esnd presentation 12112015

TRANSCRIPT

Investor PresentationDecember 2015

This presentation contains forward-looking statements, including references to goals, plans, strategies, objectives, projected costs or savings,anticipated future performance, results or events and other statements that are not strictly historical in nature. These statements are based onmanagement’s current expectations, forecasts and assumptions. This means they involve a number of risks and uncertainties that could causeactual results to differ materially from those expressed or implied here. These risks and uncertainties include, but are not limited to the following:end-user demand for products in the office, technology, and furniture product categories may continue to decline; Essendant's reliance on keycustomers, and the risks inherent in continuing or increased customer concentration and consolidations; prevailing economic conditions andchanges affecting the business products industry and the general economy; Essendant's ability to effectively manage its operations and toimplement growth, cost-reduction and margin-enhancement initiatives; the impact of Essendant's repositioning, restructuring and rebrandingactivities on Essendant's customers, suppliers, and operations; Essendant's reliance on supplier allowances and promotional incentives;Essendant's reliance on independent resellers for a significant percentage of its net sales and, therefore, the importance of the continuedindependence, viability and success of these resellers; continuing or increasing competitive activity and pricing pressures within existing orexpanded product categories, including competition from product manufacturers who sell directly to Essendant's customers; the impact of supplychain disruptions or changes in key suppliers’ distribution strategies; Essendant's ability to maintain its existing information technology systems andthe systems and e-commerce services that it provides to customers, and to successfully procure, develop and implement new systems and serviceswithout business disruption or other unanticipated difficulties or costs; the creditworthiness of Essendant's customers; Essendant's ability to manageinventory in order to maximize sales and supplier allowances while minimizing excess and obsolete inventory; Essendant's success in effectivelyidentifying, consummating and integrating acquisitions; the risks and expense associated with Essendant's obligations to maintain the security ofprivate information provided by Essendant's customers; the costs and risks related to compliance with laws, regulations and industry standardsaffecting Essendant's business; the availability of financing sources to meet Essendant's business needs; Essendant's reliance on key managementpersonnel, both in day-to-day operations and in execution of new business initiatives; and the effects of hurricanes, acts of terrorism and othernatural or man-made disruptions.

Shareholders, potential investors and other readers are urged to consider these risks and uncertainties in evaluating forward-looking statements andare cautioned not to place undue reliance on the forward-looking statements. For additional information about risks and uncertainties that couldmaterially affect Essendant's results, please see the company’s Securities and Exchange Commission filings. The forward-looking information inthis presentation is made as of this date only, and the company does not undertake to update any forward-looking statement. Investors are advisedto consult any further disclosure by United regarding the matters discussed in this presentation in its filings with the Securities and ExchangeCommission and in other written statements it makes from time to time. It is not possible to anticipate or foresee all risks and uncertainties, andinvestors should not consider any list of risks and uncertainties to be exhaustive or complete.

2

Safe Harbor Statement

3

Our Goal

To be the fastest, most convenient solution for workplace essentials

On June 1, 2015 we combined our family of brands to become

ESSENDANT (NASDAQ: ESND)

ORS Industrial

MEDCO Automotive

4

JanSan & Breakroom FY14 Revenue: $1.4B % of Total Sales: ~27% #SKUs: ~25,000

FY14 Revenue: $36M % of Total Sales: ~1%

Office Products

FY14 Revenue: $3.1B % of Total Sales: ~58% #SKUs: ~37,000

FY14 Revenue: $603M % of Total Sales: ~11% #SKUs: ~100,000

(includes Automotive)

Source: Company Filings, 2014 10-K

Essendant at a Glance

Growth category poised to accelerate

with additions of MEDCO (Nov. ‘14) and

Nestor (Aug. ‘15)

160,000 ITEMS

5

30,000RESELLERS

1600+ Manufacturers

Independent Resellers eTailers National

Accounts

Millions of Customers

Drive Profit by Enabling a Full Range of Resellers

Nationwide same / next-day

fulfillment platform

6

Unique Strengths in Network Scale and Distribution Expertise

Ship most products overnight to more than 90% of the U.S.

