#fintech regulation overview co-presented

TRANSCRIPT

FinTech and Regulation:

Recent Developments and Outlook

Professor Douglas W. Arner

Janos Barberis

Asian Institute of International Financial Law

Faculty of Law

University of Hong Kong

26 March

2015

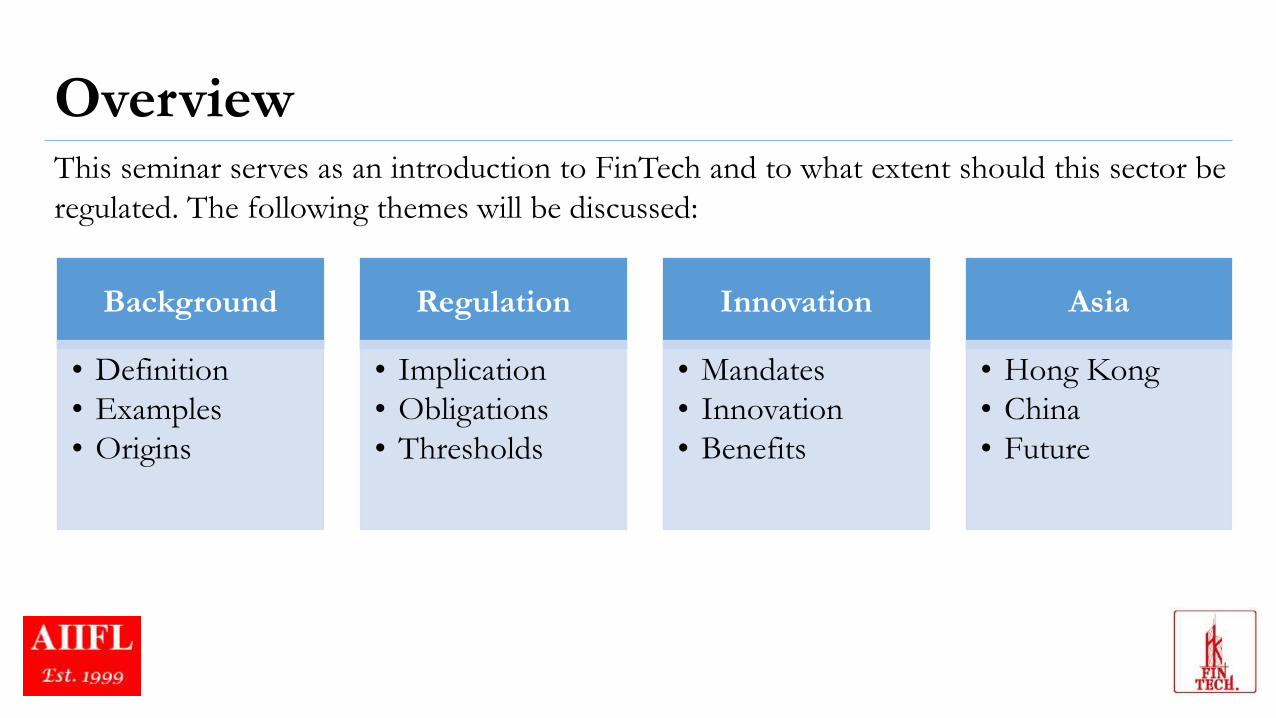

OverviewThis seminar serves as an introduction to FinTech and to what extent should this sector be

regulated. The following themes will be discussed:

Background

• Definition

• Examples

• Origins

Regulation

• Implication

• Obligations

• Thresholds

Innovation

• Mandates

• Innovation

• Benefits

Asia

• Hong Kong

• China

• Future

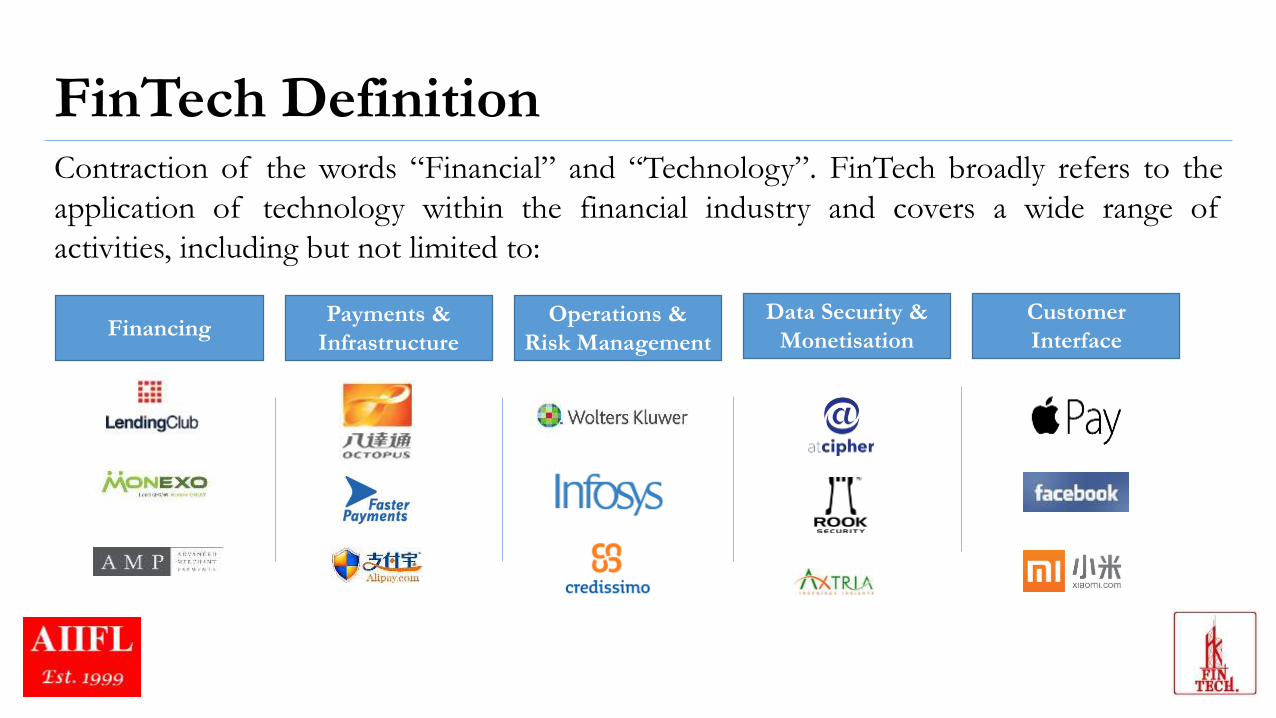

FinTech DefinitionContraction of the words “Financial” and “Technology”. FinTech broadly refers to the

application of technology within the financial industry and covers a wide range of

activities, including but not limited to:

FinancingPayments &

Infrastructure

Operations &

Risk Management

Data Security &

Monetisation

Customer

Interface

FinTech HistoryBanks have historically been the largest spender on IT their budget dedicated to IT keeps

increasing (e.g.+4% in 2014). However, today we see a new direction of the digitization

paradigm (e.g. direct consumer solutions):

• 1967: Barclays deploys first Automated Teller Machine (ATM)

• 1971: NASQAQ is created, triggering electronic trading

• 1989: Program trading starts to be used by financial institutions

• 1990: Value at Risk (VaR) model used for automatic risk pricing and portfolios

• 1997: The Octopus card is launched in Hong Kong

• 2000: Introduction of Dark Pools and High Frequency Trading

• 2005: Zoopa creates the UK first Peer-to-Peer platform

2008: A Game Changer?The 2008 global financial crisis had a catalysing effect on the growth of the FinTech

sector due to a series of factors:

• Financing gap: Contraction of the interbank market (e.g. trust issues) and increase in

regulatory capital to be held against loan portfolio (e.g. additional +US$150bn set aside)

• Operational cost reduction: Downsizing teams (e.g. IT & Back/Middle office) plus using

technology to reduce costs (e.g. straight-trough processing)

• Compliance cost increase: Increasing set of new and additional compliance

obligations for banks, diverting resources and creating chilingl effect towards

innovation

FinTech OpportunitiesThe shock experienced by the financial sector is being leveraged by new FinTech start-ups

that benefited from a set of factors:

• Human capital: Staff within financial sector that had necessary expertise and

experience left industry to join or build FinTech companies

• Public perception: Growing distrust of formal financial institutions from the public

allowed new entrants to emerge (e.g. UK challenger banks, P2P or FX platforms)

• Technology: Access to technology democratised due to new pricing models (e.g.

