gardner denver q4 and full year 2017 earnings...

TRANSCRIPT

Gardner DenverQ4 and Full Year 2017 Earnings PresentationFebruary 16, 2018

Replay Information

▪ Dial toll-free: +1.877.344.7529

▪ International: +1.412.317.0088

▪ Conference ID: #10116634

▪ Log on to: http://investors.gardnerdenver.com

2

Disclaimer

Forward-Looking Statements

During the course of this presentation, we may make “forward-looking statements” within the meaning of the USfederal securities laws. In fact, all statements made during this presentation other than statements of historical factare forward-looking statements. Words such as “expects,” “anticipates,” “believes,” “estimates,” “plans,” “intends,”“projects” and “indicates” and variations of such words or similar expressions are intended to identify forward-looking statements. Although they reflect our current expectations, these statements are not guarantees of futureperformance, and actual results may differ materially from what is expressed in or indicated by these forward-looking statements. Forward-looking statements are subject to risks and uncertainties that could cause actualperformance or results to differ materially from those expressed in such forward-looking statements, including thoserisks and uncertainties described under the section titled “Risk Factors” in our most recent annual report on form 10-K filed with the Securities and Exchange Commission (“SEC”), which risks and uncertainties may be updated fromtime to time in our periodic filings with the SEC (accessible on the SEC’s website at www.sec.gov). Forward-lookingstatements speak only as of the date the statements are made. The Company does not undertake to update anyforward-looking statements as a result of future developments or new information, except as required by law.

Non-GAAP Financial Measures

Included in this presentation are certain non-GAAP financial measures designed to supplement, and not substitute,the financial information presented in accordance with generally accepted accounting principles in the United Statesof America because management believes such measures are useful to investors. The reconciliation of thosemeasures to the most comparable GAAP measures is detailed in Gardner Denver’s press release for the fourthquarter of 2017, which is available at http://investors.gardnerdenver.com, together with this presentation.

3

Agenda

▪ Highlights

▪ Q4 & FY 2017 Financial Performance

▪ Segment Highlights

▪ Strategy Update & Runtech Acquisition

▪ 2018 Guidance

▪ Q&A

4

Q4 Highlights

5¹ Excluding the impact of any potential future acquisitions

Strong Execution

• Revenue of $665M, up 15% versus prior year

• Adjusted EBITDA of $173M, up 16% versus the prior year

• Adjusted EBITDA margin of 26.0%, an improvement of 30 basis pointsversus prior year

Improving Leverage Profile

• Free cash flow generation of $96M, up 213% versus prior year

• Net debt to Adjusted EBITDA ratio improved to 2.9x from 3.2x versus prior quarter & 1.3x turns since the time of the IPO (May 2017)

Favorable Outlook

• Providing 2018 guidance for Adjusted EBITDA of $650M to $670M

• Targeting year-end net debt to Adjusted EBITDA ratio of ~2.1X - 2.3X1

Solid performance across all three segments and continued

execution of our value-creation strategy

A premier industrial company with leading brands, mission-critical technologies, and diverse end market exposure

