department for transport hs2 property bond...

TRANSCRIPT

HS2 Property Bond Option / Final Report / September 2013

Department for Transport HS2 Property Bond Option

Contents

Important notice from Deloitte

1 Introduction 1

2 Background 3

3 What is a property bond? 4

4 What similar forms of Bond Scheme have been in operation? 5

5 Relevant Policy Aims 11

6 Features of a property bond scheme 12

7 Operation of the proposed bond scheme 20

8 Proposed bond scheme compared to the proposed “Voluntary Purchase” scheme 26

Appendix 1 – Extract from Deloitte engagement letter

Appendix 2 – Assessment of Policy Criteria

Appendix 3 – Summary of operational Bond Schemes

Important Notice from Deloitte

This final report (the “Final Report”) has been prepared by Deloitte LLP (“Deloitte”) for the Department of Transport (DfT) in accordance with the contract with them dated 10 June 2013 (“the Contract”) and on the basis of the scope and limitations set out below.

The Final Report has been prepared solely for the purposes of advising DfT on property bond options for HS2 Phase One and recommending an optimal form of such scheme, as set out in the Contract. It should not be used for any other purpose or in any other context, and Deloitte accepts no responsibility for its use in either regard, including use by the DfT for decision making or reporting to third parties.

The Final Report is provided exclusively for DfT’s use under the terms of the Contract, however it may be made publically available solely for the purpose of supplementing the public consultation documentation prepared by the DfT. No party other than the DfT is entitled to rely on the Final Report for any purpose whatsoever and Deloitte accepts no responsibility or liability or duty of care to any party other than the DfT in respect of the Final Report or any of its contents. If any other party chooses to rely on the Final Report, it does so at its own risk and without recourse to Deloitte.

As set out in the Contract, the scope of our work has been limited by the time, information and explanations made available to us. The information contained in the Final Report has been obtained from the DfT and third party sources that are clearly referenced in the appropriate sections of the Final Report. Deloitte has neither sought to corroborate this information nor to review its overall reasonableness. Further, any results from the analysis contained in the Final Report are reliant on the information available at the time of writing the Final Report and should not be relied upon in subsequent periods.

Accordingly, no representation or warranty, express or implied, is given and no responsibility or liability is or will be accepted by or on behalf of Deloitte or by any of its partners, employees or agents or any other person as to the accuracy, completeness or correctness of the information contained in this document or any oral information made available and any such liability is expressly disclaimed.

All copyright and other proprietary rights in the Final Report remain the property of Deloitte LLP and any rights not expressly granted in these terms or in the Contract are reserved.

This Final Report and its contents do not constitute financial advice, and does not constitute a recommendation or endorsement by Deloitte to invest or participate in, exit, or otherwise use any of the markets or companies referred to in it. To the fullest extent possible, both Deloitte and the DfT disclaim any liability arising out of the use (or non-use) of the Final Report and its contents, including any action or decision taken as a result of such use (or non-use).

Department for Transport HS2 Property Bond Option 1

1 Introduction 1.1 This paper considers the key features and operational practicalities of a proposed form of “property bond”

scheme that could be provided for Phase One of the High Speed Two (HS2) high speed rail project.

Instructions 1.2 We were instructed by the Department for Transport (DfT) to: investigate and make recommendations on the

key features and operational practicalities on a property bond option for Phase One of the HS2 high speed rail project; to assess that option’s performance against DfT policy aims; and provide evidence (where possible) on its profile of costs, benefits, risks and wider effects. An extract of our engagement letter is contained in Appendix 1.

1.3 In the time available, we have not been able to quantify the financial costs, benefits or risks (which, in any event, would be subject to significant uncertainties). As such, our advice is based primarily on our experience of compulsory purchase matters generally, our involvement with High Speed One (previously known as the Channel Tunnel Rail Link), our experience of property markets, and our professional judgement.

Summary 1.4 In arriving at the proposed form of property bond we have considered the pros and cons of property bond or

bond-type schemes that have been operated elsewhere and have considered various bond options against DfT’s key criteria of: fairness; value for money; community cohesion; feasibility efficiency and comprehensibility; and the functioning of the housing market.

1.5 In fulfilling our instructions, we have designed a property bond scheme that we consider is credible, is compliant with the identified policy criteria, and is capable of implementation. It should assist in enabling the local property markets to function normally during the life of HS2’s construction. Although we have not had time to work up all the detailed practicalities, in order to arrive at the proposed scheme we have given consideration to its component parts. We have undertaken qualitative analysis and subjectively tested numerous scenarios as to how we might expect it to operate in practice. Subject to more work on the detail we feel that in principle the proposed scheme is capable of being implemented.

1.6 Despite our confidence that the proposed bond scheme should work in practice, it has not been possible for us to undertake detailed evidence-based quantitative analysis and therefore the proposal remains untested. Such detailed analysis has not been possible for two reasons: first, because of the short time available for the preparation of our report; and secondly – and more significantly – because the entire property bond concept is one that remains largely untested in the UK. Although other forms of property bond scheme have been established, the criteria for qualification have been narrower than our scheme proposes (in that they are limited to land actually required for the proposed development) and none of the proposed projects has become sufficiently advanced for bonds to be capable of being triggered. We also do not have the benefit of observing any smaller scale “pilot” exercise to draw some quantitative conclusions. This is not to say that any such analysis or pilot testing might not confirm the credibility and viability of the proposed bond scheme; it is simply that such work has not been undertaken by us or (to the best of our knowledge) by anyone else.

1.7 Our subjective view, based on our experience and professional judgement, suggests that were the proposed bond scheme to be implemented, there could initially be a significant administrative burden, as a large proportion of qualifying landowners (out of an estimated 1,600 in total) may apply for a bond. This level of administration (requiring staff of the bond scheme operator, building surveyors, valuers and lawyers to

Department for Transport HS2 Property Bond Option 2

variously collaborate, inspect properties and issue bonds) might limit DfT’s desire or ability to implement it as part of a proposed package of compensation measures promptly after consultation. On the other hand, the magnitude of such mass valuation technique is not unprecedented. It is for this reason we have proposed that only those in the “inner bond area” and those owners in the “outer bond area” who have an immediate intention to put their interests on the market would be eligible for the first six months of the scheme.

1.8 Once in place, the certainty provided by the proposed bond scheme should enable property markets to operate more normally, although this cannot be tested in advance and it should not necessarily be assumed that this will happen. The number of people wishing to sell during the life of the bond (possibly 15 years), and the response of the property market to property held with a bond can also be predicted, but not with absolute certainty.

1.9 In our comparative assessment of bond options we assume that the maximum amount of compensation payable under the proposed bond scheme could be similar to that under the proposed Voluntary Purchase Scheme, in the scenario that each would be introduced alongside the proposed Express Purchase Scheme (i.e. the acquisition of all qualifying property in the Safeguarded Area and that area up to 120m either side of the railway in rural areas). Considered as alternatives to each other the proposed bond scheme and Voluntary Purchase Scheme also produce similar scores in our subjective assessment of policy criteria set out in Appendix 2.

1.10 For these reasons, although we consider the proposed bond scheme has features that should help property markets to function normally, and is in theory capable of implementation, subject to the detail being worked on in coming weeks, the DfT may consider that it is not appropriate to introduce this new concept for a project the size of HS2, within the timetable for implementation that is proposed. Conversely, the DfT may consider that the proposed bond scheme is sufficiently credible for the DfT to propose it as a mutually exclusive alternative to the Voluntary Purchase Scheme in the forthcoming consultation.

Department for Transport HS2 Property Bond Option 3

2 Background 2.1 The basis of compensation to be paid following the acquisition of land and property pursuant to compulsory

purchase is generically referred to as the “Compensation Code”. This is a collection of entitlements and assurances defined by statute (principally the Land Compensation Acts of 1961 and 1973 and the Compulsory Purchase Act 1965), by case law and by administrative practice. The over-riding principle of compensation is that of “equivalence”, that is to say that the quantum of compensation paid should put the claimant back in the same position (so far as money can) as if the compulsory purchase had not happened.

2.2 The Government is committed to honouring the entitlements of all property owners to compensation under the Compensation Code; however it recognises that due to the exceptional scale and duration of the HS2 project, this compensation regime may not fully address the reasonable needs of all property owners and occupiers affected by the HS2 proposals. Consideration has therefore been given to appropriate additional compensation measures that it might be appropriate to introduce.

2.3 The Government first consulted the public on principles of property compensation policy for HS2 phase 1 in February 2011, in ‘High Speed Rail: Investing in Britain’s Future – Consultation’. It then set out its initial decisions in January 2012 in ‘High Speed Rail: Investing in Britain’s Future – Decisions and Next Steps’, by saying it would consult in detail on a package of additional measures, but had decided not to proceed with alternative options such as a compensation bond scheme and a property bond scheme. The property bond option had been the proposed option of the HS2 Action Alliance and a number of local authorities. Accordingly, a detailed consultation on a package of measures was launched in October 2012.

