), but also gaining an understanding of the historical liquidity dynamics that

an entity has faced during economic cycles.

The liquidity scenario at a market or country level, is key to determining the ability of financial

institutions to manage their funding structure, moving from more liquid positions in the short

term to more stable funding structures targeting the long term. The access to central bank

funding or any other liquidity sources is analysed accordingly and in the context of economic

conditions. For Dagong Europe, sound liquidity management is supported by a reasonable

and equilibrated funding structure, with no overdependence on specific funding sources.

Financial Institutions

16 18 June 2013 Dagong Europe Proposed Criteria for Rating Financial Institutions

To complement the view on liquidity, Dagong Europe also considers the structure of funding

and how an entity maintains ongoing renewal. The analysis is focused on reviewing the

deposits base, interbank loans, capital market funding, central bank funding and any other

sources of funding available, if relevant.

In addition, it is important to identify regulatory measures put in place to prevent financial

institutions (particularly banks) to face uncontrolled liquidity stresses. The analysis includes

the differentiation and special conditions available (central bank funding) for specific entities

(banks in most cases) and for other non-banking institutions.

Market access for financial institutions and respective pricing continues to be linked across

most jurisdiction, given the on-going market perception of consolidated financial institutions

and country specific risk. As such Dagong Europe’s liquidity analysis is complemented with a

sovereign market indicator. The ratios that Dagong Europe uses to assess liquidity are:

Gross Loans to Deposits – 3 year average including year-to-date data

Deposits to Total Funding – 3 year average including year-to-date data

Market Access Ability (government bond 10-year rate) - most recent full year average

or year-to-date data if representative

E3 Profitability

The ability of an entity to generate and maintain strong, sustainable and stable earnings is

key to the continuity of the operation and long-term solvency. A detailed analysis of

profitability, including key business activities, sources and composition, allows the

identification of the stability and predictability of earnings. There is a given attention to those

entities in which the business model could lead to volatile earnings. In addition, the strength

of a traditional lending model with a high component of earnings from interest (mainly from

the loan book) is also highlighted in this analysis. Depending on the business model, core

earnings are identified and analysed. A business model that lacks stable core earnings is

more exposed to market and economic volatilities and therefore compares poorly with peers

that generate higher and more stable core earnings.

A deviation from the defined business model, to obtain ‘one-off’ earnings or to take

advantages of market momentums is not be considered as positive within the profitability

analysis. In fact, Dagong Europe on a case-by-case basis may adjust net income for extra-

ordinary items. In order to evaluate an entity's recurring profitability. Items that are unusual in

nature and infrequent may be deducted or added to net income for that purpose.

Data used for profitability ratios is based on the average for the last three years in order to

smooth for exceptional performances given economic cycles. The ratios that Dagong Europe

uses to assess ‘Profitability’:

Income before Provisions to Loan Loss Provisions – 3 year average including

year-to-date data

Return on Average Risk Weighted Assets – 3 year average including year-to-date

data

Income before Provisions to average Total Assets – 3 year average including year-

to-date data.

Financial Institutions

17 18 June 2013 Dagong Europe Proposed Criteria for Rating Financial Institutions

