forum on auditing in the small business environment · opening remarks charles niemeier ......

TRANSCRIPT

Forum on Auditing in The Small Business Environment

June 24, 2008

Dallas, TX

Opening Remarks

Charles Niemeier

PCAOB Board Member

June 24, 2008

Dallas, TX

3

Caveat

One of the benefits of today's session is that you will hear first-hand from one of the PCAOB Board members and numerous PCAOB staff. You should keep in mind, though, that when we share our views they are those of the speaker alone, and do not necessarily reflect the views of the Board, its members or staff. Therefore, unless it is clear that the Board has authorized the statement, you should not attribute it to the Board or staff.

Discussion of Practical Quality Control Policies and Procedures

June 24, 2008

Dallas, TX

5

Presenters

� Dima Andriyenko, Office of the Chief Auditor

� George Botic, Division of Registration and Inspections

6

What We Will Cover

� Overview of current interim quality control standards*

� For each of the five elements of the quality control standards, we will discuss

� Areas of focus and considerations

� Incorporation into firm’s control policies and procedures

� Interactive session

*http://www.pcaobus.org/Standards/QC/Pages/default.aspx

7

Restrictions on Use

� Information not necessarily compiled from inspection observations

� Information intended to provide considerations and does notrepresent requirements of the PCAOB

� Complexity of quality control system will vary by firm

8

Foundation of Audit Quality

EXECUTION DETECTIVEPREVENTIVE

Personnel

Management

Independence,

Integrity, and

Objectivity

Engagement

Performance

MonitoringAcceptance and

Continuance of

Clients and

Engagements

Execution of Issuer Audits

Tone at the Top

9

Elements of Quality Control

Engagement Performance

Independence Integrity, and Objectivity

Personnel Management

Acceptance and

Continuance of Clients and Engagements

Monitoring

10

Administration of Quality Control System

� Tone at the top

� Assignment of personnel responsible for design and maintenance of policies and procedures

� Proper and timely communication

� Documentation of policies and procedures

� Demonstrate compliance with policies and procedures

Acceptance and Continuance of Clients and Engagements

QC 20.14 -.16

12

Acceptance and Continuance of Clients and Engagements (QC20.14-.16)

� Perform procedures to determine if the accounting firm should

� Accept an issuer as a new audit client

� Continue as the auditor of a current issuer audit

� Focus on

� Company and management (integrity)

� Firm (risk and qualifications)

� Engagement terms

� Establish an understanding with the audit client regarding services to be performed

13

Acceptance and Continuance of Clients and Engagements – Areas of Focus

� Level of review

� Reviewer qualifications

� Objectivity and expertise

� Timeliness of review

� Acceptance of new client

� Continuance of existing client

14

Acceptance and Continuance of Clients and Engagements – Areas of Focus

� Factors considered to accept new issuer audits

� Source of referral

� Issuer-specific factors

� Management integrity� Significant transactions and balances� Operations or industry

� Firm-specific factors

� Professional competence � Independence� Risk

� Factors considered to continue audit of existing issuer clients

� Changes in the issuer’s management

� Significant transactions and balances

� Recent litigation or other enforcement actions taken against firm

� Fees

15

Quality Control Policies and Procedures –Considerations

� Define reviewer qualifications

� Incorporate checklists/specific procedures for accepting new clients and continuance of existing clients

� Define timing of acceptance and continuance procedures in quality control document

� Monitor compliance

Personnel Management

QC 20.11 -.13; QC 40

17

Personnel Management (QC 20.11- .13; QC 40)

� Hiring

� Persons hired possess appropriate characteristics

� Assignment of personnel to engagements

� Required professional competence considered

� Professional development

� CPE – general and industry-specific

� Advancement

� Qualifications necessary are present

18

Personnel Management – Areas of Focus

� Training

� Adequate training in audits of issuers

� Keeping current on technical literature

� Tracking professional development of firm personnel

� Create and monitor individual-specific training development plan

� Consider applicability to issuer audit assignments

� Assigning personnel to issuer audits

� Person responsible should be fully committed, if possible

� Consider expertise and availability

19

Quality Control Policies and Procedures –Considerations

� Develop requirements for “firm-wide” training program

� Independence training

� PCAOB standards

� Firm audit methodology

� SEC developments

� Perform critical evaluation of individual professional development

� Consider relationship to issuer audit assignments

� Current technical accounting pronouncements

� Industry-specific training

� Insufficient training of all staff will directly impact the quality of audits

Independence, Integrity, and Objectivity

QC 20.09 -.10

21

Independence, Integrity, and Objectivity (QC 20.09-.10)

� Independence

� In fact and in appearance in all required circumstances

� Integrity

� Honest and candid within constraints of client confidentiality

� Objectivity

� Obligation to be impartial, intellectually honest, and free of conflicts of interest

22

Independence

� Must comply with applicable independence requirements of PCAOB and SEC

� System of quality control designed to provide reasonable assurance that personnel maintain independence (in fact and in appearance) in all required circumstances

� PCAOB Independence Rules� PCAOB Rules 3501, 3502, 3520 to 3525

� Interim Independence and Ethics Rules� ET Sec. 101, 102, and 191� SECPS Appendix L

23

Independence, Integrity, and Objectivity – Areas of Focus

� Partner assigned as independence expert

� Current on all independence rules

� Training staff

� All lines of service take responsibility to keep current on independence rules

� Proper and timely communication

� Reduce risk of non-compliance with independence rules

� Monitoring independence

� SECPS 1000.08(o) and Appendix L

24

Quality Control Policies and Procedures –Considerations

� Tone at the top

� Assign qualified person as "independence expert"

� Require personnel to periodically attend independence training

� Establish framework to monitor independence

� Independence certifications

� Restricted entity list

� Random audits of associated person holdings

25

Reference Materials Relating to Independence

� PCAOB� Ethics and Independence Rules

� Interim Independence Standards

� Interim Quality Control Standards

� SECPS Requirement 1000.08(o) and Appendix L – Independence Quality Controls

� www.pcaobus.org/Standards/default.aspx� SEC

� Independence Rules – Regulation S-X, Rule 210.2-01 www.sec.gov/info/accountants/independref.shtml

� Frequently Asked Questions (updated 8/07) www.sec.gov/info/accountants/independref.shtml

� Interpretations Relating to Independence – SEC Codification of Financial Reporting – Section 602.02. (Not available on SEC web site.)

� Indemnification - SEC Frequently Asked Questions - Question 4 (issued December 13, 2004) (www.sec.gov/info/accountants/ocafaqaudind121304.htm#other), and SEC Codification of Financial Reporting – Section 602.02.f.i., Indemnification by Client

Break

(15 minutes)

26

Engagement Performance

QC 20.17 -.19

28

Engagement Performance (QC 20.17-.19)

� Encompass all phases of the design and execution of the engagement

� Planning

� Supervisory and review

� Documentation

� Concurring partner reviews

� Consultation process

29

Engagement Performance –Areas of Focus

� Methodology

� Developed or obtained

� Staff properly trained

� Tailored for specific audit engagement

� Adequate time available to supervise audits

� Multiple demands on partner/managers

� Composition of hours (supervisor vs. staff)

� Consultation

� Acknowledgment by staff that consultation is required

� Use of outside resources

30

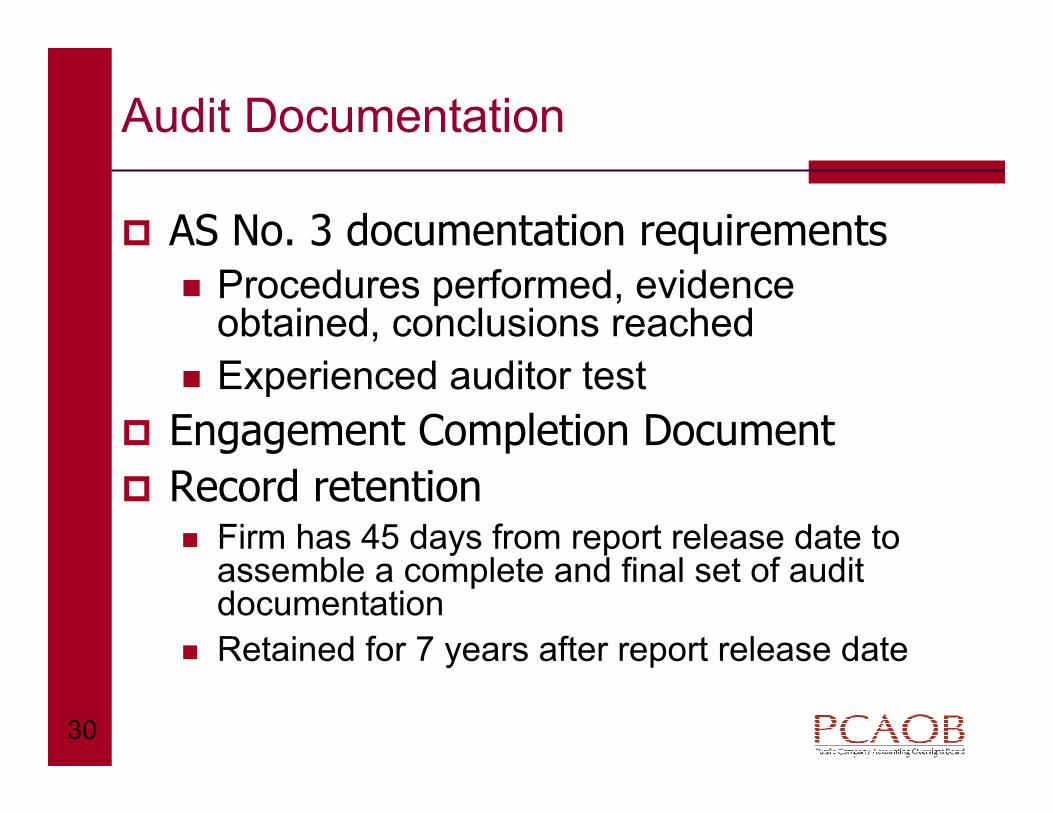

Audit Documentation

� AS No. 3 documentation requirements

� Procedures performed, evidence obtained, conclusions reached

� Experienced auditor test

� Engagement Completion Document

� Record retention� Firm has 45 days from report release date to assemble a complete and final set of audit documentation

� Retained for 7 years after report release date

31

Concurring Partner Review –Current Requirements

� SEC Practice Section, Section 1000.08(f), Appendix E – Concurring Partner Review Requirements

� Qualifications of concurring partner

� Nature, timing, and extent of concurring partner reviews

� Documentation of concurring partner review

� Quarterly reviews

32

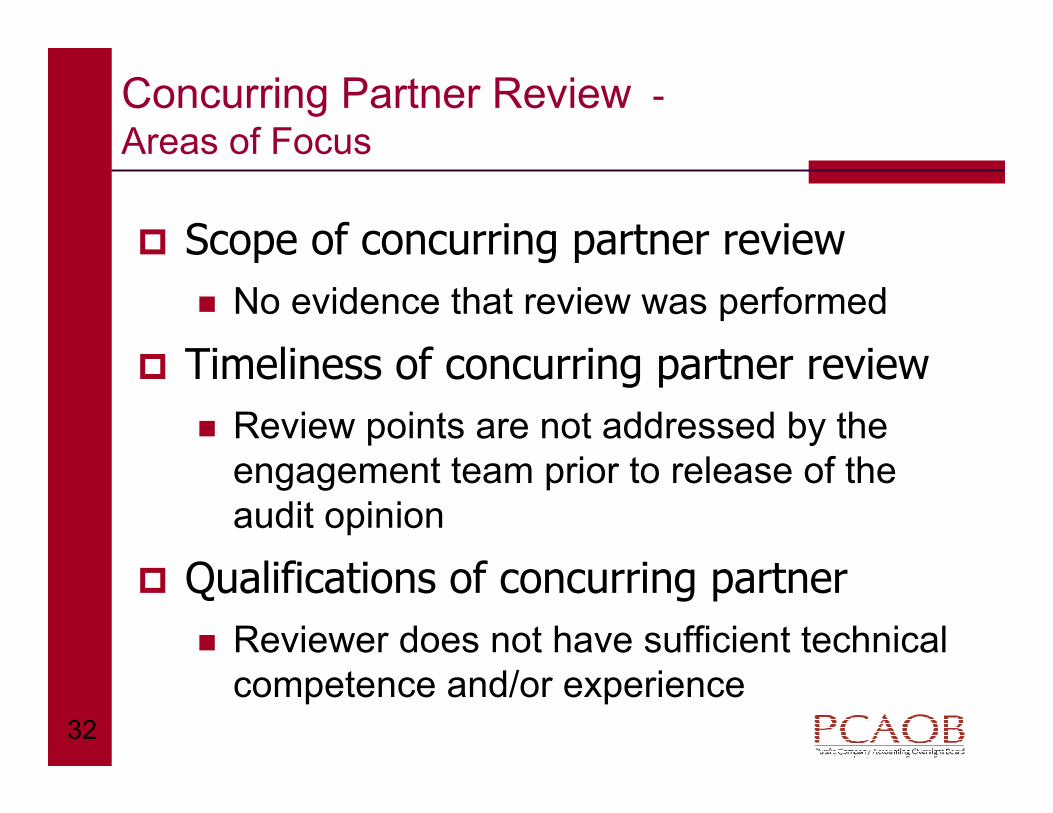

Concurring Partner Review -Areas of Focus

� Scope of concurring partner review

� No evidence that review was performed

� Timeliness of concurring partner review

� Review points are not addressed by the engagement team prior to release of the audit opinion

� Qualifications of concurring partner

� Reviewer does not have sufficient technical competence and/or experience

33

Quality Control Policies and Procedures –Considerations

� Evaluate engagement performance

� Engagement economics

� Composition of time spent (supervisor vs. staff)

� Document, document, document!

