gaap accounting update iowa - iasa.org › iasadocs › chapter › centralstates... · accounting...

TRANSCRIPT

GAAP Accounting Update

September 12, 2017

Alicia SpanburgJeff Turner

Agenda

GAAP Update

1. Insurance Contracts

• Long Duration Exposure Draft

• Short Duration Disclosures

2. Financial Instruments

• Recognition and Measurement

• Impairment

3. Revenue Recognition

4. Leases

5. Premium amortization on callable debt securities

6. Presentation of pension costs

2PwC

On the horizon

Insurance

Insurance overview

Impacts• FASB and IASB 2013 EDs had proposed fundamental changes to the

accounting for insurance contracts

• In February 2014, the FASB changed course, toward making targeted improvements to insurer accounting/disclosures:

- Q2 2015: ASU issued requiring additional disclosure for claim liabilities,effective 2016

- 2014-2016 deliberations: Proposed targeted accounting changes for long duration contracts; exposure draft issued in September 2016

Enhanced disclosures forclaim liabilities and targetedimprovements to the accounting for long durationinsurance contracts.

Improve andsimplify the financial reporting requirements

Talkingtheory

Getting feedback

Coming soon

PwC4

FASB targeted improvements – long durationcontracts

Proposed improvements:

• Annual (or more frequent) updating of cash flow assumptionsfor liability for future policy benefits using retrospective method

• Quarterly update of discount rate assumptions through OCI

• High-quality fixed income instrument yield (proxy liabilityrate) vs. “expected investment yield” used today

• Simplified DAC amortization:

• Based on insurance in-force, or straight-line

• No interest accretion and no impairment test

• Variable product/separate account guarantees (GMXBs) withcapital market risk at fair value; “instrument-specific creditrisk” adjustment through OCI

• Detailed disaggregated rollforwards of liabilities and DAC;qualitative and quantitative information about estimates

• Retrospective transition for liabilities; prospective for DAC

FASB proposed ED “targeted improvements” are pervasive

Responding to user requests to update assumptions, simplify, and improve consistency

PwC5

FASB targeted improvements – long durationIssue FASB tentative decision Contracts impacted

Updating of • Annually (same time each year) or more frequently if actual cash flow experience or other evidence indicates need for revision assumptions • Retrospective unlocking:

• Revised net premium ratio as of contract inception would be computed using actual historical experience and updated cash flow assumptions

• At-inception discount rate used for interest accretion expense and the revised net premium ratio

• No provision for adverse deviation• Net premium ratio capped at 100%, replacing the premium

deficiency test• Liability cannot be less than zero• Maintenance expenses are period costs

• Traditional fixed long-duration

• Limited-payment• Participating insurance

Discount rates • High-quality fixed-income instrument yield would:• Replace “expected investment yield” and participating insurance

contract rates for discounting purposes• Maximize the use of relevant observable inputs and minimize

the use of unobservable inputs• Reflect the duration characteristics of the liability

• Traditional fixed long-duration

• Limited-payment• Participating insurance• Portion of SOP 03-1

annuitization benefit

Updating of • Updated at each reporting period (e.g., quarterly)discount rate • Change in liability due to discount rate changes would be excluded

from income and recognized immediately in Other ComprehensiveIncome (OCI)

• The high-quality fixed-income instrument yield at the reporting date would be used to discount the present value of future benefits and future net premiums to derive the balance sheet policy benefit liability

• Traditional fixed long-duration

• Limited-payment• Participating insurance

PwC

6

FASB targeted improvements – long durationIssue FASB tentative decision Contracts impacted

DAC amortizationand recoverabilitytest

• Amortize on a ratable basis either:• In proportion to the undiscounted amount of insurance in

force over the expected term of the related contract• On a straight-line basis, if the amount of insurance in force

cannot be reasonably estimated• Renewal commission would not affect amortization before

being incurred• No interest accretion• Experience adjustments recorded immediately through the

statement of operations• Assumption changes prospectively amortized• No impairment test, by analogy to financial instrument

accounting and debt issuance costs

• All long-duration contracts (except for investment contracts that use the effective yield method because they do not include significant surrender charges or do not otherwise yield significant revenues from sources other than interest).

Sales inducement • Follows new simplified DAC guidance • Universal lifeasset and universal • Certain investmentlife unearned contractsliability

Business • Currently unclear whether the DAC proposal will impact the • Same scope as DACcombination amortization and impairment test of these balancescontract“intangible asset”or “other liability”

Net cost of • Currently unclear whether the DAC proposal will impact the • Same scope as DACreinsurance (asset amortization of these costsor liability)PwC

7

FASB targeted improvements – long duration

Issue FASB tentative decision Contracts impacted

Market risk benefits

• Fair value measurement, with changes in fair value throughstatement of operations, except that changes to instrument-specific credit risk would be recognized through OCI

• The guidance would apply to variable product guarantees of separate account or similar funds.

• Fair value measurement can be a liability or an asset.

• Certain non-traditional life and annuity contracts with GMDB, GMIB, GMAB, GMWB, or GMWBL

• Includes U.S. separate accounts and non U.S. segregated accounts meeting specified criteria

Traditional • Benefit ratio may not exceed 100%; immediate loss recognition • Traditional universal lifeuniversal life to the extent the PV of expected excess payments exceed contracts and non-and non- expected assessments. traditional universal lifetraditional • Ongoing assessment of profits followed by losses for the • Certain investmentuniversal life insurance benefit feature replaces premium deficiency test contracts with additional(with additional • Additional liability cannot be less than zero benefitsliabilities forannuitization,death or otherinsurancebenefits)

PwC8

FASB targeted improvements – long durationIssue FASB tentative decision Contracts impactedPresentation & disclosure (forannual and interimreporting periods)

• Disaggregated rollforwards for the liability for future policy benefits, policyholder account balances, market risk benefits, separate accounts, DAC, and sales inducements

• Disclosure of qualitative and quantitative information about objectives, policies, and processes for managing risks

• Liability for future policy benefits - Qualitative and quantitativediscussion about adverse development

• Policyholder account balances – Weighted-average earned and crediting rates; tabular presentation of account balances by range of guaranteed minimum crediting rates and the related range of the difference between rates being credited to policyholders and the respective guaranteed minimums

• Market risk benefits - Separate presentation of the carrying amountof the liability (or asset) and fair value changes in the statements offinancial position and operations. Fair value changes attributable toa change in the instrument-specific credit risk would be reported inOCI.

