guiding principles on stress testing for …. compilation.pdf · hong leong islamic bank hlib...

TRANSCRIPT

GUIDING PRINCIPLES ON STRESS TESTING FOR INSTITUTIONS OFFERING ISLAMIC FINANCIAL SERVICES [OTHER THAN ISLAMIC INSURANCE (TAKĀFUL) INSTITUTIONS

AND ISLAMIC COLLECTIVE INVESTMENT SCHEMES]

PUBLIC COMMENTS RECEIVED IN RESPECT OF EXPOSURE DRAFT ON ED-13

Feb 03, 2012 [V.3]

7th Meeting of Stress Testing Working Group (STWG) 31st January 2012

Kuala Lumpur, Malaysia

Confidential. This document must not be, in whole or in part, reproduced or used for any other purpose, or shown, given, copied to or filed with any other person other than a member of the STWG and/or Technical Committee without the written consent from the IFSB.

2

TABLE OF CONTENTS

PARTIES FROM WHOM WRITTEN RESPONSES WERE RECEIVED ........................................ 3

LIST OF COMMENTS..................................................................................................................... 6

GENERAL COMMENTS (WITHOUT SPECIFYING ANY PARAGRAPHS)................................. 6 SECTION 1: INTRODUCTION AND BACKGROUND ............................................................... 32 SECTION 2: NECESSARY CONDITIONS FOR AN EFFECTIVE STRESS TESTING REGIME................................................................................................................................................... 42 SECTION 3: GUIDING PRINCIPLES ON STRESS TESTING FOR IIFS .................................. 46 SECTION 4: GUIDING PRINCIPLES ON STRESS TESTING FOR SUPERVISORY AUTHORITIES......................................................................................................................... 126 DEFINITIONS.......................................................................................................................... 138

Some words of encouragement ……. “The Guiding Principles that have been laid out for national regulators are crucial for monitoring of the safety and soundness of the individual IIFS as well as identifying the weakness in the financial system. The PIDM commends IFSB’s effort and fully support its role in promoting soundness and stability of IIFS”.

Perbadanan Insurans Deposit Malaysia (PIDM) ... “We welcome the efforts of the IFSB to create a level playing field for Islamic business”.

Saudi Arabian Monetary Agency ..“We appreciate your efforts in developing and enhancing the Islamic financial services”

Central Bank of Jordan

…. “The Guiding Principles appear very useful for conducting appropriate stress tests in view of fostering market confidence with regards to the soundness and stability of IIFS and the Islamic financial services industry as a whole”.

Banque Centrale Du Luxembourg ….“Overall, we consider the Exposure Draft (ED) to be of a high quality, comprehensive and with clear guiding principles for IFIs”.

Islamic Development Bank …. “The Guiding Principles contain high level governance principles for stress testing, with which we are in agreement and feel that they will create the market discipline needed for these functions to be effective”…

Arcapita Bank, Bahrain …..“The IFSB has done an excellent work in developing a very comprehensive Guiding Principles on Stress Testing taking into considerations the additional areas that are only peculiar to Islamic [finance] such as Shari’ah non-compliance and the various underlying Islamic contracts used in the industry”…

