global macro research top mind europe a t a crossroads

TRANSCRIPT

EUROPE AT A CROSSROADS

ISSUE 102| October 18, 2021| 5:15 PM EDT—’’’’’S’’’’’

’’’’ ’ ’ ’ ’

Global Macro Research

Investors should consider this report as only a single factor in making their investment decision. For Reg AC certification and other important disclosures, see the Disclosure Appendix, or go to www.gs.com/research/hedge.html.

The Goldman Sachs Group, Inc.

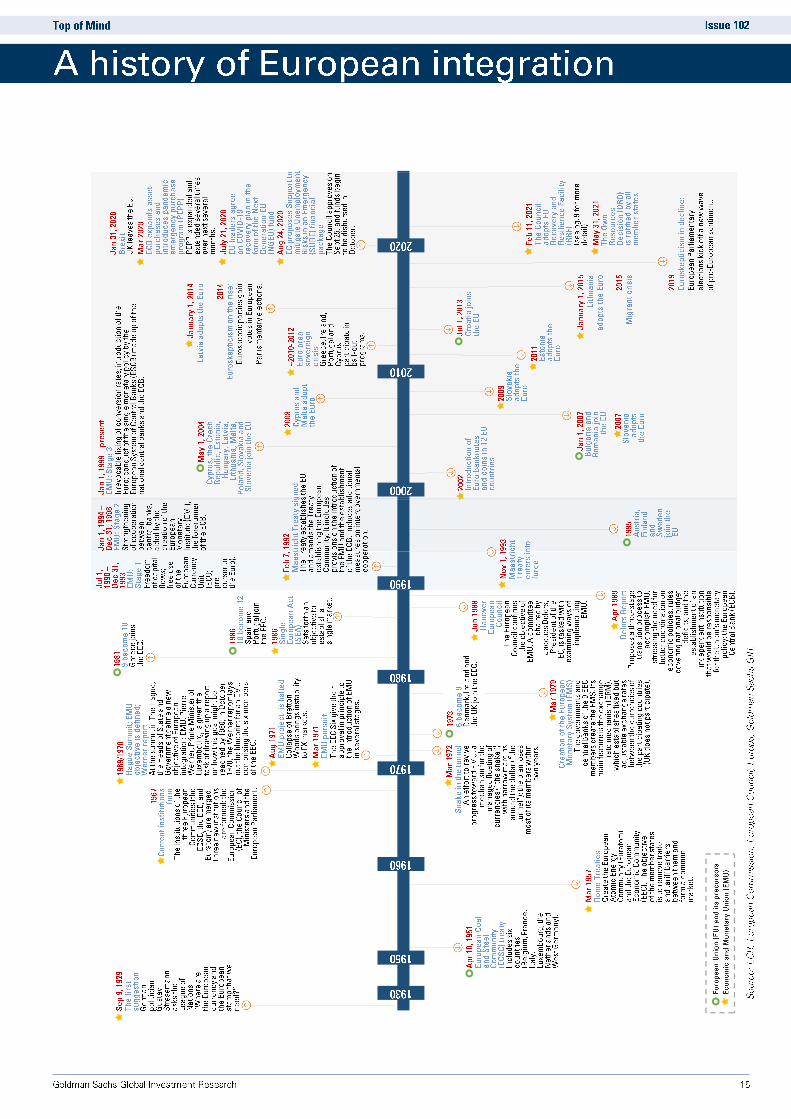

The Euro area's unprecedented program of fiscal risk sharing in response to the pandemic, and a new, likely less fiscally conservative ruling coalition in Germany, looks set to put the region on a path towards increased integration, higher growth, and better investor returns. But whether the current moment will go down as a seized—or (another) missed—opportunity for Euro area integration and growth is Top of Mind. We speak with our own Jari Stehn, who is optimistic that the fiscal shifts will move the region in the right direction over the medium term and remains constructive on the economic outlook despite China and energy risks, and former ECB Chief Economist Otmar Issing, who is more worried about the fiscal shifts and

longer-term growth. We then ask former PM of Italy and President of the EC Romano Prodi and Oxford’s Timothy Garton Ash whether these shifts will ultimately lead to a stronger EU. Prodi thinks the EU is past the point of existential danger, although integration from here will be slow. But Garton Ash warns that peak populism may not be behind us.

While I do think some progress [on integration] is possible…further progress in the most sensitive areas such as fiscal union will likely be very slow.

- Romano Prodi

“[Euro area] growth beyond 2022 will depend quite significantly on fiscal policies, and I’m afraid some countries may waste the opportunity to pursue productive investments.

- Otmar Issing

“

INTERVIEWS WITH:

Otmar Issing, Former Chief Economist of the European Central Bank

Romano Prodi, Former Prime Minister of Italy and President of the European Commission

Timothy Garton Ash, Professor, University of Oxford

Jari Stehn, Chief European Economist, Goldman Sachs

DON’T LET A GOOD CRISIS GO TO WASTE Filippo Taddei, GS Europe Economics Research

EUROPEAN EQUITIES: A STRONGER CASE Sharon Bell, GS European Equity Strategy Research

THE COSTS OF DECARBONIZATION Jeff Currie, GS Commodities Research

SAFE ASSET SUPPLY IN THE POST-MERKEL ERA George Cole, GS Markets Research

A NEW POST-MERKEL GERMAN FISCAL NORMAL Sören Radde, GS Europe Economics Research

WHAT’S INSIDE

of

Allison Nathan | [email protected] ...AND MORE

Europe has seldom missed an opportunity to miss an opportunity over the last decade.

- Timothy Garton Ash

TOP MIND

Jenny Grimberg | [email protected] Gabriel Lipton Galbraith | [email protected]

Note: The following is a redacted version of the original report published October 18, 2021 [31 pgs].

-90-75-60-45-30-15

0153045607590

105120

Jan-20 Jul-20 Jan-21 Jul-21 Jan-22 Jul-22

New CarsUsed CarsRental CarsVideo/Audio/Photo & Info. Equip.Sports & Recreational VehiclesSporting EquipmentFurnitureHousing Appliances

GS Forecast

0 1 2 3 4 5 6 7 8 9 10 11 12

US

India

Europe

Japan

Indonesia

Philippines

Australia

New Zealand

Korea

Thailand

Singapore

Malaysia

Taiwan

Hong Kong

Consumption

Investment

Percent of GDP

-0.8

-0.7

-0.6

-0.5

-0.4

-0.3

-0.2

-0.1

0.0

0.1

0.2

Q4 Q1 Q2 Q3 Q4

2021 2022

Germany France Italy Spain UK

Scenario 1 Scenario 2 Scenario 3

-5.0

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

Direct effects

Indirect effects

Financial conditions tightening

New starts: -15%Completion: +10%Sales volume: -5%ASP: -5%Land sales: -15%FCI: +35bp

New starts: -22.5%Completion: 0%Sales volume: -7.5%ASP: -7.5%Land sales: -22.5%FCI: +70bp

New starts: -30%Completion: -10%Sales volume: -10%ASP: -10%Land sales: -30%FCI: +140bp

Base case

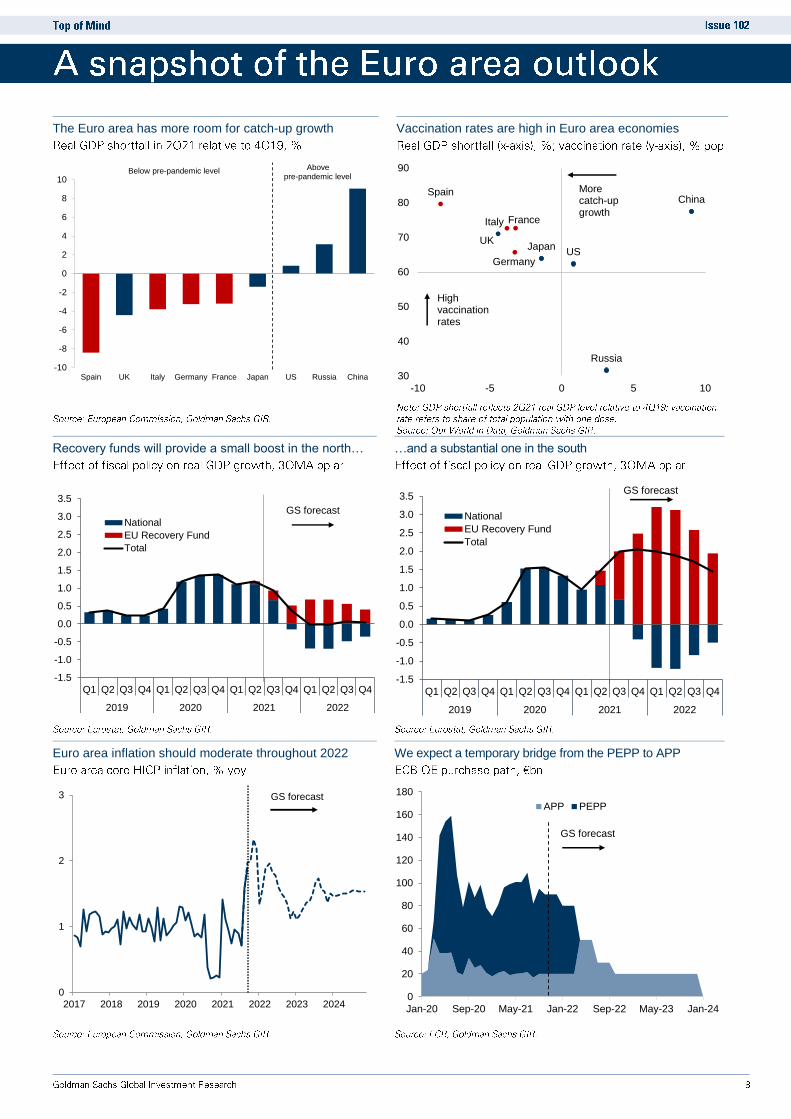

The Euro area has more room for catch-up growth Vaccination rates are high in Euro area economies