2.4 In March 2013, a Court decision on a challenge brought by the HS2 Action Alliance and others ruled that the January 2012 decisions had not been lawfully taken and that the Government had not considered the property bond option sufficiently. The Court’s ruling quashed the January 2012 decisions on property compensation, and so overturned the basis of the October 2012 consultation, which therefore could not proceed. The Government responded to the consultation by saying it would re-consult on property compensation options, including a property bond option. It is anticipated that this consultation will be launched in summer or early autumn 2013.

2.5 This paper considers the following issues:

§ What are the general operational principles of a “property bond scheme”? § What similar schemes are (or have been) in operation or are proposed by others? § What are the DfT policy criteria against which a property bond scheme should be assessed? § Consideration of the features of an proposed scheme (including scoring of options against the DfT policy

criteria) § Operation of the proposed form of property bond scheme § Comparison of the proposed form of bond scheme to existing proposals § Conclusions

2.6 A rigorous assessment of the likely costs and benefits, including a full evidential analysis and rigorous assessment to determine the optimum property bond scheme, could take 18 months or more to complete. In light of the timetable within which the revised public consultation is due to take place our conclusions are based on our knowledge of previous property bond schemes, untested propositions that we identify, and subjective opinion based on our professional judgement.

Department for Transport HS2 Property Bond Option 4

3 What is a property bond? 3.1 The concept of a property bond scheme is to help support the normal functioning of the property market by

providing eligible property owners with a mechanism that ensures no financial loss is suffered as a result of depreciation to property values that may be caused by proposed major infrastructure projects.

3.2 Such schemes are intended to underpin the market at levels before such proposals because the promoter would commit to purchasing properties – or compensating for any loss in value - if they could not be sold at or above the bond price.

3.3 The term ‘bond’ simply means a legal agreement, or promise, which would be attached to the deeds of a property and registered with the Land Registry. It would not in itself be a separate, tradable commodity.

3.4 These schemes do not have any legislative or statutory definition and therefore each has its own unique workings and characteristics. However, each scheme is based on the concept of being either “time based” or “value based”.

3.5 A time based scheme operates on the basis that if the subject property is not sold in the open market within a defined timetable, than the promoter of the works will acquire the property for the bond price.

3.6 A value based scheme operates on the basis that the promoter of the works will, if necessary, pay a “top up”, being the difference between the price that can be achieved in the open market and the bond price.

Department for Transport HS2 Property Bond Option 5

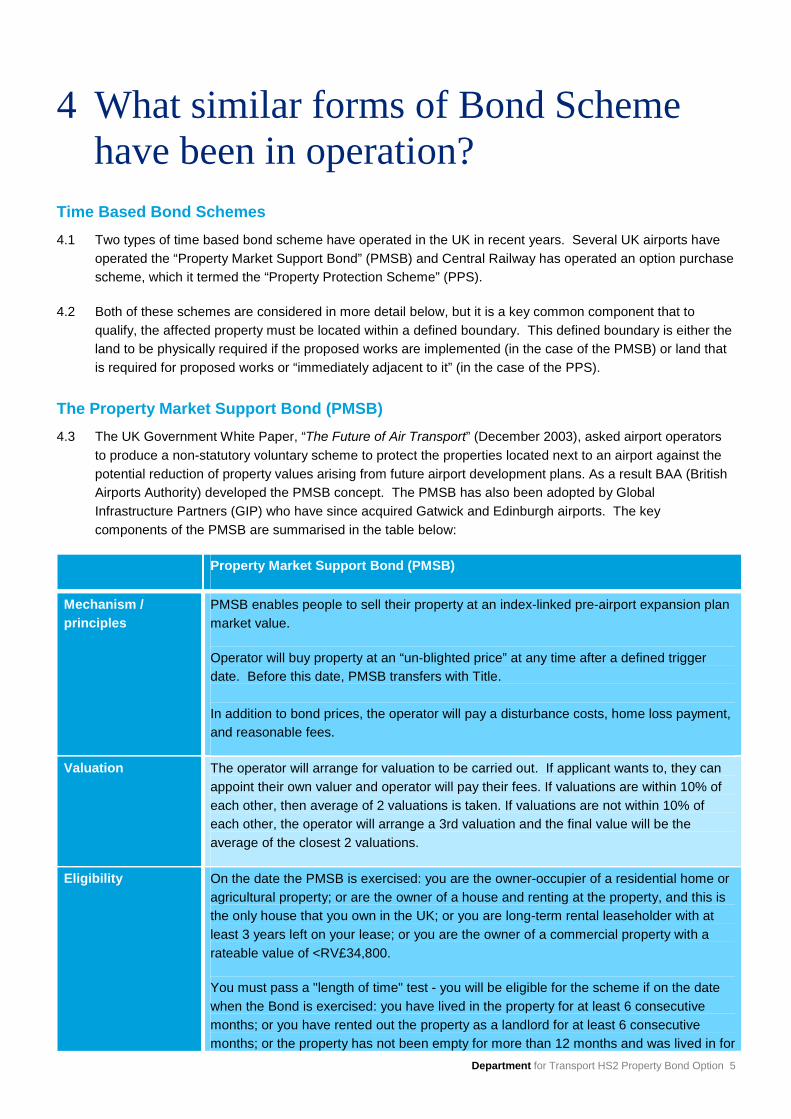

4 What similar forms of Bond Scheme have been in operation?

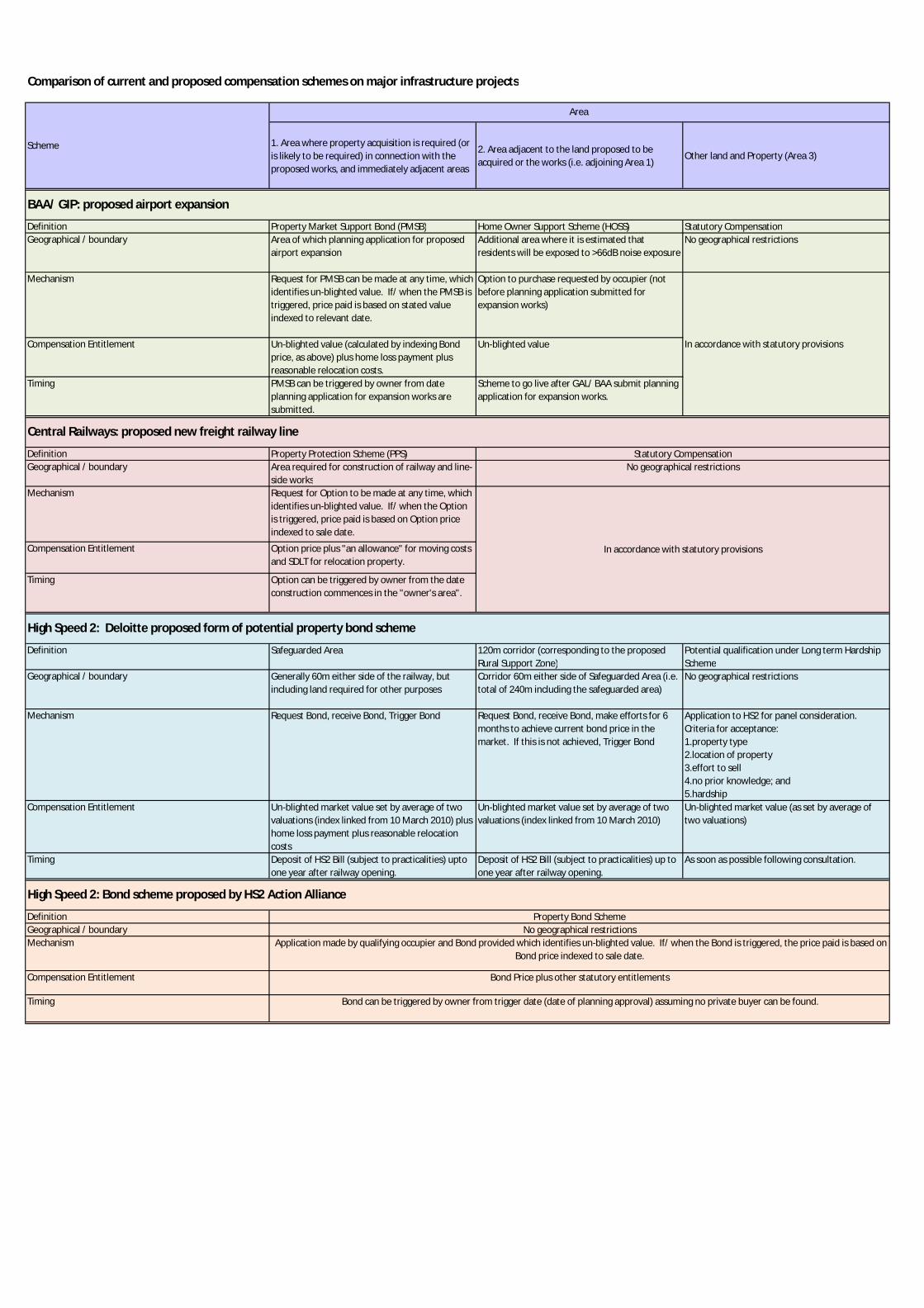

Time Based Bond Schemes 4.1 Two types of time based bond scheme have operated in the UK in recent years. Several UK airports have

operated the “Property Market Support Bond” (PMSB) and Central Railway has operated an option purchase scheme, which it termed the “Property Protection Scheme” (PPS).

