director director polyolefinspolyolefins & pvc& pvc5).pdf · natural gas ethane propane...

TRANSCRIPT

Polyolefins: North America And Polyolefins: North America And The WorldThe World

Nick VafiadisNick VafiadisDirector Director PolyolefinsPolyolefins & PVC& [email protected]@cmaiglobal.com

FPAFPASeptember 24, 2009September 24, 2009Chicago IL U S AChicago IL U S A

Flexible Packaging AssociationFlexible Packaging AssociationSingaporeSingapore ShanghaiShanghai HoustonHouston New YorkNew York LondonLondon DüsseldorfDüsseldorf DubaiDubai

Chicago, IL, U.S.A.Chicago, IL, U.S.A.

EnergyEnergygygy

Flexible Packaging AssociationFlexible Packaging Association

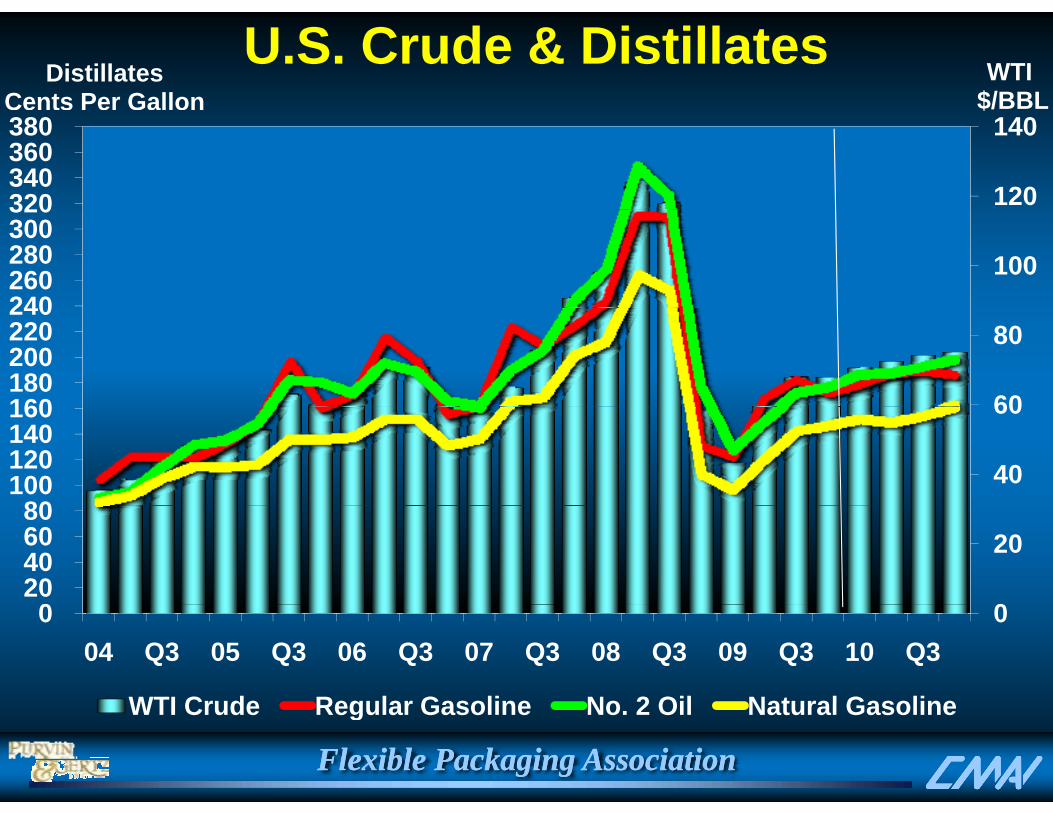

WTI$/BBL

DistillatesCents Per Gallon

U.S. Crude & Distillates

120

140

320340 360 380

$

100 240260 280 300 320

60

80

160180 200 220 240

40

60

80100 120 140 160

0

20

020 40 60 80

0 0 04 Q3 05 Q3 06 Q3 07 Q3 08 Q3 09 Q3 10 Q3

WTI Crude Regular Gasoline No 2 Oil Natural Gasoline

Flexible Packaging AssociationFlexible Packaging Association

WTI Crude Regular Gasoline No. 2 Oil Natural Gasoline

WTI$/BBL

DistillatesCents Per Gallon

U.S. Crude & Distillates

100

120

260 280 300

$

80

100

200 220 240

60 140 160 180

40

6080

100 120

0

20

020 40 60

0 0 03 04 05 06 07 08 09 10 11 12 13

WTI Crude Regular Gasoline No 2 Oil Natural Gasoline

Flexible Packaging AssociationFlexible Packaging Association

WTI Crude Regular Gasoline No. 2 Oil Natural Gasoline

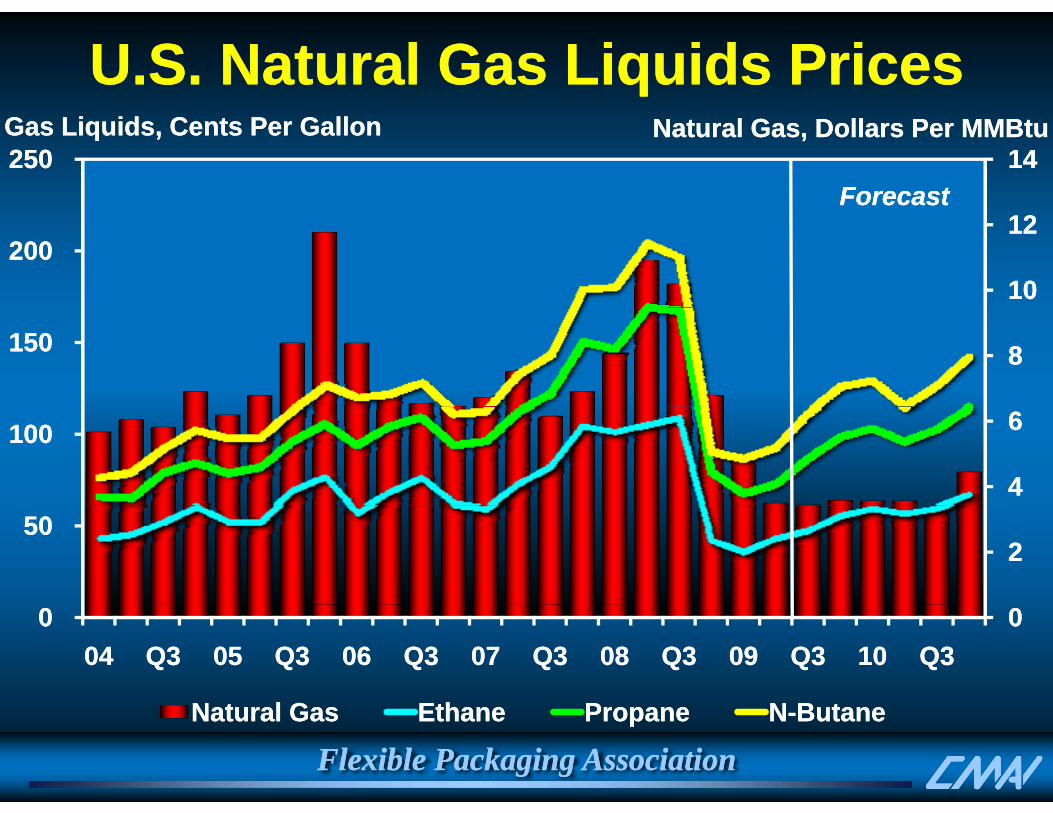

U.S. Natural Gas Liquids PricesU.S. Natural Gas Liquids Prices14 14 250 250

Gas Gas Liquids, Cents Liquids, Cents Per GallonPer Gallon Natural Natural Gas, Dollars Per Gas, Dollars Per MMBtuMMBtu

ForecastForecast

10 10

12 12 200 200

8 8 150 150

4 4

6 6 100 100

2 2 50 50

0 0 0 0 0404 Q3Q3 0505 Q3Q3 0606 Q3Q3 0707 Q3Q3 0808 Q3Q3 0909 Q3Q3 1010 Q3Q3

N t l GN t l G EthEth PP NN B tB t

Flexible Packaging AssociationFlexible Packaging AssociationNatural GasNatural Gas EthaneEthane PropanePropane NN--ButaneButane

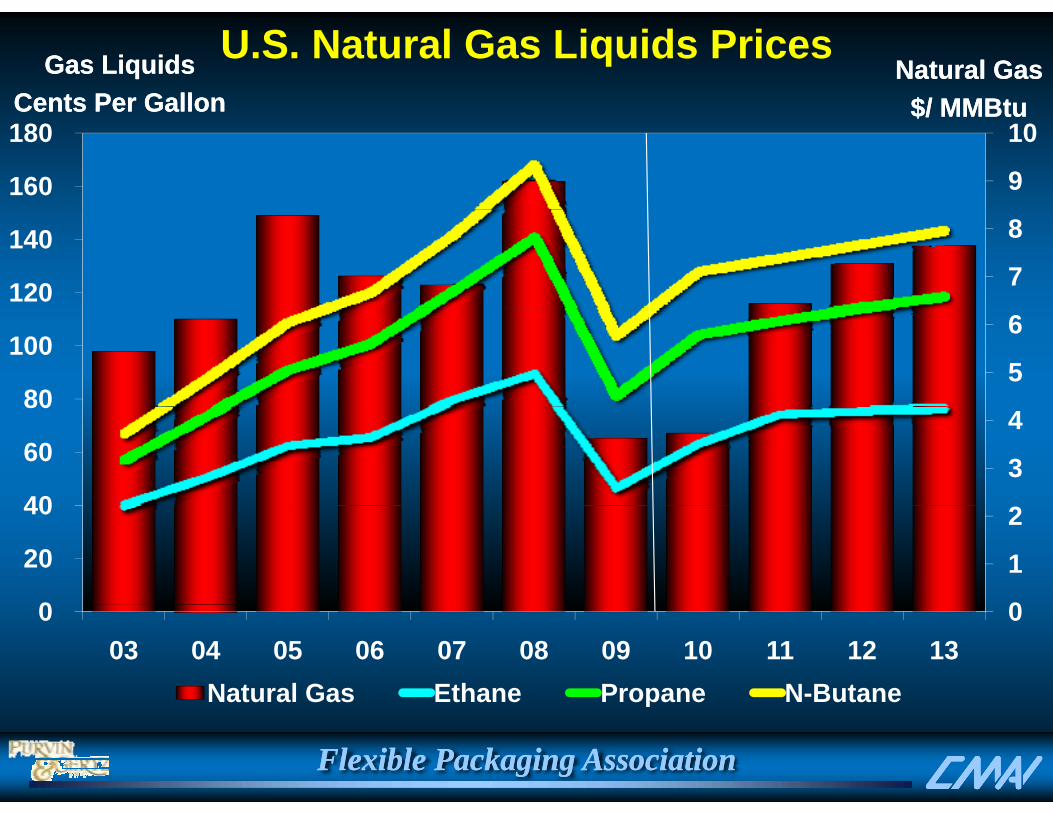

U.S. Natural Gas Liquids PricesGas LiquidsGas LiquidsCents Per GallonCents Per Gallon

Natural GasNatural Gas$/$/ MMBtuMMBtu

9

10

160

180 Cents Per GallonCents Per Gallon $/ $/ MMBtuMMBtu

7

8

120

140

5

6

80

100

3

4

40

60

80

0

1

2

0

20

40

0 0 03 04 05 06 07 08 09 10 11 12 13

Natural Gas Ethane Propane N-Butane

Flexible Packaging AssociationFlexible Packaging Association

p

Gas as % of Crude North America Energy Price Trends

Current $Current $

120%

16

18 BTU Basis$ / MM Btu

80%

100%

12

14

16

60%

80%

8

10

12

40%6

8

20%2

4

0%0 03 04 05 06 07 08 09 10 11 12 13

Crude (WTI) Natural Gas Gas as % of Crude

Flexible Packaging AssociationFlexible Packaging Association

Crude (WTI) Natural Gas Gas as % of Crude

EthyleneEthyleneEthyleneEthylene

Flexible Packaging AssociationFlexible Packaging Association

Basic Ethylene Flow ChartBasic Ethylene Flow Chart

NaphthasNaphthasCrudeCrude

••PropylenePropylene

••••ButadieneButadieneButadieneButadiene

FeedstocksFeedstocks

StSt

Gas OilsGas OilsRefineryRefinery

CrudeCrudeOilOil ••••ButylenesButylenesButylenesButylenes

••BTX BTX BTXBTX (pygas)(pygas)

SteamSteamCrackerCracker EthyleneEthyleneEthaneEthane

PropanePropaneGG ••HeavyHeavy

F i e l dF i e l dCondensatesCondensates

ButanesButanesNaturalNaturalGasGas

GasGasSeparationSeparation

UnitUnit

yyAromaticsAromatics

••MethaneMethane

••HydrogenHydrogeny gy g••Fuel OilFuel Oil

Flexible Packaging AssociationFlexible Packaging Association

United StatesUnited States2008 Ethylene Supply/Demand2008 Ethylene Supply/Demand

EthEth PEPE

y pp yy pp yProduction By FeedstockProduction By Feedstock Demand By EndDemand By End--UseUse

EthaneEthane51%51%

PEPE53%53%

OthersOthersPropanePropane

18%18%ButaneButane3%3%

NaphthaNaphthaGas OilGas Oil5%5%

OthersOthers6%6%

Ethylene Ethylene OxideOxideEDCEDCEBZEBZ

OthersOthers14%14%

3%3%17%17%5%5% 13%13%14%14%6%6%

Domestic Demand = Domestic Demand = 23.7 23.7 Million Metric TonsMillion Metric Tons

