exporting for growth: identifying leading sectors for egypt · gamal abdel nasser (1956-1970) in...

TRANSCRIPT

© 2009 German Development Institute / Deutsches Institut für Entwicklungspolitik (DIE)

Exporting for growth: identifying leading sectors for

Egypt

Amirah El-Haddad

*Senior Economist

Stabilization and Development in the Middle East and North Africa

German Development Institute / Deutsches Institut für Entwicklungspolitik (DIE)

E-mail: [email protected]

Homepage: http://www.die-gdi.de/mena https://www.die-gdi.de/en/amirah-el-haddad/

*Professor of Economics - Faculty of Economics and Political Sciences, Cairo University

Sustainable Industrial Areas Conference Cairo March 6-7, 2018

© 2009 German Development Institute / Deutsches Institut für Entwicklungspolitik (DIE)

OUTLINE

Background: History of Egypt’s Economic Policy

The Product Space

Egypt in the Product Space

Results: PS, Strategic Bets and Forward Looking

Open Discussion Points

© 2009 German Development Institute / Deutsches Institut für Entwicklungspolitik (DIE)

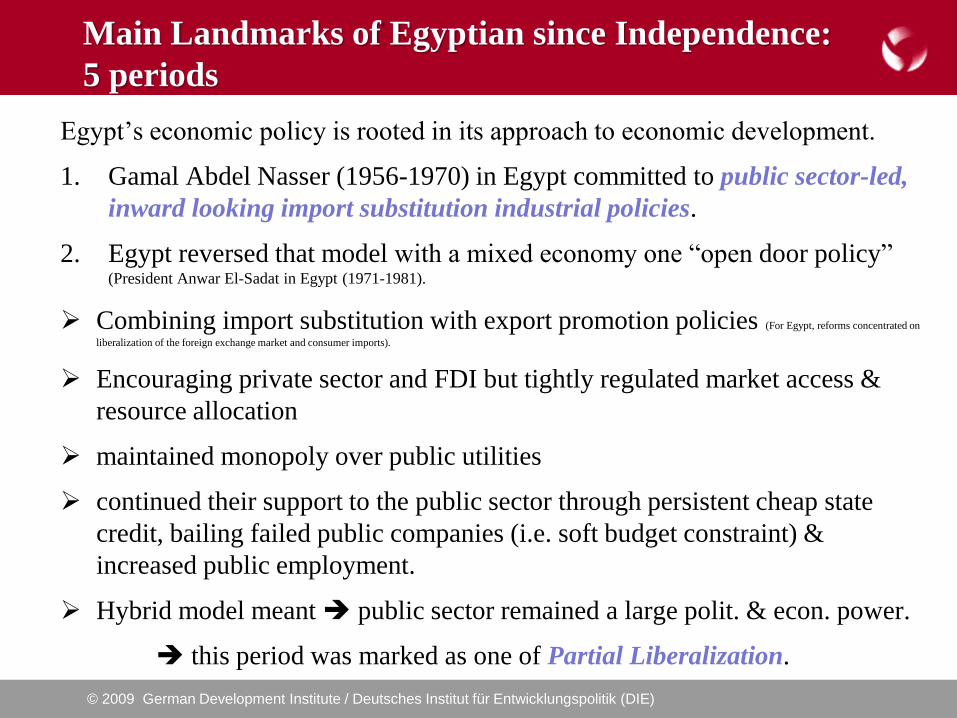

Main Landmarks of Egyptian since Independence:

5 periods

Egypt’s economic policy is rooted in its approach to economic development.

1. Gamal Abdel Nasser (1956-1970) in Egypt committed to public sector-led,

inward looking import substitution industrial policies.

2. Egypt reversed that model with a mixed economy one “open door policy” (President Anwar El-Sadat in Egypt (1971-1981).

Combining import substitution with export promotion policies (For Egypt, reforms concentrated on

liberalization of the foreign exchange market and consumer imports).

