deliverable d8 (wp 6.1 report) - trimis.ec.europa.eu · technology opportunities and strategies...

TRANSCRIPT

Technology Opportunities and Strategies towards Climate friendly trAnsport

FP7-TPT-2008-RTD-1

Coordination and Support Action (Supporting)

Deliverable D8 (WP 6.1 report)

Scenarios of European Transport Futures in a Global Context

Ecorys

Robert Kok

Konstantina Laparidou

Adnan Rahman

University of Cambridge

Lynnette M. Dray

Dissemination level

Public PU X

Restricted to other programme participants (including Commission Services) PP

Restricted to a group specified by the consortium (including the Commission Services)

PE

Confidential, only for members of the consortium (including the Commission Services)

CO

Coordinator: Dr. Andreas Schäfer

University of Cambridge

Martin Centre for Architectural and Urban Studies, and

Institute for Aviation and the Environment

1-5 Scroope Terrace, Cambridge CB2 1PX, UK

Tel.: +44-1223-760-129 Fax: +49-341-2434-133 E-Mail: [email protected] Internet: www.toscaproject.org

Contact: Ecorys

Watermanweg 44, 3067GG, Rotterdam

Tel.: +31-10-453-8800 Fax: +31-10-453-0768 E-Mail: [email protected] Internet: www.ecorys.com

Robert Kok

Tel.: +31-10-453-8647 Fax: +31-10-453-0768 E-Mail:

Konstantina Laparidou

Tel.: +31-10-453-8570 Fax: +31-10-453-0768 E-Mail: [email protected]

Adnan Rahman

Tel.: +31-10-453-8796 Fax: +31-10-453-0768 E-Mail: [email protected]

Lynnette M. Dray

Tel.: +44-1223-760-124

Fax: +44-1223-332960

E-Mail: [email protected]

Date: 27.5.2011

3

Contents

Contents .......................................................................................................................................3

Abbreviations ................................................................................................................................5

Abstract ........................................................................................................................................6

1 Introduction ......................................................................................................................7

1.1 Background ................................................................................................................................... 7

1.2 Macro-economic transport-related trends in Europe .................................................................. 7

1.3 The TOSCA Project ......................................................................................................................10

2 Review of existing transport scenarios for Europe ............................................................ 12

2.1 EU transport GHG: routes to 2050 .............................................................................................12

Description ...................................................................................................................................... 12

Results ............................................................................................................................................. 13

2.2 TRANSvisions ..............................................................................................................................13

Description ...................................................................................................................................... 13

Results ............................................................................................................................................. 14

2.3 iTREN2030 Integrated transport and energy baseline ...............................................................14

Results ............................................................................................................................................. 15

2.4 EU energy trends to 2030 (Primes 2009 baseline) .....................................................................15

Description ...................................................................................................................................... 15

Results ............................................................................................................................................. 16

2.5 Roads toward a low carbon future .............................................................................................16

Description ...................................................................................................................................... 16

Results ............................................................................................................................................. 17

2.6 Transport, Energy and CO2 scenarios .........................................................................................17

Description ...................................................................................................................................... 17

Results ............................................................................................................................................. 18

2.7 Findings from scenario review ...................................................................................................18

3 Scenario formulation ....................................................................................................... 21

3.1 Definition of a TOSCA scenario ...................................................................................................21

3.2 Identification of scenario drivers ...............................................................................................21

4

3.3 Baseline scenario ........................................................................................................................24

3.4 Challenging scenario...................................................................................................................27

3.5 Favourable scenario ...................................................................................................................28

4 Projecting intra-European passenger and freight transport demand ................................. 29

4.1 European transport network model (Transtools) ......................................................................29

Transtools Demand Model .............................................................................................................. 29

Transtools Limitations ..................................................................................................................... 30

4.2 Intra- and intercontinental air transport and maritime transport .............................................33

Passenger aviation .......................................................................................................................... 33

Aviation Integrated Model .............................................................................................................. 33

Consistency ..................................................................................................................................... 35

Air Cargo .......................................................................................................................................... 35

Maritime Cargo ............................................................................................................................... 36

4.3 Aggregated Scenario Results .....................................................................................................37

Growth rates by scenario and mode of transport .......................................................................... 37

Total passenger and freight transport by scenario ......................................................................... 40

4.4 Detailed scenario results ............................................................................................................41

Baseline scenario results ................................................................................................................. 41

Challenging scenario results ............................................................................................................ 43

Favourable scenario results ............................................................................................................ 44

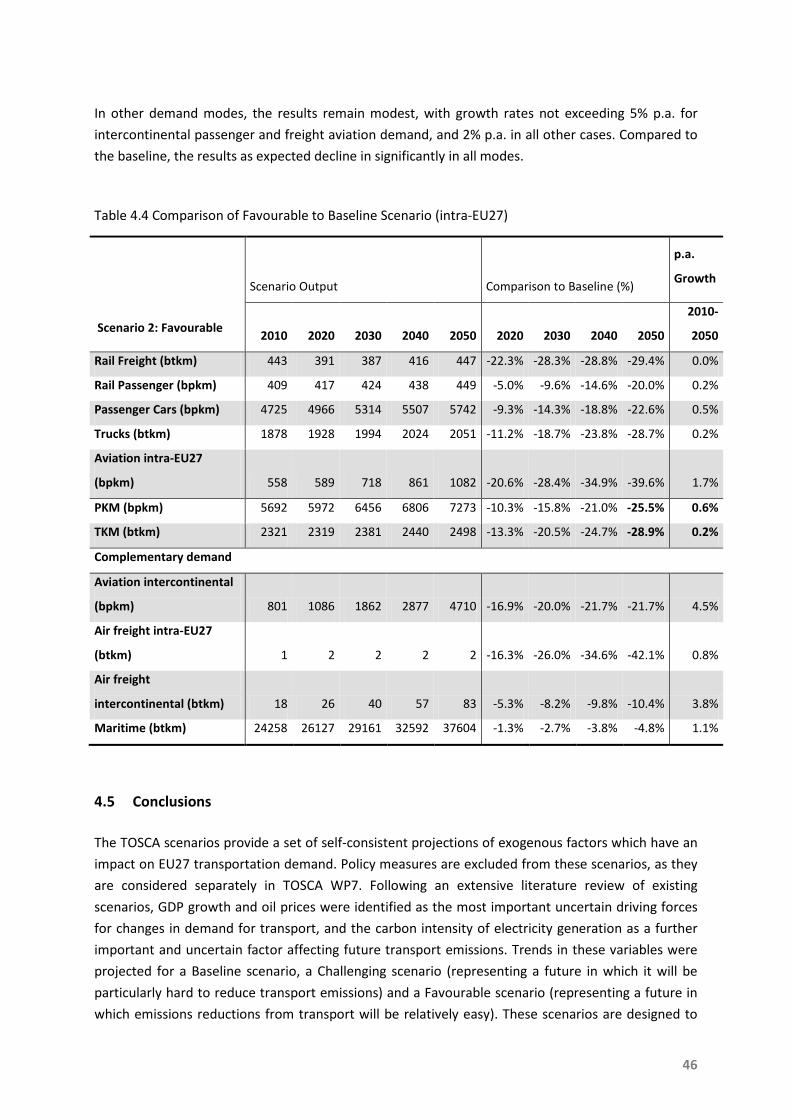

4.5 Conclusions .................................................................................................................................46

5 References ...................................................................................................................... 48

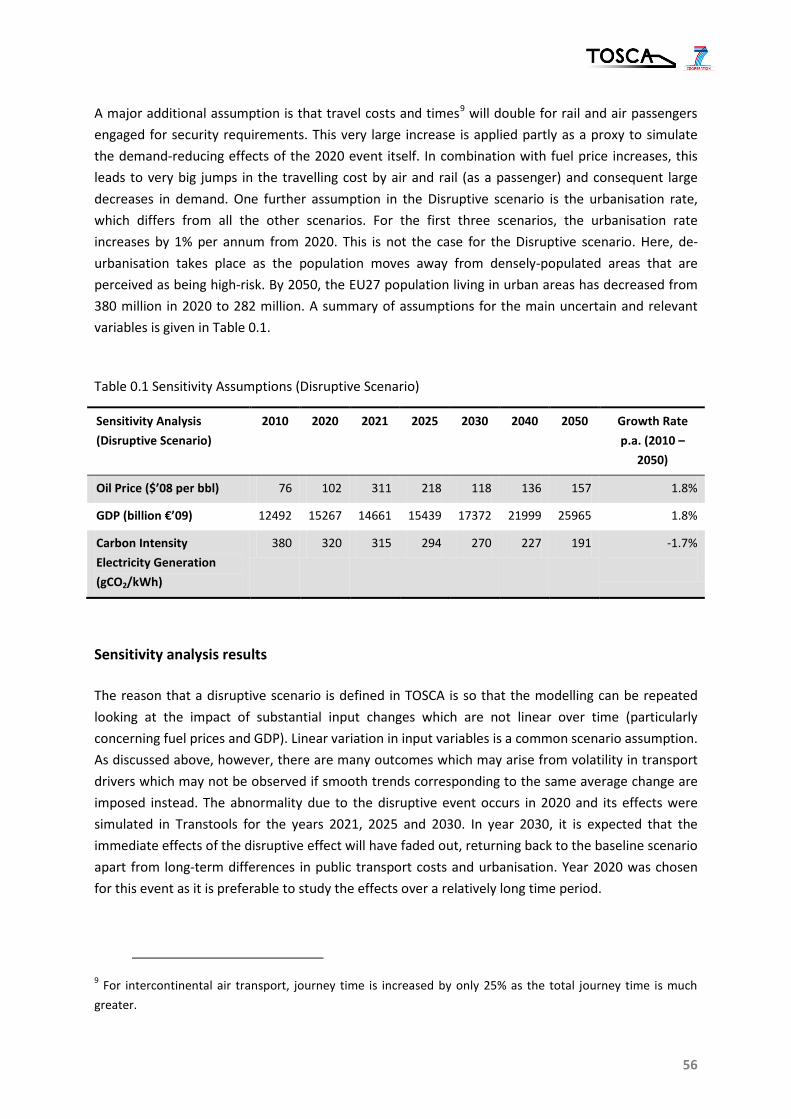

Annex A: Sensitivity Analysis - Disruptive Scenario ....................................................................... 53