Flexible Packaging AssociationFlexible Packaging Association

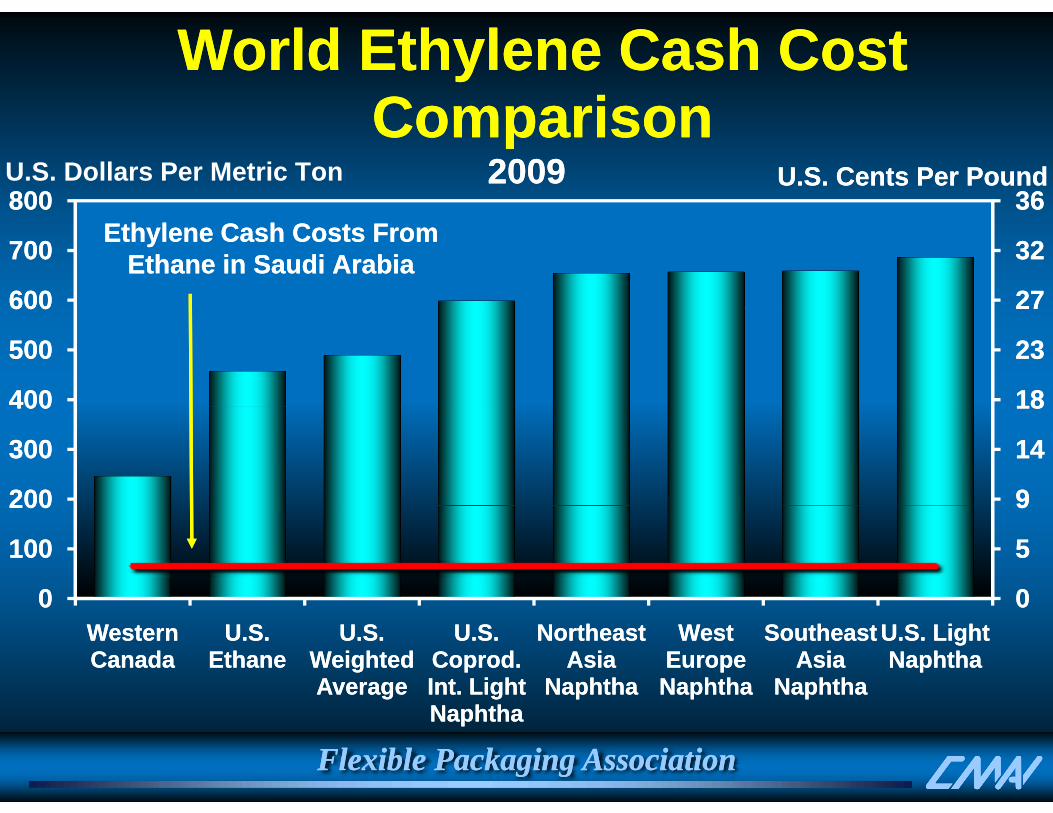

World Ethylene Cash Cost World Ethylene Cash Cost ComparisonComparison

3636800800

ComparisonComparisonU.S. Dollars Per Metric Ton U.S. Cents Per PoundU.S. Cents Per Pound20092009

2727

3232

3636

600600

700700

800800Ethylene Cash Costs From Ethylene Cash Costs From

Ethane in Saudi ArabiaEthane in Saudi Arabia

1818

2323

2727

400400

500500

600600

99

1414

1818

200200

300300

400400

00

55

99

00

100100

200200

0000Western Western CanadaCanada

U.S. U.S. EthaneEthane

U.S. U.S. Weighted Weighted AverageAverage

U.S. U.S. Coprod. Coprod. Int. Light Int. Light

Northeast Northeast Asia Asia

NaphthaNaphtha

West West Europe Europe

NaphthaNaphtha

Southeast Southeast Asia Asia

NaphthaNaphtha

U.S. Light U.S. Light NaphthaNaphtha

Flexible Packaging AssociationFlexible Packaging AssociationNaphthaNaphtha

U.S. Ethane AdvantageCents Per PoundCents Per Pound

1212

1414Cents Per PoundCents Per Pound

ForecastForecast

88

1010

44

66

00

22

44

44

--22

00

--4420032003 20042004 20052005 20062006 20072007 20082008 20092009 20102010 20112011 20122012 20132013

Propane CrackingPropane Cracking Butane CrackingButane Cracking Light Naphtha CrackingLight Naphtha Cracking

Flexible Packaging AssociationFlexible Packaging Association

Propane CrackingPropane Cracking Butane CrackingButane Cracking Light Naphtha CrackingLight Naphtha Cracking

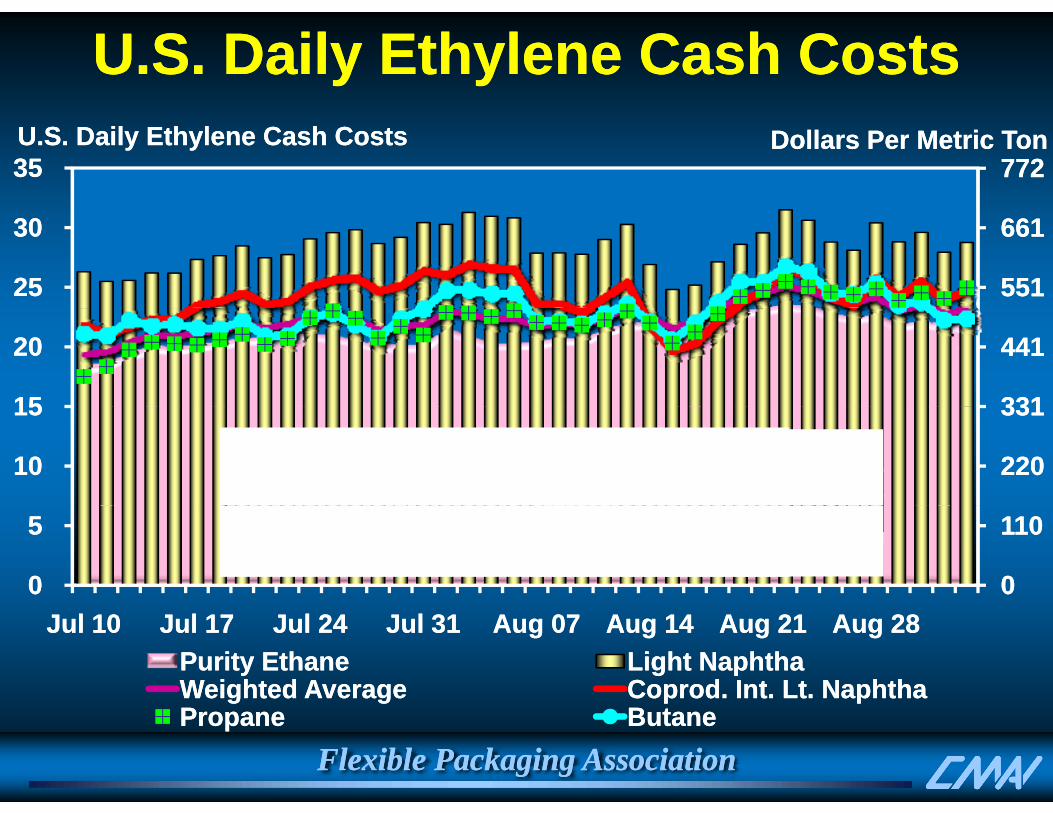

U.S. Daily Ethylene Cash CostsU.S. Daily Ethylene Cash Costs

77277235 35 U.S. Daily Ethylene Cash CostsU.S. Daily Ethylene Cash Costs Dollars Per Metric TonDollars Per Metric Ton

551551

661661

25 25

30 30

331331

441441

1515

20 20

220220

331331

10 10

15 15

00

110110

0 0

5 5

Jul 10Jul 10 Jul 17Jul 17 Jul 24Jul 24 Jul 31Jul 31 Aug 07Aug 07 Aug 14Aug 14 Aug 21Aug 21 Aug 28Aug 28Purity EthanePurity Ethane Light NaphthaLight NaphthaWeighted AverageWeighted Average Coprod. Int. Lt. NaphthaCoprod. Int. Lt. Naphtha

Flexible Packaging AssociationFlexible Packaging Association

g gg g p pp pPropanePropane ButaneButane

Global Ethylene Capacity GrowthGlobal Ethylene Capacity Growth

160160

180180Million Metric Tons

Global ethylene capacity is forecast to Global ethylene capacity is forecast to

120120

140140

160160 approach 180 million metric tons by approach 180 million metric tons by 2015, 2015, with Asia/Pacific (including India) as the with Asia/Pacific (including India) as the largest producing region. largest producing region.

8080

100100

120120

4040

6060

8080

00

2020

4040

009595 9696 9797 9898 9999 0000 0101 0202 0303 0404 0505 0606 0707 0808 0909 1010 1111 1212 1313 1414 1515

North AmericaNorth America West EuropeWest Europe Middle EastMiddle East Asia/PacificAsia/Pacific Rest of WorldRest of World

Flexible Packaging AssociationFlexible Packaging Association

North AmericaNorth America West EuropeWest Europe Middle EastMiddle East Asia/PacificAsia/Pacific Rest of WorldRest of World

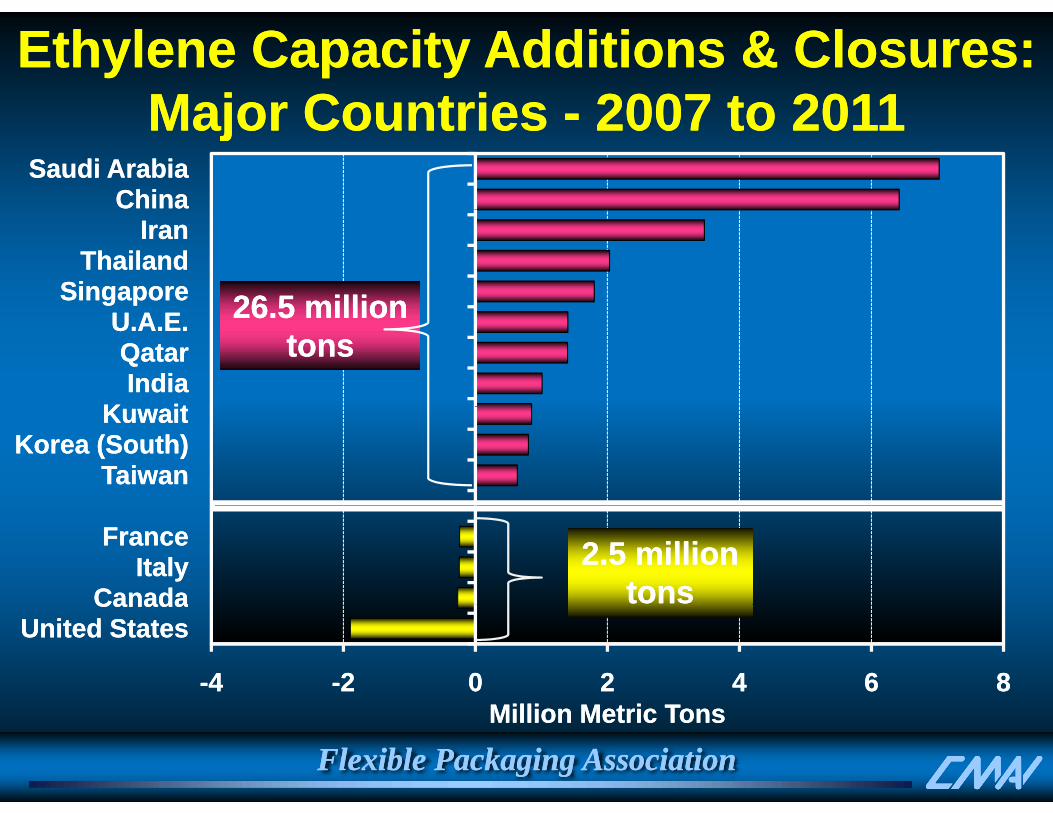

Ethylene Capacity Additions & Closures: Ethylene Capacity Additions & Closures: Major CountriesMajor Countries 2007 to 20112007 to 2011Major Countries Major Countries -- 2007 to 20112007 to 2011

ChinaChinaSaudi ArabiaSaudi Arabia

SingaporeSingaporeThailandThailand

IranIran

26 5 million26 5 million

K itK itIndiaIndiaQatarQatar

U.A.E.U.A.E. 26.5 million 26.5 million tonstons

TaiwanTaiwanKorea (South)Korea (South)

KuwaitKuwait

CanadaCanadaItalyItaly

FranceFrance 2.5 million 2.5 million tonstons

--44 --22 00 22 44 66 88

United StatesUnited StatesCanadaCanada

Flexible Packaging AssociationFlexible Packaging AssociationMillion Metric TonsMillion Metric Tons

Middle East Ethylene Capacity Middle East Ethylene Capacity Additi 2008Additi 2008 20092009Additions 2008Additions 2008--20092009

10,00010,000Ethylene Equivalent, Thousand Metric Tons

ShSh

8,0008,0009,0009,000

10,00010,000

YansabYansabRLOCRLOC

SharqSharq

5 0005 0006,0006,0007,0007,000

TKOCTKOC

PetroPetro--RabighRabigh

YansabYansab

3,0003,0004,0004,0005,0005,000

AryaArya JamJam JCPJCPSEPCSEPC

TKOCTKOC

001,0001,0002,0002,000 SasolSasol

00JanJan--0808 AprApr--0808 JulJul--0808 OctOct--0808 JanJan--0909 AprApr--0909 JulJul--0909 OctOct--0909

N Eth l C itN Eth l C it Eth l C i C itEth l C i C it

Flexible Packaging AssociationFlexible Packaging Association

New Ethylene CapacityNew Ethylene Capacity Ethylene Consuming CapacityEthylene Consuming Capacity

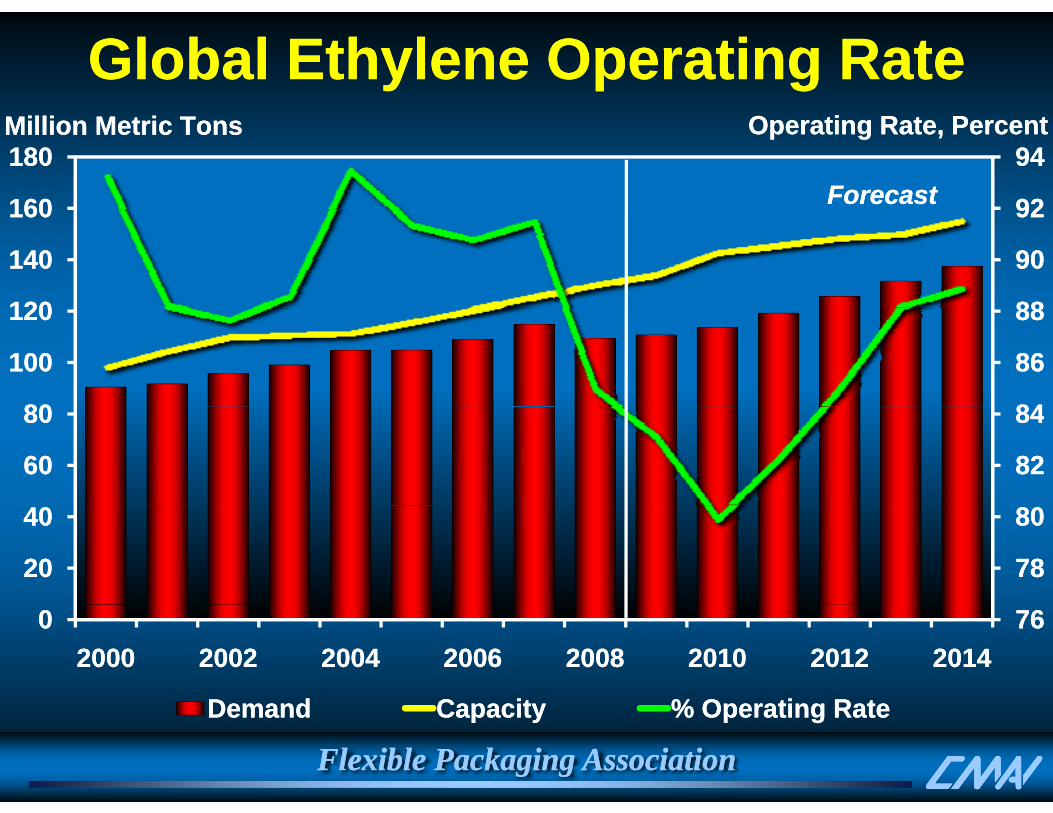

Global Ethylene Operating RateGlobal Ethylene Operating Rate

9292

9494

160160

180180Operating Rate, PercentOperating Rate, PercentMillion Metric TonsMillion Metric Tons