4.2 Both of these schemes are considered in more detail below, but it is a key common component that to qualify, the affected property must be located within a defined boundary. This defined boundary is either the land to be physically required if the proposed works are implemented (in the case of the PMSB) or land that is required for proposed works or “immediately adjacent to it” (in the case of the PPS).

The Property Market Support Bond (PMSB) 4.3 The UK Government White Paper, “The Future of Air Transport” (December 2003), asked airport operators

to produce a non-statutory voluntary scheme to protect the properties located next to an airport against the potential reduction of property values arising from future airport development plans. As a result BAA (British Airports Authority) developed the PMSB concept. The PMSB has also been adopted by Global Infrastructure Partners (GIP) who have since acquired Gatwick and Edinburgh airports. The key components of the PMSB are summarised in the table below:

Property Market Support Bond (PMSB)

Mechanism / principles

PMSB enables people to sell their property at an index-linked pre-airport expansion plan market value.

Operator will buy property at an “un-blighted price” at any time after a defined trigger date. Before this date, PMSB transfers with Title. In addition to bond prices, the operator will pay a disturbance costs, home loss payment, and reasonable fees.

Valuation The operator will arrange for valuation to be carried out. If applicant wants to, they can appoint their own valuer and operator will pay their fees. If valuations are within 10% of each other, then average of 2 valuations is taken. If valuations are not within 10% of each other, the operator will arrange a 3rd valuation and the final value will be the average of the closest 2 valuations.

Eligibility On the date the PMSB is exercised: you are the owner-occupier of a residential home or agricultural property; or are the owner of a house and renting at the property, and this is the only house that you own in the UK; or you are long-term rental leaseholder with at least 3 years left on your lease; or you are the owner of a commercial property with a rateable value of <RV£34,800.

You must pass a "length of time" test - you will be eligible for the scheme if on the date when the Bond is exercised: you have lived in the property for at least 6 consecutive months; or you have rented out the property as a landlord for at least 6 consecutive months; or the property has not been empty for more than 12 months and was lived in for

Department for Transport HS2 Property Bond Option 6

at least 6 consecutive months before it was empty.

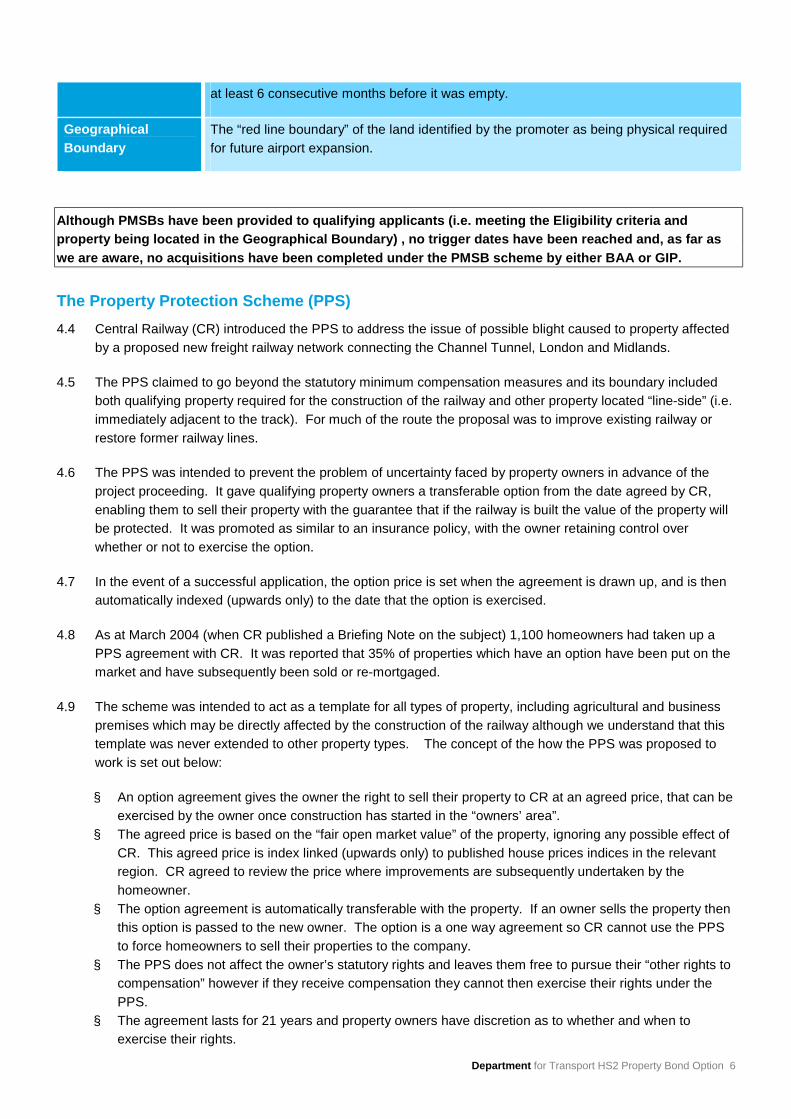

Geographical Boundary

The “red line boundary” of the land identified by the promoter as being physical required for future airport expansion.

Although PMSBs have been provided to qualifying applicants (i.e. meeting the Eligibility criteria and property being located in the Geographical Boundary) , no trigger dates have been reached and, as far as we are aware, no acquisitions have been completed under the PMSB scheme by either BAA or GIP.

The Property Protection Scheme (PPS) 4.4 Central Railway (CR) introduced the PPS to address the issue of possible blight caused to property affected

by a proposed new freight railway network connecting the Channel Tunnel, London and Midlands.

4.5 The PPS claimed to go beyond the statutory minimum compensation measures and its boundary included both qualifying property required for the construction of the railway and other property located “line-side” (i.e. immediately adjacent to the track). For much of the route the proposal was to improve existing railway or restore former railway lines.

4.6 The PPS was intended to prevent the problem of uncertainty faced by property owners in advance of the project proceeding. It gave qualifying property owners a transferable option from the date agreed by CR, enabling them to sell their property with the guarantee that if the railway is built the value of the property will be protected. It was promoted as similar to an insurance policy, with the owner retaining control over whether or not to exercise the option.

4.7 In the event of a successful application, the option price is set when the agreement is drawn up, and is then automatically indexed (upwards only) to the date that the option is exercised.

4.8 As at March 2004 (when CR published a Briefing Note on the subject) 1,100 homeowners had taken up a PPS agreement with CR. It was reported that 35% of properties which have an option have been put on the market and have subsequently been sold or re-mortgaged.

4.9 The scheme was intended to act as a template for all types of property, including agricultural and business premises which may be directly affected by the construction of the railway although we understand that this template was never extended to other property types. The concept of the how the PPS was proposed to work is set out below:

§ An option agreement gives the owner the right to sell their property to CR at an agreed price, that can be exercised by the owner once construction has started in the “owners’ area”.

§ The agreed price is based on the “fair open market value” of the property, ignoring any possible effect of CR. This agreed price is index linked (upwards only) to published house prices indices in the relevant region. CR agreed to review the price where improvements are subsequently undertaken by the homeowner.

§ The option agreement is automatically transferable with the property. If an owner sells the property then this option is passed to the new owner. The option is a one way agreement so CR cannot use the PPS to force homeowners to sell their properties to the company.

§ The PPS does not affect the owner’s statutory rights and leaves them free to pursue their “other rights to compensation” however if they receive compensation they cannot then exercise their rights under the PPS.

§ The agreement lasts for 21 years and property owners have discretion as to whether and when to exercise their rights.

Department for Transport HS2 Property Bond Option 7

§ In addition to the option price itself, the homeowner also receives “an allowance” to help with moving costs and an additional sum for the stamp duty on the alternative property purchased.

4.10 The PPS includes properties required for the proposed rail link and other “line-side” properties. It did not operate where the railway would be in tunnel, and CR reserved the right to review each application on a case by case basis.

4.11 In 1997, The Interdepartmental Working Group on Blight, which was set up by DETR to consider how best to deal with the generalised blighting effect of major infrastructure projects, reported (at paragraph 7.19.2 of their Final Report that the PPS “came closer than any other to addressing these concerns”.

The Central Railway project is not currently being pursued. The trigger date (commencement of construction in the “owners’ area”) did not commence and therefore no property was acquired by CR pursuant to the PPS scheme.

Summary of time based bond schemes 4.12 There are several key common features of the PMSB and PPS time based bond schemes:

§ To qualify, applicants must be residential owner-occupiers, or owner-occupiers of small business premises, and also meet other qualifying criteria.

§ The subject property must be within an identified boundary, which is essentially the land physically required for the proposed works or “immediately adjacent” to it.

§ If accepted, the bond price would be identified at the outset as the “pre-impact” value, and be index-linked to the date of acquisition by the promoter. This acquisition would be available after a defined “trigger date”, which is a key milestone in the timetable for the proposed works (i.e. a planning application being submitted or works commencing).