• Various transition related disclosures, including disclosures for achange in accounting principle, on a disaggregated basis

All long-durationcontracts(except for investment contracts that follow financial instrument model/effective yield method)

PwC9

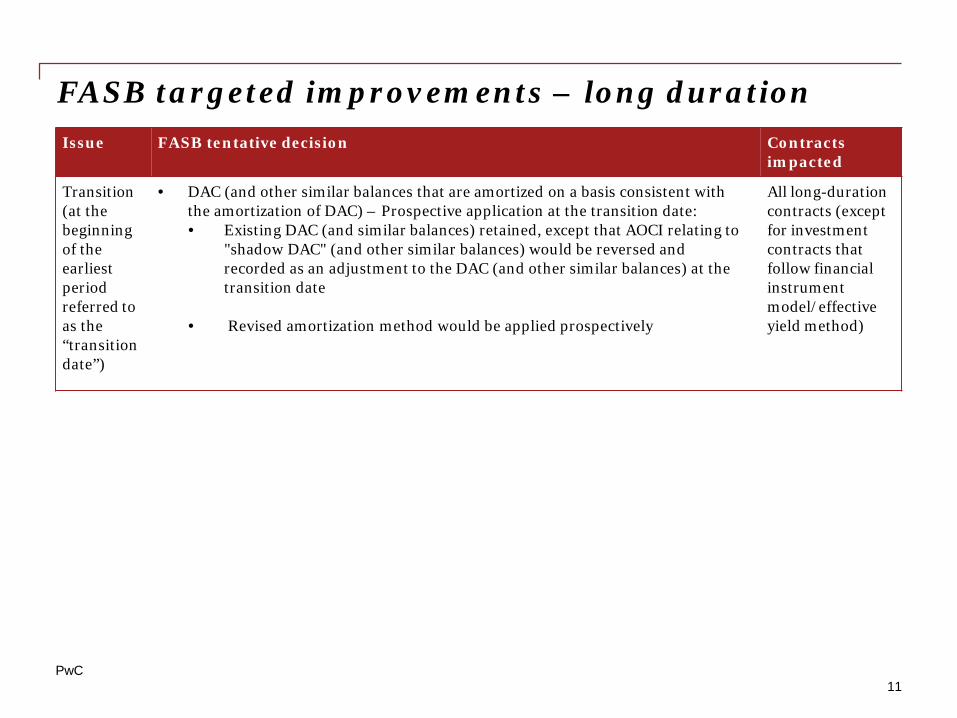

FASB targeted improvements – long durationIssue FASB tentative decision Contracts

impacted

Transition(at the beginning of the earliest period referred to as the “transition date”)

• Liability for future policy benefits - Retrospective application at the transitiondate using the following approach, applicable for each level at which liabilitiesare calculated:• Apply the guidance retrospectively as of the transition date using actual

historical informationIf actual historical information covering the entire contract period is notavailable, use estimates of historical information derived from objectivedata (internal or external)If it is impracticable to apply the guidance retrospectively to all priorperiods at the level at which liabilities are calculated, apply the guidance to in-force contracts on the basis of their existing carrying amounts at the transition date and using updated future assumptions, adjusted for the removal of any related amounts in AOCI.Opening retained earnings balance would be adjusted to the extent the net premium ratio exceeds 100%

•

•

•

• Market risk benefits – Retrospective application of the fair value requirement at the transition date• Cumulative effect of changes in the instrument-specific credit risk between

contract issue date and transition date would be recognized in the openingbalance of AOCI

• Remaining difference between fair value and carrying value at the transition date, excluding the effect of changes in the instrument-specific credit risk, would be recognized as an adjustment to opening retained earnings

All long-durationcontracts (except for investment contracts that follow financial instrument model/effectiveyield method)

PwC10

FASB targeted improvements – long durationIssue FASB tentative decision Contracts

impacted

Transition(at the beginning of the earliest period referred to as the “transition date”)

• DAC (and other similar balances that are amortized on a basis consistent with the amortization of DAC) – Prospective application at the transition date:• Existing DAC (and similar balances) retained, except that AOCI relating to

"shadow DAC" (and other similar balances) would be reversed and recorded as an adjustment to the DAC (and other similar balances) at the transition date

• Revised amortization method would be applied prospectively

All long-durationcontracts (except for investment contracts that follow financial instrument model/effectiveyield method)

PwC11

What are the next steps

Looking forward

• Given the significant nature of the proposed changes, the board decided that the proposed targeted changes would be exposed for public comment- FASB issued proposed ASU in September 2016- 75 day comment period. Comments were due December 15,

2016 ,which included the following themes;◦ Preparers favor a prospective approach for updating assumptions

and discount rate higher than AA rate.◦ Many preparers disagree with fair value for GMDBs◦ Consensus for separate project on par contracts or provide scope out◦ Supportive of simplified DAC amortization model

- Public roundtable held in April 2017.

PwC12

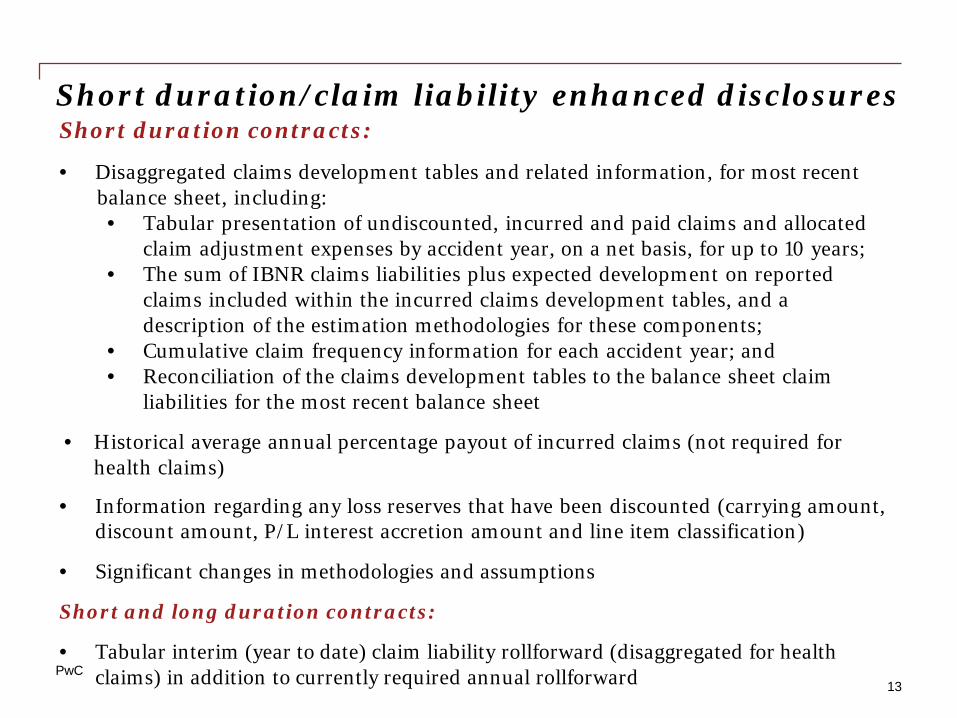

Short duration/claim liability enhanced disclosuresShort duration contracts:

• Disaggregated claims development tables and related information, for most recentbalance sheet, including:• Tabular presentation of undiscounted, incurred and paid claims and allocated

claim adjustment expenses by accident year, on a net basis, for up to 10 years;• The sum of IBNR claims liabilities plus expected development on reported

claims included within the incurred claims development tables, and adescription of the estimation methodologies for these components;

• Cumulative claim frequency information for each accident year; and• Reconciliation of the claims development tables to the balance sheet claim

liabilities for the most recent balance sheet

• Historical average annual percentage payout of incurred claims (not required forhealth claims)

• Information regarding any loss reserves that have been discounted (carrying amount,discount amount, P/L interest accretion amount and line item classification)

• Significant changes in methodologies and assumptions

Short and long duration contracts:

• Tabular interim (year to date) claim liability rollforward (disaggregated for healthclaims) in addition to currently required annual rollforwardPwC

13

Short duration disclosure observations from 2017Analysis of 41 large public P&C company disclosures

PwC

• Number of years presented in the claims development tables. The ASU directs companies to provide claims development tables for the number of years for which claims incurred typically remain outstanding (that need not exceed 10 years). Where impracticable, the insurance entity need not disclose more than 5 years in the initial year of adoption. The table to the right presents the number of accident years presented in each of the 245 disaggregated claims development tables:

• Companies’ rationale for presenting fewer than 10 years. Approximately one-third of the companies presenting fewer than 10 years of data in the claims development tables cited the "impracticable" assertion as their rationale. In most other cases the company noted that the length of time reported represents the number of years for which claims incurred typically remain outstanding for the disaggregated group.

No. of Years

No. of ClaimsDevelopment

Tables

% of Claims Development

Tables

10 163 67%

9 7 3%

8 2 1%

7 21 9%

6 4 2%

5 43 18%

4 0 0%

3 3 1%

2 2 1%

Total 245 100%

14

Short duration disclosure observations from 2017, Cont’d.Analysis of 41 large public P&C company disclosures

PwC15

• Number of P&C segments. The graph to the right shows the number of claims development tables presented compared to the number of the reporting segments for which the company provided at least one claims development table.

• Location of Required Supplementary Information (RSI) and narrative disclosures. The ASU noted thatcertain aspects of the disclosure, including the years presented in the claims development tables preceding the most recent reporting period and the average percentage payout of claims, should be considered supplementary information. The ASU did not prescribe a particular location for presenting supplementary information. In practice, companies included both the RSI and narrative disclosures in the Notes to the Financial Statements, although often in different sections. Most companies included the claims development tables in the Notes to the Financial Statement (typically within the Note related to Loss and Loss Adjustment Expense Reserves). Companies typically placed the disclosure regarding ASU 2015-09 within the section of the Notes to the Financial Statement covering Recently Issued Accounting Standards, often in Note 1.

Short duration disclosure observations from 2017, Cont’d.Analysis of 41 large public P&C company disclosures

PwC16

• Acquisitions. One of the more challenging implementation issues for companies creating the short duration contracts disclosures for the first time was how to reflect acquisitions within the claims development tables. During the several months leading up to the release of the disclosure, two common approaches emerged: prospective and retrospective. Companies using a prospective approach present the acquired business in the claims development tables beginning with the date of acquisition. Companies using a retrospective approach present the acquired business in the entire claims development tables - i.e., as if the business had always been owned. While many companies do not have significant acquisitions to disclose, affected companies include commentary in the disclosure narrative (generally as a prelude to the claims development tables), detailing the companies acquired, the timing of the acquisitions, and the presentation approach used in the claims development tables. Affected companies most frequently utilized a retrospective approach. For those several companies utilizing a prospective approach, unavailability of data at pre-acquisition evaluations or changes in claims handling practices or ceding arrangements was typically cited as a driver in choice of approach.

• Labeling of prior years. Almost all (39 of 41) companies disclosed within their reporting statement that the prior evaluation years in the claims development tables were unaudited. Most companies labeled the prior years “unaudited” as a part of the disclosure table headers. Many companies also included this fact within the accompanying narrative.

Short duration disclosure observations from 2017, Cont’d.Analysis of 41 large public P&C company disclosures

PwC17

• Companies with negative IBNR. Fifteen companies presented at least one claim development table with negative IBNR in at least one accident year. Nearly 80% of these individual years contain a very small amount of negative IBNR (less than $10 thousand). Five companies presented 11 claims development tables with at least one year with negative IBNR greater than $10 thousand. In general, instances of negative IBNR of more than $10 thousand are associated with business for which salvage and subrogation is prevalent, including: physical damage, homeowners and property.

• Reserve variability. We used the information presented in the new disclosures to compile cumulative reserve development, which measures the change in ultimate claim values that occurs as additional information regarding the claims and actual settlement activity becomes available. We reviewed trends in total and by several groupings to gain additional insights:

• By industry groupings, categorizing each company in our analysis into one of the following four groups: commercial lines focus large insurer (“large commercial”), commercial lines focus small insurer (“small commercial”), personal lines focus (“personal”), offshore insurance / reinsurance focus (“reinsurer”);

• By duration of exposure, categorizing each claims development table used in our analysis as either short tailed or long tailed; and

• By insurance or reinsurance business, categorizing each claims development table used in our analysis as insurance or reinsurance business.

•

Short duration disclosure observations from 2017, Cont’d.Analysis of 41 large public P&C company disclosures

PwC18

The table below shows how loss reserves have developed since the initial year-end balance sheet date through year ending 2016 for the various groupings. Green denotes favorable development and red denotes adverse development.