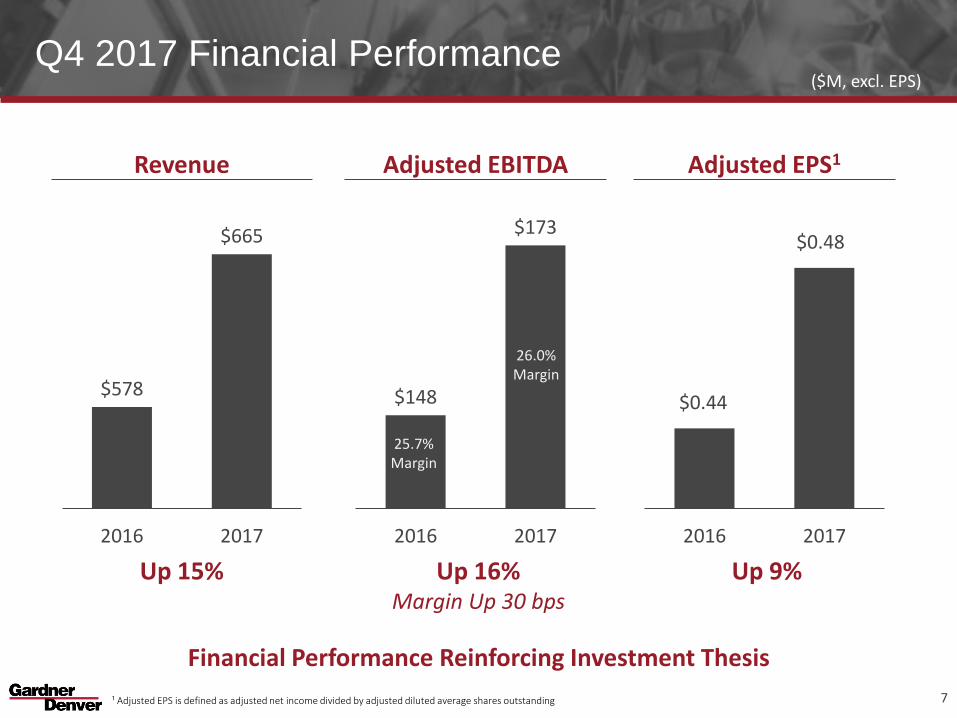

Q4 & FY 2017 Financial Performance

Q4 2017 Financial Performance

7¹ Adjusted EPS is defined as adjusted net income divided by adjusted diluted average shares outstanding

($M, excl. EPS)

Revenue

$578

$665

2016 2017

Adjusted EBITDA

$148

$173

2016 2017

Adjusted EPS1

$0.44

$0.48

2016 2017

Up 15% Up 16%Margin Up 30 bps

Up 9%

26.0%Margin

25.7%Margin

Financial Performance Reinforcing Investment Thesis

Pro-formaIPO

4.2x3.8x

3.2x2.9x

Q1'17 Q2'17 Q3'17 Q4'17

Q4 2017 Financial Performance

8

LeverageFree Cash Flow1Working Capital(Op. Working Capital as % of LTM Sales) (Net Debt / LTM Adjusted EBITDA)

$31

$96

2016 2017

Improved 180 bps Up 213% Improved 0.3x sequentially

¹ Free Cash Flow is defined as cash flows from operations less capital expenditures

31.5%

29.7%

2016 2017

Strengthening Position Through Strong FCF and De-leveraging

($M)

FY 2017 Financial Performance

9¹ Adjusted EPS is defined as adjusted net income divided by adjusted diluted average shares outstanding

Revenue

$1,939

$2,375

2016 2017

Adjusted EBITDA

$401

$562

2016 2017

Adjusted EPS1

$0.88

$1.32

2016 2017

Up 22% Up 40%Margin Up 290 bps

Up 50%

23.6%Margin

20.7%Margin

($M, excl. EPS)

Impact of U.S. Tax Legislation

10

• Net tax benefits of ~$95M recorded in 2017 related to U.S. Tax legislation

• Tax benefit of ~$90M recorded for the revaluation of U.S. deferred tax liabilities for the reduction of tax rate from 35% to 21%

• Repatriation Tax cost of ~$63M offset by the tax benefit of ~$69M for the reduction in the deferred tax liability on unremitted non-U.S. earnings and profits

• 2018 tax rate currently forecasted to improve 200 to 400 bps versus prior year to a range of 26% to 28%1

1Forecasts are subject to change based upon additional regulations and guidance from the U.S. Treasury

Q4 & FY 2017 Segment Performance

Industrials Segment – Q4 & FY Highlights

12

($M)

Highlights (All Q4 unless otherwise noted):

Orders up 25% as reported; up 20% ex-FX… strong growth in all regions

Revenue up 7% ex-FX… strong equipment sales as new product

introductions gaining momentum and healthy global demand

Adj EBITDA margin up 10 bps; lapping strong Q4’16 performance of +800

bps

FY Adj EBITDA margin up 140 bps benefiting from volume gains and

continued execution of operational excellence initiatives (VAVE, lean,

restructuring)… record margin level at 21.5%

iConn Smart Air Flow Management PlatformAir analytics cloud platform providing predictive air insights for customers’ compressed air needs. Over

2,100 iConn units registered in the field with significant ramp expected in 2018.