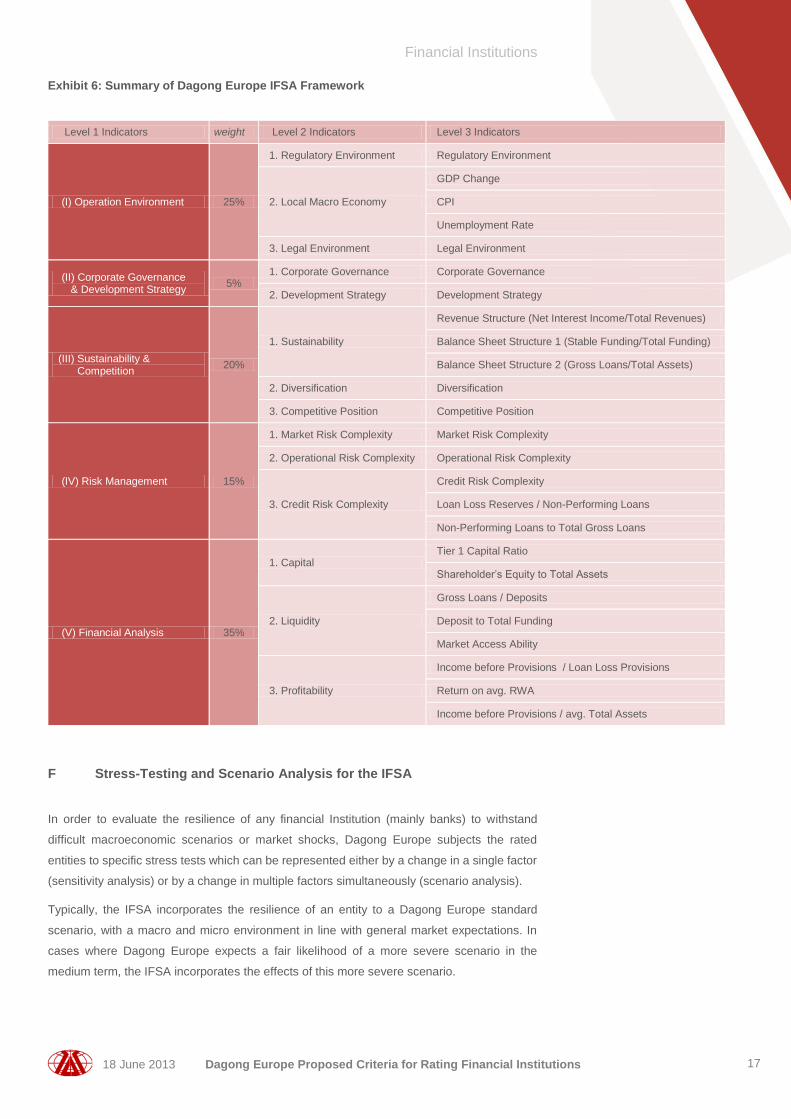

Exhibit 6: Summary of Dagong Europe IFSA Framework

Level 1 Indicators weight Level 2 Indicators Level 3 Indicators

(I) Operation Environment 25%

1. Regulatory Environment Regulatory Environment

2. Local Macro Economy

GDP Change

CPI

Unemployment Rate

3. Legal Environment Legal Environment

(II) Corporate Governance & Development Strategy

5% 1. Corporate Governance Corporate Governance

2. Development Strategy Development Strategy

(III) Sustainability & Competition

20%

1. Sustainability

Revenue Structure (Net Interest Income/Total Revenues)

Balance Sheet Structure 1 (Stable Funding/Total Funding)

Balance Sheet Structure 2 (Gross Loans/Total Assets)

2. Diversification Diversification

3. Competitive Position Competitive Position

(IV) Risk Management 15%

1. Market Risk Complexity Market Risk Complexity

2. Operational Risk Complexity Operational Risk Complexity

3. Credit Risk Complexity

Credit Risk Complexity

Loan Loss Reserves / Non-Performing Loans

Non-Performing Loans to Total Gross Loans

(V) Financial Analysis 35%

1. Capital Tier 1 Capital Ratio

Shareholder’s Equity to Total Assets

2. Liquidity

Gross Loans / Deposits

Deposit to Total Funding

Market Access Ability

3. Profitability

Income before Provisions / Loan Loss Provisions

Return on avg. RWA

Income before Provisions / avg. Total Assets

F Stress-Testing and Scenario Analysis for the IFSA

In order to evaluate the resilience of any financial Institution (mainly banks) to withstand

difficult macroeconomic scenarios or market shocks, Dagong Europe subjects the rated

entities to specific stress tests which can be represented either by a change in a single factor

(sensitivity analysis) or by a change in multiple factors simultaneously (scenario analysis).

Typically, the IFSA incorporates the resilience of an entity to a Dagong Europe standard

scenario, with a macro and micro environment in line with general market expectations. In

cases where Dagong Europe expects a fair likelihood of a more severe scenario in the

medium term, the IFSA incorporates the effects of this more severe scenario.

Financial Institutions

18 18 June 2013 Dagong Europe Proposed Criteria for Rating Financial Institutions

The stress-test and scenario analysis of the IFSA takes into account idiosyncratic financial

stress, system wide financial stress and the combination of both. The stress-test and

sensitivity analysis are built to assess the impact of unexpected events or material changes

in economic trends on a financial institution’s capital, asset quality, liquidity and profitability.

