evaluating and executing changes to spending policy (2.3.15)

TRANSCRIPT

2 0 1 4 F E G I N V E S T M E N T F O R U M

Producing Results in anUnpredictable World

GAME ON :

Rip Mecherle, CFAUniversity of TennesseeExecutive Director of Investments

NACUBO: 2015 ENDOWMENT AND DEBT MANAGEMENT FORUM

Nolan M. Bean, CFA, CAIA Fund Evaluation Group, LLCManaging Principal

EVALUATING AND EXECUTING CHANGES TO SPENDING POLICY

©2015 Fund Evaluation Group, LLC. Confidential. Not for Redistribution.2NACUBO: 2015 Endowment and Debt Management Forum

AGENDA

I. Impact of Spending Policy

II. Selecting the Right Spending Policy Methodology

III. Case Study: University of Tennessee

IV. Considerations for a Low‐Return Environment

V. Conclusion

©2015 Fund Evaluation Group, LLC. Confidential. Not for Redistribution.3NACUBO: 2015 Endowment and Debt Management Forum

Impact of Spending Policy

©2015 Fund Evaluation Group, LLC. Confidential. Not for Redistribution.4NACUBO: 2015 Endowment and Debt Management Forum

ENTERPRISE MANAGEMENT

Spending Policy

Endowment Support of Budgets

(i.e., Univ., Fdn.)

Endowment Management

Foundation & Development

Support

Governance/ Structure

SPENDING POLICY CONSIDERATIONS

©2015 Fund Evaluation Group, LLC. Confidential. Not for Redistribution.5NACUBO: 2015 Endowment and Debt Management Forum

• Long‐Term Return > Target Spending Rate + Administrative Costs + Inflation

CONSIDERATIONS:

• Spending needs should not unduly influence asset allocation decisions

• Higher spending needs could lead to overly aggressive asset allocation

• Lower spending needs could lead to overly conservative asset allocation

SPENDING IS ONLY PART OF THE EQUATION

4.5% + 1.0% + 2.5% = 8.0%Spending Fees Inflation Primary Objective

©2015 Fund Evaluation Group, LLC. Confidential. Not for Redistribution.6NACUBO: 2015 Endowment and Debt Management Forum

SPENDING AND ASSET ALLOCATION POLICY SHOULD ALIGN

RETURNS VS. OBJECTIVE60/40 Equity/Bond Portfolio, 10‐Year Rolling Return

Data Sources: Ibbotson Associates and Barclays Capital; Data as of 12/31/2013.

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

1935 1948 1961 1974 1987 2000 2013

Return

Rolling 10‐year Return8% Return Objective

60/40 achieved an 8% return

~50% of the time

©2015 Fund Evaluation Group, LLC. Confidential. Not for Redistribution.7NACUBO: 2015 Endowment and Debt Management Forum

Selecting the Right Spending Policy Methodology

©2015 Fund Evaluation Group, LLC. Confidential. Not for Redistribution.8NACUBO: 2015 Endowment and Debt Management Forum

SPENDING POLICY METHODOLOGIES

MOVING AVERAGE Spend a fixed percentage of the average market value over a set time period

CONSTANT GROWTH Increase spending each year by a constant growth rate or inflation

CONSTANT GROWTH W/BANDS

Spending is contained within a range +/‐ a percentage of previous year’s market value

GEOMETRIC Weight given to inflation adjusted spending and target spending of market value

HYBRID Custom combination of spending rules to meet the specific needs of an institution

©2015 Fund Evaluation Group, LLC. Confidential. Not for Redistribution.9NACUBO: 2015 Endowment and Debt Management Forum

SPENDING POLICY METHODOLOGIES

MOVING AVERAGE5% spending rate using a 3‐year moving average

5% x (1/3) [ Ending market valuet‐1 + Ending market valuet‐2 + Ending market valuet‐3 ] = Spendingt

ADVANTAGES DISADVANTAGES

Smooths spending more than if ending market value used

x All market values all given same level of significance

Simple to implement and explain

x Spending is highly correlated to market value fluctuations

t: time.