Assumptions ...........................................................................................................................................53

Sensitivity analysis results ......................................................................................................................56

Conclusions .............................................................................................................................................59

5

Abbreviations

Abbreviation Description

AIM Aviation Integrated Modelling

bpkm Billion passenger kilometre

btkm Billion tonne kilometre

CO2 Carbon dioxide

eg. exempli gratia – for example

Eq. equation

etc. et cetera – and the rest

GDP Gross Domestic Product

GHG Greenhouse Gas

iTREN Integrated transport and energy

Mtoe Million tonnes of oil equivalents

Mton Million tonnes

pkm Passenger kilometre

SULTAN SUstainabLe TrANsport

tkm Tonne kilometre

TOSCA Technology Opportunities and Strategies toward Climate-friendly trAnsport

Transtools TOOLS for TRansport Forecasting ANd Scenario testing

TTW Tank-to-Wheels (downstream emissions, direct emissions)

WTT Well-to-Tank (upstream emissions, indirect emissions)

WTW Well-to-Wheels (fuel lifecycle emissions) = WTT+TTW

6

Abstract

The TOSCA project aims to identify promising technology and fuel pathways to reduce

transportation-related greenhouse gas emissions through mid-century. An important building block

of this project is the techno-economic specification of low-GHG emission transportation

technologies, which are input into a scenario analysis. TOSCA considers all major modes of passenger

and freight transport, along with transportation fuels and technologies capable of enhancing

infrastructure capacity. This report is thus one out of a number of such techno-economic studies.

TOSCA Work Package 6 (WP6) integrates the technology, fuel, and infrastructure studies carried out

in WP1-5 through a scenario and modelling analysis. The first step in the scenario analysis consisted

of a systematic review of existing European transport scenarios. Consequently, we determined a set

of scenario variables that affect future passenger and freight transport demand. These are used to

formulate four distinct scenarios (three detailed scenarios and one sensitivity case) that describe the

future levels of passenger and freight transport demand. The modelling stage includes the projection

of transport demand for each scenario under the assumption of no new policies. This part of the

modelling stage was carried out with the EU demand model Transtools (JRC, 2010). Due to the

limitations of that model, we complemented the Transtools model with other models such as the

Aviation Integrated Model (AIM). This report (WP 6.1) details the scenario generation and demand

modelling steps described above. A further report (WP6.2) investigates the fleet composition and

emissions which would result in each of these scenarios.

7

1 Introduction

1.1 Background

In December 2008, in order to combat climate change and increase the EU’s energy security, the

European Union adopted a climate and energy package. This package (‘3x20%’) includes the

following emissions and energy use reduction targets to be met by 2020:

• A reduction in EU GHG emissions of at least 20% below 1990 levels

• 20% of EU energy consumption to come from renewable resources

• A 20% reduction in primary energy use compared with projected levels, to be achieved by

improving energy efficiency.

EU Member States agreed to realise the emission reduction target (EC, 2008b) by the following

actions:

• A revision and strengthening of the Emissions Trading System (EU ETS) that sets a single EU-

wide cap on emission allowances. This cap will be cut annually, reducing the number of

emission allowances available to businesses by 21% below the 2005 level in 2020.

• An 'Effort Sharing Decision’ governing emissions from sectors, such as transport, housing,

agriculture and waste that are not covered by the EU ETS. Under this decision each Member

State has agreed to a binding national emissions limitation target for 2020 which reflects its

relative wealth. These national targets will cut the EU’s overall emissions from the non-ETS

sectors by 10% by 2020 compared with 2005 levels.

• The 10% reduction from the effort sharing decision, together with the 21% reduction from

the EU ETS during the same period, will accomplish the overall emission reduction goal of the

EU Climate and Energy package (20% cut below 1990 levels by 2020).

The transport sector, being strongly interconnected with many other sectors, currently accounts for

around 25% of EU27 GHG emissions and this share is increasing (EC 2010a), so changes in the

transport sector will be vital in achieving EU targets for total emissions. Thus, thorough planning

toward climate-friendly transport is fundamental. Before proceeding to the main subject of this

document, which is a discussion of the scenario generation process for the Technology Opportunities

and Strategies toward Climate-friendly trAnsport (TOSCA) project, a short description of the

transport sector is provided regarding the elements which are emphasized in the scenario analysis.

1.2 Macro-economic transport-related trends in Europe

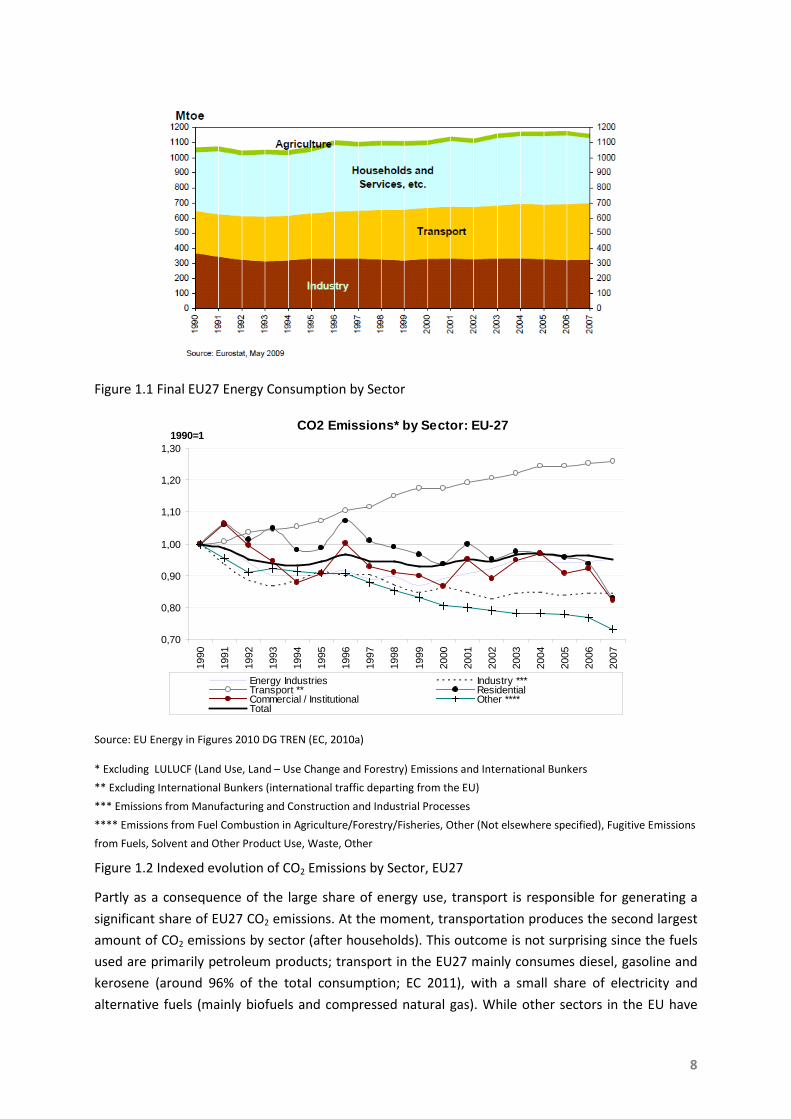

Figure 1.1 depicts Final Energy Consumption in the EU27 countries to 2007, in Mtoe. One can clearly

observe that transport is one of the highest-consumption sectors (with a percentage of 32.6% for

2007). By 2000 transport energy consumption surpassed that of the industry sector (27.9% in 2007).

Accounting for almost one third of total energy consumption, transport is a strong driver for the

definition of current and future EU policies.

8

Figure 1.1 Final EU27 Energy Consumption by Sector

CO2 Emissions* by Sector: EU-27

0,70

0,80

0,90

1,00

1,10

1,20

1,30

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

1990=1

Energy Industries Industry ***Transport ** ResidentialCommercial / Institutional Other ****Total

Source: EU Energy in Figures 2010 DG TREN (EC, 2010a)

* Excluding LULUCF (Land Use, Land – Use Change and Forestry) Emissions and International Bunkers

** Excluding International Bunkers (international traffic departing from the EU)

*** Emissions from Manufacturing and Construction and Industrial Processes

**** Emissions from Fuel Combustion in Agriculture/Forestry/Fisheries, Other (Not elsewhere specified), Fugitive Emissions

from Fuels, Solvent and Other Product Use, Waste, Other

Figure 1.2 Indexed evolution of CO2 Emissions by Sector, EU27

Partly as a consequence of the large share of energy use, transport is responsible for generating a

significant share of EU27 CO2 emissions. At the moment, transportation produces the second largest

amount of CO2 emissions by sector (after households). This outcome is not surprising since the fuels

used are primarily petroleum products; transport in the EU27 mainly consumes diesel, gasoline and

kerosene (around 96% of the total consumption; EC 2011), with a small share of electricity and

alternative fuels (mainly biofuels and compressed natural gas). While other sectors in the EU have

9

shown a decreasing trend in CO2 emissions since 1990, transport continues to emit more carbon

dioxide (Figure 1.2).

