exposure to currency risk, definition and measurement (1)

DESCRIPTION

cxcTRANSCRIPT

Exposure to Currency Risk:Definition and Measurement

Michael Adler and Bernard Dumas

The authors arc. rcspcclively. Professor. Graduate School ofBu.siness. Cohunhta Univcr.\ity and Professor of Finance, C.F.S.A./H.E.C., Jou\-en-.h>sas, Frame.

IntroductionU.S. corporations, including those with no foreign

operations and no foreign currency assets, liabilities.or transactions, are generally exposed to foreign cur-rency risk. Regional electrical utilities are a somewhatextreme case in point. With no foreign currency ac-counts on their books, they have no accounting expo-sure to exchange risk. From an economic perspective,however, the story is different. If their customer baseis dominated by either importing or exporting lirmswhose activities and demand for electricity are affectedhy exchange rate changes, the electrical utilities" oper-ations and stock prices themselves will also in princi-ple be exposed to exchange risk.'

Accounting rules for foreign currency translationare largely powerless in this situation. Economic expo-' Ih is piiini IS no! new. ll has Ils urtgins Jn tr;idilii>rial Iradc (henry andthe notion thai c:(chanj;c rale Lhiinjzes Lan cause, or LuinL'ide with,fluctuations in dumcstic aggregate demand, employment and outputand. therefore, ulsn with the activities of non-lradint; domestic firms.See Laursen and Metzlcr 1111.

sure to foreign currency risk must be defined andmeasured quite apart from the choice between currentor historical exchange rates for translating particularforeign currency positions. What is needed, in short, isto replace the accounting approach with a technique formeasuring the economic exposures of the marketprices of financial and physical assets. This is done inthe pages that follow which draw out the implicationsfor practice of recent innovations on the theoreticalfront. The objective, it should be noted, is limited todefinition and measurement; it is not the analysis of thedeterminants of exchange risk or exposure thereto. It isalso not to analyze whether individuals or firms shouldhedge. These last are important problems which arebest addressed once the exposure phenomenon itselfhas been precisely identified.

Section 1 distinguishes between currency risk andexposure. The latter is defined in Section II and meas-ured in Section 111. The practical implications oftheapproach are discussed in Sections IV and V.

41

42 FINANCIAL MANAGEMENT/SUMMER 1984

I. Risk vs. ExposureA currency is not risky because devaluation is like-

ly. It the devaluation were certain as to magnitude andtiming, there would be no risk at all. A weak currencycan be less risky than a strong currency. A strongcurrency does not become risky because it has beenused to denominate an individual's or a firm's debt. Inshort, expected exchange changes can be anticipated.Risk or uncertainty is a question of randomness, i.e..unexpected exchange rate variations.-

Currency risk is not the exposure. Currency risk is tobe identified with statistical quantities which summa-rize the probability that the actual domestic purchasingpower of home or foreign currency on a given futuredate will differ from its originally anticipated value.Exposure, in contrast, should be defined in terms ofwhat one has at risk.* The question at hand is how tomeasure it.

II. Currency-Risk ExposureFor purposes of financial analysis, a reasonable

measure t)f exposure to currency-risk should meet thefollowing three criteria:

(1) Its dimension should be an amount of currency,domestic for domestic currency risk and foreign forforeign currency risk.

(2) It should be a characteristic of any asset or li-ability, physical or financial, that a given investormight own or owe. defined from that investor's view-point.

(3) It should be implementabie in the dual sensethat, first, measurement can be accomplished withavailable techniques; and, second, exposure so meas-ured can be hedged or covered with available financialinstruments, such as forward exchange contracts.^

Assume a world with only two currencies. U.S.

•The idcnlificalion iit' exchange risk as randomness, disiinci trtmi ex-pected currency strength i>r weakness, is a by-pn>duct nt' studies otexchange rates as random walks, beginning wilh Pucile 113|, There is noneed ior present purptises to dislinguish between numina! exehanj;erisk, which niuy niH mailer under some asstimptions. and relative prieerisk, which may. A critical review oi the arcane debate on this pointappears iti Adler and Dumas ( i4 | . settion 61.

*Dtimas | 7 | seems to have been the first to make this distinction in print.Though obvious, it bears repeating,

"'The hedging scenarios to be eonsidereiJ are extremely simple by de-sign. Useful insights can nonetheless be achieveil. hulures contracts areexcluded ttiainly because most large firms slill prefer the forward to thefuiures markets. We also elide multi-period or dynamic hedging strate-gies, restricting atlention to a one-period setting. On both accounts,interest rate risk or reinvestment rate uncertainty remains outside ourpresent purview. These exclusions indicate the direction thai futureextensions and modifications of the ideas should take.

dollars and hrench francs, and that U.S. investors,who are all alike, perhaps improbably expect U.S.inflation, and therefore their domestic currency risk, tobe zero. They expect, however, that the Hrench infla-tion rate and therefore the exchange rate will be ran-dom. Forward contracts are available.

Consider next a representative U.S. investor whoexpects with certainly to receive exactly FF 1000 inthree months from today. What will be his exposure onthe target date three months away? The intuitive (andcorrect) answer is: precisely FF 1000. Why? The an-swer is apparent from Exhibit 1, FF 1000 representsexactly the sensitivity of the future dollar value of thefranc balance to variations in the exchange rate. Fur-thermore, a hedge in the form of a forward contract tosell 1000 francs for three months at the forward rate F,which will pay off $1000(F-S) at maturity, is exactlywhat is required to insulate the doUar value of thebalance from unanticipated variations in the exchangerate. The dollar value of the hedged position remainsconstant, at SiOOOF, across states of nature.