Software as a Service (SaaS)) removed high upfront cost that acted as barrier to entry

Financial RegulationDue to the breadth of the FinTech sector, it is hard to talk about “FinTech Regulation”

per-se. Better to break down high-level approaches (e.g. risk- or product-based) and

complement them with a sub-set of specific regulations (e.g. payments, anti-money laundering).

Broadly speaking, financial regulators have 4 key mandates:

Financial

Stability

Prudential

Regulation

Conduct &

Fairness

Competition &

Development

Regulatory ImplicationsThere is an emergence of new players (e.g. start-ups) alongside the existing large companies

that were already in the space (e.g. core banking vendors). However, unlike large IT vendors,

certain start-ups use technology to disintermediate banks and directly propose their

services or products to consumers.

This creates a set of questions:

• Increasingly a blurred line: Who can/should provide financial services or products?

• How to balance start-up low cost models and agility benefits with compliance costs?

• How can regulation cover an increasing number of new business models and match

speed of innovation cycles?

Regulatory ThresholdA problem with new emerging FinTech companies is that they have limited track records

regarding their business (e.g. risk management, liquidity and profitability) and a difficult time to

identify what are their obligations (e.g. applicable regulations or licences).

For regulators, these early-stage companies represent a limited prudential & consumer risk.

However, exponential company growth can create a “risk blind spot”. Additionally,

frequent failures or fraud can impact market or investor confidence (e.g. Mycoin in Hong

Kong), which are also mandates for regulators (e.g. HKMA)

Too Small

to Care

Too Big

to Fail

Too Large

to IgnoreTacit acceptance Licensing obligation

Risk Blind-SpotUsing company size (e.g. small, large, systemic) as a way to evaluate risk is not adequate, given

inter-connectedness of financial markets and rapid up-take of certain financial products.

Today, small companies’ path to become systemic is not linear but exponential:

• US (2010): Small mutual fund group Waddell & Reed suspected of being responsible

for the S&P 500 flash crash (e.g. 10% fall due to algorithm trading chain effect)

• China (2014): Third party mobile payment market reached 1,433 trillion yuan, a

+400% increase compared to 278 trillion exchanged in 2013

• China (2014): Yu’e Bao, a money market fund part of Ant Financial Group (Alibaba)

holds over US$ 90billion (e.g. 4th largest in the world) in just 10 months after its creation

New RisksNew business models and delivery mechanisms create new sets of risks:

• P2P platform capital buffers during credit cycle change or interest rate liberalisation

2.5% deposits vs 15% P2P lenders (e.g. warning over 1’250 platforms in China)

• Money Market Fund (MMF) maturity mismatch enhanced by technology

Technology facilitation of on-demand redemptions (e.g. “mobile app bank run”)

• Existing risks even for platforms that are matchmakers instead on intermediaries

Removal of CHF/EUR peg led to counterparty, settlement and market risks

• Scalability of process, policies and risk management frameworks

Particularly for companies with exponential growth (e.g. loan origination quality)

Data add-valueThe increasing use of technology within the financial sector also offers opportunities for

regulators to better perform their roles. The UK FCA has started to evaluate the benefits

provided by the blockchain technology and there are also other examples:

• Smart contracts: Reducing costs and trust issues around contractual performance

• P2P lending: Providing real-time visualisation of geographical spread of credit risk

• Blockchain: Ensuring Multilateral Trading Facilities (MTF) obligations under MiFID

• E-money: Limiting the extent of money laundering issues with cash transactions

• Data transparency: Allowing regulators to directly audit financial institutions

Regulatory InnovationSince 2008 national and international regulators have been focused on drafting and

implementing re-active regulations covering the causes of the global financial crisis to

avoid its repetition. However, the increased layering of regulations and compliance cost

also allowed new FinTech start-ups to emerge.

There is nonetheless a set of pro-active regulations that were forward-looking and have

allowed for innovative businesses propositions to emerge.