Within the transport sector, civil aviation (domestic including international bunkers) shows the

largest growth in CO2 emissions since 1990 (Figure 1.3). However, road and shipping emissions have

also been increasing.

CO2 Emissions* from Transport, EU-27

0,500,600,700,800,901,001,101,201,301,401,501,601,701,801,90

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

1990=1

Civil Aviation Road Railw ays

Navigation Other Total

Source: EU Energy in Figures 2010 DG TREN (EC, 2010a)

* Excluding LULUCF (Land Use, Land – Use Change and Forestry) Emissions and International Bunkers

Figure 1.3 Indexed evolution of CO2 emissions by transport mode, EU27

The increase in transport sector CO2 emissions is strongly linked to economic growth. Figure 1.4

illustrates the link between socio-economic trends (GDP and population) and the volume of transport

(passenger and freight), and consequently the resulting transport GHG emissions. Economic growth

is a general trigger for transport demand because it means more goods are produced and

transported and people have more income available for transportation. This means that reducing

transport CO2 emissions will require either decoupling transport demand from economic growth,

decoupling transport demand from carbon atoms that are oxidized to CO2. TOSCA looks primarily at

the second of these options.

Although the TOSCA project has the goal of investigating how greenhouse gas emissions can be

reduced by new vehicle and fuel technologies, the likely future adoption and impact of these

technologies is fundamentally dependent on the future development of various exogenous factors.

For example, in a future world with low oil prices, the demand for energy efficient low carbon

technologies and fuels will be lower than in a future world with high oil prices. The high uncertainty

attached to future projections of these exogenous factors makes a scenario-based analysis

considering multiple different futures vital.

10

Source: EU energy and transport in figures (EC, 2009c)

Figure 1.4 Indexed evolution of GDP, population and GHG emissions from freight and passenger

transport demand

WP1:Road

WP2: Air

WP3: Rail

Marine

WP1:Road

WP2: Air

WP3: Rail

Marine

WP4: Fuels

WP5: Capacity

WP6/7:Modelling

WP7:Future Policies

WP6: Future Scenarios

Promising Technology/Policy combinations for reducing EU GHG Emissions to 2050

Figure 1.5 TOSCA Work Package structure

1.3 The TOSCA Project

The TOSCA project is an EU FP7 project investigating the potential of alternative vehicle technologies

to reduce the environmental impact of EU27 transportation to 2050. The structure of the project is

shown in Figure 1.5. Initially, WP1-5 estimate the techno-economic characteristics of current and

future vehicle, fuel and infrastructure technologies. WP6 then integrates these study results with

transport demand projections through a scenario and modelling analysis. The first step in the

scenario analysis consisted of a systematic review of already existing European transport scenarios.

Consequently, we determined a set of scenario variables that affect future passenger and freight

transport demand. These are then used to formulate four distinct scenarios (three detailed scenarios

and one sensitivity case) that describe the future levels of passenger and freight transport demand.

The modelling stage includes the projection of transport demand for each scenario under the

assumption of no new policies. This part of the modelling stage was carried out with the EU demand

11

model Transtools (JRC, 2010). Due to the limitations of that model, we complemented the Transtools

model with other models such as the Aviation Integrated Model (AIM). This report (WP 6.1) covers

the scenario analysis and demand modelling stages. A further report (WP6.2) covers technology

uptake and CO2 emissions by scenario.

The basic structure of the TOSCA modelling block is shown in Figure 1.6. In addition to the exogenous

factors (growth in GDP, oil price, and the CO2 intensity of electricity) which form part of the TOSCA

scenarios, the modelling stage uses several other major inputs. These include an updated form of the

European Transport Policy Information System (ETIS), which forms the input to the Transtools model.

This database contains a wide range of transport policy-relevant variables, as appropriate for a 2005

base year (NEA, 2005). TOSCA input consists of changes to the Transtools input database to reflect

the development of baseline scenario variables from 2005 for each year run (e.g. in terms of

population, urbanisation, fuel prices, carbon prices) and any development in the characteristics of

the reference technologies identified by WP 1-5 (e.g. in terms of cost, speed and fuel consumption).

In the case that the database contains a cost to end-users rather than operators (for example, rail

ticket prices rather than costs accruing to rail operators) it is assumed that all cost increases are

passed on to consumers.

Demand, fleet and emissions

Technology Characteristics

Demand Modelling

(Trantools/AIM)

PolicyCharacteristics

ScenarioCharacteristics

Reference only

Stock Model

Changes in Demand(Summa)

All technologies

Promising Technology/Policy combinations for reducing EU GHG Emissions to 2050

Figure 1.6 TOSCA Modelling approach

The remainder of this document is structured as follows. Chapter 2 presents a review of existing

transport scenarios for the EU. Chapter 3 outlines the framework for both passenger and freight

transport that is used to construct and evaluate the TOSCA scenarios. It describes the steps leading

to the definition of the scenarios, and describes a baseline and two internally consistent alternative

scenarios including the underlying assumptions. The scenarios are based on the most relevant and

uncertain exogenous drivers with a potentially large impact on the primary outcome-of-interest, GHG

emissions reductions in transport. Chapter 4 describes the projected demand for transport and

12

modal split by scenario. Finally, in the annex we discuss the effects that a disruptive event may have

on transport demand, and give results from a sample disruptive scenario.

2 Review of existing transport scenarios for Europe

Many scenarios for future EU27 transport demand already exist. Within the scope of this work

package a large number of studies, models and data sources have been reviewed. The review focuses

on quantified transport and energy scenarios, both ‘Baseline’ (no or limited emissions mitigation

policies) and decarbonisation or GHG mitigation scenarios. In analyzing the various studies, the

scope, underlying assumptions and the evolution of key system variables or outputs of the scenarios

were compared. Specifically, the main aspects considered for this review were:

• Timeframe of the scenarios, including a horizon up to 2030 or 2050.

• Geographical scope, including the EU27 or other regions.

• Scope of the transport sector, including all modes or only selected modes.

• Volume of transport, including explicit demand modelling or not.

• Scope of the emissions, including tank-to-wheel (TTW) emissions or well-to-wheel (WTW)

emissions.

• Definition of a scenario, including exogenous drivers, policy instruments or both.

• Key assumptions including GDP per capita, oil prices, and other drivers.

• Nature of the scenario drivers (e.g. linear/continuous or disruptive).

A representative selection of these scenario exercises are reviewed and described individually below.

2.1 EU transport GHG: routes to 2050

Description

The SULTAN Illustrative Scenarios Tool was developed as part of the EU Transport GHG: Routes to

2050? Project (Hill et al, 2010). The project as a whole reviewed the abatement options – technical

and non-technical – that could contribute to reducing transport’s greenhouse gas (GHG, WTW scope)

emissions, both up to 2020 and in the period from 2020 to 2050. SULTAN is a Microsoft Excel-based

tool that can be used to investigate GHG emissions, and some other outputs, associated with

transport from the EU-27 countries in the period 2010-2050. It allows users to create and edit “Policy

Scenarios” – illustrative scenarios for the EU transport system that make assumptions on how

policies might impact on the transport system – and then view the outcomes of the scenarios in

terms of GHG emissions, some other pollutant emissions and some abatement costs. The SULTAN

13

tool is a high-level scoping tool for quick appraisals, not for detailed transport policy impact

assessments.

Results

The baseline scenario shows that the total transport GHG emissions may increase from about 1,600

Mton CO2 equivalent emissions in 2010 to more than 2,000 by 2050. The combined reduction

potential from selected technical and non-technical abatement measures indicates that a reduction

of up to 80-90% over the 1990 level in total transport GHG emissions could be achieved by 2050.

2.2 TRANSvisions

Description

TRANSvisions (2009a) discusses a wide range of drivers related to transport. Three main categories

were identified. First, external drivers, that is, drivers external to the transport sector, for which five

main categories were identified (population, economic development, energy, technology

development and social change). Second, internal drivers, that is, drivers internal to the transport

sector, e.g., infrastructure, vehicles and fuel development and transport impact on environment and

society. Finally, policy drivers, that is, broad policy responses which affect the evolution of the

transport system, and in particular the governance of the transport sector.

A number of different exploratory scenarios for 2050 were formulated based on the identified

drivers. Each scenario was formulated as a different path towards a post-carbon society. A “meta-

model” was developed for the scenario analysis for the timeframe 2005-2050. The meta-model

applied in TRANSvisions was calibrated against scenario results from the Eurpean Commission’s

transport model Transtools for 2005 and 2030. The Transtools scenarios are established based on the

main inputs for the Transtools model. Such inputs include: socio-economic input (population, GDP

development, work places); transport policy input (change in vehicle operating costs, fares and

transport costs for different transport modes); and network input (links and nodes and data related

to these). Four main scenarios were evaluated:

1. The behavioural path: “Moving Less” or Reduced Mobility: Environmental concern and

changes in behaviour.