ForecastForecast

8888

9090

9292

120120

140140

160160

8484

8686

8888

8080

100100

120120

8282

8484

6060

8080

7878

8080

2020

4040

76760020002000 20022002 20042004 20062006 20082008 20102010 20122012 20142014

D dD d C itC it % O ti R t% O ti R t

Flexible Packaging AssociationFlexible Packaging AssociationDemandDemand CapacityCapacity % Operating Rate% Operating Rate

Billion PoundsBillion PoundsU.S. Ethylene Supply/Demand OutlookU.S. Ethylene Supply/Demand Outlook

Operating RateOperating Rate

100%100%1616

1717Billion PoundsBillion Pounds

ForecastForecast

Operating RateOperating Rate

90%90%

95%95%

100%100%

1414

1515

1616

85%85%

90%90%

1313

1414

75%75%

80%80%

1111

1212

65%65%

70%70%

99

1010

65%65%990101 Q4Q4 Q3Q3 Q2Q2 0404 Q4Q4 Q3Q3 Q2Q2 0707 Q4Q4 Q3Q3 Q2Q2 1010 Q4Q4

Total DemandTotal Demand Effective Operating RateEffective Operating Rate Nameplate Operating RateNameplate Operating Rate

Flexible Packaging AssociationFlexible Packaging Association

Total DemandTotal Demand Effective Operating RateEffective Operating Rate Nameplate Operating RateNameplate Operating Rate

Dollars Per Metric Ton

Global Monthly Ethylene PricesGlobal Monthly Ethylene Prices

1,8001,800

2,0002,000Dollars Per Metric Ton

ForecastForecast

1,4001,400

1,6001,600

,,

1 0001 000

1,2001,200

1,4001,400

600600

800800

1,0001,000

400400

600600

2002000707 AA JJ OO 0808 AA JJ OO 0909 AA JJ OO 1010 AA JJ OO

U S L B C t t P iU S L B C t t P i WEP C t t P iWEP C t t P i SEA CFR S t P iSEA CFR S t P i

Flexible Packaging AssociationFlexible Packaging AssociationU.S. Large Buyer Contract PriceU.S. Large Buyer Contract Price WEP Contract PriceWEP Contract Price SEA CFR Spot PriceSEA CFR Spot Price

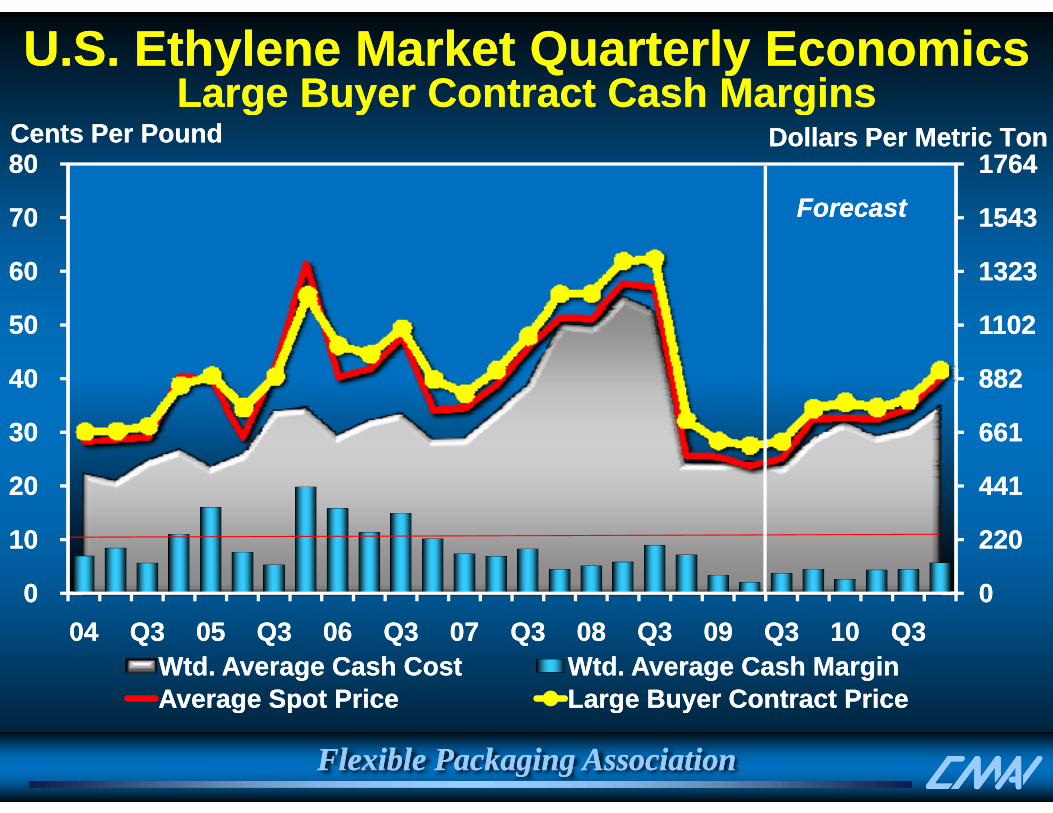

U.S. Ethylene Market Quarterly EconomicsU.S. Ethylene Market Quarterly EconomicsLarge Buyer Contract Cash MarginsLarge Buyer Contract Cash Margins

15431543

1764 1764

7070

80 80 ForecastForecast

Dollars Per Metric TonDollars Per Metric TonCents Per PoundCents Per Poundg y gg y g

1323 1323

1543 1543

60 60

70 70 ForecastForecast

882 882

1102 1102

40 40

50 50

441 441

661 661

20 20

30 30

0 0

220 220

0 0

10 10

0404 Q3Q3 0505 Q3Q3 0606 Q3Q3 0707 Q3Q3 0808 Q3Q3 0909 Q3Q3 1010 Q3Q3Wtd. Average Cash CostWtd. Average Cash Cost Wtd. Average Cash MarginWtd. Average Cash MarginAverage Spot PriceAverage Spot Price Large Buyer Contract PriceLarge Buyer Contract Price

Flexible Packaging AssociationFlexible Packaging Association

Average Spot PriceAverage Spot Price Large Buyer Contract PriceLarge Buyer Contract Price

U.S. Ethylene ConclusionsU.S. Ethylene Conclusions Oversupply and weak demand Oversupply and weak demand

result in long marketresult in long market Oversupply and weak demand Oversupply and weak demand

result in long marketresult in long marketresult in long marketresult in long market Olefins markets clearly in the Olefins markets clearly in the

trough, margins squeezed, prices trough, margins squeezed, prices

result in long marketresult in long market Olefins markets clearly in the Olefins markets clearly in the

trough, margins squeezed, prices trough, margins squeezed, prices trending upwardtrending upward

Heavy feed crackers challenged Heavy feed crackers challenged b d il i t lb d il i t l

trending upwardtrending upward Heavy feed crackers challenged Heavy feed crackers challenged

b d il i t lb d il i t lby crude oil prices vs. natural by crude oil prices vs. natural gasgas

North America ethyleneNorth America ethylene

by crude oil prices vs. natural by crude oil prices vs. natural gasgas

North America ethyleneNorth America ethylene North America ethylene North America ethylene derivative exports supported by derivative exports supported by favorable crudefavorable crude--toto--gas ratiogas ratio

North America ethylene North America ethylene derivative exports supported by derivative exports supported by favorable crudefavorable crude--toto--gas ratiogas ratio

Significant capacity reductions Significant capacity reductions are inevitableare inevitable

Significant capacity reductions Significant capacity reductions are inevitableare inevitable

Flexible Packaging AssociationFlexible Packaging Association

P l th lP l th lPolyethylenePolyethylene

Flexible Packaging AssociationFlexible Packaging Association

Since January of 09Since January of 09•• Several major resin producers were facing economic distress (Dow, LBI, Nova, Several major resin producers were facing economic distress (Dow, LBI, Nova, j p g ( , , ,j p g ( , , ,

IneosIneos etc..) and needed to take corrective action or collapse . They etc..) and needed to take corrective action or collapse . They closed closed plantsplants, , raised pricesraised prices, , controlled inventorycontrolled inventory, and took advantage of a lucrative , and took advantage of a lucrative exportexport market.market.

•• Exports became very attractive because the recession and startExports became very attractive because the recession and start--up problems up problems delayed the impact of new MDE capacity and delayed the impact of new MDE capacity and opened the window opened the window for for competitively produced US exports. competitively produced US exports.

•• A very favorable A very favorable crude oil to nat. gascrude oil to nat. gas price ratio developed leaving US price ratio developed leaving US d ll iti d t l l b l k t A f M h USd ll iti d t l l b l k t A f M h USproducers well positioned to supply global markets. As of March, US producers well positioned to supply global markets. As of March, US

producers have been exporting record volumes to China.producers have been exporting record volumes to China.

E b k d d h d f biE b k d d h d f bi b d ib d i•• Export netbacks exceeded the returns generated from bigExport netbacks exceeded the returns generated from big--buyer domestic buyer domestic sales Some producers shipping nearly 40 % of production overseas.sales Some producers shipping nearly 40 % of production overseas.

•• The strong export market allowed producers to keep inventories low, and The strong export market allowed producers to keep inventories low, and effective operating rates high despite a very weak domestic market. As a effective operating rates high despite a very weak domestic market. As a result they have been able raise prices (13 result they have been able raise prices (13 cppcpp since Jan for PE) and improve since Jan for PE) and improve

i Th t d lik l di t i t t ii Th t d lik l di t i t t i

Flexible Packaging AssociationFlexible Packaging Associationmargins. They turned a likely disaster year into a very strong earnings year.margins. They turned a likely disaster year into a very strong earnings year.

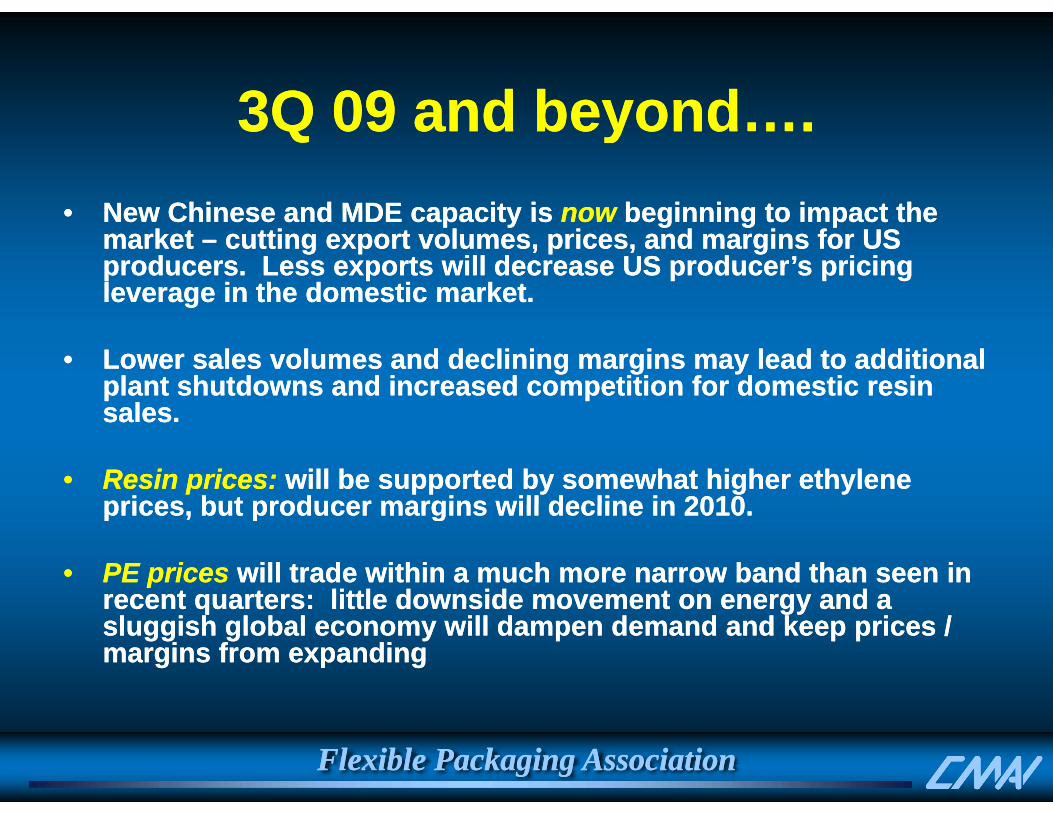

3Q 09 and beyond3Q 09 and beyond3Q 09 and beyond….3Q 09 and beyond….•• New Chinese and MDE capacity isNew Chinese and MDE capacity is nownow beginning to impact thebeginning to impact the•• New Chinese and MDE capacity is New Chinese and MDE capacity is nownow beginning to impact the beginning to impact the

market market –– cutting export volumes, prices, and margins for US cutting export volumes, prices, and margins for US producers. Less exports will decrease US producer’s pricing producers. Less exports will decrease US producer’s pricing leverage in the domestic market. leverage in the domestic market.

•• Lower sales volumes and declining margins may lead to additional Lower sales volumes and declining margins may lead to additional plant shutdowns and increased competition for domestic resin plant shutdowns and increased competition for domestic resin

llsales. sales.

•• Resin prices: Resin prices: will be supported by somewhat higher ethylene will be supported by somewhat higher ethylene prices but producer margins will decline in 2010prices but producer margins will decline in 2010prices, but producer margins will decline in 2010.prices, but producer margins will decline in 2010.

•• PE prices PE prices will trade within a much more narrow band than seen in will trade within a much more narrow band than seen in recent quarters: little downside movement on energy and arecent quarters: little downside movement on energy and arecent quarters: little downside movement on energy and a recent quarters: little downside movement on energy and a sluggish global economy will dampen demand and keep prices / sluggish global economy will dampen demand and keep prices / margins from expandingmargins from expanding

Flexible Packaging AssociationFlexible Packaging Association

3Q and beyond cont3Q and beyond cont3Q and beyond cont…3Q and beyond cont…

•• Resin Imports: Resin Imports: The relative strength of the US cost The relative strength of the US cost position along with the logistics constraints position along with the logistics constraints should minimize imports into the US. should minimize imports into the US.

