deutsche bank german & austrian corporate conference · deutsche bank german & austrian...

TRANSCRIPT

Deutsche BankGerman & Austrian Corporate Conference

May 20, 2010

Lothar Lanz, CFO & COO

2

Disclaimer

This document, which has been issued by Axel Springer Aktiengesellschaft (the "Company"), comprises the written materials/slides for a presentation of the management.

Whilst all reasonable care has been taken to ensure that the information and facts stated herein are accurate and that the opinions and expectations contained herein are fair and reasonable no representation or warranty, express or implied, is given by or on behalf of the Company, any of its directors, or any other person as to the accuracy or completeness of the information or opinions contained in this document and no liability is accepted for any such information or opinions.

This document contains forward looking statements which involves risks and uncertainties. These forward looking statements speak only as of the date of this document and are based on numerous assumptions which may or may not prove to be correct. The actual performance and results of the business of the Company could differ materially from the performance and results discussed in this document.

The Company undertakes no obligation to publicly update or revise any forward looking statements or other information contained herein whether as a result of new information, future events or otherwise.

This document does not constitute or form any part of any offer or invitation to sell or issue, or any solicitation of any offerto purchase or subscribe for, any shares in the Company, nor shall it or any part of it nor the fact of its distribution form the basis of, or be relied on in connection with, any contract or investment decision in relation thereto.

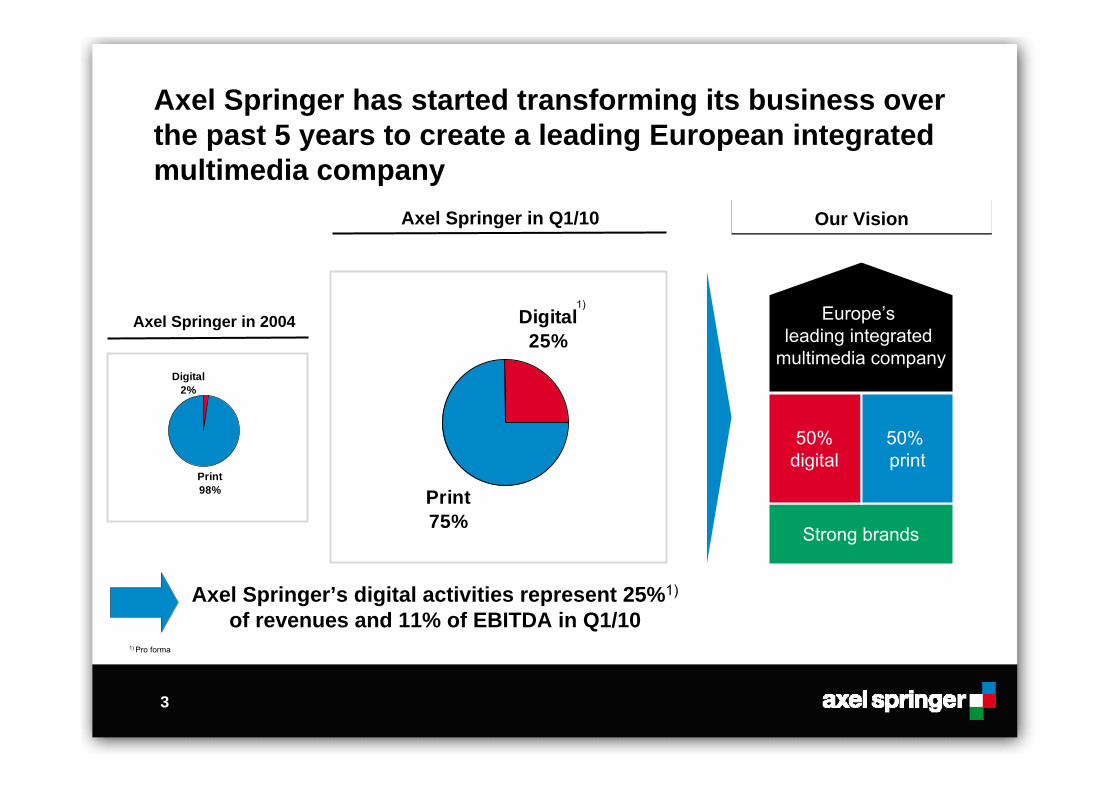

Print75%

Digital25%

3

Axel Springer has started transforming its business over the past 5 years to create a leading European integrated multimedia company

1) Pro forma

Strong brands

50%digital

50% print

Europe’s leading integrated

multimedia company

Our VisionOur Vision

Axel Springer in 2004

Axel Springer in Q1/10

Axel Springer’s digital activities represent 25%1)

of revenues and 11% of EBITDA in Q1/10

1)

Print98%

Digital2%

Our strategy focuses on our core competencies

4

International expansion

Replicating the “German model” internationally

JV with Ringier in CEE

2 Digital transformation

Existing brands extended online

Business model enhanced in digital world

3

Core Competencies

Leadership in Germany

Strengthen and expand leading market position

Strong brands drive high media reach and advertising revenues

1

55

Germany represents a unique newspaper market1

National newspaper circulation revenues(07-09 CAGR)Key themes in German market

Strong circulation revenues in Germany

– Higher proportion of total revenues than in other countries

– More resilient than in the UK and the US

– Potential for regular cover price increases

Higher share of younger readers

No free sheets

Strong position of BILD with 81%1) market share

Newspapers with higher share of advertising spend than TV as opposed to US2)

BILD reach vs TV shows5)

The Sun

11.8

BILD

9.4

Le Figaro

8.911.6

7.8

28.7

USA Today

3.72.4

The X Factor

American Idol -Tuesday

Wetten, dass…?

