dri & mini-mills - amm

TRANSCRIPT

DRI &Mini-millsConferenceSeptember 10-11, 2013Royal Sonesta Hotel, New Orleans, LA

Home

World Production of DRI and HBI

World Production of Crude Steel

Steel Production by Type in the U.S.

Global Steel Production by Type

Shale Gas and DRI Production

The Rise of EAFs

DRI and Mini-mills Conference

Back Page

W: www.amm.com/events/minimills

T: +1 212 901 3828

Click here to view the brochure

World and US Productionof DRI and HBI

This white paper has been created in conjunction with and American Metal Market andMetal Bulletin Events’upcoming DRI and Mini-mills Conferencebeing held on September10-11, New Orleans, LA.

The data and trends examined in this paper, and many others, will be addressed byexpert speakers and panellists at the event.

DRI &Mini-millsConferenceSeptember 10-11, 2013Royal Sonesta Hotel, New Orleans, LA

NEXT

World Production of DRI and HBI (‘000 tonnes)90,000

80,000

70,000

60,000

50,000

40,000

30,000

20,000

10,000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

A burgeoning DRI market in North America has the potential to be an industry game changer, the shalegas revolution and the resultant affordable natural gas has put DRI production firmly back on the agenda.DRI offers unique opportunities for mini-mill steel makers to tap into the iron ore market and protect againstthe volatility of the steel scrap market.

DRI can open up new commercial avenues and streamline the steel making process both in terms ofefficiency and cost and finished product markets. This could be one of the most influential shifts in the steelindustry for decades and will have ramifications across the entire supply chain.

The below graphical representation outlines the continuing growth in DRI consumption worldwide, it is clearto see that DRI is growing in popularity and is being utilized by more and more steel makers each year.

Tota

l (Mt)

Year

Home

World Production of DRI and HBI

World Production of Crude Steel

Steel Production by Type in the U.S.

Global Steel Production by Type

Shale Gas and DRI Production

The Rise of EAFs

DRI and Mini-mills Conference

Back Page

W: www.amm.com/events/minimills

T: +1 212 901 3828

Click here to view the brochure

DRI &Mini-millsConferenceSeptember 10-11, 2013Royal Sonesta Hotel, New Orleans, LA