While the risks which particular financial institutions and systems face can vary significantly

(country specific factors for example), Dagong Europe stress-test and sensitivity analysis are

built around four general pillars:

i. RWA Sensitivity Analysis: This is used to obtain an indication of the level of

vulnerability of capital and profitability ratios were risk-weighting on assets increased

proportionally - given for example regulatory interference or regulator instructed

calculation changes.

ii. Asset Quality and Concentration (by borrower and sector): A stress test on asset

quality (with concentrated borrower or sector credit defaults) is applied to analyse the

sensitivity of capital levels, taking into account though an entity’s standard earnings

generation. It gives an indication of the robustness of capital levels and earnings

capacity as well as an entity’s concentration levels.

iii. Profitability Volatility Analysis: This analysis assesses the predictability and stability

of both earnings and net income in previous years in the context of an institution’s

economic cycle. This analysis also gives an indication of an institution’s loan loss

provision expenditure management.

iv. Liquidity Gap Analysis: The aim of this analysis is to assess an institution’s resilience

and funding flexibility when facing unexpected liquidity stress-scenarios, e.g. material

deposit outflow, market closure, interbank funding constrains, reputational damage.

Dagong Europe applies the scenarios depending on the nature and base characteristics of

each operating environment and also on the unique characteristics of the financial institution

being analysed (e.g. business model, size, funding structure, interconnectedness). In addition,

special attention is given to the evolving context (e.g. business cycle, geographic operating

environment, regulatory changes, industry specifications) in order to identify the strength of

each entity to manage its financial position accordingly. The scenarios are based on those

most relevant to the specific institution or system. More severe scenarios reflect exceptional,

but plausible events highlighted by Dagong Europe as a fair analytical tool to determine the

soundness of each entity.

The scenario outcomes obtained help to analyse the level of resilience of each entity to face

financial distress and is therefore used in conjunction with the above described core analysis

obtained from the historical data to determine the IFSA. The clear rationale and fundamentals

of any IFSA is disclosed. If in any case the stress test and scenario lead to a perception of

evident weak financial position, the IFSA is representing it accordingly.

Financial Institutions

19 18 June 2013 Dagong Europe Proposed Criteria for Rating Financial Institutions

IV EXTERNAL SUPPORT ASSESSMENT (ESA)

For Dagong Europe, the External Support Assessment (ESA) is combined with the IFSA to

determine the final Credit Rating. The ESA is Dagong Europe’s opinion on the likelihood of

support from an identified ‘External Support Provider’. The support providers identified and

used by Dagong Europe are:

1. Cooperative/Mutualism

2. Parent / Holding Company

3. Local Government

4. National Systemic

5. Supranational

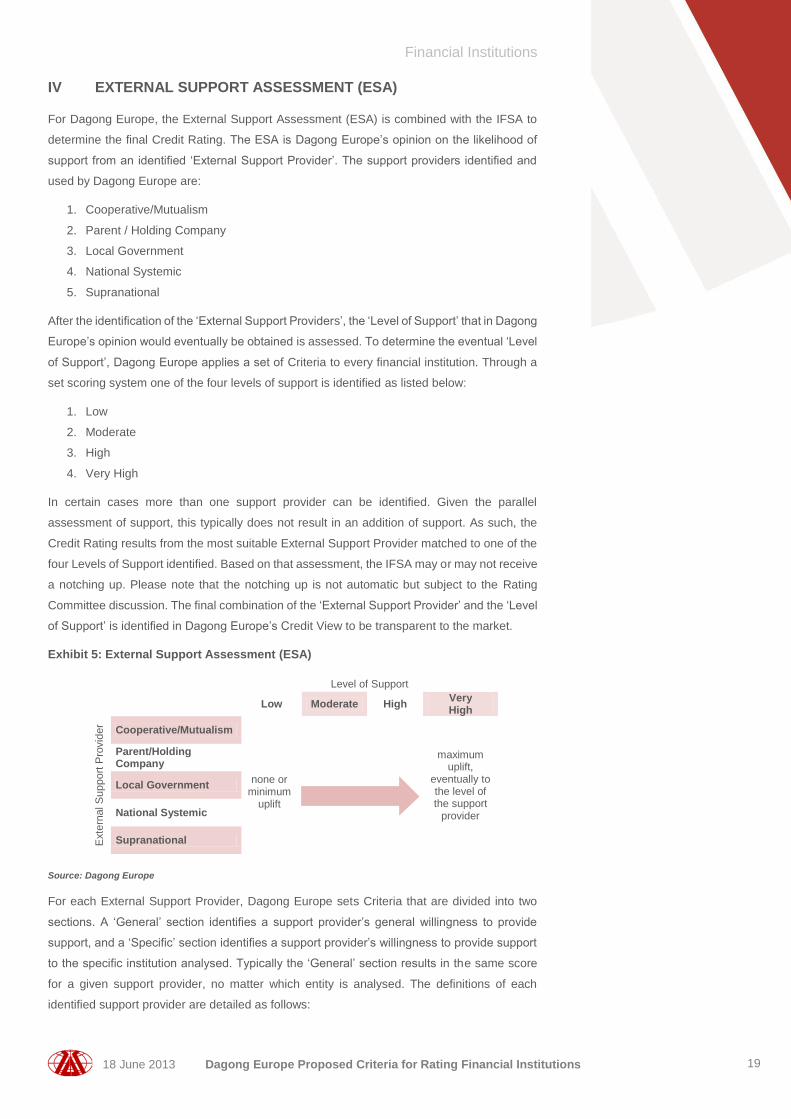

After the identification of the ‘External Support Providers’, the ‘Level of Support’ that in Dagong

Europe’s opinion would eventually be obtained is assessed. To determine the eventual ‘Level

of Support’, Dagong Europe applies a set of Criteria to every financial institution. Through a

set scoring system one of the four levels of support is identified as listed below:

1. Low

2. Moderate

3. High

4. Very High

In certain cases more than one support provider can be identified. Given the parallel

assessment of support, this typically does not result in an addition of support. As such, the

Credit Rating results from the most suitable External Support Provider matched to one of the

four Levels of Support identified. Based on that assessment, the IFSA may or may not receive

a notching up. Please note that the notching up is not automatic but subject to the Rating

Committee discussion. The final combination of the ‘External Support Provider’ and the ‘Level

of Support’ is identified in Dagong Europe’s Credit View to be transparent to the market.

Exhibit 5: External Support Assessment (ESA)

Level of Support

Low Moderate High

Very High

Exte

rnal S

upport

Pro

vid

er

Cooperative/Mutualism

none or

minimum uplift

maximum uplift,

eventually to the level of the support

provider

Parent/Holding Company

Local Government

National Systemic

Supranational

Source: Dagong Europe

For each External Support Provider, Dagong Europe sets Criteria that are divided into two

sections. A ‘General’ section identifies a support provider’s general willingness to provide

support, and a ‘Specific’ section identifies a support provider’s willingness to provide support

to the specific institution analysed. Typically the ‘General’ section results in the same score

for a given support provider, no matter which entity is analysed. The definitions of each

identified support provider are detailed as follows:

Financial Institutions

20 18 June 2013 Dagong Europe Proposed Criteria for Rating Financial Institutions

A Cooperative / Mutualism

Cooperative banking groups and mutualism mechanisms represent a very special type of

external support or solvency mechanism. In the case of cooperative banks, the support comes

from other members of the cooperative. Support coming from other members of the

cooperative is mainly a sort of intervention to avoid any reputational/business damages that

can cause contagion to the overall group of entities under the cooperative umbrella.