•• Despite the delays, the new capacity in MDE andDespite the delays, the new capacity in MDE andDespite the delays, the new capacity in MDE and Despite the delays, the new capacity in MDE and China is coming and the industry is approaching China is coming and the industry is approaching record levels of overcapacity.record levels of overcapacity.p yp y

Flexible Packaging AssociationFlexible Packaging Association 2525

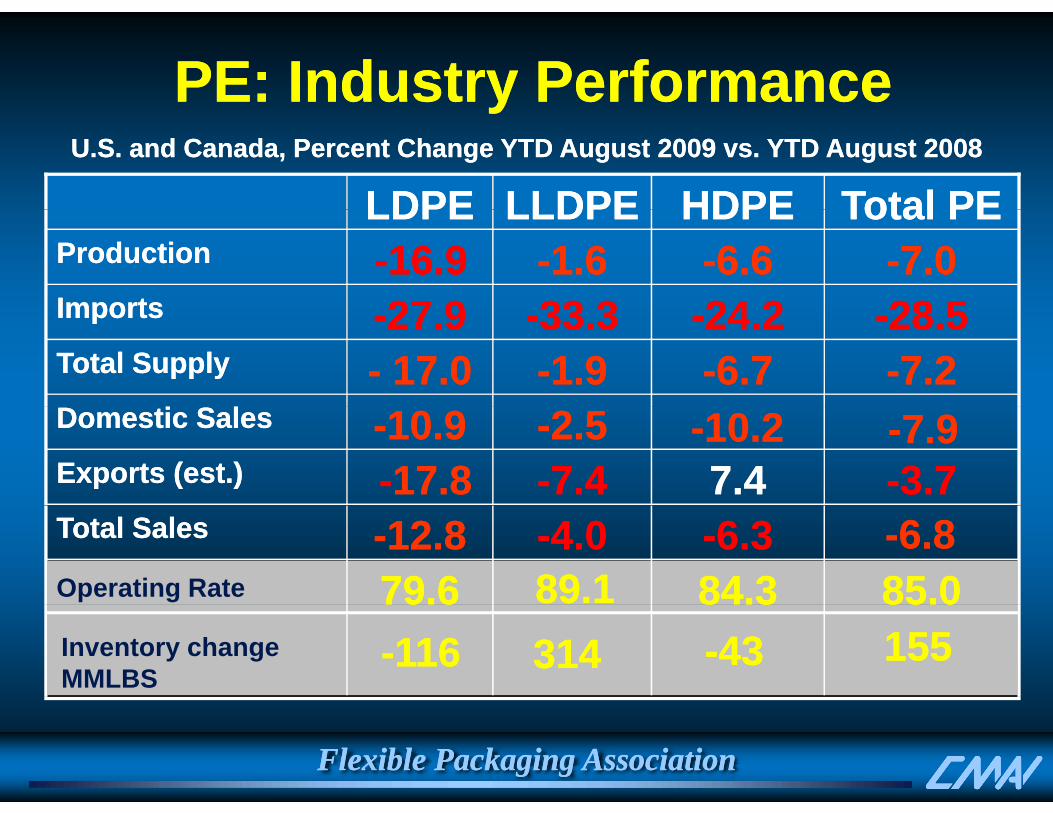

PE: Industry PerformancePE: Industry Performance

Total PETotal PEHDPEHDPELLDPELLDPELDPELDPEU.S. and Canada, Percent Change YTD August 2009 vs. YTD August 2008U.S. and Canada, Percent Change YTD August 2009 vs. YTD August 2008

yy

28 528 524 224 233 333 327 927 9ImportsImports--7.07.0--6.66.6--1.61.6--16.916.9ProductionProduction

Total PETotal PEHDPEHDPELLDPELLDPELDPELDPE

SS--7.27.2--6.76.7--1.91.9-- 17.017.0Total SupplyTotal Supply--28.528.5--24.224.2--33.333.3--27.927.9ImportsImports

--3.73.77.47.4--7.47.4--17.817.8Exports (est.)Exports (est.)--2.52.5--10.910.9Domestic SalesDomestic Sales --10.210.2 --7.97.9

85.085.084.384.389.189.179.679.6Operating Rate

--6.36.3--4.04.0--12.812.8Total SalesTotal Sales --6.86.8

155155--4343314314--116116Inventory change MMLBS

85.085.084.384.379.679.6

Flexible Packaging AssociationFlexible Packaging Association

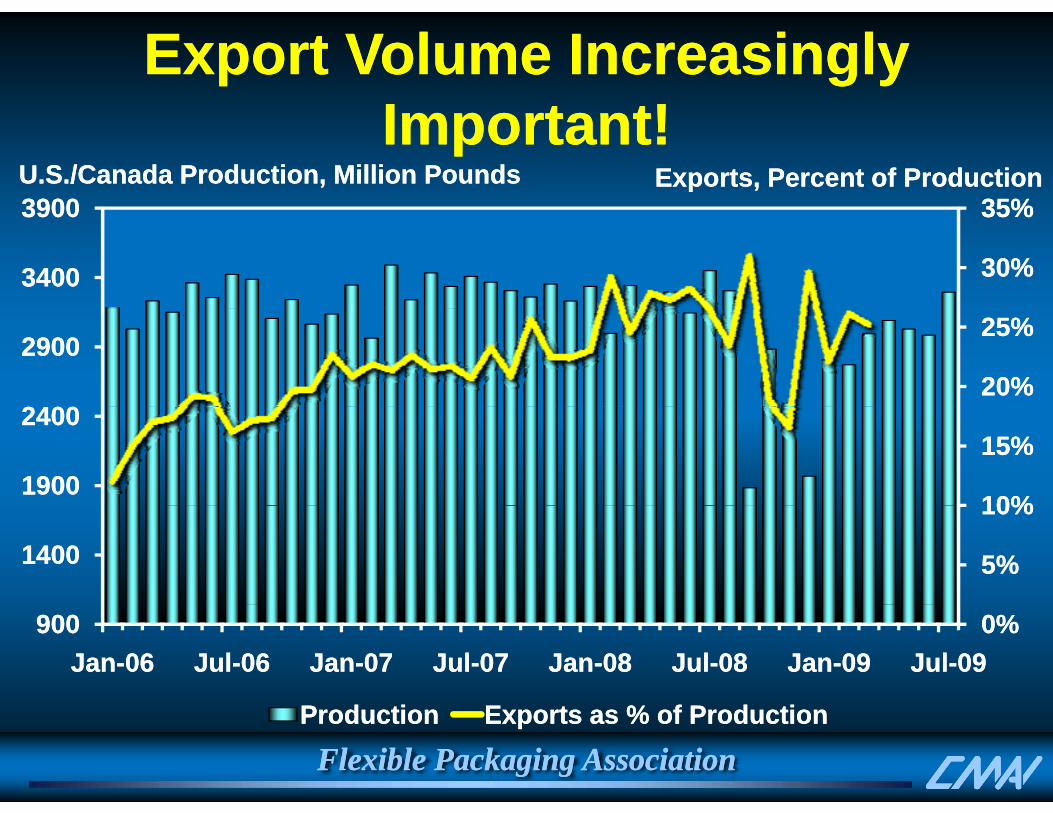

Export Volume Increasingly Export Volume Increasingly I t t!I t t!

35%35%39003900

Important!Important!U.S./Canada ProductionU.S./Canada Production, Million Pounds, Million Pounds Exports, Percent of ProductionExports, Percent of Production

30%30%

35%35%

34003400

39003900

20%20%

25%25%

24002400

29002900

10%10%

15%15%19001900

24002400

5%5%

10%10%

14001400

0%0%900900JanJan--0606 JulJul--0606 JanJan--0707 JulJul--0707 JanJan--0808 JulJul--0808 JanJan--0909 JulJul--0909

Flexible Packaging AssociationFlexible Packaging AssociationProductionProduction Exports as % of ProductionExports as % of Production

U.S. PE ExportsU.S. PE ExportsThousand Metric TonsThousand Metric Tons

450450

500500Thousand Metric TonsThousand Metric Tons

350350

400400

250250

300300

100100

150150

200200

00

5050

100100

000606 MM MM JJ SS NN 0707 MM MM JJ SS NN 0808 MM MM JJ SS NN 0909 MM MM

Total Selected RegionsTotal Selected Regions N AmericaN America S AmericaS America EuropeEurope Far EastFar East OtherOther

Flexible Packaging AssociationFlexible Packaging Association

Total Selected RegionsTotal Selected Regions N.AmericaN.America S.AmericaS.America EuropeEurope Far EastFar East OtherOther

U.S./Canada PE Film Resin Quarterly Demand

35003500

Quarterly DemandMillion PoundsMillion Pounds

ForecastForecast

30003000

25002500

20002000

10001000

15001500

100010000303 Q3Q3 0404 Q3Q3 0505 Q3Q3 0606 Q3Q3 0707 Q3Q3 0808 Q3Q3 0909 Q3Q3 1010 Q3Q3

Film Resin DemandFilm Resin Demand

Flexible Packaging AssociationFlexible Packaging AssociationSource: ACCSource: ACC, Plastics Division; , Plastics Division; Gov’tGov’t Trade DataTrade Data

HDPE Film Resin Demand July YTDHDPE Film Resin Demand July YTDHDPE Film Resin Demand July YTDHDPE Film Resin Demand July YTD

HDPEHDPE Percent ChangePercent ChangeFilm 12 Mils and BelowFilm 12 Mils and Below --2.12.1

Packaging FilmPackaging Film --8.38.3Food Packaging FilmFood Packaging Film --1.31.3NonNon--Food Packaging FilmFood Packaging Film --15.015.0

NonNon--Packaging FilmPackaging Film 0.60.6Retail BagsRetail Bags --2.82.8Trash and Can LinersTrash and Can Liners 10.410.4Other NonOther Non--Packaging FilmPackaging Film --28.028.0

Flexible Packaging AssociationFlexible Packaging AssociationSource: ACCSource: ACC, Plastics Division; , Plastics Division; Gov’tGov’t Trade DataTrade Data

LLDPE Film Resin Demand July YTDLLDPE Film Resin Demand July YTDyy

LLDPELLDPE Percent ChangePercent Change22--7.27.2

--6.86.87 37 3

Film (12 Mils and Below)Film (12 Mils and Below)Packaging FilmPackaging FilmFood Packaging FilmFood Packaging Film --7.37.3

--14.014.0--7 87 8

NonNon--Food Packaging FilmFood Packaging FilmNonNon--Packaging FilmPackaging Film

Food Packaging FilmFood Packaging Film

7.87.8NonNon--Packaging FilmPackaging Film

Flexible Packaging AssociationFlexible Packaging AssociationSource: ACCSource: ACC, Plastics Division; , Plastics Division; Gov’tGov’t Trade DataTrade Data

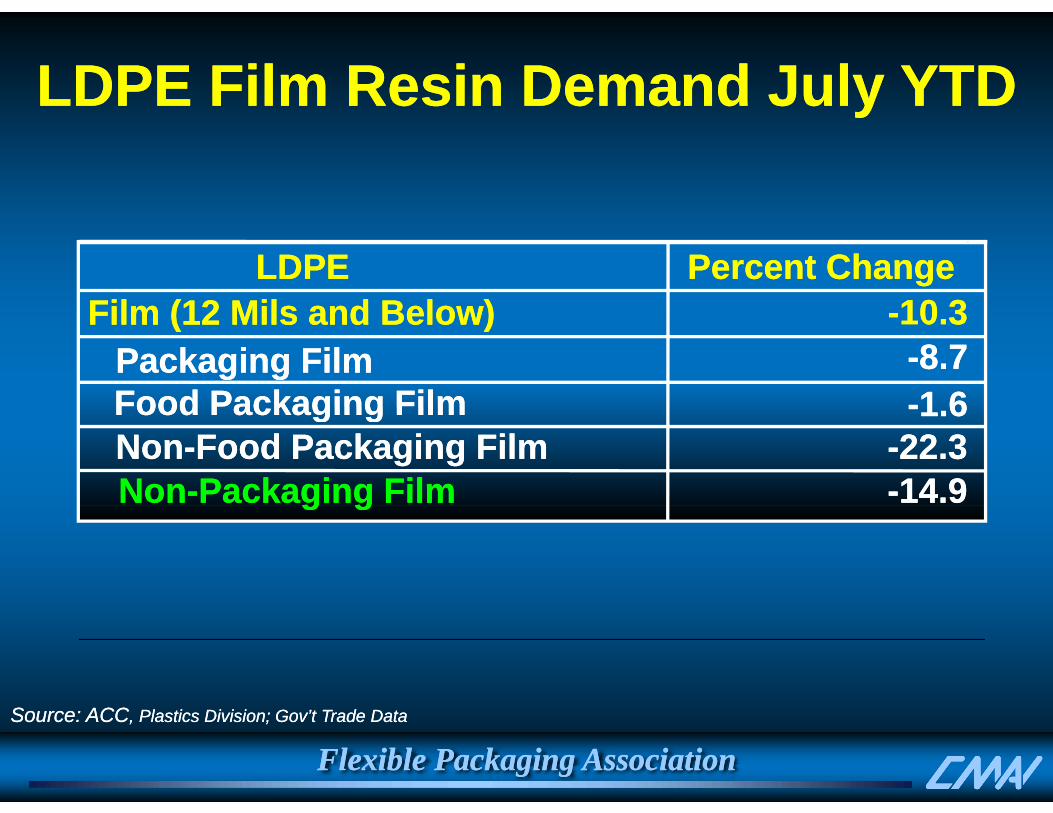

LDPE Film Resin Demand July YTDLDPE Film Resin Demand July YTDyy

LDPELDPE Percent ChangePercent Change10 310 3Film (12 Mils and Below)Film (12 Mils and Below) --10.310.3--8.78.7--1 61 6

Film (12 Mils and Below)Film (12 Mils and Below)Packaging FilmPackaging FilmFoodFood Packaging FilmPackaging Film --1.61.6NonNon--Food Packaging FilmFood Packaging Film --22.322.3NonNon--Packaging FilmPackaging Film --14.914.9

FoodFood Packaging FilmPackaging Film

g gg g

Flexible Packaging AssociationFlexible Packaging AssociationSource: ACCSource: ACC, Plastics Division; , Plastics Division; Gov’tGov’t Trade DataTrade Data

