fixed income - 2 the financial institute of israel zvi wiener 02-588-3049 mswiener/zvi.html fixed...

Post on 21-Dec-2015

215 views

TRANSCRIPT

Fixed Income - 2 http://www.tfii.orgThe Financial

Institute of Israel

Zvi Wiener

02-588-3049http://pluto.mscc.huji.ac.il/~mswiener/zvi.html

Fixed Income 2

Zvi Wiener FI - 2 slide 2

Plan FI-2

• Example of Duration and Convexity

• Treasuries

• Agencies

• Corporate

• MunicipalsThe Treasury Securities Markets: Overview and Recent Developments, by D. Dupont and B. Sack, Federal Reserve Bulletin, Dec-99.

Zvi Wiener FI - 2 slide 3

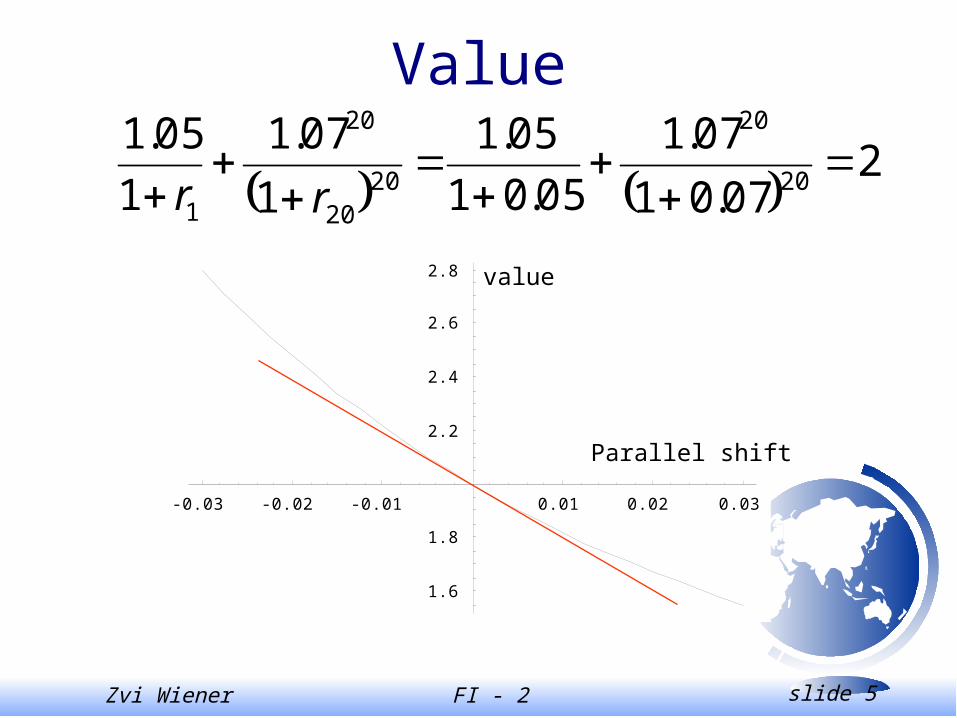

Example

Portfolio consists of $1M of a bond with duration of 1 year and $1M worth of a bond with duration of 20 years.

What is the duration of the portfolio?

Zvi Wiener FI - 2 slide 4

Rough calculationDuration of the first bond is 1 year, of the second bond is 20 years.

This means that when IR go 1% up we will lose 1% of the first bond and 20% of the second.

All together we will lose 10.5% of the portfolio.

The duration is (roughly) 10.5 years.

Zvi Wiener FI - 2 slide 5

-0.03 -0.02 -0.01 0.01 0.02 0.03

1.6

1.8

2.2

2.4

2.6

2.8

Value

2

07.01

07.1

05.01

05.1

1

07.1

1

05.120

20

2020

20

1

rr

Parallel shift

value

Zvi Wiener FI - 2 slide 6

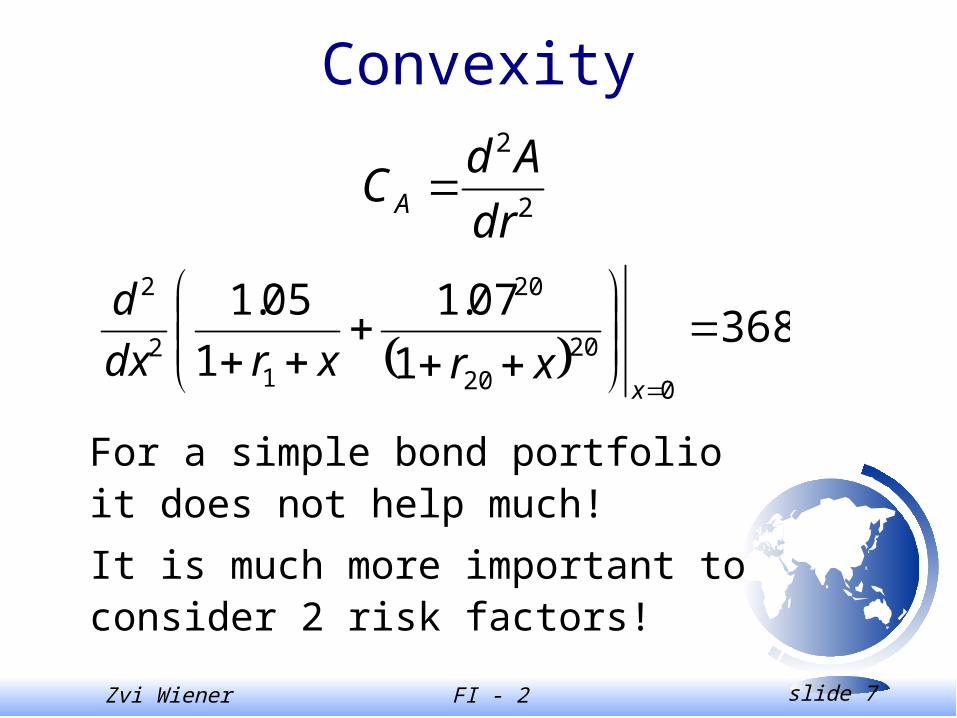

Duration

8212.907.1

20

05.1

1

2

1

8212.9

1

07.1

1

05.1

2

1

0

2020

20

1

xxrxrdx

d

dr

dA

ADA

1

BA

BD

BA

ADD BA

BA

Zvi Wiener FI - 2 slide 7

Convexity

368

1

07.1

1

05.1

0

2020

20

12

2

x

xrxrdx

d

2

2

dr

AdCA

For a simple bond portfolio it does not help much!

It is much more important to consider 2 risk factors!