The support received can range from any sort of informal support to a more formalised and

structured legally binding support, which is addressed accordingly to determine the level of

support in each case. Dagong Europe evaluates the legal framework and the specifications

of the cooperative or mutualism mechanisms in place. The set of Criteria applied to assess

the Cooperative/Mutualism Support are described as follows:

a) General

Reporting (audited, consolidated report, periodically) - could increase support

considerations

Branding (identical branding, recognizable logo) - could increase support

considerations

Structure (highly centralized or highly standardized operations, operational

independence - could increase support considerations

Legal (charter, sanction rights) - could increase support considerations

Support functions in place (legal guarantee, fully paid in sizeable support fund) - could

increase support considerations

Operational independence (choice of their own funding, investments, etc.) - could

decrease support considerations

Bail out / Intervention History (existing) - could increase support considerations

b) Specific

Operational integration high (shared services, etc) - could increase support

considerations

Funding dependence high - could increase support considerations

Geographic correlation high - could increase support considerations

Business line correlation (same or important / or Central Institution) - could

increase support considerations

Relative size (of the analysed entity, cooperative / reputational importance) high - could

increase support considerations

B Parent / Holding Company

In cases in which the financial institution is part of a group, with a parent entity or holding

company, Dagong Europe firstly evaluates the existence of any form of guarantee or legal

obligation to support the subsidiary. In that case, due to the nature of the obligation to support,

the notching up of the entity’s credit rating could be up to the level of the parent or holding

company.

It is worth noting that even though the parent company may not have any formal or explicit

commitment to support the operations of a subsidiary, Dagong Europe evaluates the strategic

Financial Institutions

21 18 June 2013 Dagong Europe Proposed Criteria for Rating Financial Institutions

importance of the subsidiary and the effects on the parent’s reputation and market confidence

if a potential default affects the operation. In that context, Dagong Europe uses the concept

of ‘strategic importance’ and considers giving uplift to the subsidiary’ IFSA based on the

financial strength of the parent. Although Dagong Europe evaluates prospectively the eventual

support from parent entities, the track record and past examples of support highlighted during

past crisis is considered a key element. The set of Criteria applied to assess the

Parent/Holding Company Support are described as follows:

a) General

Bailout history (existing) - could increase support considerations

Ultimate parent credit rating high - could increase support considerations

b) Specific

Ownership Structure (government / state owned, branch, subsidiary)

Guarantees (implicit / explicit)

Strategic Importance high (brand sharing / revenues / assets / region) - could increase

support considerations

Operational integration high - could increase support considerations

Reputational risk high - could increase support considerations

Operation Environment different - could decrease support considerations

In special cases in which the subsidiary has a stronger IFSA than the parent, the support

provided by the parent /holding company is evaluated carefully and on a case by case basis.

In these cases, Dagong Europe applies a judgment to evaluate the degree of connection and

dependence of both entities and therefore the correlation of both Credit Ratings.

C Local Government

In countries in which the financial system has a very specific role within the local economy,

there is empirical evidence of support from the Local Government. This is not recognisable in

all countries but some examples of Local Government support exist. The Criteria to identify

the potential of Local Government Support are similar and derived from the Criteria applied

for National Systemic Support, however limited to the extent of the specific local economy.

The set of Criteria applied to assess the Local Government Support are described as follows:

a) General

Bailout History (existing) - could increase support considerations

Public Sentiment (favorable) - could increase support considerations

Legal Capacity (existing) - could increase support considerations

b) Specific

Reputational Risk (high) - could increase support considerations

Guarantee (existing) - could increase support considerations

Ownership (sizeable) - could increase support considerations

Financial Institutions

22 18 June 2013 Dagong Europe Proposed Criteria for Rating Financial Institutions

D National Systemic

Support from government has been historically proven. When the stability of the domestic

financial system is at risk, governments are willing to support financial institutions. However,

a government may be more willing to support those entities in which it has direct investment,

through different mechanisms such as direct cash and capital injections, liquidity facilities,

long term debt, subordinated debt provisions, guaranteed debt programs etc.

For systemically important financial institutions (mostly banks), the incentive for the

government to provide support is driven by the catastrophic consequences of a bank facing a

scenario of insolvency, with a direct effect on depositors and investor confidence, possible

contagion to the financial system and the real economy. In those cases, the support to

systemically important financial institutions comes from a desire to avoid any further damage

to capital markets and therefore macro-economic and social stability. It is worth mentioning

that in those cases in which Dagong Europe considers that the government does not have a

sound financial profile or enough resources to provide support if needed, the level of support

expected is adjusted accordingly.