� Incorporate documentation requirements into system of quality control

� Monitor compliance

34

Quality Control Policies and Procedures –Considerations

� Consultation

� Identify specific audit areas or transactions require consultation

� Identify qualified persons or firms

� Concurring partner review

� Define scope, timing, and qualifications in quality control document

� Require approval by concurring partner prior to report release

Monitoring

QC 20.20; QC 30

36

Monitoring (QC 20.20; QC 30)

� Ensure system of quality control, taken as a whole, is effective

� Ongoing consideration and evaluation of -

� Relevance and adequacy of firm’s policies and procedures

� Appropriateness of firm’s guidance materials and practice aids

� Effectiveness of professional development activities

� Compliance with the firm’s policies and procedures

37

Monitoring – Areas of Focus

� Tone at the top

� Supports effective implementation of quality control system

� If sufficient, may reduce risk of audit failures

� "Pre-issuance" or "post-issuance" reviews

� Persons not directly associated with the performance of the engagement

� Assess compliance with professional standards and firm’s policies and procedures through selected engagements

38

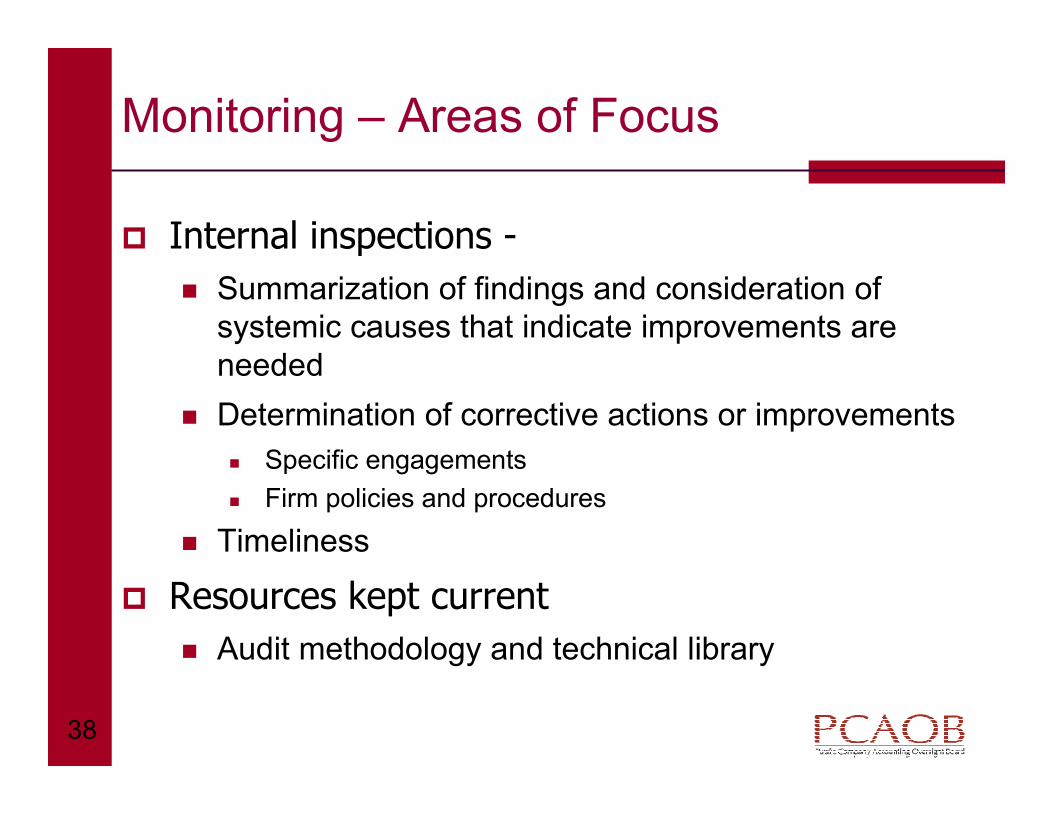

Monitoring – Areas of Focus

� Internal inspections -

� Summarization of findings and consideration of systemic causes that indicate improvements are needed

� Determination of corrective actions or improvements

� Specific engagements

� Firm policies and procedures

� Timeliness

� Resources kept current

� Audit methodology and technical library

39

Quality Control Policies and Procedures –Considerations

� Develop monitoring controls directly related to the quality and integrity of audits

� Concurring partner review

� Required consultations

� Required timely internal inspections

� Consider modifications to policies and procedures or methodology based on inspection results in a timely manner

� Impact on smaller firms

40

Questions?

Enforcement Update

Division of Enforcement and Investigations

June 24, 2008

Dallas, TX

42

Presenters

� John C. Abell, Division of Enforcement & Investigations

� Stefan Hagerup, Division of Enforcement & Investigations

43

DEI Mission

� Investigate possible violations by registered public accounting firms or their associated persons of the laws, rules and standards subject to the Board’s jurisdiction

� Recommend to the Board appropriate sanctions if violations are found

44

What We Will Cover

� Independence

� Principal Auditor

� Assignment of Engagement Personnel

� Selected Areas of Audit Execution (Confirmations, Revenue Recognition, Existence and Valuation of Assets, Disclosure of Related Party Transactions)

� Consideration of Fraud

� Illegal Acts

� Audit Documentation

45

Independence Requirements

� ET 101

� Regulation S-X

� Exchange Act Section 10A(g)

46

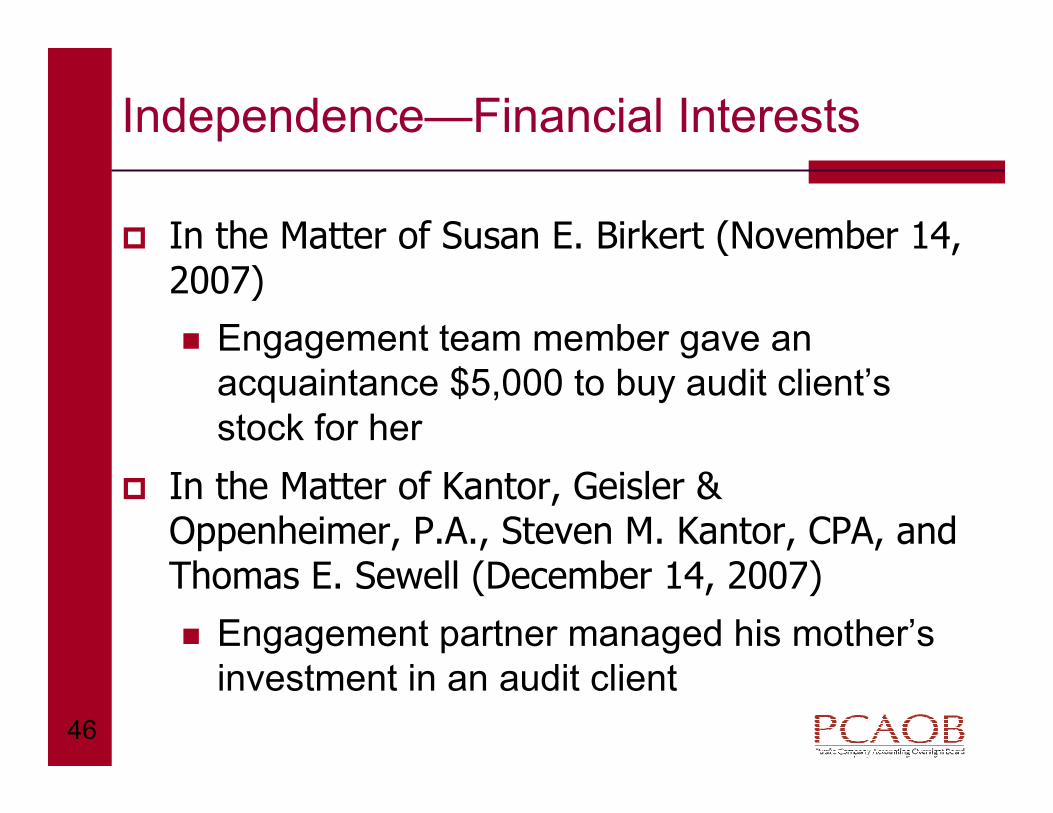

Independence—Financial Interests

� In the Matter of Susan E. Birkert (November 14, 2007)

� Engagement team member gave an acquaintance $5,000 to buy audit client’s stock for her

� In the Matter of Kantor, Geisler & Oppenheimer, P.A., Steven M. Kantor, CPA, and Thomas E. Sewell (December 14, 2007)

� Engagement partner managed his mother’s investment in an audit client

47

Independence—Bookkeeping Services

� In the Matter of Kantor, Geisler & Oppenheimer, P.A., et al.

� Firm made accounting decisions for the issuer, and performed various services related to keeping client’s books and records, including� Making journal entries directly in the client’s books and

records,

� Generating the trial balances for the financial statements,

� Generating the financial statements and footnote disclosures, and

� Computing depreciation for the client’s fixed assets.

48

Independence—Business Relationship

� In the Matter of Kenny H. Lee, CPA Group, Inc. and Kwang Ho Lee, CPA (November 22, 2005)

� Firm's engagement as auditor continued after firm principal accepted client's offer to serve on its board of directors

49

Principal Auditor—Relevant Standards

� Deciding whether the auditor can serve as principal auditor (AU sec. 543.02)

� Using other auditors to perform a portion of the audit for the auditor (AU secs. 230 and 311)

50

Enforcement Case - Principal Auditor

� In the Matter of Clyde Bailey, P.C., and Clyde B. Bailey, CPA (November 22, 2005)

� On one audit, another firm provided its work papers to the Clyde Bailey firm, and other auditor’s work constituted substantially all of the audit evidence supporting the Clyde Bailey firm’s report

� On a second audit, an unregistered auditor asked the Clyde Bailey firm to review the auditor’s work and issue a revised report. The Board found that Clyde Bailey issued the report without planning or performing an audit

51

Enforcement Case - Principal Auditor

� In the Matter of PKF, AAER No. 2409 (April 12, 2006) (SEC cease-and-desist proceeding)

� Firm used the work of other auditing firms to report on issuer's financial statements and did not refer to the work of the other firms in its audit report

� Firm assumed complete responsibility for the work of the other auditing firms

52

Assignment of Engagement Personnel

� Auditors “should be assigned to tasks and supervised commensurate with their level of knowledge, skill and ability” (AU § 230.06)

� Firms should establish policies and procedures that “provide reasonable assurance that a practitioner-in-charge of an engagement possesses the competencies necessary to fulfill his or her engagement responsibilities” (QC §40.06)

53

Assignment of Engagement Personnel

� In the Matter of Deloitte & Touche LLP (December 10, 2007)

� Firm knew of facts and circumstances that raised questions about engagement partner’s ability to lead public company audit engagements, but left engagement partner in place without taking meaningful steps to assure the quality of the audit work before issuing its audit report

54

Audit Execution

� Failure to Obtain Sufficient Audit Evidence

� Confirmations

� Revenue Recognition

� Existence and Valuation of Assets

� Related Party Transactions

� Consideration of Fraud

55

Confirmation Procedures

� In the Matter of Armando C. Ibarra, P.C., Armando C. Ibarra, Sr. and Armando C. Ibarra, Jr. (December 19, 2006)

� Repeated failure to confirm accounts receivable and failure to perform any procedures other than obtaining management representations

56

Confirmation Procedures

� In the Matter of Williams & Webster, P.S., Kevin J. Williams, CPA, and John G. Webster, CPA (June 12, 2007)

� Confirmation procedures resulted in evidence that at least 50 percent of the accounts receivable selected for confirmation were the result of consignment arrangements, not sales

57

Confirmation Procedures

� In the Matter of Turner Stone & Company, LLP, and Edward Turner, CPA (December 19, 2006)� Confirmation related to an unusual year-end transaction having a material effect on the financial statements transaction terms was signed by a managing member of the borrower who also was a director and officer of the audit client

� Auditors failed to exercise heightened degree of professional skepticism and to consider whether there was a sufficient basis to conclude that the confirmation provided meaningful and competent evidence

58

Revenue Recognition

� In the Matter of James L. Fazio (December 10, 2007)

� Auditor did not perform adequate procedures to test client’s recognition of revenue when a right of return existed

� Did not adequately assess client’s ability to estimate future returns

� Did not adequately assess reasonableness of client’s estimates of future returns

59

Revenue Recognition

� In the Matter of Williams & Webster, P.S., et al.