Zvi Wiener FI - 2 slide 8

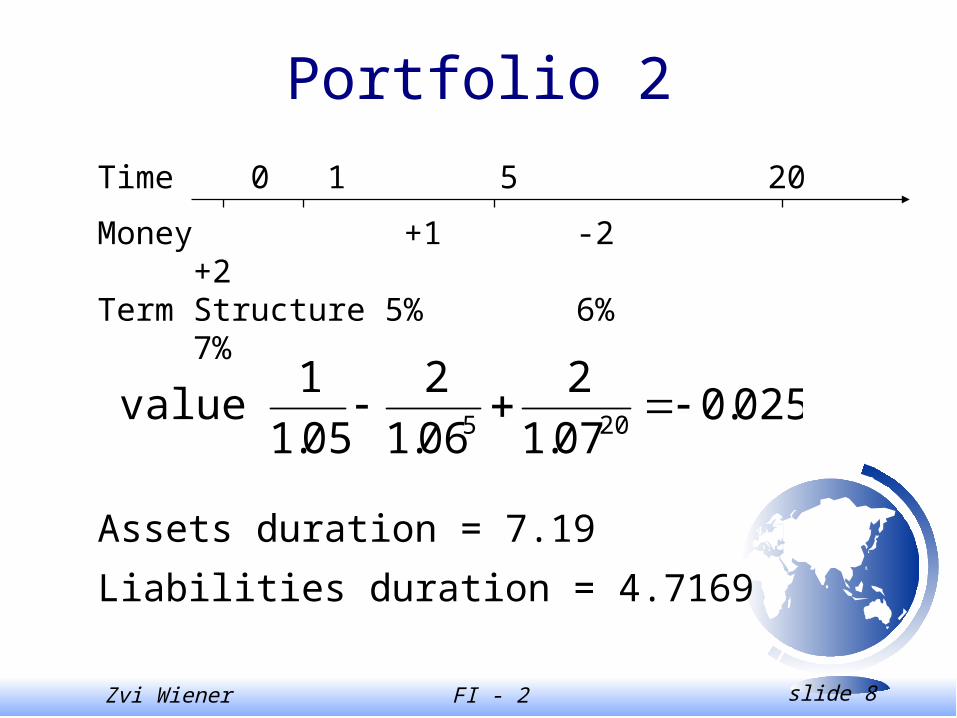

Portfolio 2

value

Money +1 -2 +2Term Structure 5% 6% 7%

Time 0 1 5 20

025.007.1

2

06.1

2

05.1

1205

Assets duration = 7.19

Liabilities duration = 4.7169

Zvi Wiener FI - 2 slide 9

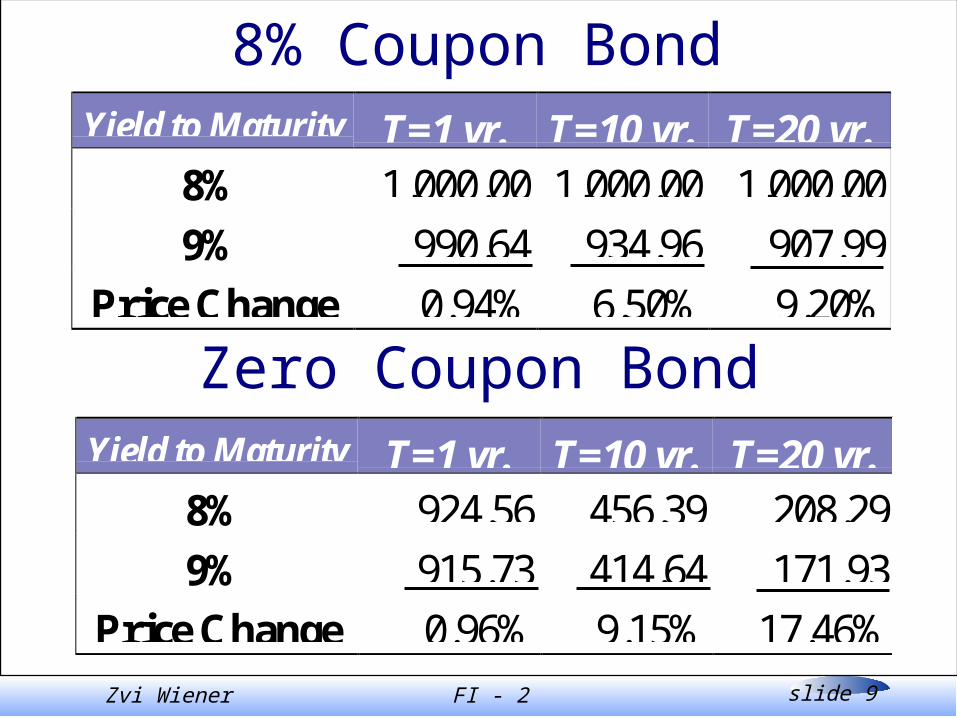

8% Coupon BondYield to Maturity T=1 yr. T=10 yr. T=20 yr.

8% 1,000.00 1,000.00 1,000.00

9% 990.64 934.96 907.99

Price Change 0.94% 6.50% 9.20%

Yield to Maturity T=1 yr. T=10 yr. T=20 yr.8% 924.56 456.39 208.29

9% 915.73 414.64 171.93

Price Change 0.96% 9.15% 17.46%

Zero Coupon Bond

Zvi Wiener FI - 2 slide 10

Macaulay Duration(1)

Time untilpayment

(in Years)

(2)

Payment

(3)Payment

Discountedat 5%

(4)

Weight

(5)column (1)multiplied

by (4)Bond A 0.5 $40 $38.095 0.0395 0.01988% 1.0 $40 $36.281 0.0376 0.0376

1.5 $40 $34.553 0.0358 0.05372.0 $1,040 $855.611 0.8871 1.7742

Sum: $964.540 1.000 1.8853

Bond B 0.5-1.5 0 $0 0 0zero 2.0 $1,000 $822.70 1 2Sum $822.70 1 2

Zvi Wiener FI - 2 slide 11

Understanding of Duration/Convexity

What happens with duration when a coupon is paid?

How does convexity of a callable bond depend on interest rate?

How does convexity of a puttable bond depend on interest rate?

Zvi Wiener FI - 2 slide 12

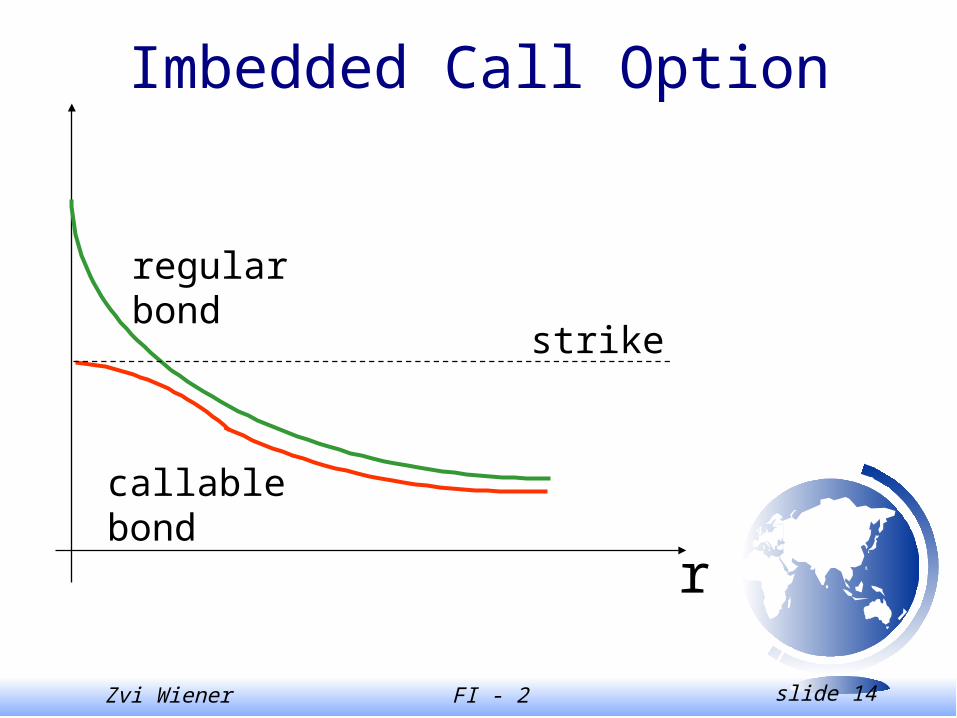

Callable bond

The buyer of a callable bond has written an option to the issuer to call the bond back.

Rationally this should be done when …

Interest rate fall and the debt issuer can refinance at a lower rate.

Zvi Wiener FI - 2 slide 13

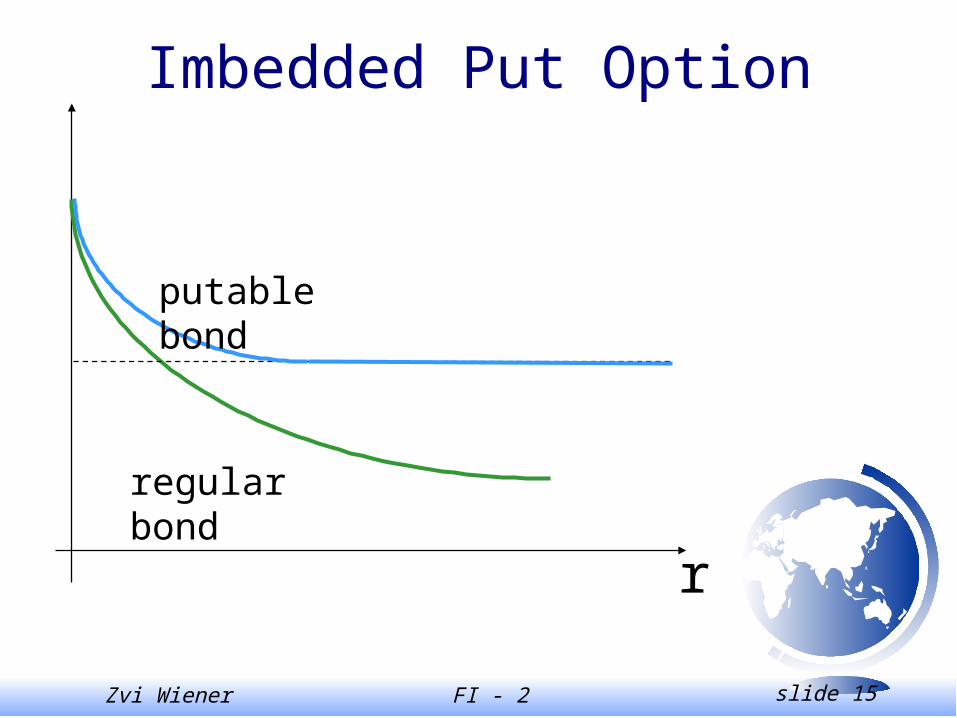

Puttable bond

The buyer of a such a bond can request the loan to be returned.

The rational strategy is to exercise this option when interest rates are high enough to provide an interesting alternative.