NEXT

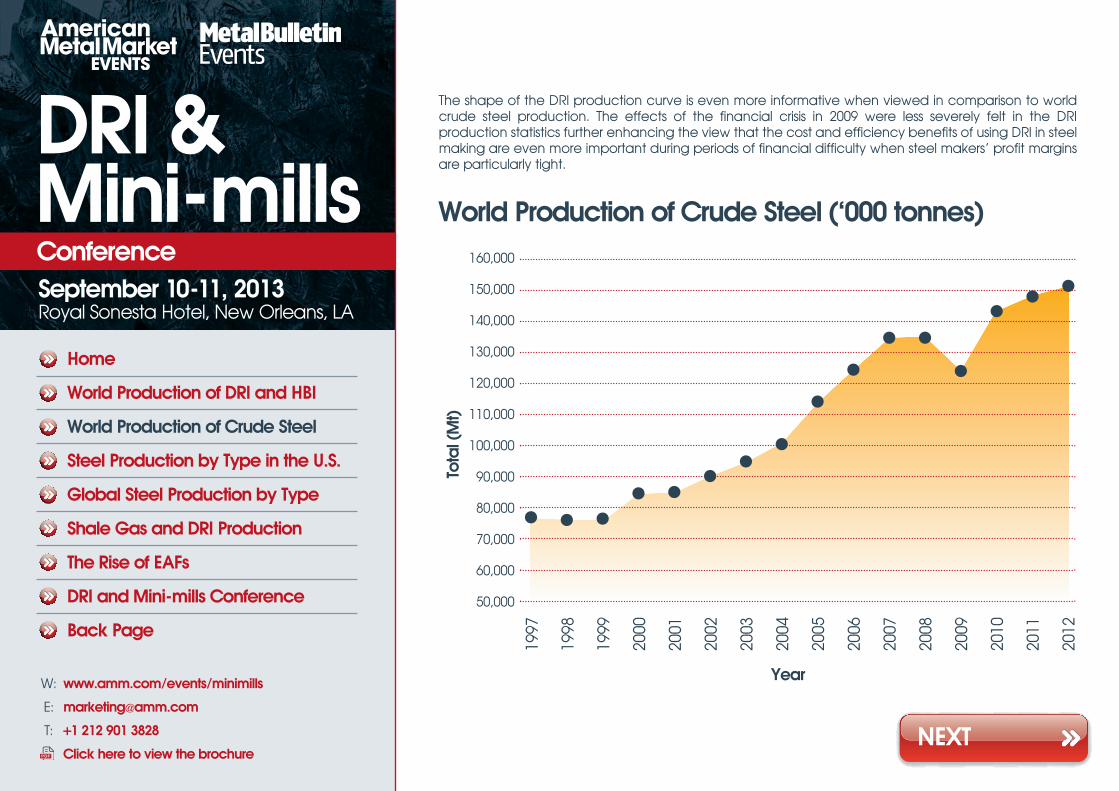

The shape of the DRI production curve is even more informative when viewed in comparison to worldcrude steel production. The effects of the financial crisis in 2009 were less severely felt in the DRIproduction statistics further enhancing the view that the cost and efficiency benefits of using DRI in steelmaking are even more important during periods of financial difficulty when steel makers’ profit marginsare particularly tight.

World Production of Crude Steel (‘000 tonnes)160,000

150,000

140,000

130,000

120,000

110,000

100,000

90,000

80,000

70,000

60,000

50,000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Total (Mt)

Year

1997

1998

1999

2000

Home

World Production of DRI and HBI

World Production of Crude Steel

Steel Production by Type in the U.S.

Global Steel Production by Type

Shale Gas and DRI Production

The Rise of EAFs

DRI and Mini-mills Conference

Back Page

W: www.amm.com/events/minimills

T: +1 212 901 3828

Click here to view the brochure

DRI &Mini-millsConferenceSeptember 10-11, 2013Royal Sonesta Hotel, New Orleans, LA

This figure graphically represents the crude steel production share of both primary BOF facilities andsecondary mini-mill based steel makers. The majority of steel is produced by mini-mills which indicates notonly the inherent environmental and feedstock advantages of EAFs but also represents the huge potentialmarket for DRI in the US. DRI will not necessarily increase the crude steel market share for mini-mills but it doesprovide mini-mill operators with the flexibility of feedstock and the opportunity to tap into the iron ore market.

Steel Production by Type in the U.S.

100,000

90,000

80,000

70,000

60,000

50,000

40,000

30,000

20,000

10,000

0

2007

2008

2009

2010

2011

2012

Tota

l (Mt)

Year

Crude Total (Mt) BOF Total (Mt) EAF Total (Mt)

NEXT

Home

World Production of DRI and HBI

World Production of Crude Steel

Steel Production by Type in the U.S.

Global Steel Production by Type

Shale Gas and DRI Production

The Rise of EAFs

DRI and Mini-mills Conference

Back Page

W: www.amm.com/events/minimills

T: +1 212 901 3828

Click here to view the brochure

DRI &Mini-millsConferenceSeptember 10-11, 2013Royal Sonesta Hotel, New Orleans, LA

Home

World Production of DRI and HBI

World Production of Crude Steel

Steel Production by Type in the U.S.

Global Steel Production by Type

Shale Gas and DRI Production

The Rise of EAFs

DRI and Mini-mills Conference

Back Page

W: www.amm.com/events/minimills

T: +1 212 901 3828

Click here to view the brochureNEXT

As the below graph contests EAF’s share of crude steel making has been on the rise in recent years and theforecast outlines how EAF steel making will overtake traditional BOF steelmaking routes by 2030. Globally thebalance between EAF and BOFs will become more similar to the current balance in the US (see next graph).The efficiency, feedstock flexibility and environmental advantages of EAFs make them a much moreattractive investment for future capacities, especially with new carbon emission laws and growing steelscrap reservoirs.

Global Steel Production by Type

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0

2000

2005

2010

2015

2020

2025

2030

Year

Crude Steel Production by Blast Furnace Crude Steel Production by Electric Arc Furnace

697Mt

814Mt1167Mt

1229Mt1278Mt

1248Mt1282Mt

163Mt286Mt

348Mt

606Mt852Mt

1152Mt1388Mt

DRI &Mini-millsConferenceSeptember 10-11, 2013Royal Sonesta Hotel, New Orleans, LA

Home

World Production of DRI and HBI

World Production of Crude Steel

Steel Production by Type in the U.S.