Dr. House

(reach in m)

5) UK: Year average for The X Factor 2009, BARB (BroadcastersAudience Research Board); average reach of Sun between Oct.08 to Sept. 09 NRS (National Readership Survey), USA: USA TODAY Reader Brand Research 2009; MRI Fall 2009, Nielsen Television - TV Ratings for Primetime: Season-to-Date (2009-2010 Season Through Jan. 24, 2010), France: Daily newspapers: EPIQ-Studie2008/2009, TV: Viewers 4J.+ Mediametrie 2009; Germany: Average for “Wetten, dass…?” 2009, Viewers age 14+, GFK/TV Panel 2009, ma 2010 Pressemedien

1) Including Berlin newsstand newspaper B.Z.; market share based on paid circulation of newsstand newspapers2) Source: ZenithOptimedia December 20093) Source: company information; National Newspaper circulation sales as % of total National Newspaper sales4) Source: PwC Global Entertainment and Media Outlook, 2009-2013, 2009E forecast

4) 4)4)

0.3%

-3.6% -3.1%

2.9%

Axel Springer Germany UK US3)

6

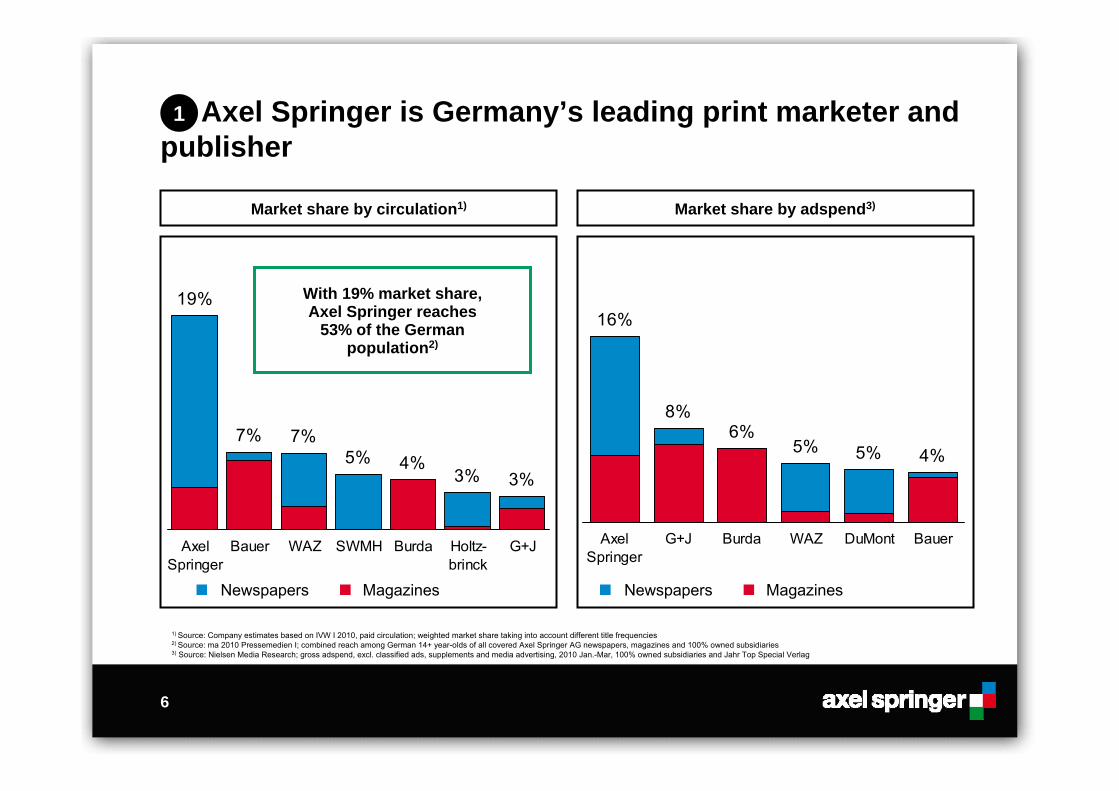

Axel Springer is Germany’s leading print marketer and publisher

Market share by adspend3)

Newspapers Magazines

16%

8%6%

5% 5% 4%

AxelSpringer

G+J Burda WAZ DuMont Bauer

Market share by circulation1)

Newspapers Magazines

19%

7% 7%5% 4%

3% 3%

AxelSpringer

Bauer WAZ SWMH Burda Holtz-brinck

G+J

With 19% market share, Axel Springer reaches

53% of the German population2)

1

1) Source: Company estimates based on IVW I 2010, paid circulation; weighted market share taking into account different title frequencies2) Source: ma 2010 Pressemedien I; combined reach among German 14+ year-olds of all covered Axel Springer AG newspapers, magazines and 100% owned subsidiaries3) Source: Nielsen Media Research; gross adspend, excl. classified ads, supplements and media advertising, 2010 Jan.-Mar, 100% owned subsidiaries and Jahr Top Special Verlag

77

(Index of media reach) (Index of net advertising spending)

Print Market

BILD’s growing reach resulted in advertising sales outperforming the market (2002-2009)

BILD’s reach increased

Source: Print ma Pressemedien 2003-1 / 2010-1 (data for 2002/2009) for market reach of BILD family print titles including new titles founded after 2002

-family print 1)