We can summarize these considerations in the fol-lowing linked definitions of exposure and hedging,based on the theory set forth in the Appendix.

Exposures = The amounts of foreign currencieswhich represent the sensitivity of thefuture, real domestic-currency (market)value of any physical or financial assetto random variations in the future do-mestic purchasing pt)wers of these for-eign currencies, at some specific futuredate.

Hedges = The amounts of the foreign-currency fi-nancial transactions {i.e.. forward con-tracting or its equivalent) required torender the future, real, domestic-cur-rency market value of an exposed posi-tion statistically independent of unantic-ipated, random variations in the futuredomestic purchasing powers of theseforeign currencies.

There are several points to observe about these defi-nitions. First, the concept of exposure has a definitetarget date. This is partly because the financial instru-ments used for hedging in practice have contractuallyfixed maturity dates. They can, therefore, protect ex-posures only within the period covered by the contract.In addition, exposures themselves may vary overtime.They are future quantities which may be imagined asthe equivalent of foreign currency deposits or debts

ADLER, DUMAS/EXPOSURE TO CURRENCY RISK 43

Exhibit 1. Exposure of FF 1000. To Be Received in lhe Future. When There AreThree States of Nature[•"uturc Quanlilics State I State 2 State 3

FF Balance: P*txchangc Rate: S = $/FFDollar Value: SP*Proceeds of Furw'ard Sale: $IOOO(F-S) :Dollar Value of Hedged Position

10000.250i25O

ilO(K)(F-O.2.'i)SIOOOF

10000.225$225

$IO(H)(F-(I.225)SIOOOF

10(H)0,2(H)$200

MIHH)|F-O.2())SIOOOF

vvhieh will exist or mature on st)rne future date.'^ Inmost practical cireumstances. exposure in any eurren-ey will not be a certain accounting quantity but willrather be a magnitude which must be projected andestimated by statistical means. Seen from the present,exposures six riKtntbs ahead may be greater or smallerthan exposures a year ahead.

A second point to be emphasized, and one that weshall investigate in detail below. Is that the notion ofexposure is not restricted to non-traded financial assetsor liabilities with fixed, nominal, foreign-eurrencypayoffs on the maturity date of the hedge. The expo-sure of such assets is easy to determine. They are \{W/(exposed in the specific sense that their exposure isexaetly equal to their foreign-eurrency face value onthat date, as the example in Exhibit 1 demonstrates.However, the (real) domestic-currency price of mn'as.set or liability, physical or financial, whose futureforeign currency value is uncertain, may also be sensi-tive to. or correlated with, exchange rate fluctuations.To the extent of this sensitivity or correlation, suchassets should indeed be considered exposed. This leadsto the notion of exposure as a statistical property.

In the Appendix and in the next section we show thatexposure is best measured with statistical regression

" This eniphiisis. thiii exposure depends i>n lhe LOV aria rice oi fiifiircprli.es with future exchange rales, marks a radiciil departure trurii theiirrrcni iCKrhiiok wrsdoiii. f-crexample. Ciimcll and Shapiro i(i| indicaleIhal exposure should be mcasirrcd in lernis ot Ihe rmpad of unexpeetedexchange rate eharijies on lhe present value ol the firm's lulure cashtlows lAithoiii rel'crcnce lo a targel dale. This apparently represents anatlempl lo collapse the dynamic evoliitmn ot exposure over time irilo asingle measure. In our opinion, il is unsuccessful. When one thinks inIcrnis ot market prices, as one should, present-values are currentlyknown They are certain. The very idea ot a covariance belween lhenon-random curreni market price anil ramlom exchange rate varialionsover an indetinite hori/on is. therefore, vacuous. The possibility otdevising any other single-valued measure ol' association tictwcen apresent value and exchange rales at every future dale seems equallyremote, in finance, iioironal changes in present values are used toevaluate the mipact ol curreni decisions Ihal will alfect fulure oulcomes:hut no linancial decision is required for measuring exposure. The ap-proach taken here enables financial decision analysis and exposuremeasurement to be kepi apart: Hxposure is a mailer of Ihe future,instantaneous covariation of contempiiraneous prices and exchangeraics either at discrete points o!. or ciinlinuously over. lime. Il is Ihevulue ol hedgrng Ihal rc'nuires preseni value comparisons.

techniques, as the coefficient(s) of the purchasingpower variables(s). (i.e.. the exchange rates when do-mestic infiation is zero), in a multiple linear regressionof an asset's future domestic-currency market price on(the set of) the contemporaneous foreign exchangerate(s).'' Each such regression coefficient has the di-mension of units of foreign currency. The idea behinddefining exposure in this fashion is that it decomposesthe probability distribution ofa risky asset's domestic-currency price at a future instant into two parts: onethat is correlated with the (set o\) exchange rate(s) anda second that is independent of them. The first compo-nent may be considered exposed as its variability maybe removed by financial hedging. It is the equivalent ofthe French franc deposit in the previous example. Re-sidual variability remains, but it is not exposed as itcannot be further reduced by hedging. It should beclear that in this approach exposures can be positive,zero or even negative depending on the direction of thecorrelations between an asset's price and the exchangerates. If, furthermore, one thinks of long-term foreignbonds with nominally fixed redemption values butwith maturities beyond the target date, the exposuresof their market prices, translated into dollars, may bemore or less than one-hundred percent.^

III. Exposure Is a Regression CoefficientAn asset may be simultaneously exposed to more

than one currency. The reader should keep this in mind

'The intellectual pedigree of ihis approach appears panly in Ihe Appen-dix 11 originated in t;)unias |7 | which lolloued several of his workingpapers beginning in 1^76.