Short duration disclosure observations from 2017, Cont’d.Analysis of 41 large public P&C company disclosures

PwC19

The table below shows how accident year loss reserves have developed since the original year-end balance sheet date through year-end 2016. Green denotes favorable development and red denotes adverse development.

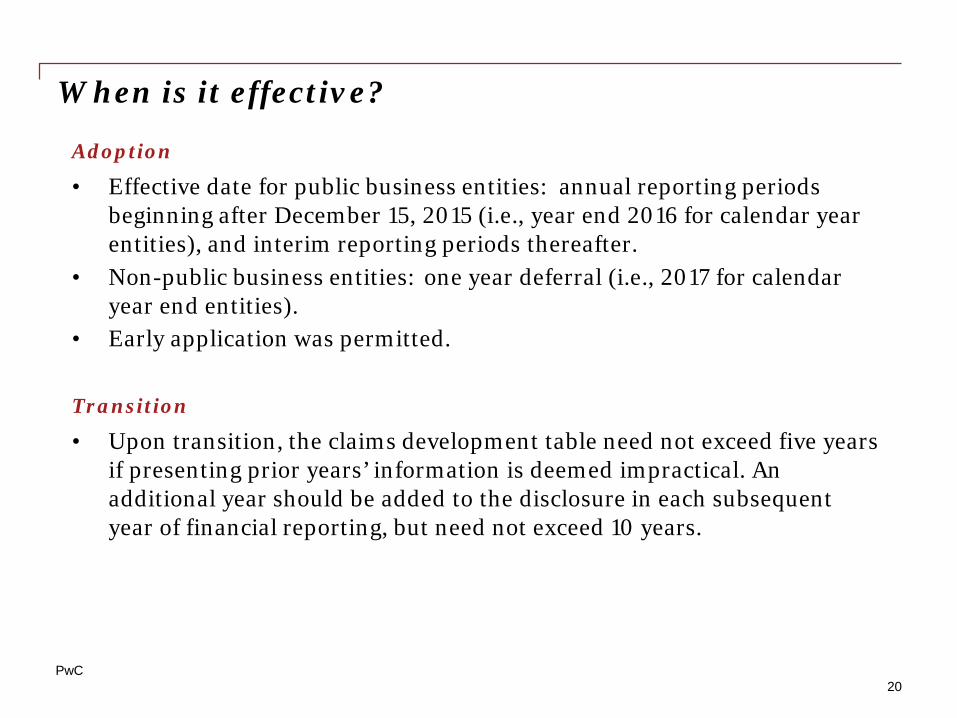

When is it effective?

Adoption

• Effective date for public business entities: annual reporting periods beginning after December 15, 2015 (i.e., year end 2016 for calendar yearentities), and interim reporting periods thereafter.

• Non-public business entities:year end entities).

• Early application was permitted.

one year deferral (i.e., 2017 for calendar

Transition

• Upon transition, the claims development table need not exceed five years if presenting prior years’ information is deemed impractical. An additional year should be added to the disclosure in each subsequent year of financial reporting, but need not exceed 10 years.

PwC20

Navigating the new landscape

Financial instruments (recognition and measurement)

Recognition and measurement overview

PwC22

Issued January 2016

Impacts• Equity investments:

- FV-NI- Measurement alternative available for

certain equity securities within the scope of the new standard

- Single step impairment model for equisecurities under the measurement alternative

• Financial liabilities under FVO:- Changes in fair value due to instrument

specific credit risk recognized in OCI• Loans, debt securities, and financial liabilities

(other than FVO) largely unchanged

Reduces complexity in accounting for financial instruments

ty Provides users decision-useful information about financial instruments

Affects public and private companies that hold financial assets or owe financial liabilities

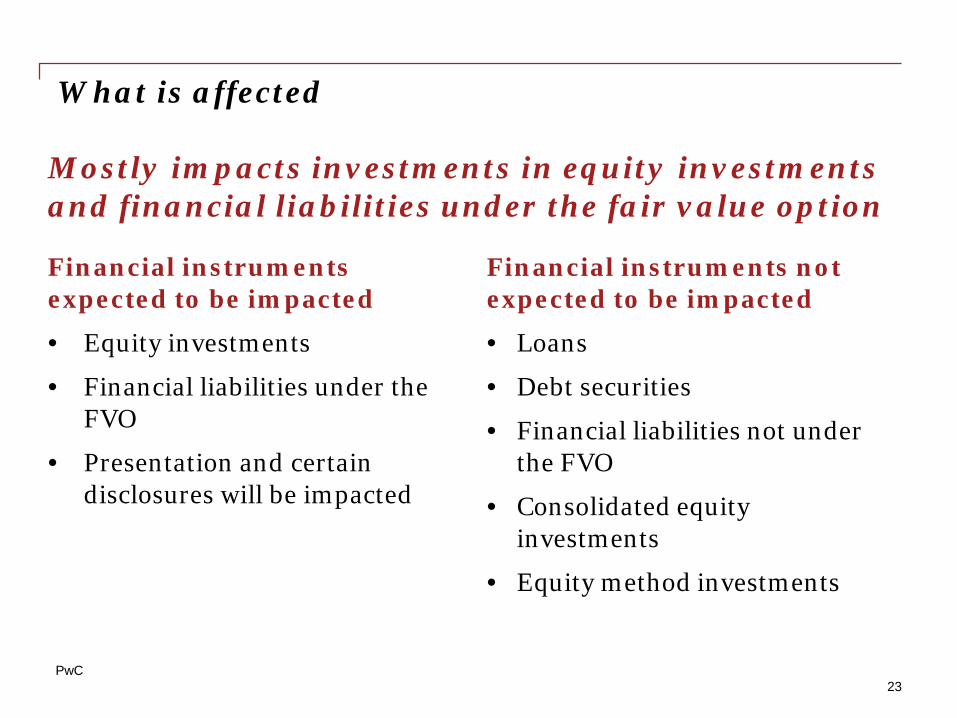

What is affected

PwC23

Financial instrumentsexpected to be impacted

• Equity investments

• Financial liabilities under the FVO

• Presentation and certain disclosures will be impacted

Financial instruments notexpected to be impacted

• Loans

• Debt securities

• Financial liabilities not underthe FVO

• Consolidated equity investments

• Equity method investments

Mostly impacts investments in equity investmentsand financial liabilities under the fair value option

Presentation and disclosure – incremental

PwC24

disclosures

*does not apply to demand deposit liabilities or receivables/payables due in less than one year