2. The technological path: “Moving Alone” or Induced Mobility: Exponential growth of

technological improvements, unlimited clean and cheap energy sources, high economic

growth.

3. The mandatory path: “Stop Moving” or Constrained Mobility: Very slow process of

technological implementation, high pensions and health cost, low productivity, strong

mobility regulation, legislation and taxation.

14

4. The organisational path: “Moving Together” or Decoupled Mobility: Strong decoupling

between economic development and growth of traffic volume is gradually achieved, changes

in behaviour.

Results

As both exogenous drivers like GDP per capita and policy assumptions like taxation are used, as well

as ‘wildcard’-type assumptions such as unlimited clean and cheap energy, the resulting demand for

transport varies considerably across the scenarios. Due to different levels of carbon intensity in each

of the scenarios, the resulting CO2 emissions show a smaller range around the baseline. The results in

terms of CO2 emissions trajectories to 2050 show that in all scenarios at least a 10% reduction in

emissions might be achieved by 2050 compared to 2005. The scenarios Decoupled and Reduced

Mobility might achieve over a 50% reduction in emissions by 2050 compared to 2005.

2.3 iTREN2030 Integrated transport and energy baseline

Description

The iTREN-2030 (iTREN, 2009) project contributes to the extension of the European policy

assessment toolbox providing improved tools as well as a consistent energy and transport baseline

scenario, called the Reference scenario, for the EU to 2030. iTREN-2030 applies updated versions of

four European models to generate the baseline scenario:

1. ASTRA (2000), an integrated and strategic transport-economy assessment model.

2. POLES (2006), a global energy model describing the supply- and demand-side of world

energy markets from a technological bottom-up perspective.

3. Transtools, a European transport model focusing on the medium- to long distance transport

flows on the European transport networks.

4. TREMOVE (2007), an environmental assessment model providing vehicle fleet, fuel

consumption and emission indicators for the European transport system.

The basic concept of the Reference scenario is “frozen policy 2008”, i.e. the scenario considers only

policies that were decided by the EU Council and/or EU parliament by mid 2008. It should be noted

that the global economic crisis that started in 2008 is not reflected in the iTREN-2030 Reference

scenario. The iTREN-2030 Reference scenario shows that transport demand will increase until 2030,

especially freight demand, which is projected to be 50% larger in the year 2030 than in the year

2005, while passenger demand is expected to grow more slowly. Therefore, for the EU27 as a whole,

some relative decoupling between economic growth and transport demand is expected, only for

passengers but not for freight. While the economy of the EU27 is expected to grow on average at

1.5% per year until 2030 (but with a decreasing level of employment), and transport increases at a

slightly lower rate, final energy demand is expected to grow less than 1% per year, which means that

the EU27 should become slightly more energy-efficient (iTREN, 2009).

15

Results

The Reference scenario developed in the iTREN-2030 project shows that transport CO2 emissions are

expected to increase from 1,268 million tons in 2005 to 1,485 million tonnes by 2030, an increase of

17% or 0.6% annually. Oil prices are expected to more than double between 2005 and 2030 from 44

to 90 € 2005 per barrel.

2.4 EU energy trends to 2030 (Primes 2009 baseline)

Description

PRIMES (PRIMES, 2010) is a general purpose energy system model supported by some more

specialised models, such as the GEM-E3 and PROMETHEUS. The GEM-E3 (World and Europe versions)

model is an applied general equilibrium model, simultaneously representing 37 World regions/24

European countries, which provides details on the macro-economy and its interaction with the

environment and the energy system. It covers all production sectors (aggregated to 26) and

institutional agents of the economy. GEM-E3 is specifically designed to provide high resolution

output by energy sector and GHG emission source (E3M-Lab, GEM-E3 model description). A fully

stochastic World energy model is used for assessing the uncertainties and risks associated with the

main energy aggregates including uncertainties associated with the impact of policy actions (R&D on

specific technologies, taxes, standards, subsidies and other supports). The model makes endogenous

projections of future energy prices, supply, demand and emissions for 10 World regions (E3M-Lab

PROMETHEUS model description).

Primes is designed for future projections, scenario building and policy impact analysis. It covers a

medium to long-term horizon to 2030. The PRIMES model simulates a market equilibrium solution

for energy demand and supply. It includes transport activity for both passengers and freight. The

model structure defines several technology types (car technology types, for example), which

correspond to the level of energy use. Within road transport, a further subdivision distinguishes

between public road transport, motorcycles and private cars. The model considers six to ten

alternative technologies for transport means such as cars, busses and trucks; the number of

alternatives is more limited for rail, air and navigation (PRIMES, 2010).

The “EU energy trends to 2030” study (E3M-Lab, 2009) is an update of previous trend scenarios, such

as the “European energy and transport - Trends to 2030” study published in 2003 and its 2005 and

2007 updates. Two scenarios, the “Baseline 2009” (finalised in December 2009) and the “Reference

scenario” (April 2010) are presented. The scenarios are available for the EU and each of its 27

Member States simulating energy balances for future years under current trends and policies as

implemented in the Member States by April 2009.

The Baseline 2009 scenario determines the development of the EU energy system under current

trends and policies; it includes current trends in population and economic development including the

recent economic downturn and takes into account the highly volatile energy import price

environment of recent years. Economic decisions are driven by market forces and technology

16

progress in the framework of concrete national and EU policies. Measures implemented before April

2009 are included. This includes the EU emissions trading scheme (ETS) and several measures for

energy efficiency but excludes the renewable energy target and the non-ETS targets. The Reference

scenario is based on the same macroeconomic conditions, price, technology and policy assumptions

as the baseline. In addition to the measures reflected in the baseline, it includes policies adopted

between April and December 2009 and assumes that national targets under the Renewables

directive 2009/28/EC and the GHG Effort sharing decision 2009/406/EC are achieved in 2020.

Results

Key assumptions for the 2009 Reference scenario include:

• a GDP growth rate of 2.2% annually between 2010 and 2020 and 1.7% between 2020 and

2030;

• Rising oil price to about 106 US$ 2008 per barrel by 2030;

• A decreasing carbon intensity of power generation to 179 grams CO2 per kWh by 2030;

• Increasing average after tax electricity prices from 110 to 144 €2005 per MWh between 2010

and 2030.

The total CO2 emissions from transport (excluding maritime and intercontinental aviation) in the

Reference scenario remain at about 1,000 to 1,100 million tonnes of CO2 between 2010 and 2030.

2.5 Roads toward a low carbon future

Description

The background of the study (McKinsey, 2009) is the increasing policy focus on carbon dioxide

emissions from passenger vehicles, due to the fact that these vehicles are a highly visible source of

greenhouse gases and total passenger vehicle emissions are projected to grow to 2030. Three

scenarios are defined assuming different rates and time frames for the diffusion of different

technology packages. These scenarios are:

• ICE scenario

This scenario assumes optimization of the fuel efficiency of ICE-powered vehicles. The sector

does not witness any meaningful global penetration of hybrid or electric vehicles.

• Mixed-technology scenario

A balanced mix of technological solutions reaches the market, including optimized ICEs,

hybrids, and electric vehicles.

• Hybrid-and-electric scenario

There is a rapid transition toward a world of electricity-based vehicle propulsion systems.

17

Results

The CO2 abatement curve that was constructed for Europe in this study includes a number of

abatement options ordered with increasing cost per tonne of CO2. The x-axis represents cost-

effectiveness levels at an oil price of US$ 60 WTI (West Texas Intermediate) or 45€. In addition, two

other dashed horizontal lines represent cost-effective abatement levels at oil prices of 100 (or 75€)

and 150 US$ (or around 110€) per barrel. The results show that over 200 million tons of CO2

equivalent emissions can be abated by abatement options at negative marginal abatement costs

assuming a 60 US$ per barrel oil price.

2.6 Transport, Energy and CO2 scenarios

Description

This study (IEA, 2009) shows how the introduction and widespread adoption of new vehicle

technologies and fuels, along with some shifting in passenger and freight transport to more efficient

modes, could result in a 40% reduction in CO2 emissions below year-2005 levels. This analysis uses

the same basic set of scenarios originally developed for the Energy Technology Perspectives (ETP,

2008) publication. These cover various futures through 2050, including several alternative routes to

achieve very low CO2 emissions for transport. Specific scenarios include:

• Baseline: follows the IEA World Energy Outlook 2008 (WEO 2008) Reference Case to 2030

and then extends it to 2050. It reflects current and expected future trends in the absence of

new policies.

• High Baseline: considers the possibility of higher growth rates in car ownership, aviation and

freight travel over the period to 2050 than occur in the Baseline.

• BLUE CO2 reduction scenarios: these scenarios update those presented in the IEA Energy

Technology Perspectives 2008 report. The BLUE variant scenarios are developed based on

achieving the maximum CO2 reductions achievable from transport by 2050 using measures

costing up to USD 200 per tonne of CO2. These scenarios will require significant policy

intervention if they are to be achieved.

• BLUE Map: this scenario achieves CO2 emissions by 2050 that are 30% below 2005 levels. It

does this via improvements in vehicle efficiency and the introduction of advanced

technologies and fuels such as plug-in hybrids (PHEVs), electric vehicles (EVs), and fuel cell

vehicles (FCVs). It does not envisage significant changes in travel patterns.