Zvi Wiener FI - 2 slide 14

Imbedded Call Option

r

regular bond

callable bond

strike

Zvi Wiener FI - 2 slide 15

Imbedded Put Option

r

regular bond

putable bond

Zvi Wiener FI - 2 slide 16

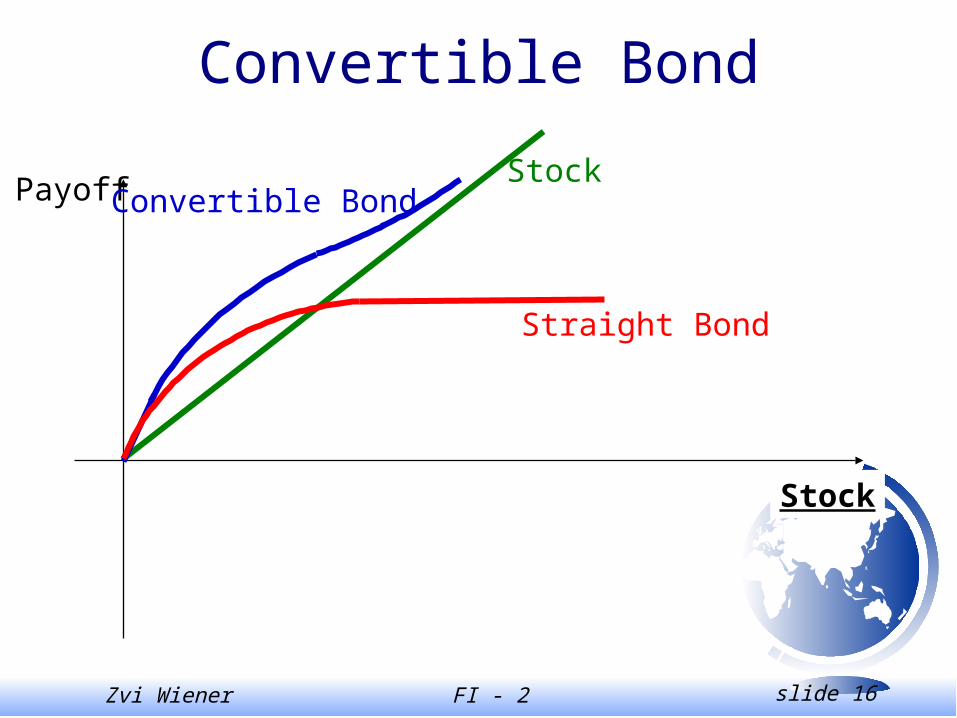

Convertible Bond

PayoffStock

Stock

Convertible Bond

Straight Bond

Zvi Wiener FI - 2 slide 17

Timing of exercise

• European

• American

• Bermudian

• Lock up time

Zvi Wiener FI - 2 slide 18

Passive Bond Management

Passive management takes bond prices as fairly set and seeks to control only the risk of the fixed-income portfolio.

• Indexing strategy– attempts to replicate a bond index

• Immunization– used to tailor the risk to specific needs (insurance companies, pension funds)

Zvi Wiener FI - 2 slide 19

Bond-Index Funds

Similar to stock indexing.

Major indices: Lehman Brothers, Merill Lynch, Salomon Brothers.

Include: government, corporate, mortgage-backed, Yankee bonds (dollar denominated, SEC registered bonds of foreign issuers, sold in the US).

Zvi Wiener FI - 2 slide 20

Bond-Index Funds

Properties:

many issues

not all are liquid

replacement of maturing issues

Tracking error is a good measurement of performance. According to Salomon Bros. With $100M one can track the index within 4bp. tracking error per month.

Zvi Wiener FI - 2 slide 21

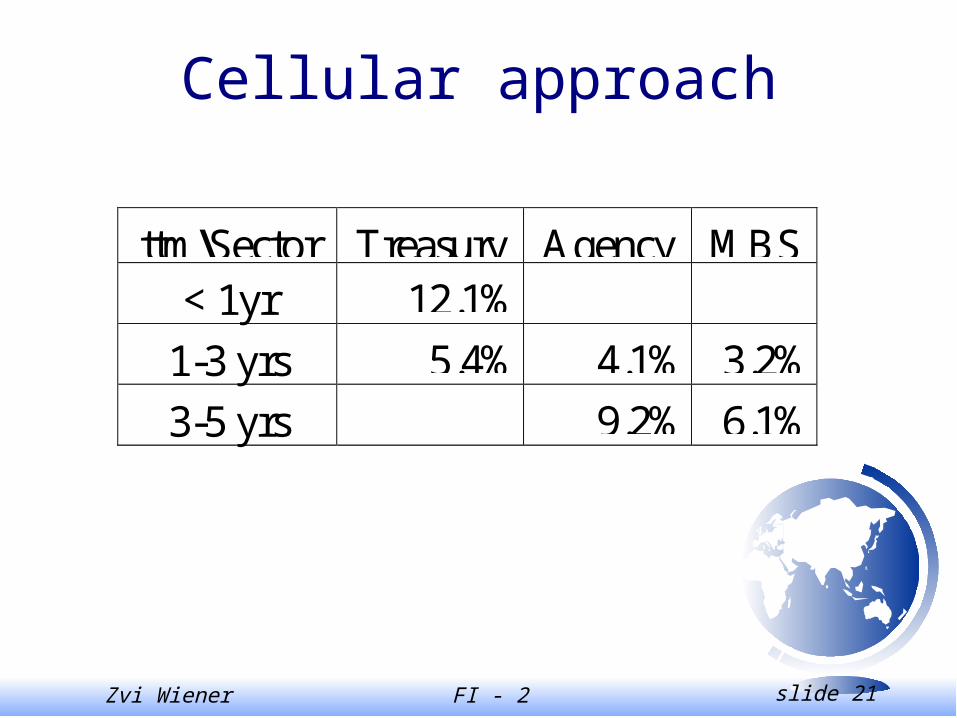

Cellular approach

ttm\Sector Treasury Agency MBS< 1yr 12.1%

1-3 yrs 5.4% 4.1% 3.2%

3-5 yrs 9.2% 6.1%

Zvi Wiener FI - 2 slide 22

Immunization

Immunization techniques refer to strategies used by investors to shield their overall financial status from exposure to interest rate fluctuations.

Zvi Wiener FI - 2 slide 23

Net Worth Immunization

Banks and thrifts have a natural mismatch between assets and liabilities. Liabilities are primarily short-term deposits (low duration), assets are typically loans or mortgages (higher duration).

When will banks lose money, when IR increase or decline?

Zvi Wiener FI - 2 slide 24

Gap Management

ARM are used to reduce duration of bank portfolios.

Other derivative securities can be used.

Capital requirement on duration (exposure).

Basic idea:

to match duration of assets and liabilities.

Zvi Wiener FI - 2 slide 25

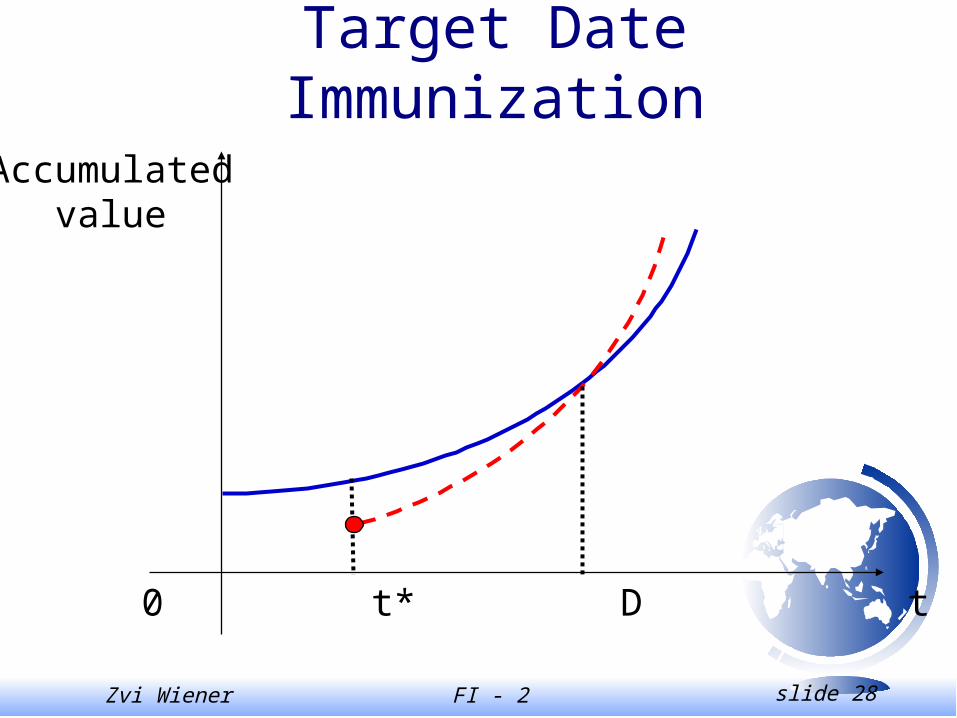

Target Date Immunization

Important for pension funds and insurances.

Price risk and reinvestment risk.

What is the correlation between them?