'See Adler and Dumas |2| fora two-period analysis of the determinantsof exposure in this case. In lhe one-period framework of the presenipa|K'r. a financial or physical asset is risky if its end-of-period, dollarmarkei prrce is random, Financial assets include stocks and short andlong-term bonds: physical assels are (manufactured) goods like planiand equipment and inventory. Financial and physical assets need noitunlierbe ilisiinguished. as ihey must in mulliperind or continuous limemodels, according Io the source of uncertainty: interest-rate risk in thecase of long-lerm Kinds: and eash tlow or replaeemenl-value risk,combined with interesl-rale risk, in that of stocks and physical assels.Nominally riskless bonds and deposits are free of default risk in theirrespective currencies. Deposits are noi Iraded prior lo mairjrily andtheretore are also free of interest rale risk. Nominally riskless foreigncurrency deposits are risky in dollar lerms.

44 FINANCIAL MANAGEMENT/SUMMER 1984

throughout what follows. It is only tor simplicity ofexposition that we construct the examples of this sec-tion using a single exchange rate. The intention ofthese examples is to demonstrate how exposure may bemeasured using well-known linear regression tech-niques. That it should be so measured is proved in theAppendix. When one wants to determine exposure tomany currencies, the regressions in question simplybecome multiple linear regressions. This extensionof the methodology will be mentioned again in Sec-tion IV.

For the purpose ofthe exercises that follow, we needno more than a simple setting with three possible futurestates of nature and two currencies, dollars and francs.We continue to assume that dollar inflation is non-random. The setting is fully described by Exhibit 2.Looking ahead from now. time 0, to a future targetdate, the dollar value of a nominally riskless or riskyFrench asset is uncertain. Uncertainty is captured bythe fact that one out of three possible states of nature.subscripted by s, will occur. In each state the Frenchasset will have a franc price denoted by P*. P^will havethe same value in each state if the asset is nominallyriskless. such as a bank deposit or a T-bill. and if itmatures on the target date; and it will have differentvalues across states if it is risky like a stock or a long-term bond which matures after the target date. Seenfrom now. the exchange rate, S,, is also uncertain: itwill take on different values within its possible rangeof variation in each future state of nature. Consequent-ly, whether ornot Pf itself is constant, the dollar valueof the French asset, S^P* — P . will be random,

in the Appendix we show that the exposure of theFrench asset, from the viewpoint of a U.S. investorwho assumes that U.S. inflation is non-random andwho has access to forward contracts, is properly meas-ured by the coefficient, h. in a linear regression of P onS across the states of nature:

P = a + b-S + e

where

a = regression constant;e = random error term such that E(e) - 0 =

cov(e.S).

Note that the dimension of b is units of French francs: ittherefore meets the first of tiur criteria for an exposuremeasure in the previous section.

We now demonstrate the application of this expo-sure measurement technique through two numericalexamples. In each, the state probabilities are 1/3, thatis. the states are equi-probable, a condition often asso-ciated with ignorance. The first, in Exhibit 3. whichcalculates the exposure of a French franc deposit, isincluded for comfort. It should be consoling to discov-er that the computed exposure is in fact equal to thedeposit's face value as intuition demands. The seconddeals with a slightly more complex situation in whichthe French franc asset-price is also random. We deferdiscussion of the results till later.

Exhibit 3 provides the requisite consolation. In thesituation where we know that the exposure is FF 1000.the regression technique produces exactly that result.This is also exactly the amount that can be hedged.Following the procedures of Exhibit 1 above, the out-come is that a hedge in the amount of FF 1000 willmake the dollar value of the franc deposit constantacross states of nature.

This constancy of the dollar value of the hedgedposition is possible only when the franc price o{ theFrench asset is itself constant across states of nature,that is, when the French asset is nominally riskiess infranc terms and its maturity coincides with that oftheforward contract. It is only such assets that are 100%exposed in the dual sense that their exposures equaltheir tace values and they can be perfectly hedged.

When the underlying French franc price at the hedg-ing horizon is random, the risky asset cannot be per-fectly hedged. The Appendix teaches us that in such

Exhibit 2. The Dollar Price of a Risky Foreign Asset in Three States of Nature

f-rcni.liFrancPrice. P*

fixchangcRate: S.

I'.S. DollarPrice; S.P* = P.