As Reported

YOYChange

Ex-FX YOY Change

Revenue $311.7 11.8% 6.7%

Adj EBITDA $69.0 12.4% 6.4%

Adj EBITDA Margin 22.1% 10 bps

Innovation in Action

Q4 2017

As Reported

YOYChange

Ex-FX YOY Change

Revenue $1,130.7 4.5% 3.4%

Adj EBITDA $242.7 11.5% 10.2%

Adj EBITDA Margin 21.5% 140 bps

FY 2017

Energy Segment – Q4 & FY Highlights

13

($M)

Upstream Energy Consumables: Redline PackingPacking is the critical seal system in the heart of a fluid

end. Redline Packing’s increased life versus competitor’s offerings and ability to increase product uptime led to

recent adoption by a Tier 1 pressure pumper.

Highlights (All Q4 unless otherwise noted):

Orders up 62% as reported; up 58% ex-FX

Revenue up 18% ex-FX; aftermarket revenue up 54%

Upstream revenue up 99% ex-FX; Mid/Downstream down double

digits due to timing of prior year project shipments

Adj EBITDA margins up 250 bps due to strong upstream volume

performance & operational efficiencies

As Reported

YOYChange

Ex-FX YOY Change

Revenue $295.1 21.6% 18.3%

Adj EBITDA $96.9 31.7% 28.1%

Adj EBITDA Margin 32.8% 250 bps

Innovation in Action

As Reported

YOYChange

Ex-FX YOY Change

Revenue $1,014.5 61.4% 60.0%

Adj EBITDA $296.1 105.9% 104.0%

Adj EBITDA Margin 29.2% 630 bps

Q4 2017 FY 2017

As Reported

YOYChange

Ex-FX YOY Change

Revenue $58.2 3.0% (1.2)%

Adj EBITDA $15.5 (9.9)% (14.0)%

Adj EBITDA Margin 26.6% (380) bps

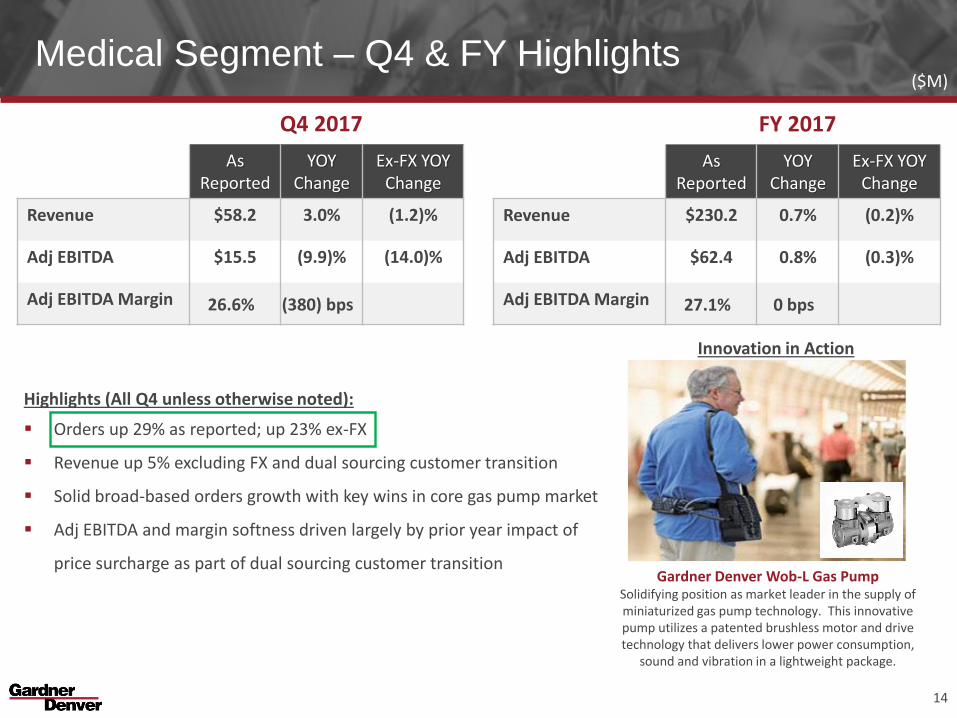

Medical Segment – Q4 & FY Highlights

14

($M)

Gardner Denver Wob-L Gas PumpSolidifying position as market leader in the supply of miniaturized gas pump technology. This innovative pump utilizes a patented brushless motor and drive technology that delivers lower power consumption,

sound and vibration in a lightweight package.