OCBC Al-Amin, Malaysia

3

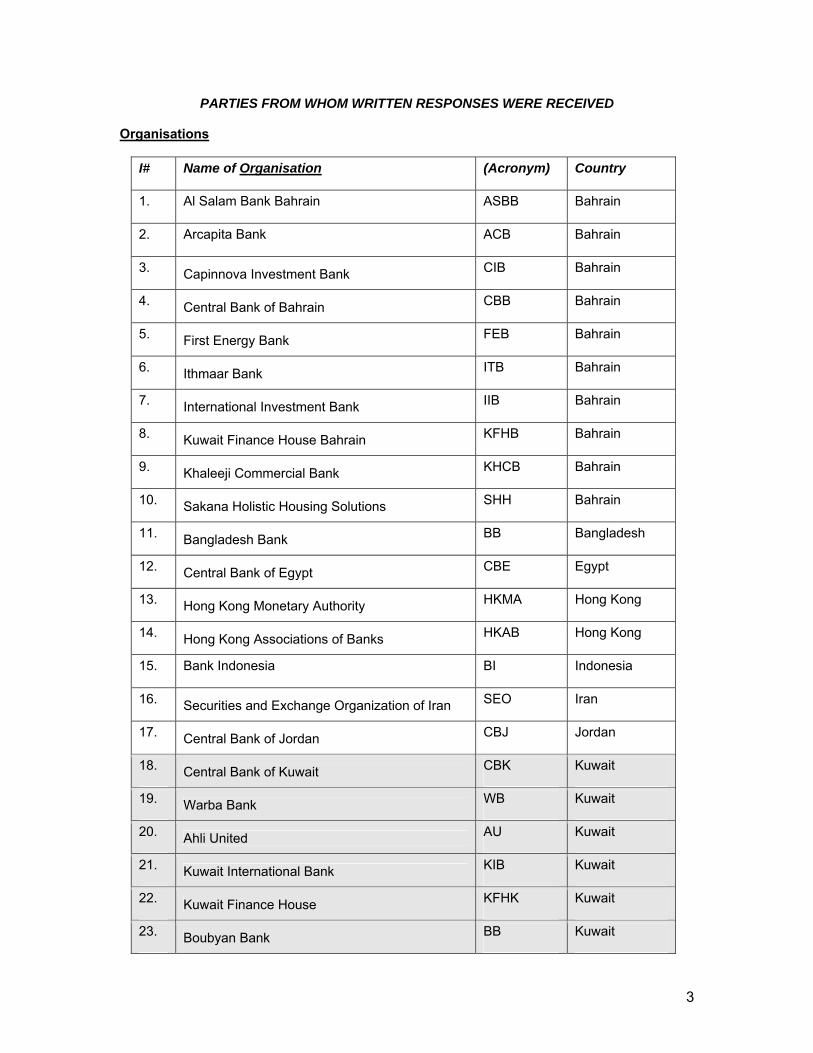

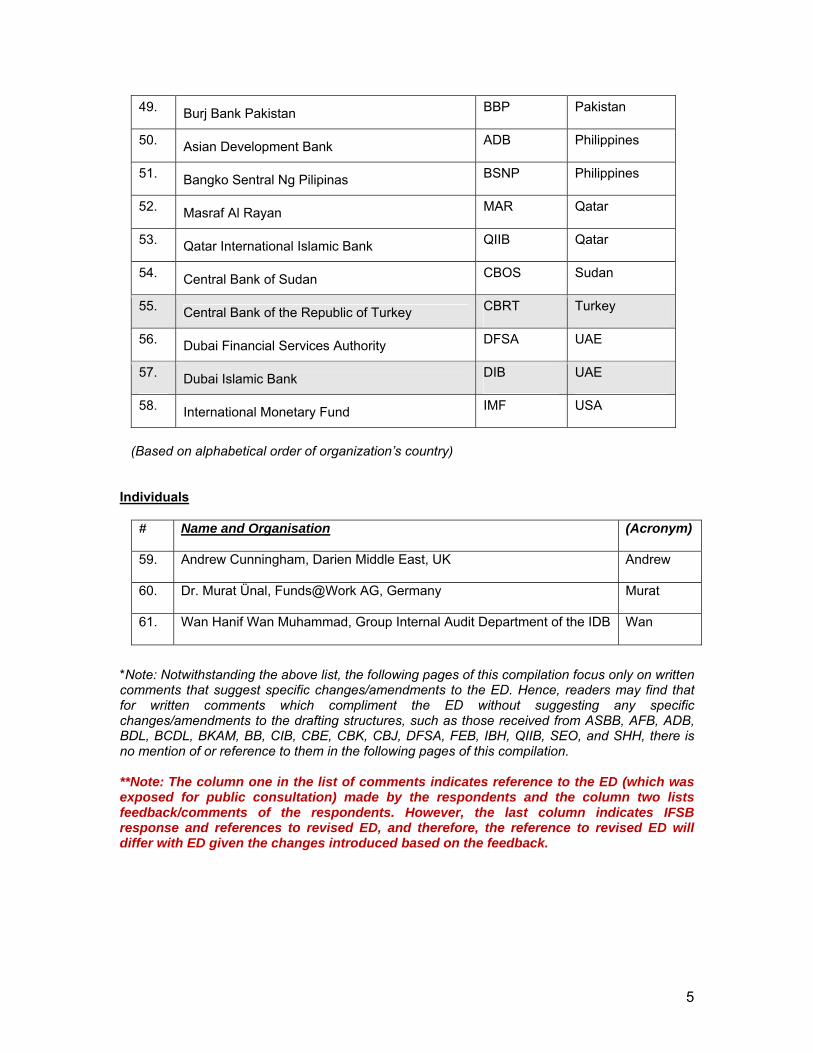

PARTIES FROM WHOM WRITTEN RESPONSES WERE RECEIVED Organisations

I# Name of Organisation (Acronym) Country

1. Al Salam Bank Bahrain ASBB Bahrain

2. Arcapita Bank ACB Bahrain

3. Capinnova Investment Bank CIB Bahrain

4. Central Bank of Bahrain CBB Bahrain

5. First Energy Bank FEB Bahrain

6. Ithmaar Bank ITB Bahrain

7. International Investment Bank IIB Bahrain

8. Kuwait Finance House Bahrain KFHB Bahrain

9. Khaleeji Commercial Bank KHCB Bahrain

10. Sakana Holistic Housing Solutions SHH Bahrain

11. Bangladesh Bank BB Bangladesh

12. Central Bank of Egypt CBE Egypt

13. Hong Kong Monetary Authority HKMA Hong Kong

14. Hong Kong Associations of Banks HKAB Hong Kong

15. Bank Indonesia BI Indonesia

16. Securities and Exchange Organization of Iran SEO Iran

17. Central Bank of Jordan CBJ Jordan

18. Central Bank of Kuwait CBK Kuwait

19. Warba Bank WB Kuwait

20. Ahli United AU Kuwait

21. Kuwait International Bank KIB Kuwait

22. Kuwait Finance House KFHK Kuwait

23. Boubyan Bank BB Kuwait

4

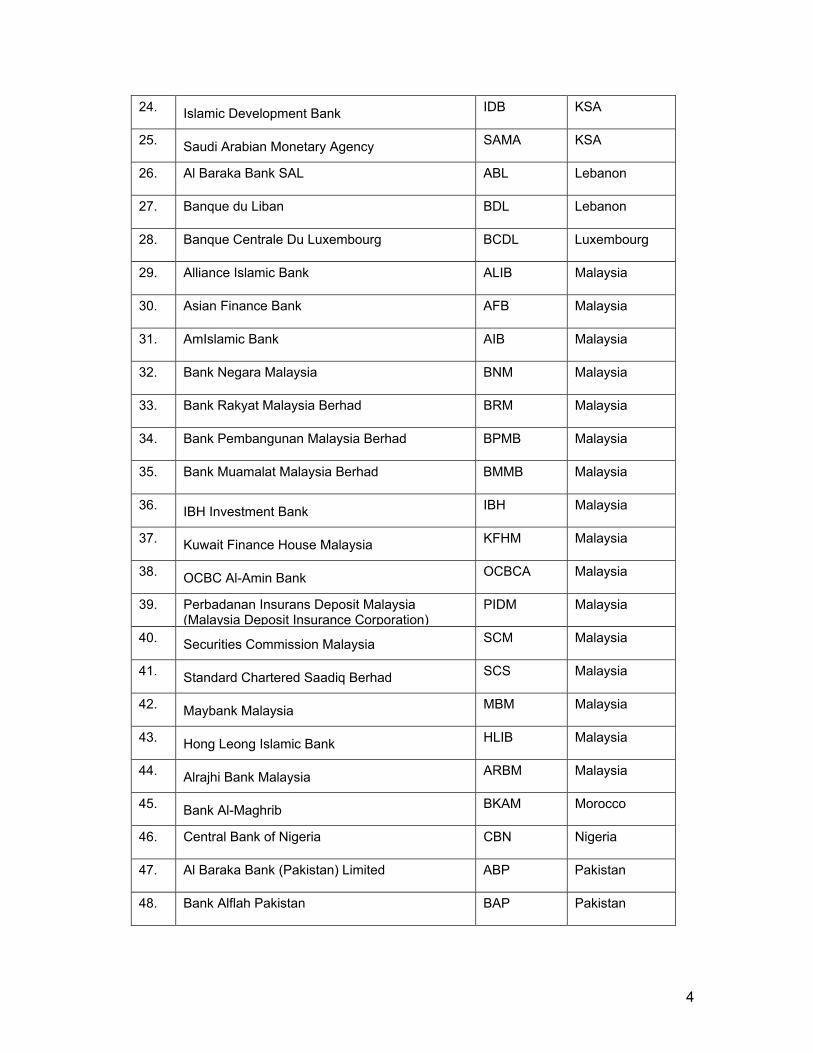

24. Islamic Development Bank IDB KSA

25. Saudi Arabian Monetary Agency SAMA KSA

26. Al Baraka Bank SAL ABL Lebanon

27. Banque du Liban BDL Lebanon