• BLUE EV Success: Similar to BLUE Map and achieving a similar CO2 reduction, but with electric

and plug-in hybrid vehicles achieving greater cost reductions and better performance to the

point where they dominate light-duty vehicle (LDV) sales by 2050, to the exclusion of fuel cell

vehicles.

18

• BLUE Shifts: this scenario focuses on the potential of modal shift to cut energy use and CO2

emissions. Air and LDV travel grow by 25% less than in the Baseline to 2050, and trucking by

50% less. The travel is shifted to more efficient modes and (for passenger travel) to some

extent eliminated via better land-use planning, greater use of information technology, and

other measures that reduce the need for motorised travel. Compared to the Baseline in

2050, BLUE Shifts results in a 20% reduction in energy use and CO2.

• BLUE Map/Shifts: this scenario combines the BLUE Map and BLUE Shifts scenarios, gaining

CO2 reductions from efficiency improvements, new vehicle and fuel technologies, and modal

shift. It results in a 40% reduction in CO2 below 2005 levels by 2050.

Results

The oil price is assumed to remain at 120 US$ per barrel from 2030 to 2050 in 2006 real US$. In

nominal prices this means the oil price will increase to over US$ 300 per barrel by 2050. In the

baseline for OECD Europe transport GHG emissions are expected to remain at the 2005 level of about

1,500 Mton CO2 eq. to 2050. Worldwide transport sector GHG emissions in the BLUE Map/Shifts

scenarios are 40% below year-2005 levels.

2.7 Findings from scenario review

• Based on the review of scenarios in this chapter, which are summarised in Table 2.1 below,

we draw the following conclusions:

• Scenario timeframes vary:

O Some studies focus on the end results by 2030 or 2050, while others focus on the

trajectory to the time horizon as well.

• Geographical scope varies:

O Some studies include the EU27, whereas others include world regions, OECD areas or

Western Europe only.

• The investigated scope of the transport sector varies:

o Some studies include all modes; others include selected modes.

o Some studies include main transport corridors/network; others include the full

transport network.

• The volume of transport varies:

o Some studies include explicit demand modelling, others do not. In the latter case,

fixed demand assumptions are applied in all scenarios.

• The scope of emissions varies:

o Some studies include only TTW emissions, where others include WTW emissions.

19

• The definition of a scenario varies:

o Some studies include only exogenous drivers (external forces), while others include

policy instruments or both.

• Key determinants vary:

o Some studies include only GDP and population, whereas others include oil prices and

other variables.

o Few studies include the carbon intensity of electricity as a scenario variable for

transport scenarios.

• The nature of the scenarios varies:

o Most scenarios are linear/ continuous (growth rate extrapolations).

o Few scenarios include disruptive developments/events.

Table 2.1 Review of existing transport scenarios

Scenario exercise:

Review element:

Hill et al., 2010

TRANSvisions, 2009a

iTREN, 2009 E3M-Lab, 2009

McKinsey, 2009

IEA, 2009

Timeframe 2050 2030 and 2050

2030 2030 2030 2050

Geographical scope

EU27 EU27 EU27 EU27 Europe World region, OECD Europe

Transport sector scope

All modes All modes (only intra-EU)

All modes (only intra-EU)

All modes (only intra-EU)

Passenger vehicles

All modes

Transport demand scope

No demand modelling, fixed assumption

Demand modelling

Demand modelling

No demand modelling, fixed assumption

No demand modelling, fixed assumption

No demand modelling, fixed assumption

Scope of emissions

WTW WTW Not specified Not specified WTW WTW

Scenario definition

Policy scenarios (technical and non-technical)

Exogenous and policy scenarios (mixed)

Baseline exogenous and policy assumptions (mixed)

Baseline exogenous and policy assumptions (mixed)

Policy assumptions (abatement options)

Policy assumptions (transport system assumptions)

Nature of scenarios

Continuous Continuous Continuous Continuous Continuous Continuous

Key assumptions

Based on TREMOVE, ExTremis, MARKAL-ED

Based on Transtools (metamodel)

Based on Transtools, TREMOVE, POLES, ASTRA

Based on Primes energy baseline 2009

Based on Global GHG abatement cost curve v2.0

Based on Mobility Model (MoMo)

20

In combination, these factors mean that it can be difficult to compare the results and projected

reductions in emissions from different scenario studies. For example, a study on a scope which

includes only emissions sources which have a relatively large range of mitigation options (e.g.

passenger cars) will project greater reduction potentials than one which includes sources which have

fewer options (e.g. intercontinental aviation). Based on the observations made in this review, the

next chapter clearly defines the approach used in TOSCA for the scenario formulation.

21

3 Scenario formulation

3.1 Definition of a TOSCA scenario

As mentioned in section 2, many scenario exercises use a mix of policy instrument and exogenous

factors to define scenarios. In TOSCA scenarios are defined as follows:

• Scenarios include exogenous variables only

• These exogenous variables are both uncertain and relevant for reducing GHG emissions

• The scenarios include a set of consistent assumptions about the future development of these

variables

• The scenarios are not forecasts, but represent a range of plausible futures

• The scenarios are intended to describe the uncertainty about the future collection of

consistent assumptions

3.2 Identification of scenario drivers

In TOSCA we focus exclusively on exogenous scenario drivers. A framework is used to select variables

that are both relevant and uncertain in terms of reducing GHG from transport. Relevant and

uncertain variables form one block of the evaluation framework used in this project (Table 3.1).

Variables having a low relevance are ignored. Variables which are relevant but not highly uncertain

are included in the Baseline scenario. The Baseline scenario is the reference development used to

evaluate the impact of alternative exogenous scenario developments. Variables with a high relevance

and high uncertainty are used as key scenario variables for the definition of the TOSCA scenarios. The

variables with the highest relevance and largest uncertainty include oil prices (and other energy

prices as a derivative of oil prices), GDP growth and the carbon intensity of electricity generation. The

reasons for these choices are described below.

EU transport depends on oil products for 96% of its energy needs. Transport accounts for 73% of all

oil consumed in Europe (EC, 2011). Oil prices depend on many factors, which are difficult to predict.

Oil prices generally have a large impact on the total volume of passenger and freight transport and

on mode/technology choices. Higher oil prices improve the business case of low carbon alternative

technologies and fuels.

Economic growth, measured as GDP, is another important driver of the volume of transport. Lower

economic growth (or an economic crisis) leads to lower transport demand, which may require less

stringent policy measures for reducing GHG emissions to a certain desired level. In addition, lower

economic growth may also lead to different fuel/technology choices by transport users. Similar

responses are found in certain transport service operations like in shipping; reduced demand for

consumer goods leads to a lower volume of freight transport which leads to overcapacity in (for

instance) container shipping. In response to this, shippers implement slow steaming, leading to

longer voyages (in days) but lower emissions.

22

Table 3.1 Evaluation framework for selecting exogenous drivers in TOSCA.

Uncertainty about development

Low High

Rele

vanc

e fo

r EU

27 G

HG

em

issi

on r

educ

tion

Low IGNORE

IGNORE

High Include on baseline: - Aging population - Population size - Urbanisation - Motorisation rate

Exogenous drivers: - Oil prices - Economic growth (GDP) - Carbon intensity of electricity

The carbon intensity of electricity generation is defined as the amount of CO2 equivalent emissions

per kilowatt hour (kWh) electricity generation (gram CO2 per kWh). This variable will become highly

relevant to transport as many future projections include electricity becoming a significant energy

source for EU transport (via plug-in hybrids, battery electric vehicles or a mode shift to rail). If

transport becomes highly electrified, but electricity does not improve considerably in terms of

carbon intensity, EU transport may not be able to significantly reduce its emissions.

Based on our review of a long-list of existing transport scenarios and models, of which a selection is

presented in chapter 2, we formulated a set of scenarios which include a wide range of the evolution

of the three scenario drivers. The table below depicts four scenarios. The first three scenarios are

defined as follows:

• A reference for the evolution of exogenous factors (Baseline)

• Challenging evolution of exogenous factors in terms of GHG emissions (Challenging)

• Favourable evolution of exogenous factors in terms of GHG emissions (Favourable)

Table 3.2 Overview of the key scenario assumptions which define the three TOSCA scenarios

Scenario assumptions:

Oil prices (US$2008/bbl)

GDP (p.a. % growth)

Carbon intensity (p.a. % growth)

Scenario 0: ‘Baseline’ Increasing 76 to 157 (+1.8%)

Increasing +1.7%

Decreasing -1.7%

Scenario 1: ‘Challenging’

- 76 to 76 (0%)

+ + +2.5 %

+ -0.5%

Scenario 2: ‘Favourable’

+ 76 to 200 (+2.5%)

- +0.7%

- - -3.0%

Scenario 3: ‘Disruptive’ (Annex A)

0 76 to 157 (+1.8%)

0 +1.7%

0 -1.7%

23

0

50

100

150

200

250

1850 1870 1890 1910 1930 1950 1970 1990 2010 2030 2050

Oil

Pric

es U

SD'0

8 pe

r bar

rel

BP Historic Prices Scenario 0: 'Baseline'

Scenario1: 'Challenging' Scenario 2: 'Favourable'