©2015 Fund Evaluation Group, LLC. Confidential. Not for Redistribution.10NACUBO: 2015 Endowment and Debt Management Forum

4.7

4.8

4.8

4.9

4.9

5.0

SPENDING METHODOLOGY COMPARISON

YoY CHANGE IN SPEND ($)1992‐2013, Standard Deviations

Data Source: Lipper; Data as of 12/31/2013. YoY: Year‐over‐Year; MA: Moving Average.

AVERAGE SPEND (%)1992‐2013

3 Yr. 5 Yr. 7 Yr.MA MA MA

0

1

2

3

4

5

6

7

3 Yr. 5 Yr. 7 Yr.MA MA MA

©2015 Fund Evaluation Group, LLC. Confidential. Not for Redistribution.11NACUBO: 2015 Endowment and Debt Management Forum

SPENDING POLICY METHODOLOGIES

CONSTANT GROWTH

Spendingt‐1 x (1 + Consumer Price Index YoY % change) = Spendingt

ADVANTAGES DISADVANTAGES

Smooths spending x Judgment in setting annual increase

Higher probability spending increases over previous year

x Does not considerendowment market value

t: time; YoY: Year‐over‐Year.

©2015 Fund Evaluation Group, LLC. Confidential. Not for Redistribution.12NACUBO: 2015 Endowment and Debt Management Forum

SPENDING POLICY METHODOLOGIES

CONSTANT GROWTH WITH BANDS

Spendingt‐1 x (1 + Consumer Price Index YoY % change) = SpendingtIf spending is < floor, spending = floorIf spending is > cap, spending = cap

ADVANTAGES DISADVANTAGES

Increases endowment value during strong markets

x Moderated spending amount during strong markets

More predictable spending x Spending higher during prolonged bear markets

t: time; YoY: Year‐over‐Year.

©2015 Fund Evaluation Group, LLC. Confidential. Not for Redistribution.13NACUBO: 2015 Endowment and Debt Management Forum

SPENDING POLICY METHODOLOGIES

CONSTANT GROWTH WITH BANDSHypothetical 3‐Year Scenario

• Beginning Market Value Y0=$100m, Y1=$125m, Y2=$150m• Spending Y0=5%• Inflation Y2=2.0%, Y3=3.5% • 4‐7% Band

Steps:1. Calculate the Bands2. Calculate the $ Spending3. Verify Spending Falls within Band

For illustrative purposes only.

©2015 Fund Evaluation Group, LLC. Confidential. Not for Redistribution.14NACUBO: 2015 Endowment and Debt Management Forum

SPENDING POLICY METHODOLOGIES

1. Calculate the Bands

BEG. MV FLOOR (4%) CAP (7%)

Year 0 $100m $100m x 4% = $4.0m $100m x 7% = $7.0m

Year 1 $125m $125m x 4% = $5.0m $125m x 7% = $8.8m

Year 2 $150m $150m x 4% = $6.0m $150m x 7% = $10.5m

Floor = Market Value x 4%Cap = Market Value x 7%

For illustrative purposes only.

©2015 Fund Evaluation Group, LLC. Confidential. Not for Redistribution.15NACUBO: 2015 Endowment and Debt Management Forum

SPENDING POLICY METHODOLOGIES

2. Calculate the $ Spending

BEGINNING SPENDING ($)

CPI YoY % CHANGE

CONSTANT GROWTH

ENDING SPENDING ($)

Year 0 $5.0m

Year 1 $5.0m 2% =$5.0m x 1.02 $5.1m

Year 2 $5.1m 3.5% =5.1m x 1.035 $5.3m

Spendingt = Spendingt‐1 x (1 + Consumer Price Index YoY % change)

For illustrative purposes only.