28. Banque Centrale Du Luxembourg BCDL Luxembourg

29. Alliance Islamic Bank ALIB Malaysia

30. Asian Finance Bank AFB Malaysia

31. AmIslamic Bank AIB Malaysia

32. Bank Negara Malaysia BNM Malaysia

33. Bank Rakyat Malaysia Berhad BRM Malaysia

34. Bank Pembangunan Malaysia Berhad BPMB Malaysia

35. Bank Muamalat Malaysia Berhad BMMB Malaysia

36. IBH Investment Bank IBH Malaysia

37. Kuwait Finance House Malaysia KFHM Malaysia

38. OCBC Al-Amin Bank OCBCA Malaysia

39. Perbadanan Insurans Deposit Malaysia (Malaysia Deposit Insurance Corporation)

PIDM Malaysia

40. Securities Commission Malaysia SCM Malaysia

41. Standard Chartered Saadiq Berhad SCS Malaysia

42. Maybank Malaysia MBM Malaysia

43. Hong Leong Islamic Bank HLIB Malaysia

44. Alrajhi Bank Malaysia ARBM Malaysia

45. Bank Al-Maghrib BKAM Morocco

46. Central Bank of Nigeria CBN Nigeria

47. Al Baraka Bank (Pakistan) Limited ABP Pakistan

48. Bank Alflah Pakistan BAP Pakistan

5

49. Burj Bank Pakistan BBP Pakistan

50. Asian Development Bank ADB Philippines

51. Bangko Sentral Ng Pilipinas BSNP Philippines

52. Masraf Al Rayan MAR Qatar

53. Qatar International Islamic Bank QIIB Qatar

54. Central Bank of Sudan CBOS Sudan

55. Central Bank of the Republic of Turkey CBRT Turkey

56. Dubai Financial Services Authority DFSA UAE

57. Dubai Islamic Bank DIB UAE

58. International Monetary Fund IMF USA

(Based on alphabetical order of organization’s country)

Individuals

# Name and Organisation (Acronym)

59. Andrew Cunningham, Darien Middle East, UK Andrew

60. Dr. Murat Ünal, Funds@Work AG, Germany Murat

61. Wan Hanif Wan Muhammad, Group Internal Audit Department of the IDB Wan

*Note: Notwithstanding the above list, the following pages of this compilation focus only on written comments that suggest specific changes/amendments to the ED. Hence, readers may find that for written comments which compliment the ED without suggesting any specific changes/amendments to the drafting structures, such as those received from ASBB, AFB, ADB, BDL, BCDL, BKAM, BB, CIB, CBE, CBK, CBJ, DFSA, FEB, IBH, QIIB, SEO, and SHH, there is no mention of or reference to them in the following pages of this compilation. **Note: The column one in the list of comments indicates reference to the ED (which was exposed for public consultation) made by the respondents and the column two lists feedback/comments of the respondents. However, the last column indicates IFSB response and references to revised ED, and therefore, the reference to revised ED will differ with ED given the changes introduced based on the feedback.