Encouraging private sector and FDI but tightly regulated market access &

resource allocation

maintained monopoly over public utilities

continued their support to the public sector through persistent cheap state

credit, bailing failed public companies (i.e. soft budget constraint) &

increased public employment.

Hybrid model meant public sector remained a large polit. & econ. power.

this period was marked as one of Partial Liberalization.

© 2009 German Development Institute / Deutsches Institut für Entwicklungspolitik (DIE)

Main Landmarks of Egyptian and Tunisian

Economic Policies since Independence: 5 periods 2 oil price shocks in 1973 & 1979 + consumption phase (70s & 80s)

budgetary deficits (18% in Egypt but only 4.5% in Tunisia) & a severe - trade balance, external

debt (116% (63%) of GDP Egypt (Tun) depleted foreign exchange resources

3. Growing severity of situation Egypt pursued an Economic Reform and

Structural Adjustment Program in 1991

Programs targeted:

– macroeconomic stability of external accounts and state budgets

– promoting greater market orientation, both decentralizing and

liberalizing the economy through reduction of state intervention and

price distortions.

– Ensuring greater trade liberalization (joining WTO & Euro-

Mediterranean Partnership (EMP) & signing association agreements

1995, 2001)

Thus deepening Egypt’s integration into the international global market

economy.

© 2009 German Development Institute / Deutsches Institut für Entwicklungspolitik (DIE)

Main Landmarks of Egyptian and Tunisian

Economic Policies since Independence: 5 periods

4. 4th stage in 2004 introduced more profound economic reforms: slashing of

customs and tariffs, and the replacement of politicians with techno-bureaucrats

The Arab Spring sparked in Tunisia in 2010 propagating to Egypt in 2011.

Most recent policy period: a return to state control and more protectionist

measures backed up by a severe foreign exchange and youth unemployment

crisis (13%) a budget and current account deficits mounting to 12% and 7% of GDP respectively, government debt exceeding the 100% mark and inflation reaching its highest level in

seven years. Was reported at over 15% in August, climbing to 19% by November 2016 (CBE, 2016).

© 2009 German Development Institute / Deutsches Institut für Entwicklungspolitik (DIE)

The Product Space Methodology

Product Space Analysis

Ǝ an established + relationship btw export diversification & growth

(by boosting economies of scale , so becoming highest productivity

activity in country( (e.g. de Ferranti et al., 2005; Feenstra et al., 2005))

Exports diversification (& sophistication) r distinct goals to

any active industrial policy

PS approach considers how countries may achieve that.

PSM is outcome of combined efforts of six scholars in Hausmann,

Hwang and Rodrik (2005), Hausman and Klinger (2006), Hidalgo et

al. (2007), Hidalgo and Hausmann (2009), and Hausmann et al.

(2011).

© 2009 German Development Institute / Deutsches Institut für Entwicklungspolitik (DIE)

Product Space Analysis

Drawing on the tools of Network Analysis, they empirically map the

product space for exported products.

It is ↑ likely that a country exporting asparagus to b also able 2

export artichoke (as Ǝ rural infrastructure in appropriate climatic zone suitable

for both + cold storage transp. systems + customs & regulatory regimes+ services

that support export of fresh produce,e.g. product approval and phytosanitary

permits).

Since the set of capabilities requisite 4 1 existing industry is easily

redeployed to another new industry spillover effects r at the heart

of the analysis.

it is easier to start on an industry when the other already exists

Therefore artichoke and asparagus are near each other in z product

space whereas oil and asparagus r not (implication of path

dependence).

© 2009 German Development Institute / Deutsches Institut für Entwicklungspolitik (DIE)

The Global Product Space and Leamer clusters

1) each node is a product 2) node size reflects product’s size in world trade 3) Proximity as explained above is expressed by the color-coded links between pairs of products according to linkage

strength 4) Specifically light blue links indicate proximity less than 0.4, beige links proximity of 0.40-0.55, dark blue proximity of 0.55-0.65 and finally a red link depicts proximity greater than 0.65.