§ None of the proposed works that these bond schemes relate to have become sufficiently advanced for the trigger dates to be met. Although bonds have been provided, no acquisitions have ever been completed pursuant to these schemes.

Value based bond schemes 4.13 We have identified two “value based” bond schemes that have been offered by promoters of major

infrastructure projects. Summaries of these are set out below:

4.14 The Home Owner Support Scheme (HOSS): This is a scheme operated by BAA and GIP in addition to their PMSB scheme. The extent of land covered by the HOSS is defined as being those qualifying properties which are not required in connection with proposed airport expansion, but which might be subject to noise above a 66dB threshold as a result. Briefly, under the HOSS, if qualifying homeowners are unable to sell for a price within 15% of the market value then the airport will buy the property at an un-blighted price. If they can sell within 15% of market value, the airport will make a contribution to sales costs (of up to 5% of the sales price) to assist with the move process.

4.15 The EdF Main Site Neighbourhood Support Scheme: The EdF scheme applies to residential property within a defined boundary that is located close to the site of the proposed new nuclear power station at Hinkley Point (Hinkley Point C), but is not directly required for the development (which is being built on land that is mostly already owned by the promoter). Under this scheme, both parties’ valuers assess the pre-Hinkley Point C value (September 2008) and take an average. If the homeowner chooses to sell, the September 2008 indexed value is calculated and compared to market value on date of sale; irrespective of the price achieved, the difference between these numbers is paid in compensation together with a fixed £5,000 for moving costs.

Department for Transport HS2 Property Bond Option 8

Summary of value based bond schemes 4.16 There are several key common features of the HOSS and EdF valued based schemes:

§ To qualify, applicants must be residential owner-occupiers. § The subject property must be within an identified boundary where criteria for potential impact can be

assessed in an unambiguous and clear way. § The qualifying homeowner may be required to sell at a price which is less than the open market value

that would have been achieved in the absence of the proposed works. That homeowner might receive some financial assistance from the promoter of the scheme to compensate for this financial shortfall, but this is not a tool to underpin the market, or to bring stability to it.

The Proposals of HS2 Action Alliance (HS2AA) 4.17 HS2AA has constructed a form of “Recommended Bond Scheme” (RBS) that it has suggested HS2 Ltd

should adopt. This bond scheme would be available to property owners who suffer a “loss in property value” due to HS2. It would remain in effect until one year after HS2 becomes operational (2027 at the earliest for Phase 1).

4.18 Under this scheme, eligible owners would be able to apply to HS2 Ltd for a property bond. The bond would guarantee that HS2 Ltd will assume a role of “purchaser of last resort” and purchase the property at an ‘un-blighted value’ in the event that the HS2 project has reached a specified trigger point (i.e. planning approval date) and no private buyer is found at the un-blighted price when the owner wants to sell.

4.19 This proposed scheme would have no qualifying reason for sale, restrictions on proximity, impact or threshold loss. The sole criteria would be whether or not there is a financial impact on the market value of a property due to HS2.

4.20 In order to provide an incentive to sell property privately (rather than to exercise the bond) it is proposed that properties held with a bond are exempt from Stamp Duty Land Tax (SDLT).

4.21 Under the proposed scheme, any bond still in place when construction of HS2 has finished and train operation has begun would entitle the owner to compensation of the loss in value from HS2 rather than the statutory compensation provisions (under Part 1 of the Land Compensation Act 1973).

4.22 HS2AA have identified some “general conditions” that must be met:

§ A property must have been marketed for a minimum period (determined by price bands). § No ‘serious offers’ at blight-free value (with evidence to justify this value) be made. § The belief that its reduced value is due to HS2 must be reasonable and evidenced.

Issues with the HS2AA proposed form of bond scheme 4.23 The property bond scheme proposed by HS2AA raises various issues of practicality, administration and cost.

These concerns and issues that we have raised in respect of this scheme have influenced our review and assessment of a property bond scheme that we consider to be “proposed”, which is set out below.

4.24 Our main concerns with the HS2AA proposed bond scheme are:

§ It has no geographical boundary. This means that, in theory, any owner of any property could request a bond from HS2 without having to provide any rationale or evidence as to why they think their property values is either affected by HS2, or might be in the future. This evidence would only need to be provided in the event that the bond was exercised at some later date (when the bond holder would be requesting purchase by the bond scheme operator).

Department for Transport HS2 Property Bond Option 9

§ A property bond scheme with no geographical boundary is unprecedented: in fact, the PMSB and PPS schemes had geographical boundaries linked to the extent of land required for the proposed works, which is comparable to the “safeguarded” area for HS2.

§ Although it is not absolutely clear how the HS2AA would envisage its proposed scheme to operate, it would appear that in order to function as the HS2AA proposes (i.e. with absolute transparency on the housing and mortgage markets), each bond would need to state an “un-blighted” value. The mechanism for this is not stated, but it could involve two estate agents or surveyors undertaking “no-HS2 World” valuations and an average being taken, with reference to a third party if these two valuations were significantly different. The administrative cost to put these bonds in place could be substantial and a significant element of this cost could be abortive expenditure.

§ HS2AA propose that there should be no threshold on the loss that is suffered before the bond can be

triggered; merely that the bond holder is unable to obtain the “un-blighted value” in the market. The PMSB and PPS schemes have been offered by HS2AA as examples of where there was no threshold of loss, however on both these schemes it was necessary to own a property that was actually required for the works (rather than potentially affected by the works) to qualify for a bond, and this bond can only be triggered after a defined date. There was no requirement to demonstrate loss in value as, after this trigger date, the promoter of the works would actually want (and need) to acquire the property.

§ It is not clear how the RBS would work for property that is physically required for HS2 (being either directly along the route or within the safeguarded area). The PMSB and PPS schemes were designed purely for property that would be directly affected in this way. It would not be appropriate for the “general conditions” (of qualification) to be met in these circumstances, and the timing and mechanism could mean the statutory blight provisions would provide a more certain and defined mechanism to property owners in this category.

§ It is proposed that 'eligible' properties should be exempt from stamp duty in order to incentivise sales. As there is no geographical boundary to receive a bond, any property owner wishing to sell their property could obtain a bond and therefore avoid SDLT having to be paid on the disposal price. Even with a geographical boundary this would have contingent liability and potential fraud implications.

§ If SDLT were waived on bond property, purchasers in the market may be willing to pay a higher price for

property as they would not need to allocate a budget for the payment of SDLT. This may, in turn, mean that more property is sold in the market and therefore fewer properties would need to be acquired by HS2. However, such an arbitrary “sweetener” may simply have the self-fulfilling impact of increasing the price by an equivalent amount. The “normal” market functions with SDLT, so this could be a further signal that the market is not “normal”, and could also reinforce impacts around the boundary. It could also make it more difficult for valuers to assess how the market is functioning as it introduces a distortionary lack of comparability in and out of the bond area.

§ The mere presence of a bond on a property could have a negative impact on the marketability of that property due to the perceived future impact. For example, although HS2 might not have any impact on the value of a particular bond-held property, the fact that the property has a bond may result in potential purchasers thinking that some future impact is more likely when compared to a property without a bond. Although this potential purchaser will be aware that – in the event of future impact - HS2 will acquire the property for a specified future price, this may not be consolation for the upheaval and other impacts of having to move. This “purchaser psychology” cannot be tested as no property bond schemes have previously been put in place in respect of property that is not directly required in connection with proposed infrastructure works.

Department for Transport HS2 Property Bond Option 10

§ The HS2AA RBS is introducing an entirely new concept of property bond, which is fundamentally different to anything that has been used in the UK (past or present) to deal with the potential impact of any other proposed major infrastructure project.

A bond scheme that only becomes capable of being triggered after the opening of HS2

4.25 We have also been asked to consider the case for a variant on the type of bond scheme devised by HS2AA, under which bonds only become capable of being triggered after the opening of HS2. This option has been suggested on the basis that it may reduce potential adverse impacts of a bond scheme while still helping to reinforce market confidence and prevent blight during the construction phase, minimising the need for bonds to be triggered. In our view, putting a greater number of obstacles in the way of triggering the bond (and arguably creating a much less attractive and helpful scheme) would introduce a level of uncertainty that would not be likely to support the housing market. A purchaser of a property with a bond might have to wait 12 years before having the assurance that the bond scheme operator would be willing to acquire his property (in the event that he was unable to sell it) and the price he or she would be willing to pay today would be likely to reduce as a consequence.

4.26 In addition to the operation of HS2, the impacts of construction (whether they are perceived or actual) could create market impacts that this type of bond scheme would do little to address. Furthermore, the “compensation” payable (effectively being the depreciation caused as a result of the operation of HS2) is unlikely to be dis-similar to a property owner’s statutory entitlement under Part 1 of the Land Compensation Act 1973.