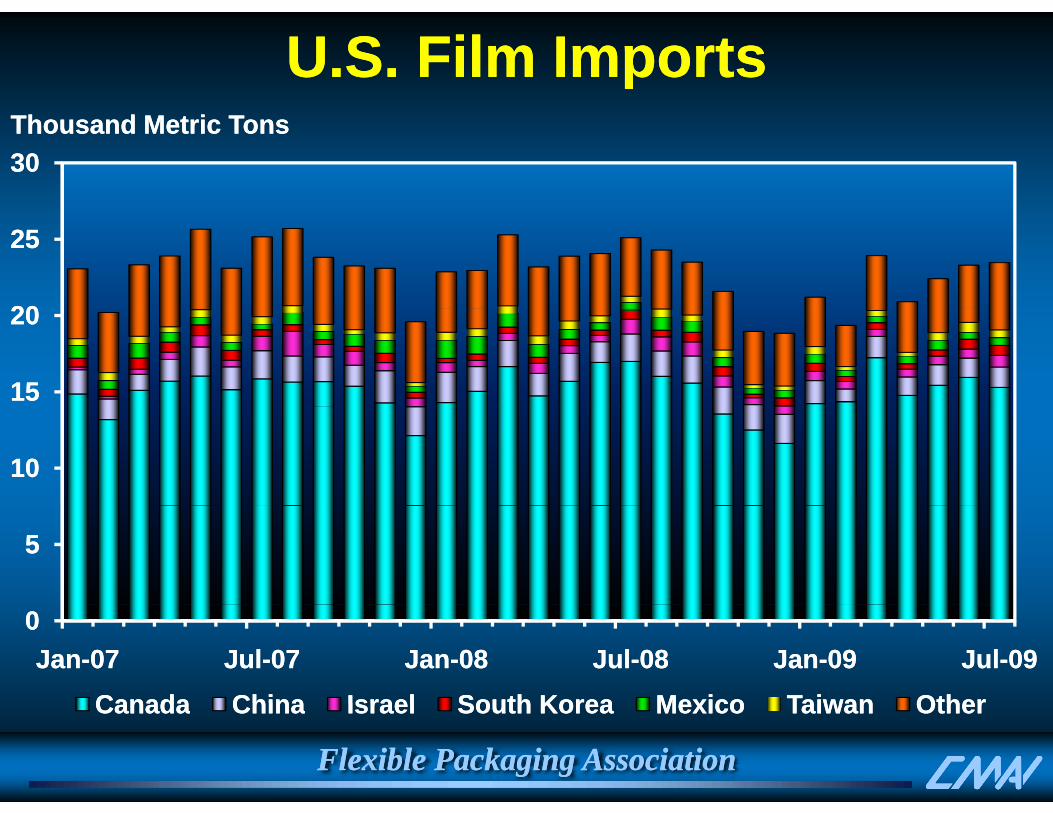

U.S. Film ImportsU.S. Film Imports3030Thousand Metric TonsThousand Metric Tons

2020

2525

1515

2020

1010

55

00JanJan--0707 JulJul--0707 JanJan--0808 JulJul--0808 JanJan--0909 JulJul--0909

CanadaCanada ChinaChina IsraelIsrael South KoreaSouth Korea MexicoMexico TaiwanTaiwan OtherOther

Flexible Packaging AssociationFlexible Packaging Association

CanadaCanada ChinaChina IsraelIsrael South KoreaSouth Korea MexicoMexico TaiwanTaiwan OtherOther

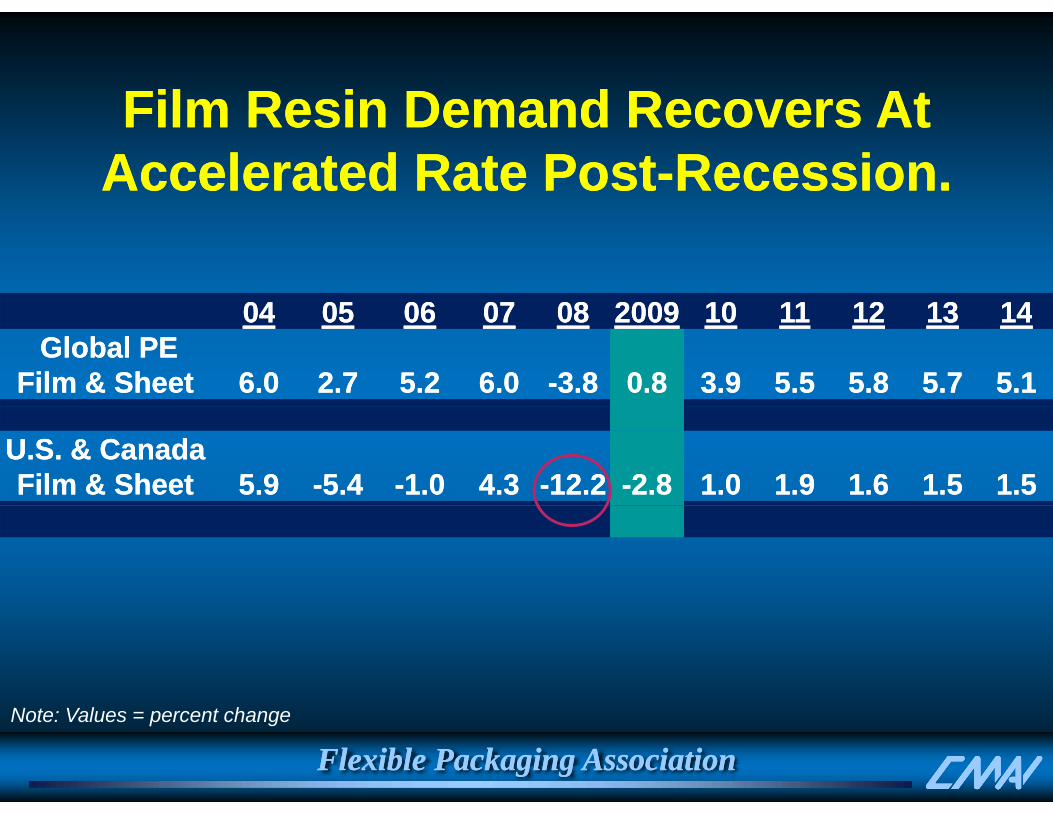

Film Resin Demand Recovers AtFilm Resin Demand Recovers AtFilm Resin Demand Recovers At Film Resin Demand Recovers At Accelerated Rate PostAccelerated Rate Post--Recession.Recession.

0404 0505 0606 0707 0808 20092009 1010 1111 1212 1313 14140404 0505 0606 0707 0808 20092009 1010 1111 1212 1313 1414Global PE Global PE

Film Film & Sheet& Sheet 6.06.0 2.72.7 5.25.2 6.06.0 --3.83.8 0.80.8 3.93.9 5.55.5 5.85.8 5.75.7 5.15.1

U.S. & CanadaU.S. & CanadaFilm & SheetFilm & Sheet 5.95.9 --5.45.4 --1.01.0 4.34.3 --12.212.2 --2.82.8 1.01.0 1.91.9 1.61.6 1.51.5 1.51.5

Flexible Packaging AssociationFlexible Packaging AssociationNote: Values = percent change

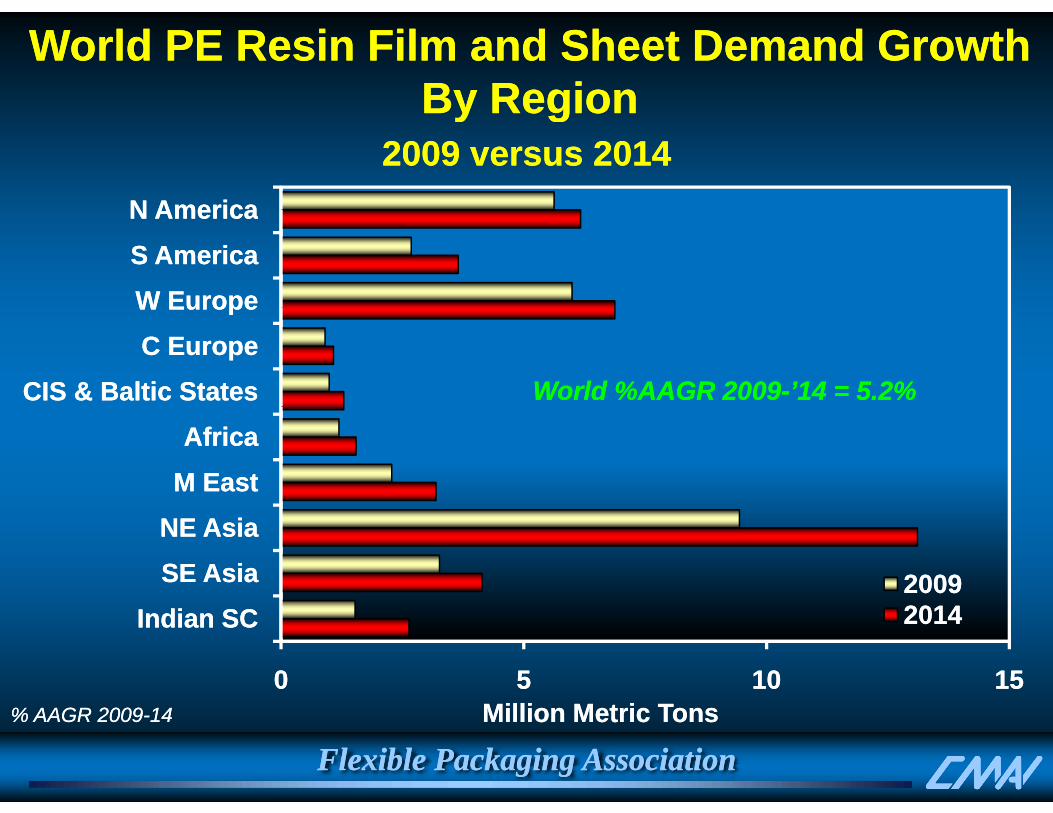

World World PE Resin PE Resin Film and Sheet Demand Film and Sheet Demand Growth Growth ByBy RegionRegion

N AmericaN America

2009 2009 versus versus 20142014By By RegionRegion

W EuropeW EuropeS AmericaS AmericaN AmericaN America

CIS & Baltic StatesCIS & Baltic StatesC EuropeC EuropeW EuropeW Europe

World %AAGR 2009World %AAGR 2009--’14 = 5.2%’14 = 5.2%

M EastM EastAfricaAfrica

SE AsiaSE AsiaNE AsiaNE Asia

20092009

00 55 1010 1515

Indian SCIndian SC 20142014

Flexible Packaging AssociationFlexible Packaging AssociationMillion Metric TonsMillion Metric Tons% AAGR 2009% AAGR 2009--1414

PolyethylenePolyethylene Capacity ChangesCapacity ChangesNAMNAM WEPWEP MDEMDE NEA / SEA / ISCNEA / SEA / ISC Net Net

IncreaseIncreaseCompanyCompany ktakta CompanyCompany ktakta CompanyCompany ktakta CompanyCompany ktaktaCompanyCompany ktakta CompanyCompany ktakta CompanyCompany ktakta CompanyCompany ktakta

1Q-0

9 LBI USA LD (68) SABIC GFR HD x 150 Jam PC IRN HD/LL 300 PT Titan INO HD/LL x 50 Honam KOS LL x 70

502502

9

Dow USA LD (100) SEPC KSA LD 400 Reliance IND HD 90 P t R bi h KSA HD 300

2Q-0

9 Petro-Rabigh KSA HD 300 Laleh IRN LD 300 TKOC KUW HD/LL 225 Arya Sasol IRN HD 300 1515 1515

LBILBI USAUSA HDHD (181)(181) LBILBI FRAFRA LDLD (110)(110) Mehr PC IRN HD 300 Secco CHI HD/LL x 150

3Q-0

9 FPCFPC USAUSA HD xHD x 42 42 SABIC UK LD 400 Petro-Rabigh KSA LL 600 FujianFujian CHICHI HD/LLHD/LL 800 800 Flint HillsFlint Hills USAUSA LLLL (150)(150) YansabYansab KSAKSA LLLL 500 500 DushanziDushanzi CHICHI HDHD 300 300 Flint HillsFlint Hills USAUSA LDLD (194)(194) DushanziDushanzi CHICHI HD/LLHD/LL 600 600

Shenyang ParaffinShenyang Paraffin CHICHI HD/LLHD/LL 120 120 3177 3177 TotalTotal FRAFRA LDLD (230)(230) QatofinQatofin QATQAT LLLL 450450 PanjinPanjin EthEth CHICHI HD/LLHD/LL 300300

4Q-0

9

TotalTotal FRAFRA LDLD (230)(230) QatofinQatofin QATQAT LLLL 450 450 PanjinPanjin Eth.Eth. CHICHI HD/LLHD/LL 300 300 Total Total FRAFRA LDLD (160)(160) Bangkok PEBangkok PE THATHA HDHD 250 250 SABICSABIC NETNET LDLD (120)(120) SHARQSHARQ KSAKSA HDHD 400 400 PTT PTT ChemChem THATHA LLLL 400 400 BorealisBorealis SWESWE HD/LLHD/LL (90)(90) SHARQSHARQ KSAKSA LLLL 400 400 PTT PTT ChemChem THATHA HD xHD x 50 50

Amir Amir KabirKabir IRNIRN LDLD 300 300 1950 1950

1Q-1

0 BorealisBorealis SWESWE LDLD 350350 YansabYansab KSAKSA HDHD 400400 GailGail INDIND LL xLL x 5050LBILBI GFRGFR HDHD 250250 QQ--ChemChem IIII QATQAT HDHD 350 350 Tianjin PCTianjin PC CHICHI HD/LLHD/LL 600600

2000 2000 BorealiBorealiss BELBEL HDHD (200)(200) Indian OilIndian Oil INDIND HDHD 300300

2Q-1

0

ss BELBEL HDHD (200)(200) Indian OilIndian Oil INDIND HDHD 300300Indian OilIndian Oil INDIND HD/LLHD/LL 350350PTT PTT ChemChem THATHA LDLD 300300Baotou Baotou ShenhuaShenhua CHICHI HD/LLHD/LL 300300ZRCCZRCC CHICHI HD/LLHD/LL 450450MOCMOC THATHA LLLL 300300

Flexible Packaging AssociationFlexible Packaging Association

MOCMOC THATHA LLLL 300300TPETPE THATHA HDHD 400400 2200 2200

Still Too Much CapacityStill Too Much Capacity

9595

100100

2020

2424Million Metric TonsMillion Metric Tons Operating Rate, PercentOperating Rate, Percent

9090

9595

1616

2020

8080

8585

88

1212

7070

7575

00

44

6060

6565

--88

--44

19971997 19991999 20012001 20032003 20052005 20072007 20092009 20112011 20132013

Capacity Increase Capacity Increase -- Demand IncreaseDemand Increase Cummulative Delta CapsCummulative Delta Caps--Delta DemDelta DemO ti R tO ti R t

Flexible Packaging AssociationFlexible Packaging AssociationOperating RateOperating Rate

Energy: PE Price DriverEnergy: PE Price Driver25002500140140

U.S. Dollars Per BarrelU.S. Dollars Per Barrel LLDPE, U.S. Dollars Per TonLLDPE, U.S. Dollars Per Ton

ForecastForecast

20002000100100

120120ForecastForecast

15001500

6060

8080

500500

10001000

4040

6060

00

500500

00

2020

JanJan--0707 JulJul--0707 JanJan--0808 JulJul--0808 JanJan--0909 JulJul--0909 JanJan--1010 JulJul--1010

