fha training hope for homeowners december 2008. housing and economic recovery act of 2008 hope for...

TRANSCRIPT

FHA TrainingHope For Homeowners

December 2008

Housing and Economic Recovery Act of 2008

Hope for Homeowners Overview

A temporary program to assist struggling homeowners remain in their homes by refinancing to a safe and affordable FHA insured mortgage

Program oversightSecretaries of Treasury and HUDChairpersons of Board of Governor’s for

Federal Reserve and Board of Directors of the FDIC

Hope for Homeowners Overview (Cont.)

Built on five principles Long term affordability – ability to repay No investor/lender bailout No windfall for borrower’s new equity shared

with FHA Voluntary participation by lenders Restore confidence and liquidity to mortgage

market

Hope for Homeowners Overview (Cont.)

Participation by lenders in program is voluntary Existing lien-holder(s) must accept proceeds of

new FHA loan as satisfaction of all existing liens All penalties and fees related to default or

delinquency must be waived or forgiven On existing loans By existing lenders

Hope for Homeowners Program Guidelines

Implementation date October 1, 2008

Expiration date September 30, 2011 Maximum loan-to-value

96.5% if debt ratios </= 31%/43%90% if debt ratios > 31%/43%

Includes Up-Front MIP Includes closing costs

6

Hope for Homeowners Program Guidelines (Cont.)

Existing mortgage must have originated on or before January 1, 2008

Owner-occupant only Borrower may not own or have interest in any other

property Second homes Rental property Co-borrower or co-signer on other property

Hope for Homeowners Program Guidelines (Cont.)

Current housing debt must be > 31% as of 3/1/08 New FHA-insured mortgage may not exceed

$550,400 (132% of 2007 conforming loan limit) New FHA-insured mortgage must be a fixed rate New FHA-insured mortgage may be 30 or 40 year

term based on affordability

7

8

Hope for Homeowners Program Guidelines (Cont.)

Debt ratios may not exceed 96.5% Loan To Value

31% Housing (PITI & Monthly Mortgage Insurance)

43% All Debt (PITI, MMI, and consumer debt)

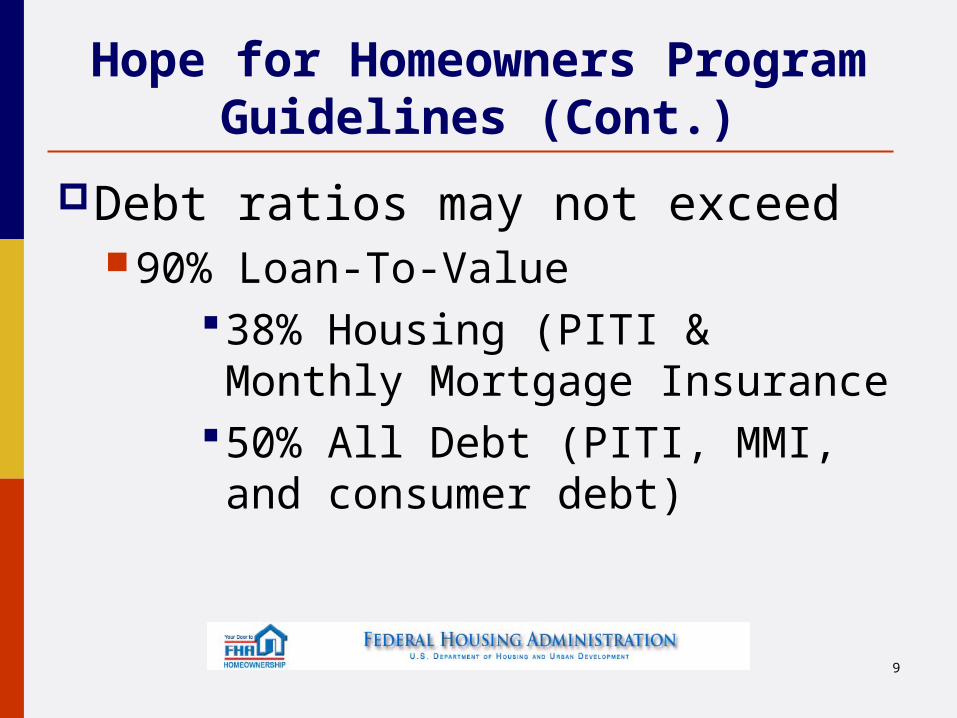

Hope for Homeowners Program Guidelines (Cont.)

Debt ratios may not exceed 90% Loan-To-Value

38% Housing (PITI & Monthly Mortgage Insurance

50% All Debt (PITI, MMI, and consumer debt)

9

Hope for Homeowners Program Guidelines (Cont.)