©2015 Fund Evaluation Group, LLC. Confidential. Not for Redistribution.16NACUBO: 2015 Endowment and Debt Management Forum

SPENDING POLICY METHODOLOGIES

3. Verify Spending Falls within Band

Floor < Spending < Cap

FLOOR (4%) ENDINGSPENDING

CAP (7%) ADJUSTED SPENDING

Year 0 $4.0m $5.0m $7.0m $5.0m

Year 1 $5.0m $5.1m $8.8m $5.1m

Year 2 $6.0m $5.3m $10.5m $6.0m

For illustrative purposes only.

©2015 Fund Evaluation Group, LLC. Confidential. Not for Redistribution.17NACUBO: 2015 Endowment and Debt Management Forum

GEOMETRIC

Smoothing rate x [Spendingt‐1 x (1+inflationt‐1) ] + (1‐ smoothing rate) x (target spending rate x beginning market

value) = Spendingt

SPENDING POLICY METHODOLOGIES

ADVANTAGES DISADVANTAGES

Accounts for inflation and market movements

x Slightly lower endowment values

Good balance between spending and market value – can customize smoothing rate

x Complex

t: time.

©2015 Fund Evaluation Group, LLC. Confidential. Not for Redistribution.18NACUBO: 2015 Endowment and Debt Management Forum

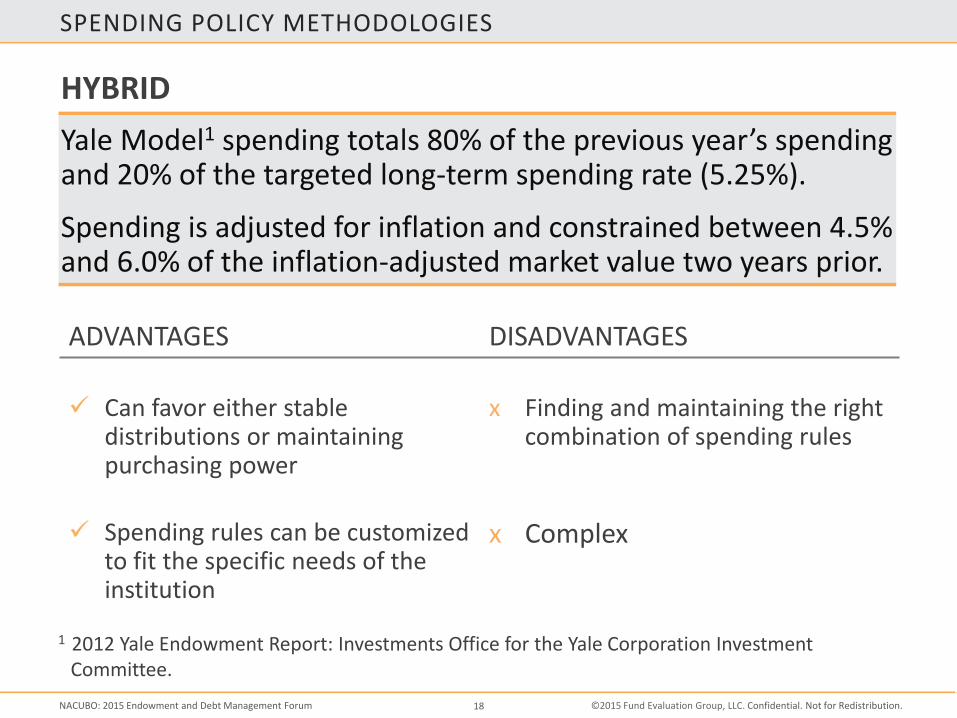

SPENDING POLICY METHODOLOGIES

HYBRIDYale Model1 spending totals 80% of the previous year’s spending and 20% of the targeted long‐term spending rate (5.25%).

Spending is adjusted for inflation and constrained between 4.5% and 6.0% of the inflation‐adjusted market value two years prior.

ADVANTAGES DISADVANTAGES

Can favor either stable distributions or maintaining purchasing power

x Finding and maintaining the right combination of spending rules

Spending rules can be customized to fit the specific needs of the institution

x Complex

1 2012 Yale Endowment Report: Investments Office for the Yale Corporation Investment Committee.