Zvi Wiener FI - 2 slide 26

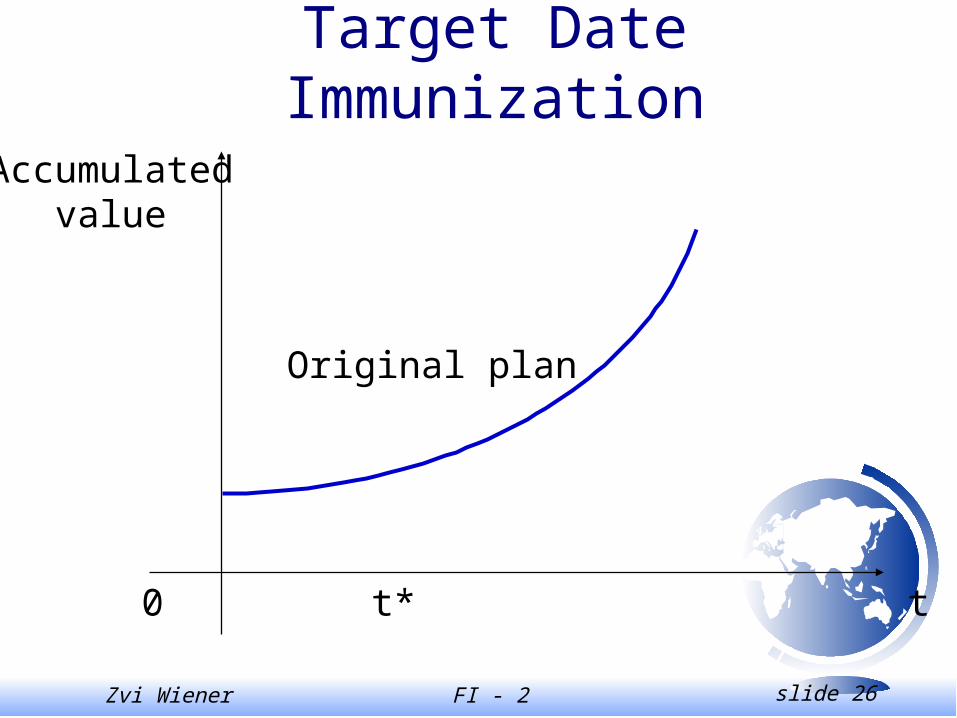

Target Date Immunization

Accumulatedvalue

0 t* t

Original plan

Zvi Wiener FI - 2 slide 27

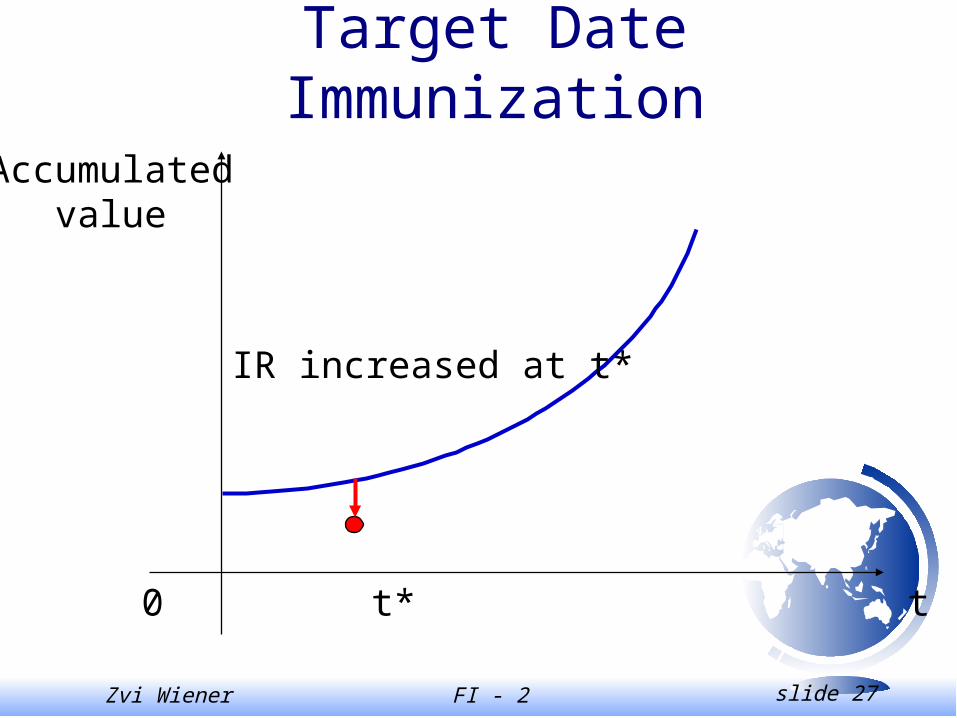

Target Date Immunization

Accumulatedvalue

0 t* t

IR increased at t*

Zvi Wiener FI - 2 slide 28

Target Date Immunization

Accumulatedvalue

0 t* D t

Zvi Wiener FI - 2 slide 29

Target Date Immunization

Accumulatedvalue

0 t* D t

Continuous rebalancingcan keep the terminal value

unchanged

Zvi Wiener FI - 2 slide 30

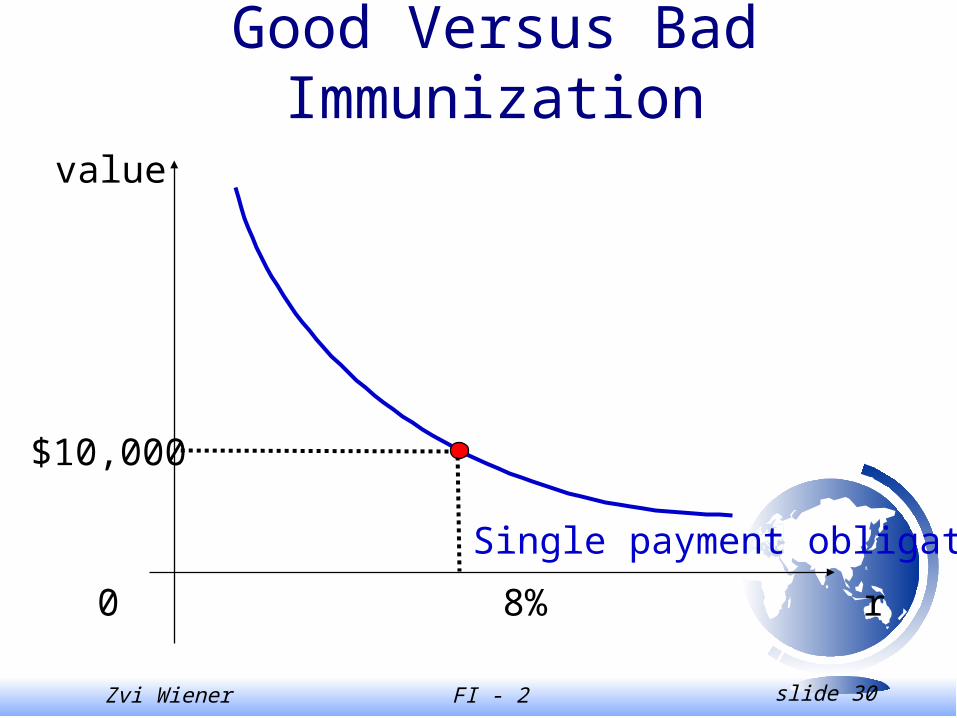

Good Versus Bad Immunization

value

0 8% r

Single payment obligation

$10,000

Zvi Wiener FI - 2 slide 31

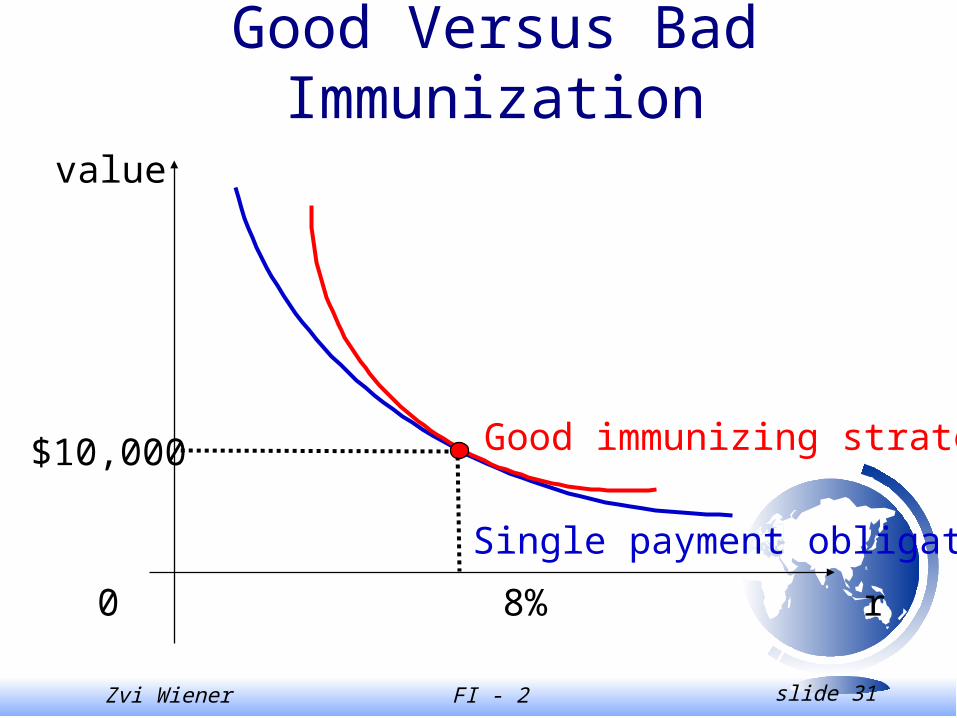

Good Versus Bad Immunization

value

0 8% r

Single payment obligation

Good immunizing strategy$10,000

Zvi Wiener FI - 2 slide 32

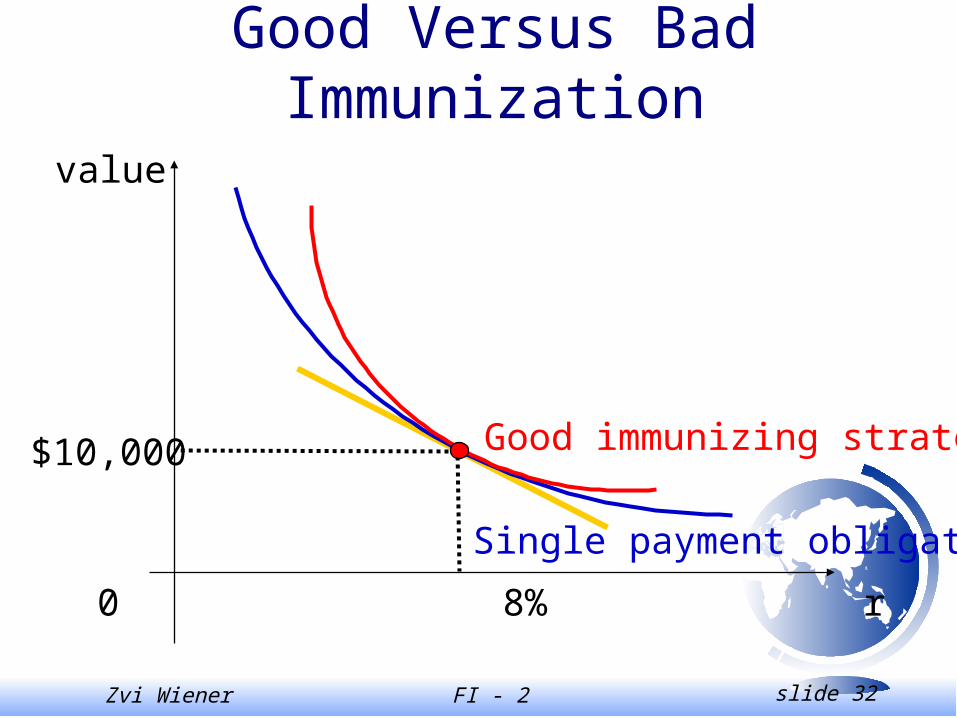

Good Versus Bad Immunization

value

0 8% r

Single payment obligation

Good immunizing strategy$10,000

Zvi Wiener FI - 2 slide 33

Good Versus Bad Immunization

value

0 8% r

Single payment obligation

Good immunizing strategy$10,000

Bad immunizing strategy

Zvi Wiener FI - 2 slide 34

Standard Immunization

Is very useful but is based on the assumption of the flat term structure. Often a higher order immunization is used (convexity, etc.).