Recovery funds will provide a small boost in the north… …and a substantial one in the south

Euro area inflation should moderate throughout 2022 We expect a temporary bridge from the PEPP to APP

-10

-8

-6

-4

-2

0

2

4

6

8

10

Spain UK Italy Germany France Japan US Russia China

Above pre-pandemic level

Below pre-pandemic level

UK

Spain

Italy

Germany

France

JapanUS

Russia

China

30

40

50

60

70

80

90

-10 -5 0 5 10

High vaccination rates

More catch-upgrowth

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2019 2020 2021 2022

National

EU Recovery Fund

Total

GS forecast

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2019 2020 2021 2022

National

EU Recovery Fund

Total

GS forecast

0

1

2

3

2017 2018 2019 2020 2021 2022 2023 2024

GS forecast

0

20

40

60

80

100

120

140

160

180

Jan-20 Sep-20 May-21 Jan-22 Sep-22 May-23 Jan-24

APP PEPP

GS forecast

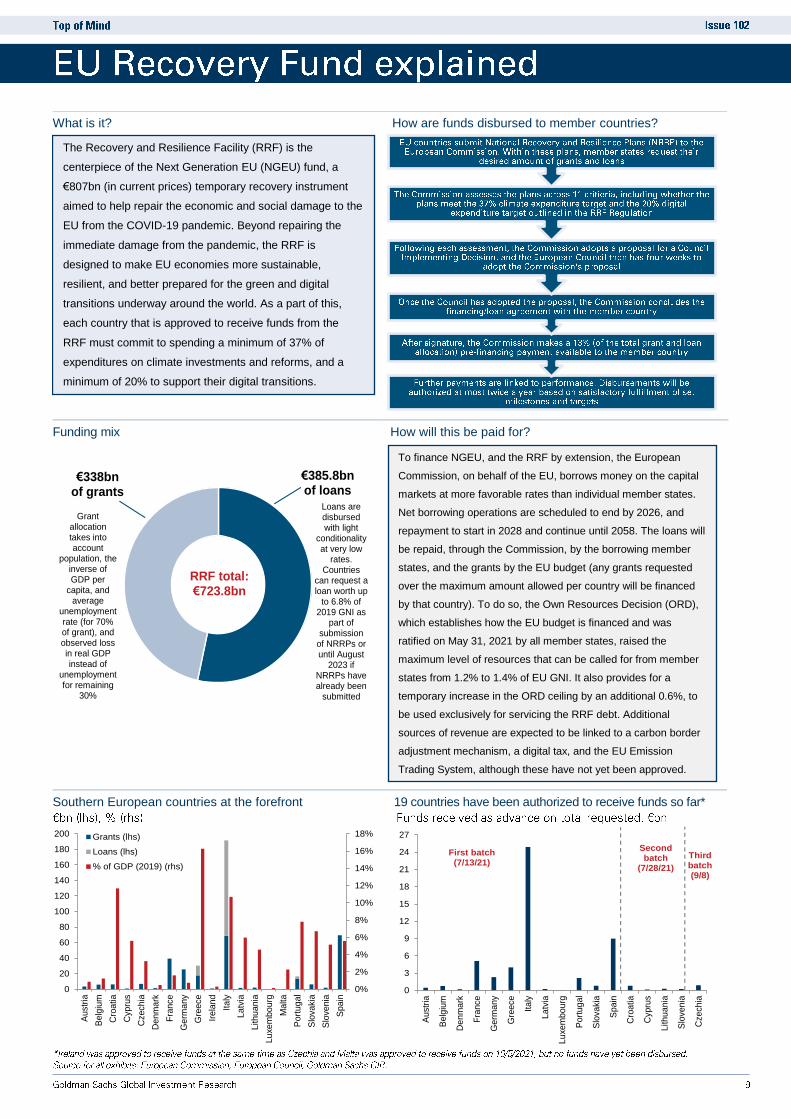

What is it? How are funds disbursed to member countries?

Funding mix How will this be paid for?

Southern European countries at the forefront 19 countries have been authorized to receive funds so far*

€338bn of grants

€385.8bn of loans

RRF total:€723.8bn

Loans are disbursed with light

conditionality at very low

rates. Countries

can request a loan worth up

to 6.8% of 2019 GNI as

part of submission

of NRRPs or until August

2023 if NRRPs have already been

submitted

Grantallocation takes into account

population, the inverse of GDP per

capita, and average

unemployment rate (for 70% of grant), and observed loss in real GDP instead of

unemployment for remaining

30%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0

20

40

60

80

100

120

140

160

180

200

Austr

ia

Belg

ium

Cro

atia

Cypru

s

Czechia

De

nm

ark

Fra

nce

Germ

any

Gre

ece

Irela

nd

Ita

ly

La

tvia

Lithu

ania

Lu

xe

mbo

urg

Ma

lta

Port

ug

al

Slo

vakia

Slo

ven

ia

Spain

Grants (lhs)

Loans (lhs)

% of GDP (2019) (rhs)

0

3

6

9

12

15

18

21

24

27

Austr

ia

Belg

ium

De

nm

ark

Fra

nce

Germ

any

Gre

ece

Ita

ly

La

tvia

Lu

xe

mbo

urg

Port

ug

al

Slo

vakia

Spain

Cro

atia

Cypru

s

Lithu

ania

Slo

ven

ia

Czechia

Third batch (9/8)

First batch (7/13/21)

Second batch

(7/28/21)

The Recovery and Resilience Facility (RRF) is the

centerpiece of the Next Generation EU (NGEU) fund, a

€807bn (in current prices) temporary recovery instrument

aimed to help repair the economic and social damage to the

EU from the COVID-19 pandemic. Beyond repairing the

immediate damage from the pandemic, the RRF is

designed to make EU economies more sustainable,

resilient, and better prepared for the green and digital

transitions underway around the world. As a part of this,

each country that is approved to receive funds from the

RRF must commit to spending a minimum of 37% of

expenditures on climate investments and reforms, and a

minimum of 20% to support their digital transitions.

To finance NGEU, and the RRF by extension, the European

Commission, on behalf of the EU, borrows money on the capital

markets at more favorable rates than individual member states.

Net borrowing operations are scheduled to end by 2026, and

repayment to start in 2028 and continue until 2058. The loans will

be repaid, through the Commission, by the borrowing member

states, and the grants by the EU budget (any grants requested

over the maximum amount allowed per country will be financed

by that country). To do so, the Own Resources Decision (ORD),

which establishes how the EU budget is financed and was

ratified on May 31, 2021 by all member states, raised the

maximum level of resources that can be called for from member

states from 1.2% to 1.4% of EU GNI. It also provides for a

temporary increase in the ORD ceiling by an additional 0.6%, to

be used exclusively for servicing the RRF debt. Additional

sources of revenue are expected to be linked to a carbon border

adjustment mechanism, a digital tax, and the EU Emission

Trading System, although these have not yet been approved.

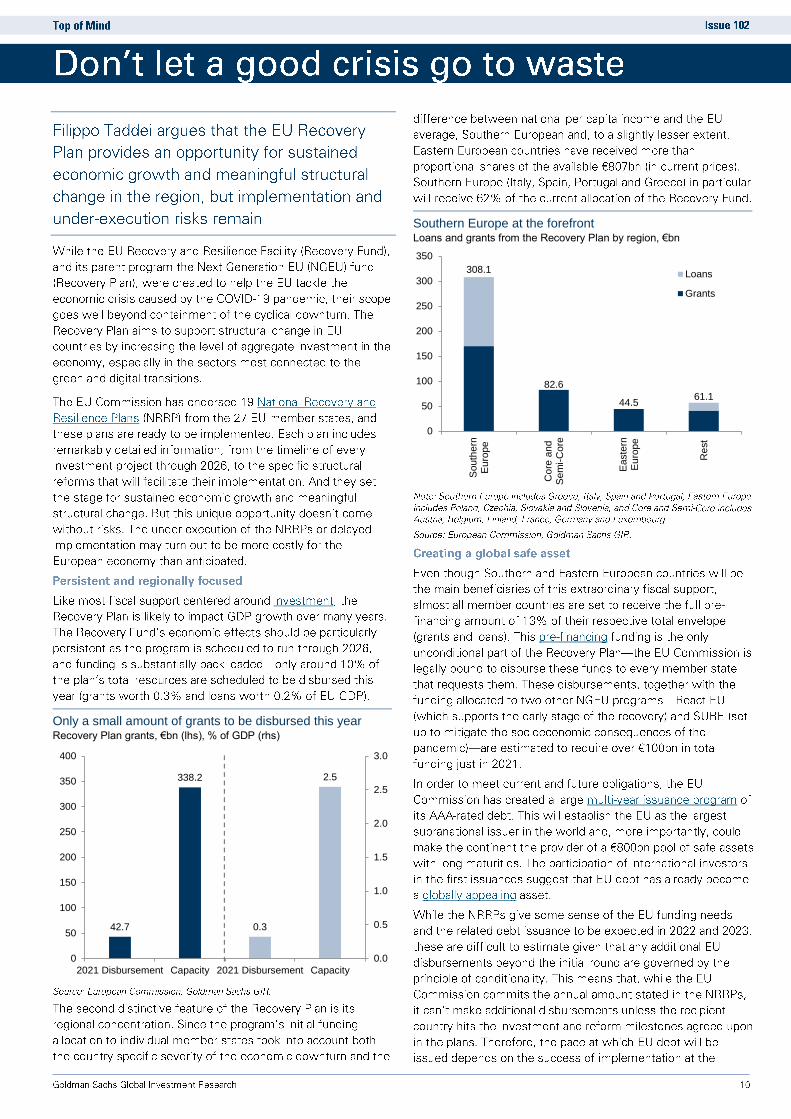

Only a small amount of grants to be disbursed this year Recovery Plan grants, €bn (lhs), % of GDP (rhs)