©2015 Fund Evaluation Group, LLC. Confidential. Not for Redistribution.19NACUBO: 2015 Endowment and Debt Management Forum

SPENDING METHODOLOGY COMPARISON

$145m

$191m

$151m

$100

$120

$140

$160

$180

$200

1992 1995 1998 2001 2004 2007 2010 2013

Market V

alue

Constant Growth CPI 3Yr MA Geometric

Data Source: Lipper; Data as of 12/31/2013.

IMPACT ON SPENDING1992‐2013, 70/30 Equity/Bond Portfolio

©2015 Fund Evaluation Group, LLC. Confidential. Not for Redistribution.20NACUBO: 2015 Endowment and Debt Management Forum

SPENDING METHODOLOGY COMPARISON

CUMULATIVE SPENDING1992‐2013

Data Source: Lipper; Data as of 12/31/2013.

VOLATILITY OF SPEND1992‐2013

$135

$140

$145

$150

$155

$160

$165

$170

$175

Constant 3 Yr. GeometricGrowth CPI MA

0

1

2

3

4

5

6

7

8

Constant 3 Yr. GeometricGrowth CPI MA

©2015 Fund Evaluation Group, LLC. Confidential. Not for Redistribution.21NACUBO: 2015 Endowment and Debt Management Forum

Case Study: University of Tennessee

©2015 Fund Evaluation Group, LLC. Confidential. Not for Redistribution.22NACUBO: 2015 Endowment and Debt Management Forum

BACKDROP

1 As of September, 2014. Based on UT's current allocation. Information provided by UT.

Instruction/ Academic Support

46%

Scholarships35%

Research13%

Other6%• Endowment assets

of $815m1

• Endowment supports 2% of University Operating Budget

©2015 Fund Evaluation Group, LLC. Confidential. Not for Redistribution.23NACUBO: 2015 Endowment and Debt Management Forum

CATALYST FOR CHANGE

• FY 2012 university decided to fund development efforts by shifting 50 bps from spending to fees

• Shift in spending distribution, along with post‐Credit Crisis market returns, created confusion amongst beneficiaries – Forgot (underestimated the impact of) shift on distributions

– Didn’t understand the look‐back impact of rolling average calculation

4.5% + 1.0% + 2.5% = 8.0%Spending Fees Inflation Primary Objective

5.0% + 0.5% + 2.5% = 8.0%Spending Fees Inflation Primary Objective

‐ 50 BPS + 50 BPS

©2015 Fund Evaluation Group, LLC. Confidential. Not for Redistribution.24NACUBO: 2015 Endowment and Debt Management Forum

OBJECTIVES

Volatility and the impact (real/perceived) focused attention on the Spending Formula

• Lower the year‐to‐year volatility in distributions while maintaining the target payout rate

• Preserve the long‐term purchasing power of the endowment

• More closely align spending policy time horizon with that of the investments, which are assessed on a 5/10 year rolling basis

©2015 Fund Evaluation Group, LLC. Confidential. Not for Redistribution.25NACUBO: 2015 Endowment and Debt Management Forum

PROPOSAL

Move from 3‐Year Moving Average (without cap and floor) to a 7‐Year Moving Average with a 6% Cap and 3% Floor1

• Gradual increase of 1 additional year per year to formula until 7 years included in calculation

• Starting year new formula would be 2011: post‐Credit Crisis, after endowment had 3‐year annualized returns of 11%– “Anchor” the transition formula in a period of strong performance– Maintain the average effective payout rate2

– Lower year‐to‐year volatility in distributions

1 % of Prior Calendar Year‐End Market Value2 Dollars Spent ÷ Beginning Market Value

©2015 Fund Evaluation Group, LLC. Confidential. Not for Redistribution.26NACUBO: 2015 Endowment and Debt Management Forum

EXECUTION

CONSENSUS

InvestmentCommittee

Congressional Budget Officer

Chancellors Board

©2015 Fund Evaluation Group, LLC. Confidential. Not for Redistribution.27NACUBO: 2015 Endowment and Debt Management Forum