Hierarchically clustered proximity matrix representing the 775 SITC-4 product classes exported in the 1998-2000 period. This network representation of the product space is laid out using a force

spring algorithm and retouched by hand (Hidalgo et. al 2007).

© 2009 German Development Institute / Deutsches Institut für Entwicklungspolitik (DIE)

Community Characteristics: Complexity & Connectedness

© 2009 German Development Institute / Deutsches Institut für Entwicklungspolitik (DIE)

Egypt and Tunisia in the Product Space (2014)

2014 Egypt’s Exports 2014 Tunisia’s Exports

2014 Egypt 2014 Tunisia

© 2009 German Development Institute / Deutsches Institut für Entwicklungspolitik (DIE)

Location Opportunities: Cross Country Comparisons

What exactly is Egypt’s prospects for greater diversification and

sophistication?

OV is a unique measure 4 each country & measures the benefit of a

country’s export basket/location in the PS.

It measures how many other different and/or sophisticated products

are near a country’s current set of productive capabilities

OV is a strong determinant of a country’s future

ability to move into new, and eventually more sophisticated

activities over time.

© 2009 German Development Institute / Deutsches Institut für Entwicklungspolitik (DIE)

Location Opportunities: Opportunity Value & GDP per capita, 2015

CAF

BDICODLBRNER

MWIMOZGINGNB

TGOMDG

COM

SLE

ETHGMBBFAHTI

RWA

ZWE

UGA

SSDAFGKIRMLIBEN

TCDSLBTLS

SEN

NPL

TZA

YEM

TJKLSOVUT

KEN

CMR

STP

BGD

KGZ

KHMDJIFSMCIVZMB

MHLTUV

GHASDN

PAK

PSE

MDA

HND

NICMMR

TON

LAO

WSM

NGA

VNM

UZB

IND

COGCPVBOL

AGO

PHL

GUY

GTM

MAR

UKR

BTN

ARMBLZ

SLV

SWZ

JAMPRY

FJIGEO

NAM

BIH

DMA

JOR

EGY

LCA

IDN

VCT

TUN

ECU

ALB

LKA

MNG

PER

MDV

NRU

ZAF

MKD

GRD

COL

LBN

SRB

DOM

CHN

DZAPLWIRQ

BRA

CRI

BWA

MNE

THA

BRB

TKMSUR

MEX

BLR

AZE

BGR

GAB

MUS

ARG

TUR

URY

ROUHRV

PAN

CUBBHSATG

CHL

LVA

KAZKNA

GRC

RUS

HUNMYSPOL

SYC

PRT

LTU

ESTSVKSVN

CZECYP

TTO

ISR

ESP

MLT

ITAKOR

NZL

OMN

FRA

JPN

GNQ

GBRFINBEL

ISL

CAN

AUS

BHR

DEU

AUT

DNK

SWE

NLD

SAUUSA

HKGCHE

IRLNOR

ARE

KWTBRN

SGPLUX

MAC

QAT

EGY

TUN

Algeria Iraq

-4-2

02

4

Opp

ort

un

ity V

alu

e

6 8 10 12Real GDP per capita (ln, PPP)

© 2009 German Development Institute / Deutsches Institut für Entwicklungspolitik (DIE)