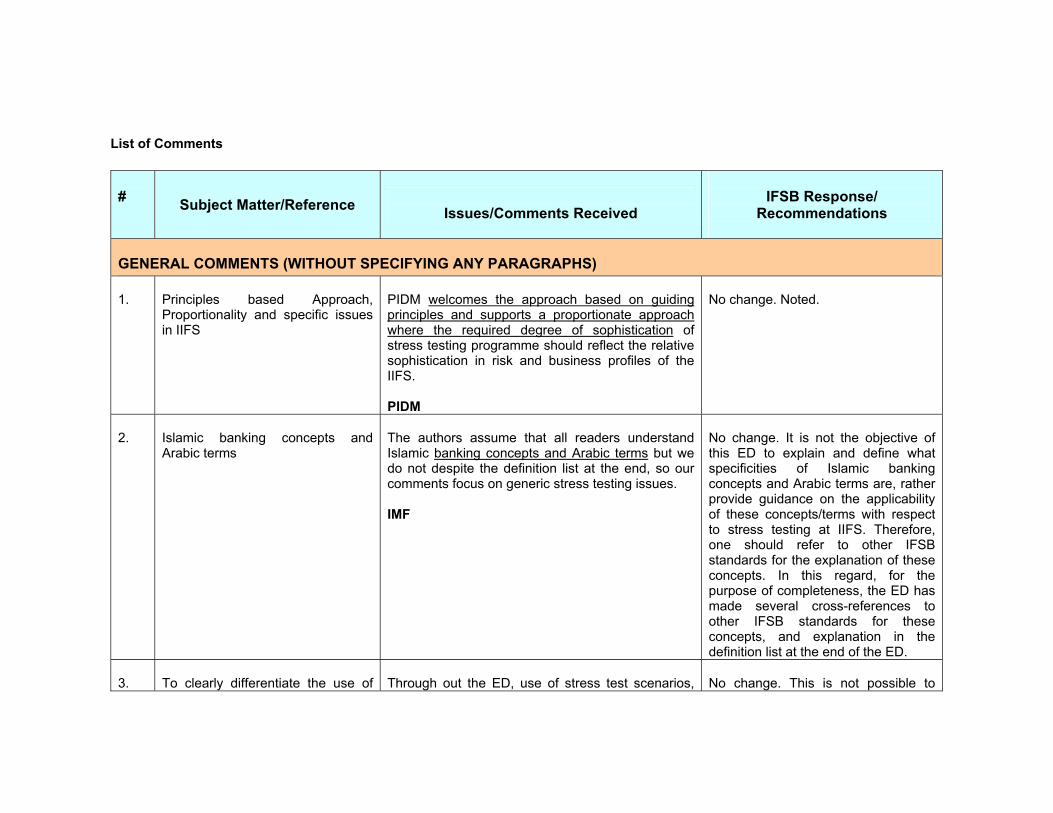

List of Comments

# Subject Matter/Reference

Issues/Comments Received

IFSB Response/

Recommendations

GENERAL COMMENTS (WITHOUT SPECIFYING ANY PARAGRAPHS) 1.

Principles based Approach, Proportionality and specific issues in IIFS

PIDM welcomes the approach based on guiding principles and supports a proportionate approach where the required degree of sophistication of stress testing programme should reflect the relative sophistication in risk and business profiles of the IIFS. PIDM

No change. Noted.

2.

Islamic banking concepts and Arabic terms

The authors assume that all readers understand Islamic banking concepts and Arabic terms but we do not despite the definition list at the end, so our comments focus on generic stress testing issues. IMF

No change. It is not the objective of this ED to explain and define what specificities of Islamic banking concepts and Arabic terms are, rather provide guidance on the applicability of these concepts/terms with respect to stress testing at IIFS. Therefore, one should refer to other IFSB standards for the explanation of these concepts. In this regard, for the purpose of completeness, the ED has made several cross-references to other IFSB standards for these concepts, and explanation in the definition list at the end of the ED.

3.

To clearly differentiate the use of

Through out the ED, use of stress test scenarios,

No change. This is not possible to

7

the terminology scenarios, risk drivers and process

risk drivers and process (i.e., things to look out for) have been jumbled up without clarity of the context. Suggest defining these terminologies including its use in respective stage in the stress testing process. BNM

explain each terminology in the ED as these terminologies are well understood by IIFS and supervisory authorities as shown in the Survey. Further, the systematic flow of Guiding Principles has provided greater clarity to the IIFS and others. For instance, the ED does not move to discuss scenarios before discussing the risk factors and risk drivers. Whereas process refers to whole stress testing programme with respect to each component, which is well understandable.

4.

Time horizon for stress test

Suggest including a requirement or clarification on the time horizon a stress testing should be conducted. The stress testing time horizon should consider the type of risk and the purpose of the stress testing. BNM

No change. This has already been addressed under Principle 3.20 (i.e. frequency of stress testing). The opening paragraph makes it very clear that in order for stress testing to be a meaningful part of the risk management framework, stress tests should be undertaken with appropriate frequency in the light of the nature of the risks to which the IIFS are exposed and the types of tests performed.

5.

Frequency of stress testing

Although the guiding principles are there for use of multiple stressing scenarios, however, the frequency of simultaneous multiple stress scenarios may be set different from the regular stress testing for example it may be set to be annual instead of bi-annual or quarterly. ABP

No change. This issue has already been addressed under Principle 3.20 (i.e. frequency of stress testing). See also above.