Disclosure of financial instruments

• Requires disclosure of financial assets and financial liabilities separately, grouped by measurement category (e.g., FV, amortized cost, LOCOM) and class of financial asset (e.g., loans, securities)

Financial instruments at amortized cost

• Requires public business entities to report (parenthetically in the statement of financial position or in the notes to the financial statements) all fair values of financial instruments measured at amortized cost based on an exit price, eliminating the ability to use an entry price for certain fair value disclosures (e.g. loans)*

• Non-public business entities exempt from disclosing fair value offinancial instruments measured at amortized cost in the financialstatements (previously disclosed in accordance with ASC 825-10)

• Eliminates the requirement for public business entities to disclose the method(s) and significant assumptions used to estimate the fair value for disclosure purposes of financial instruments measured at amortized cost

• Public business entities to disclose the fair value hierarchy levelwithin which the fair value measurement is categorized for eachinterim and annual period

Presentation and disclosure – incremental

PwC25

disclosures (continued)Equity investmentswithout readily determinableFVs

• Disclose:• The carrying value of investments without readily

determinable fair values measured using the measurementalternative

• The total amount of adjustments resulting from impairment• Total amount of adjustments for observable prices

What are the next steps

PwC26

Looking forward• Effective dates:

• Public business entities - annual periods (and interim periods within those annualperiods) beginning after December 15, 2017.

• All other entities – annual periods beginning after December 15, 2018, and forinterim periods within annual periods beginning after December 15, 2019.

• Early adoption:

• All entities can early adopt the provision to record fair value changes for financial liabilities under the fair value option resulting from changes in instrument-specificcredit risk in other comprehensive income.

• Non-PBEs can early adopt the provision permitting the omission of fair valuedisclosures for financial instruments reported at amortized cost.

• Early adoption of these provisions can be elected for all financial statements of fiscalyears and interim periods that have not yet been issued or that have not yet beenmade available for issuance.

Where to find additional informationIn depth US2016-01, New guidance on recognition and measurement to impact financial instrumentsPwC Guide: Loans and investments

Navigating the new landscape

Financial instruments -Impairment

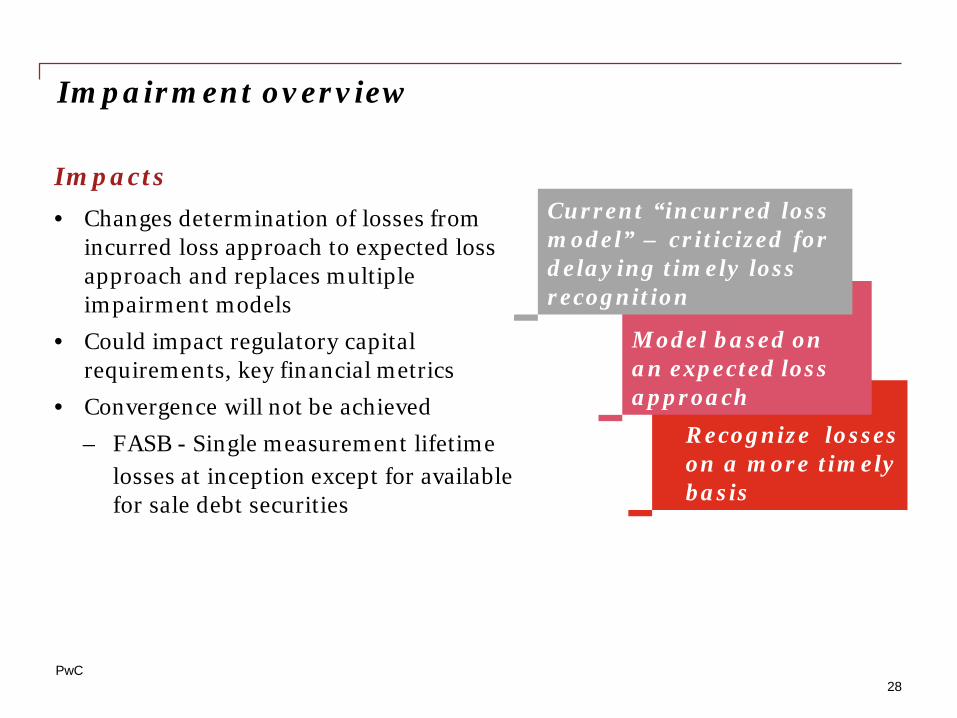

Recognize losseson a more timelybasis

Model based onan expected lossapproach

Impairment overview

PwC28

Impacts• Changes determination of losses from

incurred loss approach to expected loss approach and replaces multiple impairment models

• Could impact regulatory capital requirements, key financial metrics

• Convergence will not be achieved– FASB - Single measurement lifetime

losses at inception except for availablefor sale debt securities

Current “incurred lossmodel” – criticized fordelaying timely lossrecognition

What’s in scope of CECL?

PwC29

CECL applies to financial assets subject to credit losses and measured at amortized cost, and certain off-balance sheet credit exposures

Scope of the standard Specifically excluded

• Loans• Held to maturity debt

securities• Loan commitments• Trade receivables• Lease receivables• Reinsurance receivables• Financial guarantees• Purchased credit deteriorated

assets recorded at amortized cost

• Loan receivables held for sale• Financial assets where fair

value option is elected• Equity instruments and

equity method investments

• Derivatives• Related party loans to entities

under common control

Current Expected Credit Loss model (CECL)• Single measurement objective for assets held at amortized cost:

Expected credit losses over the life of the financial asset

• No “triggers” before recognizing impairment

• CECL reserves are the amount not expected to be collected

• The allowance is a valuation account that is deducted from theamortized cost basis to present the net carrying value at theamount expected to be collected

Overview of the CECL modelHow does it work

PwC30

How does it work

PwC31

• Financial assets within scope must be pooled when similar risk characteristics exist; otherwise assessed individually

• Use of a discounted cash flow model is not required

• The allowance should be calculated based on the amortized costbasis of the financial asset

• Consider relevant internal and external information, including:o Historical experienceo Current conditionso Reasonable and supportable forecasts

• Future periods beyond which the entity is able to make a reasonable and supportable forecast – reversion to historical loss information