� Products shipped pursuant to a consignment arrangement are not sales and do not qualify for revenue recognition until a sale occurs

� Transactions recorded as sales were subject to a right of return which issuer did not account for in accordance with GAAP

60

Revenue Recognition

� In the Matter of Clyde Bailey, P.C., et al.

� Auditor did not perform adequate audit procedures to evaluate whether client earned amounts recognized as revenue on a consulting contract

� auditor had evidence that the contract was not completed in the year in which the revenue was recognized, and

� the contract did not provide for payment for partial performance

61

Existence and Valuation of Assets

� In the Matter of Kantor, Geisler & Oppenheimer, P.A., et al.

� Auditors failed to perform adequate audit procedures to test property and equipment in audits for two different clients

� Existence and valuation of sample boards and display boards used to market products to end users

� Existence and valuation of laboratory equipment

62

Existence and Valuation of Assets

� In the Matter of Thomas Benson and Thomas Benson, CPA (June 29, 2007)

� Auditor failed to perform adequate audit procedures to test the existence and valuation of securities totaling some 97 percent of reported assets

� bonds in the amount of $500 million issued by the Republic of Venezuela and

� a note valued at $310 million

63

Existence and Valuation of Assets

� In the Matter of Timothy L. Steers, CPA, LLC and Timothy L. Steers (November 14, 2007)

� Auditor failed to perform adequate audit procedures to test the existence and valuation of issuer’s reported interest in a limited liability company valued at $10.7 million.

64

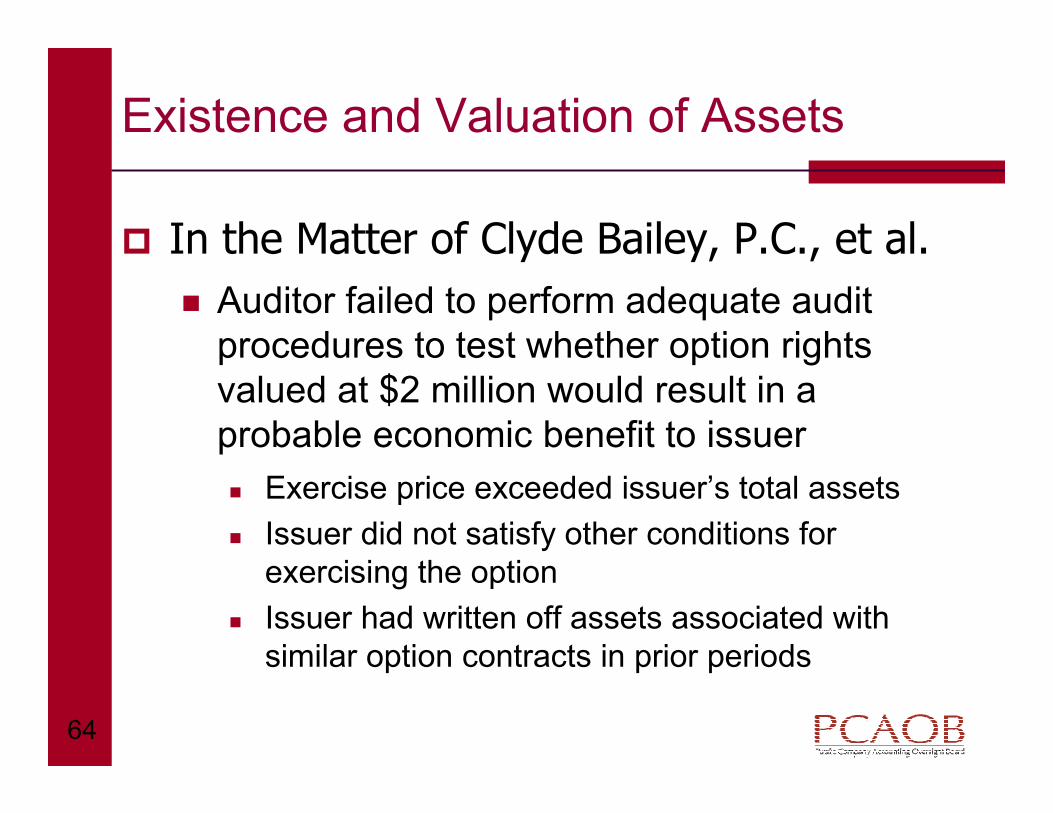

Existence and Valuation of Assets

� In the Matter of Clyde Bailey, P.C., et al.

� Auditor failed to perform adequate audit procedures to test whether option rights valued at $2 million would result in a probable economic benefit to issuer

� Exercise price exceeded issuer’s total assets

� Issuer did not satisfy other conditions for exercising the option

� Issuer had written off assets associated with similar option contracts in prior periods

65

Related Party Transactions

� In the Matter of Timothy L. Steers, CPA, LLC, et al.

� Material transaction with audit client’s majority shareholder was not disclosed in accordance with GAAP

� Auditor knew transaction was with a majority shareholder, but failed to identify and appropriately address audit client’s departure from the GAAP disclosure requirement

66

Related Party Transactions

� In the Matter of Williams & Webster, P.S., et al.

� Sale of mining claims acquired at a cost of $540 for over $31 million

� Sale was to a limited liability company that was owned and controlled by a director and shareholder of the audit client

67

Related Party Transactions

� In the Matter of Turner Stone & Company, LLP, et al.

� Requirements concerning related parties do not depend upon an ownership interest

� Loan agreement was with a related party because managing member of the borrower also was a director and officer of the audit client

68

Consideration of Fraud

� In the Matter of Turner Stone & Company, LLP, et al. � Assessment of risk of material misstatement due to fraud should be ongoing throughout the audit

� Firm failed to reassess whether the nature of auditing procedures performed needed to be changed to obtain additional or more reliable corroborative information after being presented with numerous warning signs, such as

� Unusual, significant year-end transactions� The involvement of a related party in a significant transaction

� Questionable confirmations � Conflicting evidential matter concerning a significant transaction

69

Consideration of Fraud

� In the Matter of Thomas Benson and Thomas Benson, CPA (June 29, 2007)

� Auditor failed to respond appropriately to numerous warning signs, including:

� Issuer did not make bond certificates available for inspection despite repeated requests,

� Issuer did not receive interest contractually due

� No evidence of payment for either the bonds or the note

70

Illegal Acts

� Audit Requirements, Exchange Act §10A(b)

� Illegal Acts by Clients, AU § 317

71

Illegal Acts

� In the Matter of Kantor, Geisler & Oppenheimer, P.A., et al.

� Firm discovered payments from audit client to a limited liability company and payments from the limited liability company that appeared to have been used to pay for personal expenses of certain of the audit client’s executives

� Firm did not take adequate steps to determine whether it was likely that an illegal act occurred

72

Illegal Acts – Unauthorized Use of Auditor's Name

� In the Matter of Reuben E. Price & Co. Public Accountancy Corp. (April 18, 2006)

� Issuer filed financial statements including a document it claimed was an audit report with Form 10-KSB

� Auditor had neither issued the audit report nor completed the audit at the time of the issuer's filing

� Auditor did not inform issuer's Board of Directors as required under Section 10A(b)(2) of the Securities Exchange Act

73

Documentation Requirements

� Auditing Standard No. 3

� SEC Rule 2-06 of Regulation S-X, Retention of Records Relevant to Audits and Reviews

74

Documentation Requirements

� In the Matter of Stephen J. Nardi, CPA (December 14, 2007)

� In the Matter of Ann Marie Fitzpatrick, CPA (December 14, 2007)

� Auditors added initials and signatures to workpapers that falsely indicated that a timely detailed review of the audit work was performed

75

Documentation Requirements

� In the Matter of Kantor, Geisler & Oppenheimer, P.A., et al.

� Audit partner signed audit work paper falsely stating that he performed certain supervisory duties, approved audit procedures and reviewed and approved working papers

76

Non-Cooperation

� In the Matter Of Goldstein and Morris, CPAs, P.C. and Edward B. Morris, CPA (May 25, 2005)

� In the Matter of Alan J. Goldberger, CPA and William A. Postelnik, CPA (May 25, 2005)

� Auditors created and back-dated documents and tried to conceal information from PCAOB inspectors

77

For More Information

� On the Web -www.pcaobus.org/Enforcement

� Board Disciplinary Orders

� Rules on Investigations and Adjudications

� PCAOB Center for Enforcement Tips, Complaints and Other Information

78

Questions?

Update on Standards-Setting Activities

June 24, 2008

Dallas, TX

80

Presenters

� Dima Andriyenko, Office of the Chief Auditor

� Diane Jules, Office of the Chief Auditor

81

What We Will Cover

� Audit Practice Alert – Matters Related to Auditing Fair Value

� Ethics and Independence

� Auditing Standard No. 6 – Evaluating Consistency of Financial Statements

� Internal Control Over Financial Reporting Developments

� Proposed Auditing Standard – Engagement Quality Review

� Current Standards-Setting Priorities

PCAOB Audit Practice Alert – Matters Related to Auditing Fair Value Measurements of Financial Instruments and the Use of Specialist

83

Practice Alert on Auditing Fair Value and Use of Specialist

� Matters likely to increase risk related to financial statements in current environment

� Highlights aspects of audit standards – practice alert not a PCAOB standard

� Highlights specific risks related to auditing fair value, including risks related to FAS 157

� Highlights specific risks related to use of pricing services

� Highlights key aspects of specialist standards

PCAOB Ethics and Independence Rules

85

PCAOB Rule 3523 - Tax Services to Persons in Financial Reporting Oversight Roles

� A registered public accounting firm is not independent of its audit client if the firm, or any affiliate of the firm, during the [audit and]* professional engagement period, provides any tax service to a person in a financial reporting oversight role at the audit client or their immediate family member

� Financial reporting oversight role ("FROR") means a role in which a person is in a position to or does exercise influence over the contents of the financial statements or anyone who prepares them

*Deleted

86

PCAOB Rule 3523 Example

� Issuer A is a calendar year-end company

� ABC accounting firm, who was not the auditor, provided personal tax return preparation services to CEO (FROR) from January to April 2008

� Issuer A asks ABC firm to become their auditor on June 1, 2008 for their 2008 year-end audit

� Audit period – January 1, 2008 to December 31, 2008

� Professional engagement period begins the earlier of when the engagement letter is signed or the firm begins audit, review, or attest procedures – June 1, 2008 or later

� Tax services to CEO must be ceased by the beginning of the professional engagement period – June 1, 2008 or later

87

PCAOB Rule 3526 - Communication with Audit Committees Concerning Independence

A registered public accounting firm must –� Prior to accepting an initial engagement pursuant to the standards

of the PCAOB –� describe, in writing, to the audit committee of the issuer, all

relationships between the registered public accounting firm or any affiliates of the firm and the potential audit client or persons in a financial reporting oversight role at the potential audit client that, as of the date of the communication, may reasonably be thought to bear on independence;

� discuss with the audit committee of the issuer the potential effects of the relationships on the independence of the registered public accounting firm, should it be appointed the issuer's auditor; and

� document the substance of its discussion with the audit committee of the issuer.