Figure 3.1 Assumptions for Oil prices in all scenarios

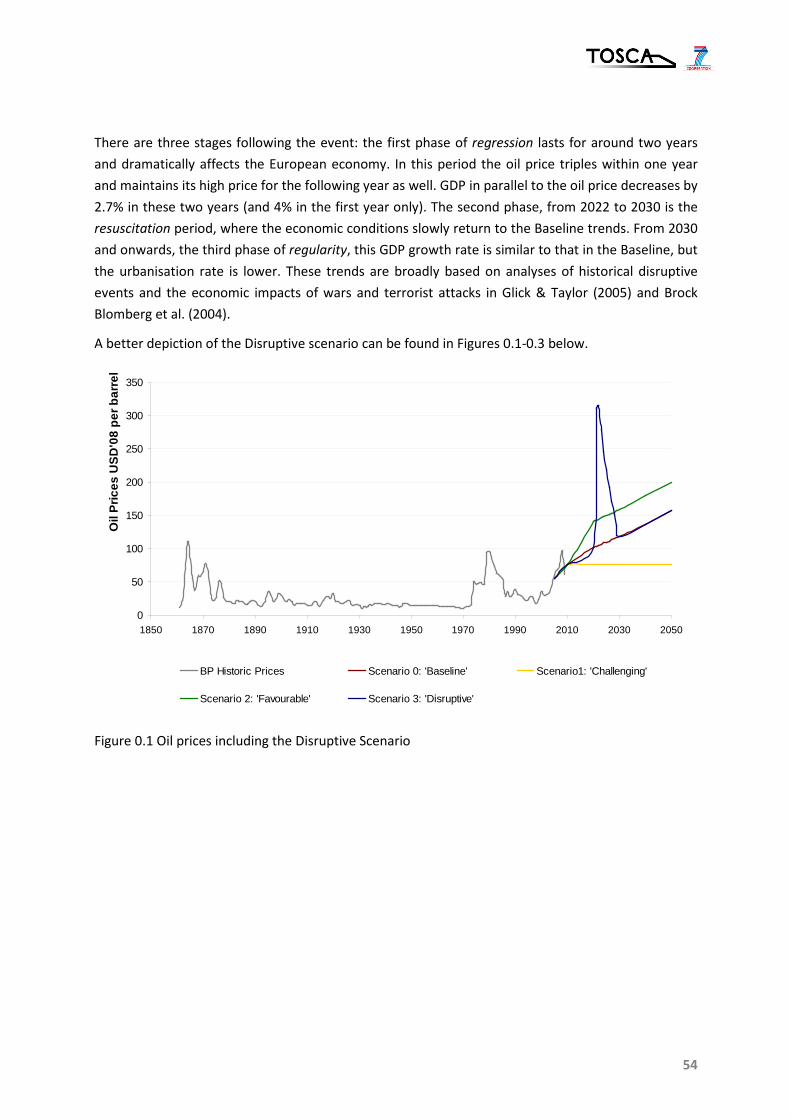

The fourth scenario, Disruptive, mainly functions as a sensitivity analysis. The disruptive scenario

explores the behaviour of the TOSCA framework conditions under the occurrence of an extreme

event in the year 2020 (see Annex A). The development of the identified drivers for the other

scenarios is described below. The assumptions as mentioned in the table above are shown in the

following graphs. In the following sections, each scenario is described in detail. Figure 3.1 above

shows the historic development of yearly average oil prices from 1861 to 2009 and three alternative

oil price scenarios from 2009 to 2050.

0

5000

10000

15000

20000

25000

30000

35000

40000

1990 2000 2010 2020 2030 2040 2050

EU27

GD

P in

bill

ion

EUR

'09

Scenario 0: 'Baseline' Scenario 1: 'Challenging'

Scenario 2: 'Favourable' Eurostat

Figure 3.2 Assumptions for GDP in all scenarios

24

Figure 3.2 shows the historic development of GDP in the EU27 from 1990 to 2005 and the three

alternative GDP scenarios from 2009 to 2050.

0

200

400

600

800

1000

1200

1960 1970 1980 1990 2000 2010 2020 2030 2040 2050

Car

bon

Inte

nsity

g C

O 2 /

kWh

World energy balances (IEA, 2010) and Emission Factors (ETC/ACC, 2003)Scenario 0: 'Baseline' Scenario 1: 'Challenging'Scenario 2: 'Favourable'

Figure 3.3 Assumptions for Carbon Intensity of electricity generation in all scenarios

Figure 3.3 above shows the historic development of the carbon intensity of electricity generation in

the EU27 from 1960 to 2007 and the three alternative carbon intensity scenarios from 2009 to 2050.

3.3 Baseline scenario

The Baseline scenario assumes a continuation of the existing socio-economic trends for EU transport

demand drivers. It is assumed that current policies1

will be successfully implemented and that no

other significantly different policies are introduced. In this scenario, as for all scenarios, the EU is

committed to reduce total GHG emissions by at least 20% relative to the 1990 level by 2020, as

specified in COM (2007), with a further tightening beyond 2020. Table 3.3 presents the evolution of

the relevant and uncertain scenario drivers and baseline variables which are relevant and less

uncertain.

1 This includes, for example, maintaining existing levels of fuel excise duty and VAT, and including aviation in

the EU emissions trading scheme from 2012.

25

Table 3.3 ‘Baseline’ scenario drivers and baseline variables

Scenario 0: ‘Baseline’ Unit 2010 2020 2030 2040 2050 Growth Rate

2010-2050

Relevant and uncertain scenario drivers:

Oil price US$ per bbl, 2008

76 102 118 136 157 1,8%

Carbon intensity electricity generation (DBFZ forecast /EURelectric)

g CO2 / kWh 380 262 145 117 89 -3,6%

GDP EU27 Billion €, 2009

12811 15747 18621 21999 25965 1,8%

GDP per Capita, EU27 €, 2009 PPP2 25674 30636 35810 42510 50417 1,7% Relevant and low-uncertainty baseline variables:

Population size EU27 Million, EU27 499 514 520 518 515 0,1% Urbanisation (EU27) Million, EU27 369 392 413 426 438 0,4% Urbanisation Rate (EU27) % 74 76 79 82 85 0,3% Motorisation rate (EU27) cars/1000

inhabitants 451 512 566 626 692 1,1%

Electricity prices € 2009/MWh 118 150 155 151 147 0,5%

Oil prices3 are shown in figure 3.1. This graph depicts the development of crude oil prices from BP

since 1861. One can here observe the price fluctuations which contribute to the high uncertainty in

the future development of this variable4

. From 2010 on, these prices steadily increase in the baseline

scenario with an average annual growth rate of 1.8%. By 2020 oil price is expected to rise beyond

100 US$’08 per barrel, originally due to growing demand but, later on, also because of being a finite

resource. Gas prices are assumed to be highly positively correlated to oil prices.

GDP growth is expected to increase moderately in the EU27 to 2050. The average EU27 growth rate

for GDP in the baseline scenario is projected to be 1.8% per annum for the EU27 countries (Table

3.3). GDP per capita demonstrates a slightly smaller growth rate of 1.7% per annum, due to a small

growth in population.

2 Note that some of the models within TOSCA used require input in the form of market exchange rate (MER)

GDP. In this case, the study of Manne, Richels & Edmonds (2005) was used to provide a plausible conversion

factor.

3 Oil prices affect transport costs. The effect though may be limited as a high proportion of gasoline and diesel

price is tax which is assumed to remain at present-day levels. In addition, for some transport modes energy

costs represent only a low proportion of operating costs (e.g. around 10% for rail).

4 Some of the main influencing factors of the oil price are economic growth, car ownership and in general fuel

demand, the existing –known and unknown- fuel reserves and the producing countries’ relationships to the

rest of the world.

26

The carbon intensity of electricity is projected to decrease due to cleaner, more efficient electricity

generation techniques and different primary energy sources. This expected technological evolution,

combined with the EU ETS regulation applicable to stationary emission sources such as power plants,

is projected to reduce the carbon intensity of electricity generation by 3.6% annually from 2010 to

2050.

Other relevant but less uncertain factors were studied for the Baseline scenario. Population is

projected to grow moderately for both the EU27 as a whole and the EU15 countries (table 3.3), but

not for the EU12 countries due to expected emigration. Urbanisation follows an increasing trend,

with 85% of the population living in urban areas by 2050. The motorisation rate is expected to grow

on average by 1.1% annually. Motorisation is expected to increase due to increasing GDP and income

levels, especially in Eastern Europe where motorisation rates rapidly catch up with those of Western

European countries. The baseline electricity prices are projected to reach their highest level around

2030 and drop slightly afterwards to 2050. The baseline electricity prices are based on the PRIMES

energy baseline 2009 for the EU (EC, 2010). Furthermore, assumption are made about the GDP

growth in non-EU world regions as these are relevant and required to determine intercontinental

transport flows. The economically developing countries (China, India, Brazil) are projected to lead

GDP growth with more than double the growth factors observed in Europe.

Table 3.4 ‘Baseline’ non-European GDP projections (adapted from Duval & de la Maisonneuve 2010).

Scenario 0: ‘Baseline’

Relevant and less uncertain scenario drivers: Non_EU27 GDP growth

Growth Rate

2010-2050

USA + Canada 2,3%

Japan 1,2%

China + India 5,8%

Brazil 4,0%

Russian federation 2,7%

Rest of World 4,8%

World total 3,6%

Even though major technological breakthroughs are not assumed in the Baseline, there is a moderate

efficiency improvement of current technologies in all modes of transportation. These autonomous

efficiency improvements are taken from the background trends in reference technology

development from WP1-5 of TOSCA, with the exception of aviation for which the evolutionary

replacement technology is specifically included. They are used as baseline developments in TOSCA.