4.27 This form of bond scheme could operate for a lower total cost then the proposed bond scheme we have identified. “Value for money” is one of the Policy Criteria (set out in section 5, below) which we have considered, and this form of bond scheme could therefore achieve a higher score against this criteria. However, as set out above, there are deficiencies with this proposal which would result in a lower score for at least three other Policy Criteria (Fairness; Community cohesion; and, Functioning of Housing Market) and our proposed bond scheme produces a higher overall score.

Alternative Schemes – a summary 4.28 Appendix 3 to this report sets out a summary comparison of the property bond schemes provided by airport

operators (BAA/ GIP) and Central Railways, split into three different geographical boundaries (the land required for and immediately adjacent to the scheme, the land adjacent to this area, and other land). This analysis is compared to two concepts proposed for HS2 – the proposed form of bond scheme we have identified (details of which are set out below), and the form of bond scheme proposed by HS2AA.

Department for Transport HS2 Property Bond Option 11

5 Relevant Policy Aims 5.1 Before giving consideration to the optimum form of bond scheme that might be appropriate for HS2, the

Department for Transport has identified five policy aims (referred to as the Policy Criteria) against which all options for consideration have been assessed. These are:

§ Fairness – the Government should ensure that owner-occupiers whose properties (and property values) are most directly and specifically affected by the proposals for Phase One of HS2 are eligible for compensation; and that those eligible for compensation receive fair and reasonable settlements reflecting the location and circumstances of their property.

§ Value for money – the Government should ensure that HS2 property schemes are likely to offer satisfactory value for money to the taxpayer, are affordable, do not involve disproportionate expense and that any risks relating to the costs of property schemes can be effectively managed, within HS2’s long term funding settlement.

§ Community cohesion – the Government should maintain as far as practicable the stability and cohesion of communities along the route, for example by enabling existing residents to remain in their homes where possible; by minimising the potential adverse effects of significant population turnover associated with multiple short-term tenancies; by ensuring that there is the best understanding about the likely effect of the railway on the enjoyment of properties; and by compensating those most affected by the project on a fair and reasonable basis.

§ Feasibility, efficiency and comprehensibility – the Government should devise clear and easily explained rules so that home owners can readily understand their entitlements and the Government can predict how costs will be determined in any individual case. It is important also to have assurance that any scheme can be administrated efficiently and effectively to provide good customer service for those whose property is affected by the railway.

§ Functioning of housing market – the Government should enable local residential property to function as normally as possible during the development and construction phases of the railway project.

Department for Transport HS2 Property Bond Option 12

6 Features of a property bond scheme 6.1 In determining the headline features of the proposed form of property bond scheme, we have considered the

options for eight different bond “components” under four broad categories:

§ Overall Bond Concept o Value based or time based approach?

§ Criteria o Boundary o Definition of Qualifying Interest

§ Mechanism o Fixing base price and indexation approach o Demonstrating efforts to sell (where appropriate)

§ Timetable o Earliest date for applying and triggering the bond o Active marketing period before triggering the bond o Expiry date for triggering the bond

6.2 We have considered these options in the context of our experience of major infrastructure projects, having regard to published evidence (regarding the operation of the property market and the properties along the route of HS2) and our previous experience and knowledge of bond schemes and other forms of “discretionary purchase”.

6.3 However, we have not been able to undertake any meaningful quantitative assessment or sensitivity analysis. First, we have only had a short time available to undertake this exercise of review and recommendation and we would expect that a full review and preparation of an evidence tested model, with full scenario testing and sensitivity analysis, could take 18 months or more to complete.

6.4 Second, and more significantly, whilst other bond schemes have been introduced, no property has ever been acquired pursuant to these schemes and, in any event, the boundary for these includes only property that it actually proposed to be acquired for the underlying works. With more time available, quantitative analysis could be undertaken; however some subjective analysis would always be necessary when considering the behaviour of qualifying landowners and purchasers.

6.5 We have also scored each option against the Policy Criteria identified above, and a summary of our scoring matrix is contained as Appendix 2. This scoring matrix also sets out the detail of the variables we have considered for each of the eight component parts. As a comparison, Appendix 2 also sets out our Policy Criteria scoring for the “Voluntary Purchase Scheme” which is also being considered by HS2.

Overall Bond Concept

Value based or time based approach? 6.6 As previously considered, there are two fundamental bases on which a bond scheme could operate. Firstly,

a “time based” scheme which requires the promoter of a scheme to acquire qualifying property at the “pre-impact” price following a particular event and secondly, a “value based” approach which requires the promoter to pay a “top up” in the event that an “un-blighted” price cannot be achieved by the owner.

Department for Transport HS2 Property Bond Option 13

6.7 In our view, a time based scheme would create greater certainty in the market and allow it to function in the most unaffected way.

6.8 The property market is created by certainty; homeowners want the ability to trade on the market and the ability to buy and sell freely without external influences. Mortgage lenders, who have a vested interest in the event of arrears or default, will have the same criteria and any detrimental impact on the market (which, at this stage is influenced largely by perception) will cause uncertainty and potential changes to lending criteria.

6.9 Due to the lack of progress with other bond schemes, we cannot point to any clear evidence of the general impact that property bonds have on property markets. However it would appear logical that where there is a defined scheme where the bond price (and mechanism for future change and acquisition) is certain, the property market can also be more certain.

6.10 A “value based” approach would effectively require HS2 to underpin market impact, which will (to some degree) be linked to perception and uncertainty which may prove to be a short term issue [as homeowners may “fear the worst” before further details can be provided (on mitigation measures, route alignment, environmental protection etc.)] . An agreement to “crystallize” this loss now will effectively mean accepting a principle of loss that may be short term, and perceptive only. As this depreciated sale would become a market transaction which would become a “comparable” market transaction, this is likely to have a cumulative effect beyond whatever geographical boundary might be set.

6.11 In addition to crystallizing a loss that may only be perceptive and temporary, a value based scheme could encourage market sales at artificially low prices (on the basis that the vendor will receive a larger “top up” from the bond scheme operator), which will risk a more significant and widespread impact on local property markets.

6.12 Having a “value based” approach also risks greater exposure to fraud. For example, Landowner A could agree to sell his property to Landowner B for a 40% discount, and obtain this 40% difference from HS2. At the time of sale, Landowner B (who is more than happy with the reduced price achieved) could agree to make an additional payment of 10% to Landowner A in acknowledgement of the discounted price agreed. Landowner A has got 110% of the value (60% initial payment, 40% from HS2, 10% top up payment), Landowner B has paid a total of 70% (60% initial payment and 10% top up) and HS2 has paid compensation of 40%.

Criteria

Boundary 6.13 There are, broadly, four categories of boundary, all of which have their pros and cons.

§ Unbounded; § A variable boundary by reference to the increase in assessed noise level from the operation of the

railway; § A fixed boundary by reference to the linear distance from the centre line of the permanent way; and, § A defined boundary having regard to local topography and pattern of settlements.

Unbounded

6.14 We have considered if a “no boundary” scheme, of the sort proposed by the HS2AA, would be practicable. Whilst a bond may potentially benefit an unlimited number of homeowners, we have concluded that it would not. With an unlimited boundary, in theory any owner of property could request a bond from HS2 without having to provide any rationale or evidence as to why they think the value of their property is either affected by HS2, or might be in the future. Homeowners who might be hundreds of metres (or hundreds of miles)

Department for Transport HS2 Property Bond Option 14

from the works might apply, risking a huge administrative burden, with every property being inspected and valued. Moreover, the universal presence of a bond might, in itself, exacerbate the perception of blight, and so create self-fulfilling blight conditions.

6.15 On this basis, some boundary will be necessary to limit the perception of blight and to avoid an unreasonable administrative burden, which would be contrary to the “Feasibility, Efficiency and Comprehensibility” Policy Criteria.

6.16 Moreover, we are not aware of any evidence as to how such an unbounded scheme would operate in practice, as it is unprecedented. The schemes that we have reviewed are the PMSB (Airport) and PPS (Railway) schemes, both of which had specific geographical limits linked to the extent of land actually required for the works.

Variable boundary based on predicted noise levels

6.17 After rejecting the concept of an unbounded scheme, we sought to identify whether a more ‘scientific’ site-specific boundary might be appropriate. A noise-based boundary would be based on the noise caused by the operation of the railway. This would present a number of difficulties. Apart from the practical difficulties of establishing an accurate noise contour, from work previously undertaken by DfT, we understand that only about 60 properties would be entitled to noise insulation under current regulations. As such, a lower threshold might need to be adopted to increase the number of qualifying properties, which could set a precedent that potentially lowers the threshold for “Part 1” claims at a later date. A noise level based contour would suggest that operational noise is the sole issue that might cause a “blighting effect”. From our experience at public consultation events, the blighting effect is caused not only by noise, but by a variety of factors (perception, the presence of the railway, visual amenity, topographical features, construction noise, and possible road diversions), which are specific to the individual location and individuals’ perceptions. That is, it is far from scientific.

6.18 So, whilst in theory a scientific approach based on noise levels might be considered to be attractive because of its objectivity, it would in our view be very difficult to assess in practice and not necessarily end up being consistent and fair. For these reasons, we do not consider a noise level boundary to be appropriate.