� At least annually thereafter –� All of the above, and

� Affirm to the audit committee of the issuer, in writing, that, as of the date of the communication, the firm is independent in compliance with Rule 3520

PCAOB Auditing Standard No. 6 –Evaluating Consistency of Financial Statements

89

Auditing Standard No. 6 – Evaluating Consistency of Financial Statements

� Aligns auditing standards with FASB Statement No. 154, Accounting Changes and Error Corrections

� Specific direction for auditor reporting on restatements

� Standard clarifies that auditor should evaluate changes even when retrospectively applied

� Provides additional direction regarding evaluation of reclassifications

� Remove GAAP hierarchy from the auditing standards

Internal Control Over Financial Reporting Developments

91

What We Will Cover

� Refresher on Auditing Standard No. 5

� Overview of Staff Views, Guidance for Auditors of Smaller Companies

� Provisions of AU sec. 722 related to the review of management’s quarterly certifications

Refresher on Auditing Standard No. 5

93

� Integrating the audits

� Risk assessment, including fraud risk assessment

� Top-down approach

� Small company considerations

AS No. 5 – Integrated Audit Process

94

� Audit of ICFR should be integrated with the audit of the financial statements

� Objectives of the audits are not identical, and the auditor must plan and perform the work to achieve the objectives of both audits

� Auditor should design testing of controls to accomplish the objectives of both audits simultaneously

Integrating the Audits

95

� Risk assessment underlies the entire audit process described by AS No. 5, including

� The determination of significant accounts and disclosures and relevant assertions,

� The selection of controls to test, and

� The determination of the evidence necessary for a given control.

Role of Risk Assessment

96

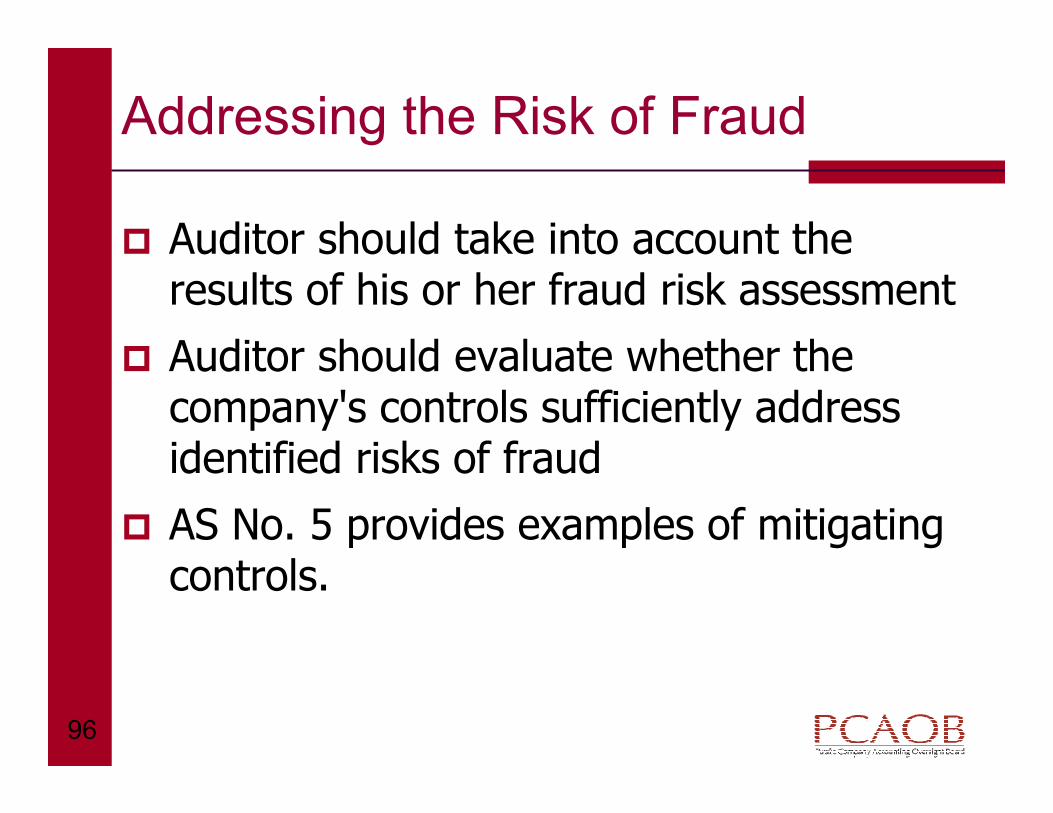

� Auditor should take into account the results of his or her fraud risk assessment

� Auditor should evaluate whether the company's controls sufficiently address identified risks of fraud

� AS No. 5 provides examples of mitigating controls.

Addressing the Risk of Fraud

97

� Auditor should use a top-down approach to the audit of ICFR to select the controls to test

� Top-down approach begins at the financial statement level and with the auditor's understanding of the overall risks to ICFR

� Auditor then focuses on entity-level controls and works down to significant accounts and disclosures and their relevant assertions

Using a Top-down Approach

98

� The size and complexity of the company, its business processes, and business units, may affect the way in which the company achieves many of its control objectives; the risks of misstatement and the controls necessary to address those risks.

� Six example areas where tailoring based on size and complexity may be necessary� Assessing entity-level controls

� Evaluating risk of management override and mitigating actions

� Evaluating controls implemented in lieu of segregation of duties

� Evaluating information technology ("IT") controls

� Evaluating financial reporting competencies

� Obtaining sufficient evidence with limited company documentation

Smaller Company Considerations

Staff Views - Guidance for Auditors of Smaller Public Companies

100

Evaluating Entity-Level Controls

� Auditor must test those entity-level controls that are important to the auditor's conclusion about whether the company has effective ICFR.

� Auditor's evaluation of entity-level controls can result in increasing or decreasing the testing that the auditor otherwise might have performed on other controls.

101

Assessing Risk of Management Override

� Additional opportunities of override exist because� Senior management is extensively involved in operations

� There are fewer levels of management

� Controls that might address risk of management override� Maintaining integrity and ethical values

� Monitoring of controls over journal entries

� Increased oversight by audit committee

� Whistleblower program

102

Evaluating Segregation of Duties and Alternative Controls

� Fewer employees – therefore limited opportunities to segregate duties

� Auditor can evaluate involvement of external parties

� Auditor can evaluate alternative controls, including

� Management review

� Management oversight

� ELC

103

Auditing Information Technology

� Off-the-shelf software commonly used

� Few users and few dedicated IT personnel

� End-user computing prevalent

� IT-generated reports used in manual controls

104

Considering Financial Reporting Competencies and Their Effect on ICFR

� Smaller companies may use outside professionals because of the lack of internal expertise

� Auditor should consider management oversight over the work of outside professionals

� Who evaluates the professional qualifications

� Who makes key judgments

� What controls exist over their work

105

Obtaining Sufficient Competent Evidence When the Company has Less Formal Documentation

� Depending on risk, inquiry combined with other procedures might provide sufficient evidence of control effectiveness

� Consider using walkthroughs to understand the flow of transactions if management documentation is limited

� Consider other documentation of processes and controls e.g., what company uses to run its business

106

Auditing Smaller, Less Complex Companies with Pervasive Control Deficiencies

� Pervasive deficiencies may adversely affect other controls, but pervasive deficiencies do not necessarily prevent an auditor from expressing an opinion on ICFR, and even if auditor cannot express an opinion on ICFR, he or she might be able to opine on financial statements

Review of Management's Quarterly ICFR Certifications

(Amended AU sec. 722)

108

� AU sec. 722 requires performance of limited procedures on management’s quarterly certifications

� These responsibilities are different from auditor’s responsibilities under AS No. 5 (audit of management’s annual certification)

� The AU sec. 722 responsibilities take effect with the first quarter after the company’s first annual assessment of ICFR

Auditor's Responsibilities

109

� Inquire of management about significant changes in the design and operation of ICFR

� Evaluate the implication of misstatements identified as part of the auditor’s other review procedures

� Determine whether any change in ICFR has, or is reasonably likely to, materially affect the company’s ICFR

Required Limited Procedures

110

� The auditor may become aware of matters indicating that modification is necessary to the management’s quarterly certification

� AU 722 requires the auditor communicate these matters to the appropriate level of management as soon as practicable

� Further communication, to the audit committee, or even resignation from the engagement could be necessary, if the appropriate action has not been taken by the issuer

Communication Requirements

111

� The auditors are not required to scope their review to identify significant deficiencies

� The auditors are required to report significant deficiencies to the audit committee, if the auditors become aware of such matters

� AU sec. 722.33 has the same definition of a significant deficiency as paragraph A11 in AS No. 5

Communication Requirements (cont'd)

Proposed Auditing Standard – Engagement Quality Review

113

Proposed Standard – Engagement Quality Review

� Required for all engagements performed pursuant to PCAOB standards

� Qualifications of a reviewer

� EQR process

� Evaluate significant judgments and conclusions

� Higher-risk areas of the engagement

� Evaluate engagement documentation

114

Proposed Standard – Engagement Quality Review (cont'd)

� Reviewer must not provide concurring approval of issuance if

� Engagement team failed to obtain sufficient competent evidence

� Engagement team reached an inappropriate overall conclusion

� Firm's report is not appropriate

� Firm is not independent

� Documentation

Current Standards-Setting Priorities

116

Current Proposed Standards-Setting Priorities*

� Risk assessment, including fraud risk assessment

� Fair value

� Specialists

� Related parties

� Confirmations

� Action plan for review of interim standards

* Priorities subject to change based on emerging issues

117

Questions?

Current Accounting and Auditing Issues

Joanne O’Rourke Hindman

John C. Abell

June 24, 2008

Dallas, TX

119

Accounting Hot Topics

1. Financial Markets Turmoil

2. Fair Value

3. Other Than Temporary Impairment (OTTI)

4. Other Impairment Risks

5. Off-balance Sheet Accounting

6. Revenue Recognition

7. IFRS

8. XBRL

9. CIFiR

10. Treasury Committee

120

Financial Markets Turmoil

� Breakdown in underwriting standards

� Erosion of market discipline in securitizations

� Flaw in credit rating agencies assessment of structured products

� Weakness in risk management practices

� Regulatory policies and disclosure practices that failed to mitigate these weaknesses

� Contagion

121

Market Turmoil: Contagion

It’s not just subprime collateral:

� Prime conforming loans

� Credit card receivables

� Auto loans

� Availability of credit

� Consumer spending

122

Market Turmoil: Contagion (cont’)

And the effects are far-reaching:

� Financial institutions of course, but also

� Pension plans

� Mutual funds

� Corporate balance sheets

123

Fair Value: Issues

� Training, bias, controls

� Valuation complexity

� FAS 157 / 159

� OTTI and Other Impairment Issues

� Disclosures

124

Fair Value: FAS 157

� Doesn’t increase the use of fair value accounting

� Adds new measurement requirements

� Exit price

� Principle (or most advantageous market)

� Market participant view

� Highest and best use

� Fair value hierarchy

� Many other nuances

� Adds new disclosure requirements

125

Fair Value: Recent Guidance

� CAQ White Papers

� Illiquid instruments

� Conduits

� Loan commitments

� PCAOB Practice Alert # 2

� Classification of fair value measurements

� Use of specialists

� Use of pricing services

� AU 328 / 332 / 336 / 324 / 342

126

Other Than Temporary Impairment (OTTI)

� HTM and AFS Securities

� Highly subjective

� FSP FAS 115-1 and 121-1, SAB 59

� Time and extent fair value below cost

� Intent and ability to hold

� Prospects of the issuer

127

Fair Value Accounting: FAS 159

� Another new standard, (FAS 159) provides companies with the option to elect fair value accounting for financial assets and liabilities

� Election permitted on a contract-by-contract basis

� Concern expressed by users of financial statements regarding comparability

� Some potential abuses have been observed and addressed

� Continued requirement for OTTI evaluation

128

Other Impairment Risks

� Loans

� Long-lived assets

� Goodwill

� Deferred tax assets

� Inventory

129

Off Balance Sheet Accounting

� A very hot issue

� Structured transactions create complex accounting and audit issues

� Auditor skepticism needed

� FAS 140 / FIN 46(R)

130

Off-balance Sheet Accounting: VIE Test

� Total equity investment at risk is not sufficient to permit the entity to finance its activities without additional support

� As a group, the holders of the equity investment at risk lack any one of the following three characteristics � Voting rights or similar rights

� Obligation to absorb the expected losses

� Right to receive the expected residual returns

� Voting rights that are not proportionate to economic interests, and the entity acts on behalf of an investor with a disproportionately small voting interest

131

Off-balance Sheet Accounting: Primary Beneficiary Test

� If an entity is a VIE, an analysis must be performed to determine the Primary Beneficiary (if any)

� The enterprise that has a variable interest that will absorb a majority of the entity’s expected losses, receive a majority of the entity’s expected residual returns, or both

� If no one holds the majority of the variable interests, no one would consolidate the VIE

� FIN 46(R) is an economic model

132

Off-Balance Sheet Issues: Reconsideration

� An enterprise with an interest in a VIE shall reconsider whether it is the PB if the VIE’s governing documents or contractual arrangements are changed in a manner that reallocates between the existing PB and other unrelated parties the:

� Obligation to absorb the expected losses of the VIE; or

� Right to receive the expected residual returns of the VIE

� PB to reconsider if it disposes of all or part of its variable interests or if the VIE issues new variable interests to parties other than the PB

� Non-PB to reconsider if it acquires additional variable interests in the VIE

� Analysis at reconsideration must consider current market conditions

133

Revenue Recognition

� SEC’s top questioned accounting area

� Allowance for sales returns, rebates, chargebacks, etc.