1) Net figures, excluding BILDWOCHE2) ZenithOptimedia: Net Advertising Revenues newspapers & magazines 2002-2009

BILD’s advertising sales

-14.7% -4.1%

1

-0.3% +2.5%

Market 2)-family print 1)

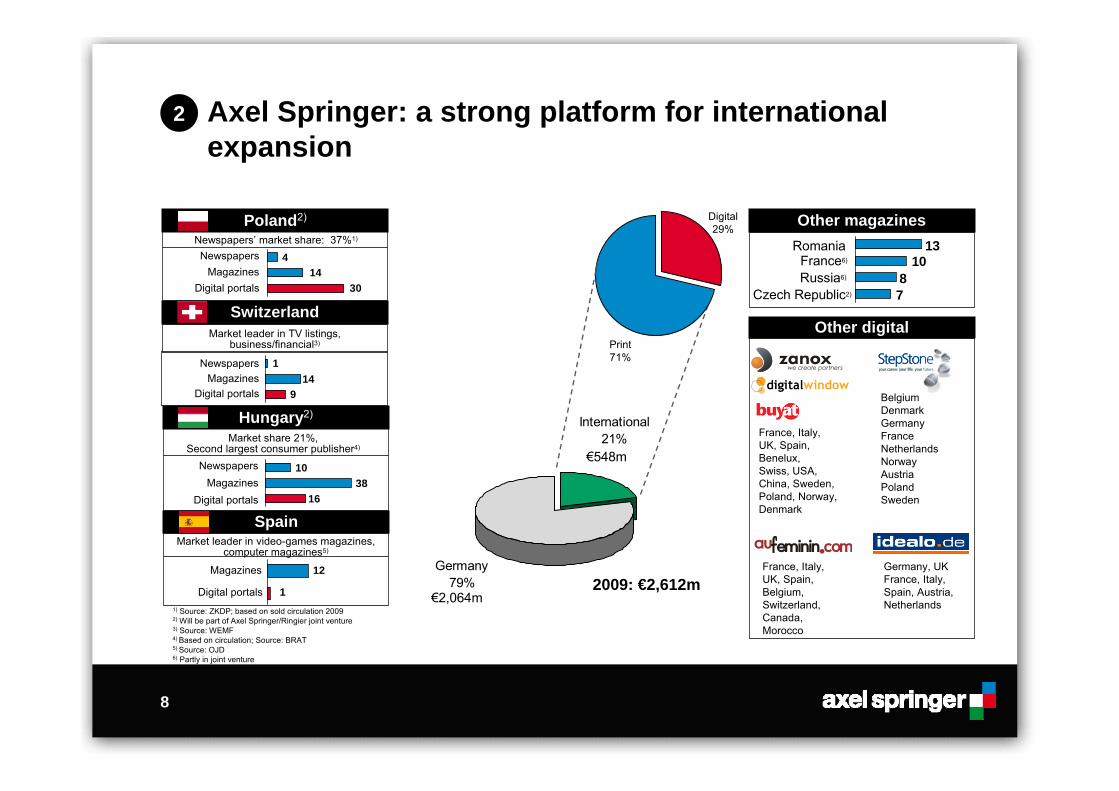

Axel Springer: a strong platform for international expansion

8

Germany79%

International21%

€2,064m

€548m

2009: €2,612m

Spain

12Magazines

1Digital portals

Market leader in video-games magazines, computer magazines5)

Newspapers

Poland2)

14Magazines4

30Digital portals

Newspapers’ market share: 37%1)

Market share 21%, Second largest consumer publisher4)

Hungary2)

38Newspapers 10

Magazines16Digital portals

Other magazines13

France6) 10Russia6) 8

Romania

Czech Republic2) 7

Print 71%

SwitzerlandMarket leader in TV listings,

business/financial3)

Newspapers14Magazines

1

9Digital portals

Digital 29%

2

Other digital

France, Italy, UK, Spain, Benelux, Swiss, USA, China, Sweden, Poland, Norway, Denmark

BelgiumDenmark GermanyFrance NetherlandsNorwayAustriaPolandSweden

France, Italy, UK, Spain, Belgium, Switzerland, Canada, Morocco

Germany, UK France, Italy, Spain, Austria, Netherlands1) Source: ZKDP; based on sold circulation 2009

2) Will be part of Axel Springer/Ringier joint venture3) Source: WEMF4) Based on circulation; Source: BRAT5) Source: OJD6) Partly in joint venture

Goal: Growth and digitization

Successful Eastern European

business since the 1990s

> 100 print titles, > 70 online

offerings

PF 2009 JV financials: revenues

€414m, EBITDA €62m

50% economic ownership with

100% consolidation for Axel

Springer

9

CEE JV with Ringier: 5 market-leading mass market brands, strong digitization potential

Ringier PresenceAxel Springer Presence

Poland

Czech Republic

Slovakia

Hungary

Serbia

2

No. 1 tabloid: Blesk(Ringier)No. 1 tabloid: Blesk(Ringier)

No. 1 tabloid: NovýČas (Ringier)No. 1 tabloid: NovýČas (Ringier)

No. 1 tabloid: Blic(Ringier)No. 1 tabloid: Blic(Ringier)

No 1 tabloid: FAKT (Axel Springer)

No 1 tabloid: FAKT (Axel Springer)

No. 1 tabloid: Blikk (Ringier)No. 1 tabloid: Blikk (Ringier)

10

We have become the largest digital player by revenue among European print publishers