In that context, Dagong Europe identifies those financial institutions (mostly banks) that can

be defined as systemically important and who are very likely to receive national support in

case of financial distress. The following Criteria are used by Dagong Europe to assess the

potential of National Systemic Support:

a) General

Banking system importance (Bank Assets / Total GDP sizeable) - could increase

support considerations

Bail out history (existing) - could increase support considerations

Legal capacity (existing) - could increase support considerations

Public sentiment (favorable) - could increase support considerations

Strength of banking system (weak) - could increase support considerations

b) Specific

Bank Importance / Substitutability (deposit share sizeable - could increase support

considerations, lending share sizeable - could increase support considerations, non-

national or extra-monetary union deposits sizeable - could decrease support

considerations, non-national or extra-monetary union lending sizeable - could

decrease support considerations)

Geographic diversity (low) - could increase support considerations

Payments, settlements services and similar (dominant player) - could increase support

considerations

Business Activity (traditional, monopole position, important niche player, important

capital market position) - could increase support considerations

Support due to capital short fall from regulatory requirements - could increase support

considerations; loan losses - could increase support considerations; fraud or similar -

could decrease support considerations; extra-national problems - could decrease

support considerations; issues from non-core operations - could decrease support

considerations.

State Guarantee

Financial Institutions

23 18 June 2013 Dagong Europe Proposed Criteria for Rating Financial Institutions

State Ownership

It is worth noting that Dagong Europe’s opinion on national systemic importance could differ

from the definition of systemic importance that a country could set for its domestic banks.

E Supranational Support

The interconnection and globalisation of financial markets highlights the critical issue of

globally systemically important financial institutions (not only banks) and the effects that

liquidity, capital erosion and lack of market confidence could cause to the overall financial

system. In addition, when governments are facing tight fiscal balances and deep crises in the

real economy, the ability to provide funds to support the needs of a stressed financial system

are fairly limited.

Dagong Europe evaluates supranational systemic importance of those entities and assigns

an ESA related to their importance. However, since the supranational support is mostly

triggered after all other external support providers are not available, the assessment for the

recognition of supranational support follows a dynamic approach. Dagong Europe expects to

apply the supranational support as an ultimate source of notching up, mainly to stabilise the

Credit Rating of the affected entity. Therefore, the supranational support sets the floor until

the rated financial institution recovers a relatively stable solvency level to continue operating.

The following Criteria are used by Dagong Europe to assess the potential of Supranational

Support:

a) General

Corruption Index3 (low) - could increase support considerations

Economic sector distribution / GDP (healthy) - could increase support considerations

EU / IMF Support Program approved - could increase support considerations

ECB / Central Bank cooperation (e.g. liquidity) - could increase support considerations

Country Strength (low) - could increase support considerations

b) Specific

Bank Importance / Substitutability (deposit share sizeable - could increase support

considerations, lending share sizeable - could increase support considerations)

Geographic Diversity (low) - could increase support considerations

Business Activity (traditional, monopolistic position, important niche player, important

capital market position) - could increase support considerations

Payments, settlements services and similar (dominant player) - could increase support

considerations

Support due to (capital short fall from regulatory requirements) - could increase support

considerations, (loan losses) - could increase support considerations, (fraud or similar)

- could decrease support considerations, (extra-national problems, procedure more

length/complex) - could decrease support considerations, (issues from non-core

operations) - could decrease support considerations

3 as per World Bank latest governance indicator

Financial Institutions

24 18 June 2013 Dagong Europe Proposed Criteria for Rating Financial Institutions

V OTHER CONSIDERATIONS FOR FINANCIAL INSTITUTIONS’

CREDIT RATINGS

A Reporting and Information Risk

Dagong Europe’s analysis and ratings rely on a wide range of information sources including

audited historical financial reports and legal documentation of credit facilities. In addition to

this, management information such as preliminary financial data, projections, scenario

analyses, liquidity and cash flow figures are also evaluated. Dagong Europe uses an entity’s

internal and external data, the latter provided by valid publically available sources of

information, to complement and verify validity, consistency and the rationale of the information

provided by the entity.

Dagong Europe always relies on audited financial statements and does not implement any

further audit or verification to the already-audited financial accounts. Consistency in

accounting policies and financial strategies is, however, always assessed in a critical manner

by the analytical team. Dagong Europe understands the importance of the information risk as

it significantly influences decisions on rating, including assignment, maintenance or

withdrawal. In cases where the information risk is so significant that it prevents a meaningful

analysis, Dagong Europe will decline to assign a credit rating, or where a credit rating is

already assigned, withdraw it.