Compensating factors not applicable 96.5 or 90% Loan-to-Value

Board has option to amend Already amended once

90% maximum to 96.5 Based on debt ratios

Board may amend again in future

10

11

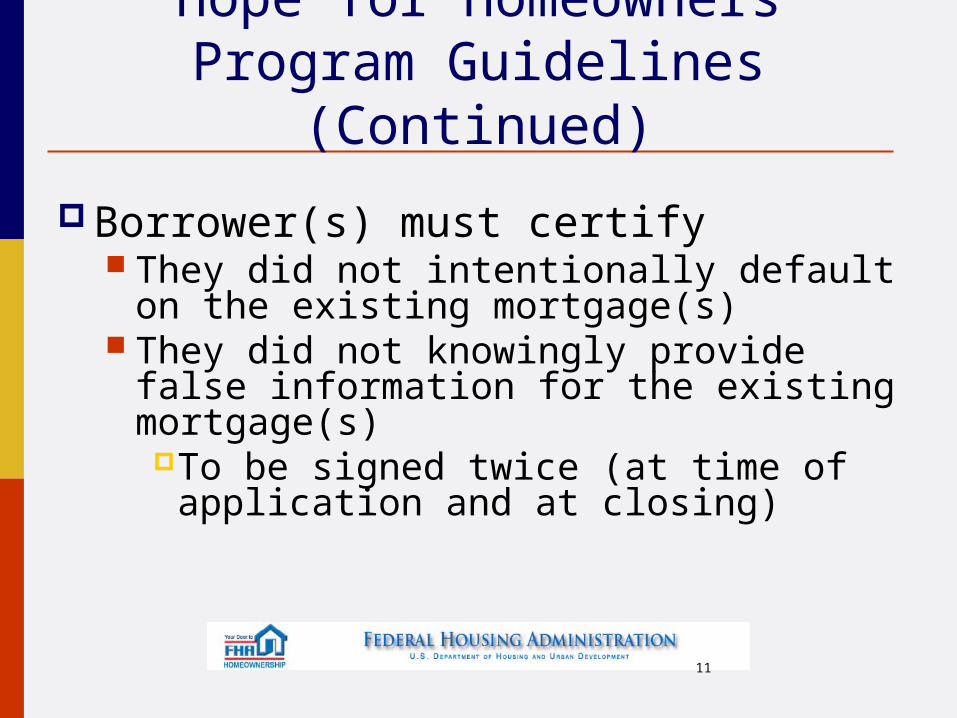

Hope for Homeowners Program Guidelines (Continued)

Borrower(s) must certify They did not intentionally default on the existing

mortgage(s) They did not knowingly provide false information

for the existing mortgage(s)To be signed twice (at time of application and at

closing)

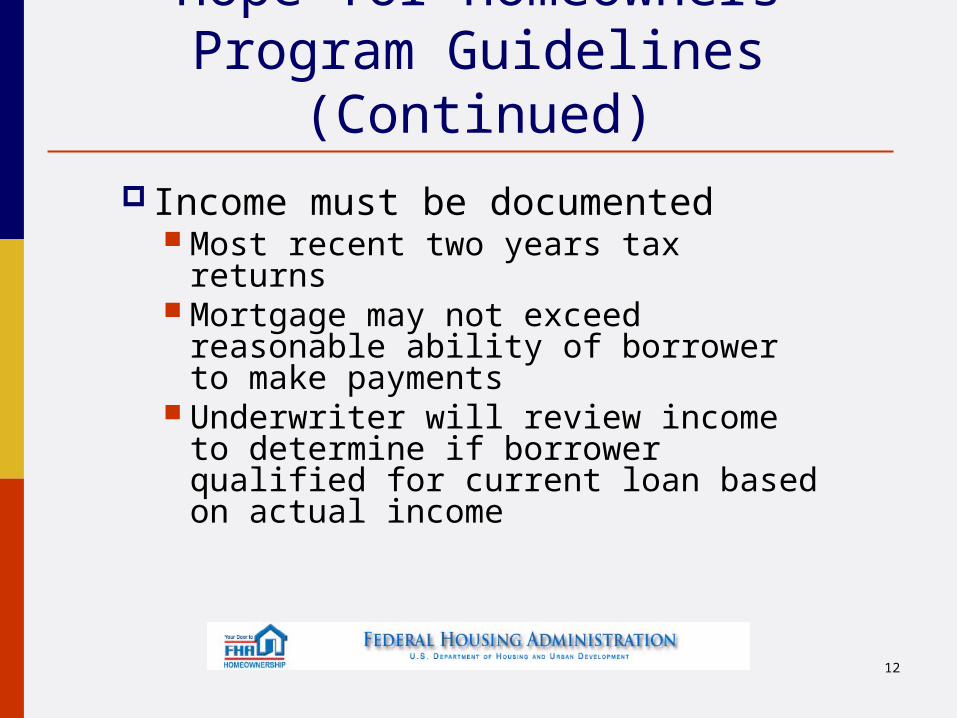

Hope for Homeowners Program Guidelines (Continued)