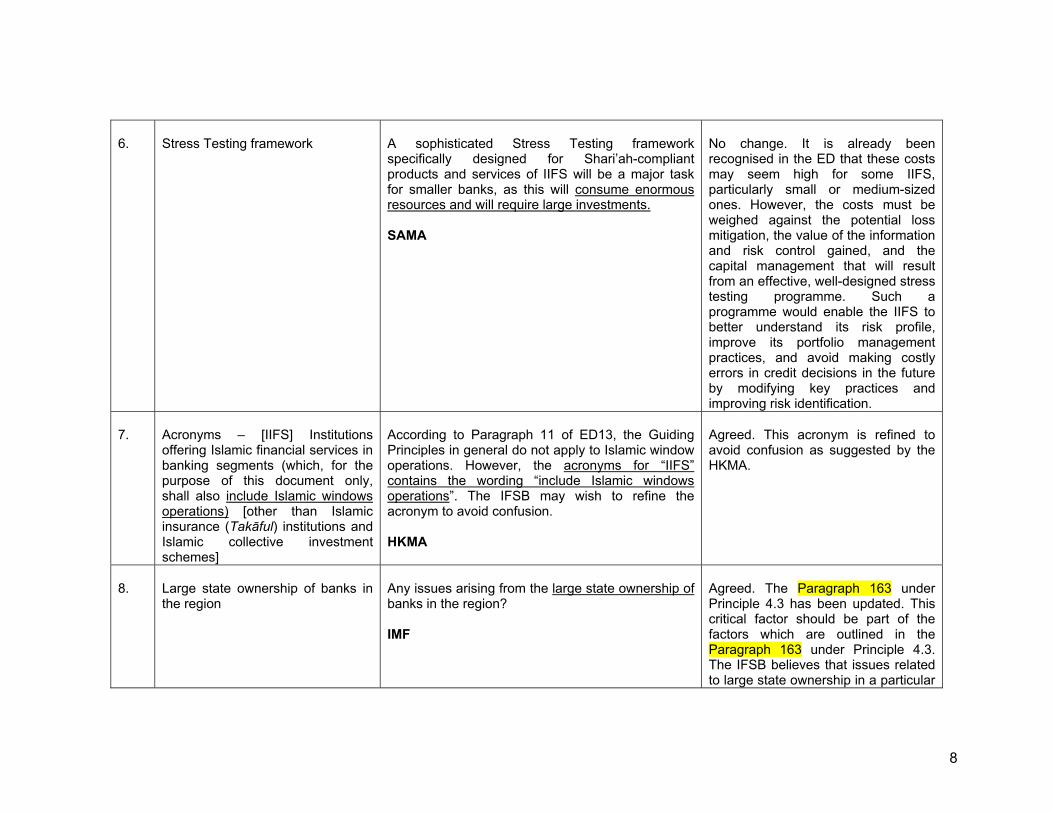

8

6.

Stress Testing framework

A sophisticated Stress Testing framework specifically designed for Shari’ah-compliant products and services of IIFS will be a major task for smaller banks, as this will consume enormous resources and will require large investments. SAMA

No change. It is already been recognised in the ED that these costs may seem high for some IIFS, particularly small or medium-sized ones. However, the costs must be weighed against the potential loss mitigation, the value of the information and risk control gained, and the capital management that will result from an effective, well-designed stress testing programme. Such a programme would enable the IIFS to better understand its risk profile, improve its portfolio management practices, and avoid making costly errors in credit decisions in the future by modifying key practices and improving risk identification.

7.

Acronyms – [IIFS] Institutions offering Islamic financial services in banking segments (which, for the purpose of this document only, shall also include Islamic windows operations) [other than Islamic insurance (Takāful) institutions and Islamic collective investment schemes]

According to Paragraph 11 of ED13, the Guiding Principles in general do not apply to Islamic window operations. However, the acronyms for “IIFS” contains the wording “include Islamic windows operations”. The IFSB may wish to refine the acronym to avoid confusion. HKMA

Agreed. This acronym is refined to avoid confusion as suggested by the HKMA.

8.

Large state ownership of banks in the region

Any issues arising from the large state ownership of banks in the region? IMF

Agreed. The Paragraph 163 under Principle 4.3 has been updated. This critical factor should be part of the factors which are outlined in the Paragraph 163 under Principle 4.3. The IFSB believes that issues related to large state ownership in a particular

9

region are important on the functionality of stress testing exercise across the system; however, the IFSB also understands that this will be tackled at respective supervisory authority level.

9.

How to consider/embed correlations? What are scenarios?

We believe that IIFS would be more interested in knowing the followings along with examples: • More specifically defined/recommended stress

scenarios, their severity and other possible specific assumptions;

• how to aggregate the effects of specific and market wide, Micro- and Macro- stress events on IIFS corporate level;

• How to consider/embed correlations among risk factors when performing scenario analysis;

• Any recommended sources for past data/figures, correlations.

IDB

No change. It is outside the scope of this ED and the IFSB to define or recommend any particular stress scenario and how to consider correlations among risk factors, and recommend sources of data for any IIFS. This should be done within IIFS and management of the IIFS should address these concerns and specifically data limitation (see also Section 2.2). In regard, how to apply the Guiding Principles contained in the ED, this is one of the issues which the IFSB may consider addressing in detail through “implementation guidance” that can cover illustrations on how to perform stress testing through different approaches.

10.

Practicability of the document

I am a little concerned that the document may be too detailed for some supervisors, or even banks, to digest. For example, the guidance on ICAAP provided to banks by the U.K.’s Financial Services Authority (“ICAAP Submission – suggested formal”) runs to only eight pages. Publishing documents which are authoritative should of course be a central feature of the IFSB’s work, but I wonder whether some thought could be given to facilitating

No change. Noted. This is one of the issues which the IFSB may consider addressing in detail through “implementation guidance” that will cover operationalisation of the Principles, check lists, and illustrations of how to perform stress testing through different approaches and their impacts.