� Collaboration agreements

� Multi-element arrangements

� Vendor rights and obligations

� Presentation of product and service revenues

134

IFRS

� “Allowing filing in IFRS for U.S. issuers is something we want to accomplish this year,” said SEC Chairman Cox on February 5, 2008

� Steps have been made toward expanding the use of IFRS in the US� Elimination of US GAAP reconciliation for foreign private

issuers who use IFRS as adopted by the IASB

� Concept Release allowing US issuers to file under IFRS

� Canada is adopting IFRS in 2011

� Issues:� Target dates and transition method

� Education

� Addressing specific issues (e.g. LIFO)

� Role of FASB and SEC

� IASB funding, governance and oversight

135

XBRL

� Updated US GAAP taxonomies released

� Preparer’s XBRL guide available

� IFRS taxonomies

� SEC XBRL-tools

� SEC Proposed Rule on use of XBRL

� Mandatory

� Phased-in

� Auditor assurance

136

CIFiR

� Also known as the Pozen Committee

� Launched in August 2007

� Created to tackle complexity in financial disclosures

� Addressing:

� Substantive complexity

� Standard setting

� Audit process and compliance

� Delivering financial information

� Final report expected in August 2008

137

CIFiR: Preliminary Proposals

� Substantive Complexity

� GAAP should be based on business activities, not industries, and similar activities should be accounted for in a similar manner

� GAAP should be based on a presumption that scope exceptions should not exist (i.e. GAAP should not provide additional optionality)

� No bright lines

138

CIFiR: Preliminary Proposals (cont’d)

� Standard-Setting Process

� User / investor involvement in the standard-setting process is key to improved financial reporting

� SEC should assist the Financial Accounting Foundation (FAF) in its guidance over the FASB

� SEC to encourage FASB to further improve standard-setting process and timeliness

� Reduction in number of parties interpreting GAAP and issuing implementation guidance

139

CIFiR: Preliminary Proposals (cont’d)

� Audit Process and Compliance and Delivering Financial Information

� SEC or FASB should supplement existing guidance related to materiality and correction of errors

� Accounting and audit “statement of policy”

� Mandatory phase-in of XBRL

� Assurance on XBRL

140

Treasury Committee

� Purpose - develop recommendations to:

� Increase investor protection and

� Enhance sustainability of public company auditing profession

� Preliminary recommendations released, final report expected in the summer

� Key recommendations of the Human Capital Subcommittee:

� Develop and continuously update a market-driven academic curriculum for accounting students

� Ensure sufficient supply of accounting and tax faculty

� Improve the representation of minorities in the profession

141

Treasury Committee (cont’)

� Key recommendations of the Firm Structure and Finances Subcommittee:

� Create a center to share fraud prevention/detection experiences

� Encourage states to adopt CPA mobility provisions

� Explore the possibility of firms appointing independent members to firm boards to improve governance and transparency of audit process

� Urge SEC to require disclosure of reason for: 1) any auditor change; 2) audit partner change prior to rotation period end.

� Key recommendations of the Concentration and Competition Subcommittee:

� Promote the growth of smaller auditing firms

� Create a mechanism to preserve and rehabilitate any troubled larger public accounting firm

� Promote better understanding and compliance with independence rules

� Develop key indicators of audit quality and effectiveness for possible public disclosure by audit firms.

142

Managing Complexity

� Complete understanding of transaction, including terms, economics, rights, obligations, risks and rewards

� Adequate accounting resources: knowledgeable, experienced and unbiased

� Ongoing auditor discussions

� Issue identification and evaluation

� Management and Audit Committee involvement

� Potentially more than one correct answer

� Financial statement transparency

143

Questions?

144

Kevin WoodyKevin Woody

Branch ChiefBranch Chief

Division of Corporation FinanceDivision of Corporation Finance

June 3, 2008June 3, 2008

SEC Staff Review of Common SEC Staff Review of Common

Financial Reporting Issues Financial Reporting Issues

Facing Smaller IssuersFacing Smaller Issuers

145

AgendaAgenda

��Overview Overview

��Recent DevelopmentsRecent Developments

��The Comment Letter ProcessThe Comment Letter Process

��Financial Reporting Issues Frequently Raised Financial Reporting Issues Frequently Raised

in Comment Lettersin Comment Letters

��ResourcesResources

146

DisclaimerDisclaimer

The Securities and Exchange Commission, The Securities and Exchange Commission,

as a matter of policy, disclaims as a matter of policy, disclaims

responsibility for any private publication or responsibility for any private publication or

statement by any of its employees. statement by any of its employees.

Therefore, the views expressed today are Therefore, the views expressed today are

those of the speaker, and do not those of the speaker, and do not

necessarily reflect the views of the necessarily reflect the views of the

Commission or the other members of the Commission or the other members of the

staff of the Commission.staff of the Commission.

147

OverviewOverview

148

OverviewOverview

Divisions and Offices reporting to the Office of the Divisions and Offices reporting to the Office of the Chairman Chairman

�� Four Divisions Four Divisions

�� Corporation FinanceCorporation Finance

�� Enforcement Enforcement

�� Investment Management Investment Management

�� Trading and Markets Trading and Markets

�� Eighteen Offices Eighteen Offices

�� Chief Accountant (includes Interactive Disclosure)Chief Accountant (includes Interactive Disclosure)

�� Compliance Inspections and Examinations Compliance Inspections and Examinations

�� Economic AnalysisEconomic Analysis

�� 15 Others15 Others

149

Division of Corporation Finance Division of Corporation Finance

(DCF)(DCF)

Mission Mission –– ““To see that investors are provided with To see that investors are provided with material information in order to make informed material information in order to make informed investment decisions investment decisions —— both when a company both when a company initially offers its stock to the public and on a initially offers its stock to the public and on a regular basis as it continues to give information to regular basis as it continues to give information to the marketplace.the marketplace.””

�� Review the disclosure documents filed by public Review the disclosure documents filed by public companies (including initial registrations)companies (including initial registrations)

�� Provide interpretive assistance to companies on SEC Provide interpretive assistance to companies on SEC rules and forms rules and forms

�� Propose new and revised rules to the CommissionPropose new and revised rules to the Commission

Organization Organization �� 11 industry groups 11 industry groups

�� Support OfficesSupport Offices

150

Division of Corporation Finance Division of Corporation Finance

(DCF)(DCF)

Assistant Director

Senior AssistantChief

Accountant

Accounting BranchChiefs (3)

Staff Accountants

Legal Branch Chief Special Counsel

Legal ExaminersAssistant ChiefAccountant

151

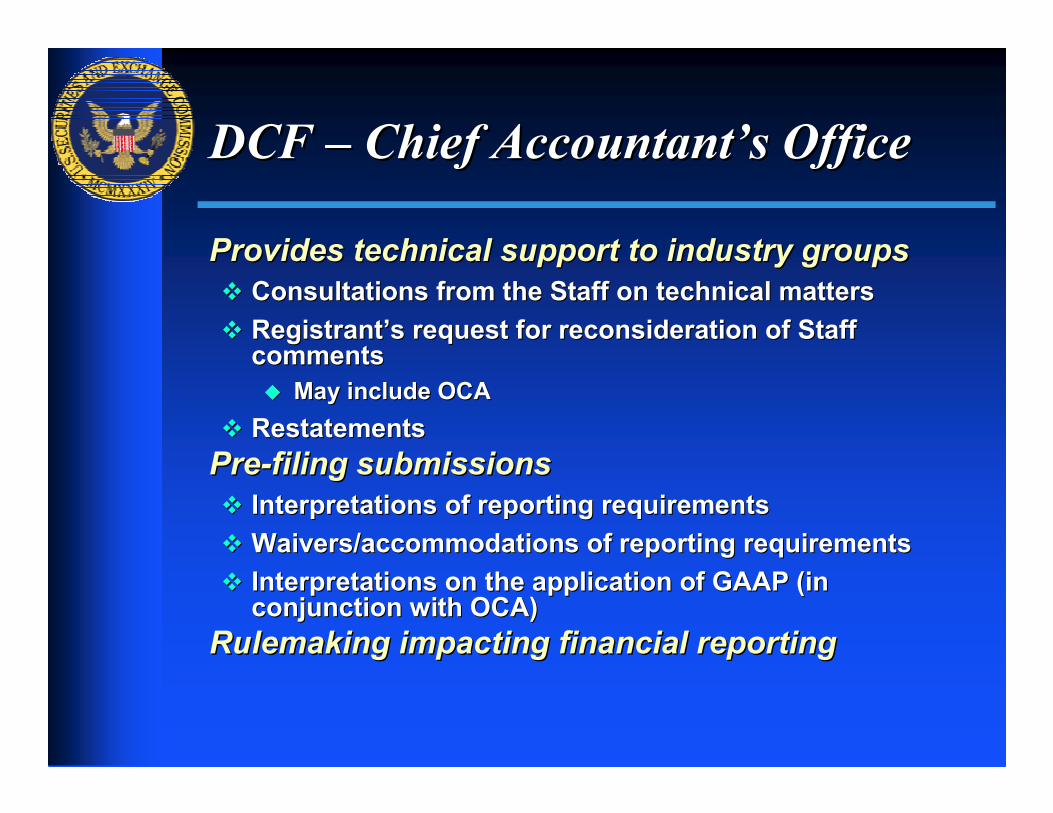

DCF DCF –– Chief AccountantChief Accountant’’s Offices Office

Provides technical support to industry groupsProvides technical support to industry groups

�� Consultations from the Staff on technical mattersConsultations from the Staff on technical matters

�� RegistrantRegistrant’’s request for reconsideration of Staff s request for reconsideration of Staff commentscomments

�� May include OCAMay include OCA

�� RestatementsRestatements

PrePre--filing submissionsfiling submissions

�� Interpretations of reporting requirementsInterpretations of reporting requirements

�� Waivers/accommodations of reporting requirementsWaivers/accommodations of reporting requirements

�� Interpretations on the application of GAAP (in Interpretations on the application of GAAP (in conjunction with OCA)conjunction with OCA)

Rulemaking impacting financial reportingRulemaking impacting financial reporting

152

Office of the Chief Accountant Office of the Chief Accountant

�� Carries out the dayCarries out the day--toto--day work to assist the Commission in its day work to assist the Commission in its oversight role over the FASB, which the Commission has oversight role over the FASB, which the Commission has designated as a privatedesignated as a private--sector accounting standard settersector accounting standard setter

�� Also carries out oversight responsibilities related to the Also carries out oversight responsibilities related to the PCAOB PCAOB