EXECUTION

20212020201920182017201620152014201320122011

2015 2016 2017 2018 2019 2020 2021 2022

ANCHORING TO 2011Incremental Increase to 7‐Year Moving Average

CYE Market V

alue

FY Spend

©2015 Fund Evaluation Group, LLC. Confidential. Not for Redistribution.28NACUBO: 2015 Endowment and Debt Management Forum

RESULTS

Spending Policy MethodEnding 2013 Market Value

Total $ Spent

2013 $ Spent

Average % Spent

Std. Dev. of Spending

4.5% 3 Year Moving Average $227.3 $200.8 $9.93 4.4% 6.6%

4.5% 5 Year Moving Average $233.7 $200.1 $9.97 4.3% 4.9%

4.5% 7 Year Moving Average $240.5 $198.9 $10.40 4.2% 3.5%

Constant Growth (CPI) $276.9 $176.8 $10.41 3.6% 3.0%

Hybrid $230.2 $202.8 $10.43 4.3% 3.8%

SPENDING FORMULA RESULTS1990–2013

Analysis begins in 1990 and assumes an initial value of $100.The Moving Average formulas incorporate a 3% floor and 6% cap.Hybrid policy is 70% of last year's distribution adjusted for inflation and 30% of a 3 year moving average 4.5% policy.

©2015 Fund Evaluation Group, LLC. Confidential. Not for Redistribution.29NACUBO: 2015 Endowment and Debt Management Forum

$9.86

$9.32$9.97

$8.56

0

0

0

0

0

1

1

1

1

1

1

$4

$5

$6

$7

$8

$9

$10

$11

$12

1989 1993 1997 2001 2005 2009 2013

$10.40

$9.936.6%

3Y MA5Y MA7Y MA

Std. Dev. in YoY

Spending:3.5%

RESULTS

Data Sources: University of Tennessee and Fund Evaluation Group, LLC; Data as of 6/30/2014.

HISTORICAL DISTRIBUTIONS AT 4.5% SPEND RATE

4.9%

Shaded areas represent recessions.

©2015 Fund Evaluation Group, LLC. Confidential. Not for Redistribution.30NACUBO: 2015 Endowment and Debt Management Forum

RESULTS

$12.78

$11.22

$9.61 $9.00

$4.50

$8.76

$11.47

$8.82

$4

$5

$6

$7

$8

$9

$10

$11

$12

$13

1989 1993 1997 2001 2005 2009 2013 2017

3Y Growth7Y Growth7Y Recession3Y RecessionHistorical

Data Sources: University of Tennessee and Fund Evaluation Group, LLC; Data as of 6/30/2014.

HISTORICAL SPENDING ($) AND HYPOTHETICAL FORWARD‐LOOKING SCENARIOS3Y / 7Y Moving Average Spending During Growth / Recession

©2015 Fund Evaluation Group, LLC. Confidential. Not for Redistribution.31NACUBO: 2015 Endowment and Debt Management Forum

Considerations for a Low‐Return Environment

Confidential. Not for Redistribution.322014 FEG Investment Forum

“The market’s not a very accommodating machine; it won’t provide high returns just because you need them.”

‐ Peter L. Bernstein, Financial Historian (1919‐2009)

©2015 Fund Evaluation Group, LLC. Confidential. Not for Redistribution.33NACUBO: 2015 Endowment and Debt Management Forum