A fixed boundary by reference to the linear distance from the centre line of the permanent way

6.19 We understand that the concept of a fixed boundary of “potential impact” was adopted by the promoter of High Speed 1 (previously known as the Channel Tunnel Rail Link) in 1988. This corridor was based on a 40m wide permanent way (i.e. that area permanently required and contained within the line side fence either side of the railway) together with two corridors, each 100m wide, on either side. We understand that this corridor was used as it was thought to represent the area within which there may be a discernible impact from the operation of the railway

6.20 For High Speed 1, this 240m corridor (120m on each side) was adopted in the period from 1988 to 1993, when the design and route alignment was more certain. In 1993, the 120m on each side was replaced by the “Limit of Land to be Acquired or Used” (“LLAU”) which was a reduced area (not dis-similar to the safeguarded area) of potential impact. The Channel Tunnel Rail Link Act received Royal Assent three years later in 1996.

6.21 We have considered whether any fixed boundary should be any different to the 120m on each side used in the early stages of High Speed 1. For the reasons set out below we have concluded that it should not.

Department for Transport HS2 Property Bond Option 15

Defined boundary having regard to local topography and settlement patterns

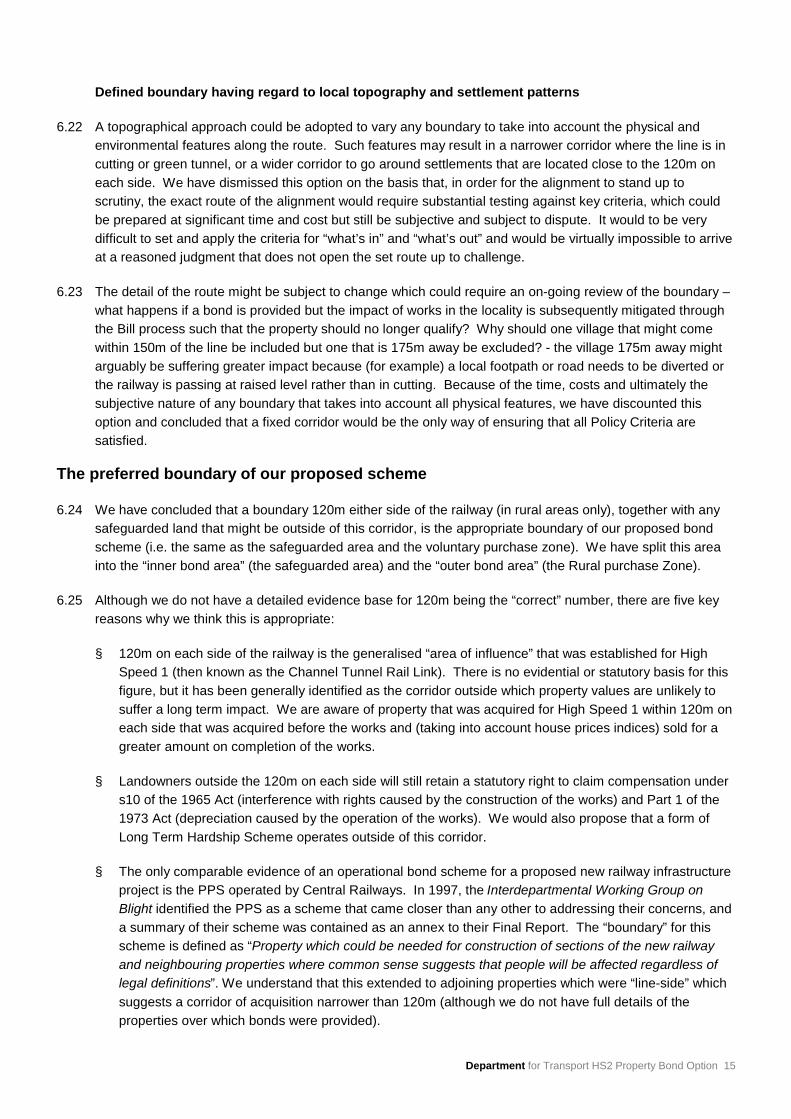

6.22 A topographical approach could be adopted to vary any boundary to take into account the physical and environmental features along the route. Such features may result in a narrower corridor where the line is in cutting or green tunnel, or a wider corridor to go around settlements that are located close to the 120m on each side. We have dismissed this option on the basis that, in order for the alignment to stand up to scrutiny, the exact route of the alignment would require substantial testing against key criteria, which could be prepared at significant time and cost but still be subjective and subject to dispute. It would to be very difficult to set and apply the criteria for “what’s in” and “what’s out” and would be virtually impossible to arrive at a reasoned judgment that does not open the set route up to challenge.

6.23 The detail of the route might be subject to change which could require an on-going review of the boundary – what happens if a bond is provided but the impact of works in the locality is subsequently mitigated through the Bill process such that the property should no longer qualify? Why should one village that might come within 150m of the line be included but one that is 175m away be excluded? - the village 175m away might arguably be suffering greater impact because (for example) a local footpath or road needs to be diverted or the railway is passing at raised level rather than in cutting. Because of the time, costs and ultimately the subjective nature of any boundary that takes into account all physical features, we have discounted this option and concluded that a fixed corridor would be the only way of ensuring that all Policy Criteria are satisfied.

The preferred boundary of our proposed scheme

6.24 We have concluded that a boundary 120m either side of the railway (in rural areas only), together with any safeguarded land that might be outside of this corridor, is the appropriate boundary of our proposed bond scheme (i.e. the same as the safeguarded area and the voluntary purchase zone). We have split this area into the “inner bond area” (the safeguarded area) and the “outer bond area” (the Rural purchase Zone).

6.25 Although we do not have a detailed evidence base for 120m being the “correct” number, there are five key reasons why we think this is appropriate:

§ 120m on each side of the railway is the generalised “area of influence” that was established for High Speed 1 (then known as the Channel Tunnel Rail Link). There is no evidential or statutory basis for this figure, but it has been generally identified as the corridor outside which property values are unlikely to suffer a long term impact. We are aware of property that was acquired for High Speed 1 within 120m on each side that was acquired before the works and (taking into account house prices indices) sold for a greater amount on completion of the works.

§ Landowners outside the 120m on each side will still retain a statutory right to claim compensation under s10 of the 1965 Act (interference with rights caused by the construction of the works) and Part 1 of the 1973 Act (depreciation caused by the operation of the works). We would also propose that a form of Long Term Hardship Scheme operates outside of this corridor.

§ The only comparable evidence of an operational bond scheme for a proposed new railway infrastructure project is the PPS operated by Central Railways. In 1997, the Interdepartmental Working Group on Blight identified the PPS as a scheme that came closer than any other to addressing their concerns, and a summary of their scheme was contained as an annex to their Final Report. The “boundary” for this scheme is defined as “Property which could be needed for construction of sections of the new railway and neighbouring properties where common sense suggests that people will be affected regardless of legal definitions”. We understand that this extended to adjoining properties which were “line-side” which suggests a corridor of acquisition narrower than 120m (although we do not have full details of the properties over which bonds were provided).

Department for Transport HS2 Property Bond Option 16

§ Although we have not undertaken any financial analysis, a widening of the corridor will open up a greater number of potentially qualifying properties. For example, (according to data we have seen) if this corridor were to be increased from 120m to 300m, there would be 56% increase in potentially qualifying interests, from about 1,600 to about 2,500.

§ A widening of the corridor would present a perception that we consider (and perhaps accept) this is the zone of potential impact. In addition to the higher numbers of bonds that may be sought (and, possibly, triggered), accepting a wider corridor could influence a boundary precedent for successful “Part 1” claims when the HS2 trains start running.

6.26 The cause of any impact to property prices will, in most cases, result from either the construction or operation of the railway. If follows from this that the further away from the railway line that property is located, the less likelihood there is that property values will be impacted. We have identified that the 120m on each side is an established “area of influence” and would expect that – generally speaking – property located close to the outer extremity of this corridor is less likely to be affected then property closer to the proposed route alignment. It would follow that at the outside of the boundary the impact may be reduced (and in some cases negligible) and there would be fewer purchases required. Although our proposed bond scheme has a defined corridor, we would expect different market characteristics within that corridor.

6.27 There will inevitably be some cases where the personal circumstances of home owners outside of this corridor results in HS2 having an impact. However, there is no evidence to suggest a different corridor boundary - which would be purely arbitrary in any event – is appropriate and, as considered above, a “no boundary” model would fail most of the Policy Criteria we have been asked to consider. To take this into account we suggest that a form of hardship scheme (currently known as the exceptional hardship scheme) continues to operate outside of the bond boundary.

Definition of Qualifying Interest 6.28 We have concluded that the proposed bond scheme should apply to owner-occupiers of residential property,

with this being extended in the inner bond areas to those parties who would otherwise be entitled to serve a blight notice (residential owner occupiers, owner-occupiers of small business premises (with a rateable not exceeding £34,800) and owner occupiers of agricultural units). The rationale for this is that any impact in the outer bond area, which is not actually required for HS2, is likely to be limited to residential property (although there may be exceptions to this) as commercial property values do not normally reduce as a result of being located near a road or railway, whereas residential property values may do: it has a more personal and emotive impact.