Time 0

ADLER, DUMAS/EXPOSURE TO CURRENCY RISK 45

Exhibit 3 . Exposure and Hedging When There are Three States of Nature andFixed Amount. FF 1000. Due in the Future

1)

(2)

l3)

14)

To Show; Hxposure is the regression ci^ffieient ofthe future dollar value oftheFF position in a regression of that position on the exchange rate. Inthis

Definitions: P*P

Regresion: PbPPS

eov(P.S)var(S)

Dala:

Slales p S

(5)

1/3 0.251/3 0.225

* 1/3 0.20

ease, exposure must also necessarily be FF 1000.= FF IO(X) in each state= Dollar value ot FF 1000 in state s at time-t- $S,P* = SKKK) S, in this case. _^ a H- bS + e, where here, a = P - bS = 0;= cov(P.S)/Var(S|;^ Probability of state s:- X,p,S,P* - $l(H)O S = $225 below, since- S,p,S, - 0.225 $/FF. from the data.= X.pjP. - P)(S, - Si= S.pjS, - S)-

P, S, - S P, P IS.. - S)- iP, - PHS, - Si

S25O 0.025 $25 0.000625 0.625$225 0 0 0 0$200 -0.025 -S25 O.(HK)f)25 0.625

Caleulated Regression Coeffieient;cov(P,S) (2/3)10.625) ^^ ^^^^

var(S| (2/3)(0.000625)

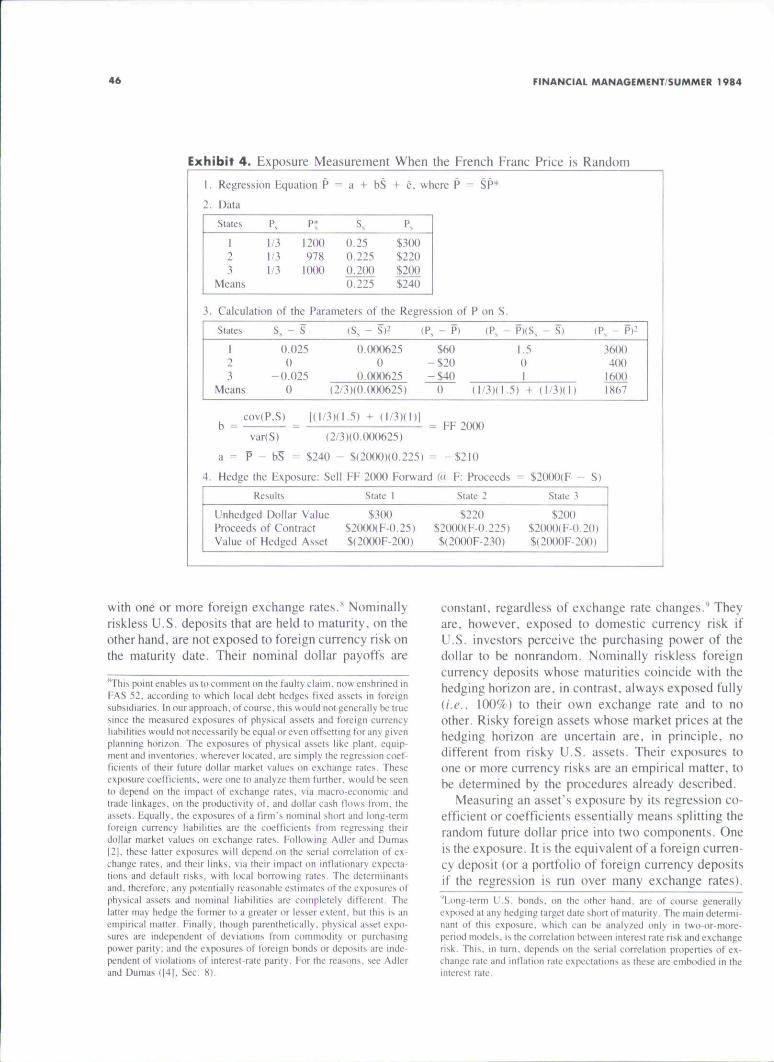

cases the be.st one can do is to hedge in the amount oftho exposure. This will minimize the variance of thehedized asset and render the residual variability oftheasset price in dollars, after hedging, independent oftheexchange rate. The effect of determining exposure viaregression, in other words, is tt) decompose the ran-domness of P = SP* into two components: one whichis correlated with the exchange rate and is removed byhedging; and u second, that remains after hedging.whose variance is minitnal and which is statisticallyunrelated to the exchange rate. This is demonstrated inExhibits 4 and 5.

The top panel of Exhibit 4 provides the data for thedollar value of a risky French asset in each of threestates o{ nature. In the tniddle panel we compute theregression coefficient, b. in the regression of P on S.This coefficient represents the exposure: it is FF 2000in this example. The bottom panel reveals the results ofa hedge in the amount of the exposure. Quite clearly,the dollar value of the hedged asset is not constantacross states of nature. The hedge in this situation isobviously not perfect: the hedged asset is still risky.

It is. however, the best that ean be done in a veryspecific sense. As shown in Exhibit 5. the residualvariability in the dollar value of the hedged asset, de-noted by R. is statistically independent ofthe exchange

rate: that is. as shown in the third panel. cov(R,S) = 0.What then has been accomplished by hedging? This isshown in the fourth panel of Exhibit -*i. The variance ofthe unhedged position, computed in the righttnost col-umn of panel 3 in Exhibit 4. is I867($)-. The varianceofthe hedged but still risky asset, calculated in panel 2of Exhibit 5. is200($)-. Hedging has removed the partof the variance due to exchange rate variability, in theamount of 1667 ($)-. The remaining variability hasbeen tninimized and cannot further be reduced by for-ward exchange contracts or their equivalent. Otherhedging instruments or methods such as diversificationmust be sought if it is to be avoided.