Another reason for goal oriented mutual funds

(retirement, education, housing, medical expenses).

Zvi Wiener FI - 2 slide 35

Cash Flow Matching and Dedication

Is a very reasonable strategy, but not always realizable.

Uncertainty of payments.

Lack of perfect match

Saving on transaction fees.

Zvi Wiener FI - 2 slide 36

Active Bond Management

Mainly speculative approach based on ability to predict IR or credit enhancement or market imperfections (identifying mispriced loans).

Zvi Wiener FI - 2 slide 37

Substitution Swap

Exchange of one bond for a very similar bond.

Motivation: belief that one of them is mispriced.

Example: 20-yr, 9% coupon Ford Motor bond callable after 5 years at $1,050 versus a 9% coupon Chrysler bond with 20 yr to maturity.

Zvi Wiener FI - 2 slide 38

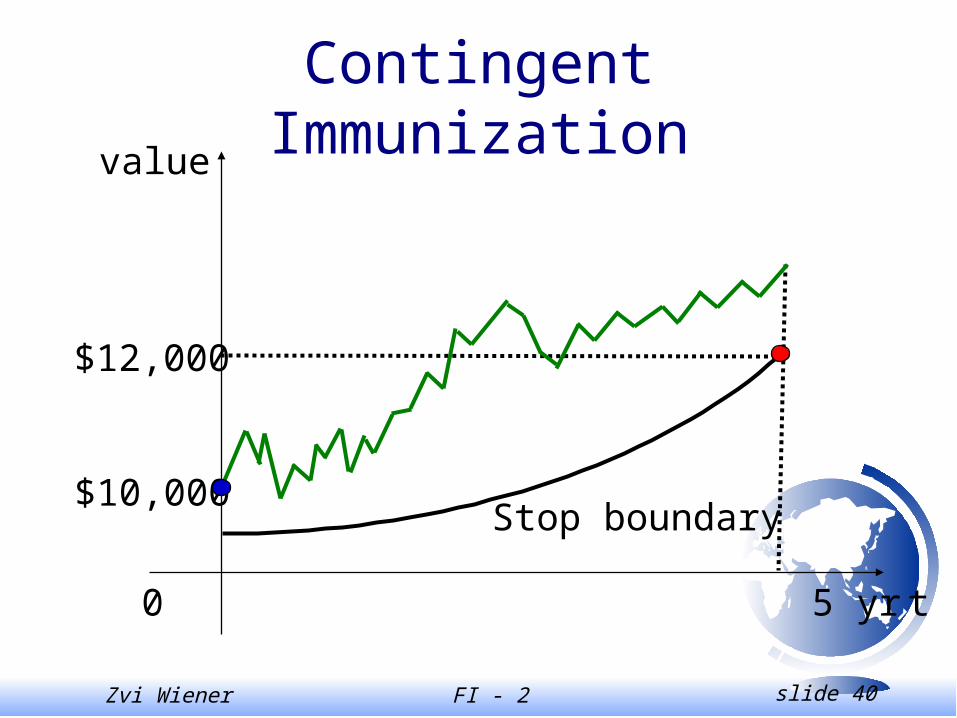

Contingent Immunization

0 5 yr t

value

$10,000

$12,000

Zvi Wiener FI - 2 slide 39

Contingent Immunization

0 5 yr t

value

$10,000

$12,000

Stop boundary

Zvi Wiener FI - 2 slide 40

Contingent Immunization

0 5 yr t

value

$10,000

$12,000

Stop boundary

Zvi Wiener FI - 2 slide 41

Contingent Immunization

0 5 yr t

value

$10,000

$12,000

Stop boundary

Zvi Wiener FI - 2 slide 42

Interest Rate Swap

One of the major fixed-income tools.

Example: 6m LIBOR versus 7% fixed.

Exchange of net cash flows.

Risk involved: IR risk, default risk (small).

Why the default risk on IR swaps is small?

Zvi Wiener FI - 2 slide 43

Interest Rate Swap

Company A Company BSwap dealer

6.95% 7.05%

LIBOR LIBOR

No need in an actual loan.Can be used as a speculative tool or for hedging.

Zvi Wiener FI - 2 slide 44

Currency Swap

A similar exchange of two loans in different currencies.

Subject to a higher default risk, because of the principal.

Is useful for international companies to hedge currency risk.

Zvi Wiener FI - 2 slide 45

The Treasuries Securities Market

US Treasury debt $3.6Trillion

daily transactions: $190B

yields are viewed as benchmarks

1776, first US issue (Revolutionary War)

Increase during the Civil war, WW1,

tripled during the great depression

exploded during WW2.

Zvi Wiener FI - 2 slide 46

Types of Treasuries securities

• $3.2T - marketable– Bills - up to one year

– Notes 1-10 years when issued

– Bonds longer then 10 years

• 57% are notes, 20% bills and 20% bonds.

• Some are callable (by the Treasury)

• 97% are nominal

Zvi Wiener FI - 2 slide 47

Nonmarketable securities

• Government account series (83%)

• State and Local Government Series (7%)

• saving bonds (7%)

held by off-budget government programs, like social security, local governments, etc.

yield is at least 5bp below marketable Treasuries.

Zvi Wiener FI - 2 slide 48

Issuance of Treasuries

• regularly scheduled auctions = primary market.

• 2,000 brokers and dealers are registered

• Prime dealers are selected by NY Fed - counterparites for open market operations.

Zvi Wiener FI - 2 slide 49

Auctions

• The process begins several days before.

• “when issued market” after the announcement but before it takes place.

• On the day of the auctions bids may be submitted to FED.

• Competitive bids - quantity and yield

• Noncompetitive bids - small orders

Zvi Wiener FI - 2 slide 50

Auctions

• Uniform price method for 2, 5 year notes, TIPS

• Other issues have multiple price auction

• Bidders get securities at their bid price.

• Non-competitive get at the average price of competitive bids.

Zvi Wiener FI - 2 slide 51

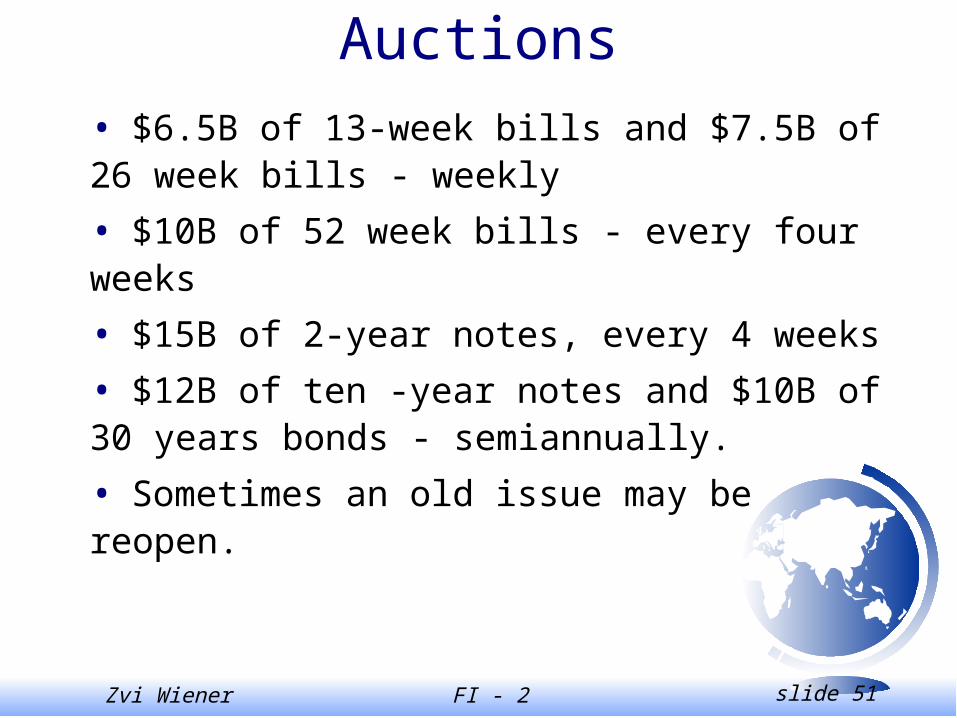

Auctions

• $6.5B of 13-week bills and $7.5B of 26 week bills - weekly

• $10B of 52 week bills - every four weeks

• $15B of 2-year notes, every 4 weeks

• $12B of ten -year notes and $10B of 30 years bonds - semiannually.