Location Opportunities: OV versus ECI, 2015

ABW

AFGAGO

AIAALB

ANDARE

ARG

ARMASM ATA

ATFATG

AUS

AUT

AZEBDI

BEL

BEN BES

BFABGD

BGR

BHR

BHS

BIH

BLM

BLR

BLZ BMUBOL

BRA

BRB

BRNBTNBVT

BWA

CAF

CAN

CCK

CHE

CHL

CHN

CIVCMR

CODCOGCOK

COL

COMCPV

CRI

CUBCUWCXRCYM

CYP CZE

DEU

DJI

DMA

DNK

DOM

DZAECU

EGY

ERI

ESH

ESP

EST

ETH

FIN

FJI

FLK

FRA

FRO FSMGAB

GBR

GEO

GHAGIB

GIN GMBGNB GNQ

GRC

GRD

GRL

GTM

GUM

GUY

HKG

HMD

HND

HRV

HTI

HUN

IDN

IND

IOT

IRL

IRN

IRQ

ISL

ISRITA

JAM

JOR

JPN

KAZ

KEN

KGZ

KHMKIR

KNA

KOR

KWT

LAO

LBN

LBRLBY

LCA

LKA

LSO

LTU LUXLVA

MAC

MAR MDA

MDGMDV

MEX

MHL

MKD

MLI

MLT

MMR

MNE

MNG

MNP

MOZMRT

MSRMUS

MWI

MYS

NAMNCLNER

NFK

NGANIC

NIU

NLD

NORNPL

NRU

NZL

OMN

PAK

PAN

PCN

PER

PHL

PLWPNG

POL

PRK

PRT

PRY

PSE

PYFQAT

ROU

RUS

RWA SAU

SDN

SEN

SGP

SGSSHN

SLB

SLE

SLVSMR

SOM

SPM

SRB

SSD

STP

SUR

SVK SVNSWE

SWZ

SXMSYC

SYR

TCA

TCDTGO

THA

TJK

TKL

TKM TLS

TON

TTO

TUN

TUR

TUV

TWN

TZA

UGA

UKR

UMIURY USA

UZBVAT

VCT

VEN

VGB

VNM

VUT

WLF

WSM

YEM

ZAF

ZMBZWE

EGY

TUN

-4-2

02

4

Op

po

rtu

nity

Valu

e

-3 -2 -1 0 1 2Economic Complexity Index

© 2009 German Development Institute / Deutsches Institut für Entwicklungspolitik (DIE)

Product Feasibility: Complexity and Opportunity

Gain (2014)

Opportunity Gain vrsus Distance

Complexity versus Distance

Industrial or laboratory

electric furnaces

Other articles of

iron or steel nes

Medicaments

Other plastic plates,

sheets, film, foil &

strip

Ice cream

Medicaments

Other plastic

plates, sheets,

film etc. Polishes

and creams

Ice cream

Other articles of

iron or steel nes

Springs of iron

or steel

Appliances for

thermostatically controlled

valves

© 2009 German Development Institute / Deutsches Institut für Entwicklungspolitik (DIE)

Distance vrs. Product Complexity and

Opportunity Gain regressionsDistance versus Complexity

Distance versus Opportunity Gain

© 2009 German Development Institute / Deutsches Institut für Entwicklungspolitik (DIE)

Product Space Potential Up-Market Export

Sectors for Egypt, 2015

HS Product Chapter Section Group RCA PCI

Opp-

gain Distance

Exports

(US$mil)

Imports

(US$ mil)

World

exports

(US$mil)

4 Birds eggs, in shell,

fresh, preserved or

cooked

Dairy products, eggs,

honey, edible animal

product nes

Live animals; animal

products

Agr. Pr. 0.0 -0.17 0.27 0.7 0 0 4144

73 Tube, pipe of iron or

steel, except seamless

> 406.4m

Articles of iron or steel Base metal & articles of

base metal

Metals &

Manuf.

0.3 0.18 0.26 0.7 9 231 20621

48 Paper, board

containers, packing

items, box files

Paper & paperboard,

articles of pulp, paper &

board

Pulp of wood or other;

waste & scrap of paper,

paper & paperboard &

articles

Non Cons

An. & Plnt

Pr.

0.8 -0.06 0.29 0.7 28 115 20792

25 Quicklime,slaked,

hydraulic lime for

construction etc

Salt, sulphur, earth,

stone, plaster, lime &

cement

Min. Pr. Min. Pr. 0.0 0.09 0.24 0.7 0 0 997

22 Unsweetened

beverage waters, ice &

snow

Beverages, spirits &

vinegar

Prprd foods., bevr., sprts,

tobacco & subs

Agr. Pr. 0.2 -0.08 0.28 0.7 1 2 3599

19 Cereal food (roasted,

swelled), cooked grain

not maiz

Cereal, flour, starch,

milk preparations &

products

Prprd foods., bevr., sprts,

tobacco & subs

Agr. Pr. 1.0 0.51 0.47 0.7 9 5 5683

21 Ice cream & other

edible ice

Miscellaneous edible

preparations

Prprd foods., bevr., sprts,

tobacco & subs

Agr. Pr. 0.4 0.53 0.46 0.7 2 2 3248

39 Containers, bobbins &

packages, of plastics

Plastics & articles

thereof

Plastics & Rubber Chemical

& R. P.