10

the implementation of such documents, both by supervisors and banks. For example, a stress testing checklist – of one or two pages – may give both supervisors and banks an easy entry point into what is necessarily a complex and detailed exercise. Such an initiative would also enable to IFSB to use its position as a supra-national body to standardize basic approaches to stress testing across the Shair’ah-compliant landscape. Andrew

11.

Provide IIFS with a detailed framework covering all the guiding principles

We recommend IFSB to provide IIFS with a detailed framework covering all the guiding principles highlighted in subject document which would enable IIFS to comply with the implementation date of January 2013. The absence of such detailed framework may lead to inappropriate application of these guiding principles across the IIFS levels. AU

No change. The ED is already detailed and comprehensive, and detailed and specific framework is expected to be provided to the IIFS by respective supervisory authority. With respect to implementation guidance, please see response in (9) and (10) above respectively.

12.

Methodology to conduct its stress testing

Islamic Banks in Kuwait has been undertaking stress testing based on the Instruction (No. 2/RBS/44/2009) from the Central Bank of Kuwait in this regard. Based on the same, KIB while preparing its methodology to conduct its stress testing had adhered to the CBK requirement in this regard as well as used the best practice principles on stress testing as prescribed by the BIS. KIB

No change. Noted.

13.

Stress testing Guiding Principles are very comprehensive and the related expectations are over …..country-specific interpretations

As a general comment, the proposed guiding principles on stress testing are very comprehensive and the related expectations are over and above those placed on non-Islamic banking institutions.

No change. Providing an execution tool to allow for consistent, practical implementation across the industry/country is not the main intent

11

These comprehensive principles could be accompanied by an execution tool to allow for consistent, practical implementation across the industry/country. In the Malaysian context, the Islamic banking industry may, in general, face challenges in meeting all the recommendations as most of the institutions are leveraging on expertise from their parent, non-Islamic banking institution and inconsistent expectations may be difficult to execute. Additionally, having different stress testing practices would result in complications when consolidating the results to obtain a “bank-wide” view. There may also be country-specific interpretations that need to be aligned first, prior to rolling-out a comprehensive industry-wide stress testing policy. By way of example, the Malaysian Islamic banking industry treats Mudarabah funding as liability, whereas the proposed guiding principles interprets it as investment accounts. SCS

of the Guiding Principles rather that is left to the IIFS and in order to enhance the consistent and practical implementation, the role of supervisory authorities is significant. It is expected that respective supervisory authorities will ensure that the implementation of the Guiding Principles has taken into account the local context (i.e. country-specific legal, regulatory considerations) and concept of proportionality as also discussed in the document. In addition, this is a matter of the value of alpha, which is addressed separately in IFSB GN-4.

14.

Several MIS reports covering stress Testing

The system/Modules selected by Islamic Institutions should carry the similar dimensions to bring in uniformity and clarity in Operations. Under the present scenario at Bank Alfalah we produce several MIS reports covering stress Testing and Liquidity on daily, weekly, Monthly, Quarterly basis for Senior Managements including RMD’s review and any change is highlighted and brought to their notice to seek advice. BAP

No change. Noted.

12

15.

Factors that may be put before the implementation of these principles.

Further, the application of these guidelines is dependent on the following factors that may be put before the implementation of these principles.

1- Close coordination between regulators, IIFS and IFSB to come up with a strategy in implementing these guidelines in stages i.e. simple, intermediate and advance approaches.

a. This will help in understanding the issues

faces by IIFS in gathering the data b. This will help regulators in better controls on

IIFS c. This will help IFSB in preparing a standard

guideline across the globe

2- IIFS would need much stronger IT support than they have i.e.

a. More robust software and hardware support would be need at the time of implementation.

b. If a standard off the shelf software is prepared for these risk management tool that would help the industry in going forward in same and right direction

3- Most importantly training and development of

the staff related in the exercise would be required.

a. Training of the techniques/tools applied should be given to the risk related personnel while

b. Software related training should be given to the IT.

c. With this, a sample document should be prepared to teach the staff involved in the exercise.

No change. Suggested factors are already being discussed in the ED and the list of critical factors is presented in Section 2.

13

BBP

16.

Specificities of IIFS such as direct equity investment risk and rate of return risk

The STWG should also highlight other risk specificities of IIFS such as direct equity investment risk and rate of return risk. Both were defined and described in detail in the IFSB-1. Both are important to the IDBG, especially the direct equity investment risk.

Wan

No change. These specificities are addressed already by the STWG in the ED. For instance, the rate of return risk is discussed in Principle 3.6 and equity investment risk is discussed in detail in Principle 3.13.

17.