97% line fill rate 99.7% order accuracy rate 79 distribution centers and 475

trucks “Wrap and label” programs Drop ship directly to end customer:

single order up to full truckload

Categoryand channel

expertise

Comprehensive reference guides & catalogs

Promotional materials Primary research efforts Brand strategy and development Campaign development Customer segmentation Cost management Training programs

Enhanced digital

services

Item content: photos, dimensions and descriptions

Analytics and digital promotional campaigns

Website development Digitalized database for

e-commerce

• Product delivery with high order accuracy/rapid fulfillment, and provide geographic reach

• Promotional materials, brand and campaign development, website development and analytics, customer segmentation

• Cost management & training programs to improve efficiency

Customer Offering Tailored to Channel

Independent Resellers –79% of sales

• Drop ship to end customer or direct into stock of online seller

• Item content: photos, dimensions and descriptions

• Growth channel—sales grew over 14% YOY in Q3 2015

eTailers –11% of sales

• Provide long-tail of inventory: items that are OOS or retailer chooses not to stock

• Capabilities include bulk ship to warehouse, “wrap and label” for seller to combine with other parts of order, or drop-ship to end consumer

• Highly integrated operating model

• Opportunity to grow channel regardless of merger outcome

National Accounts –10% of sales

7

• Next day delivery to over 90% of the U.S.

• 79 distribution centers and 450+ trucks

• Extend the supply chain and inventory of national account & online resellers

• Existing capacity sufficient to support growth

8

Nationwide Distribution

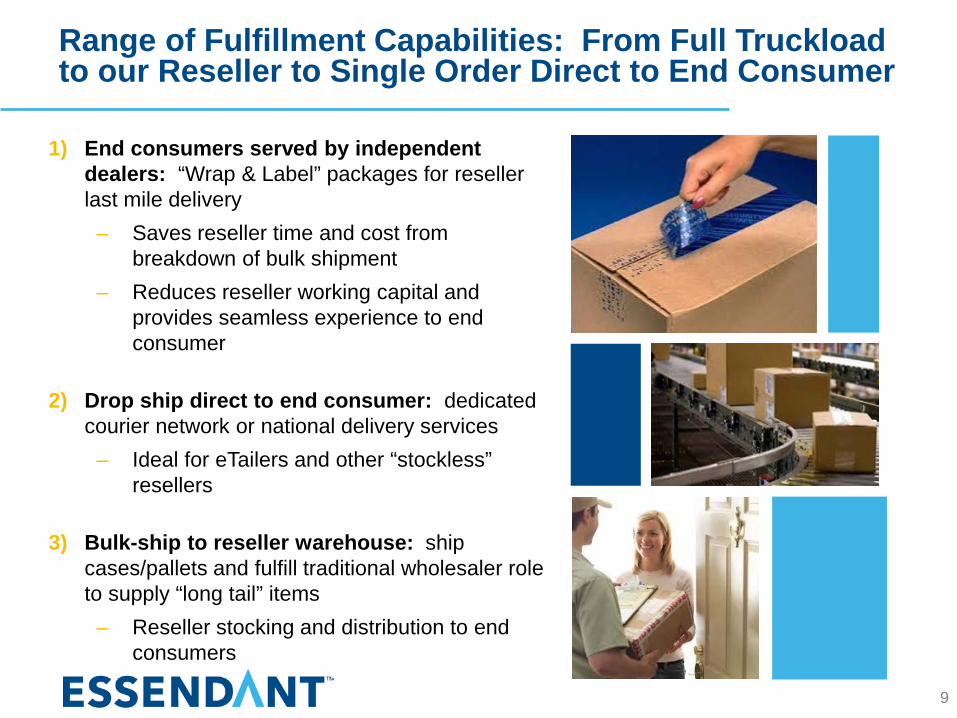

1) End consumers served by independent dealers: “Wrap & Label” packages for reseller last mile delivery

– Saves reseller time and cost from breakdown of bulk shipment

– Reduces reseller working capital and provides seamless experience to end consumer

2) Drop ship direct to end consumer: dedicated courier network or national delivery services

– Ideal for eTailers and other “stockless” resellers

3) Bulk-ship to reseller warehouse: ship cases/pallets and fulfill traditional wholesaler role to supply “long tail” items

– Reseller stocking and distribution to end consumers

9

Range of Fulfillment Capabilities: From Full Truckload to our Reseller to Single Order Direct to End Consumer

Strategic Pillars

Grow Share in Core Office

Products and JanSan

Businesses

Win the Shift to Online

Diversifyinto Channels

and Categories that Leverage our Common

Platform

Refined Strategy Leverages Competitive Strengths

Accelerate organic sales growth in core by using scale and distribution capability to grow share, control cost and expand earnings dollars

Focus M&A on opportunities that leverage common platform---not only IT system but distribution, data infrastructure, digital expertise and

functional capabilities in merchandising, sales and operations

Two key refinements

1

2

10

Key Objectives Over Next Two Years

1) Generate profitable sales growth– Aligning with customers who are taking share in each channel we

serve

2) Move all businesses onto common platform– Beginning with Office Products, JanSan and Breakroom– CPO and Automotive to follow