Naphtha SEANaphtha SEA Dubai Crude OilDubai Crude Oil LLDPE CFR ChinaLLDPE CFR ChinaLLDPE NAMLLDPE NAM LLDPE WEPLLDPE WEP

Flexible Packaging AssociationFlexible Packaging AssociationLLDPE NAMLLDPE NAM LLDPE WEPLLDPE WEP

Dollars Per Metric TonDollars Per Metric Ton

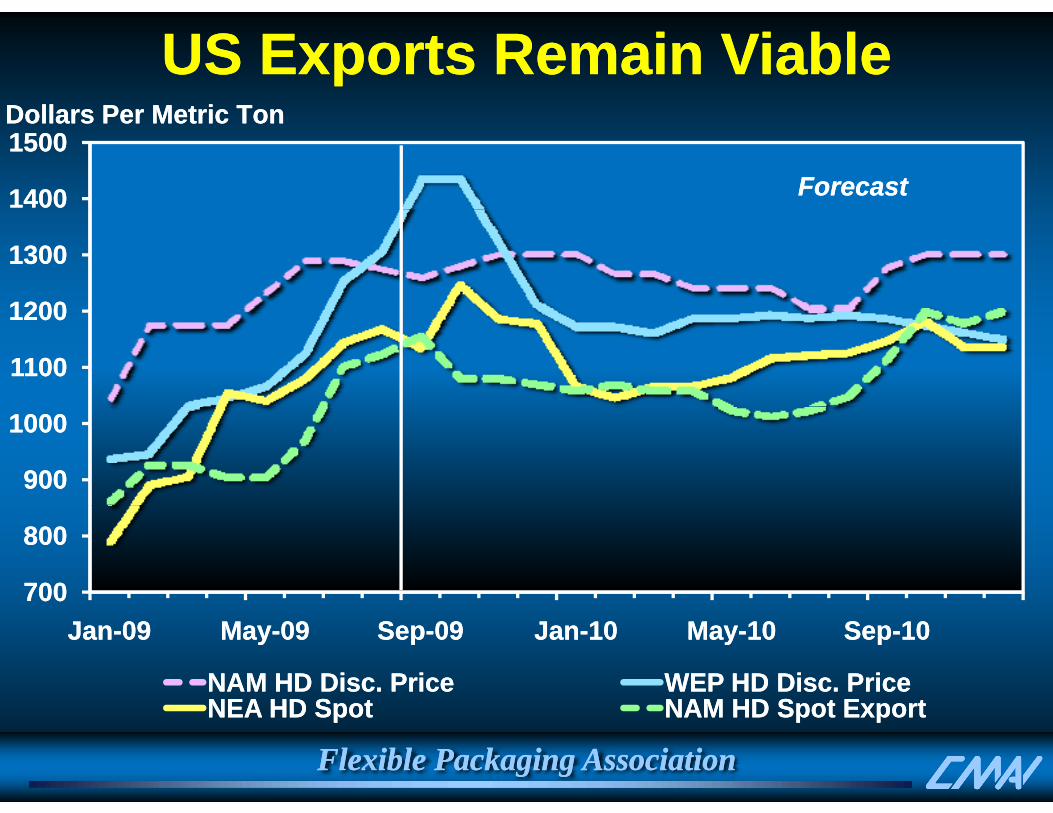

US Exports Remain Viable US Exports Remain Viable

14001400

15001500Dollars Per Metric TonDollars Per Metric Ton

ForecastForecast

12001200

13001300

11001100

12001200

900900

10001000

700700

800800

JanJan--0909 MayMay--0909 SepSep--0909 JanJan--1010 MayMay--1010 SepSep--1010

NAM HD Disc. PriceNAM HD Disc. Price WEP HD Disc. PriceWEP HD Disc. PriceNEA HD S tNEA HD S t NAM HD S t E tNAM HD S t E t

Flexible Packaging AssociationFlexible Packaging Association

NEA HD Spot NEA HD Spot NAM HD Spot ExportNAM HD Spot Export

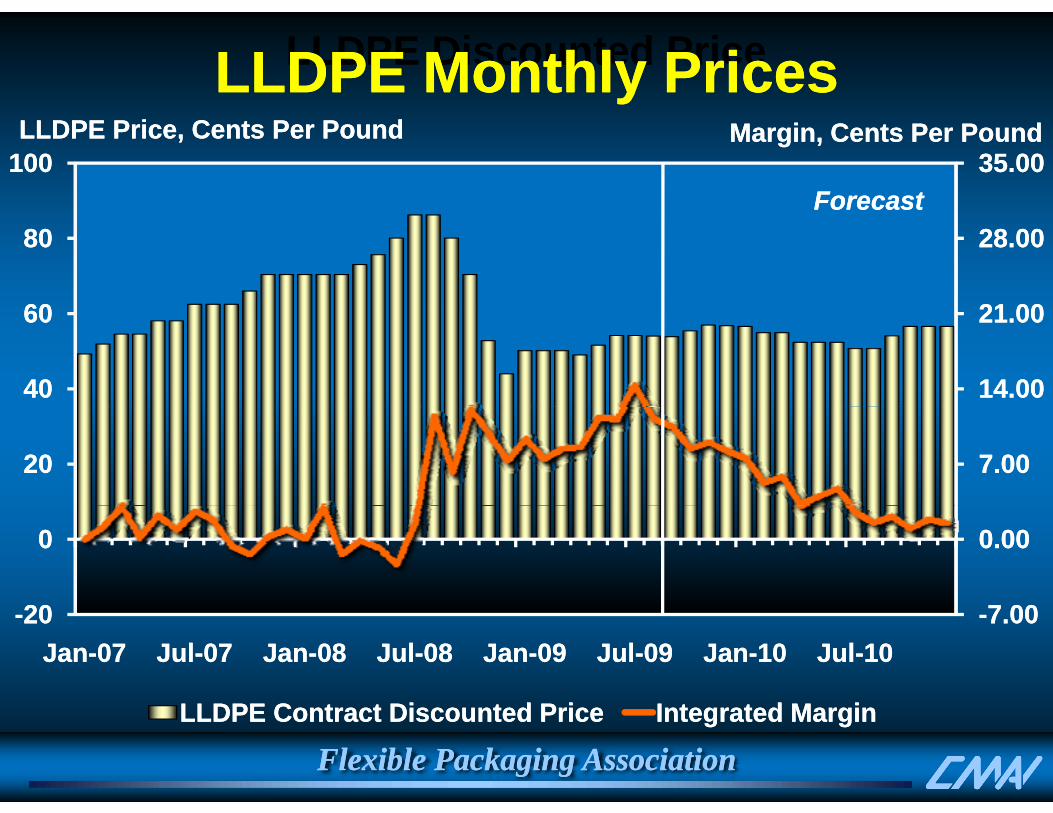

LLDPE Discounted PriceLLDPE Monthly PricesLLDPE Monthly Prices35.0035.00100100

LLDPE Price, CentsLLDPE Price, Cents Per PoundPer Pound Margin,Margin, Cents Per PoundCents Per Pound

ForecastForecast

21 0021 00

28.0028.00

6060

8080ForecastForecast

14.0014.00

21.0021.00

4040

6060

7.007.002020

0.000.0000

--7.007.00--2020JanJan--0707 JulJul--0707 JanJan--0808 JulJul--0808 JanJan--0909 JulJul--0909 JanJan--1010 JulJul--1010

LLDPE C Di d P iLLDPE C Di d P i I d M iI d M i

Flexible Packaging AssociationFlexible Packaging AssociationLLDPE Contract Discounted PriceLLDPE Contract Discounted Price Integrated MarginIntegrated Margin

PEPE TakeTake--AwaysAwaysPE PE TakeTake AwaysAways•• PE prices less volatile through 2010 than in PE prices less volatile through 2010 than in

t tt trecent past.recent past.•• YTD margins stronger than expected due to YTD margins stronger than expected due to

robust exports capacity shutdowns / turndownsrobust exports capacity shutdowns / turndownsrobust exports, capacity shutdowns / turndowns robust exports, capacity shutdowns / turndowns and unusual producer market / production and unusual producer market / production disciplinediscipline

•• NAM PE cost advantage strong NAM PE cost advantage strong vsvs other regions other regions ex. MDEex. MDE

•• Despite delays and shutdowns unprecedentedDespite delays and shutdowns unprecedented•• Despite delays and shutdowns, unprecedented Despite delays and shutdowns, unprecedented oversupply conditions will drive down operating oversupply conditions will drive down operating rates and margins beginning 4Q 09.rates and margins beginning 4Q 09.

•• The cycle trough is expected from 4Q 09 The cycle trough is expected from 4Q 09 -- 2010, 2010, global recovery evident by 2011global recovery evident by 2011

Flexible Packaging AssociationFlexible Packaging Association

PROPYLENE & PROPYLENE & POLYPROPYLENEPOLYPROPYLENE

Flexible Packaging AssociationFlexible Packaging Association

Propylene Supply ProfilePropylene Supply ProfileAlkylationMM MotorMotor

FCC U it

Alkylation

Unit

IsobutaneIsobutane

High Octane Alkylate High Octane Alkylate GasolineGasoline

Crude

Motor Motor GasolineGasoline

Motor Motor GasolineGasoline

Unit Other Fuel UsesOther Fuel Uses

Refining IndustryRefining Industry

Gas Gas OilOil

UnitCrude Crude OilOil

Cumene, Oligomers Cumene, Oligomers IsopropanolIsopropanol

Purification Splitter Unit

Chemical IndustryChemical Industry

RG RG Propylene Propylene MarketMarket Polypropylene I j tiI j ti

Steam Cracker orPropane to LPGPropane to LPG

Splitter UnitMarketMarket

NaphthaNaphtha

Polypropylene

Unit

Injection Injection Molding, Molding, Fibers, Fibers, FilmsFilms

Steam Cracker or Olefin Plant

Ethane Ethane PropanePropane Other propylene consumers: acrylonitrile, Other propylene consumers: acrylonitrile,

propylene oxide, acrylic acid, oxopropylene oxide, acrylic acid, oxo--alcoholsalcoholsEthyleneEthylene

Propane Propane DehydroDehydro

Other Technologies PG & CG PG & CG

Propylene Propylene MarketsMarkets

Ethylene Ethylene & Olefins& OlefinsMetathesisMetathesis

Olefin CrackingOlefin Cracking

HSFCCHSFCC

Flexible Packaging AssociationFlexible Packaging Association

MarketsMarketsGasGas--toto--OlefinsOlefins

OthersOthers

U.S. PROPYLENEU.S. PROPYLENECurrent SituationCurrent Situation

Key PointsKey PointsKey PointsKey Points•• Derivative operating rates reduced with weak Derivative operating rates reduced with weak

d dd ddemand.demand.•• Steam cracker production reduced by 1/3 with Steam cracker production reduced by 1/3 with p yp y

move to light move to light feedslatesfeedslates and shutdowns.and shutdowns.•• Refinery production reduced by 8 to 10Refinery production reduced by 8 to 10•• Refinery production reduced by 8 to 10 Refinery production reduced by 8 to 10

percent with lower refinery rates.percent with lower refinery rates.I t i lI t i l•• Inventories lowInventories low

•• Tight supply/demand globallyTight supply/demand globally

Flexible Packaging AssociationFlexible Packaging Association

g pp y g yg pp y g y

Propylene ScarcePropylene Scarce6.06.0U.S. Weekly Propylene (NonU.S. Weekly Propylene (Non--Fuel Use) Ending Stocks, MM BarrelsFuel Use) Ending Stocks, MM Barrels

4 04 0

5.05.0

3.03.0

4.04.0

2.02.0

1.01.0

Source: EIA; Data Through 21Source: EIA; Data Through 21--AugAug--09090.00.0

JanJan FebFeb MarMar AprApr MayMay JunJun JulJul AugAug SepSep OctOct NovNov DecDec

55 Y MINY MIN MAX RMAX R 55 Y MINY MIN 20072007 20082008 20092009

Source: EIA; Data Through 21Source: EIA; Data Through 21 AugAug 0909

Flexible Packaging AssociationFlexible Packaging Association55--Yr MINYr MIN--MAX RangeMAX Range 55--Yr MINYr MIN 20072007 20082008 20092009

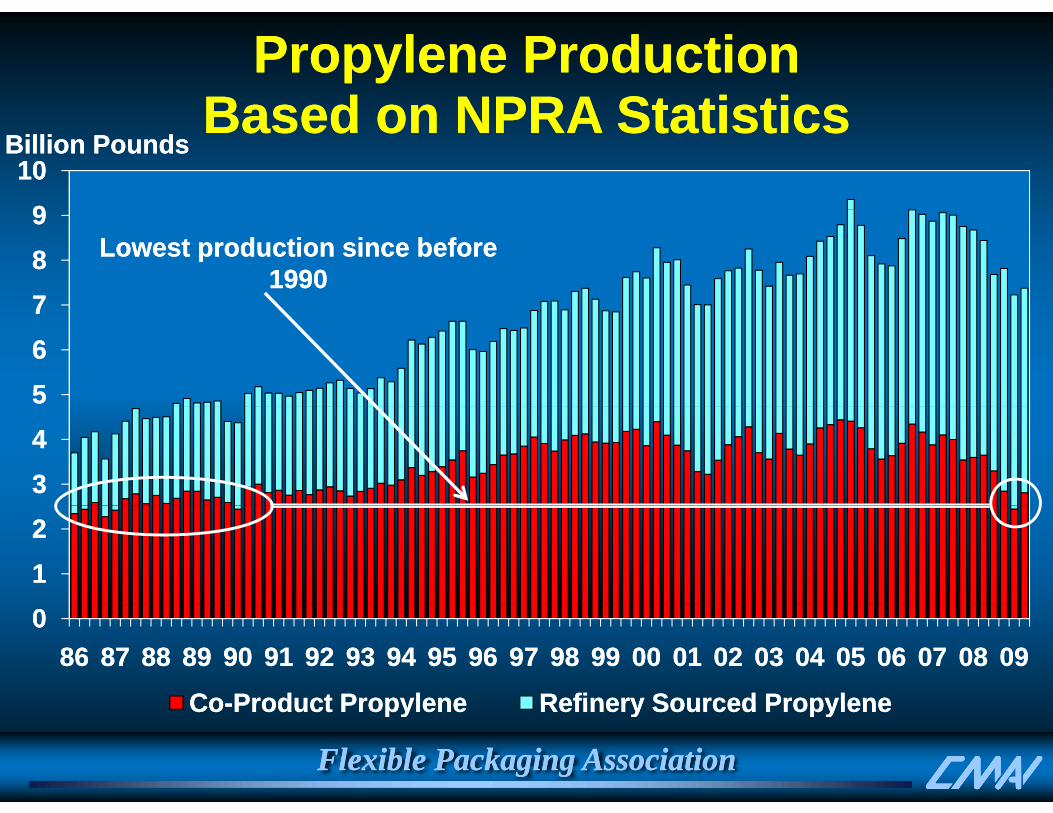

Propylene ProductionPropylene ProductionBased on NPRA StatisticsBased on NPRA Statistics