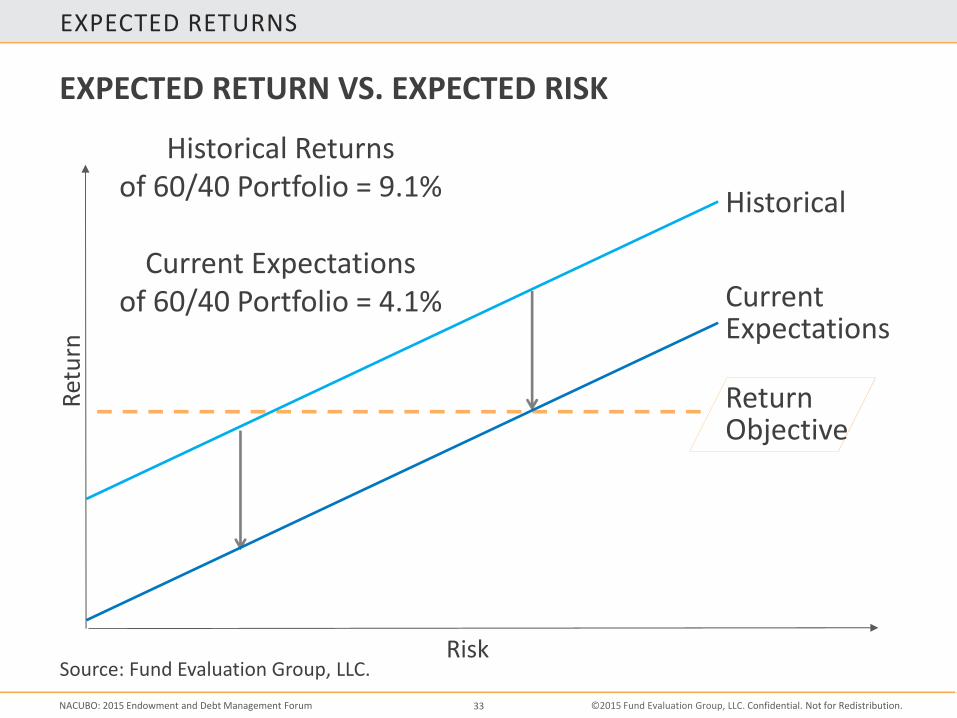

EXPECTED RETURN VS. EXPECTED RISK

Historical

Current Expectations

Return

Risk

Return Objective

Source: Fund Evaluation Group, LLC.

EXPECTED RETURNS

Historical Returns of 60/40 Portfolio = 9.1%

Current Expectationsof 60/40 Portfolio = 4.1%

©2015 Fund Evaluation Group, LLC. Confidential. Not for Redistribution.34NACUBO: 2015 Endowment and Debt Management Forum

LOWERING SPENDING RATE

4.9%

4.7%

4.7%4.6%

4.3%4.4%

4.5%4.6%

4.2%

4.4%

3.8%

4.0%

4.2%

4.4%

4.6%

4.8%

5.0%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Data Source: NACUBO‐Commonfund Study of Endowments 2013.

AVERAGE ANNUAL EFFECTIVE SPENDING RATE2004‐2013

©2015 Fund Evaluation Group, LLC. Confidential. Not for Redistribution.35NACUBO: 2015 Endowment and Debt Management Forum

LOWERING SPENDING RATE: IMPACT ON GROWTH

Data Source: Lipper; Data as of 12/31/2013.Returns represented by 70% S&P 500 Index and 30% Barclays U.S. Aggregate Index.

SPENDING GROWTH4% vs. 6% Spending Rates

$0

$20

$40

$60

$80

$100

$120

$1404% Spending Rate6% Spending Rate

©2015 Fund Evaluation Group, LLC. Confidential. Not for Redistribution.36NACUBO: 2015 Endowment and Debt Management Forum

SPENDING POLICY CONSIDERATIONS

0%

10%

20%

30%

40%

50%

60%

3.0% 4.0% 5.0% 6.0% 7.0%

Spending Rate

Increased probability of achieving the

portfolio’s objective

Prob

ability of M

eetin

g Objectives

IMPACT OF CHANGE IN SPENDING RATES

Source: FEG modeling 10 year projection, assuming a global 70/30 stock/bond split and startingmarket value of $250m.

©2015 Fund Evaluation Group, LLC. Confidential. Not for Redistribution.37NACUBO: 2015 Endowment and Debt Management Forum

SPENDING DECAY

020406080100120140160180200

40 138 237 335 433 531 630 728 826 925 1,023 1,121

Freq

uency

Distribution of Projected Wealth

Projected Median Market Values:6% Spending $227M5% Spending $258M4% Spending $292M

IMPACT OF CHANGE IN SPENDING RATESStarting market value of $250m

Source: FEG modeling 10 year projection, assuming a global 70/30 stock/bond split.