Southern Europe at the forefront Loans and grants from the Recovery Plan by region, €bn

42.7

338.2

0.3

2.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

0

50

100

150

200

250

300

350

400

2021 Disbursement Capacity 2021 Disbursement Capacity

82.6

44.5

308.1

61.1

0

50

100

150

200

250

300

350

So

uth

ern

Eu

rop

e

Co

re a

nd

Se

mi-

Co

re

Easte

rnE

uro

pe

Re

st

Loans

Grants

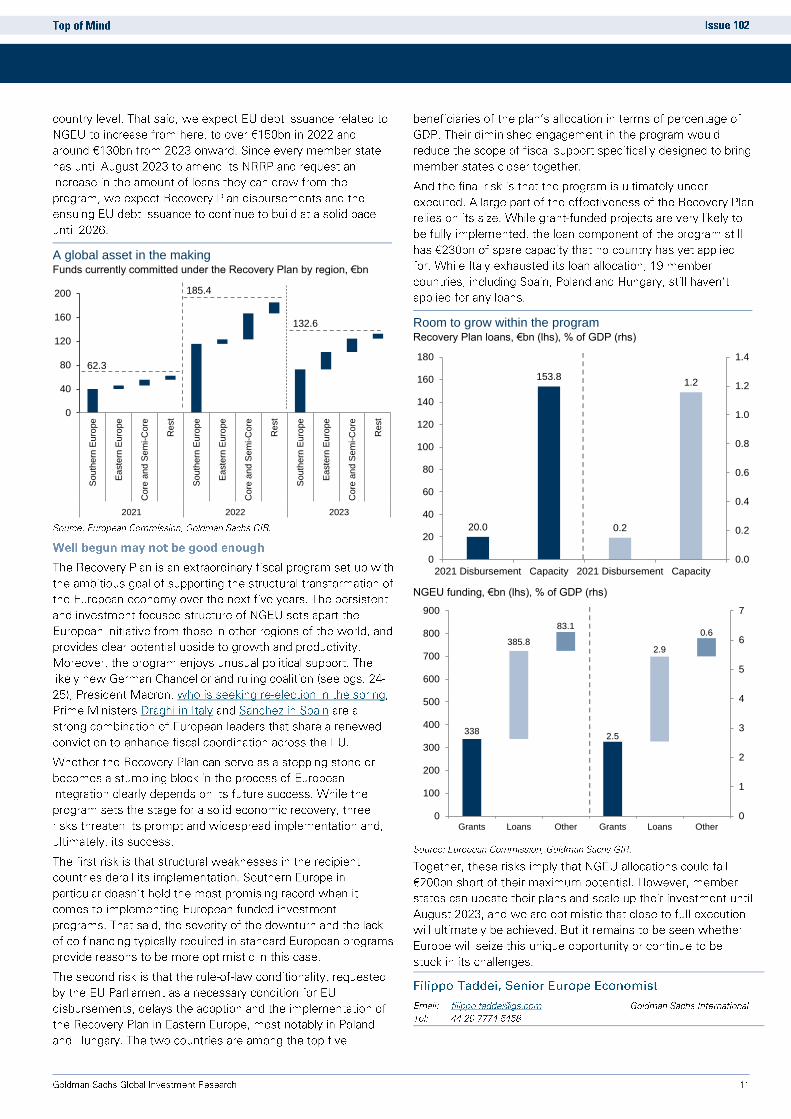

A global asset in the making Funds currently committed under the Recovery Plan by region, €bn

Room to grow within the program Recovery Plan loans, €bn (lhs), % of GDP (rhs)

NGEU funding, €bn (lhs), % of GDP (rhs)

0

40

80

120

160

200

So

uth

ern

Eu

rope

Ea

ste

rn E

uro

pe

Co

re a

nd

Se

mi-C

ore

Re

st

So

uth

ern

Eu

rope

Ea

ste

rn E

uro

pe

Co

re a

nd

Se

mi-C

ore

Re

st

So

uth

ern

Eu

rope

Ea

ste

rn E

uro

pe

Co

re a

nd

Se

mi-C

ore

Re

st

2021 2022 2023

62.3

185.4

132.6

20.0

153.8

0.2

1.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

0

20

40

60

80

100

120

140

160

180

2021 Disbursement Capacity 2021 Disbursement Capacity

338

385.8

83.1

2.5

2.9

0.6

0

1

2

3

4

5

6

7

0

100

200

300

400

500

600

700

800

900

Grants Loans Other Grants Loans Other

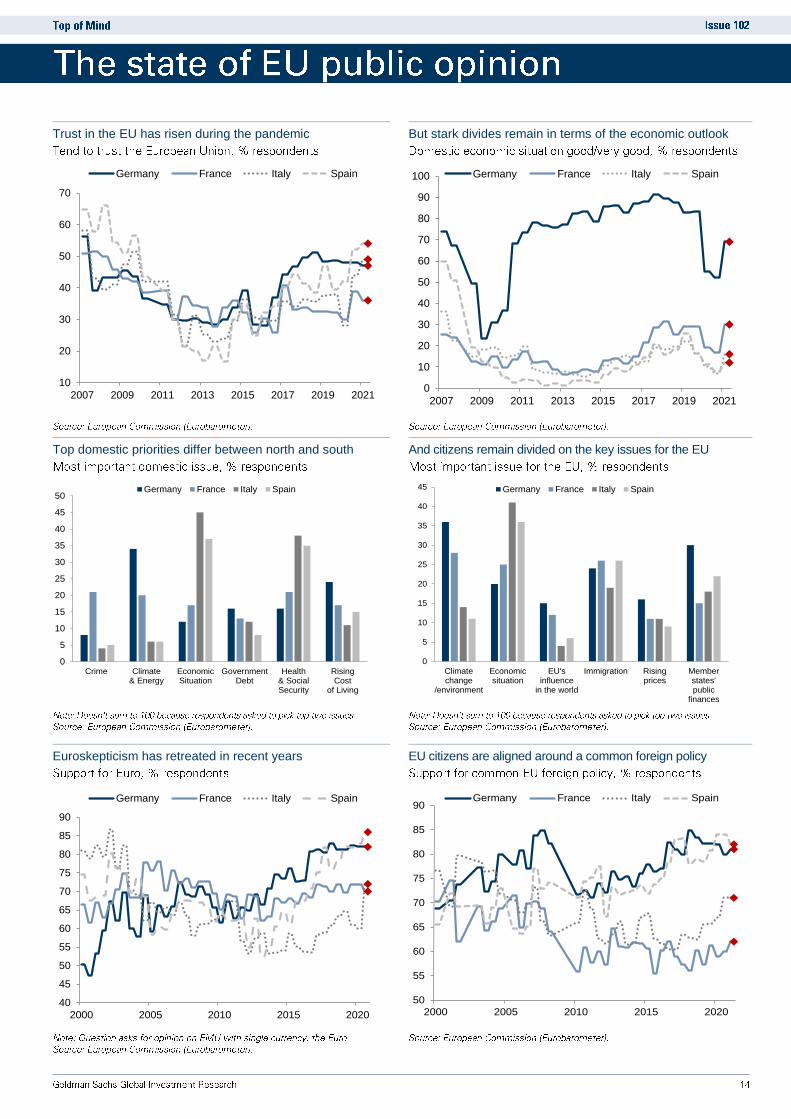

Trust in the EU has risen during the pandemic But stark divides remain in terms of the economic outlook

Top domestic priorities differ between north and south And citizens remain divided on the key issues for the EU

Euroskepticism has retreated in recent years EU citizens are aligned around a common foreign policy