In addition, because TOSCA WP3 anticipate significant changes in future maximum rail speeds for

both passengers and freight, an increase in maximum speed of 5% to 2020 and 15% to 2030 from

base year levels is assumed in all scenarios.

27

For the following two scenarios (favourable and challenging) only the uncertain and relevant

parameters (Oil price, GDP and the carbon intensity of electricity) are examined. In addition, a

further scenario for sensitivity testing (disruptive) is described in Annex A.

3.4 Challenging scenario

This scenario, representing an era of economic prosperity in the EU27 countries, leads to a challenge

in terms of emissions reduction. GDP is assumed to increase in the EU27 at a faster pace than in the

Baseline scenario. Energy-wise, this scenario assumes a situation in which sufficient oil and gas fields

are explored and recovered by conventional as well as unconventional but affordable techniques and

in both OPEC and non-OPEC countries. Hence, the oil price continues below the oil price trajectory in

the Baseline scenario (except for the starting year) and remains constant at the 2010 price level to

2050 (76 US$/bbl).

The availability of resources and the low fuel prices combined with high economic growth is likely to

increase demand for transport in Europe. In addition, the carbon intensity of electricity generation

only decreases by 0.5% per annum, leading to an overall 18.2% decrease in carbon intensity to 2050

where the Baseline projects an almost 50% decrease. These factors in combination are likely to lead

to high emissions from transport. The table below summarises the main indicators for the

‘challenging’ scenario.

Table 3.5 ‘Challenging’ Scenario Assumptions

Challenging Scenario 2010 2020 2030 2040 2050 Growth Rate p.a.

(2010 – 2050)

Oil Price ($’08 per bbl) 76 76 76 76 76 0.0%

Difference from Baseline 0% -25% -36% -44% -52%

GDP (billion €’09) 12492 15990 20469 26202 33540 2.5%

Difference from Baseline 0% +5% +13% +19% +29%

Carbon Intensity Electricity Generation

(gCO2/kWh)

380 361 344 327 311 -0.5%

Difference from Baseline 0% +13% +27% +44% +63%

As depicted above, the growth profile for key drivers differs significantly from the Baseline. The oil

price reaches a relative difference from the Baseline level of 52% in 2050. GDP also increases at a

faster pace and, in 2050, is higher by 29% than in the Baseline scenario. Finally, the carbon intensity

of electricity generation is assumed to only moderately decrease, ending up being 63% higher than

the baseline in 2050. These factors in combination mean that it will be difficult to reduce CO2

emissions in this scenario.

28

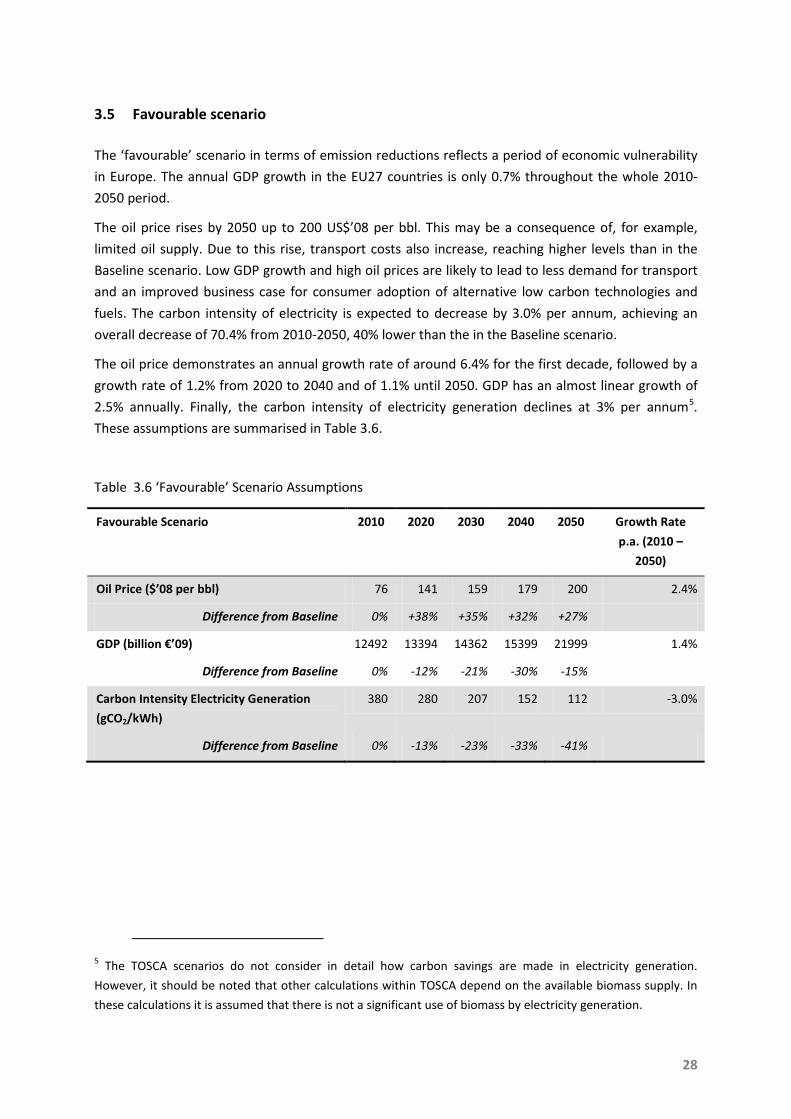

3.5 Favourable scenario

The ‘favourable’ scenario in terms of emission reductions reflects a period of economic vulnerability

in Europe. The annual GDP growth in the EU27 countries is only 0.7% throughout the whole 2010-

2050 period.

The oil price rises by 2050 up to 200 US$’08 per bbl. This may be a consequence of, for example,

limited oil supply. Due to this rise, transport costs also increase, reaching higher levels than in the

Baseline scenario. Low GDP growth and high oil prices are likely to lead to less demand for transport

and an improved business case for consumer adoption of alternative low carbon technologies and

fuels. The carbon intensity of electricity is expected to decrease by 3.0% per annum, achieving an

overall decrease of 70.4% from 2010-2050, 40% lower than the in the Baseline scenario.

The oil price demonstrates an annual growth rate of around 6.4% for the first decade, followed by a

growth rate of 1.2% from 2020 to 2040 and of 1.1% until 2050. GDP has an almost linear growth of

2.5% annually. Finally, the carbon intensity of electricity generation declines at 3% per annum5

.

These assumptions are summarised in Table 3.6.

Table 3.6 ‘Favourable’ Scenario Assumptions

Favourable Scenario 2010 2020 2030 2040 2050 Growth Rate

p.a. (2010 –

2050)

Oil Price ($’08 per bbl) 76 141 159 179 200 2.4%

Difference from Baseline 0% +38% +35% +32% +27%

GDP (billion €’09) 12492 13394 14362 15399 21999 1.4%

Difference from Baseline 0% -12% -21% -30% -15%

Carbon Intensity Electricity Generation

(gCO2/kWh)

380 280 207 152 112 -3.0%

Difference from Baseline 0% -13% -23% -33% -41%

5 The TOSCA scenarios do not consider in detail how carbon savings are made in electricity generation.

However, it should be noted that other calculations within TOSCA depend on the available biomass supply. In

these calculations it is assumed that there is not a significant use of biomass by electricity generation.

29

4 Projecting intra-European passenger and freight transport demand

In order to estimate the impact that each scenario described in Section 3 has on EU27 transport

emissions, we need to determine how transportation demand will develop in each case. Different

scenario assumptions are likely to have varying effects depending on the mode, country, population

segment and existing transportation system looked at. Therefore demand modelling that considers

these effects as far as possible is needed. This section describes the demand modelling process in

TOSCA.

4.1 European transport network model (Transtools)

As explained in chapter 1, the scenario assumptions described above are implemented within the

European transport demand model Transtools, to simulate the intra-EU demand impact for

passenger and freight transport by mode. The Transtools model input consists of a detailed database,

based on the European Transport Policy Information System (ETIS) database of transport policy-

relevant European variables, as appropriate for a 2005 base year (NEA, 2005). TOSCA input consists

of changes to the Transtools input database to reflect the development of baseline scenario variables

from 2005 for each year run (e.g. in terms of population, urbanisation, fuel prices, carbon prices) and

any development in the characteristics of the reference technologies identified by WP 1-5 (e.g. in

terms of cost, speed and fuel consumption). In the case that the database contains a cost to end-

users rather than operators (for example, rail ticket prices rather than costs accruing to rail

operators) it is assumed that all cost increases are passed on to consumers. A description of the

model itself is given below.

Transtools Demand Model

Transtools (DTU, 2010) is a large and complex demand model which includes several different,

interacting modules to calculate the end-results of passenger and freight demand, as shown in figure

4.1. These are:

• The regional economic model, which models interdependencies in economic processes

(using a multiregional computable general equilibrium model), incorporating transport costs

and other cost components.