Highlights (All Q4 unless otherwise noted):

Orders up 29% as reported; up 23% ex-FX

Revenue up 5% excluding FX and dual sourcing customer transition

Solid broad-based orders growth with key wins in core gas pump market

Adj EBITDA and margin softness driven largely by prior year impact of

price surcharge as part of dual sourcing customer transition

As Reported

YOYChange

Ex-FX YOY Change

Revenue $230.2 0.7% (0.2)%

Adj EBITDA $62.4 0.8% (0.3)%

Adj EBITDA Margin 27.1% 0 bps

Innovation in Action

Q4 2017 FY 2017

Strategy Update & 2018 Guidance

Our Strategy

Deploy Talent

Creating a performance driven culture with highly engaged employees

– Creating a great place to work – Launched multi-year engagement initiative

– Acting like owners – Awarded ~$100M in equity across ~6,000 employees

Continue to enhance expertise and talent in critical functions

Expand Margins

Driving Lean Manufacturing across multitude of sites (still early)

Leveraging spend across organization (e.g., freight, sourcing) to generate further savings

Maturing Value Engineering process to drive further product enhancements and efficiencies

Accelerate Growth

Commercializing new products with new sophisticated Demand Generation process

Embedding smart technologies (e.g., iConn) into products

Leveraging investments in emerging markets – “innovation in the region for the region”

Allocate Capital Effectively

Invest in core: new products, new technologies and emerging markets

Reduce leverage: Net Debt-to-Adjusted EBITDA target

Execute disciplined M&A based on clear strategic and financial criteria

16

Strong Foundation, Clear Strategy, Committed Leadership

Acquisition of Runtech Systems

17¹ Financial estimates are included in total Gardner Denver’s FY2018 guidance.

Runtech is a leader in turbo vacuum technology systems and optimization solutions for use in a variety of industrial process-oriented end markets

Patented technology designed to provide energy efficient, environmentally friendly vacuum solutions … 50%-70% energy efficiency vs. alternative technologies and 100% water-free

Net purchase price of ~$93 million funded by cash on hand; will be included in GDI’s Industrials Segment1

EcoPump™ EcoFlow™

Mission-Critical Technologies with Low Cost Relative to Overall System

Growing Aftermarket Platform

Highly Complementary, Innovative & Differentiated Technology

Meaningful Synergies Identified

Strong Growth Potential Backed by Solid Secular Trends

ROIC, Mid-Teens by Year 3

Attractive Profile

2018 Guidance

18

1 Represents the full year expectation of weighted average diluted shares outstanding based on 2017 year end share count and share price. Outlook does not include impacts of option or share grants in 2018 associated with Company’s 2017 long term incentive plan.2 All revenue outlook commentary expressed in percentages

Secular Drivers Growth Profile 2018 Revenue Outlook2

Industrials Increasing Need for Efficiency & Technology GDP+Mid-high single

digit3

Medical Growing Health Needs Globally GDP+ Mid-single digit

Mid &Downstream Energy

Growing Need for Energy & Infrastructure GDP+Mid-single digit

Upstream Energy

Multiple Layers of GrowthIncreasing intensity of fracturing (longer laterals) & growing backlog of DUCsPending replacement cycle

Activity & Intensity-driven

Mid-teens

ENERGY

▪ Adjusted EBITDA $650M to $670M

▪ Capital Expenditures $65M to $75M

▪ Tax Rate 26% to 28%

▪ Average Shares Outstanding1 209.3M

▪ Segment Sales Outlook:

3 Includes the impact of Runtech acquisition

Continuing to Execute Our Strategy

19

DeployTalent

• Continued talent infusion in critical functions & domain expertise (P&L Leadership, Board of Directors)