0.6 0.35 0.38 0.7 47 115 46552

22 Waters, non-alcoholic

sweetened or flavoured

beverage

Beverages, spirits &

vinegar

Prprd foods., bevr., sprts,

tobacco & subs

Agr. Pr. 0.5 0.44 0.38 0.7 14 15 17474

41 Raw hides & skins of

bovine, equine animals

Raw hides & skins

(other than furskins) &

leather

Raw hides & skins, leather

articles, salldlery &

harness, trvl goods,

Non Cons

An. & Plnt

Pr.

0.0 0.21 0.41 0.7 0 4 5572

© 2009 German Development Institute / Deutsches Institut für Entwicklungspolitik (DIE)

Top Five Up-Market Export Products by Methodology Egypt

Product Space Methodology Strategic

BetsForward Looking

1 Birds eggs, in shell, fresh,

preserved or cooked

Medicaments, therapeutic,

prophylactic use, indosageDairy products, eggs, honey,

edible animal productPharmaceutical products

Live animals; animal

products

Products of the chemical or

allied industries

Agricultural Products Chemical & R. P.

2 Tube, pipe of iron or steel,

except seamless > 406.4m Seats (except dentist, barber, etc. chairs)

Articles of iron or steel Furniture, lighting, signs,

prefabricated buildings

Base metal & articles of base

metal

Miscellaneous manufactured

articles

Metals & Manuf.

3 Paper, board containers,

packing items, box files

Paper & paperboard, articles of

pulp, paper & board

Pulp of wood/other, waste &

scrap of paper, paper &

paperboard & articles

Non Cons An. & Plnt Pr.

4 Quicklime,slaked, hydraulic

lime for construction etcSalt, sulphur, earth, stone,

plaster, lime & cement

Mineral products

Mineral Products

5 Unsweetened beverage

waters, ice & snow

Beverages, spirits & vinegar

Prprd foods., bevr sprts

tobacco&subs

Agricultural Products

O Highly Manf. & Spcl-

Purpose Goods

Metals & Manuf.

Base metal & articles of base

Metal

Articles of iron or steel

Articles of iron or steel

Chemical & R. P.

Plastics&Rubber

Plastics & articles thereof

Containers, bobbins

&packages, of plastics

Chemical & R. P.

Plastics & articles thereof;

rubber & articles thereof

Rubber & articles thereof

New pneumatic tires, off

rubber

Hand saws and blades for

saws of all kindsTools, implements, cutlery, etc of

base metal

Base metal & articles of base

metal

Metals & Manuf.

Moulds for metals (except

ingot), plastic, rubber, etc

Nuclear reactors, boilers,

machinery, etc

Machinery, Mechanical

Appliance, Electrical Equip. &

Accessories

Metals & Manuf.

Newsprint

Paper & paperboard, articles of

pulp, paper and board

Pulp of wood/other, waste &

scrap of paper, paper &

paperboard & articles

Non Cons An. & Plnt Pr.

Metals, clad with platinum,

semi-manufacturedPearls, precious stones, metals,

coins, etc

Pearls, stones, metals, imitation

Jewl.

Metals & Manuf.

Polyamides in primary forms

Plastics & articles thereof

Plastics&Rubber

Chemical & R. P.

