energy technology perspectives 2015 - unece · energy technology perspectives 2015: mobilising...

TRANSCRIPT

© OECD/IEA 2015

Energy Technology Perspectives 2015: Mobilising Innovation to Accelerate Climate Action

David Elzinga, Economic Affairs Officer (Former Senior Energy Analyst and lead author of ETP)

Geneva

May 27, 2015

© OECD/IEA 2014

Energy Innovation is crucial in making the 2DS possible

Energy innovation has already started delivering, but more is needed

Contribution of technology area to global cumulative CO2 reductions

6DS

2DS

© OECD/IEA 2014

Global ESCII trends

Ambitious efforts are needed to reduce the carbon intensity of the global energy sector

© OECD/IEA 2014

What does this mean for economies?

Decouple economic growth and primary energy use AND reduce CO2 intensity of primary energy

2DS energy system development

© OECD/IEA 2014

Clean energy deployment is not ramping up fast enough

Evidence shows that despite continued progress in many areas, for the first time none of the technologies are in line with 2DS goals

© OECD/IEA 2014

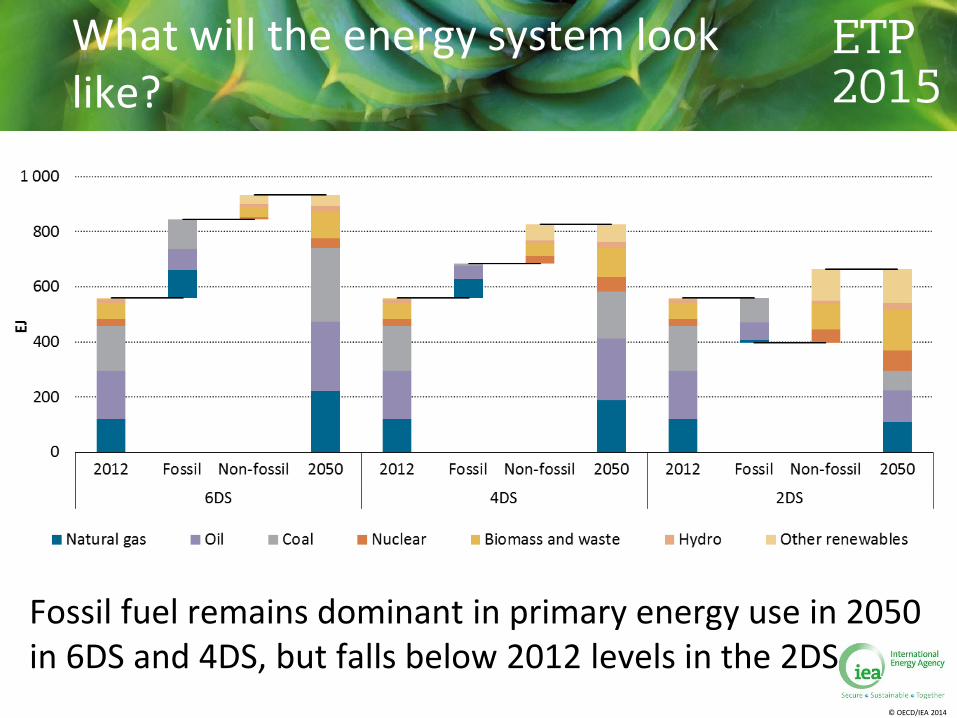

What will the energy system look like?

Fossil fuel remains dominant in primary energy use in 2050 in 6DS and 4DS, but falls below 2012 levels in the 2DS