Income must be documented Most recent two years tax returns Mortgage may not exceed reasonable

ability of borrower to make payments Underwriter will review income to

determine if borrower qualified for current loan based on actual income

12

13

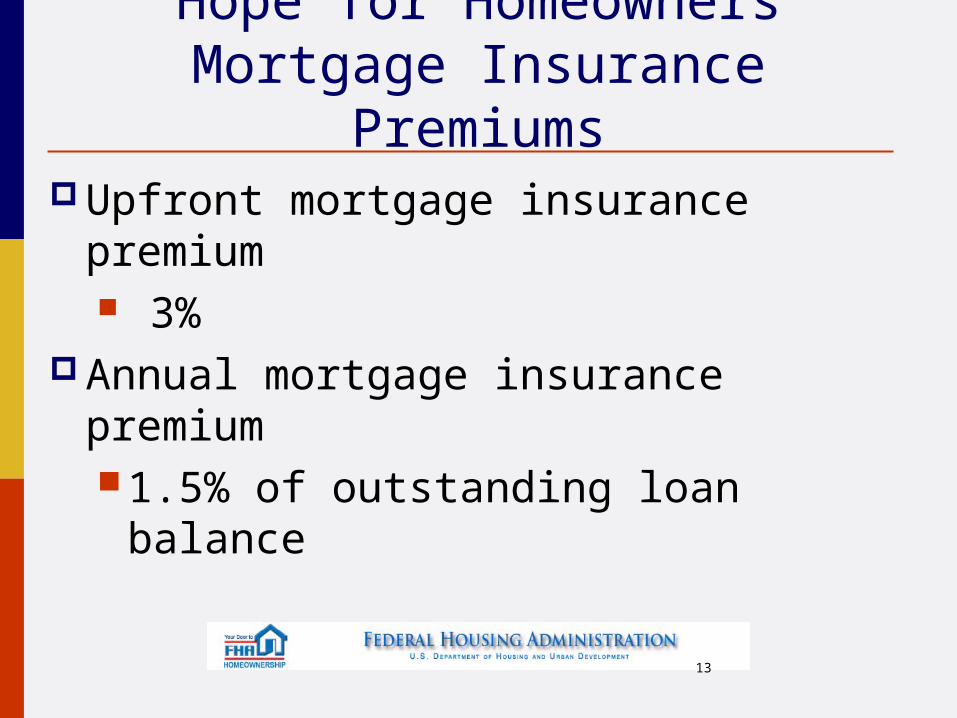

Hope for Homeowners Mortgage Insurance Premiums

Upfront mortgage insurance premium 3%

Annual mortgage insurance premium 1.5% of outstanding loan balance

14

Hope for HomeownersShared Equity with FHA

FHA shares initial equity 10% initial equity is 100% to FHA

Decreases 10% per year throught the 5th yearFHA then holds 50% of initial 10% equity

until paid offBorrower may be able to buy out this initial

equity at some time in the future, but no sooner than 12 months

FHA will not subordinate to any future subordinate financing

Hope for Homeowners Shared Appreciation With FHA

As a condition of the H4H loan FHA shares in all future appreciation Share is 50/50 between FHA and

borrowerDoes not change over timeNo amount capsShared appreciation cannot be paid

off except Sale or disposition of property

15

Hope for Homeowners Shared Appreciation With FHA

Borrower may be able to borrower 50% of their 50% appreciation plus a percentage of any capital improvements

No earlier than five years from the date of the H4H mortgage

FHA will not subordinate to any future subordinate financing

16

Hope for Homeowners Shared Appreciation With FHA

Current junior lienholders only may also be able to share in future appreciation Board established standards for sharing

future appreciation Induce subordinate liens to exit the

property now so borrower can retain home

Ranges from 9% to 12% on the dollar Paid to junior lienholder in future

At time of sale or disposition of property Board may amend

17

Final Notes on Hope for Homeowners

This is a loss mitigation tool only Originators can only earn a maximum of

1% origination fee No miscellaneous fees allowed

Administration, YSP, underwriting, processing, etc.

Borrower may be subject to tax liability Debt forgiveness

18

Final Notes on Hope for Homeowners Lender must evidence borrower made first

payment from own funds before FHA will insure Cannot be funded at time of close and held

by escrow FHA will not pay claim in the event of first

payment default Ginnie Mae pool to sell loan to recently

established Rates expected to be 8.5% - 9%

19