Transparency and thorough reporting standards are fundamental to Dagong Europe credit

analysis and ratings. Dagong Europe recognises that lengthy reporting delays, material

restatements, inconsistencies and related investigations indicate poor quality of reporting.

Close attention must be given to any adverse developments such as regulatory challenges,

lawsuits, and challenges in capital markets or frequent auditor changes. Managements’

approach to resolution of these matters is also a pivotal part of the analysis.

B Financial Institutions Holding Companies

In the cases of pure holding companies within a group of financial institutions, for which cash

flows are represented mainly by dividends received from the operating subsidiary (a rated

financial institution), Dagong Europe analyses the holding either on a non-operating or

operating basis.

In the case of a non-operating holding, the initial anchor for the IFSA of the holding company

is the IFSA of the operating financial institution, notching down from it due to the lack of

independent earnings generation and dependency on dividends as the only income source.

Further notching down applies depending on the level of leverage and any lack of financial

flexibility of the holding company.

An operating holding could be rated at the same IFSA level as the operating subsidiary if it

has proven additional sources of earnings or cash e.g.:

(i) Significant investment assets (real estate, marketable securities) that can be

easily liquidated and transformed into an immediate source of cash.

Financial Institutions

25 18 June 2013 Dagong Europe Proposed Criteria for Rating Financial Institutions

(ii) Other important and significantly earning generator businesses that contribute

stable cash flows and help the holding company to keep a very flexible and

healthy financial position without over-dependency on one subsidiary only.

C Subsidiaries, Branches and other Vehicles

Large financial institutions usually keep small operations in non-core countries for special

purposes as alternative booking units, debt issuance or other reasons. In those cases, the

subsidiary (vehicle, or branch) is highly integrated with the parent, sharing IT, funding, risk

management operations and most core services. This makes the IFSA of the subsidiary (or

branch) highly dependent on the IFSA of the parent entity. Therefore, the IFSA of the

subsidiary is mostly likely at a similar level to the one of the parent entity, considering that

these subsidiaries have a limited independence and that decision-making processes and

operations are concentrated at the parent level.

The IFSA can instead differ from that of the parent in cases where the subsidiary (or branch)

is located in countries in which the jurisdiction differs substantially from that of the parent.

It is worth noting that Dagong Europe assesses these subsidiaries on a case by case basis in

order to clearly identify the potential risks or weaknesses that debt-holders could face within

those specific jurisdictions.

D Foreign Currency and Local Currency Ratings

Dagong Europe assigns ‘Foreign Currency’ ratings in cases in which the entity issues debt

instruments in a currency different from the local or domestic currency. However, those ratings

are not independent and are obtained through the ‘Local Currency’ rating. The debt

obligations that an issuer has in a ‘Foreign Currency’ are subject to notching adjustments

based on the access of the rated entity to the specific foreign currency. The adjustment also

takes into account the specific features of the foreign currency issuance and any other factor

that Dagong Europe considers could constrain the access to foreign currency and therefore

reduce the ability of the entity to fulfill its obligation accordingly.

In addition, a ceiling on the possible rating on ‘Foreign Currency’ applies if Dagong Europe

believes that the access to that currency is considerably restricted within the country in which

the entity operates or if there is a government restriction to access foreign currency in events

of financial distress. In those cases, the ‘Foreign Currency’ rating mostly follows the external

restrictions and therefore is not in alignment with the ‘Local Currency’ rating in place. The

difference in notching is analysed on a case by case basis, depending on the strength of the

rated entity is to ring-fence the specific ‘Foreign Currency’ debt obligation.

E Subordinated Debt Obligations

Subordinated debt instruments are notched down from the IFSA. Dagong Europe believes

that given ongoing promotion of overall burden sharing in case of distress by policy makers

and the political system, debt instruments should be notched down the individual financial

strength assessment, excluding any form of support. Debt instruments can be notched down

from the final Credit Rating (including the External Support Assessment – ESA) in exceptions

Financial Institutions

26 18 June 2013 Dagong Europe Proposed Criteria for Rating Financial Institutions

for certain state-owned financial institutions (mostly banks) and also in cases in which parental

linkages are strongly proven.