CECL measurement principles

How does it work

PwC32

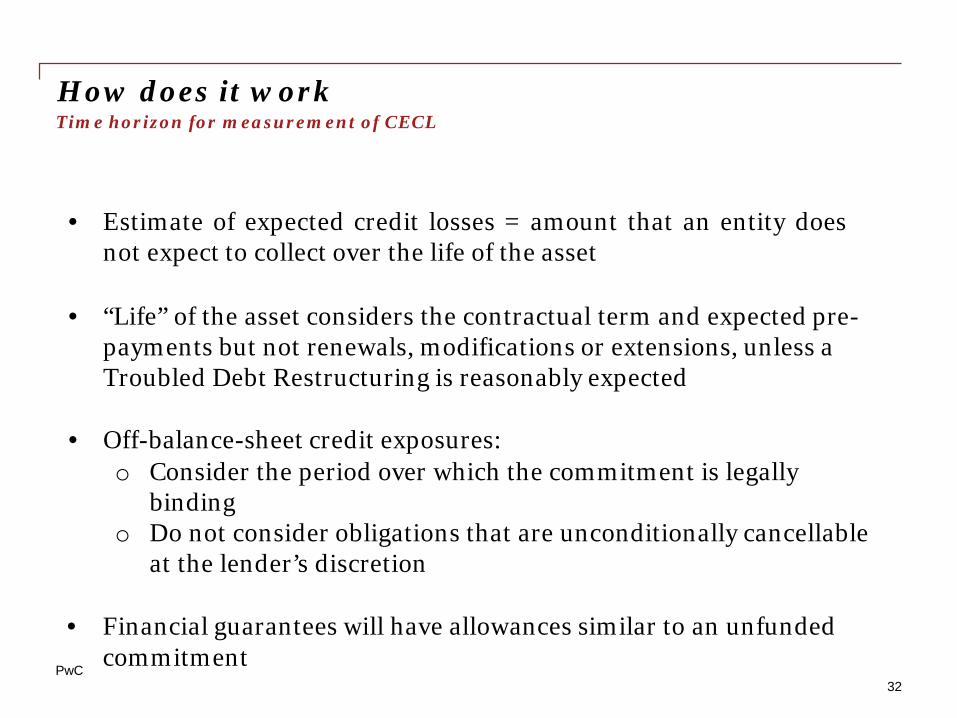

• Estimate of expected credit losses = amount that an entity doesnot expect to collect over the life of the asset

• “Life” of the asset considers the contractual term and expected pre-payments but not renewals, modifications or extensions, unless aTroubled Debt Restructuring is reasonably expected

• Off-balance-sheet credit exposures:o Consider the period over which the commitment is legally

bindingo Do not consider obligations that are unconditionally cancellable

at the lender’s discretion

• Financial guarantees will have allowances similar to an unfunded commitment

Time horizon for measurement of CECL

How does it work

PwC33

• Consideration of collateral• Mitigation of credit risk• Measurement when foreclosure is probable• Collateral dependent financial assets

• Impact of “embedded” vs freestanding credit enhancements

• Other allowance considerations:• Trade receivables• Lease receivables

CECL measurement – Other key considerations

Key differences from “Incurred losses” for loansToday Some of the key changesASC 450 (FAS 5) for incurred losses in the loan portfolio (collectively evaluated for impairment)

• Replace incurred loss model with expected loss model• Use reasonable and supportable forecasts• Reflects contractual life considering prepayments, but without

consideration of renewals, extensions, or modifications, unlessTDR is reasonably expected

ASC 310 (FAS 114) specific valuation allowances

• No threshold for identification of individually impaired loans• Measurement approach is similar to today if elect to use

discounted cash flow modelling approach• Continues to maintain practical expedient for collateral dependent

loans

ASC 310-40 TDRs • Measured using the CECL model• Recognize credit losses, including certain concessions

ASC 310-30 Purchase CreditImpaired

• Purchased with more than insignificant credit deterioration (PCD)

• Basis “grossed up” to reflect expected loss estimate

• Initial credit loss will not be recognized in income

• Changes in allowance recognized immediately in income

• Follow an “accrete to contractual” interest model

Under the new standard, assets with similar risk characteristics shall be collectively assessed for expected credit losses.PwC

34

How does it work

PwC35

Purchased financial assets with credit deterioration (PCD)*

Scope: Assets with more than insignificant deterioration in credit qualitysince origination

• Basis “grossed up” to reflect expected loss estimate on Day 1• Initial credit loss not recognized in income• If a discounted cash flow (DCF) model is used:

• Step 1: Calculate the effective interest rate (EIR) by solving forthe discount rate such that discounted expected cash flows equalthe purchase price

• Step 2: Calculate the initial allowance by discounting thecashflows not expected to be collected (i.e., difference betweencontractual and expected cashflows) by the EIR

• If a non-DCF model is used, the Day 1 allowance is based on “par”**• Subsequently apply CECL and “accrete to contractual” interest models

*The PCD model is applicable to AFS debt securities and assets within scope of CECL**Not applicable to AFS debt securities

New disclosure requirements

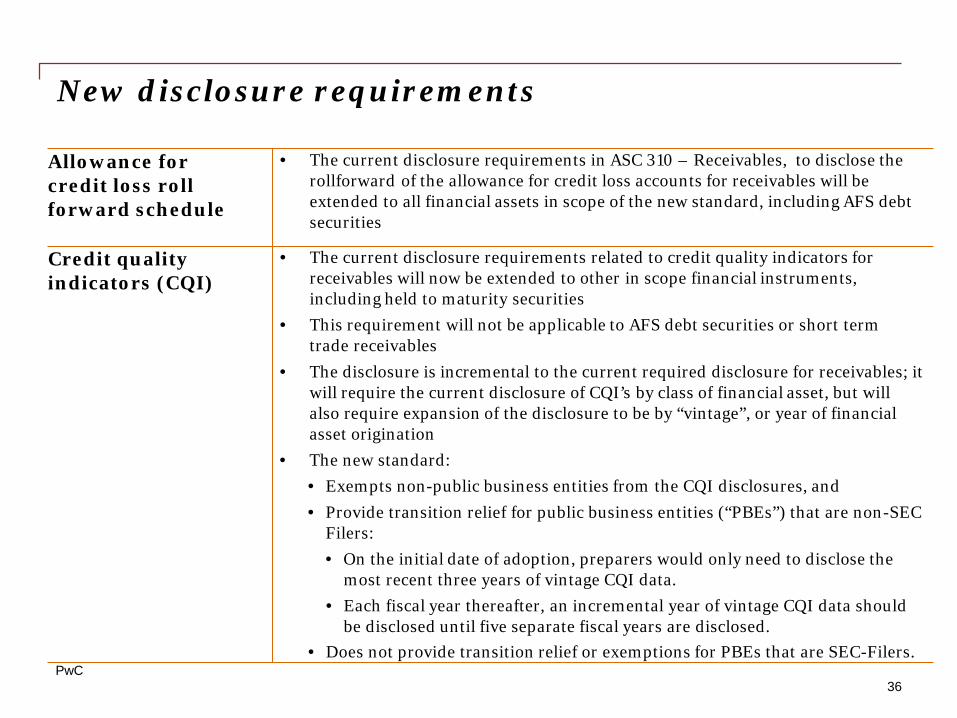

Allowance for credit loss roll forward schedule

• The current disclosure requirements in ASC 310 – Receivables, to disclose the rollforward of the allowance for credit loss accounts for receivables will be extended to all financial assets in scope of the new standard, including AFS debt securities