Global Steel Production by Type

Shale Gas and DRI Production

The Rise of EAFs

DRI and Mini-mills Conference

Back Page

W: www.amm.com/events/minimills

T: +1 212 901 3828

Click here to view the brochureNEXT

The shale gas revolution is the undoubted catalyst for US DRI production. The below figure outlines how DRIcapacities are likely to grow exponentially with reliably low natural gas prices, whilst natural gas prices staycompetitive DRI based steel production is likely to remain an attractive, cost effective option

Shale Gas and DRI Production

6.0

5.0

4.0

3.0

2.0

1.0

0.0

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

US Produc

tion of DRI (Mt)

Year

12

10

8

6

4

2

0

Gas Price (US$/m

mBtu

DRI production, Mt (LHS) Gas Prices, US$/mmBtu

Source: WSA, Wood Mackenzie Steel Market and Global Gas Service

DRI &Mini-millsConferenceSeptember 10-11, 2013Royal Sonesta Hotel, New Orleans, LA

Home

World Production of DRI and HBI

World Production of Crude Steel

Steel Production by Type in the U.S.

Global Steel Production by Type

Shale Gas and DRI Production

The Rise of EAFs

DRI and Mini-mills Conference

Back Page

W: www.amm.com/events/minimills

T: +1 212 901 3828

Click here to view the brochureNEXT

The rise of EAF based steel making both in the US and globally is being driven by a combination of factors:

l Environmental – EAF based steel making generates significantly less carbonemissions than the traditional BOF route, both in actual production process andbecause they predominantly utilize and recycle ferrous scrap. As more carbonemission taxes and restrictions are being enforced by governments across theglobe, this factor will only grow in importance.

l Flexibility – The volatility of raw material prices and slackening of global steeldemand makes the flexibility of EAFs even more important. EAFs are considerablymore flexible than primary steel maker and can economically and efficientlyreduce their output and capacity according to market pressures.

l Feedstock – The traditional BF and BOF route are reliant on coking coal supplieswhich are beginning to tighten. EAFs do not have any coal requirements and aretherefore unaffected from the dwindling coking coal availability.

The Rise of EAFs

DRI &Mini-millsConferenceSeptember 10-11, 2013Royal Sonesta Hotel, New Orleans, LA

This white paper has been created in conjunction with and American Metal Market and Metal BulletinEvents’ upcoming DRI and Mini-mills Conference being held on September 10-11, New Orleans, LA. Withover 120 delegates expected, this is an ideal opportunity to meet your customers and suppliers in theburgeoning market as well as hearing from the senior level decision makers at market leading companiesdiscuss the following:

l The growing role of DRI in the North American steel industryl Shale gas availability and its ramifications for manufacturing and steel makingl The applications and advantages of DRI in mini-mill operationslA detailed evaluation and comparison of the available DRI technologieslAn overview of potential DRI projects in the regionlDRI/HBI as a merchant productlDRI logistics – the safe handling and shipping of DRIlA comparison of ore based metallics and their useslComprehensive analysis of DR grade iron ore pellet availabilityl EAF technologies – how they are maximizing efficiencyl Burdening optimization and procurement strategies for mini-millslVertical integration and mitigating volatility through raw material control

Unless specified, all data is sourced from Metal Bulletin Research and presentations delivered at Metal Bulletin Events

NEXT

Home

World Production of DRI and HBI

World Production of Crude Steel

Steel Production by Type in the U.S.

Global Steel Production by Type

Shale Gas and DRI Production

The Rise of EAFs

DRI and Mini-mills Conference

Back Page

W: www.amm.com/events/minimills

T: +1 212 901 3828

Click here to view the brochure

DRI and Mini-mills Conference

Research Partner:Signature Sponsor: Gold Sponsor: Silver Sponsors:

TM

TM

DRI &Mini-millsConferenceSeptember 10-11, 2013Royal Sonesta Hotel, New Orleans, LA

Home

World Production of DRI and HBI

World Production of Crude Steel

Steel Production by Type in the U.S.

Global Steel Production by Type

Shale Gas and DRI Production

The Rise of EAFs

DRI and Mini-mills Conference

Back Page

W: www.amm.com/events/minimills

T: +1 212 901 3828

Click here to view the brochure

FIVE EASY WAYS TO ORDER+44 (0) 20 7779 8000 +44 (0) 20 7779 8090 [email protected]

www.metalbulletinstore.com Metal Bulletin Research, Nestor House, Playhouse Yard, London, EC4V 5EX UK

You are also able to request a brochure, sample extracts and detailed table of contents for more information Quote promo code 5356 when ordering

A Ten Year Strategic Outlook for the

Global Iron Ore Industry

New andUpdated

Part 1: A Ten Year Strategic Outlook for the Global Iron Ore Industry

Part 2: Dynamic Demand, Supply and Price Model for the Global Iron Ore Industry