20293640

117127

332

423

569

JohnstonPress

L'EspressoTelegraafTrinityMirror

DMGTLagardereSanomaSchibstedAxelSpringer

FY09

reve

nues

(€m

)Digital media revenues (in €m)

3

29% 13%

2% 5% 5% 3%

7%

4%

% o

f tot

al

reve

nues

25%2)

1) Based on pro forma revenues for Digital Media in 20092) Based on pro forma revenues for Digital Media in Q1/10m

12%29%21% 6%FY09

Q1/10 n/a n/a n/a n/a n/a

1)

Performance marketing

Classifieds / Marketplaces

Content portals

Digital strategy along core competencies

11

Core Competencies

Audience Advertisers

A

B

C

Cross-synergies between core competencies increase revenues and profitability

12

BILD – example of our successful transition to digital channels

67.2

33.4 27.5

Kick

er O

nlin

e

Spor

t1.d

e

A

50m

100m

Jan-08 Jul-08 Jan-09 Jul-09 Jan-10

5.5

2.9

0.3

Auto

Mot

orun

d S

port

Auto

New

s

52.7

22.412.3

Chi

p.de

Pcw

elt.d

e

News

Sport Automotive Computer

3)

2) 2) 2)

1)

Site

vis

its (i

n m

)S

ite v

isits

(in

m)

Site

vis

its (i

n m

)

Site

vis

its (i

n m

)

1) Source: IVW, March 20102) Source: IVW, Jan – Mar 2010 (Average Q1/10)3) Axel Springer’s sport sites include: sportbild.de, Bild.de/Sport and Transfermarkt; Source: IVW (sportbild.de and Transfermarkt), Google Analytics (Bild.de/Sport)

13

auFeminin – strengthening market leadership

6.8auFeminin5.4LeJournal de

Femmes

France: #1

3.0enFemenino1.1Terra Mujer

Spain: #13.5alFemminile

1.6Donna Moderna

Italy: #1

2.6goFeminin2.1Fem

Germany: #1iVillagesoFeminine

0.60.5

UK: #2

0.5auFeminin0.3Libelle

Belgium: #1

Unique Users in Mio.Source: Nielsen/comScore/AGOF/IVW, March 2010

International platform outside of France experiencing accelerated growth with tripled revenues since Axel Springer’s investment in auFeminin in 2007

17.518.219.2

11.36.53.3

2007 2008 2009

France International

Strong international presence International revenue contribution (in €m)

22.5

28.824.7+9.8%

+16.5%

A

14

Paradigm shift in 2009: Monetization of digital content works

A

20092008 2010

Free BILD mobile portal Premium initiative with innovative pay-for-service programs and exclusive content

Quality content for the most demanding readers

No. 1 mobile portal1) – not only among BILDmobil customersInnovative paid content, services and functions with simple billing arrangementsApprox. 180,000 paid BILD and WELT iPhone apps to datePaid for mobile and online regional content introduced in 2009

No. of paid content packages: 8

No. of paid content packages: >20

1) Source: INFonline

15

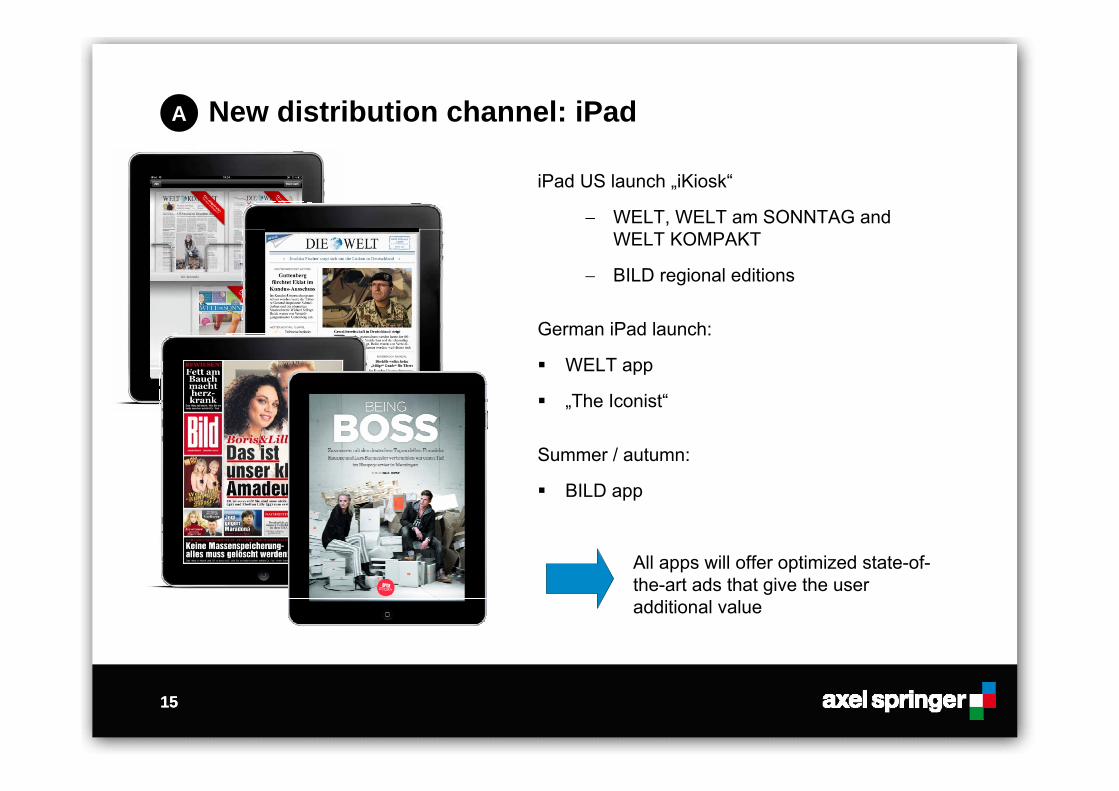

New distribution channel: iPadA

2010iPad US launch „iKiosk“

− WELT, WELT am SONNTAG and WELT KOMPAKT

− BILD regional editions

German iPad launch:

WELT app

„The Iconist“

Summer / autumn:

BILD app

All apps will offer optimized state-of-the-art ads that give the user additional value

15

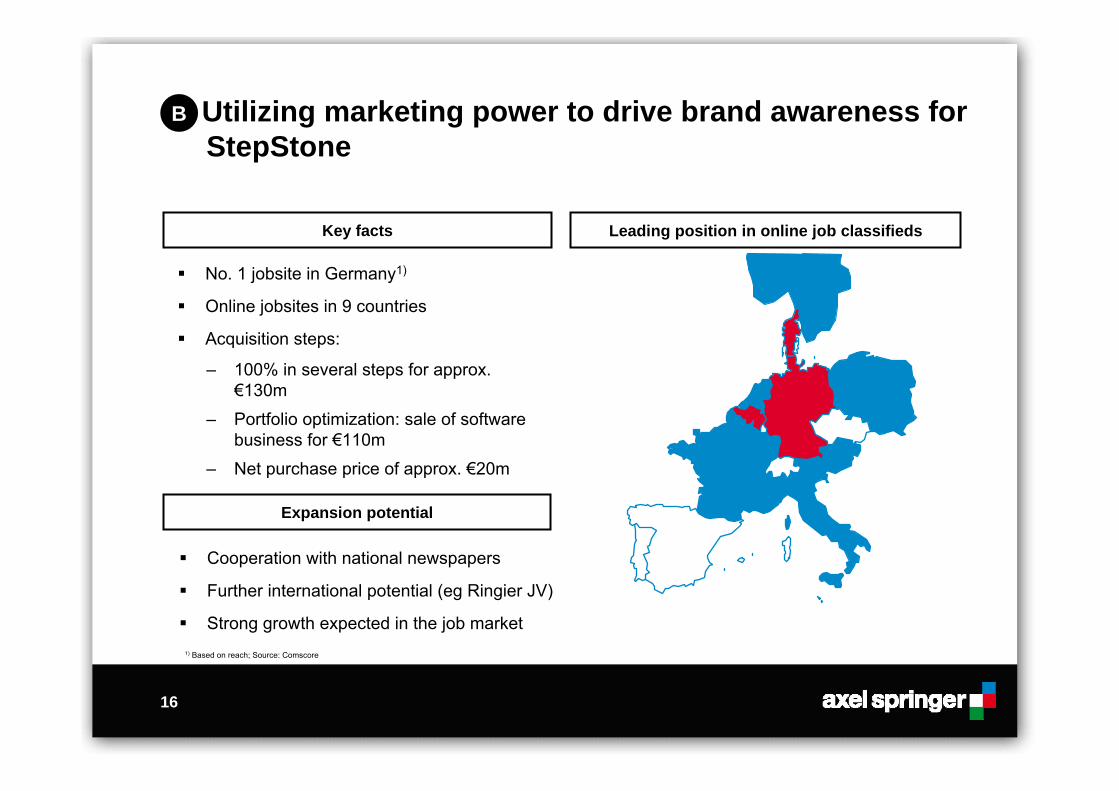

No. 1 jobsite in Germany1)

Online jobsites in 9 countries

Acquisition steps:

– 100% in several steps for approx. €130m

– Portfolio optimization: sale of software business for €110m

– Net purchase price of approx. €20m

16

Utilizing marketing power to drive brand awareness for StepStone

Key facts Leading position in online job classifieds

B

Expansion potential

Cooperation with national newspapers

Further international potential (eg Ringier JV)

Strong growth expected in the job market1) Based on reach; Source: Comscore

17

17

Online Performance Marketing –Axel Springer shapes European market leader

Revenues (in €m)