© 2009 German Development Institute / Deutsches Institut für Entwicklungspolitik (DIE)

Strategic Bets: More Invasive Active Industrial Policy

Compare results to more invasive active IP

One that tries to quickly steer the economy away from light industries such as

food processing and clothing to more sophisticated, capital-intensive heavy

industries such as machinery and iron and steel (provide ↑ OG but far away)

(similar 2 dev strategis dominated much of thinking of several newly-independent countries in the 2nd half of the 20th century, such as India and the Maghrib countries).

Can refer 2 this strategy as Strategic Bets: ↑ weight 2 PC & OG less 2 distance (a strategy that underscores more sophisticated sectors and greater opportunity gain (OG) and so gives less weight 2

distance)

Results r at the v end of the spectrum lead by machinery, equipment, and

high complex chemicals.

© 2009 German Development Institute / Deutsches Institut für Entwicklungspolitik (DIE)

Products in top 40% of PCI & OG , Distance

>=0.8, Egypt 2015, ordered by distance

HS Product Chapter Section Group RCA PCI

Opp-

gain Distance

Exports

(US$mil)

Imports

(US$

mil)

World

exports

(US$mil)

82 H& saws & blades for

saws of all kinds

Tools, implements,

cutlery, etc of base metal

Base metal & articles of base

metal

Metals &

Manuf.

0.00 2.58 1.09 0.80 0 14 3493

84 Moulds for metals (except

ingot), plastic, rubber, etc

Nuclear reactors, boilers,

machinery, etc

Machinery, Mechanical

Appliance, Electrical Equip. &

Accessories

Metals &

Manuf.

0.11 3.04 1.22 0.80 3 87 17150

48 Newsprint Paper & paperboard,

articles of pulp, paper &

board

Pulp of wood or other; waste &

scrap of paper,

paper&paperboard&articles

Non Cons

An. & Plnt

Pr.

0.00 2.54 0.83 0.80 0 48 5758

71 Metals, clad with platinum,

semi-manufactured

Pearls, precious stones,

metals, coins, etc

Pearls, stones, metals,

imitation jewl.

Metals &

Manuf.

0.00 2.02 0.85 0.80 0 0 47

39 Polyamides in primary

forms

Plastics & articles thereofPlastics&Rubber Chemical

& R. P.

0.01 3.77 1.48 0.80 0 17 12979

38 Reaction initiators,

accelerators & catalysts,

nes

Miscellaneous chemical

products

Products of the chemical or

allied industries

Chemical

& R. P.

0.02 2.63 1.26 0.80 1 19 16317

84 Gaskets & similar joints of

metal sheet

Nuclear reactors, boilers,

machinery, etc

Machinery, Mechanical

Appliance, Electrical Equip. &

Accessories

Metals &

Manuf.

0.10 3.61 1.47 0.80 1 35 3845

84 Machine-tool for working

stone, ceramics, cold glass

Nuclear reactors, boilers,

machinery, etc

Machinery, Mechanical

Appliance, Electrical Equip. &

Accessories

Metals &

Manuf.

0.00 2.93 1.14 0.80 0 29 2330

84 Converters, ladles, ingot

moulds etc, for metallurgy

Nuclear reactors, boilers,

machinery, etc

Machinery, Mechanical

Appliance, Electrical Equip. &

Accessories

Metals &

Manuf.

0.00 2.78 1.15 0.80 0 8 2971

38 Chemical industry

products nes

Miscellaneous chemical

products

Products of the chemical or

allied industries

Chemical

& R. P.

0.18 3.35 1.31 0.80 13 246 44528

© 2009 German Development Institute / Deutsches Institut für Entwicklungspolitik (DIE)

Strategic Bets: More Invasive Active Industrial Policy

SB promotes industries that will push

– economic growth,

– more diversification and

– urban job-creation

Drawback especially 4 countries with high (youth) unemployment rates

(e.g. Egypt and Tunisia).

Sectors r mostly less labor intensive and require high skilled workers.

If workers r moved quickly out of labor intensive light sectors agricultural

products, garments and food processing

labor maybe moved into unemployment or into low productivity

informal sectors.

The tradeoff more jobs versus better jobs or penniless versus jobless

growth is quite apparent here.