Higher Spending: Greater likelihood of market value decline

Lower Spending: Higher chance of growing capital base

©2015 Fund Evaluation Group, LLC. Confidential. Not for Redistribution.38NACUBO: 2015 Endowment and Debt Management Forum

Conclusion

©2015 Fund Evaluation Group, LLC. Confidential. Not for Redistribution.39NACUBO: 2015 Endowment and Debt Management Forum

SPENDING POLICY CONSIDERATIONS

• Coordinate asset allocation and spending policies to ensure the long‐term spending rate is consistent with the investment approach and an institution’s risk tolerance, factoring in level of institutional support (% of operating budget funded)

• Spending policy can be designed to “smooth” amount distributed from year‐to‐year

• When selecting a methodology, no correct answer, just a “best‐fit” solution that addresses institutions’ varying needs to maximize spending, minimize volatility, or maximize market value

• Expected returns today are lower this historically—consider reducing absolute spending level

2 0 1 4 F E G I N V E S T M E N T F O R U M

Producing Results in anUnpredictable World

GAME ON :

v

Questions?

NACUBO: 2015 ENDOWMENT AND DEBT MANAGEMENT FORUM

©2015 Fund Evaluation Group, LLC. Confidential. Not for Redistribution.41NACUBO: 2015 Endowment and Debt Management Forum

DISCLOSURES• This was prepared by Fund Evaluation Group, LLC (FEG), a federally registered investment adviser under the Investment Advisers

Act of 1940, as amended, providing non‐discretionary and discretionary investment advice to its clients on an individual basis. Registration as an investment adviser does not imply a certain level of skill or training. The oral and written communications of an adviser provide you with information about which you determine to hire or retain an adviser. Fund Evaluation Group, LLC, Form ADV Part 2A & 2B can be obtained by written request directed to: Fund Evaluation Group, LLC, 201 East Fifth Street, Suite 1600, Cincinnati, OH 45202 Attention: Compliance Department.

• The information herein was obtained from various sources. FEG does not guarantee the accuracy or completeness of such information provided by third parties. The information in this report is given as of the date indicated and believed to be reliable. FEG assumes no obligation to update this information, or to advise on further developments relating to it.

• Neither the information nor any opinion expressed in this report constitutes an offer, or an invitation to make an offer, to buy or sell any securities. Net Returns – Returns net of fees may or may not include the reinvestment of all dividends and income.

• Results on pages 13‐16 and 19 are based on hypothetical projections and may differ from actual results.

• Past Performance is not indicative of future results.

• This report is prepared for informational purposes only. It does not address specific investment objectives, or the financial situation and the particular needs of any person who may receive this report.

• Index performance results do not represent any managed portfolio returns. An investor cannot invest directly in a presented index, as an investment vehicle replicating an index would be required. An index does not charge management fees or brokerageexpenses, and no such fees or expenses were deducted from the performance shown.

• Any return expectations provided are not intended as, and must not be regarded as, a representation, warranty or predication that the investment will achieve any particular rate of return over any particular time‐period or those investors will not incurlosses.

• The information on pages 33 was obtained from the 2013 NACUBO‐Commonfund Study of Endowments (NCSE). The study includes a survey of 835 U.S. colleges and universities. The study divided the data into six categories according to size of endowment, ranging from institutions with endowment assets under $25 million to those with assets in excess of $1 billion. Data is for the 2013 fiscal year (July 1, 2012 ‐ June 30, 2013). The National Association of College and University Business Officers ( NACUBO) is a membership organization representing more than 2,500 colleges, universities and higher education service providers across the country and around the world. Commonfund Institute houses the education and research activities of Commonfund and provides the entire community of long‐term investors with investment information and professional development programs. NCSE returns are presented net of fees.