• Sometimes an old issue may be reopen.

Zvi Wiener FI - 2 slide 52

Cancellations

1986 20 year bond

1990 4 year note

1993 7 year note

1998 3 year note

Zvi Wiener FI - 2 slide 53

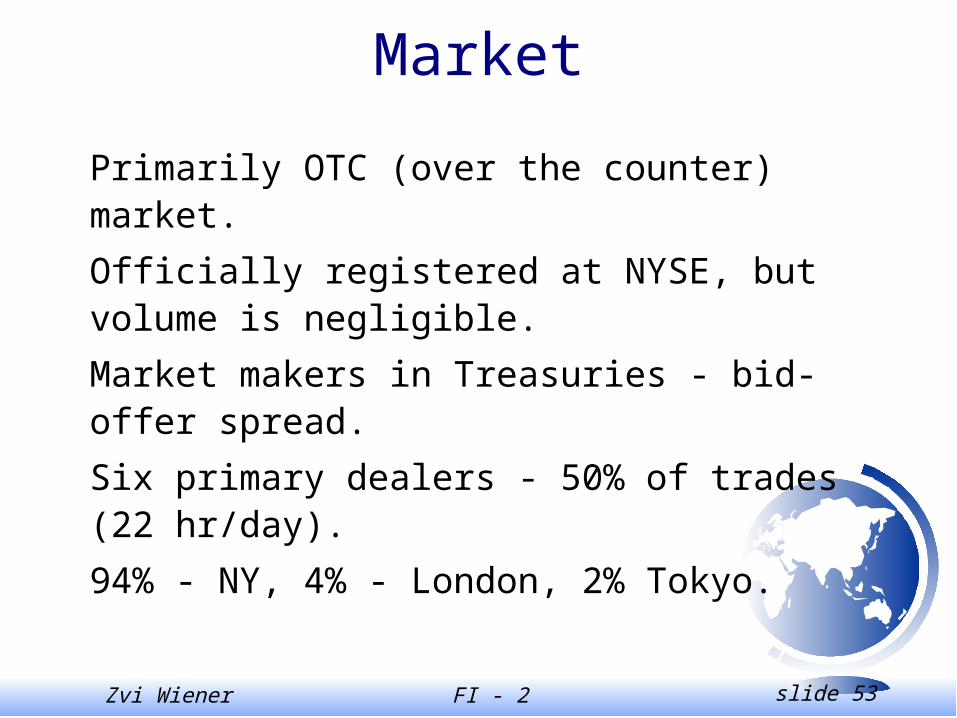

Market

Primarily OTC (over the counter) market.

Officially registered at NYSE, but volume is negligible.

Market makers in Treasuries - bid-offer spread.

Six primary dealers - 50% of trades (22 hr/day).

94% - NY, 4% - London, 2% Tokyo.

Zvi Wiener FI - 2 slide 54

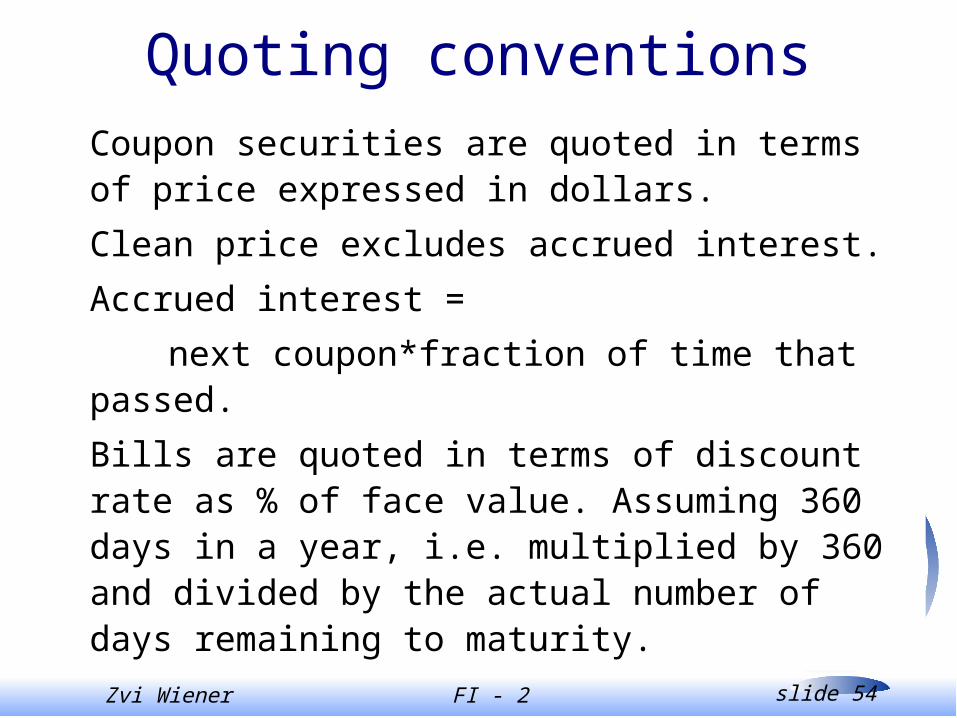

Quoting conventions

Coupon securities are quoted in terms of price expressed in dollars.

Clean price excludes accrued interest.

Accrued interest =

next coupon*fraction of time that passed.

Bills are quoted in terms of discount rate as % of face value. Assuming 360 days in a year, i.e. multiplied by 360 and divided by the actual number of days remaining to maturity.

Zvi Wiener FI - 2 slide 55

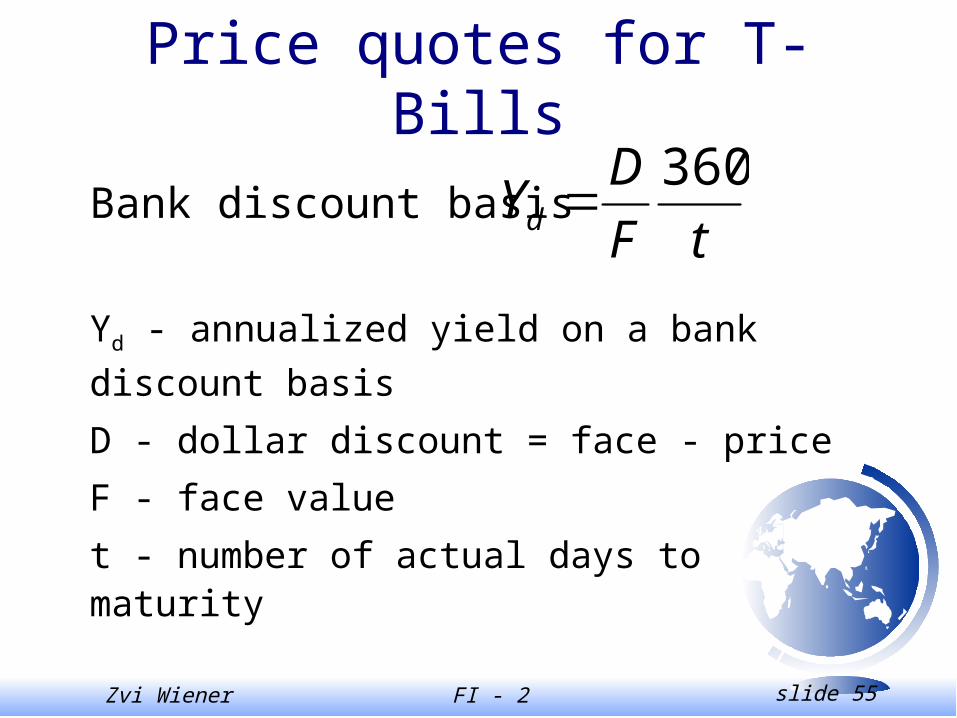

Price quotes for T-Bills

Bank discount basistF

DYd

360

Yd - annualized yield on a bank discount basis

D - dollar discount = face - price

F - face value

t - number of actual days to maturity

Zvi Wiener FI - 2 slide 56

Price quotes for T-Bills

360

FtYD d

3601

tYFDFprice d

Zvi Wiener FI - 2 slide 57

Price quotes for T-Bills

%75.8100

360

100

569.97100

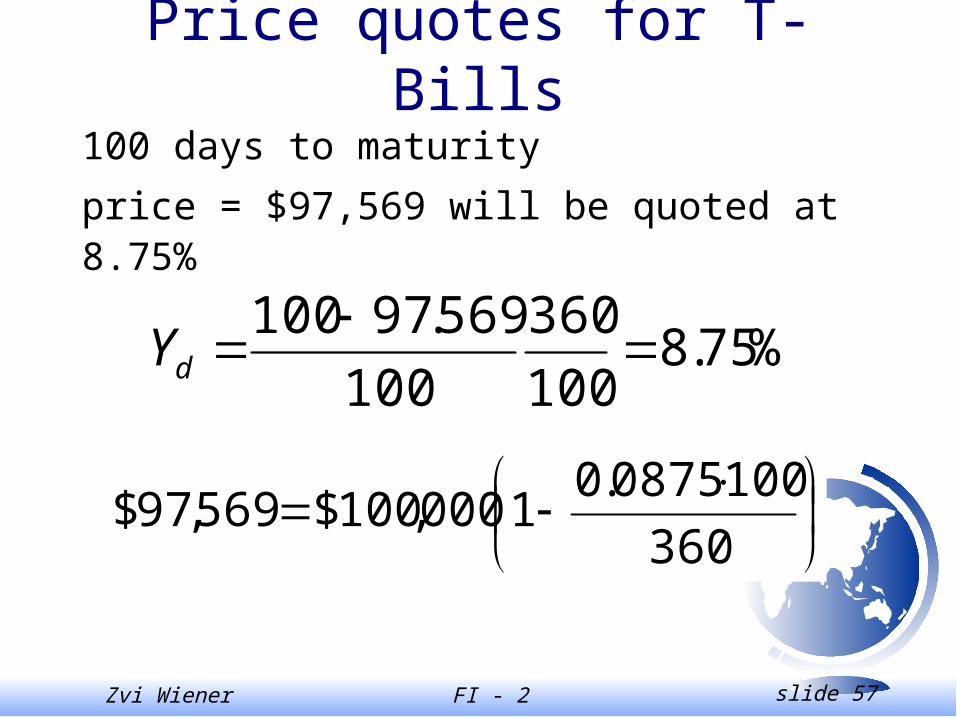

dY

100 days to maturity

price = $97,569 will be quoted at 8.75%

360

1000875.01000,100$569,97$

Zvi Wiener FI - 2 slide 58

Price quotes for T-Bills

The quoted yield is based on the face value

and not on the actual amount invested.