IV. 5ummary Observations on theMeaning of Exposure

It is perhaps worth reconsidering the concept of ex-posure in light of the measurement procedures de-scribed above. From the viewpoint of U.S. investorsexposure, to be sure, is the regression coefficient or. ifthere are tiiany currencies, the vector of partial regres-sion coefficients, when an asset's dollar price is re-gressed on exchange rates. Seen in this way. it is clearthat any asset, regardless of its location, may be ex-posed. U.S. stocks and real estate are exposed, forexample, if their (future) market prices are correlated

46 FINANCIAL MANAGEMENT/SUMMER 1984

Exhibit 4. Exposure Mea.surement When the Freneh Franc Price is Random

1. Regression Equation P - a + bS + e. where P = SP*

2. Data

Slales

123

Means

P..

t/3t/31/3

Pt

1200978

!(H)0

0.250.2250.2000.225

P,

$300$220$200$240

3. Calculation

States

123

Means

of the

S, - S

0.0250

-0.0250

Parameters

(S,

0

0(2/3)(O

ot the Regression of

- S)'^

.0006250

.000625000625)

(P, - P)

$60-$20-$40

0

P on S.

IPs -

(!/3)(l.5

P)(S, S)

1.501

) + ( l / 3 ) ( l |

(P. - P)-

3600400

1600IK67

b =eovtP.Sl

- FF 2000var(S) (2/3)(0.000625)

a - P - b5 - $240 - $(20O0M0.225) = -$210

4. Hedge the Exposure: Sell FF 2000 Forward (<> F: Proceeds - $2000(F - S)

Results Slalc I SI State 3

Unhedged Dollar ValueProceeds of ContractValue of Hedged Assel

$300$2(.K)0(F-0.25)$|2O()OF-2(H)I

$220$20(K)(F-0.225)

$(2(XK)F-230)

$200$2(K)O(F-O.2O|$(2OO()F-2OO)

with one or more foreign exchange rates.^ Nominallyriskless U.S. deposits that are held to maturity, on theother hand, are not exposed to foreign currency risk onthe maturity date. Their nominal dollar payoffs are

" This point enables us lo comment on the faulty claim, now enshrined inFAS 52, according to which liKal debt hedges tixed assets in foreignsubsidiaries. In our approach, of course, this would notgcncrally belrucsince ihe measured exposures of physical asscis and fi>rcign currencyiiabililies would not necessarily be equal or even olfsetting lor any givenplanning hori/on. The exposures of physical assels like plant, equip-ment and inventories, wherever located, are simply ihe regression coef-ficients ol' their future dollar market values on exchange rales. Theseexposure coetficienls. were one !o analyze them funhcr. would be seento depend on the impact of exchange rales, via macro-economic andtrade linkages, on the produclivity of, and doliar cash Hows from, theassels. F.qually, ihe exposures of a firm's nominal short and long-iermforeign currency liabililies are the eoefficienis from regressing iheirdollar market values on exchange rales, hollowing Adler and Dumas|21. these latter exposures will depend on the serial correlation of ex-ehange rates, and their links, via their inipaci on intlationar\ expeda-lions and delaull risks, with local borrowing rates. The determinantsand, therefore, any piitenlially reasonable csiimates ofthe exposures ofphysical assets and nominal liabililies are completely ditfereni. Thelatter may hedge the former lo a greaier or lesser extent, but this is anempirical matter. Finally, though parenthetically, physical asset expo-sures are independent of devialions from commodity or purchasingpower parity: and (he exposures ol' foreign bonds or deposits arc mJe-pendent of violations of inlerest-ratc parily. For Ihe reasons, see Adlerand Dumas Il4|, Sec. S).

constant, regardless of exchange rate changes,'' Theyare. however, exposed to domestic currency risk ifU.S. investors perceive the purchasing power of thedollar to be nonrandom. Nominally riskless foreigncurrency deposits whose maturities coincide with thehedging horizon are. in contrast, always exposed fully[i.e.. 100%) to their own exchange rate and to noother. Risky foreign assets whose market prices at thehedging hori/.on are uncertain are. in principle, nodifferent from risky U.S. assets. Their exposures toone or more currency risks are an empirical matter, tohe determined by the procedures already described.

Measuring an asset's exposure by its regression co-efficient or coefficients essentially means splitting therandom future dollar price into two components. Oneis the exposure. It is the equivalent of a foreign curren-cy deposit (or a portfolio of foreign currency depositsif the regression is run over many exchange rates).

''t,ong-term U.S. bonds, on the olher hand, are of course generallyexposed al any hedging largel dale short of maturity. The main determi-nant of this exposure, which can be analyzed only in two-or-more-period models, is the correlation between interest rate risk and exchangerisk. This, in turn, depends on llie serial correlation properties of ex-change rate and inflation rale expectations as these are embodied in iheinterest rale.

ADLER, DUMAS/EXPOSURE TO CURRENCY RISK 47

Exhibit 5. Demonstration That the Hedged French Asset Is Independent of the ExchangeRate

1. Dollar Value of Hedged Asset = R, = P, + b(F - S j

2. From Exhihit 4 calculate the following data:

Slates

12

3Means

P,

1/31/31/3

Rv

$(2OO0F-20O)$(2OOOF-23O)$(2(KK)F-2(K))$(2O(KIF-21O}

R,. - R

+ SIO-$20+ $10

0

s, - s0.0250

-0.0250

(R, - R)lS, - S)

0.250

-0.25(l/3)(0.25) - (1/3)10.25)

IR, - R)=

100400KKI200

3. cov(R.S) - E|(R,

4. Summary of Results of Hedging

- (1/3)10.25) - (l/3)({).25) - 0

Variance of Unhedged A.ssel - Var(P) - 1867 ($)-Variance of Hedged Asset = Var(P - bS) = Var(R) - 200 ($)-Variance Removed hy Hedging - b'VariS) = (20(H))-(2/3)(0.(X)0625) - 1667

This component can be perfectly hedged by an offset-ting forward exchange transaction, just as foreign cur-rency deposits themselves could be hedged. Thisequivalence of exposure to a (portfolio of) foreign cur-rency deposit(s) is an idea to which we shall subse-quently return. The second component is not exposedto exchange risk, in the specific sense that its random-ness is not correlated with any exchange rate. It may.of course, be exposed to other identifiable risks: butthese cannot be hedged with forward currency transac-tions.