• Company-wide engagement starting to deliver results

MarginExpansion

• FY’17 Adjusted EBITDA margin of 23.6%, up 290 bps

• Continued execution of lean, sourcing, VAVE initiatives

GrowthAcceleration

• FY’17 revenue growth of 21% ex-FX and strong momentum exiting the year (all three segments +20% orders in Q4’17)

• NPD acceleration driving growth

Capital Allocation

• FY’17 strong free cash flow generation, up 58%

• Reduced 2017 year-end leverage to 2.9x, down 1.3x from IPO

• Executing on disciplined M&A strategy (LeROI, Runtech)

Delivering Results in 2017 & Building Momentum for 2018+

Q&A

Appendix

Reconciliation of Net Income/(Loss) and Earnings/(Loss) per Share to Adjusted Net Income and Adjusted Earnings per Share

22

2017 2016 2017 2016

Net Income (Loss) 143.8$ (4.3)$ 18.5$ (31.3)$

Basic Earnings (Loss) Per Share (As Reported)1,20.71$ (0.07)$ 0.10$ (0.25)$

Diluted Earnings (Loss) Per Share (As Reported)1,20.69$ (0.07)$ 0.10$ (0.25)$

Plus:

(Benefit) provision for income taxes (90.1) 1.3 (131.2) (31.9)

Amortization of acquisition related intangible assets 27.3 27.4 107.7 110.6

Impairment of goodwill and other intangible assets 1.6 23.8 1.6 25.3

Sponsor fees and expenses - 1.0 17.3 4.8

Restructuring and related business transformation costs 4.2 32.5 24.7 78.7

Acquisition related expenses and non-cash charges 1.0 0.6 4.1 4.3

Environmental remediation loss reserve - 5.6 0.9 5.6

Expenses related to public stock offerings 0.5 - 4.1 -

Establish public company financial reporting compliance 0.9 0.1 8.1 0.2

Stock-based compensation 28.2 - 194.2 -

Loss on extinguishment of debt - - 84.5 -

Foreign currency transaction losses (gains), net 3.0 (3.3) 9.3 (5.9)

Other adjustments 7.5 3.5 10.9 7.9

Minus:

Income tax provision, as adjusted 27.8 21.8 105.4 34.7

Adjusted Net Income 100.1$ 66.4$ 249.3$ 133.6$

Adjusted Basic Earnings Per Share20.50$ 0.45$ 1.37$ 0.90$

Adjusted Diluted Earnings Per Share2,40.48$ 0.44$ 1.32$ 0.88$

Average shares outstanding:

Basic, as reported 201.4 148.7 182.2 149.2

Diluted, as reported3209.3 148.7 188.4 149.2

Adjusted diluted4209.3 151.9 188.4 151.0

3 Due to net losses in certain periods shown, basic and diluted average shares outstanding are the same in those periods.4 Adjusted diluted share count and adjusted diluted earnings per share include incremental dilutive shares, using the

treasury stock method, which are added to average shares outstanding.

1 Basic and diluted earnings per share (as reported) are calculated by dividing net income (loss) attributable to Gardner

Denver Holdings, Inc. by the basic and diluted average shares outstanding for the respective periods.2 Basic and diluted earnings per share (as reported) and adjusted basic and diluted earnings per share for the three month

and years ended December 31, 2017 and 2016 are not comparable due to the significant change in capital structure as a

result of the initial public offering in May of 2017.

Month Period Ended Year Ended

December 31, December 31,

GARDNER DENVER HOLDINGS, INC. AND SUBSIDIARIES

RECONCILIATION OF NET INCOME (LOSS) AND EARNINGS (LOSS) PER SHARE TO ADJUSTED NET

INCOME AND ADJUSTED EARNINGS PER SHARE

(Dollars in millions, except per share amounts)

(Unaudited)

For the Three For the

Reconciliation of Net Income/(Loss) to Adjusted EBITDA and Adjusted Net Income and CFOA to Free Cash Flow

23

2017 2016 2017 2016

Net Income (Loss) 143.8$ (4.3)$ 18.5$ (31.3)$

Plus:

Interest expense 25.2 41.6 140.7 170.3

(Benefit) provision for income taxes (90.1) 1.3 (131.2) (31.9)