The yield is annualized on 360 days basis.

Bond equivalent yield = CD equivalent yield

d

d

Yt

YyielequivCD

360

360.

%97.8%75.8100360

%75.8360.

yielequivCD

Zvi Wiener FI - 2 slide 59

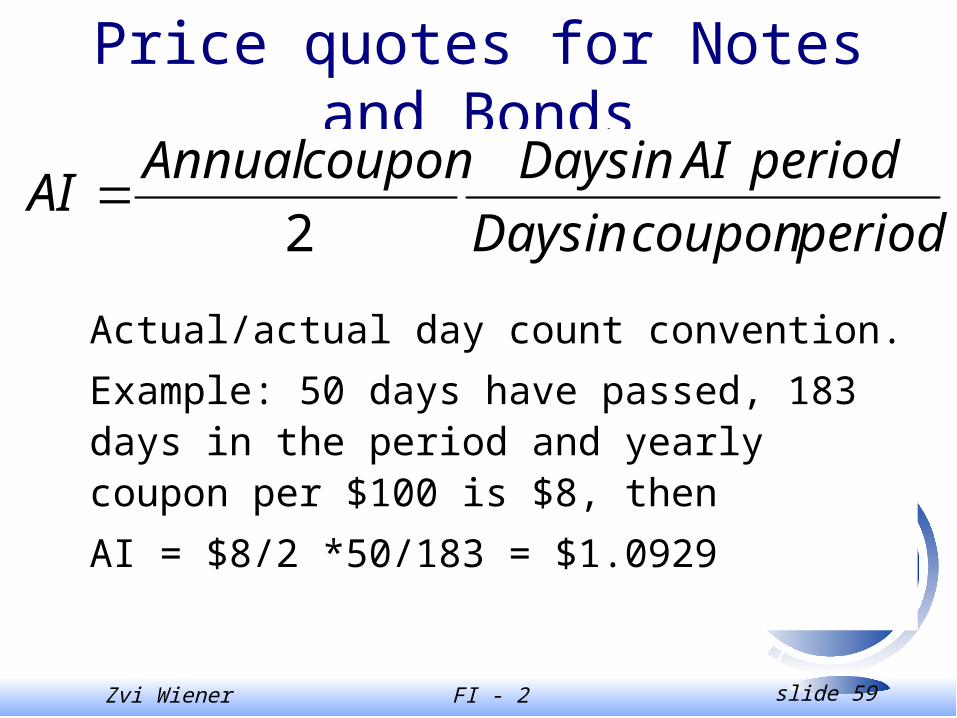

Price quotes for Notes and Bonds

periodcouponinDays

periodAIinDayscouponAnnualAI

2

Actual/actual day count convention.

Example: 50 days have passed, 183 days in the period and yearly coupon per $100 is $8, then

AI = $8/2 *50/183 = $1.0929

Zvi Wiener FI - 2 slide 60

Recordkeeping

National Book-Entry System (NBES) maintains

records for depository institutions.

Most trades are delivery versus payment.

Federal Reserve grants finality and provides an

intraday credit to financially healthy depository

institutions.

Zvi Wiener FI - 2 slide 61

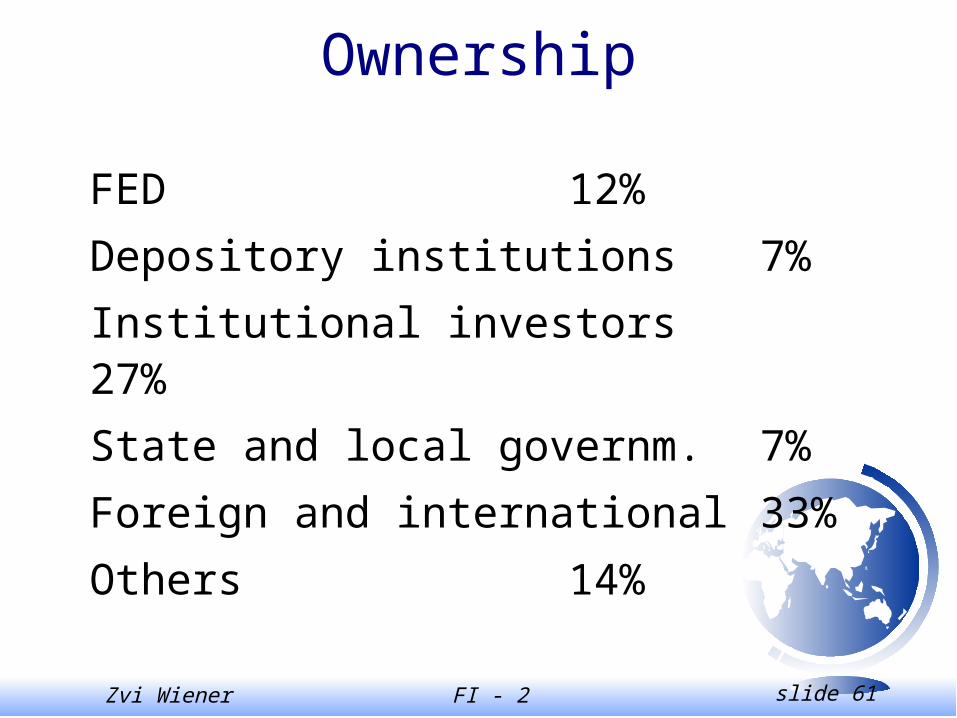

Ownership

FED 12%

Depository institutions 7%

Institutional investors 27%

State and local governm. 7%

Foreign and international 33%

Others 14%

Zvi Wiener FI - 2 slide 62

STRIPS

Separate Trading of Registered Interest and Principal of Securities.

Stripping and reconstitution.

About 33% of all outstanding T-bonds are stripped.

Creates zero-coupon securities.

US company must pay tax on accrued interest is taxed every year, so strips create a negative CF.

Zvi Wiener FI - 2 slide 63

Determinants of the Yield Curve

Federal Reserve sets a target level for the fed funds rate - the rate at which depository institutions make uncollaterized overnight loans to one another.

Long-term rates reflect expectations of future rates and can be influenced by the outlook for monetary policy.

Zvi Wiener FI - 2 slide 64

Liquidity

• Bid-offer spread 1-2 cents per $100 face

• Corporate bonds for example 13 cents

• High yield bonds 19 cents

• on-the-run - recently issued in a particular maturity class. With time became off-the-run.

• Flight to Quality (fall 98) bid-ask 16-25 cents.

Zvi Wiener FI - 2 slide 65

Repurchase Agreements

Borrowing and lending using Treasuries and other debt as collateral.

Repo (loan). You sell a security to counterparty and agree to repurchase the same security at a specified price at a later date (often next day).

Reverse Repo - you agree to purchase a security and sell it back at a specified price later.

Zvi Wiener FI - 2 slide 66

Repurchase Agreements

Most repos are general-collateral repo rate.

Some securities are special (for example on-the-run).

Specialness peaks around next auction, then declines sharply.

NY FED operates a securities lending for primary dealers using FED’s portfolio while posting other Treasury security as collateral.

Zvi Wiener FI - 2 slide 67

Treasury Based Derivatives

Futures and options for 2, 5, 10 year notes and bonds are listed by CBOT and CFFE. CNE offers futures and options on bills and other short term interest rate products.

End of October 99 open interest for CBOT long-bond futures was 635,000 (each one based on $100,000 face value).

Daily volume 300,000 contracts.

Zvi Wiener FI - 2 slide 68

Treasury Based Derivatives

CBOT also offers options on Treasury futures

- contract that allows the holder to buy/sell a

future contract at a specified price.

Cheapest-to-deliver option and conversion

factor (compare to commodities).

Zvi Wiener FI - 2 slide 69

TIIS = TIPS

Treasury Inflation Indexed (Protected) Securities.

Since 97, $92B were issued, based on the non-seasonally adjusted CPI lagged 2.5 months.

The quoted price do not reflect the accumulated inflation compensation.

Real price = quoted*index ratio + accrued interest

I-bonds saving bonds that are also CPI indexed.

Zvi Wiener FI - 2 slide 70

TIIS = TIPS

5, 10, 30 years notes and bonds.