Credit quality indicators (CQI)

• The current disclosure requirements related to credit quality indicators for receivables will now be extended to other in scope financial instruments, including held to maturity securities

• This requirement will not be applicable to AFS debt securities or short term trade receivables

• The disclosure is incremental to the current required disclosure for receivables; it will require the current disclosure of CQI’s by class of financial asset, but will also require expansion of the disclosure to be by “vintage”, or year of financial asset origination

• The new standard:• Exempts non-public business entities from the CQI disclosures, and• Provide transition relief for public business entities (“PBEs”) that are non-SEC

Filers:• On the initial date of adoption, preparers would only need to disclose the

most recent three years of vintage CQI data.• Each fiscal year thereafter, an incremental year of vintage CQI data should

be disclosed until five separate fiscal years are disclosed.• Does not provide transition relief or exemptions for PBEs that are SEC-Filers.

PwC36

Transition guidance

PwC37

• Generally, cumulative transition adjustment will be required on thedate of adoption

Purchased financial assets with credit deterioration• Current PCI financial assets will be classified as PCD at transition• PCD guidance will be applied prospectively for financial assets that

previously applied the purchased credit impaired (PCI) model• At date of adoption, record allowance for credit loss “gross-up” to the

balance sheet

Debt instruments that experienced other-than-temporary-impairment• Adopt ASU prospectively

What are the next steps

PwC38

Looking forward

• The effective date for the impairment standard is:• PBEs that meet the definition of an SEC filer in fiscal years beginning after December

15, 2019 including interim periods within those fiscal years;• PBEs that do not meet the definition of an SEC filer in fiscal years beginning after

December 15, 2020 including interim periods within those fiscal years; and• Non-PBEs (including certain not-for-profit entities and employee benefit plans) in

fiscal years beginning after December 15, 2020 and interim periods within fiscal years beginning after December 15, 2021.

• Early application of the guidance will be permitted for fiscal years beginning afterDecember 15, 2018, including interim periods within those fiscal years.

• IFRS 9: Issued and effective for annual periods beginning on or after January 1, 2018

• A transition resource group (TRG) has been created (similar to TRG for revenue standard).

Navigating the new landscape

Revenue from contracts with customers

Revenue recognition overviewIssued May 2014

Impacts• Standard could significantly change

how many entities recognize revenue• Standard is intended to be principles-

based• Will remove existing industry-specific

guidance• Expanded qualitative and quantitative

disclosures (annual and interim)• Transition Resource Group

Achieve a single, comprehensive revenue recognition model

Core principle is that revenue recognition depicts transfer of control to customer in an amount that reflects consideration to which an entity expects to be entitled

PwC40

Who is affected

PwC41

Scope of the standardContracts with customers of all entities and industries within scope with onlycertain transactions excluded

Specifically excluded• Lease contracts• Insurance contracts• Financial instruments• Guarantees (other than product

warranties)• Certain nonmonetary exchanges• Contracts with other than customers

(e.g., collaborations)

Scope set to improve consistency and comparability within industries, across industries, and across capital markets

When is it effective

PwC42

U.S. GAAPPublic

U.S. GAAPNon-public

IFRS

Effective Date

Early adoption permitted?

Method of adoption

Beginning after December 15, 2017

2018 calendar year

Beginning after December 15, 2018

2019 calendar year

Beginning on January 1, 2018

2018 calendar yearYes

No earlier than the original effective datefor public entities

2017 calendar year

Yes

No earlier than the original effective datefor public entities

2017 calendar year

Yes

Retrospective (with certain practical expedients allowed) or modified retrospective

AICPA TaskForce Topics: InsuranceSome potential services and related issues included:

PwC43

P&C insurance• High deductible policies (ASC 606/944 split or all insurance?)

Mortgage insurance• Out of scope of ASC 606?

Health insurance• Administrative service only (ASO) contracts • ASO with aggregate stop loss coverage (ASC 606/944 split or all insurance?)

Life insurance• Investment contracts

- Explicit fees for asset management service: financial instrument accounting or U/L model?

FASB Issued Technical Corrections and Improvements for InsuranceScope of Revenue Recognition

FASB issued a technical correction to clarify that contracts within scope of Topic 944 are excluded from scope of Topic 606

- Includes life and health, property casualty, and mortgage guaranty insurance

- Investment contracts (accounted for as a financial instrument 944-825)

- Non-insurance contracts written by an insurance entity are accounted for under ASC 606

Bifurcating elements of an insurance contract

Wording added to Basis for Conclusion;

- Insurance mitigation or cost containment activities (such as claims handling/process) are part of fulling the insurance obligation or mitigating insurance risk

- Totally non-insurance related activities added to an insurance contract (anti-abuse provision)

Apply combination of contracts guidance (ASO and Stop Loss)

AICPA proposed clarification;

- Evaluate contract economics and nature of arrangements (including pricing interdependencies) to assess if contracts should be combined for accounting performance (assessing performance obligations)

PwC44

Navigating the new landscape

Leases

Leases

Leases – executive summary

PwC46

Issued February 2016

What you need to know• Virtually all leases on balance sheet• Renewal options will be included when

a significant economic incentive toexercise exists

• FASB and IASB diverged on lessee pattern of income statement recognition

– FASB similar to today – operatinglease expense on a straight-line basis

– IASB all financing, therefore front loaded expense

• Lessors in a sales-type or directfinancing lease derecognize theunderlying asset and recognize a leasereceivable and unguaranteed residualasset

Impacts• Balance sheet will be grossed up

for lessees• Financial metrics and debt

covenants may be impacted• Leases may be embedded in

other contracts and will now be on balance sheet

Looking forward• Effective CY 2019 for public

business entities (includinginterim periods – Q1 2019)