2008 2009e 2008 2009

+9% -21%

323284297

360

Acquired

08/2009

02/2010

C

600150

200

250

18

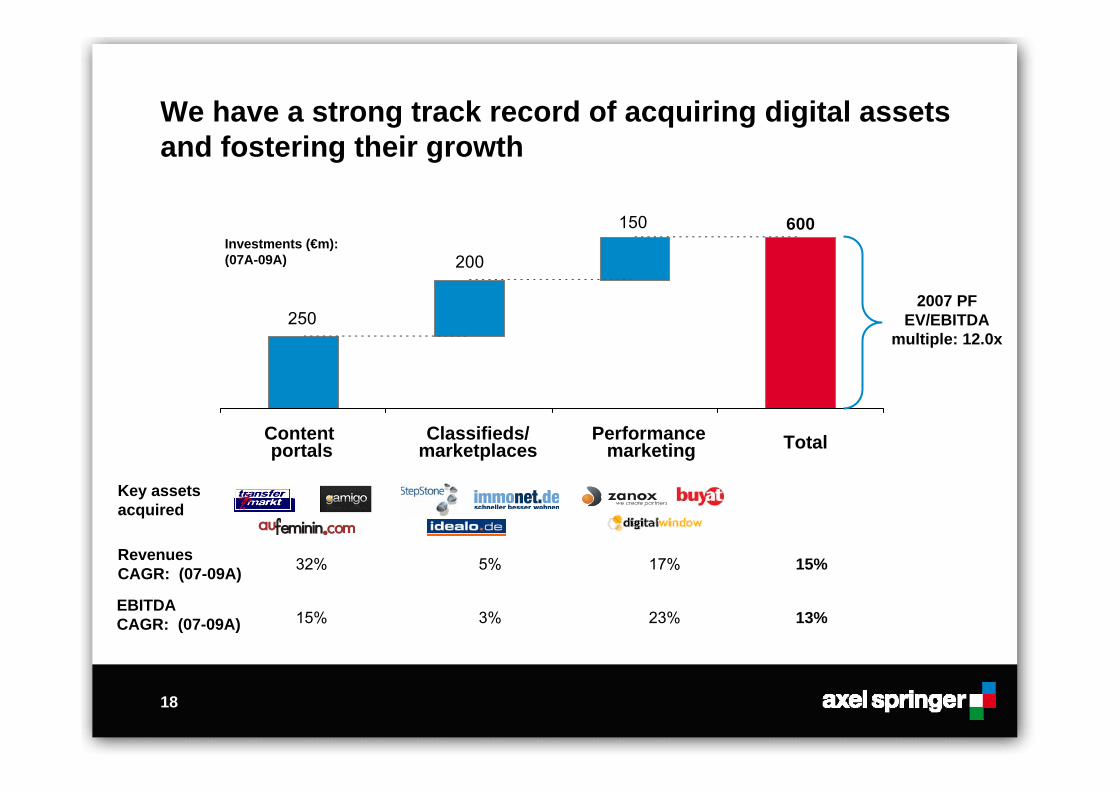

We have a strong track record of acquiring digital assets and fostering their growth

RevenuesCAGR: (07-09A)

EBITDACAGR: (07-09A)

Investments (€m):(07A-09A)

32% 5% 17% 15%

15% 3% 23% 13%

Key assetsacquired

Content portals

Classifieds/marketplaces

Performance marketing Total

2007 PF EV/EBITDA

multiple: 12.0x

Financial performance

80

119

13.0%18.0%

0

100

Q1/09 Q1/10

EBIT

DA

(€m

)

0%5%

10%15%

20%25% E

BITD

A m

argin

334

486470434414

17.8%18.2%18.3%17.3%

12.8%

0

200

400

2005 2006 2007 2008 2009

EBIT

DA

(€m

)

0%5%10%

15%20%25%

EBITDA m

argin

EBITDA EBITDA margin

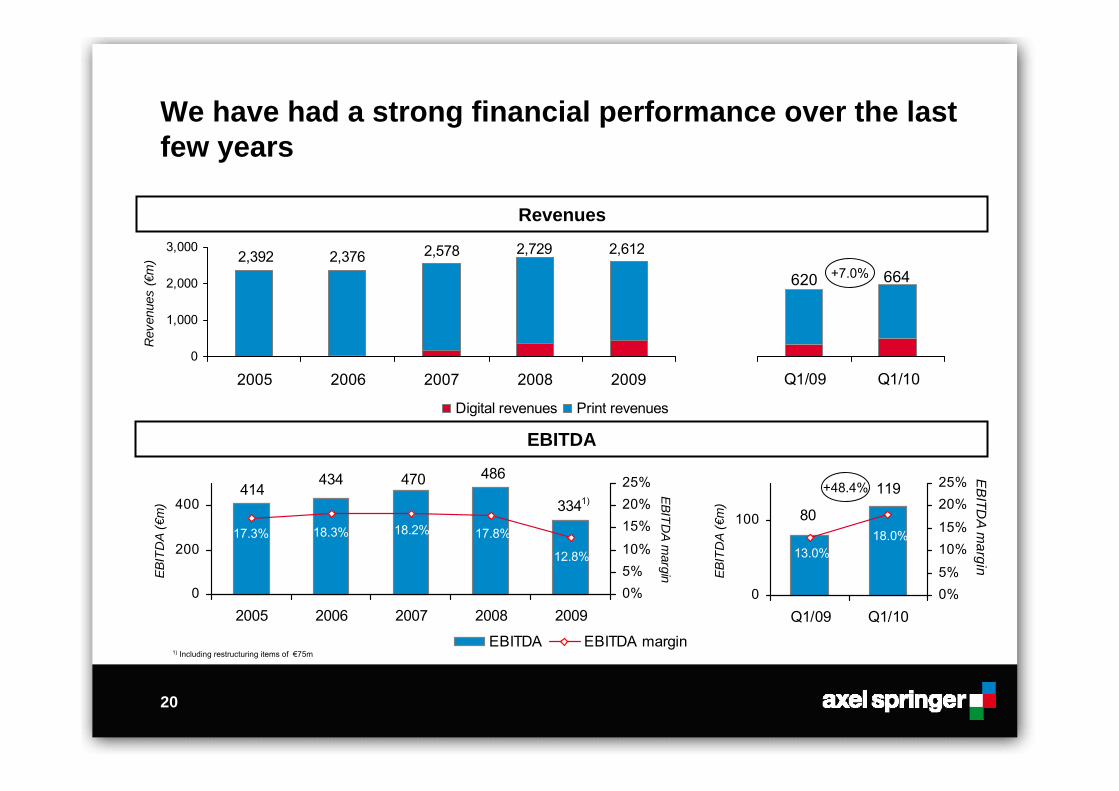

We have had a strong financial performance over the last few years

20

Revenues

2,6122,7292,5782,3762,392

0

1,000

2,000

3,000

2005 2006 2007 2008 2009

Rev

enue

s (€

m)

Digital revenues Print revenues

664620

Q1/09 Q1/10

+7.0%

+48.4%

EBITDA

1)

1) Including restructuring items of €75m

Axel Springer starts 2010 with record quarter

Revenue increase of 7% to €664m1.