10

20

30

40

50

60

70

2007 2009 2011 2013 2015 2017 2019 2021

Germany France Italy Spain

0

10

20

30

40

50

60

70

80

90

100

2007 2009 2011 2013 2015 2017 2019 2021

Germany France Italy Spain

0

5

10

15

20

25

30

35

40

45

50

Crime Climate& Energy

EconomicSituation

GovernmentDebt

Health& SocialSecurity

RisingCost

of Living

Germany France Italy Spain

0

5

10

15

20

25

30

35

40

45

Climatechange

/environment

Economicsituation

EU'sinfluence

in the world

Immigration Risingprices

Memberstates'public

finances

Germany France Italy Spain

40

45

50

55

60

65

70

75

80

85

90

2000 2005 2010 2015 2020

Germany France Italy Spain

50

55

60

65

70

75

80

85

90

2000 2005 2010 2015 2020

Germany France Italy Spain

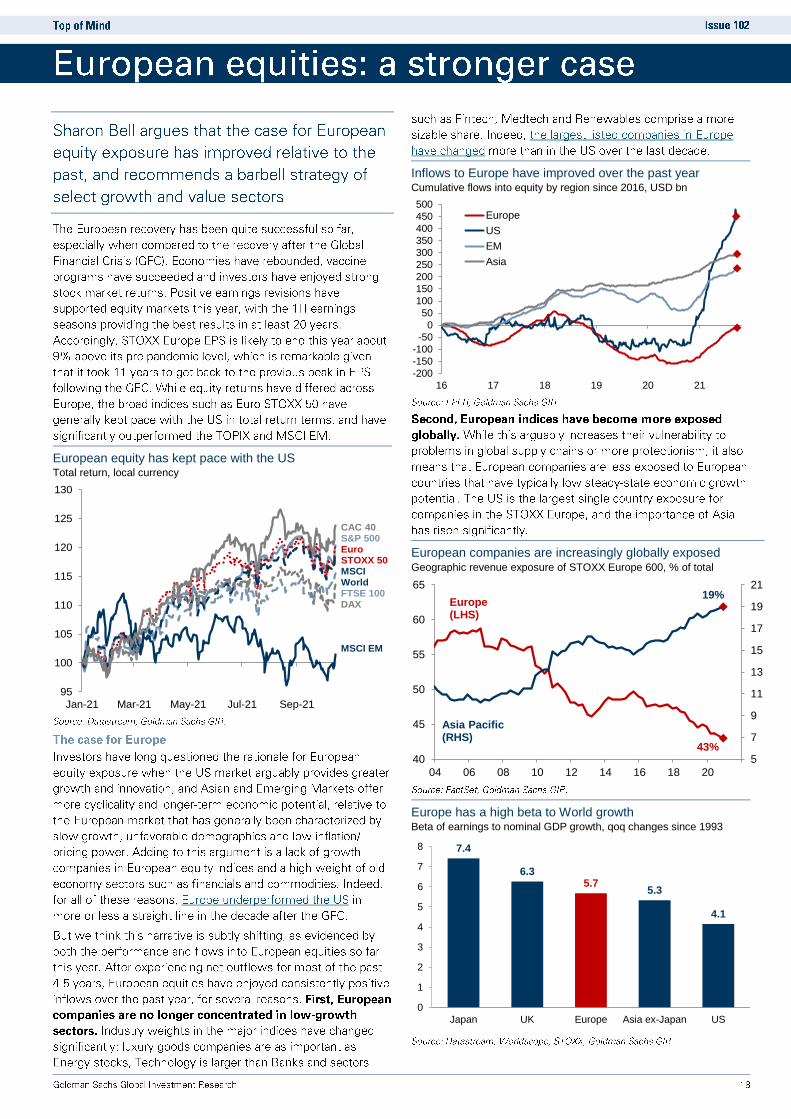

European equity has kept pace with the US Total return, local currency

Inflows to Europe have improved over the past year Cumulative flows into equity by region since 2016, USD bn

European companies are increasingly globally exposed Geographic revenue exposure of STOXX Europe 600, % of total

Europe has a high beta to World growth Beta of earnings to nominal GDP growth, qoq changes since 1993

95

100

105

110

115

120

125

130

Jan-21 Mar-21 May-21 Jul-21 Sep-21

CAC 40S&P 500Euro STOXX 50MSCI WorldFTSE 100DAX

MSCI EM

-200

-150

-100

-50

0

50

100

150

200

250

300

350

400

450

500

16 17 18 19 20 21

Europe

US

EM

Asia

5

7

9

11

13

15

17

19

21

40

45

50

55

60

65

04 06 08 10 12 14 16 18 20

Europe(LHS)

Asia Pacific(RHS)

43%

19%

7.4

6.35.7

5.3

4.1

0

1

2

3

4

5

6

7

8

Japan UK Europe Asia ex-Japan US

Even accounting for sector differences, European valuations

remain well below those of the US 24m fwd P/E with global equity weights, MSCI indices

6x

8x

10x

12x

14x

16x

18x

20x

01 03 05 07 09 11 13 15 17 19 21

US

Europe

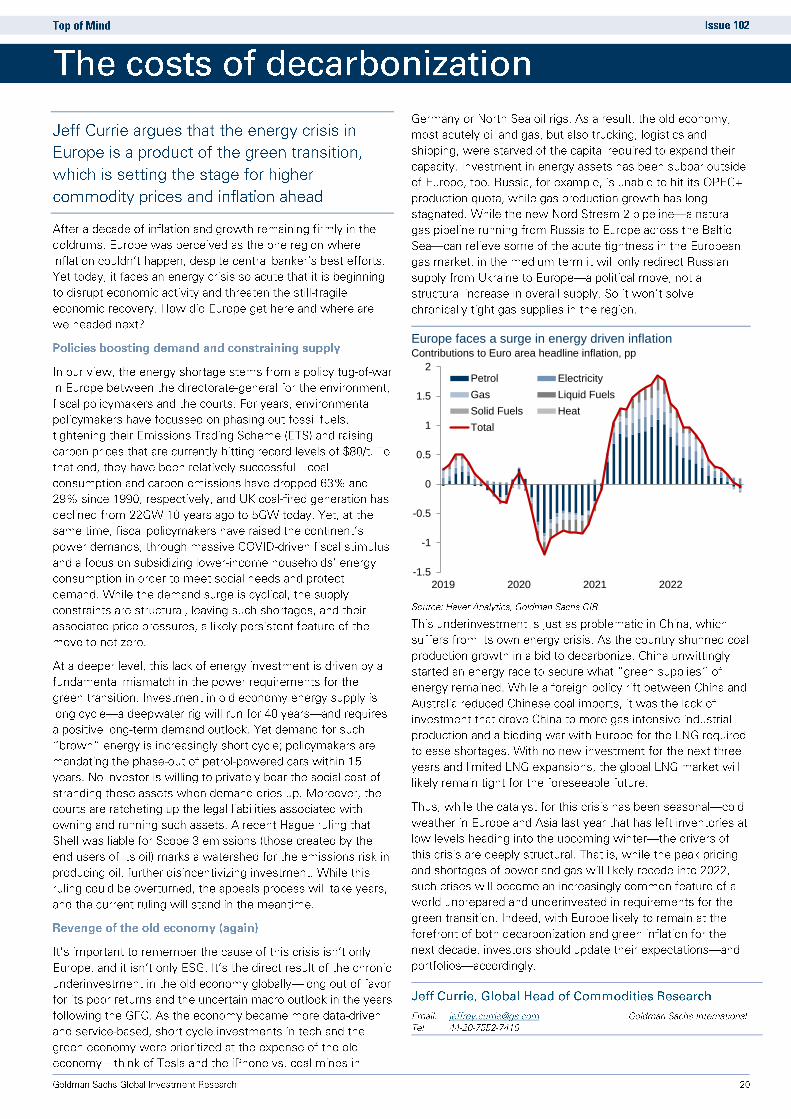

Europe faces a surge in energy driven inflation Contributions to Euro area headline inflation, pp

-1.5

-1

-0.5

0

0.5

1

1.5

2

2019 2020 2021 2022

Petrol Electricity

Gas Liquid Fuels

Solid Fuels Heat

Total

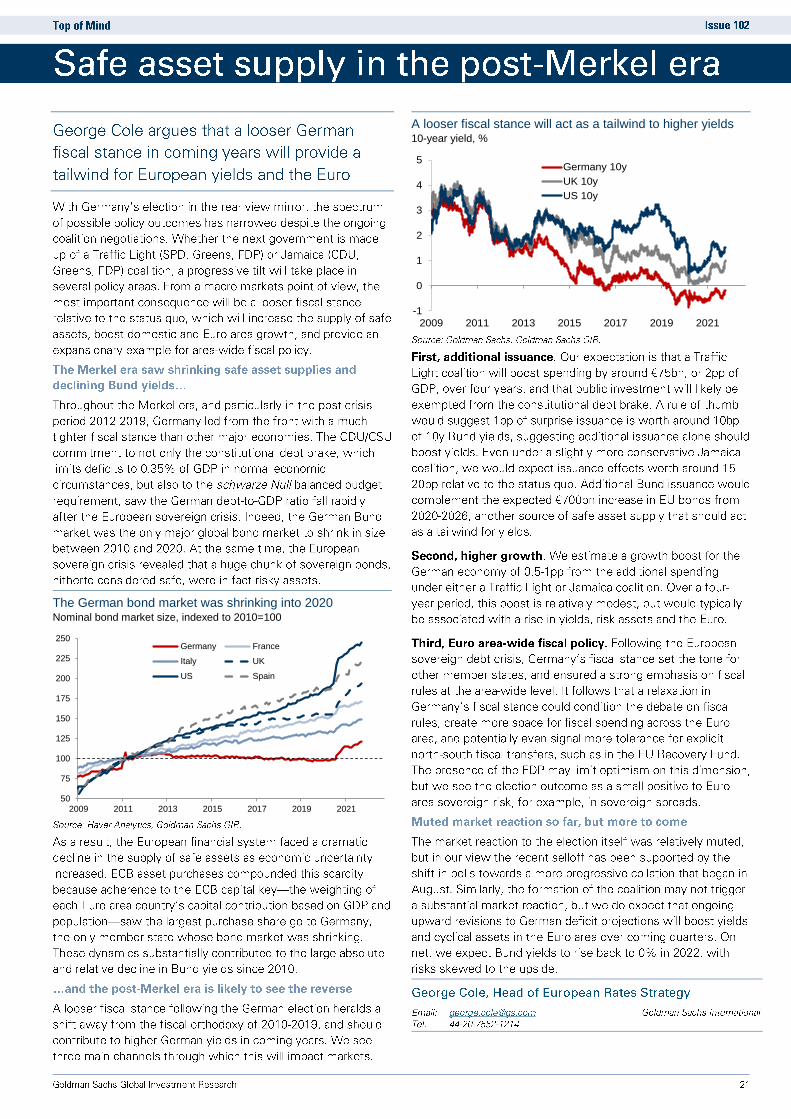

The German bond market was shrinking into 2020 Nominal bond market size, indexed to 2010=100