• US: Jump-start Our Business Start-up Act 2012 (JOBS Act) Alternative

financing

• EU: Payment System Directive 2008 Real-time payments

• UK: Small Business, Enterprise and Employment Bill Loan referral to P2P

Amending MandatesThe regulatory threshold approach has its limits since it can prevent regulators from

engaging early-on with new FinTech companies.

In the UK, the Financial Conduct Authority has under the Financial Services Act 2012 a

new mandate whereby it should be ‘promoting effective competition in the interest of

consumers in the market for regulated financial services’

As a result, this pushes the FCA to engage with even earlier-stage companies, provided

that they can stimulate competition and have a positive impact on consumers (e.g. better

services, cost reductions).

Institutional ChangeHaving regulatory supervision conducted by specialist bodies focused on products appears

inadequate when looking at the rate at which technological progress occurs. Indeed, this

can create grey areas as to what is the regulatory body on which a specific business falls

(e.g. insurance companies performing banking activities in the US pre-2007).

Additionally, the use of personal data to tailor pricing levels or risk thresholds of

consumers means that there will be an increasing granularity of products and services

provided.

Thus, financial innovation driven by technology must be preferably overseen in the

context of a twin peak model such as the one used in the UK. This would be particularly

relevant in Hong Kong and China that have more a sectorial approach.

Asian OpportunitiesThe growth potential of the FinTech sector in Asia is substantial, given the physical

financial infrastructure gap and limited legacy behaviour of consumers. Additionally, the

level of development of the financial services industry is comparatively less mature than

the West.

The FinTech sector offers an opportunity for governments to infuse innovation within

their traditional financial sector by driving competition and weeding-out inefficiencies.

However, liberalisation and increased competition are only gradually introduced (e.g.

touching the stones to cross the river) due to the highly political, social and economic impact of

financial sector.

Asian Fragmentation

APAC

25 Jurisdictions

25 sets of

regulations

25 sets of

infrastructures25 sets of

behaviours

Europe:

27 Jurisdictions

Harmonized Regulation

Homogeneous Market

USA:

51 Jurisdictions

National Regulation

Homogeneous Market

Vs Vs

However, unlike the US and EU markets that are more homogeneous in their

composition, the Asian market remains fragmented, limiting the rapid scalability of certain

FinTech businesses.

China’s ApproachBalancing innovation and development.

China has a very rapidly changing environment, recent news:

• Provide backdoor to IT systems of financial institutions

• 1’250 credit rating alert on 1’250 P2P platforms

• Consideration of regulatory capital requirements (e.g. US$3.5million) for P2P platforms

Hong Kong ContextHong Kong is a major international financial centre, located in the heart of the world’s

largest opportunity for FinTech growth:

Hong Kong

4.3m HNWIs

600m Digital Bank Customers

28% world middle class

Government Support

5h flight

+ 13% p.a

+ 300% by 2020

25th Feb 2015 budget speech

66% by 2030

1st Financial Centre in Asia – 3rd in world

Hong Kong OpportunitiesGiven its location, expertise and role as a financial Centre Hong Kong can play a key role

in some of these opportunities:

FinTech FinancingPayments &

InfrastructureOperations &

Risk ManagementData Security &Monetisation

Early & AngelVCListingHK + Mainland

RMB InternationalizationMainland in-outConnectsMutual RecognitionASEANAPEC

RegulationIT – RegionalInternational HQ

Data ProcessingData MiningData Storage

Open Questions

• What is Hong Kong’s role in China’s financial transition, given its role as a FinTech hub

and how will this shape the city’s future as a financial center?

• Can Hong Kong establish its FinTech leadership by creating a set of regulations or

mutual recognition regimes allowing the scalability of certain products and services?

• Can regulators set a framework that allows the low-cost business model of FinTech

companies to co-exist with the perceived costly financial regulation?

• What are the regulatory consequences of China leapfrogging the world by delivering

financial services and products on a scale that was never done before?

The emergence of the FinTech sector in Hong Kong and its recent establishment as a

FinTech hub opens a series of questions:

Q&A

Thank you!

Douglas Arner

Janos Barberis