25% of revenues digital 1)2.

Improved advertising environment and market share expanded3.

5. Raised guidance 2010: EBITDA to increase significantly >10%

EBITDA at all-time high of €119m in a first quarter, margin at 18% 4.

1) Pro forma

21

6. Dividend of €4.40 on record level of 2008

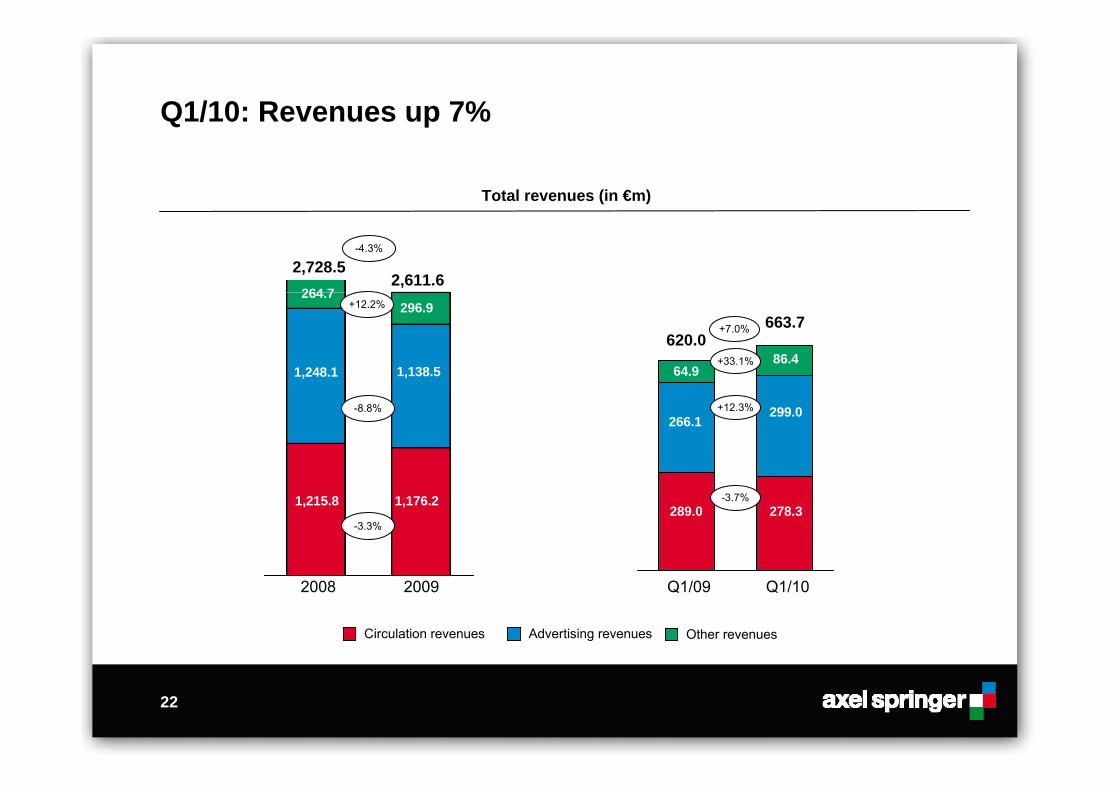

Q1/10: Revenues up 7%

1,215.8

264.72,611.6

1,248.1

296.9

1,138.5

1,176.2

2,728.5

20092008

Advertising revenues Other revenuesCirculation revenues

Total revenues (in €m)

+12.2%

-8.8%

-3.3%

-4.3%

-3.7%

+12.3%

+33.1%

22

+7.0%

Q1/10Q1/09

289.0

64.9

663.7

266.1

86.4

299.0

278.3

620.0

Print margins close to record high, Digital Media continues to grow and expand margins

2323

(in €m)

Revenues

EBITDA

EBITDAmargin

Circulation

Advertising

Other

Newspapers National

Q1/09292.4

64.8

22.2%

153.9

131.5

7.0

289.4

77.6

26.8%

149.6

132.7

7.1

yoy-1.0%

+19.7%

-2.8%

+0.9%

+1.6%

Q1/10

Magazines National

126.9

13.1

10.3%

89.1

33.2

4.7

119.2

25.2

21.1%

82.9

30.4

5.9

Q1/09 yoyQ1/10-6.1%

+92.8%

-6.9%

-8.4%

+27.5%

Print International

72.4

-2.4

-

46.0

24.3

2.2

71.6

5.4

7.5%

45.8

22.3

3.4

Q1/09 yoyQ1/10-1.2%

nm

-0.3%

-8.2%

+58.0%

Digital Media

104.7

6.8

6.5%

-

77.1

27.6

160.0

13.3

8.3%

-

113.5

46.5

Q1/09 yoyQ1/10+52.9%

+94.6%

-

+47.3%

+68.7%

24

Strong cash flow generation and high dividend yield

209

250 260

292

239

199177 175

220243 246

233 231

0

100

200

300

400

Q1/07 Q3/07 Q1/08 Q3/08 Q1/09 Q3/09 Q1/10

Free cash flow (ltm1), in €m) Dividend yield2)