A looser fiscal stance will act as a tailwind to higher yields 10-year yield, %

50

75

100

125

150

175

200

225

250

2009 2011 2013 2015 2017 2019 2021

Germany France

Italy UK

US Spain

-1

0

1

2

3

4

5

2009 2011 2013 2015 2017 2019 2021

Germany 10y

UK 10y

US 10y

Left

Can

did

ate

s:

An

nale

na

Baerb

ock

Wo

n 1

5%

of

vo

tes a

nd

118

of

735 s

eats

in

th

e

Bu

nd

esta

g

•R

oots

in the 1

970s;

his

torically

focused o

n

pacifis

m a

nd e

nvironm

enta

l

activis

m

•S

upport

sconstitu

tional

change t

o d

ebt

bra

ke t

o

allo

w f

or

public

investm

ent

with a

specifie

d lim

it

•In

favor

of

rais

ing h

ighest

incom

e t

ax r

ate

s;

support

s

wealth t

ax,

25%

corp

ora

te

tax,

dig

ital corp

ora

te t

ax

•S

upport

s E

UR

50bn o

f

annual additio

nal public

investm

ent

until 2030

•A

ims to r

educe c

arb

on

em

issio

ns b

y 70%

by

2030;

aim

s f

or

carb

on n

eutr

alit

y

well

befo

re m

id-c

entu

ry

•S

upport

s incre

asin

g

unem

plo

yment

benefits

LIN

KE

Fre

e D

em

oc

rati

c

Pa

rty

(FD

P)

“Y

EL

LO

W”

GR

EE

NS

So

cia

l D

em

oc

rats

(SP

D)

“R

ED

”

Ch

ris

tia

n

De

mo

cra

tic

Un

ion

of

Ge

rma

ny/C

hri

sti

an

So

cia

l U

nio

n o

f

Ba

va

ria

(CD

U/C

SU

)

“B

LA

CK

”

PO

TE

NT

IAL

CO

AL

ITIO

NS

Cen

ter-

rig

ht

Can

did

ate

: A

rmin

Lasch

et

Wo

n 2

4%

of

vo

tes a

nd

196

of

735 s

eats

in

th

e

Bu

nd

esta

g

•C

DU

has r

oots

in the

Cath

olic

Cente

r P

art

y th

at

was f

ounded in 1

870

•C

SU

is the B

avarian s

iste

r

part

y of

the C

DU

•C

om

mitte

dto

debt

bra

ke;

wants

a s

wift

retu

rn t

o

bala

nced b

udgets

and t

he

60%

debt

ratio

•A

gain

st

rais

ing t

axes,

as

well

as w

ealth o

r

inherita

nce t

ax

•In

favor

of

main

tain

ing a

n

ele

vate

d level of

infr

astr

uctu

re i

nvestm

ent

•A

ims to r

educe c

arb

on

em

issio

ns b

y 65%

by

2030;

aim

s f

or

carb

on n

eutr

alit

y

by

2045

•C

om

mitte

d t

o p

ensio

n a

ge

of

67 b

y 2030

Cen

ter-

left

Can

did

ate

: O

laf

Sch

olz

Wo

n 2

6%

of

vo

tes a

nd

206

ou

t o

f 735 s

eats

in

th

e

Bu

nd

esta

g

•F

ounded in 1

875;

traditio

nally

repre

sents

the

inte

rests

of

the w

ork

ing

cla

ss

•R

eje

cts

auste

rity

;seeks to

levera

ge t

he f

iscal ro

om

allo

wed c

onstitu

tionally

•S

upport

s w

ealth t

ax,

financia

l tr

ansaction t

ax,

dig

ital ta

x,

and inte

rnational

min

imum

corp

ora

te t

ax

•In

favor

of

susta

inin

g E

UR

50bn o

f centr

al govern

ment

investm

ent

annually

•A

ims to r

educe c

arb

on

em

issio

ns b

y 65%

by

2030

and 8

8%

by

2040;

aim

s f

or

carb

on n

eutr

alit

y by

2045;

wants

to e

nhance g

reen

transport

ation

•A

ims to incre

ase m

inim

um

wage

to E

UR

12/h

our

Far-

left

Can

did

ate

s:

Jan

ine

Wis

sle

r an

d D

ietm

ar

Bart

sch

Wo

n <

5%

of

vo

tes a

nd

39

ou

t o

f735 s

eats

in

th

e

Bu

nd

esta

g

•F

ounded in 2

007 a

s a

merg

er

of

the P

art

y of

Dem

ocra

tic S

ocia

lism

(PD

S)

(successor

to t

he

Com

munis

t P

art

y th

at

rule

d

East

Germ

any)

and t

he

Ele

cto

ral A

ltern

ative f

or

Labor

and S

ocia

l Justice

(WA

SG

), c

om

prised o

f

trade u

nio

nis

ts a

nd

dis

gru

ntled f

orm

er

mem

bers

of

the

SP

D

•In

favor

of

a p

rogre

ssiv

e

wealth t

ax

•A

ims to r

educe p

ensio

n

age t

o 6

5

•A

ims to r

educe c

arb

on

em

issio

ns b

y 70%

by

2030;

aim

s f

or

carb

on n

eutr

alit

y

by

2035

Lib

era

l

Can

did

ate

:C

hri

sti

an

Lin

dn

er

Wo

n 1

2%

of

vo

tes a

nd

92

ou

t o

f 735 s

eats

in

th

e

Bu

nd

esta

g

•F

ounded in 1

948;

traditio

nally

pro

-

busin

ess/s

mall

govern

ment

•C

om

mitte

dto

debt

bra

ke

and w

ants

sw

ift

retu

rn t

o

60%

debt

ratio

•In

favor

of

rais

ing t

he

corp

ora

te t

ax r

ate

to a

t

most

25%

•A

ims for

gro

ss investm

ent

at

25%

of

GD

P

•A

ims for

carb

on n

eutr

alit

y

by

2050,

main

ly a

chie

ved

thro

ugh c

arb

on p

ricin

g

•In

favor

of

more

fle

xib

ility

in

the w

ork

ing w

eek,

more

support

for

fam

ilies,

and

more

adult r

eskill

ing

PA

RT

IES

Alt

ern

ati

ve

fo

r

Ge

rma

ny (

AfD

)

Far-

rig

ht

Can

did

ate

s:

Alice W

eid

el

an

d T

ino

Ch

rup

alla

Wo

n 1

0%

of

vo

tes a

nd

83

ou

t o

f 735 s

eats

in

th

e

Bu

nd

esta

g

•F

igure

heads a

re m

ostly

form

er

mem

bers

of

the

CD

U;part

y w

as f

orm

ed t

o

oppose p

olic

ies o

f th

e

Euro

zone

•A

nti-E

uro

and a

nti-

mig

ration,

far-

right

nationalis

t

•F

irst

gain

ed s

eats

in t

he

2017 e

lection

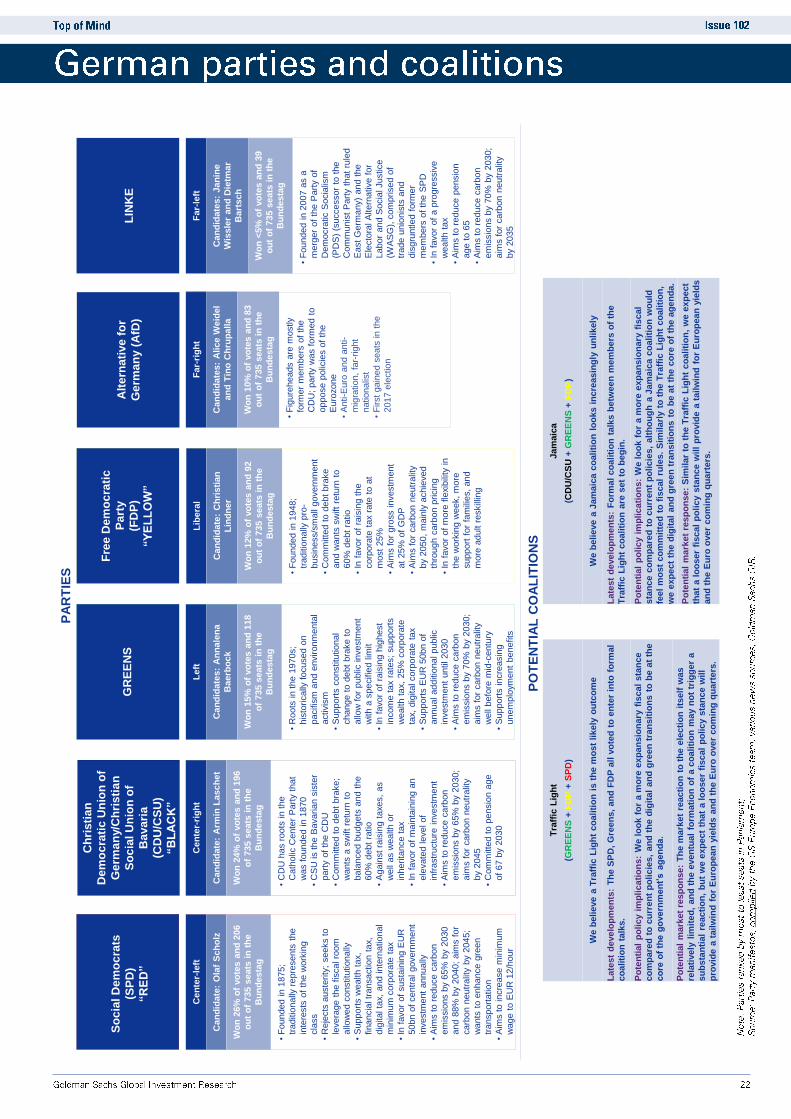

Jam

aic

a

(CD

U/C

SU

+ G

RE

EN

S+

FD

P)

We b

elieve a

Jam

aic

a c

oaliti

on

lo

oks i

ncre

asin

gly

un

likely

Late

st

develo

pm

en

ts:

Fo

rmal

co

aliti

on

talk

s b

etw

een

mem

bers

of

the

Tra

ffic

Lig

ht

co

aliti

on

are

set

to b

eg

in.