991010

Billion PoundsBillion PoundsBased on NPRA StatisticsBased on NPRA Statistics

778899

Lowest production since before Lowest production since before 19901990

556677

3344

1122

008686 8787 8888 8989 9090 9191 9292 9393 9494 9595 9696 9797 9898 9999 0000 0101 0202 0303 0404 0505 0606 0707 0808 0909

CoCo Product PropyleneProduct Propylene Refinery Sourced PropyleneRefinery Sourced Propylene

Flexible Packaging AssociationFlexible Packaging Association

CoCo--Product PropyleneProduct Propylene Refinery Sourced PropyleneRefinery Sourced Propylene

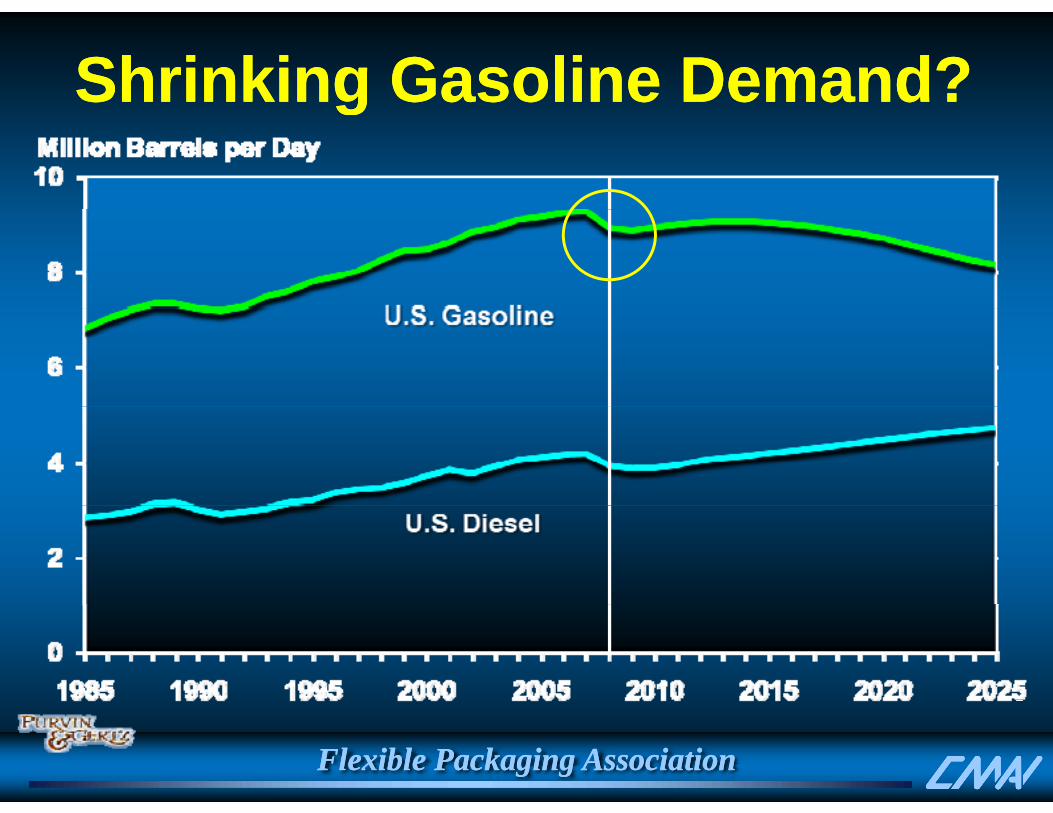

Shrinking Gasoline Demand?Shrinking Gasoline Demand?gg

Flexible Packaging AssociationFlexible Packaging Association

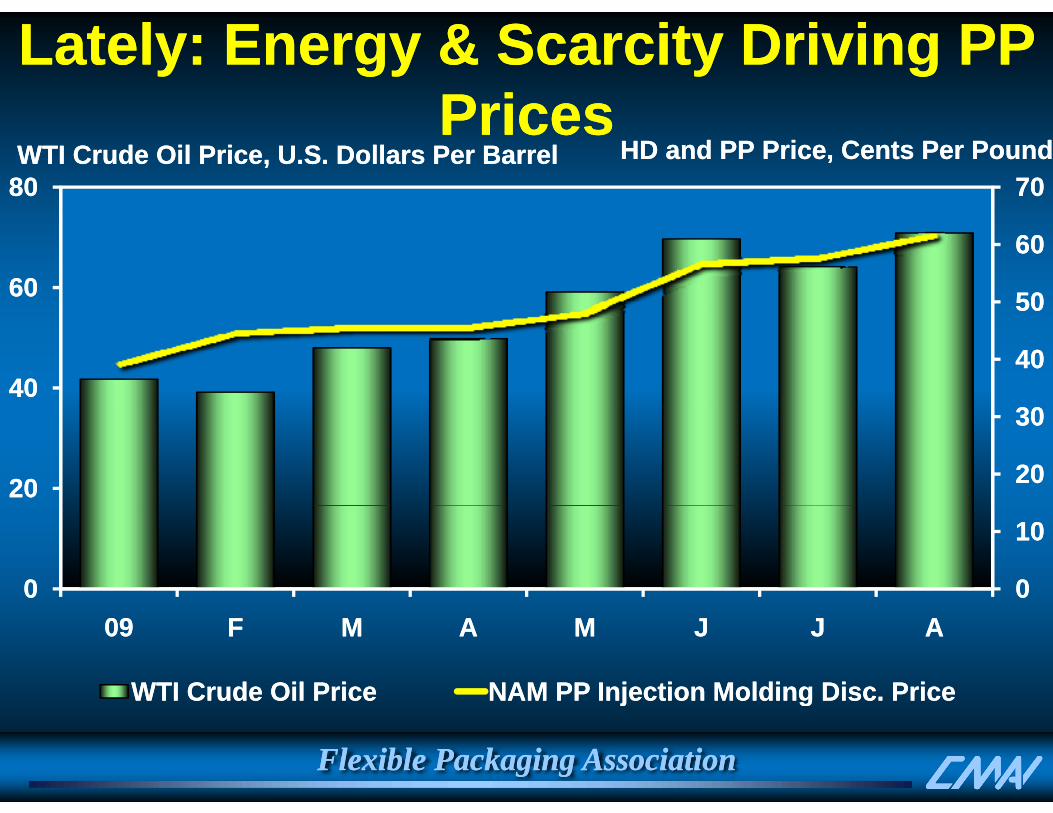

Lately: Energy & Scarcity Driving PP Lately: Energy & Scarcity Driving PP PricesPrices

70708080WTI Crude OilWTI Crude Oil Price,Price, U.SU.S. Dollars . Dollars Per BarrelPer Barrel HD and PP Price, Cents Per PoundHD and PP Price, Cents Per Pound

Prices Prices

5050

60606060

3030

4040

5050

4040

2020

3030

2020

00

1010

000909 FF MM AA MM JJ JJ AA

WTI Crude Oil PriceWTI Crude Oil Price NAM PP Injection Molding Disc. PriceNAM PP Injection Molding Disc. Price

Flexible Packaging AssociationFlexible Packaging Association

j gj g

Exports to Asia Soared…Exports to Asia Soared…120120US PP US PP , , Thousand Metric TonsThousand Metric Tons

pp

100100

6060

8080

4040

00

2020

000606 AA JJ OO 0707 AA JJ OO 0808 AA JJ OO 0909 AA

N AmericaN America S AmericaS America EuropeEuropeOtherOther Far EastFar East

Flexible Packaging AssociationFlexible Packaging Association

N. AmericaN. America S. AmericaS. America EuropeEuropeOtherOther Far EastFar East

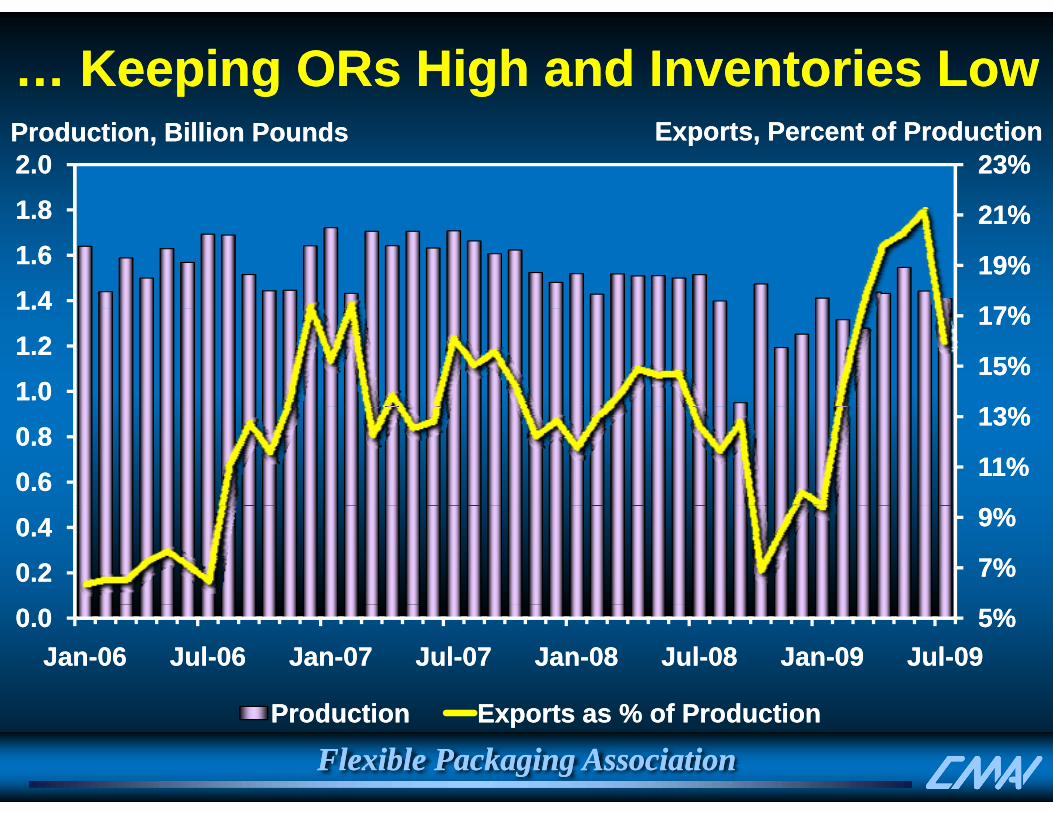

… Keeping ORs High and Inventories Low… Keeping ORs High and Inventories Low

21%21%

23%23%1 81 82.02.0Production, Production, Billion Billion PoundsPounds Exports, Percent of ProductionExports, Percent of Production

17%17%

19%19%

21%21%

1.41.41.61.61.81.8

13%13%

15%15%

17%17%

1.01.01.21.21.41.4

11%11%

13%13%

0.60.60.80.8

7%7%

9%9%

0.20.20.40.4

5%5%0.00.0JanJan--0606 JulJul--0606 JanJan--0707 JulJul--0707 JanJan--0808 JulJul--0808 JanJan--0909 JulJul--0909

Flexible Packaging AssociationFlexible Packaging AssociationProductionProduction Exports as % of ProductionExports as % of Production

PP Demand July YTDPP Demand July YTDPP Demand July YTDPP Demand July YTD

PPPP Percent ChangePercent ChangeFilm 10 Mils and BelowFilm 10 Mils and Below --8.48.4Oriented FilmOriented Film --7.27.2

NonNon--Oriented FilmOriented Film --12.412.4Sheet (Over 10 Mils)Sheet (Over 10 Mils) --2.22.2PackagingPackaging --25.325.3

NonNon--PackagingPackaging --38.338.3

Flexible Packaging AssociationFlexible Packaging AssociationSource: ACCSource: ACC, Plastics Division; , Plastics Division; Gov’tGov’t Trade DataTrade Data

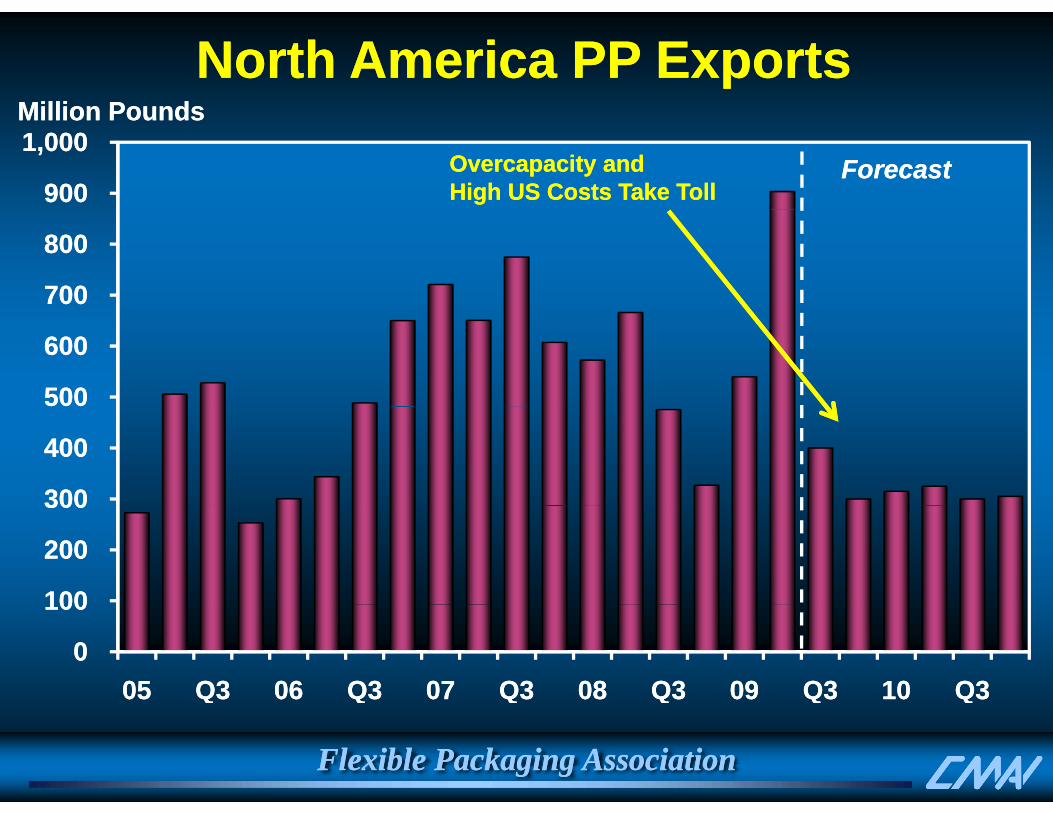

Million PoundsMillion PoundsNorth America PP ExportsNorth America PP Exports

900 900

1,000 1,000 Million PoundsMillion Pounds

ForecastForecastOvercapacityOvercapacity and and High US Costs Take TollHigh US Costs Take Toll