Less liquid: 2-6 cents per $100 face.

CBOT offers options and futures on TIPS

Canada, France, England, Israel have similar types of debt.

Zvi Wiener FI - 2 slide 71

T-bills markets

Issuance of T-bills was cut sharply.

Between Dec-96 and Sep-99 the total

outstanding amount of coupon securities

declined 7% while bills declined 16%.

Treasury Debt buybacks. Reverse auctions

trying to remove small issues.

Zvi Wiener FI - 2 slide 72

Government-Sponsored Enterprises

Fannie Mae “benchmark” and Freddie Mac “reference” notes and bond.

Can be electronically transferred through clearing houses as Euroclear and Cedel and NBES.

Outstanding amount $150B with 2-30 years to maturity.

Zvi Wiener FI - 2 slide 73

Government-Sponsored Enterprises

GNMA - Government National Mortgage Association

FHLBS - Federal Home Loan Bank System

Sallie Mar - Student Loan Marketing Association

Zvi Wiener FI - 2 slide 74

Corporate Debt Instruments

• corporate bonds

• medium-term notes

• CP = commercial papers

• ABS = asset backed securities

They have priority over common stocks in the case of bankruptcy.

Zvi Wiener FI - 2 slide 75

Corporate Bonds

Main types of issuers

• utilities

• transportation

• industrial

• banks and financial companies

Zvi Wiener FI - 2 slide 76

Bond Indentures

• trustee

• term bonds, serial bonds

• collateral

• debenture bond - not secured

• guaranteed bonds

Zvi Wiener FI - 2 slide 77

Bond Provisions

• Call and refund provisions - the issuer has the right to redeem the entire amount before maturity. Sometimes there is a premium to be paid in such a case (redemption schedule).

• Special redemption prices for debt redeemed through the sinking fund

• Refunding means replacing by another debt.

Zvi Wiener FI - 2 slide 78

Bond Provisions

• Sinking fund provision sometimes the issuer is required to retire a portion of an issue each year.

– either by cash payment to bondholders (lottery)

– or by buyback bonds

Zvi Wiener FI - 2 slide 79

Bond Rating

• Duff and Phelps Credit Rating Co.

• Fitch Investors Service

• Moody’s Investors Service

• Standard & Poor’s Corporation

Zvi Wiener FI - 2 slide 80

Rating

Moody’s S&P Fitch D&P

Aaa AAA AAA AAA

Aa1 AA+ AA+ AA+

Aa2 AA AA AA

Aa3 AA- AA- AA-

A1 A+ A+ A+

A2 A A A

A3 A- A- A-

Zvi Wiener FI - 2 slide 81

Rating

• BBB- or better = investment grade

• BB+ and below - speculative grade

• D to DDD default

• transition matrix

Zvi Wiener FI - 2 slide 82

One year transition matrix

Aaa Aa A Baa Ba B C&D

Aaa 91.9 7.38 0.72 0 0 0 0

Aa 1.1 91.3 7.1 0.3 0.2 0 0

A 0.1 2.6 91.2 5.3 0.6 0.2 0

Baa 0 0.2 5.4 87.9 5.5 0.8 0.2

Zvi Wiener FI - 2 slide 83

High Yield Bonds

• LBO, downgrading, refinancing

• fallen angels

• deferred interest bonds

• Step-up bonds pay initially low interest which increases with time

Zvi Wiener FI - 2 slide 84

SEC rule 144A

Allows to trade private placements among

qualified institutions.

Zvi Wiener FI - 2 slide 85

Medium Term Notes (MTN)

Notes are registered with the SEC under Rule 415 (the shelf registration) and are offered continuously to investors by an agent of the issuer.

Maturities vary from 9 months to 30 years.

Can be either fixed or floating.

Very flexible way to raise debt!

Zvi Wiener FI - 2 slide 86

Primary Market (MTN)

Issuer posts spreads over Treasuries for a variety of maturities.

Then an agent tries to find an investor. Minimal size is between $1M and $25M.

The schedule can be changes at any time!

Often structured MTNs are used (caps, floors, etc.) = structured notes.

Zvi Wiener FI - 2 slide 87

Structured Notes

Many institutional investors can use swaps and structured notes to participate in markets that were prohibited.

Another use of structured notes is in risk management.

Financial Engineering is used to create securities satisfying the needs of investors.

Zvi Wiener FI - 2 slide 88

Commercial Papers

• Short term unsecured promissory note

• An alternative to short term bank borrowing

• A typical round-lot transaction is $100,000

• In the USA maturity is up to 270 days

• Requires less paperwork

• Those with maturity up to 90 days can be used as collateral for FED discount window.

Zvi Wiener FI - 2 slide 89

Commercial Papers

• Typically rolled over

• Rollover risk is backed by an unused bank credit line

• In order to issue CP one need either a high rating or good collateral

• Sometimes credit enhancement is used (LOC)

• CP issued in the USA by foreigners are called Yankee CP

Zvi Wiener FI - 2 slide 90

Commercial Papers

• Between 71 an 89 there was one default on CP.

• 3 defaults occurred in 89 and 4 in 90

• Direct paper is sold without an agent

• Secondary market is thin

• There is a special rating for CP, P-1,3, A-1,3

• discount instruments, used by money market

Zvi Wiener FI - 2 slide 91

Bankruptcy and Credit Rights

• liquidation - all assets will be distributed

• reorganization - a new corporate entity will result

• a company that files for protection becomes a debtor in possession and continues to operate under the supervision of the court

Zvi Wiener FI - 2 slide 92

Bankruptcy and Credit Rights

Absolute priority rule - senior creditors are paid in full before junior creditors are paid anything.

Works in liquidation but often does not work in reorganization.

Zvi Wiener FI - 2 slide 93

Municipal Securities

Exemption of interest income from federal

taxation.

Issued by states, counties, special districts, cities,

towns, school districts.

Zvi Wiener FI - 2 slide 94

Municipal Securities

Exemption of interest income from federal taxation.

General obligation bonds - backed by tax power

Limited tax general obligation bonds

Revenue bonds - based on specific projects

Zvi Wiener FI - 2 slide 95

Municipal Securities

Airport Revenue Bonds

College and University Revenue Bonds

Hospital Revenue Bonds

Industrial Revenue Bonds

Single-Family Revenue Bonds (mortgages)

Multifamily Revenue Bonds (housing projects)

Water Revenue Bonds

Zvi Wiener FI - 2 slide 96

Hybrid and Special Bond Securities

• Insured bonds - typically by an insurance firm

• Bank-backed municipal bonds (letter of credit)

• Refunded Bonds - a portfolio of safe securities is

placed in trust and they will cover the payments.

• Troubled city bailout bonds

Zvi Wiener FI - 2 slide 97

Municipal Money Market Products

• TAN = tax anticipation notes

• RAN = revenue anticipation notes

• GAN = grant anticipation notes

• BAN = bond anticipation notes

• Tax exempt commercial paper

Zvi Wiener FI - 2 slide 98

Municipal Derivatives

• floaters = floating rate + spread

• inverse floaters = interest - floating rate

• strips

• partial strip = are zeros till a call date and then become coupon type

Zvi Wiener FI - 2 slide 99

Yield on Municipal Bonds

tax-exempt yieldequivalent taxable yield =

1-marginal tax rate

for example bond offers 6.5% and marginal tax rate 40%:

0.065 = 0.1083

1-0.40

Zvi Wiener FI - 2 slide 100

Non-US Bonds

• national bond markets– domestic market

– Foreign marketYankee USA Samurai Japan bulldog UK Rembrandt Holland matador Spain

Zvi Wiener FI - 2 slide 101

International bond market

• Eurobond and Euroyen markets

• Global bond - simultaneous offering

• Typically registered in Luxembourg,

London or Zurich, but traded OTC.

• Supranationals - IBRD, World Bank, etc.

Zvi Wiener FI - 2 slide 102

Eurobond market

• Dual currency bonds (coupon in one currency, principal in another).

• Option currency bond one side can choose the currency.

• Convertible bonds with warrants - can be converted into another asset. Equity, debt, gold or currency warrant.

Zvi Wiener FI - 2 slide 103

Eurobond market

• Floating Rate Notes = FRN based on LIBOR or LIBID

• many are collared

• some are perpetual

Zvi Wiener FI - 2 slide 104

Comparing Yields

bond equivalent yield of Eurodollar bond

= 2[(1+yield to maturity)0.5-1]

for example: A Eurodollar bond with 10% yield has the bond equivalent yield of

2[1.100.5-1] = 9.762%

Zvi Wiener FI - 2 slide 105

Japanese Government Bonds JGB

• short term Treasury bills

• medium term bonds

• long term bonds

• super long term bonds (20 years)

Zvi Wiener FI - 2 slide 106

German Government Bonds

• U-Schatze discount paper up to 2 years

• Kassens = federal government notes (2-6 y.)

• OBLEs = 5 year federal government notes

• Bunds = federal government bonds (6-30 y.)

all coupon payments are annual

Zvi Wiener FI - 2 slide 107

UK Government Bonds Gilts

• straights = bullet bonds (some callable)

• convertibles (option to holder to convert to longer gilts)

• index linked low coupon 2-2.5%

• irredeemable (perpetual)

Zvi Wiener FI - 2 slide 108

Brady Bonds

Argentina, Brazil, Costa Rica, Dominican Republic, Ecuador, Mexico, Uruguay, Venezuela, Bulgaria, Jordan, Nigeria, Philippines, Poland.

Partially collateralized by US government securities