Risky assets other than domestic and foreign curren-cy deposits and long-term bonds, which promise pay-ment of a specific amount of currency at maturity,have no intrinsic denomination in any currency. Inother words, they are generally risky regardless of thechoice of reference or measurement currency. An assetean be said to be denominated in a currency to theextent that its future dollar value, or some fractionthereof, behaves as if it were a riskless deposit in thatcurrency.'" Another way of looking at our concept ofexposure is that it measures the extent to which anyasset can be said to be denominated in one or morecurrencies. Common stocks, for example, regardlessof where they are traded, and physical assets, regard-less of where they are located, can therefore equally

"The quesiion of denominalion. il should be clear, is quite differenttrom the issue of the corrccl dcflalor for a firm's resulls discussed bytaker |S|. His suggesleit numeraire is. in any event, problematic: (mehas lew choites between the owners" t'PI and separate indices for eachof the firm's output and inpul goods. The latter, furthermore, willgenerally have diiterent exposures. F.xchangc rate changes ean indeedaftect a firm's comixjlitiveness even if CPP holds for every good andPPP holds al lhe level of the CPI, if the relative priees of inputs andoutputs vary.

well be said to have no intrinsic currency denominationor to be denominated, to the extent of their exposures,in one or more currencies. In these cases, denotnina-tion like exposure cannot be identified in advance butinstead is an empirical matter.

Finally, it is perhaps worthwhile emphasizing whathedging with forward exchange contracts can do andwhat it cannot. Hedging with forward exchange trans-actions does not in general remove currency risk." Itmerely substitutes exposure to domestic purchasingpower risk for exposure to foreign currency risk. Whendomestic purchasing power uncertainty is negligible,forward exchange transactions can remove the impactof exchange risk variability. They do so in effect byredenominating the exposed fraction of an asset's fu-ture domestic value, from foreign currency into do-mestic currency. When foreign asset prices are uncer-tain and/or when domestic inflation risk is present, the(real) dollar values of these assets cannot be fixed inadvance merely with forward contracts. At most, onecan hedge away that part of the nominal variationwhich is linearly correlated with exchange-rate ran-domness. The dollar prices of these assets will remainuncertain after hedging. The remaining uncertaintywill be independent of the exchange rate. Only to thisextent can the asset's total risk be said to have beenhedged.

"Different limitations of hedging with forward conlracts have beendiscussed by other auihors. One key issue, which is largely outside theprovince ol this paper, is whether hedging foreign exchange risk can add\alue to the firm. In intormalionally symmetrie, quasi-complete mar-kets, it cannot; see Adler and Dumas 111. Baron |S| . l-ogueand Oldfield112|. and Dumas |7 | .

48 FINANCIAL MANAGEMENT SUMMER 1984

V. ConclusionUntil now. corporate exposure to foreign exchange

risk has largely been investigated in the literature fromthe viewpoint ot the firm and its managers. Here wehave looked at it in a way that conforms to the interestsof stockholders and analysts. The notion that exposurecan be measured as a regression coefficient shouldhave immediate appeal to this group.

Stock analysts have lonjz been accustorned to meas-uring the riskiness ofa security or a portfolio by its betain a regression of the portfolio's returns on the marketindex. Viewed slightly differently, beta represents atransformation of the exposure of the portfolio to themarket. To hedge a portfolio with initial value V,. onesbouid short a quantity of index futures equal to (beta)(V,).'^ Such a hedge, if interest rates remain constant,will render the future vuiuc of the portfolio largelyindependent of the index for the life of the contract.

Clearly, the idea of exposure to exchange risk is notintrinsically different from that of exposure to niurkelrisk. It is not. therefore, surprising that the two can beestimated in similar ways. Thus, for example, a portfo-lio's average exposure toe.xchange risk in the past can.in principle, be obtained by regressing its total dollarvalue on a vector of exchange rates: the partial regres-sion coefficients will represent its exposure to eachcurrency. If the future is like the past, portfolio manag-ers could conceivably use the procedure usefully tostrip the exchange risk component out of portfolio re-turns by hedging these exposures. The promise isthere. Before it can be implemented, however, onemust confront the usual but intricate problems of sta-tionarity and multicollineurity. As exposures vary overtitiif. it will be necessary further to attempt to derivemultiperiod hedging rules. These are matters for futureresearch.