Depreciation expense 15.5 12.5 54.9 48.5

Amortization expense 31.3 33.4 118.9 124.2

Impairment of goodwill and other intangible assets 1.6 23.8 1.6 25.3

Sponsor fees and expenses - 1.0 17.3 4.8

Restructuring and related business transformation costs 4.2 32.5 24.7 78.7

Acquisition related expenses and non-cash charges 1.0 0.6 4.1 4.3

Environmental remediation loss reserve - 5.6 0.9 5.6

Expenses related to public stock offerings 0.5 - 4.1 -

Establish public company financial reporting compliance 0.9 0.1 8.1 0.2

Stock-based compensation 28.2 - 194.2 -

Loss on extinguishment of debt - - 84.5 -

Foreign currency transaction losses (gains), net 3.0 (3.3) 9.3 (5.9)

Other adjustments 7.5 3.5 10.9 7.9

Adjusted EBITDA 172.6$ 148.3$ 561.5$ 400.7$

Minus:

Interest expense 25.2 41.6 140.7 170.3

Income tax provision, as adjusted 27.8 21.8 105.4 34.7

Depreciation expense 15.5 12.5 54.9 48.5

Amortization of non-acquisition related intangible assets 4.0 6.0 11.2 13.6

Adjusted Net Income 100.1$ 66.4$ 249.3$ 133.6$

Free Cash Flow

Cash flows - operating activities 116.6 58.8 200.5 165.6

Minus:

Capital expenditures 20.4 28.1 56.8 74.4

Free Cash Flow 96.2$ 30.7$ 143.7$ 91.2$

Month Period Ended Year Ended

December 31, December 31,

For the Three For the

GARDNER DENVER HOLDINGS, INC. AND SUBSIDIARIES RECONCILIATION OF NET INCOME (LOSS) TO ADJUSTED EBITDA AND ADJUSTED NET INCOME AND

CASH FLOWS - OPERATING ACTIVITIES TO FREE CASH FLOW

(Dollars in millions)

(Unaudited)

Reconciliation of Segment Adjusted EBITDA to Income/(Loss) Before Income Taxes

24

2017 2016 2017 2016

Revenue

Industrials 311.7$ 278.7$ 1,130.7$ 1,082.3$

Energy 295.1 242.6 1,014.5 628.4

Medical 58.2 56.4 230.2 228.7

Total Revenue 665.0$ 577.7$ 2,375.4$ 1,939.4$

Segment Adjusted EBITDA

Industrials 69.0$ 61.4$ 242.7$ 217.6$

Energy 96.9 73.6 296.1 143.8

Medical 15.5 17.2 62.4 61.9

Total Segment Adjusted EBITDA 181.4$ 152.2$ 601.2$ 423.3$

Less items to reconcile Segment Adjusted EBITDA to

Income (Loss) Before Income Taxes:

Corporate expenses not allocated to segments 8.8$ 3.9$ 39.7$ 22.6$

Interest expense 25.2 41.6 140.7 170.3

Depreciation and amortization expense 46.8 45.9 173.8 172.7

Impairment of goodwill and other intangible assets 1.6 23.8 1.6 25.3

Sponsor fees and expenses - 1.0 17.3 4.8

Restructuring and related business transformation costs 4.2 32.5 24.7 78.7

Acquisition related expenses and non-cash charges 1.0 0.6 4.1 4.3

Environmental remediation loss reserve - 5.6 0.9 5.6

Expenses related to public stock offerings 0.5 - 4.1 -

Establish public company financial reporting compliance 0.9 0.1 8.1 0.2

Stock-based compensation 28.2 - 194.2 -

Loss on extinguishment of debt - - 84.5 -

Foreign currency transaction losses (gains), net 3.0 (3.3) 9.3 (5.9)

Other adjustments 7.5 3.5 10.9 7.9

Income (Loss) Before Income Taxes 53.7$ (3.0)$ (112.7)$ (63.2)$

Month Period Ended Year Ended

December 31, December 31,

For the Three For the

GARDNER DENVER HOLDINGS, INC. AND SUBSIDIARIES

RECONCILIATION OF SEGMENT ADJUSTED EBITDA TO INCOME (LOSS) BEFORE INCOME TAXES

(Dollars in millions)

(Unaudited)