© OECD/IEA 2014

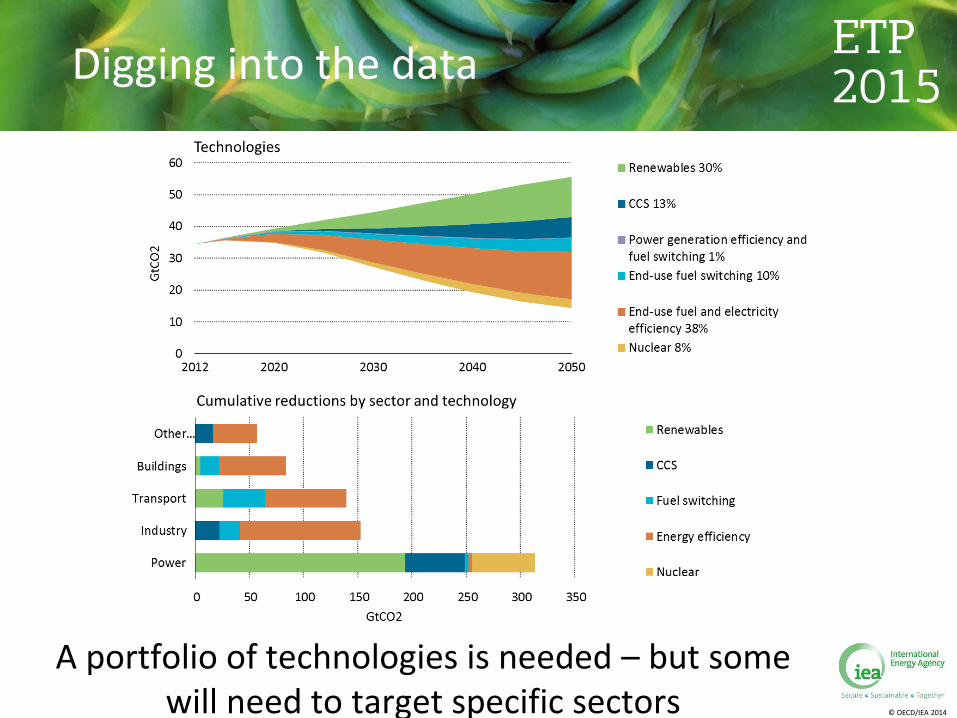

Digging into the data

A portfolio of technologies is needed – but some will need to target specific sectors

© OECD/IEA 2014

Having the right information can help stimulate support

Emerging economies is where the bulk of emission will need to come from

© OECD/IEA 2014

There is no “one-size fits all” solution that can meet all local requirements

National circumstances and resources will drive different technology portfolios and pathways

Regional technology shares in primary energy supply

© OECD/IEA 2014

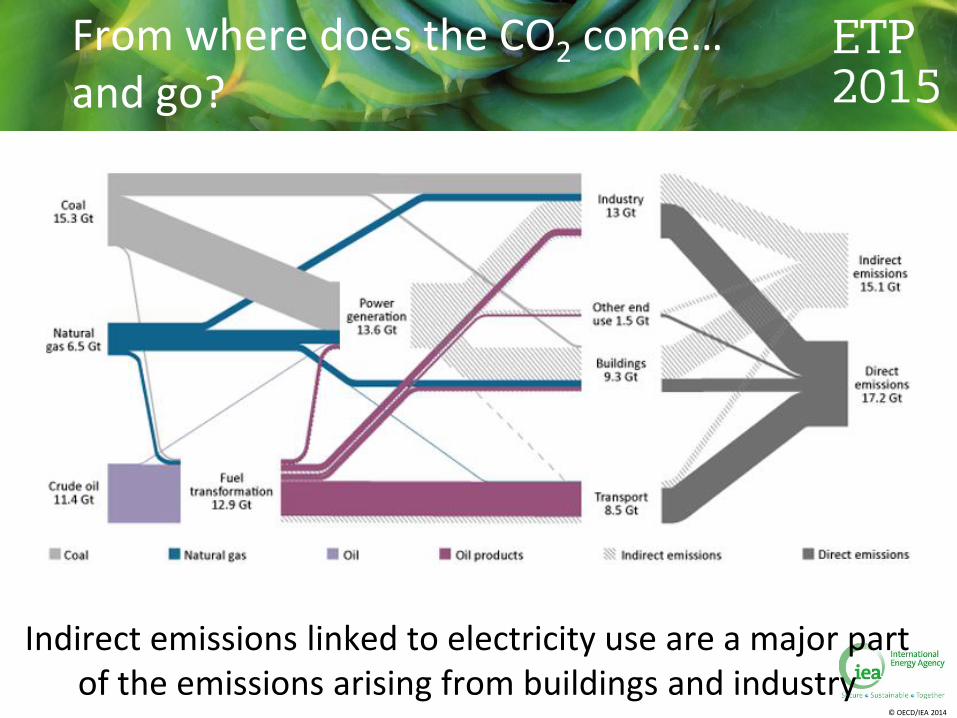

From where does the CO2 come… and go?