�� Consults with registrants and auditors regarding the Consults with registrants and auditors regarding the application of accounting, auditing, and independence application of accounting, auditing, and independence standardsstandards

�� www.sec.gov/info/accountants/ocasubguidance.htmwww.sec.gov/info/accountants/ocasubguidance.htm

�� OCA and DCF work together closely on: OCA and DCF work together closely on:

�� Consultations on certain technical matters relating to the Consultations on certain technical matters relating to the application of GAAPapplication of GAAP

�� Rulemaking impacting financial reportingRulemaking impacting financial reporting

�� Consultations from registrantsConsultations from registrants

�� PrePre--clearanceclearance

�� Staff commentsStaff comments

153

Recent DevelopmentsRecent Developments

154

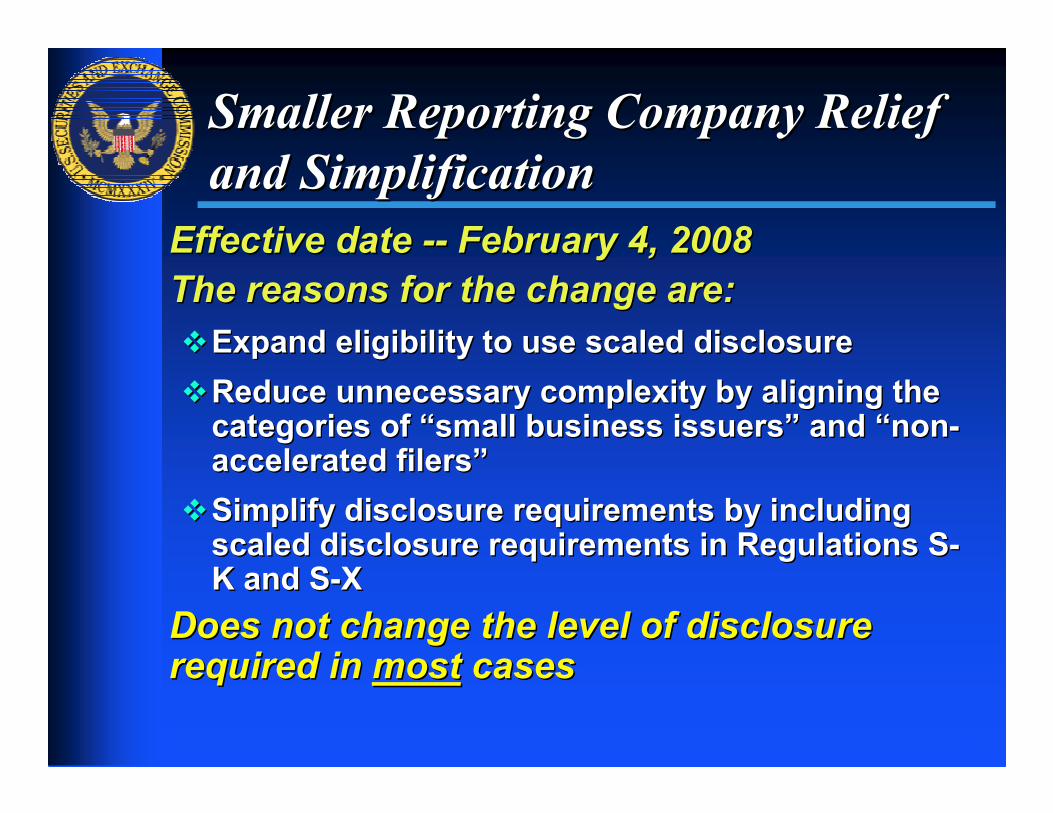

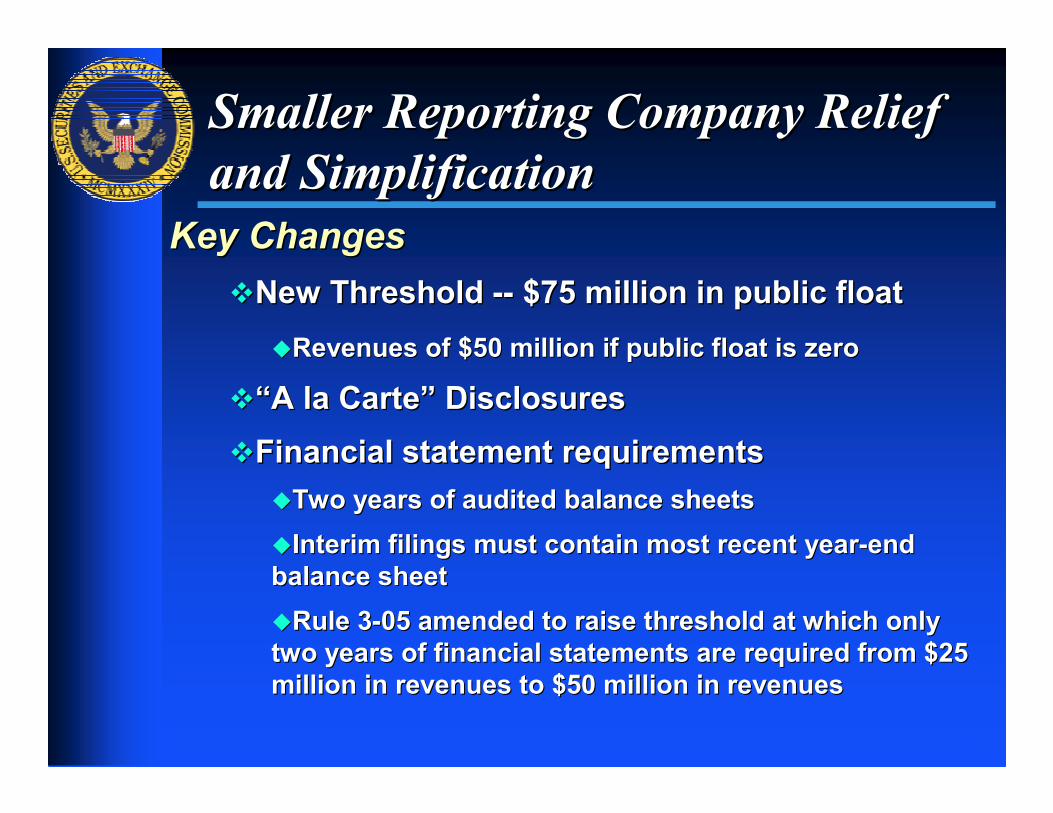

Smaller Reporting Company Relief Smaller Reporting Company Relief

and Simplificationand Simplification

Effective date Effective date ---- February 4, 2008February 4, 2008

The reasons for the change are:The reasons for the change are:

��Expand eligibility to use scaled disclosureExpand eligibility to use scaled disclosure

��Reduce unnecessary complexity by aligning the Reduce unnecessary complexity by aligning the categories of categories of ““small business issuerssmall business issuers”” and and ““nonnon--accelerated filersaccelerated filers””

��Simplify disclosure requirements by including Simplify disclosure requirements by including scaled disclosure requirements in Regulations Sscaled disclosure requirements in Regulations S--K and SK and S--X X

Does not change the level of disclosure Does not change the level of disclosure required in required in mostmost casescases

155

Smaller Reporting Company Relief Smaller Reporting Company Relief

and Simplificationand Simplification

Key ChangesKey Changes

��New Threshold New Threshold ---- $75 million in public float$75 million in public float

��Revenues of $50 million if public float is zeroRevenues of $50 million if public float is zero

��““A la CarteA la Carte”” DisclosuresDisclosures

��Financial statement requirementsFinancial statement requirements

��Two years of audited balance sheets Two years of audited balance sheets

��Interim filings must contain most recent yearInterim filings must contain most recent year--end end

balance sheetbalance sheet

��Rule 3Rule 3--05 amended to raise threshold at which only 05 amended to raise threshold at which only

two years of financial statements are required from $25 two years of financial statements are required from $25

million in revenues to $50 million in revenuesmillion in revenues to $50 million in revenues

156

Smaller Reporting Company Relief Smaller Reporting Company Relief

and Simplificationand Simplification

Where can I find more information?Where can I find more information?

�� The final rule release The final rule release ----http://www.sec.gov/rules/final/2007/33http://www.sec.gov/rules/final/2007/33--8876.pdf8876.pdf

�� The Small Entity Compliance Guide The Small Entity Compliance Guide ----http://www.sec.gov/info/smallbus/secg/smrepcosysguid.http://www.sec.gov/info/smallbus/secg/smrepcosysguid.pdfpdf

�� Smaller Reporting Company Compliance and Disclosure Smaller Reporting Company Compliance and Disclosure Interpretations Interpretations ---- http://www.sec.gov/info/smallbus/srchttp://www.sec.gov/info/smallbus/src--cdinterps.htmcdinterps.htm

157

Other SEC Key DevelopmentsOther SEC Key Developments

��SarbanesSarbanes--OxleyOxley

��Proposed Rule to Delay Requirement for Proposed Rule to Delay Requirement for Attestation of Effectiveness Internal Control Attestation of Effectiveness Internal Control Over Financial Reporting of NonOver Financial Reporting of Non--Accelerated Accelerated Filers (Release 33Filers (Release 33--8889)8889)

��Would delay Section 404(b) requirement Would delay Section 404(b) requirement until fiscal years ended after 12/15/09until fiscal years ended after 12/15/09

��Costs and Benefits Study of SarbanesCosts and Benefits Study of Sarbanes--Oxley Oxley Act Section 404 (Press Release 2008Act Section 404 (Press Release 2008--8)8)

�� International Financial Reporting StandardsInternational Financial Reporting Standards

��eXtensibleeXtensible Business Reporting Language Business Reporting Language (XBRL)(XBRL)

��Committee on Improvements to Financial Committee on Improvements to Financial Reporting recommendations (CIFiR)Reporting recommendations (CIFiR)

158

Key US GAAP DevelopmentsKey US GAAP Developments

��Fair Value Accounting Fair Value Accounting –– SFAS 159 and 157SFAS 159 and 157

�� Effective for fiscal years beginning on or after 11/15/07Effective for fiscal years beginning on or after 11/15/07

��Business Combinations and Business Combinations and NoncontrollingNoncontrolling

interestsinterests–– SFAS 141(R) and SFAS 160SFAS 141(R) and SFAS 160

�� Effective for fiscal years beginning on or after 12/15/08Effective for fiscal years beginning on or after 12/15/08

��FASB Accounting Standards Codification FASB Accounting Standards Codification ----

asc.fasb.orgasc.fasb.org

�� OneOne--year Verification Phaseyear Verification Phase

��SAB 74 SAB 74 –– Requires disclosure regarding impact of Requires disclosure regarding impact of

new standards new standards

159

The Comment Letter ProcessThe Comment Letter Process

160

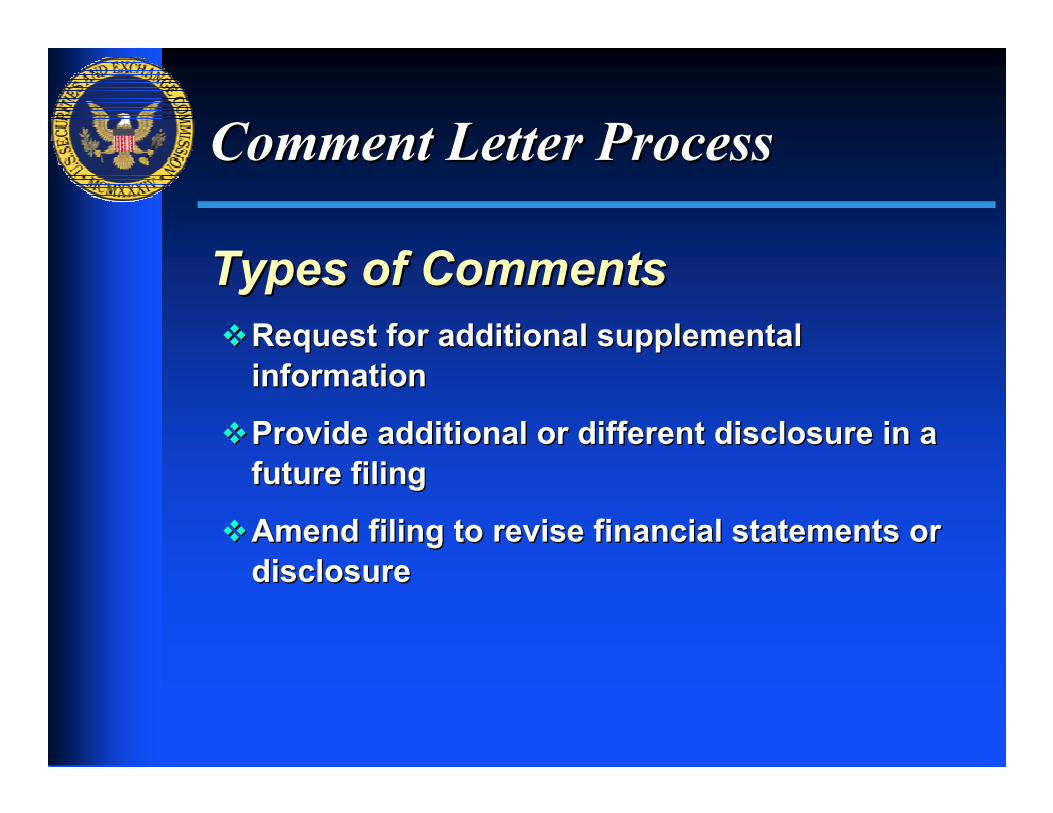

Comment Letter ProcessComment Letter Process

Filings Subject to Staff ReviewFilings Subject to Staff Review

�� IPOs, other registration statements, annual IPOs, other registration statements, annual