• Effective CY 2020 for non-public entities

On the horizon

Premium amortization on callable debt securities

Premium amortization on callable debt securities

PwC48

Issued April 2017

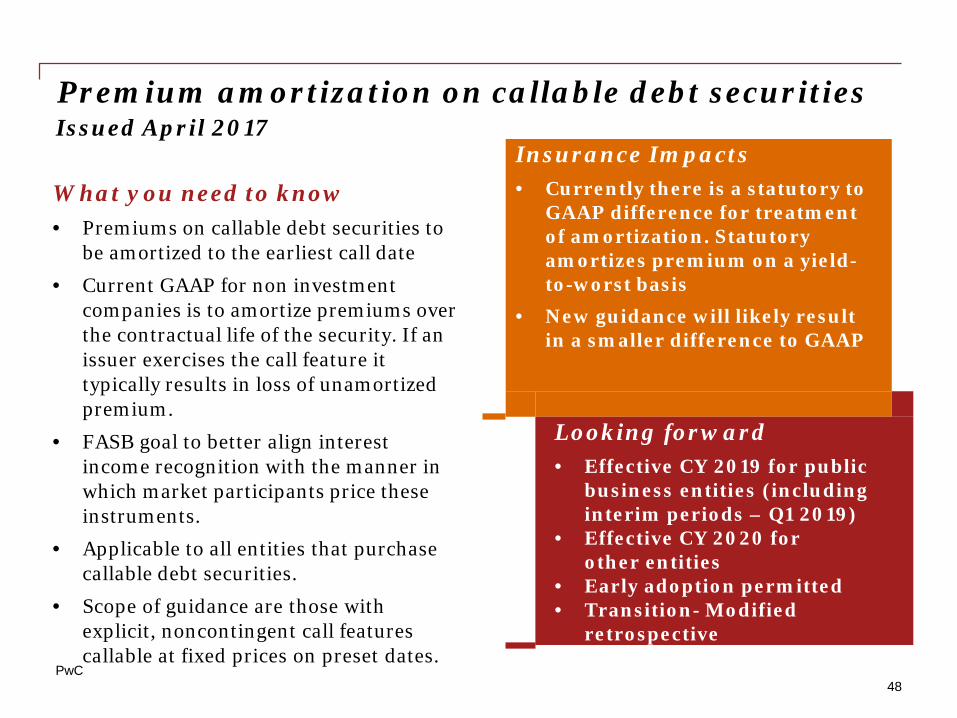

What you need to know• Premiums on callable debt securities to

be amortized to the earliest call date

• Current GAAP for non investment companies is to amortize premiums over the contractual life of the security. If an issuer exercises the call feature it typically results in loss of unamortized premium.

• FASB goal to better align interest income recognition with the manner in which market participants price these instruments.

• Applicable to all entities that purchase callable debt securities.

• Scope of guidance are those with explicit, noncontingent call features callable at fixed prices on preset dates.

Insurance Impacts• Currently there is a statutory to

GAAP difference for treatment of amortization. Statutory amortizes premium on a yield-to-worst basis

• New guidance will likely result in a smaller difference to GAAP

Looking forward• Effective CY 2019 for public

business entities (includinginterim periods – Q1 2019)

• Effective CY 2020 forother entities

• Early adoption permitted• Transition- Modified

retrospective

Navigating the new landscape

Development Stage EntitiesPresentation of pension cost

Presentation of pension costIssued March 2017

What you need to know

• Service cost to be presented with other employee compensation costs within operations, if such a subtotal is presented,

• Other components of net benefit cost reported separately outside of income from operations (in one or more line items), if such a subtotal is presented, and

• Capitalize only the service cost component, when applicable.

Looking forward• Effective CY 2018 for public

business entities (other entities should adopt a year later)

• Retrospective transition for presentation and prospective for capitalization

Insurance Impacts• Present other components in

separate line item or adequately disclose where the costs are included

• For establishing deferred acquisition costs or loan origination costs, limit costs to service component only

PwC50

Where to find additional information

PwC51

PwC FASB/IASB Insurance Contracts Project

http://www.pwc.com/us/en/insurance/publications/iasb-fasb-insurance-contracts-project.html#insuranceProjects

PwC Insurance Alert: FASB Roundtable on Insurance Contracts – April 19, 2017

http://www.pwc.com/us/en/cfodirect/assets/pdf/insurance-contracts/fasb-roundtable-insurance-contracts-april-2017.pdf

PwC Insurance Alert: FASB Meeting on Insurance Contracts – February 8, 2017

http://www.pwc.com/us/en/insurance/publications/assets/pwc-notes-fasb-meeting-february-8-2017.pdf

PwC In Depth: FASB Issues Enhanced Disclosure Guidance for Insurer Claim Liabilities

http://www.pwc.com/en_US/us/cfodirect/assets/pdf/in-depth/us2015-10-fasb-insurer-claim-disclosures.pdf

PwC In Depth: New Guidance on Recognition and Measurement to Impact Financial Instruments

https://www.pwc.com/us/en/cfodirect/assets/pdf/in-depth/us2016-01-fasb-financial-instruments-recognition-measurement.pdf

PwC Loan & Investments Guide http://www.pwc.com/us/en/cfodirect/publications/accounting-guides/pwc-guide-loans-investments-cecl-impairment-model.html

PwC In Depth: The FASB’s New Financial Instruments Impairment Model

http://www.pwc.com/us/en/cfodirect/publications/in-depth/fasb-financial-instruments-credit-losses-impairment.html

PwC In Brief: Allowance for Loan and Lease Losses – FASB Issues Final Impairment Standard

http://www.pwc.com/us/en/cfodirect/publications/in-brief/fasb-new-impairment-guidance-financial-instruments.html

FASB: ASU 2016-20 Technical Corrections and Improvements to Topic 606, Revenue from Contracts with Customers

http://www.fasb.org/jsp/FASB/Document_C/DocumentPage?cid=1176168723765&acceptedDisclaimer=true

In closing

Follow @CFOdirect on Twitter

This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, PricewaterhouseCoopers LLP, its members, employees and agents do not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.

© 2016 PricewaterhouseCoopers LLP. All rights reserved. In this document, “PwC” refers to PricewaterhouseCoopers LLP which is a member firm of PricewaterhouseCoopers International Limited, each member firm of which is a separate legal entity.