Po

ten

tial

po

licy i

mp

licati

on

s:

We l

oo

k f

or

a m

ore

exp

an

sio

nary

fis

cal

sta

nce c

om

pare

d t

o c

urr

en

t p

olicie

s,

alt

ho

ug

h a

Jam

aic

a c

oaliti

on

wo

uld

feel

mo

st

co

mm

itte

d t

o f

iscal

rule

s.

Sim

ilarl

y t

o t

he T

raff

ic L

igh

t co

aliti

on

,

we e

xp

ect

the d

igit

al

an

d g

reen

tra

nsit

ion

s t

o b

e a

t th

e c

ore

of

the a

gen

da.

Po

ten

tial

mark

et

resp

on

se:

Sim

ilar

to t

he T

raff

ic L

igh

t co

aliti

on

, w

e e

xp

ect

that

a l

oo

ser

fiscal

po

licy s

tan

ce w

ill

pro

vid

e a

tailw

ind

fo

r E

uro

pean

yie

lds

an

d t

he E

uro

over

co

min

g q

uart

ers

.

Tra

ffic

Lig

ht

(GR

EE

NS

+ F

DP

+ S

PD

)

We b

elieve a

Tra

ffic

Lig

ht

co

aliti

on

is t

he m

ost

likely

ou

tco

me

Late

st

develo

pm

en

ts:

Th

e S

PD

, G

reen

s,

an

d F

DP

all v

ote

d t

o e

nte

r in

to f

orm

al

co

aliti

on

talk

s.

Po

ten

tial

po

licy i

mp

licati

on

s:

We l

oo

k f

or

a m

ore

exp

an

sio

nary

fis

cal

sta

nce

co

mp

are

d t

o c

urr

en

t p

olicie

s,

an

d t

he d

igit

al

an

d g

reen

tra

nsit

ion

s t

o b

e a

t th

e

co

re o

f th

e g

overn

men

t’s a

gen

da.

Po

ten

tial

mark

et

resp

on

se:

Th

e m

ark

et

reacti

on

to

th

e e

lecti

on

its

elf

was

rela

tively

lim

ited

, an

d t

he e

ven

tual

form

ati

on

of

a c

oaliti

on

may n

ot

trig

ger

a

su

bsta

nti

al

reacti

on

, b

ut

we e

xp

ect

that

a lo

oser

fiscal

po

licy s

tan

ce w

ill

pro

vid

e a

tailw

ind

fo

r E

uro

pean

yie

lds a

nd

th

e E

uro

over

co

min

g q

uart

ers

.

CIT

IZE

NS

ST

AT

E G

OV

ER

NM

EN

TF

ED

ER

AL

GO

VE

RN

ME

NT

LE

GIS

LA

TU

RE

EX

EC

UT

IVE

JU

DIC

IAL

P U B L I C

BU

ND

ES

TA

G

(FE

DE

RA

LD

IET

)

•P

rim

ary

legis

lative b

ody

of

Parlia

ment

•A

t le

ast

598 d

eputies d

irectly

ele

cte

d b

y th

e p

ublic

every

four

years

(half e

lecte

d p

ers

onally

; half

via

vote

s f

or

their p

art

y)

•E

lects

the C

hancello

r; c

an b

e

dis

so

lved b

y th

e F

edera

l P

resid

ent

if t

here

is a

vote

of

no c

onfidence

•M

ost

legis

lation is in

itia

ted in

the

Executive b

ranch,

but

the

Bundesta

g a

ssesses a

nd a

mends

the le

gis

lation a

nd its

support

is

required f

or

the p

assage o

f all

law

s

•M

ost

of

the f

orm

al le

gis

lative w

ork

takes p

lace in

com

mitte

es t

hat

follo

w t

he d

ivis

ion o

f fe

dera

l

min

istr

ies (

i.e.

defe

nse,

labor,

etc

.)

•S

cru

tiniz

es

the a

ctions o

f th

e

Executive b

ranch

BU

ND

ES

RA

T

(FE

DE

RA

L C

OU

NC

IL)

•Legis

lative b

ody

that

repre

sents

the s

ixte

en f

edera

l sta

tes o

f

Germ

any

at

the n

ational le

vel

•T

he 6

9 m

em

bers

are

dele

gate

d b

y

their r

espective s

tate

govern

ments

•T

he p

resid

ency

of

the B

undesra

t

rota

tes a

nnually

am

ong t

he

Min

iste

r P

resid

ents

of

the s

tate

s

•T

he n

um

ber

of

vote

s p

er

sta

te is

based o

n p

opula

tio

n;

each s

tate

is

allo

cate

d a

min

imum

of

thre

e v

ote

s

and a

maxim

um

of

six

; th

e s

tate

must

cast

its v

ote

in

a s

ingle

blo

c

•T

he f

edera

l gov’t is r

equired t

o

subm

it a

ll le

gis

lation t

o t

he

Bundesra

t befo

re t

he B

undesta

g

and B

undesra

t appro

val is

required

when t

he s

tate

has c

oncurr

ent

pow

ers

or

when it

must

adm

inis

ter

federa

l re

gula

tio

ns

•H

as s

om

e v

eto

pow

er

whic

h c

an

be p

ow

erf

ul

if t

he o

ppositio

n

contr

ols

the B

undesra

t

•U

nlik

e the B

undesta

g,

the

Bundesra

t cannot

be d

issolv

ed

CH

AN

CE

LL

OR

•T

he H

ead

of

Govern

ment

and t

he

effective le

ader

of

Germ

any

•S

ele

cts

the F

edera

l C

abin

et

•R

esponsib

le f

or

all

gov’t p

olic

ies;

the C

abin

et

carr

ies o

ut

the

Ch

ancello

r’s v

isio

n

•E

lecte

d b

y th

e m

ajo

rity

in

the

Bundesta

g;

•U

su

ally

als

o t

he c

hair p

ers

on o

f

his

/her

part

y, d

irecting p

art

y

str

ate

gy

•H

as s

ubsta

ntial auth

ority

as h

ead

of

the E

xecutive a

nd le

ader

of

the

part

y th

at

has a

majo

rity

in

the

Bundesta

g;

i.e.

contr

ols

both

the

executive a

nd le

gis

lative b

ranches

CA

BIN

ET

•C

om

prise

d o

f M

inis

ters

that

head

depart

ments

org

aniz

ed b

y key

are

as (

defe

nse,

labor,

etc

.)

•C

hancello

rdete

rmin

es t

he n

um

ber

and id

entity

of

Min

iste

rs

•F

orm

ally

subord

inate

to t

he

Ch

ancello

r in

polic

ymakin

g;

expecte

d t

o c

arr

y out

the v

isio

n o

f

the C

hancello

r

•S

uperv

ise

their d

epart

ment’s p

olic

y

pla

nnin

g,

legis

lative in

itia

tives,

and

adm

inis

tration o

f fe

dera

l la

ws,

in

accord

ance w

ith t

he C

hancello

r’s

polit

ical directives

FE

DE

RA

L P

RE

SID

EN

T

(FR

AN

K-W

AL

TE

R

ST

EIN

ME

IER

)

•A

larg

ely

cere

monia

l post;

gre

ets

vis

itin

gheads o

f sta

te,

attends

offic

ial govt

functions,

etc

.

•F

orm

ally

in

volv

ed in

the p

olit

ical

pro

cess b

y sig

nin

g la

ws a

nd

appoin

tin

g c

abin

et

min

iste

rs b

ased

on C

hancello

r’s r

ecom

mendations.

•S

ele

cte

d e

very

fiv

e y

ears

by

a

Federa

l C

onvention c

om

posed o

f

the B

undesta

g a

nd a

n e

qual

num

ber

of

reps f

rom

the s

tate

s

ST

AT

EG

OV

ER

NM

EN

TS

•S

ixte

en f

edera

l sta

tes o

f G

erm

any

•P

arlia

menta

ry s

yste

m m

odele

d

after

the n

ational govt; s

tate

s h

ave

a u

nic

am

era

l le

gis

latu

re t

hat

is

directly

ele

cte

d b

y popula

r vote

•T

he p

art

y or

coalit

ion t

hat

contr

ols

the le

gis

latu

re s

ele

cts

a M

inis

ter

Pre

sid

ent

to h

ead t

he s

tate

gov’t

•T

he M

inis

ter

Pre

sid

ent

wie

lds

consid

era

ble

in

flu

ence a

t th

e s

tate

and n

ational le

vel and o

ften g

oes

on t

o s

ecure

national positio

ns

•T

he M

inis

ter

Pre

sid

ent

appoin

ts a

cabin

et

to a

dm

inis

ter

sta

te

agencie

s a

nd r

un t

he s

tate

govt

•S

epara

tion o

f pow

ers

assig

ns

gre

ate

r le

gis

lative r

esponsib

ility

at

the f

edera

l le

vel and g

reate

r

adm

inis

trative r

esponsib

ility

at

the

sta

te le

vel, b

ut

there

are

severa

l

are

as w

here

sta

tes h

ave

concurr

ent

pow

er

(i.e

. public

health

and r

efu

gee m

atters

) or

prim

ary

pow

er

(education,

law

enfo

rcem

ent, e

tc.)