reports, and proxy statements as selected by reports, and proxy statements as selected by

the SECthe SEC’’s confidential internal screening s confidential internal screening

criteria and Sarbanescriteria and Sarbanes--Oxley requirementsOxley requirements

�� Item 4.01 and Item 4.02 Form 8Item 4.01 and Item 4.02 Form 8--KsKs

161

Comment Letter ProcessComment Letter Process

Types of CommentsTypes of Comments

��Request for additional supplemental Request for additional supplemental

informationinformation

��Provide additional or different disclosure in a Provide additional or different disclosure in a

future filingfuture filing

��Amend filing to revise financial statements or Amend filing to revise financial statements or

disclosuredisclosure

162

Comment Letter ProcessComment Letter Process

Best Practices for Resolving IssuesBest Practices for Resolving Issues

�� Prepare a thorough response Prepare a thorough response

�� An invitation to a dialogueAn invitation to a dialogue

�� Key response to initial commentKey response to initial comment

�� Indicate specifically where revisions have been madeIndicate specifically where revisions have been made

�� Discuss supporting authoritative literature in detailDiscuss supporting authoritative literature in detail

�� Inform Staff if you are unable to respond by the Inform Staff if you are unable to respond by the

requested daterequested date

�� Document accounting decisions contemporaneouslyDocument accounting decisions contemporaneously

163

Financial Reporting Issues Financial Reporting Issues

Frequently Raised in Comment Frequently Raised in Comment

LettersLetters

164

Financial Reporting Issues Frequently Financial Reporting Issues Frequently

Raised in Comment LettersRaised in Comment Letters

Revenue RecognitionRevenue Recognition

Business Combinations (incl. Reverse Mergers)Business Combinations (incl. Reverse Mergers)

Equity TransactionsEquity Transactions

Embedded Conversion Options and WarrantsEmbedded Conversion Options and Warrants

ManagementManagement’’s Discussion and Analysiss Discussion and Analysis

Forms 8Forms 8--K on Item 4.01 and Item 4.02K on Item 4.01 and Item 4.02

Internal Controls over Financial ReportingInternal Controls over Financial Reporting

CertificationsCertifications

Audit ReportsAudit Reports

Other Areas (see Appendix)Other Areas (see Appendix)

165

Revenue RecognitionRevenue Recognition

Common Areas of CommentCommon Areas of Comment

��Policy disclosures (i.e., SAB 104) Policy disclosures (i.e., SAB 104)

�� ““BoilerplateBoilerplate”” disclosuresdisclosures

��Disclosure should be specific to companyDisclosure should be specific to company’’s s

revenue streamsrevenue streams

��EITF 00EITF 00--21 21 –– MultipleMultiple--Element ArrangementsElement Arrangements

��EITF 99EITF 99--19 19 –– Gross versus Net Revenue Gross versus Net Revenue

RecognitionRecognition

166

Business CombinationsBusiness Combinations

Business combination or asset purchaseBusiness combination or asset purchase

�� EITF 98EITF 98--33

�� Rule 11Rule 11--01(d) of Regulation S01(d) of Regulation S--XX

Purchase Price AllocationPurchase Price Allocation

�� Allocated to all assets and liabilities acquired based Allocated to all assets and liabilities acquired based upon fair valueupon fair value

�� Fair value of securities issuedFair value of securities issued

DisclosuresDisclosures

�� Annual vs. Interim periodsAnnual vs. Interim periods

167

Business CombinationsBusiness Combinations

Reverse Acquisitions/RecapitalizationsReverse Acquisitions/Recapitalizations

�� Determination of the accounting acquirerDetermination of the accounting acquirer

�� Consider all factors in paragraph 17 of SFAS 141Consider all factors in paragraph 17 of SFAS 141

�� Cost of the acquired entity Cost of the acquired entity

�� Depends on whether it is a business combination or Depends on whether it is a business combination or recapitalizationrecapitalization

�� Accounting acquirerAccounting acquirer’’s audited F/S presented for all s audited F/S presented for all historical periods in subsequent reportshistorical periods in subsequent reports

�� Earnings per share recast to reflect exchange ratioEarnings per share recast to reflect exchange ratio

�� Eliminate retained earnings of shell or legal acquirerEliminate retained earnings of shell or legal acquirer

�� Common stock of shell or legal acquirer continuesCommon stock of shell or legal acquirer continues

�� Form 8Form 8--K requirementsK requirements

168

Business CombinationsBusiness Combinations

Entities Under Common ControlEntities Under Common Control

�� Net assets of Net assets of acquireeacquiree are recorded at historical basisare recorded at historical basis

�� Determining control groupDetermining control group

Separate Financial Statements of an Acquired Separate Financial Statements of an Acquired

BusinessBusiness

�� Rule 3Rule 3--05/Rule 805/Rule 8--04 of Regulation S04 of Regulation S--XX

Predecessor Financial StatementsPredecessor Financial Statements

�� Registrant succeeds to substantially all of the Registrant succeeds to substantially all of the

business of another entitybusiness of another entity

�� RegistrantRegistrant’’s own operations are relatively insignificants own operations are relatively insignificant

169

Equity TransactionsEquity Transactions

Fair Value DeterminationFair Value Determination

�� If publicly traded, use quoted market price If publicly traded, use quoted market price

�� No discounts for illiquidity, trading restrictions or block No discounts for illiquidity, trading restrictions or block discounts. discounts.

�� If stock not publicly tradedIf stock not publicly traded

�� Contemporaneous equity transactions with third partiesContemporaneous equity transactions with third parties

�� Fair value of the services or goods provided may be used to Fair value of the services or goods provided may be used to measure the transaction, if more reliablemeasure the transaction, if more reliable

DisclosureDisclosure

�� All major assumptions used to value stock options, warrants and All major assumptions used to value stock options, warrants and other equity instrumentsother equity instruments

�� Footnotes Footnotes

�� MD&A (critical accounting estimates)MD&A (critical accounting estimates)

�� Consider sensitivity analysisConsider sensitivity analysis

170

Embedded Conversion Options and Embedded Conversion Options and

Freestanding WarrantsFreestanding Warrants

Primary issues:Primary issues:

�� Bifurcation of conversion optionBifurcation of conversion option

�� Classification as liability or equityClassification as liability or equity

Instruments involved:Instruments involved:

�� Convertible debtConvertible debt

�� Convertible preferred stockConvertible preferred stock

�� Freestanding warrants to buy registrantFreestanding warrants to buy registrant’’s s

stockstock

171

Embedded Conversion Options and Embedded Conversion Options and

Freestanding Warrants Freestanding Warrants (cont(cont’’d)d)

AnalysisAnalysis

��Is the instrument within scope of SFAS 150?Is the instrument within scope of SFAS 150?

��Analyze under SFAS 133 Analyze under SFAS 133 –– two routestwo routes

1.1.FreestandingFreestanding

•• Account for as a derivative under SFAS 133Account for as a derivative under SFAS 133

•• Perform 00Perform 00--19 Analysis19 Analysis

•• Account for as equityAccount for as equity

•• Account for as a liabilityAccount for as a liability

2.2.EmbeddedEmbedded

•• Do not bifurcate under SFAS 133 (this often requires Do not bifurcate under SFAS 133 (this often requires performing an EITF 00performing an EITF 00--19 Analysis which may require 19 Analysis which may require bifurcation)bifurcation)

•• Consider ASR 268 and APB 14Consider ASR 268 and APB 14

•• BCF under EITF 98BCF under EITF 98--5 and 005 and 00--2727

•• Bifurcate Bifurcate –– Account as derivative liability (SFAS 133)Account as derivative liability (SFAS 133)

172

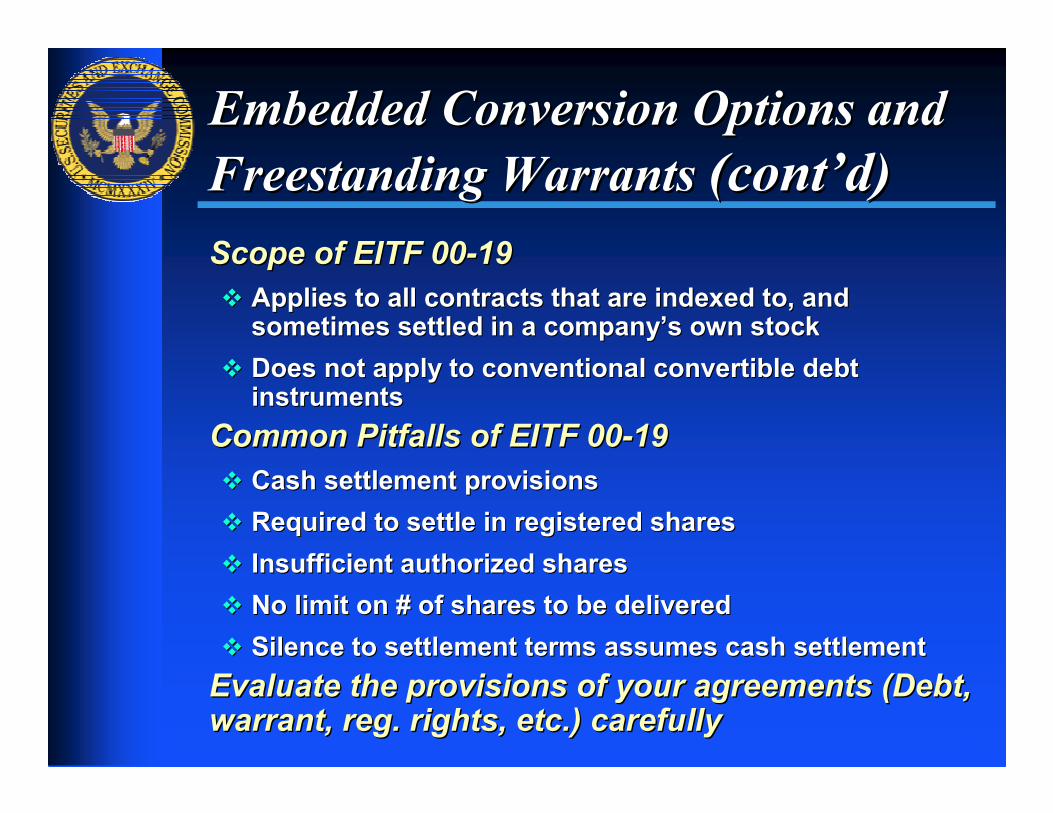

Embedded Conversion Options and Embedded Conversion Options and

Freestanding Warrants Freestanding Warrants (cont(cont’’d)d)

Scope of EITF 00Scope of EITF 00--1919

�� Applies to all contracts that are indexed to, and Applies to all contracts that are indexed to, and sometimes settled in a companysometimes settled in a company’’s own stocks own stock

�� Does not apply to conventional convertible debt Does not apply to conventional convertible debt instrumentsinstruments

Common Pitfalls of EITF 00Common Pitfalls of EITF 00--1919

�� Cash settlement provisionsCash settlement provisions

�� Required to settle in registered sharesRequired to settle in registered shares

�� Insufficient authorized sharesInsufficient authorized shares

�� No limit on # of shares to be deliveredNo limit on # of shares to be delivered

�� Silence to settlement terms assumes cash settlementSilence to settlement terms assumes cash settlement

Evaluate the provisions of your agreements (Debt, Evaluate the provisions of your agreements (Debt, warrant, reg. rights, etc.) carefullywarrant, reg. rights, etc.) carefully

173

ManagementManagement’’s Discussion & s Discussion &

Analysis (MD&A)Analysis (MD&A)

Release Nos. 33Release Nos. 33--6835 and 336835 and 33--83508350

Best PracticesBest Practices

�� ExecutiveExecutive--level overview level overview

�� Critical accounting estimates Critical accounting estimates

�� Provide insight into the quality and variability of financial Provide insight into the quality and variability of financial informationinformation

�� Comparative results of operations that are thorough and Comparative results of operations that are thorough and address the address the causal factorscausal factors of changeof change

�� Liquidity and capital resources Liquidity and capital resources

�� Enhanced analysis and explanation of the sources and uses of Enhanced analysis and explanation of the sources and uses of cashcash

�� Consider categories reported on statement of cash flowsConsider categories reported on statement of cash flows

�� Address going concern mattersAddress going concern matters

�� Consider enhanced disclosure regarding debt instruments, Consider enhanced disclosure regarding debt instruments, guarantees and related covenants.guarantees and related covenants.