• The freight models (mode and logistics). This module uses a top-down approach

incorporating global economic trends and national GDP, and calculates the trade volume

between countries and regions (NUTS 26

6 The EU Nomenclature of Territorial Units for Statistics (NUTS) system splits Europe into a number of

geographical regions for modelling purposes. Transtools uses NUTS2 and NUTS3-level data. These

classifications divide the EU27 countries into 271 and 1303 regions respectively.

level). The logistics module ranks the regions

30

according to their attractiveness for freight transhipment and assigns the freight demand to

the logistics chains. The output consists of trip matrices at a NUTS2 geographic level.

• The passenger demand model. This module is implemented as stored procedures in a

database. The inputs to the model are cost matrices, rail ticket prices, and zone data (e.g.

population, GDP, employment). It is specified for four trip purposes (e.g. business) for both

short and long trips (short trips do not include the air mode). The output consists of NUTS3-

level Matrices7

• The network model (for all modes). The network uses stochastic processes and calculates the

demand for each mode of transport. The road network consists of 50,000 links and 30,000

nodes, the air network 450 airports, the rail freight network from 6,000 links and 4,500

nodes and the rail passenger network 5,500 links and 4,500 nodes. The network model is

used to calculate routing and congestion on major routes, which in turn may impact demand.

.

• The air journey model. This is a stochastic model which uses the link times and the costs to

calculate the air passenger demand.

• The impact models. These are the environmental and the transport impact models. The first

includes indicators for energy consumption, emissions and external costs for road, rail and

air. The second includes the safety impact and the fatalities for road and rail.

Because network effects may impact on demand, an iterative run structure is used. Initially, the

network model is run, based on the model input variables and a starting set of demand inputs. After

this, the full passenger and freight demand models are run. Finally, the network model is run again

with the updated demand values. These steps can be iterated as necessary.

Transtools covers the whole of the EU27 and a number of other countries (e.g. the Ukraine). For the

present study, only EU27 results were extracted.

Transtools Limitations

Transtools simulates all major European networks (air, road, train and inland waterways) at NUTS2

(271 provinces/regions) and NUTS3 (1,303 districts/ groups of municipalities) geographical levels. The

output, in terms of network passenger and freight flow for a scenario year, is represented at a NUTS2

level for freight and at NUTS3 for passengers. Output is provided in vehicles-km for road transport,

tonnes-km for inland navigation and rail freight transport and passenger-km for aviation and rail

passenger transport. As well as demand flows, Transtools calculates detailed matrices for travel

costs, speed and travel times by mode as part of its demand and modal split calculations.

7 The air mode is calculated per airports (specified regions are included).

31

Figure 4.1 Transtools modules

However, Transtools has a number of limitations that means it is primarily suitable only for baseline

demand modelling within TOSCA. TOSCA has two broad requirements for demand modelling (Figure

1.6). The first is for scenario-dependent projections of demand by mode to 2050 in the case without

significant changes to vehicle technology. The second is for projections of how that demand may

change in response to developments in technology characteristics or changes in policy. Whilst the

first requirement may be satisfied with a small set or model runs per scenario, the latter case

requires a far greater number of model runs. Transtools allows a comprehensive, network-based

investigation of future transportation scenarios which includes many important effects, including

congestion and population heterogeneity. Some elements within the model are stochastic and

require several iterations for the results to stabilise. However, these factors result in a high

calculation time (approximately a week per run, where one run generates demand output for a single

year). This makes it infeasible in terms of time to run large grids of Transtools runs.

In addition, Transtools has a limited scope of the European network (e.g. covering mostly highways,

national roads, and interregional/provincial roads for the road network, and not covering tram,

metro and regional lines for railways). Whilst the network modelling carried out in Transtools is

valuable for projecting congestion effects, it is only carried out for this network scope, and modelling

outside this network is more limited. It does not model intercontinental air or marine transport, or

32

air freight. The rail modelling is limited, resulting in rough estimates of travel time, cost and flows.

Vehicle stock is also not modelled in detail.

Because of these limitations, some elements of the TOSCA demand modelling are calculated outside

the main model using alternative models. First, some demand calculations were made to cover areas

not included in Transtools. This includes estimates of intercontinental marine and air freight demand,

for which simple models from the literature were used. Intercontinental passenger aviation was

modelled using the Aviation Integrated Model (Reynolds et al. 2007). These models are described in

Section 4.2 below. In each case care was taken to ensure that the input assumptions were consistent

with those used in the Transtools input. Second, Transtools output is calculated until 2030. As not all

of the components of Transtools are designed to function after 2030, the long-term effects (beyond

2030) of the scenarios are simulated by meta-models and trend extrapolations. Besides the regular

runs for each scenario in Transtools (2010, 2020, 2030), two additional runs were used for the

Disruptive scenario (2021 and 2025) so as to fully depict the disruptive effect.

As Transtools is a network model, some of its network calculations exclude passengers and freight

travelling on minor roads or rail routes. For example, for rail transport, Transtools covers only the

main stations, excluding regional rail transport, metros and trams. This leads to underestimates

which need to be corrected for when using these calculations to estimate aggregate demand, as

discussed in TENconnect (2010). Therefore it was also necessary to calibrate the remaining data,

both rail and road transport, to Eurostat data for the base year (Eurostat, 2010) to account for these

excluded trips (see Table 4.1).

Table 4.1 Comparison of Transtools to Eurostat results

Mode Eurostat Transtools

output Divergence Rail Freight 443 461 4%

Rail Passenger 409 292 -29%

Passenger Cars 4725 4073 -14%

Trucks 1878 1897 1%

Finally, the long runtime of Transtools made it necessary to make runs before the final versions of

the results of TOSCA work packages 1-5 were available. In a few cases, the change from intermediate

to final values resulted in changes to technology characteristics which had been used as input to

Transtools. To account for these changes, the elasticity model developed as part of the stock

modelling (See WP6.2 Report, section 2.7) was used to adjust the total demand. For the scenarios

discussed here, changes were typically under 1%.

33

4.2 Intra- and intercontinental air transport and maritime transport

Passenger aviation

Transtools does not include a model for intercontinental aviation. However, there are several

reasons why having an estimate of intercontinental aviation demand is useful for the TOSCA project.

First, many intercontinental air passengers make multi-segment journeys which include an intra-EU

segment. Projections of intercontinental aviation demand typically show faster growth than for intra-

EU demand (e.g. Boeing 2010, Airbus 2009), so intra-EU journeys by intercontinental passengers will

also grow in importance in the future. Second, intercontinental and intra-EU flights share the same

airports and airspace. This means that any consideration of airport or airspace capacity is incomplete

if only one type of flight is considered. Third, although TOSCA does not consider specific alternative

technologies for long-haul aircraft, this is due to an anticipated lack of new technologies for these

aircraft which could make a significant fleet impact before 2050, not because they are unimportant

in terms of emissions. In fact, long-haul aviation is one of the fastest-growing sectors both in terms of

demand and emissions, with growth in pkm in excess of 5% per year predicted on some route groups

(Airbus 2009, Boeing 2010) and it is already included in EU climate policy via the EU’s inclusion of

aviation from 2012 in its emissions trading scheme (EU 2009). Therefore estimating intercontinental

aviation emissions is important in terms of estimating the relative importance of different future

transport emissions sources.

As Transtools excludes intercontinental transport, estimates of intercontinental aviation demand are

made using an existing model at the University of Cambridge, the Aviation Integrated Model. Since

this is a global model of aviation, it also provides an alternative forecast for intra-EU aviation. This

model, and its use within TOSCA, are described below.

Aviation Integrated Model

The Aviation Integrated Model (AIM) is a systems model of global aviation, covering around 95% of

global air pkm (Dray et al. 2010a). The future demand estimates provided by AIM are scenario-based

and require GDP, population, fuel and carbon prices as input. Output in terms of demand and

emissions is provided on a city-pair basis, allowing the change in demand over arbitrary geographical

regions to be calculated. These factors make the model suitable as a method of estimating

intercontinental aviation demand to and from the EU27 countries within TOSCA. A summary of the

model structure, inputs and outputs and use in TOSCA is given below.

Figure 4.2 shows the basic structure of AIM. AIM consists of seven interconnected modules,

programmed in Java and Matlab. Of these, only the first four are relevant for TOSCA demand

estimation.

The Air Transport Demand module projects true origin-ultimate destination demand for air travel

for a set of 700 global cities, served by 1,127 airports, which accounts for around 95% of global

34

scheduled air pkm. For use in TOSCA, population and GDP per capita from the TOSCA scenarios by

world region are provided as inputs8

.

Figure 4.2 Aviation Integrated Model structure

The Airport Activity Module assigns passenger routing, a flight schedule, and aircraft types by

flight segment, calculates the resulting flight delay and airport capacity requirements to maintain

future flight delays close to existing levels. This approach assumes that airport regions will be able to

expand runway capacity to meet demand requirements (if necessary by utilising secondary airports).

The Aircraft Movement Module calculates the location of emissions, accounting for en-route

inefficiencies.

The Aircraft Technology and Cost Module computes costs and emissions by aircraft type, and fleet

turnover rates, including airline decisions to invest in new technology. For the purposes of the TOSCA

baseline runs, it was assumed that no new technologies were available to airlines other than air

traffic management improvements provided by the SESAR project, and evolutionary replacement

narrowbody aircraft. The changes in costs resulting from these technologies were taken from TOSCA

WP2 data (Vera-Morales et al. 2011), in combination with TOSCA scenario data about fuel and

carbon prices. Airline costs are used in AIM to estimate average airfares, which are input to the Air

Transport Demand module, for the estimation of passenger demand. These modules are therefore