CO

NS

TIT

UT

ION

AL

CO

UR

T

•D

ivid

ed into

tw

osenate

s;

each h

as

its o

wn p

anel of

eig

ht

judges,

its

ow

n a

dm

inis

trative s

taff a

nd its

ow

n C

hie

f Justice.

The first

senate

is c

urr

ently

pre

sid

ed o

ver

by

the

Pre

sid

ent

of

the C

ourt

, th

e s

econd

by

the V

ice

Pre

sid

ent

•T

he f

irst

senate

prim

arily

deals

with

fundam

enta

l rig

hts

, w

hile

the

second s

enate

is p

rim

arily

a c

ourt

for

sta

te m

atters

•M

em

bers

sele

cte

d in

equal

num

bers

by

the B

undesta

g a

nd t

he

Bundesra

t

•Justices c

an b

e r

em

oved f

rom

offic

e o

nly

for

abuse o

f th

eir

positio

n

Ele

cts

Appoin

ts

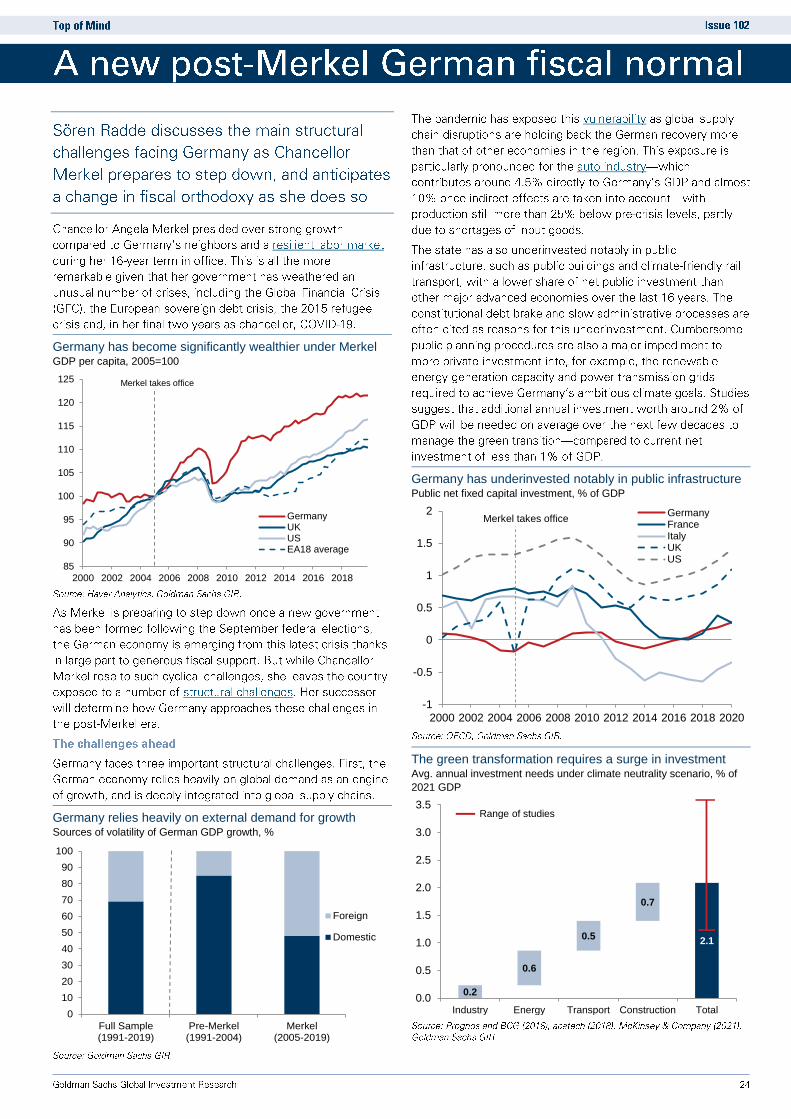

Germany has become significantly wealthier under Merkel GDP per capita, 2005=100

Germany relies heavily on external demand for growth Sources of volatility of German GDP growth, %

Germany has underinvested notably in public infrastructure Public net fixed capital investment, % of GDP

The green transformation requires a surge in investment Avg. annual investment needs under climate neutrality scenario, % of

2021 GDP

85

90

95

100

105

110

115

120

125

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

GermanyUKUSEA18 average

Merkel takes office

0

10

20

30

40

50

60

70

80

90

100

Full Sample(1991-2019)

Pre-Merkel(1991-2004)

Merkel(2005-2019)

Foreign

Domestic

-1

-0.5

0

0.5

1

1.5

2

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

GermanyFranceItalyUKUS

Merkel takes office

0.2

0.6

0.5

0.7

2.1

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Industry Energy Transport Construction Total