700 700

800 800

500 500

600 600

300300

400 400

100100

200 200

300 300

0 0

100 100

0505 Q3Q3 0606 Q3Q3 0707 Q3Q3 0808 Q3Q3 0909 Q3Q3 1010 Q3Q3

Flexible Packaging AssociationFlexible Packaging Association

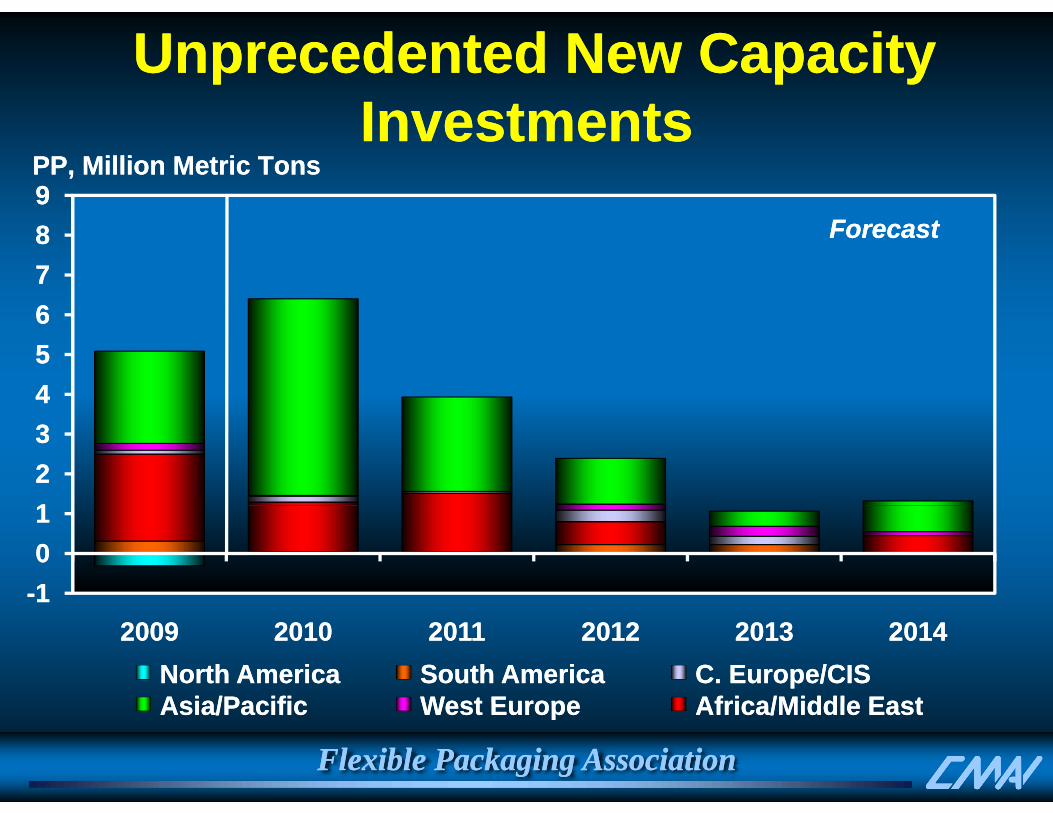

Unprecedented New Capacity Unprecedented New Capacity I t tI t tInvestmentsInvestments

99PP, Million Metric TonsPP, Million Metric Tons

667788 ForecastForecast

445566

112233

--110011

20092009 20102010 20112011 20122012 20132013 20142014North AmericaNorth America South AmericaSouth AmericaAsia/PacificAsia/Pacific West EuropeWest Europe

C. Europe/CISC. Europe/CISAfrica/Middle EastAfrica/Middle East

Flexible Packaging AssociationFlexible Packaging Association

Asia/PacificAsia/Pacific West EuropeWest Europe Africa/Middle EastAfrica/Middle East

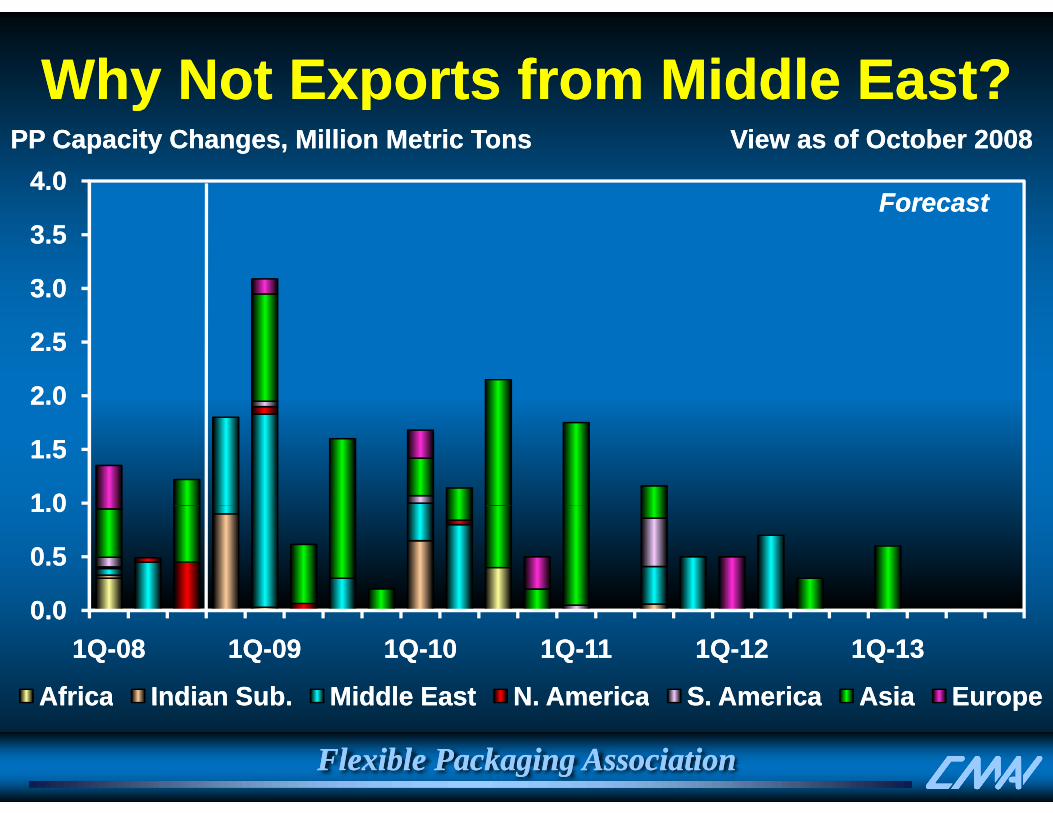

Why Not Exports from Middle East?Why Not Exports from Middle East?yy4.04.0

View as of October 2008View as of October 2008PP Capacity Changes, Million Metric TonsPP Capacity Changes, Million Metric Tons

ForecastForecast

3.03.0

3.53.5ForecastForecast

2.02.0

2.52.5

1 01 0

1.51.5

0 00 0

0.50.5

1.01.0

0.00.01Q1Q--0808 1Q1Q--0909 1Q1Q--1010 1Q1Q--1111 1Q1Q--1212 1Q1Q--1313

AfricaAfrica Indian Sub.Indian Sub. Middle EastMiddle East N. AmericaN. America S. AmericaS. America AsiaAsia EuropeEurope

Flexible Packaging AssociationFlexible Packaging Association

AfricaAfrica Indian Sub.Indian Sub. Middle EastMiddle East N. AmericaN. America S. AmericaS. America AsiaAsia EuropeEurope

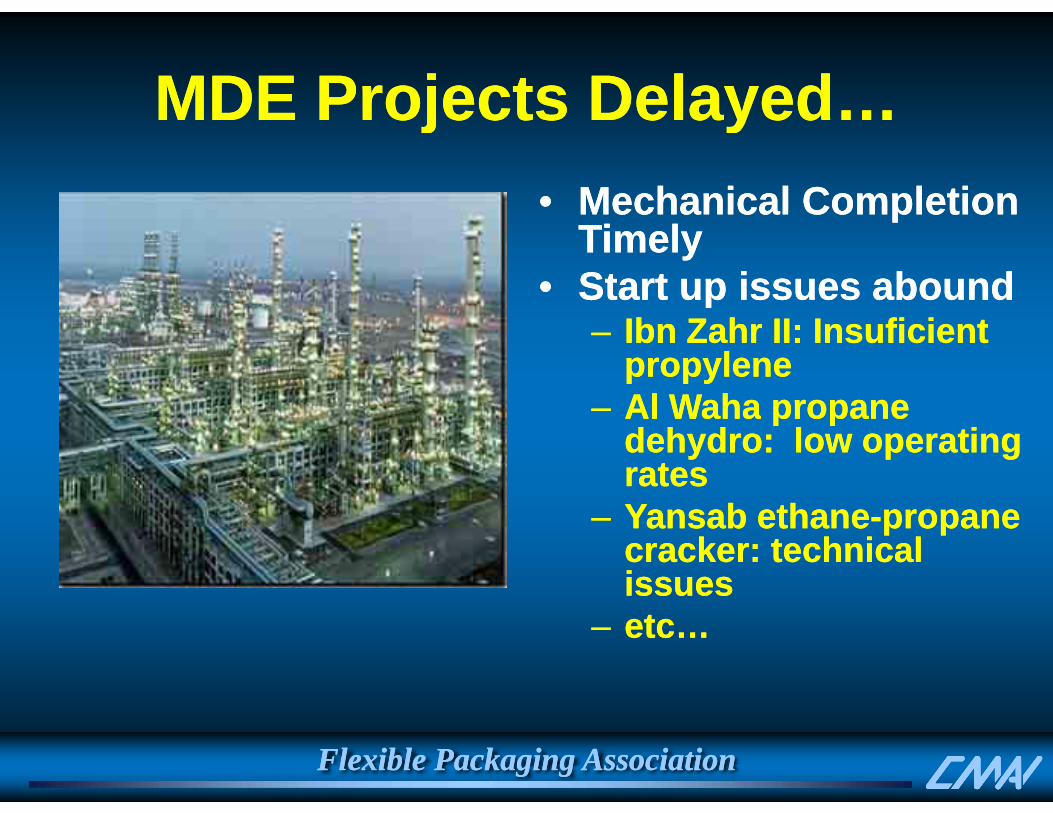

MDE Projects DelayedMDE Projects DelayedMDE Projects Delayed…MDE Projects Delayed…•• Mechanical CompletionMechanical CompletionMechanical Completion Mechanical Completion

TimelyTimely•• Start up issues aboundStart up issues abound

–– IbnIbn ZahrZahr II: II: InsuficientInsuficientpropylenepropyleneAlAl WahaWaha propanepropane–– Al Al WahaWaha propane propane dehydrodehydro: low operating : low operating ratesratesY bY b thth–– YansabYansab ethaneethane--propane propane cracker: technical cracker: technical issuesissues

–– etc…etc…

Flexible Packaging AssociationFlexible Packaging Association

Projects Very Delayed…Projects Very Delayed…

4.04.0PP Capacity Changes, MillionPP Capacity Changes, Million Metric Metric TonsTons View as of July 2009View as of July 2009

ForecastForecast

3.03.0

3.53.5

2.02.0

2.52.5

1 01 0

1.51.5

0 00 0

0.50.5

1.01.0

0.00.01Q1Q--20082008 1Q1Q--20092009 1Q1Q--20102010 1Q1Q--20112011 1Q1Q--20122012 1Q1Q--20132013

AfricaAfrica EuropeEurope Indian Sub.Indian Sub. Middle EastMiddle East N. AmericaN. America AsiaAsia S. AmericaS. America

Flexible Packaging AssociationFlexible Packaging Association

AfricaAfrica EuropeEurope Indian Sub.Indian Sub. Middle EastMiddle East N. AmericaN. America AsiaAsia S. AmericaS. America

Investment Investment ExcessExcess

Demand Demand DropDrop Oversupply!Oversupply!++ ==

1001001818PP, Million PP, Million Metric TonsMetric Tons Operating Rate, PercentOperating Rate, Percent

ExcessExcess DropDrop pp ypp y

9595

100100

1212141416161818

ForecastForecast

8585

9090

6688

10101212

8080224466

7070

7575

--44--2200

20042004 20062006 20082008 20102010 20122012 20142014

Capacity Increase Capacity Increase -- Demand IncreaseDemand Increase Cummulative Delta CapsCummulative Delta Caps--Delta DemDelta DemO ti R tO ti R t

Flexible Packaging AssociationFlexible Packaging AssociationOperating RateOperating Rate

Pricing and Margins to Slide•• Producers had Producers had

b bl t f llb bl t f llPrice, Cents Per PoundPrice, Cents Per Pound Margin, Cents Per PoundMargin, Cents Per Pound

99

1212

9090

120120 been able to follow been able to follow propylene price propylene price increases; tightincreases; tight

ForecastForecast

66

99

6060

9090 increases; tight increases; tight supply and exports supply and exports helpedhelped

33

66

3030

6060 •• As overAs over--supply supply ensues and ensues and exports declineexports decline

00

33

00

3030 exports decline, exports decline, will become difficult will become difficult to push cost to push cost

JanJan--0707 OctOct--0707 JulJul--0808 AprApr--0909 JanJan--1010 OctOct--1010 increasesincreasesCash Margin PP Discounted Price Cash Costs

Flexible Packaging AssociationFlexible Packaging Association

North America Moving to Top of PP North America Moving to Top of PP Price ChainPrice Chain

18001800Dollars Per Metric TonDollars Per Metric Ton

Price ChainPrice Chain

16001600

18001800ForecastForecast

12001200

14001400

10001000

12001200

600600

800800

JanJan--0909 MayMay--0909 SepSep--0909 JanJan--1010 MayMay--1010 SepSep--1010NAM PP Disc. PriceNAM PP Disc. Price WEP PP Disc. PriceWEP PP Disc. PriceNEA PP SpotNEA PP Spot NAM PP Spot ExportNAM PP Spot Export

Flexible Packaging AssociationFlexible Packaging Association

NEA PP Spot NEA PP Spot NAM PP Spot ExportNAM PP Spot Export

PolypropylenePolypropylene ConclusionsConclusionsPolypropylene Polypropylene -- ConclusionsConclusions•• PP price climb seems to be reaching a PP price climb seems to be reaching a p gp g

tipping point.tipping point.•• Overcapacity looming; effects areOvercapacity looming; effects are•• Overcapacity looming; effects are Overcapacity looming; effects are

different depending on the geographydifferent depending on the geographyD d d d t b i b lD d d d t b i b l•• Demand recovery needed to bring balance Demand recovery needed to bring balance to the marketto the market

•• Prices in North America to remain Prices in North America to remain elevated elevated

•• Polypropylene Polypropylene –– no longer cheap?no longer cheap?

Flexible Packaging AssociationFlexible Packaging Association