Indirect emissions linked to electricity use are a major part of the emissions arising from buildings and industry

© OECD/IEA 2014

Global electricity generation mix – a share reversal

Today fossil fuels dominate electricity generation with a 68% share of the generation mix; by 2050 in the 2DS,

renewables reach an almost similar share of 63%.

© OECD/IEA 2014

Decarbonising the electricity system

New build generation capacity needs to decarbonise very quickly to meet long term goals

Electricity Sector Carbon Intensity

© OECD/IEA 2014

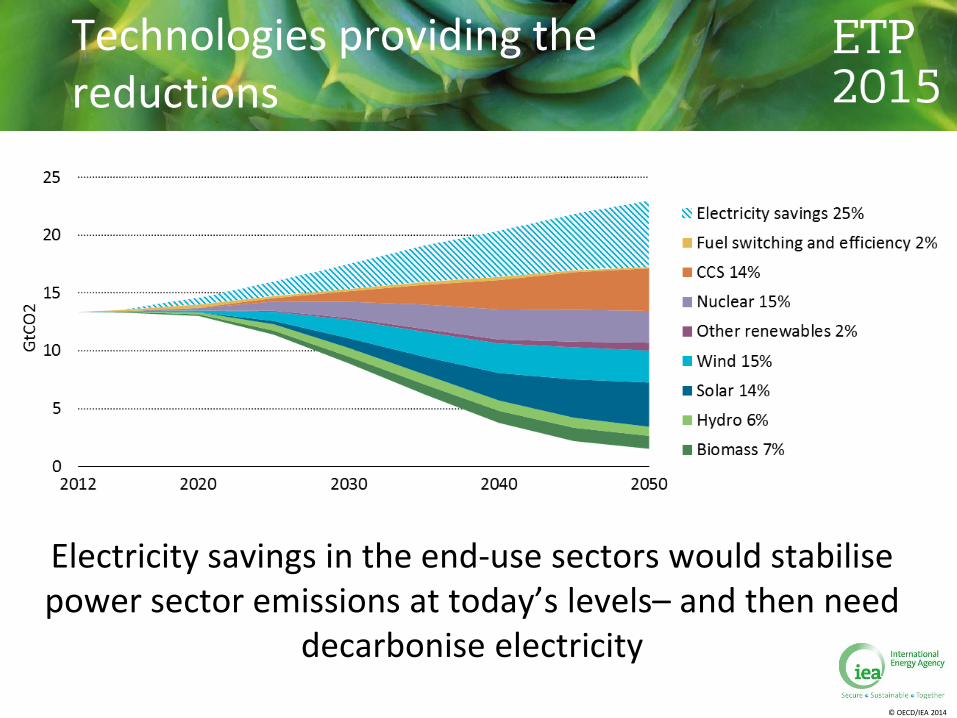

Technologies providing the reductions

Electricity savings in the end-use sectors would stabilise power sector emissions at today’s levels– and then need

decarbonise electricity

© OECD/IEA 2014

Again….regional differences

Electricity generation mixes all evolve to 2050

© OECD/IEA 2014

Heating and Cooling should not be overlooked.

Heating and cooling in industry and buildings accounts for more than 40% of final energy consumption and 30% of

global CO2 emissions.

© OECD/IEA 2014

Emissions from heating and cooling can be reduced

In the 6DS, direct and indirect CO2 emissions from heating and cooling continue to grow over time; in the 2DS they

peak by 2015 and then decline

6DS 2DS

© OECD/IEA 2014

Better understanding innovation can increase confidence in its outcomes

In order to accelerate technological progress in low-carbon technologies, innovation policies should be

systemic

© OECD/IEA 2014

Energy RD&D funding now targets the right issues, but is not enough

Energy RD&D spending should reflect the importance of energy technology in meeting climate objectives

IEA government Energy RD&D expenditure

© OECD/IEA 2014

China is taking action to reap the benefits of a strong innovation system

China is poised to become the global leader in R&D spending by 2019.