3) Simplify business and continue to lower costs– Gain operating leverage and reduce overhead by fully integrating

recently acquired businesses

4) Pursue merchandising excellence – Optimize assortment and create additional value for business and

customers

5) Refine industrial channel value proposition– Re-orient towards industrial and retail, de-emphasize energy

11

12

Generating Sales Growth in Challenging Markets

Current Market• Office Products in

structural decline

• Industrial in cyclical downturn

• Headwind in energy markets

Take share by aligning with resellers who are growing, and buying smaller players

Bring businesses onto common platform—cross-sell and expand our offering

Continue to deliver on what customers value: consistency of platform, cross-country coverage, and digital/merchandising capabilities

Capabilities & Plan

Targeting low to mid-single digit sales growth in 2016

• Acquired MEDCO, an automotive aftermarket wholesaler of tools, equipment, and paint & body supplies

• Acquired Nestor Sales, a wholesaler and distributor of tools, equip. and supplies to fleet, marine and automotive markets

• Acquired CPO Commerce, an e-retailer of power tools and equipment

• Acquired O.K.I. Supply, a welding, safety and industrial wholesaler

• Acquired ORS Nasco, an industrial wholesaler and entered industrial category

13

Nestor Sales LLC acquired in 2Q 2015 to complement existing industrial and automotive aftermarket offerings

Acquisitions leverage our existing network and distribution capabilities particularly as we move businesses onto common operating and IT platform

2007 2012 2014 2015

Total Revenue $820M+

M&A Growth Opportunities

14

Financial PerformanceSales($B)

4.75.04.64.54.33.85.35.15.15.04.8

200920082007200620052004 2013 2014

+3%

2010 20122011

Adjusted Operating Income(1)

($M)

207221209195198177189204184171162

20072006 2008 2010200920052004 201420132011 2012

+2%

Return on Invested Capital(%)

-3%

2013

9.6%

20142012

10.9%10.9%10.8%

2010

11.4%

2011

Adjusted EPS – Diluted(1)

($/share)

$3.08 $3.26

$2.85 $2.39 $2.19 $1.96

$2.00 $1.94 $1.53

$1.45 $1.32

2014

+9%

20122011 20132008 2009 20102004 200720062005

1) For a definition and reconciliation of Adjusted Operating Income and Adjusted EPS, please see appendix.

15

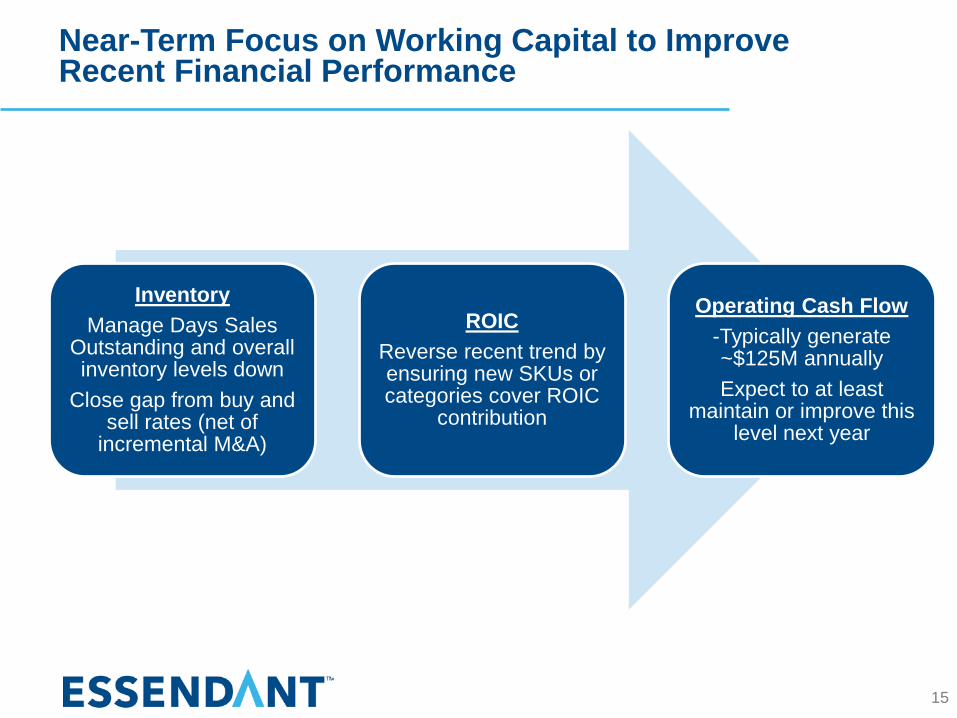

Near-Term Focus on Working Capital to Improve Recent Financial Performance

InventoryManage Days Sales

Outstanding and overall inventory levels down

Close gap from buy and sell rates (net of

incremental M&A)