6.29 In the inner bond area, the bond scheme could offer a credible and perhaps more attractive option to the service of a blight notice (under the statutory compensation regime), which both the landowner and HS2 might prefer because of the certainty that it provides.

Mechanism

Bond – Fixing Base Price and Indexation Approach 6.30 To identity the value of the property interest in the most appropriate way, we consider it appropriate to have

regard to the valuation date immediately prior to the announcement of the HS2 route and apply an indexation (based on a wider sample of property values) from that date to the date of sale. As the initial proposed route for HS2 was published on 11 March 2010, we consider that a date of 10 March 2010 is appropriate for this purpose.

6.31 The concept of valuing with regard to an antecedent valuation date is the usual method adopted in valuing pursuant to compulsory purchase (when the date of entry marks the valuation date but a claim might not be

Department for Transport HS2 Property Bond Option 17

submitted until months or years later) and is also used for assessing business rates and Council Tax bands. Given the information on historical house price transactions, which is publically available, we do not consider this should present any practical difficulties.

6.32 For the purpose of indexation, we suggest adopting the House Price Index (HPI) operated by the Land Registry, which publishes a monthly index of house prices at national, regional, London Borough and County level. Indexation for the following areas will be required: London Borough of Camden, Buckinghamshire, Oxfordshire, Warwickshire and Staffordshire.

Demonstrating "Effort to Sell" (where appropriate) 6.33 We have considered whether the Bond Holder, if required to demonstrate efforts to sell, should be required

to accept a price in the open market that is lower than the bond price, but close to it (say within 10% or 15%).

6.34 This requirement could undermine the overall concept and purpose of a bond scheme, and be contrary to the Policy Criteria, as it would have the impact of creating an artificially low market. Potential purchasers would know the bond holder has to accept a “low” price, and speculators could offer a price £1 higher than the minimum threshold and the bond holder could be required to accept it.

Timetable

Earliest Date for applying for and triggering the bond 6.35 We consider that an appropriate date for the commencement of a bond scheme (assuming that it would not

require legislative consent) could be the date on which the Hybrid Bill for HS2 is Deposited to Parliament (expected to be late 2013), as this is analogous with the date of “making” a compulsory purchase order (CPO) which is generally regarded to be the date on which the underlying proposal becomes more certain and the provisions for statutory blight commence.

6.36 As the Hybrid Bill process runs its course and the HS2 project gathers momentum, there will be increased certainty that HS2 will be built, and a positive vote from the House of Commons at the Second Reading of the Bill (due Spring 2014) should provide a clear signal that HS2 is likely to proceed. This later milestone might be more appropriate, and will provide some time for the administration for the scheme to be established.

6.37 To try and avoid potential congestion of applications following the commencement of the scheme, we suggest that for the first six months, only qualifying interests located in the inner bond area, and qualifying interests in the outer bond area who wish to put their homes on the market, would be able to qualify for the bond scheme. After six months we suggest it would be open to all qualifying applicants in both the inner and outer bond areas.

Active marketing Period before triggering the bond (where appropriate) 6.38 In the outer bond area, we consider it reasonable for efforts to be made to dispose of the property in the

open market before the bond can be “triggered” and acquired by the bond scheme operator. It is suggested that this is not a requirement in the inner bond area.

6.39 We have adopted six months as being the period for which property must have been marketed and not sold (subject to contract), before the Bond can be triggered. This has been assessed with regard to the current (June 2013) average length of time that property has been on the market and unsold. The website www.home.co.uk suggests the following “days unsold” for different property types in Counties along the route of HS2:

Department for Transport HS2 Property Bond Option 18

Property Type Northants Warwickshire

Detached 158 165

Semi-detached 130 143

Terrace 148 153

Flat 192 172

All 152 159

6.40 The average of the two areas is 156 days, which is just over 22 weeks or 5.2 months, which we have rounded to six months.

Expiry date for triggering the bond 6.41 We have identified that the life of the bond should extend to a date one year (less one day) after the trains

start running, following which bond holders will be able to claim statutory compensation pursuant to Part 1 of the 1973 Act. This will ensure a fair entitlement to compensation, with no break in service. Where a property is physically required for the works, this expiry date will be the date of possession pursuant to the HS2 Act.

Review of possible response rate and trigger rate of a property bond 6.42 As we have previously identified, there is an absence of other property bond schemes that have advanced to

a stage of property acquisition. This means that much of our assessment and review is based on a qualitative assessment and subjective behavioural review rather than a sound evidence base.

6.43 An example of this uncertainty can be illustrated by reviewing the potential “take up” rate at various stages of the bond process.

6.44 Once the geographical boundary of a property bond scheme has been established, it should be fairly straightforward to determine the number of qualifying properties. In the case of the proposed bond scheme, we have received data from DfT that suggests that, there are a total of 823 dwellings within the inner bond area (i.e. excluding other properties that may be able to serve blight notices) and an additional 788 dwellings in the outer bond area. We do not know when these dwellings were counted, and what revisions to land requirements and definitions may have taken place since this time, but this suggests a total of about 1,600 homeowners may qualify to apply for a bond under our proposed scheme.

6.45 From this headline number we could determine the “worst case” gross cost of acquisition (i.e. the unaffected property value of all the qualifying properties within the boundary, plus other associated fees and costs), but this is unlikely to be a realistic outcome. To achieve this, we need to consider the component stages of the process, and at each stage this introduces a greater degree of subjectivity and potential variance. The summary outcome is likely to produce a range of potential outcomes (and subsequently values) that is too large to be helpful.

6.46 In order to undertake an evidential analysis it would be necessary to model outcomes to the following questions:

Department for Transport HS2 Property Bond Option 19

§ How many applications for bonds would be submitted by qualifying owners, and over what time duration? As set out above, on our proposed scheme we understand from information provided by DfT that 1,600 homeowners (excluding other qualifying interests in the inner bond area) might be entitled to apply for a bond (although we have suggested that only property owners in the outer bond area who actually wish to move can apply in the first six months of operation).

§ How many bond holders would wish to sell their property during the life of the bond? Government sources state that there are about 19 million private dwellings in England and a current annual sales rate of 750,000 per annum, meaning that about 4% of private dwellings are sold each year. We have identified there are about 1,600 residential properties within our proposed bond boundary area, so in the absence of HS2, we might expect 64 of these to transact in the market each year. Assuming a bond “life” of 13 years (2014 to 2027), this means that (assuming the property market is not influenced, in any direction, by HS2) we could expect 52% of property to transact during this period (although this will include property that sells more than once during this period). We can expect a higher “churn” rate in the inner bond area (as property owners will be aware that their property will be required), but whether HS2 results in a greater “churn” rate in the outer bond area will depend on a whole host of factors including local perception and neighbourhood issues, the overall physical impact of HS2 in the locality, and the provision of information (on noise mitigation, construction methodology etc.) that may enable more reasoned judgements to be made.

§ What proportion of property owners (in the outer bond area) will be able to sell in the open market? How many property owners will be unable to sell and trigger bonds requiring HS2 to acquire? These are the two questions that we cannot provide any evidential support for. If the bond scheme were to operate as purely as theory would suggest, the property market would continue to operate in a manner unaffected by HS2, and intervention by the bond scheme operator would be infrequent. However, the practical application of this is something that has not been tested and any estimates on take up rate would be based on reasoned speculation rather than evidenced analysis.

Department for Transport HS2 Property Bond Option 20

7 Operation of the proposed bond scheme 7.1 From the conclusions reached from our analysis we have identified a proposed form of bond scheme. The

seven separate procedural steps of this proposed design are set out below, with definitions of terms used set out in blue boxes and additional explanatory notes and comments shown in pink boxes.

7.2 Within this commentary, some details are provided on the timetable for service of various notices that we propose would be required as part of the process. These are summarised at the end of this note.

Step 1: Qualifying criteria to apply for a Bond 7.3 At any time after commencement of the bond scheme the owner of a Qualifying Interest can apply for a

Bond. A simple application form, capable of completion directly by the applicant, will be available on a website run by the bond scheme operator.

“Qualifying Interest” – The owner occupier of a residential dwelling or mixed hereditament (i.e. residential property held together with commercial premises under single occupation) that is located within (or substantially within) either the Inner Bond Area or the Outer Bond Area. For properties within the Inner Bond Area, this definition is extended to include any persons who would otherwise be entitled to serve a “blight notice” (i.e. owner occupier of business property with a Rateable Value below RV£34,800 and owner occupiers of agricultural units). The Qualifying Interest must have been acquired prior to the Base Date

“Inner Bond Area” – the area safeguarded for HS2.

“Outer Bond Area” – the area also known as the Rural Support Zone, being the area outside of the safeguarded area, outside of the M25 and within 120m either side of the centre line of HS2.

“Base Date” is 10 March 2010, being the day before the initial announcement of the initial alignment of the HS2 route.