5.9%

5.1%

4.6%

3.5%

2.7%

1.2%

0.0%

0.0%

0.0%

0.0%

0.0%

Axel Springer

Sanoma

Lagardere

DMGT

Telegraaf Media

Schibsted

Gruppo L'Espresso

Johnston Press

Mondadori

RCS Media Group

Trinity Mirror

1) Last twelve months2) Based on actual 2009 dividend per share divided by share price as of December 31, 2009; Source: CapitalIQ

Outlook and conclusion

(0.2)%

0.9%

3.4%2.6%

1.0%

(4.9)%

1.8%1.6%0.7%

2.7%

(1.4)%

(8.7)%

1.0%

5.7%

(5.8)%

1.1%

5.5%7.8%

(15)%

(10)%

(5)%

0%

5%

10%

15%

2003 2004 2005 2006 2007 2008 2009 2010E 2011E

Real GDP growth y-o-y German advertising growth y-o-y

Outlook: Progressive recovery of the German advertising market

26

Source: Global Insight, March 2010; ZenithOptimedia, December 2009

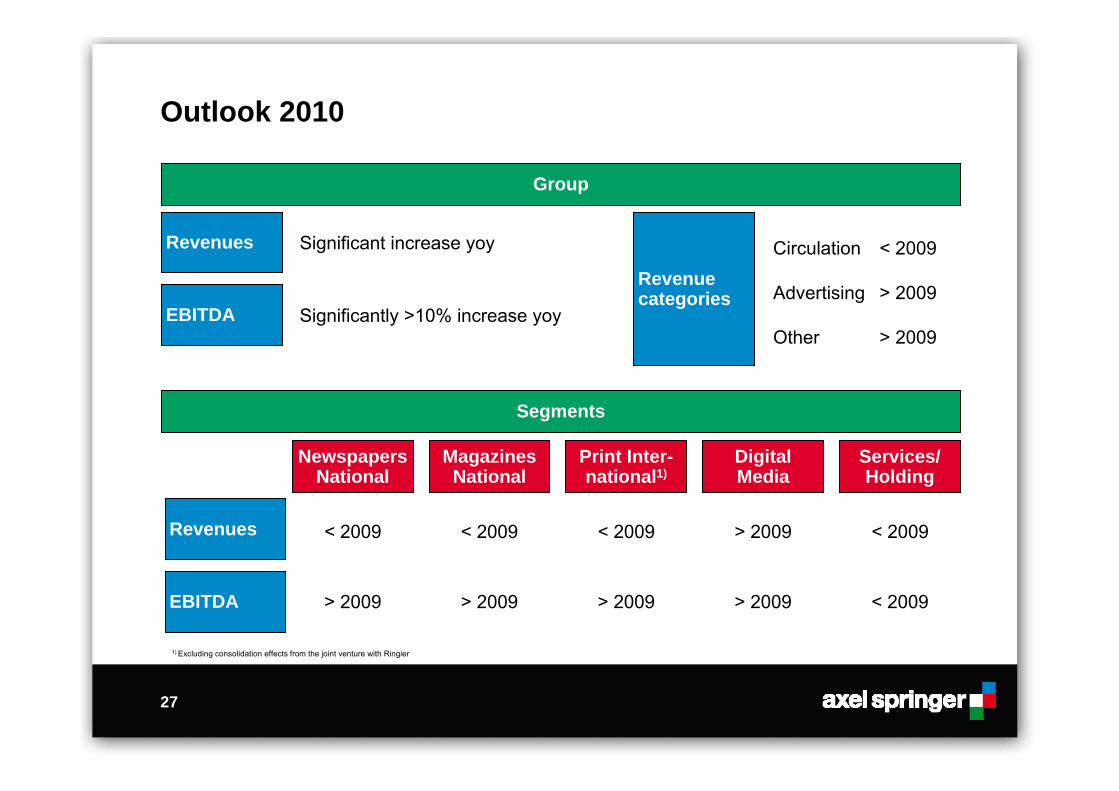

27

Outlook 2010

Group

Segments

Revenuecategories

Newspapers National

Magazines National

Print Inter-national1)

Digital Media

Services/ Holding

Revenues

EBITDA

Significant increase yoy

Significantly >10% increase yoy

Circulation

Advertising

Other

< 2009

> 2009

> 2009

< 2009

> 2009 > 2009 > 2009 > 2009 < 2009

< 2009< 2009 > 2009< 2009Revenues

EBITDA

1) Excluding consolidation effects from the joint venture with Ringier

Key investment highlights

28

No. 1 publisher in Germany reaching 53% of the population

Leading market positions and brands across Europe

Strong profitability, healthy balance sheet, and high dividend

Attractive portfolio of leading online properties that scale internationally

Geared for cyclical advertising recovery

CEE JV creates the leading platform for growth in the region

Proven strategy to transition and monetize our leading media brands online

29

Investor Relations contacts

Claudia Thomé

Head of Investor Relations

Phone: +49 (0)30 2591 77421

Mobile: +49 (0)160 90445035

Axel Springer AG

Axel-Springer-Str. 65

10888 Berlin / Germany

Fax: +49 (0)30 2591 77422

Daniel Fard-Yazdani

Deputy Head of Investor Relations

Phone: +49 (0)30 2591 77425

Mobile: +49 (0)151 52844459