174

Form 8Form 8--KK

Form 8Form 8--K interpretations updated on April 10, 2008 at K interpretations updated on April 10, 2008 at http://www.sec.gov/divisions/corpfin/guidance/8http://www.sec.gov/divisions/corpfin/guidance/8--kinterp.htmkinterp.htm

All Item 4.01 and Item 4.02 8All Item 4.01 and Item 4.02 8--K filings reviewed for K filings reviewed for strict compliancestrict compliance

Frequent Item 4.01 commentsFrequent Item 4.01 comments

�� Failure to specify whether former accountants resigned, Failure to specify whether former accountants resigned, declined to stand for redeclined to stand for re--election, or were dismissed and the election, or were dismissed and the date date

�� Reverse acquisitionsReverse acquisitions

�� Accounting firm mergersAccounting firm mergers

�� Exhibit 16 letterExhibit 16 letter

175

Form 8Form 8--KK

Most Item 4.02 comments relate to Item Most Item 4.02 comments relate to Item

4.02(a)4.02(a)

��Triggering event other than nonTriggering event other than non--reliance reliance

conclusion (e.g., completion of restatement) conclusion (e.g., completion of restatement)

��Unclear statement regarding nonUnclear statement regarding non--reliance reliance

��Brief description of facts lacking or unclearBrief description of facts lacking or unclear

��““Stealth restatementsStealth restatements””

176

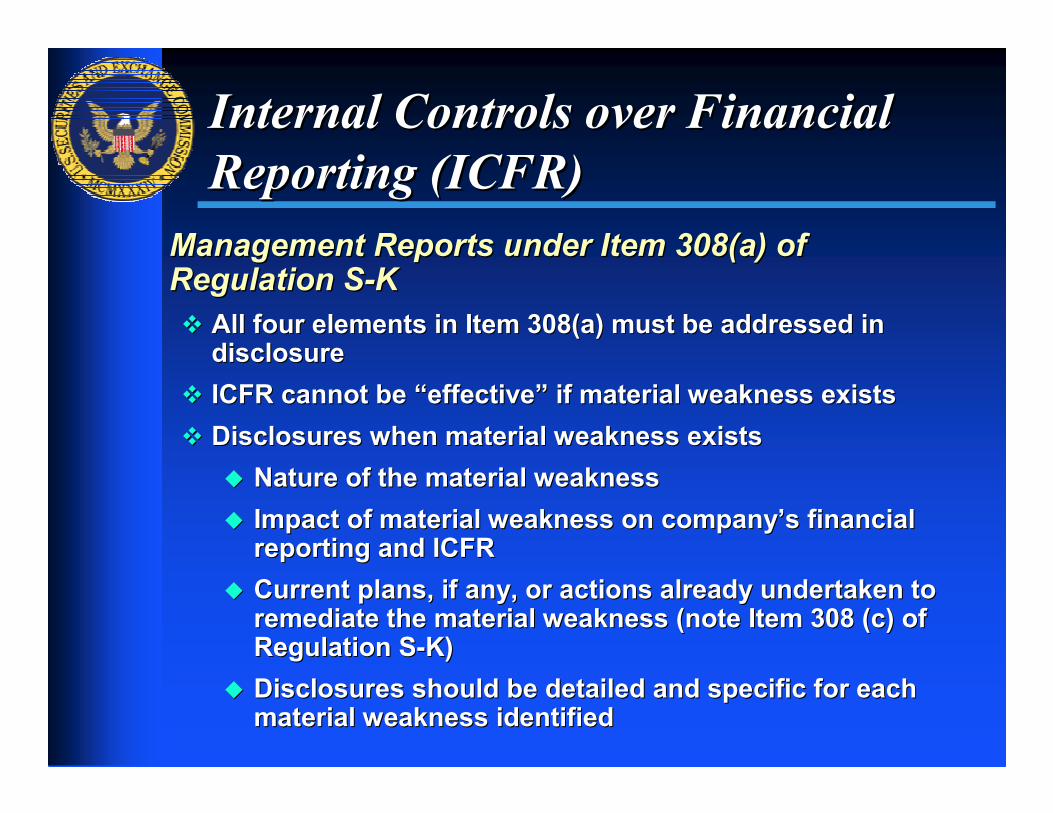

Internal Controls over Financial Internal Controls over Financial

Reporting (ICFR)Reporting (ICFR)

Management Reports under Item 308(a) of Management Reports under Item 308(a) of Regulation SRegulation S--KK

�� All four elements in Item 308(a) must be addressed in All four elements in Item 308(a) must be addressed in disclosuredisclosure

�� ICFR cannot be ICFR cannot be ““effectiveeffective”” if material weakness existsif material weakness exists

�� Disclosures when material weakness existsDisclosures when material weakness exists

�� Nature of the material weaknessNature of the material weakness

�� Impact of material weakness on companyImpact of material weakness on company’’s financial s financial reporting and ICFRreporting and ICFR

�� Current plans, if any, or actions already undertaken to Current plans, if any, or actions already undertaken to remediate the material weakness (note Item 308 (c) of remediate the material weakness (note Item 308 (c) of Regulation SRegulation S--K)K)

�� Disclosures should be detailed and specific for each Disclosures should be detailed and specific for each material weakness identifiedmaterial weakness identified

177

Internal Controls over Financial Internal Controls over Financial

Reporting (ICFR)Reporting (ICFR)

Auditor attestation under Item 308(b) of Auditor attestation under Item 308(b) of

Regulation SRegulation S--KK

��No specific requirement for location in filingNo specific requirement for location in filing

�� Generally in close proximity to financial statement opinion or Generally in close proximity to financial statement opinion or

managementmanagement’’s reports report

��Not currently required for nonNot currently required for non--accelerated filersaccelerated filers

�� If auditor attestation not included, registrant must If auditor attestation not included, registrant must

include statement that ICFR has not been attested include statement that ICFR has not been attested

to by auditor (See Item 308T of Regulation Sto by auditor (See Item 308T of Regulation S--K)K)

178

CEO/CFO CertificationsCEO/CFO Certifications

Certifications should not deviate from specific form Certifications should not deviate from specific form

and content in Item 601(b)(31)(ii) of Regulation Sand content in Item 601(b)(31)(ii) of Regulation S--KK

Internal control over financial reporting (ICFR)Internal control over financial reporting (ICFR)

�� SEC Release 33SEC Release 33--8238 (June 2003) permitted exclusion of:8238 (June 2003) permitted exclusion of:

�� introductory language in paragraph 4 referring to introductory language in paragraph 4 referring to

responsibility for establishing and maintaining ICFRresponsibility for establishing and maintaining ICFR

�� Paragraph 4(b) (certifying officer has designed or Paragraph 4(b) (certifying officer has designed or

supervised the design of ICFR)supervised the design of ICFR)

�� Starting with first period in which management is required Starting with first period in which management is required

to assess ICFR, these statements can no longer be to assess ICFR, these statements can no longer be

excludedexcluded

179

Audit ReportsAudit Reports

Auditor must be PCAOB registered Auditor must be PCAOB registered

accountant that meets all of the accountant that meets all of the

requirements of Article 2 requirements of Article 2

Audit reports must be filed for all financial Audit reports must be filed for all financial

statements required to be auditedstatements required to be audited

If audit report refers to the If audit report refers to the report(sreport(s) of ) of

another another auditor(sauditor(s), the registrant must ), the registrant must

include those reports in the filinginclude those reports in the filing

180

ResourcesResources

181

ResourcesResources

SEC Website SEC Website –– www.sec.govwww.sec.gov

�� Information for Accountants Information for Accountants --

www.sec.gov/about/offices/oca.htmwww.sec.gov/about/offices/oca.htm

�� Information for Small Businesses Information for Small Businesses --

www.sec.gov/info/smallbus.shtmlwww.sec.gov/info/smallbus.shtml

��Division of Corporation Finance Division of Corporation Finance --

www.sec.gov/divisions/corpfin.shtmlwww.sec.gov/divisions/corpfin.shtml

FASB Website FASB Website –– www.fasb.orgwww.fasb.org

SEC Regulations Committee SEC Regulations Committee ----

thecaq.org/resources/secregs.htmthecaq.org/resources/secregs.htm

182

QuestionsQuestions??????

Key Telephone NumbersKey Telephone Numbers

DCF Chief AccountantDCF Chief Accountant’’s Office (202) 551s Office (202) 551--34003400

DCF Office of the Chief Counsel (202) 551DCF Office of the Chief Counsel (202) 551--35003500

Office of the Chief Accountant (202) 551Office of the Chief Accountant (202) 551--53005300

183

AppendixAppendix

184

Financial Statement ClassificationFinancial Statement Classification

Registrants that qualify as smaller reporting companies Registrants that qualify as smaller reporting companies reporting under Article 8 of Regulation Sreporting under Article 8 of Regulation S--XX

�� Need not apply the other form and content requirements in Need not apply the other form and content requirements in Regulation SRegulation S--X except:X except:

�� Report and qualifications of the independent accountant Report and qualifications of the independent accountant (Article 2)(Article 2)

�� Description of accounting policies (Rule 4Description of accounting policies (Rule 4––08(n))08(n))

�� Companies engaged in oil and gas producing activities (Rule 4Companies engaged in oil and gas producing activities (Rule 4––10)10)

�� Guidance outside of Regulation SGuidance outside of Regulation S--X continues to apply that may X continues to apply that may result in comments. For example:result in comments. For example:

�� Equity vs. nonEquity vs. non--equity (EITF Topic Dequity (EITF Topic D--98 and SFAS No. 150)98 and SFAS No. 150)

�� Operating, investing, and financing cash flows (SFAS No. 95)Operating, investing, and financing cash flows (SFAS No. 95)

�� Discontinued operations (SFAS No. 144)Discontinued operations (SFAS No. 144)

�� StockStock--based compensation expense (SAB Topic 14F)based compensation expense (SAB Topic 14F)

185

Financial Statement ClassificationFinancial Statement Classification

Registrants that do not qualify to report under Article Registrants that do not qualify to report under Article

8 of Regulation S8 of Regulation S--XX

�� Subject to more detailed classification rules (e.g., Article 5 Subject to more detailed classification rules (e.g., Article 5

of Regulation Sof Regulation S--X for commercial and industrial companies)X for commercial and industrial companies)

�� Rule 5Rule 5--02 02 -- balance sheetsbalance sheets

�� Rule 5Rule 5--03 03 –– income statementsincome statements

�� These additional rules most often result in comments These additional rules most often result in comments

relating to Rule 5relating to Rule 5--0303

�� Components of revenue Components of revenue

�� Cost of salesCost of sales

�� Classification of shareClassification of share--based paymentsbased payments

�� Operating vs. nonOperating vs. non--operatingoperating