We suggest that the bond scheme commences following a positive vote from the House of Commons at the Second Reading of the Bill (due Spring 2014) as this should provide greater certainty that HS2 is likely to proceed. This date will provide time for the administration for the scheme to be established.

To try and avoid potential congestion of applications following the commencement of the scheme, we suggest that for the first six months, only qualifying interests located in the Inner Bond Area see definition below), and qualifying interests in the Outer Bond Area (see definition below) who wish to put their homes on the market, would be able to qualify for the bond scheme. After six months we suggest it would be open to all qualifying applicants in both the Inner Bond Area and the Outer Bond Areas.

Step 2: Issue of the Bond 7.4 If a valid application is submitted, a Bond will be issued by the bond scheme operator to the applicant that

states the Base Bond Price.

“Base Bond Price” - the greater of either the Assessed Property Value, or the price paid by the applicant for the Qualifying Interest, if this was in the 12 months prior to the Base Date.

Department for Transport HS2 Property Bond Option 21

“Assessed Property Value” – The average of two valuations of the Qualifying Interest that are undertaken by qualified valuers (instructed by the bond scheme operator) who will have regard to the physical condition of the Qualifying Interest at the date of application and assume the Base Date as the valuation date. In the event that these two valuations differ by more than 15%, a third valuation will be undertaken and an average taken of the higher two values

7.5 Immediately prior to issue of the Bond, a Schedule of Condition of the Qualifying Interest will be undertaken at the expense of the bond scheme operator, and will be signed by both the bond scheme operator and the Bond Holder. This Schedule of Condition will be appended to the Bond.

“Schedule of Condition” - a brief internal and external record of the condition of the Qualifying Interest, that includes photographic evidence. A copy of this is to be provided to both the Bond Holder and the bond scheme operator.

“Bond Holder” – the person with the benefit of the Bond

7.6 Upon receipt of the Bond, the applicant will become the Bond Holder. The Bond will be registered on the Local Land Charges register.

7.7 The Bond will state the Base Bond Price, but the Bond Holder will be able to check the Current Bond Value at any time by reference to an indexation calculator provided on the website run by the bond scheme operator.

“Current Bond Value” – the notional value of the Bond at any time. This will be the Base Bond Price, with a relevant regional house price index applied on a monthly basis up to the current date. This value will be subject to change if there is a Revaluation Request outstanding or the condition of the Qualifying Interest has substantially declined since the Schedule of Condition was undertaken.

“Independent Dispute Panel” – Panel established by the bond scheme operator to consider any disputes arising from the bond scheme.

The bond scheme operator would be required to appoint a panel of qualified valuation surveyors, who would be responsible for undertaking the property valuations (to set the Assessed Property Value), and a panel of building surveyors to undertake the Schedules of Condition. As considered above, based on the data available we understand about 1,600 residential properties may qualify for the bond scheme and this therefore sets the maximum number of valuations and Schedules of Condition that will need to be undertaken.

For the purpose of indexation, we suggest adopting the House Price Index (HPI) operated by the Lands Registry, which publishes a monthly index of house prices at national, regional, London Borough and County level.

We consider that the bond scheme operator should issue Bonds requested under the bond scheme within two months of request. This is consistent with the timetable within which an authority is required to respond to claims for statutory blight (service of blight notices).

Department for Transport HS2 Property Bond Option 22

Step 3: Keeping the Bond up to date

Revaluation 7.8 If any improvements or alterations are undertaken to the Qualifying Interest, the Bond Holder may make a

Revaluation Request to the bond scheme operator. This request will be submitted in a form that is available on a website run by the bond scheme operator. This form will enable the Bond Holder to detail the nature of works that have been undertaken and determine whether a Revaluation is necessary. Cyclical repair, cosmetic and maintenance would not require a revaluation to be undertaken, but improvement works may require it.

“Revaluation Request” – A request made by the Bond Holder to the bond scheme operator to review, at its reasonable discretion, the Assessed Property Value due to improvement or alteration works undertaken at the Qualifying Interest. Upon confirmation of the works undertaken, the Assessed Property Value will be re-assessed.

Any unnecessary re-inspections should be avoided. To achieve this, the Revaluation Request form should ask detailed questions to confirm the exact nature of the works that have been undertaken, i.e. was a planning application required? What additional space was added to the property? And, what costs were incurred? Supplementary evidence may be requested from the Bond Holder to supplement the Revaluation Request form.

In response to the Revaluation Request, the bond scheme operator will either confirm they will appoint a surveyor from the panel of qualified valuation surveyors to re-assess the Assessed Property Value or confirm they do not consider any re-assessment to be necessary and therefore that the Assessed Property Value should remain unchanged. In the event the Bond Holder wishes to challenge this decision, they may appeal to the Independent Dispute Panel established by the bond scheme operator, whose decision shall be final.

To avoid any Bonds being sought prematurely, and to try and reduce administration during the early stages of the bond scheme we suggest a restriction on Revaluation Requests being made within one year of the opening of the bond scheme.

Sale of property (excluding where acquisition is by the bond scheme operator) 7.9 The Bond runs with the Qualifying Interest and it will transfer (if appropriate) to the Estate of the Bond

Holder, any beneficiaries, mortgage lenders and any subsequent owner(s) of the Bond, who will have the full benefit of the terms of the Bond.

Monitoring the current value of the Bond 7.10 The Current Bond Value (see definition and notes under Step 2, above) will be the Base Bond Price as

adjusted by the House Price Index (as produced monthly by the Land Registry) in respect of the county or district in which the Qualifying Interest is located, applied on a monthly basis.

7.11 At any time after the Bond has been issued, the Bond Holder will be able to check the Current Bond Value by reference to an indexation calculator provided on the website run by the bond scheme operator.

Department for Transport HS2 Property Bond Option 23

7.12 At the date the Bond is triggered, the Current Bond Value becomes the Bond Purchase Price.

“Bond Purchase Price” – The price paid by the bond scheme operator for the Qualifying Interest if the Bond is validly triggered by the Bond Holder. This will be the Base Bond Price, with the relevant Land Registry House Price Index applied on a monthly basis up to the date that the Bond is triggered by the Bond Holder. The bond scheme operator will reserve the right to adjust the Bond Purchase Price if the condition of the Qualifying Interest at the date of trigger is significantly different to that recorded in the Schedule of Condition

The Bond Purchase Price is not a confirmed final figure and will be subject to change if, a Revaluation Request is outstanding or the Qualifying Interest is significantly different to that recorded in the Schedule of Condition undertaken prior to issue of the Bond.

Step 4: Triggering the Bond - General 7.13 The earliest date for triggering the bond is the date of a positive vote from the House of Commons at the

Second Reading of the Bill (due Spring 2014).

7.14 There are two mechanisms for triggering the Bond. For Qualifying Interests that are located in (or substantially within) the Outer Bond Area go to Step 5. For Qualifying Interests that are located in the Inner Bond Area go to Step 6.

Under this timetable, it would be possible for a Qualifying Interest who does not need to demonstrate an Effort to Sell (see Step 5, below) to request a Bond and trigger the Bond at the date on which the bond scheme commences operation. To avoid the practical issues and administration associated with this, and to clearly set out the timetable in which the bond scheme operator can respond to the various steps of the process, it will be appropriate to introduce separate notice periods for the stages of the bond scheme process. These notice periods are set out at the end of this note.

Step 5: Triggering the Bond – Qualifying Interests in the Outer Bond Area 7.15 Prior to triggering the Bond, the Bond Holder must demonstrate they have made an Effort to Sell.

7.16 The Bond Holder must complete a form, which can be downloaded from the website run by the bond scheme operator, confirming their intention to put the Qualifying Interest on the market. This form will identity the proposed Bond Purchase Price, provide details of the estate agent that the Bond Holder intends to instruct, and set out the proposed fees.

7.17 Upon receipt of this form, the bond scheme operator will inspect the Qualifying Interest (to compare with the Schedule of Condition previously undertaken); confirm the Bond Purchase Price; and confirm the basis on which they will pay the fees of the estate agent appointed by the Bond Holder in the event that a purchaser is not found (and the Bond is triggered). If there is a dispute in respect of the Bond Purchase Price, reference can be made to the Independent Dispute Panel.

“Effort to Sell” – The efforts that must be made by the owner of the Qualifying Interest to sell it in the open market prior to triggering the Bond. The Bond Holder must be able to demonstrate they have been unable to sell the Qualifying Interest for a price at or above the Bond Purchase Price (as calculated on the date that the Qualifying Interest was first put on to the market) within six months of it being actively marketed by

Department for Transport HS2 Property Bond Option 24

a local estate agent.

If the Effort to Sell does not result in an offer to purchase the Qualifying Interest at a price at or above the Bond Purchase Price, the Bond Holder can trigger the Bond and demand that the bond scheme operator acquire the Qualifying Interest at the Bond Purchase Price set at the commencement of the marketing period. The Bond can be triggered by the Bond Holder by submitting an application form available from the website run by the bond scheme operator.

In the event the bond scheme operator acquires the Qualifying Interest it will also pay the agreed fixed fee to the instructed estate agent. No further payments will be made to the Bond Holder.