China’s total R&D spending and OECD projections

© OECD/IEA 2014

Technology innovation is making renewable energy markets viable

Thanks to 40 years of innovation efforts, solar PV generation is an increasingly cost competitive option

Cost of electricity generated and PV capacity installations in Germany

© OECD/IEA 2014

Energy efficient technologies are also constantly improving

Fuel economy is improving as policy increasingly drives the deployment of more efficient vehicle technologies

Average new Light-duty vehicle fuel economy evolution by country, 2005 to 2013

© OECD/IEA 2014

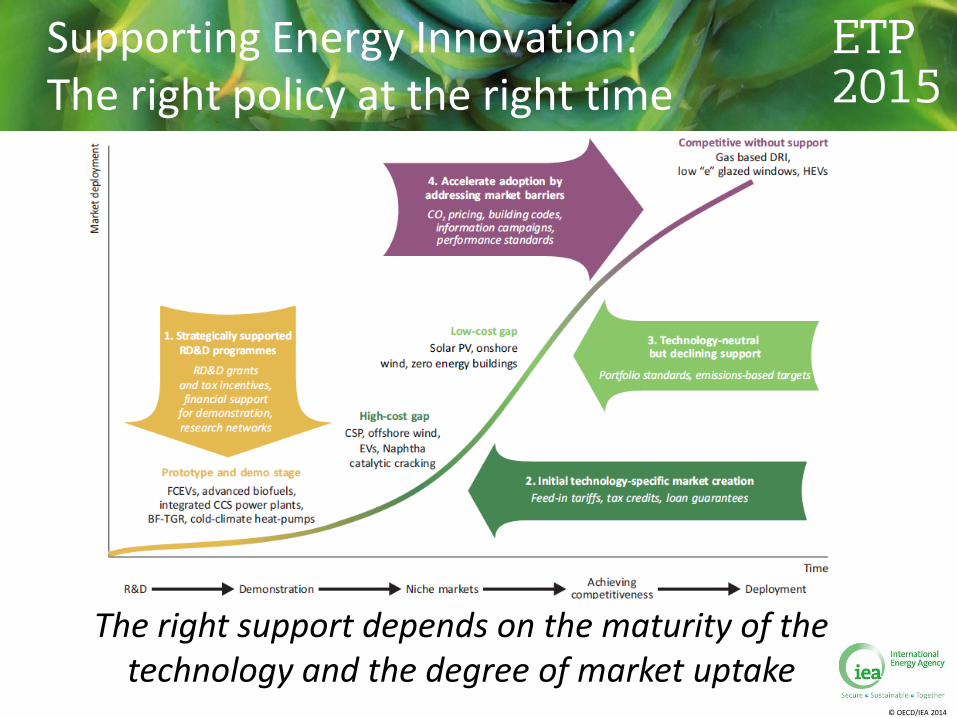

Supporting Energy Innovation: The right policy at the right time

The right support depends on the maturity of the technology and the degree of market uptake

© OECD/IEA 2014

Later stage innovation support must focus on market uptake barriers

Wind and solar PV support needs to move from strictly incentives to integrated and well-designed market,

policy and regulatory frameworks

Projections of wind and solar PV generation

© OECD/IEA 2014

Energy technologies needed to meet long-term goals also show progress

Ratcheting up of investments in CCS demonstrations is yielding progress – but more is needed

CCS Investments

© OECD/IEA 2014

Early stage support is key to improve future technology competitiveness

Aggressive cost reductions are needed in the near term to make these projections a reality

Projected Levelised Cost of Electricity of coal power generation in the USA

© OECD/IEA 2014

Innovation is essential for sustainable growth in the industrial sector

The deployment of innovative technologies is crucial to making a 2DS scenario possible

Annual energy-related CO2 Emissions in the industrial sector in the 2DS

6DS

2DS

© OECD/IEA 2014

Building innovation capacity is key to successful technology deployment

Cooperation between industrial and emerging economies could be a win-win solution

© OECD/IEA 2014

Thank you