© 2009 German Development Institute / Deutsches Institut für Entwicklungspolitik (DIE)

Forward Looking: Trends in International Markets

PSM & SB both do not consider effect of world trade on future viability

of selected sectors (see criticisms of PSM in Altenburg 2016).

Developed countries have increasingly lost market share to developing

countries.

important 2 take international trade trends into account

when identifying upmarket sectors to strike balance btw PSM & SB

Taking into account the significance of every product in world trade (remember size of the bubble in product community figure)

Results of Up-Market Products weighted by their share in world exports

© 2009 German Development Institute / Deutsches Institut für Entwicklungspolitik (DIE)

Up-Market Products weighted by World

Trade, 2015

© 2009 German Development Institute / Deutsches Institut für Entwicklungspolitik (DIE)

Top Five Up-Market Export Products by Methodology Egypt

Product Space Methodology Strategic Bets Forward Looking

1 Birds eggs, in shell, fresh,

preserved or cooked

Medicaments, therapeutic,

prophylactic use, indosageDairy products, eggs, honey,

edible animal productPharmaceutical products

Live animals; animal

products

Products of the chemical or

allied industries

Agricultural Products Chemical & R. P.

2 Tube, pipe of iron or steel,

except seamless > 406.4m Seats (except dentist, barber, etc. chairs)

Articles of iron or steel Furniture, lighting, signs,

prefabricated buildings

Base metal & articles of base

metal

Miscellaneous manufactured

articles

Metals & Manuf.

3 Paper, board containers,

packing items, box files

Paper & paperboard, articles of

pulp, paper & board

Pulp of wood/other, waste &

scrap of paper, paper &

paperboard & articles

Non Cons An. & Plnt Pr.

4 Quicklime,slaked, hydraulic

lime for construction etcSalt, sulphur, earth, stone,

plaster, lime & cement

Mineral products

Mineral Products

5 Unsweetened beverage

waters, ice & snow

Beverages, spirits & vinegar

Prprd foods., bevr sprts

tobacco&subs

Agricultural Products

O Highly Manf. & Spcl-

Purpose Goods

Metals & Manuf.

Base metal & articles of base

Metal

Articles of iron or steel

Articles of iron or steel

Chemical & R. P.

Plastics&Rubber

Plastics & articles thereof

Containers, bobbins

&packages, of plastics

Chemical & R. P.

Plastics & articles thereof;

rubber & articles thereof

Rubber & articles thereof

New pneumatic tires, off

rubber

Hand saws and blades for

saws of all kindsTools, implements, cutlery, etc of

base metal

Base metal & articles of base

metal

Metals & Manuf.

Moulds for metals (except

ingot), plastic, rubber, etc

Nuclear reactors, boilers,

machinery, etc

Machinery, Mechanical

Appliance, Electrical Equip. &

Accessories

Metals & Manuf.

Newsprint

Paper & paperboard, articles of

pulp, paper and board

Pulp of wood/other, waste &

scrap of paper, paper &

paperboard & articles

Non Cons An. & Plnt Pr.

Metals, clad with platinum,

semi-manufacturedPearls, precious stones, metals,

coins, etc

Pearls, stones, metals, imitation

Jewl.

Metals & Manuf.

Polyamides in primary forms

Plastics & articles thereof

Plastics&Rubber

Chemical & R. P.

© 2009 German Development Institute / Deutsches Institut für Entwicklungspolitik (DIE)

Discussion

Top sectors’ barriers to entry, e.g. medicaments

subject to predatory anti-competitive practices (cartels e.g.

Mario Mariniello and Marco Antonielli, 2014)

highly protected sector (in Egypt limited licenses, bribes)

Type of Value Chain (captive or modular)

PSM is quiet as to how to proceed (97, 106)

Dynamic aspects: IP Target Sectors during last 20 years

Ability of IP to steer economy towards these sectors but

creates distortions Active vrs neutral IP (Lin and

Monga, 2010)

Technology Life Cycle of Products (Lee 2013)