ROICReverse recent trend by ensuring new SKUs or categories cover ROIC

contribution

Operating Cash Flow-Typically generate ~$125M annuallyExpect to at least

maintain or improve this level next year

16

Capital Allocation 2009-2014($M)

162

252

83

458

Cash M&A

Share Repurchase

Dividends

Capex

$955

Operating Cash Flow

$849

Note: Dividend initiated in Q1 2011; current dividend pays $0.14/share per quarter

Strong Cash Flow with Effective Capital Deployment

Leadership position in core categories with extensive nationwide distribution

Attractive organic and M&Agrowth opportunities

Highly scalable business model

Generating strong free cash flow and returning cash to investors

17

Summary

Appendix

Non-GAAP Reconciliations

17

Adjusted Operating Income, Net Income and Earnings Per Share

2006 2009 2010 2013 2014Net Sales 3,838,701$ 4,279,089$ 4,546,914$ 4,646,399$ 4,986,879$ 4,710,291$ 4,832,237$ 5,005,501$ 5,080,106$ 5,085,293$ 5,327,205$ Gross profit 584,532$ 642,024$ 754,081$ 706,715$ 740,679$ 690,641$ 730,555$ 732,889$ 776,328$ 787,340$ 802,529$ Operating expenses 422,595$ 469,862$ 518,175$ 504,188$ 548,249$ 503,013$ 520,754$ 543,168$ 573,645$ 580,141$ 603,907$

Workforce reduction and facility closure charge - 1,331 (1,941) - - - - - (6,247) (12,975) - Asset impairment charge - - - - (6,700) - - (1,635) - (1,183) - Vacation pay policy change - - - - - - 11,871 - - - - Early retirement/workforce realignment - - - - - - (9,116) 723 - - - Equity compensation charge - - - - - - - (4,409) - - - Retiree medical plan termination - - - - - - 8,856 - - - - Negotiated settlement with a service supplier - - - - - 14,000 - - - - - Severance charge - - - - - (3,400) - - - - - Gain on the sale of distribution centers - - - - 5,100 - - - - - - Gain on sale of former corporate headquarters - - - - 4,700 - - - - - - Restructuring charge - - - (1,378) - - - - - - - Product content syndication and marketing program changes

- - 60,600 - - - - - - - -

Loss on disposition of business - - - - - - - - - - (8,234) Adjusted operating expenses 422,595$ 471,193$ 576,834$ 502,810$ 551,349$ 513,613$ 532,365$ 537,847$ 567,398$ 565,983$ 595,673$ Operating income 161,937$ 172,162$ 235,906$ 202,526$ 192,430$ 187,628$ 209,801$ 189,722$ 202,683$ 207,200$ 198,622$

Operating expense item noted above - (1,331) (58,659) 1,378 (3,100) (10,600) (11,611) 5,321 6,247 14,158 8,234 Adjusted operating income 161,937$ 170,831$ 177,247$ 203,904$ 189,330$ 177,028$ 198,190$ 195,043$ 208,930$ 221,358$ 206,856$ Net income 89,971$ 97,501$ 132,213$ 107,195$ 98,413$ 100,984$ 112,757$ 103,696$ 112,881$ 122,053$ 112,117$

Operating expense item noted above, net of tax - - (36,454) 1,378 (3,100) (6,700) (7,158) 3,920 3,873 9,227 8,234 Adjusted net income 89,971$ 97,501$ 95,759$ 108,573$ 95,313$ 94,284$ 105,599$ 107,616$ 116,754$ 131,280$ 120,351$ Diluted earnings per share 1.32$ 1.45$ 2.11$ 1.92$ 2.06$ 2.10$ 2.34$ 2.30$ 2.75$ 3.03$ 2.87$

Per share operating expense item noted above - - (0.58) 0.02 (0.06) (0.14) (0.15) 0.09 0.09 0.23 0.21 Adjusted diluted earnings per share 1.32$ 1.45$ 1.53$ 1.94$ 2.00$ 1.96$ 2.19$ 2.39$ 2.85$ 3.26$ 3.08$

Weighted average number of common shares - diluted 67,970 67,224 62,742 55,952 47,694 48,192 48,286 45,014 40,991 40,236 39,130

For the Years Ended December 31,2004 2005 2007 2008 2011 2012