Range of studies

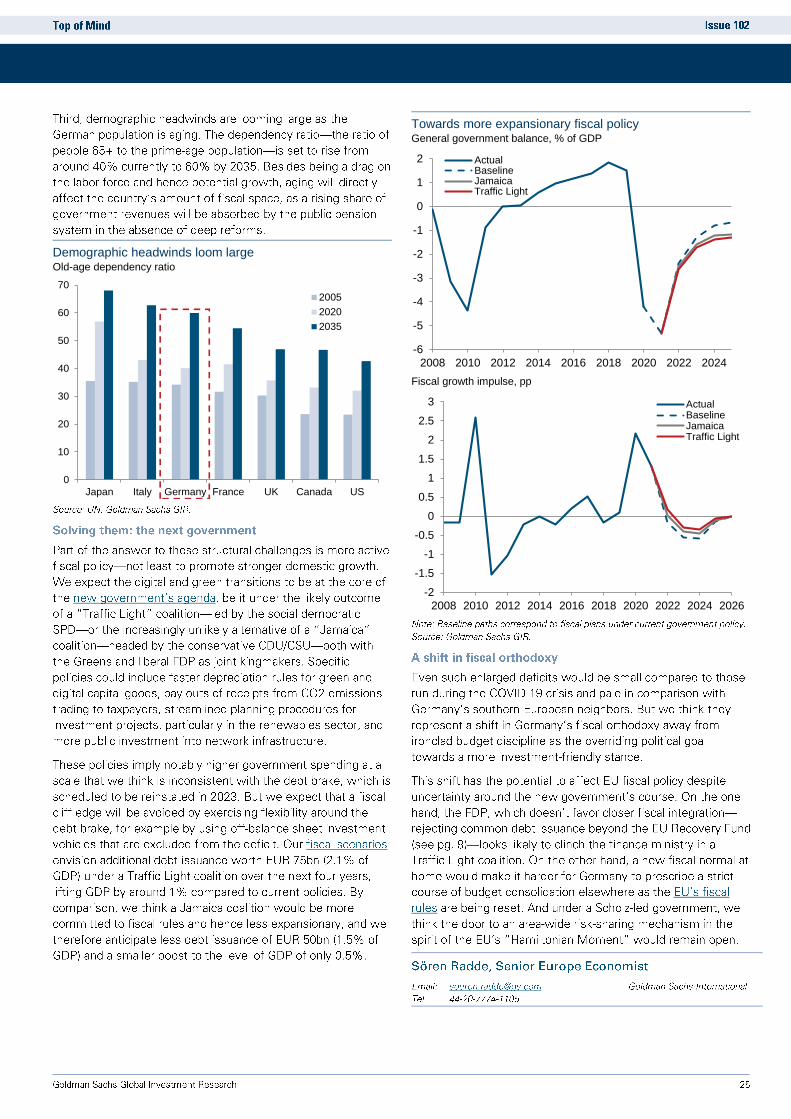

Demographic headwinds loom large Old-age dependency ratio

Towards more expansionary fiscal policy General government balance, % of GDP

Fiscal growth impulse, pp

0

10

20

30

40

50

60

70

Japan Italy Germany France UK Canada US

2005

2020

2035

-6

-5

-4

-3

-2

-1

0

1

2

2008 2010 2012 2014 2016 2018 2020 2022 2024

ActualBaselineJamaicaTraffic Light

-2

-1.5

-1

-0.5

0

0.5

1

1.5

2

2.5

3

2008 2010 2012 2014 2016 2018 2020 2022 2024 2026

ActualBaselineJamaicaTraffic Light

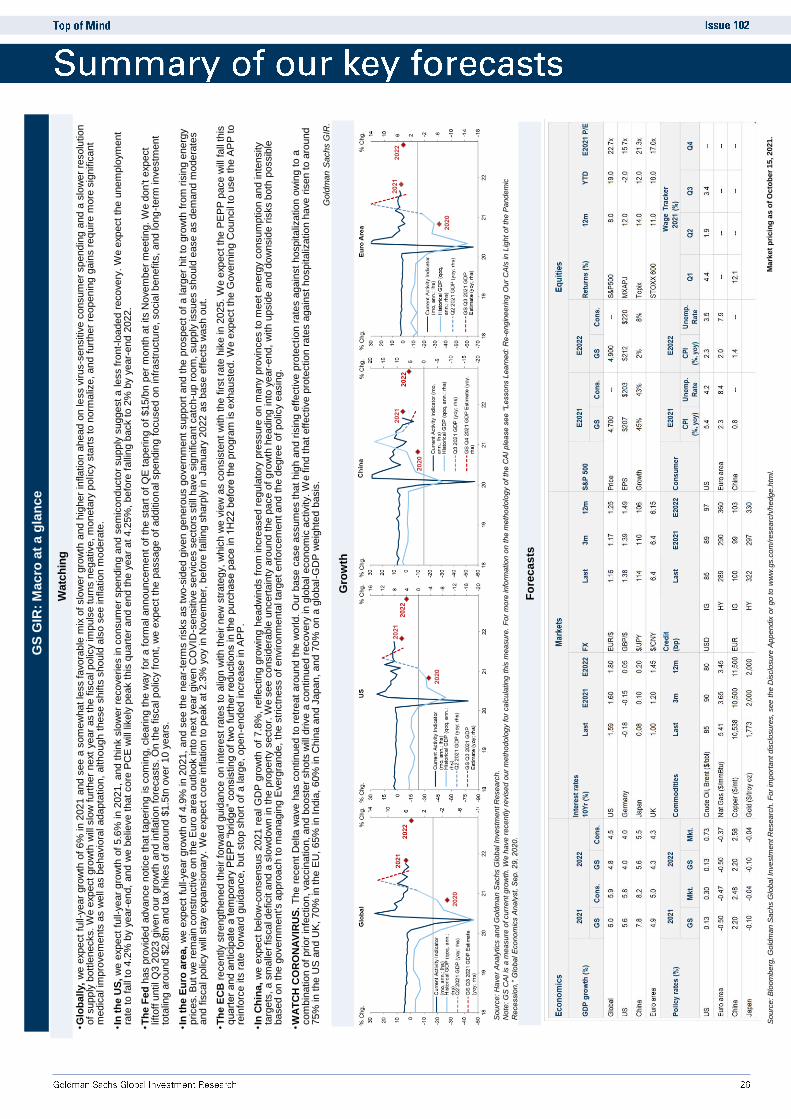

GS

GIR

: M

acro

at

a g

lan

ce

Watc

hin

g

•Glo

ba

lly,

we e

xpect

full-

year

gro

wth

of

6%

in

2021 a

nd s

ee a

som

ew

hat

less favora

ble

mix

of

slo

wer

gro

wth

and h

igher

infla

tio

n a

head o

n le

ss v

irus-s

ensitiv

e c

onsum

er

spendin

g a

nd a

slo

wer

resolu

tio

n

of

supply

bott

lenecks.

We e

xpect

gro

wth

will

slo

w f

urt

her

next

year

as the f

iscal polic

y im

puls

e turn

s n

egative,

moneta

ry p

olicy

sta

rts to n

orm

aliz

e, and f

urt

her

reopenin

g g

ain

s r

equire m

ore

sig

nific

ant

medic

al im

pro

vem

ents

as w

ell

as b

ehavio

ral adapta

tio

n,

although t

hese s

hifts

should

als

o s

ee in

fla

tio

n m

odera

te.

•In

th

e U

S,

we e

xpect

full-

year

gro

wth

of

5.6

% in

2021,

and t

hin

k s

low

er

recoverie

s in

consum

er

spendin

g a

nd s

em

iconducto

r supply

suggest

a l

ess fro

nt-

loaded r

ecovery

. W

e e

xpect

the u

nem

plo

ym

ent

rate

to f

all

to 4

.2%

by y

ear-

end,

and w

e b

elie

ve t

hat

core

PC

E w

ill lik

ely

peak t

his

quart

er

and e

nd t

he y

ear

at

4.2

5%

, befo

re f

alli

ng b

ack t

o 2

% b

y y

ear-

end 2

022.

•Th

e F

ed

has p

rovid

ed a

dvance n

otice t

hat

taperin

g is c

om

ing, cle

arin

g t

he w

ay f

or

a f

orm

al announcem

ent

of

the s

tart

of

QE

taperin

g o

f $15/b

n p

er

month

at

its N

ovem

ber

meetin

g. W

e d

on't e

xpect

lifto

ff u

ntil Q

3 2

023 g

iven o

ur

gro

wth

and in

fla

tio

n f

ore

casts

. O

n t

he f

iscal polic

y f

ront,

we e

xpect

the p

assage o

f additio

nal spendin

g f

ocused o

n in

frastr

uctu

re, socia

l benefits

, and lo

ng

-term

in

vestm

ent

tota

ling a

round $

2.8

tn a

nd t

ax h

ikes o

f aro

und $

1.5

tn o

ver

10 y

ears

.

•In

th

e E

uro

are

a,

we e

xpect

full-

year

gro

wth

of

4.9

% in

2021,

and s

ee t

he n

ear-

term

s r

isks a

s tw

o-s

ided g

iven g

enero

us g

overn

ment

support

and t

he p

rospect

of

a la

rger

hit to g

row

th f

rom

ris

ing e

nerg

y

prices. B

ut w

e r

em

ain

constr

uctive o

n t

he E

uro

are

a o

utlo

ok in

to n

ext

year

giv

en C

OV

ID-s

ensitiv

e s

erv

ices s

ecto

rs s

till

have s

ignific

ant catc

h-u

p r

oom

, supply

issues s

hould

ease a

s d

em

and m

odera

tes

and f

iscal polic

y w

ill s

tay e

xpansio

nary

. W

e e

xpect

core

in

fla

tio

n t

o p

eak a

t 2.3

% y

oy in

Novem

ber,

befo

re f

alli

ng s

harp

ly in

January

2022 a

s b

ase e

ffects

wash o

ut.

•Th

e E

CB

recently s

trength

ened t

heir f

orw

ard

guid

ance o

n in

tere

st ra

tes t

o a

lign w

ith t

heir n

ew

str

ate

gy,

whic

h w

e v

iew

as c

onsis

tent

with t

he f

irst ra

te h

ike in

2025.

We e

xpect

the P

EP

P p

ace w

ill f

all

this

quart

er

and a

nticip

ate

a t

em

pora

ry P

EP

P “

bridge”

consis

ting o

f tw

o f

urt

her

reductions in t

he p

urc

hase p

ace in 1

H22 b

efo

re t

he

pro

gra

m is e

xhauste

d.

We e

xpect

the G

overn

ing C

ouncil

to u

se t

he A

PP

to

rein

forc

e its

rate

forw

ard

guid

ance,

but

sto

p s

hort

of

a la

rge,

open

-ended i

ncre

ase in

AP

P.

•In

Ch

ina

, w

e e

xpect

belo

w-c

onsensus 2

021 r

eal G

DP

gro

wth

of

7.8

%, re

fle

ctin

g g

row

ing h

eadw

inds f

rom

in

cre

ased r

egula

tory

pre

ssure

on m

any p

rovin

ces t

o m

eet energ

y c

onsum

ptio

n a

nd in

tensity

targ

ets

, a s

malle

r fiscal deficit a

nd a

slo

wdow

n in

the p

ropert

y s

ecto

r. W

e s

ee c

onsid

era

ble

uncert

ain

ty a

round t

he p

ace o

f g

row

th h

eadin

g in

to y

ear-

end,

with u

psid

e a

nd d

ow

nsid

e r

isks b

oth

possib

le

based o

n t

he g

overn

ment's a

ppro

ach t

o m

anagin

g E

verg

rande,

the s

tric

tness o

f environm

enta

l ta

rget

enfo

rcem

ent and t

he d

egre

e o

f polic

y e

asin

g.

•WA

TC

H C

OR

ON

AV

IRU

S.

Th

e r

ecent

Delta w

ave h

as c

ontin

ued t

o r

etr

eat

aro

und t

he w

orld

. O

ur

base c

ase a

ssum

es that

hig

h a

nd r

isin

g e

ffective p

rote

cti

on

rate

s a

gain

st

hospitaliz

atio

n o

win

g t

o a

com

bin

atio

n o

f prio

r in

fectio

n,

vaccin

atio

n,

and b

ooste

r shots

will

drive a

contin

ued r

ecovery

in

glo

bal econom

ic a

ctivity. W

e fin

d t

hat

eff

ective p

rote

ctio

n r

ate

s a

gain

st

hospitaliz

atio

n h

ave r

isen to a

round

75%

in

the U

S a

nd U

K, 70%

in

the E

U, 65%

in

India

, 60%

in

Chin

a a

nd J

apan,

and 7

0%

on a

glo

bal-

GD

P w

eig

hte

d b

asis

.

Gold

man S

achs G

IR.

Gro

wth

So

urc

e: H

ave

r A

na

lytics a

nd

Go

ldm

an

Sa

ch

s G

lob

al In

ve

stm

en

t R

ese

arc

h.

Note

: G

S C

AI

is a

me

asu

re o

f cu

rre

nt g

row

th. W

e h

ave

re

ce

ntly r

evis

ed

ou

r m

eth

od

olo

gy f

or

ca

lcula

tin

g t

his

me

asu

re.

Fo

r m

ore

info

rma

tio

n o

n t

he

me

tho

do

log

y o

f th

e C

AI

ple

ase

se

e “

Le

sso

ns L

ea

rne

d: R

e-e

ng

ine

erin

g O

ur

CA

Is in

Lig

ht

of

the

Pa

nd

em

ic

Rece

ssio

n,”

Glo

ba

l E

co

no

mic

s A

na

lyst, S

ep

. 2

9,

20

20

.

Fo

rec

as

ts

So

urc

e: B

loo

mb

erg

, G

old

ma

n S

ach

s G

lob

al In

ve

stm

en

t R

ese

arc

h.

Fo

r im

po

rta

nt

dis

clo

su

res,

se

e t

he

Dis

clo

su

re A

pp

en

dix

or

go

to

ww

w.g

s.c

om

/re

se

arc

h/h

ed

ge

.htm

l.M

ark

et

pri

cin

g a

s o

f O

cto

be

r 1

5,

20

21

.

Disclosure Appendix