In addition, several implications for corporate prac-tice emerge from redefining exposure properly interms of market rather than book values and measuringit as a regression coefficient. For one thing it tnaychange or refine the way some treasurers think aboutexposure: that indeed is the paper's main aim. Expo-sure is a statistical quantity rather than a (projected)

'"More precisely, since lhe regression is run on rates of return, bela isthe elasticity ofthe stixrk price with respect to the market. The elasticityIS a diniensionless number while exposure is a dollar amount in thiscase. It is apparent Irom the Appendix that in this case: IZxposure, =ibetJllV,). where V, is the initial price ofthe stock. Naturally, if beta isstationary', exposure will change as V, varies over titiie. This raises theissue of the specification of dynamic hedging strategies which is theobject of much current research in connection witb (he use of mdexfulures.

accounting number. Foreign currency liabilities andforward contracts have their own measurable expo-sures. They cannot therefore be expected to perfectlyhedge fixed assets or foreign operating results, whoseexposures are generally different, and in some circum-stances may not do so at all. The firm as a whole isexposed. Its global exposure is not necessarily the sumofthe exposures of the individual foreign operations orof specific foreign currency accounts, for this ignoresthe exposure of domestic operations. Nor is its globalexposure some sum of its so-called "accounting" and"economic" exposures," £.v ante, the two cannot bemeasured or hedged separately, in as much as futurefinancial reports will reflect the impact ofthe econom-ic environment and the firm's responses via currentand future managerial decisions.

What the regression coefficient concept of exposurecan provide is a single comprehensive measure thatsummarizes the sensitivity of the whole firm, as of agiven future date, to all the various ways in whichexchange rate changes can affect it. While problems ofimplementing this approach must be left to be treatedelsewhere, it offers a further insight.'^ Once exposuresare so measured they can. for purposes of managerialcontrol, be decomposed into components, one for eachkind of influence that exchange rates can have. If nec-essary, the decomposition can produce the counter-parts of translation and transaction exposures as part ofthe total. Neither should necessarily be ignored, norshould they be hedged alone. When and if hedging is adesirable corporate decision, it is exposure as a whole,not some part of it. that should be protected. All this isat least conceptual progress in the direction of clarity.

We cannot end without a warning. Adapting firms'planning systems to the requirements (if the proposedapproach to exposure measurement may be expensive.Furthermore, financial theory suggests that hedgingany exposure, however measured, might be useless tostockholders if they had the information to hedge forthemselves. There is no empirical evidence to showthat exchange risk exposure reduces, or that compa-

"The notion that economic exposure and aeeounting exposure are dif-ferent is not new: the origin of the idea is obscure and the references loomany to list. Most textbooks, ci,'., titeman and Stonehill [IO| andShapiro! '^l- rightly emphasize thedislinetion However, they leave theimpression that eeonomic exposure is something which one somehowadds on to accounting exposure. Nor do they offer a summary measureof economic exposure.'" An exiended example which illustrales the requisite simulation analy-sis in a simple one period setting wilh twd states of nature appears inAdler and Dumas |2|. Adding slales presents no particular difficulties.The multi-period extension is moreproblemalic. ll could conceivably bestructured as a (complex) dynamic progrum. Shapiro and Rutenbergll.' l reveals the hazards of such efforts.

ADLER, DUMAS/EXPOSURE TO CURRENCY RISK 49

nies" hedging activities improve, stock values. Theissues addressed here could conceivably be irrelevantfrom this viewpoint. There seem, however, to be twoways to justify costly exchange risk management in thename of the stockholders" interests. Once they are pre-htninariiy identified, exposures can often be wholly orpartly closed by shifting funds across borders throughchannels, other than forward contracts, that also re-duce taxes. Identifying and hedging large exposures,furthermore, can lead to reduced perceptions of defaultrisk, improved bond ratings and lower borrowingrates. When such savings are available, managers maybalance the benefits against the costs.

ReferencesI. M Adler and B. Dumas. "The Long-Term Decisions of

the Multinational Corporatioti." In E. J. Elton and M. J.Gruhcr (eds,). Inrenuitional Capiiol Murkets. Amsterdam.North Hollatid. I*-)??,

the hxposure ul Long-Term" Journal of FInaiuial andcn\hcx I9SO». pp. 973-995.Foreign iixehange Ri.sk Man-Currem\ Risk and the Corpo-

M. Adler atid B. Uiinia.s.Horeigti Curreney BondsQiuiiititative Analysi.s {\^oM. Adler and B. Dumas.

agement." In B. Anil (ed.)

ration. London: Euromoney Publications. 19K(). pp. 145-iss.

4. M, Adler and B. Dunids. "International Portfolio Choieeand Corptiration Finance: A Synthesis," Journal of Fi-nance (June 1983). pp. 925-984.

5. D, P. Baron, "Flexible Exehange Rates. Forward Marketsand the t-cvel of Trade," American Economic Review(Jutic 1976). pp, 253-266.

6. B. Cornell and A. C. Shapiro. "Managing Foreign bx-ehanac Risks.'" Midland Corporate Finance Journal (Fall1983). pp. I6-3L

7. B. Dumas, "The Theory of the trading Firm Revisited,"Journal of Finance {iunc 1978), pp. 1019-1029.

8. M. R. Baker. "The Numeraire Problem and Foreign Ex-ehange Risk." Journcil of Finance (May 1981). pp. 419-426,

9. L. H. Ederington. "'Ihe Hedging Performance ot the NewFutures Markets." Journal of Finance (March 1979). pp.157-170.

10. D, K. Eiteman and A. 1. Stonehill, Muhinaiional BtminessFinance. 3rd edition. Reading. Mass.. Addison-Wesley.1983.

11. S. Laursen and L. Metzler, "Flexible Exchange Rates andthe Theory of Employment," Review of Economics andStati.-^ric.s (November 1950), pp. 281-299.

12. D. E. Logue and G. S, Oldfield. "Managing Foreign As-sets When Foreign Exehange Markets are Efficient. Finan-cuil Management [Summer 1977). pp. 16-22.