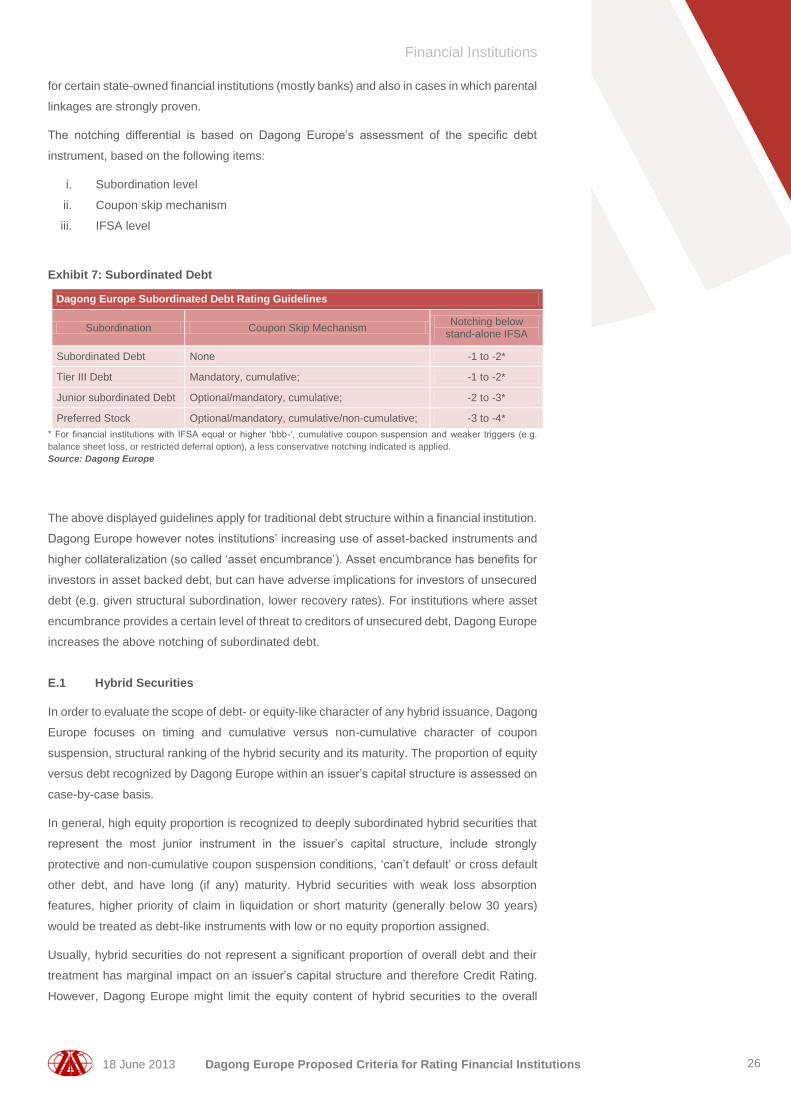

The notching differential is based on Dagong Europe’s assessment of the specific debt

instrument, based on the following items:

i. Subordination level

ii. Coupon skip mechanism

iii. IFSA level

Exhibit 7: Subordinated Debt

Dagong Europe Subordinated Debt Rating Guidelines

Subordination Coupon Skip Mechanism Notching below

stand-alone IFSA

Subordinated Debt None -1 to -2*

Tier III Debt Mandatory, cumulative; -1 to -2*

Junior subordinated Debt Optional/mandatory, cumulative; -2 to -3*

Preferred Stock Optional/mandatory, cumulative/non-cumulative; -3 to -4*

* For financial institutions with IFSA equal or higher ‘bbb-‘, cumulative coupon suspension and weaker triggers (e.g.

balance sheet loss, or restricted deferral option), a less conservative notching indicated is applied.

Source: Dagong Europe

The above displayed guidelines apply for traditional debt structure within a financial institution.

Dagong Europe however notes institutions’ increasing use of asset-backed instruments and

higher collateralization (so called ‘asset encumbrance’). Asset encumbrance has benefits for

investors in asset backed debt, but can have adverse implications for investors of unsecured