L3. W. Poole. "Speculative Prices as Random Walks: AnAnalysis of Ten Titiie Scries of Flexible Exchange Rates."Southern Economic Journal (1968).

14. M. E. Rubinstein. "'I'he Valuation of Uncertain IneomeStreams and the Pricing ol'Options." Bell Journal of Eco-nomics (Autumn 1976). pp. 407^25.

15. A. C, Shapiro and D. P. Rutenberg, "When to HedgeAgainst Devaluation," Management Science (August1974). pp. 1514-1530,

16. A. C, Shdp'no. Mulunational Financial Management. Bos-ton, Allyn & Bacon. 1982.

AppendixThis Appendix offers a general and intuitively ap-

pealing definition of exposure and links it with hedg-ing. Under specific assumptions exposure boils downto a (partial) regression coefficient. Hedging in theamount of the exposure minimizes the variance of thehedged position and leaves a residual randomness thatis independent of exchange rates.

Consider the randotn dollar price. P. ofa risky asseton a given future date. The number of states of nature.K. is finite with known probabilities. In a given state.k. the outcome P is associated with a vector of statevariables. 5;, = {S, SJ^_. which may include ex-change rates if these are called for by some underlyingtheory. Let S, represent the ith state variable. Follow-ing Adler and Dumas |2 | . we may then define:

Exposure of P to S, = EOP/3S,)

This defines exposure as the current expectation,across future states of nature, of the partial sensitivityof P to S,. the effects of all other variables held con-stant. The definition is intuitive and quite general. Forthe exposure to be hedgeable. side bets such as forwardcontracts on S, must be possible and available.

When P and S are jointly normal, exposure as de-fined by (3) becomes the partial regression coefficientof S, in a linear regression of P on 5. This rests on twoprevious results. Rubinstein [14) considered the pric-ing of a contingent claim on P. g(P). in the presence ofa single state variable S. When P and S are jointlynormal, he obtained that:

covlg(P). S] = E[g'(P)] cov(P,S)

Utilizing the satne setting, Adler and Dutnas |2 | ex-tended this result and showed that:

3E[g(Pl|S|

3S var (S)

where bj,| ^ is the regression coefficient of Pon S, in thebivariate case.

The application of these relationships to present

50 FINANCIAL MANAGEMENT/SUMMER 1984

needs is immediate. First, note that in connection withexposure measurement, j:(P) - Psothatg'(P) = 1 inall states of nature. Second, the definition of exposurecan therefore be rewritten in the multivariate case as:

EOP/3S,) - E{ }

as,= cov|S. P|51/var(S,

where b ,,_,, is the partial regression coefficient on S, ina regression of P on S. The extension to jointly lognor-mal random variables is equally immediate, with simi-lar results.

The link between exposure and hedging can easilybe inferred from the futures literature. The requisiteinsight emerges from a modification of Ederington |9 | .

Let P. as before, be the future price of a risky assetwith current price P ,. Assume that there exists a cost-less forward sale contract on state variable S: the cur-rent forward price is F,,. At maturity the random gain orloss on the contract is (F,, - S). Define the expectedretum and variance ofa portfolio consisting of w unitsof P and w, units of the forward contract:

E(R) =var(R) =

E(P -; var(P)

cov(P,S)w

^ , , - S); var(S) - 2 w

Let:

In the futures literature, a = wyw , is called the hedgeratio or the proportion of the spot position that ishedged. In our terminology, the optimal value ofa isthe exposure. Substituting, we rewrite

var{R) = w^ var(P) -I- a-2 w^ a cov(P.S)

^ var(Sl —

The regression coefficient definition emerges fromcomputing the minimum variance hedge, a ':

3var (R)/8a = 2wJ|a var(S) - cov(P.S)l - 0^ a * = cov(P.S)/var(S) - b^,,

In short, when hedging so as to minimize the varianceof the hedged position, one should hedge in the amountof the exposure.

We next show that, after hedging the exposure, theresidual randomness of the hedged position is inde-pendent of S. First, we specify the regression to meas-

ure the exposure:

P = a + bS + ewhere: a - regression constant;

b = regression coefficient, the expo-sure;

e = regression residual: where b) con-struction.

E(e) = 0 = cov(e.S): andE = expectation, denoted by a superbar:

E(X) - X

The linear regression technique produces the followingdefinitions:

a = P - bSb = cov(P.S)/var(S), so that

E(P|Sl = a + bSvadPjS) - b- var(S) -I- var(e), since cov(e,S)

- 0.

The random dollar value. R. ofa position consistingof one dollar's worth of P hedged by the forward saleof b unils of S at the forward rate F,, is:

R - P + b(F,, - S)

The variance oi the hedged position is given by:

var(R) - var(P - bS) _- E(P - bS - P + bSy= E|(P - P) - b(S - S)_[-- E|(P - P)- - 2b(P - P)(S - S)

+ b- (S - S)-l= var(P) - 2bcov(P.S} + b-var(S),

Recall from the definition of the regression parametersthat:

cov(P.S) = b var(S)

b- var(S) = var(P) — var(e).

Hence, after substitution and rearrangement:

var(R) = var(e).What we have shown is that the variance of the

hedged position is equal to the variance of the regres-sion error. Since this residual is hy construcrion inde-pendent vi S. so therefore is R. In other words.

cov(R.S) = E|(P - bS - P + bS)(S - S)l^ cov(P,S) - b var(S)= 0. by virtue of the definition of b.