Welcome the proposals, which are in line with our thinking on the developing capability and role of stress testing within the Enterprise Risk Management Framework (ERMF)

KFH welcomes the opportunity to comment on this Exposure Draft. We welcome the proposals, which are in line with our thinking on the developing capability and role of stress testing within the Enterprise Risk Management Framework (ERMF) that we are putting into place. We are currently in the process of substantially upgrading our stress test capability in preparation for the Internal Capital Adequacy Assessment for the year-end and have the active engagement of Senior Management and the Board in the implementation of the stress tests and the analysis of the results. We expect to use these results to calibrate our Risk Appetite and support the Corporate Strategy. KFHK

No change. Noted.

18.

Consistent benchmarking

Regulators should set internationally accepted criteria that are standardised for consistent benchmarking and avoidance of inappropriate selectivity by regulated institutions. BB

No change. The Council of the IFSB is comprised of various regulators and supervisory authorities and various representatives of these regulators and supervisory authorities were part of the STWG, to prepare

14

internationally accepted best practices for consistent benchmarking across the IFSI. In addition, these Guiding Principles take into account the international developments related to stress testing such as those of BCBS and CEBS.

19.

Advanced approaches of capital adequacy

We recommend IFSB to encourage IIFS in migrating towards advanced approaches of capital adequacy which would ensure better infrastructure in place thereby improving the overall stress testing exercise at IIFS. AU

No change. Agreed on substance. The IFSB has required in its standards only standardised approaches, however, it has mentioned in its IFSB-2 (capital adequacy standard) that IIFS can use the advance approaches but subject to the approval of respective supervisory authorities. The IFSB intends to work on the advance approaches, and it hopes that then these approaches will be adopted by the IIFS thereby improving the overall stress testing exercise at IIFS

20

Higher and more rigorous standards

Higher and more rigorous standards are needed for banks that post systemic risk, such as those with a market share of 10% or more. BB

No change. The IFSB is aware of the systemic risk and systemically important IIFS, which is addressed in the ED in the Paragraph 164 in Principle 4.3. The ED has already included the concept and application of proportionality with respect to stress testing practices and in this regard, respective supervisory authority is expected to provide clarity on the application of proportionality for IIFS within its jurisdictions and it is up to the supervisory authority to set any criteria or indicators to identify

15

systemically important IIFS. See Principle 4.3.

21.

Design of the stress testing framework (STF)

The Design of the stress testing framework (STF) should avoid undue complexity in order to maximize transparency to and the understanding of those responsible for the appropriateness of the STF. BB

No change. The BOD (as the ultimate internal policy-maker) should have ultimate responsibility for the overall stress testing programme, whereas senior management should be accountable for the programme’s implementation, management and oversight. Further, it has been highlighted in the ED that the managements of IIFS should recognise that the application of stress testing to different IIFS will vary in scope and complexity depending on the size and nature of operations of each institution. It is also recommended that the design of the STF should take into account the views from the organisations.

22.

Various trigger-events and supervisory stress testing

The document should mention situations that would trigger stress tests and state how the supervisory authorities should ensue that the tests are carried out when these trigger-events happen. CBN

No change. Various trigger events and factors are already outlined in the Principle 4.3 and specifically the Paragraph 163 addresses this concern.

23.

Comparison of the Basel and IFSB papers

In our review of the stress testing exposure draft, we noted that the paper is over twice as long (53 pages) as the Basel Paper (20 pages), but is not twice as helpful. It is true that it has extra Principles such as Principle 3.8 with no direct equivalent in Basel, but Principle 3.8 extends over one and a half

No change. It’s clear that one shouldn’t expect a straightforward mapping of the BCBS principles. The market response (consisting of more than 60 Organisations) received from various stakeholders (including 18

16

pages of description but ends up saying little that is specific for a bank to follow. 3.12 and 3.13 extend to over five pages but it is debatable how much value is added. But the critical aspect of the IFSB paper is the ‘cut & paste’ approach. Principle 3 of Basel is spread across 4 principles of the IFSB paper (3.2, 3.6, 3.7 and 3.17). Meanwhile IFSB Principle 3.11 covers 4 Basel Principles. This cutting and pasting, coupled with the descriptive length of the IFSB paper make comparison of the Basel and IFSB papers very difficult. CBB

central banks, more than 30 market players, and IMF, ADB, IDB, and others) indicates the usefulness of the ED. However, it is not clear from CBB response, in what ways; the guidance has not been helpful. Further, as set out in the objectives of the IFSB as mandated under its Articles of Agreement, the STWG should not “reinvent the wheel” but instead, wherever appropriate, reinforce the existing internationally recognised frameworks or standards for stress testing so that IIFS stand on a “level playing field” with their conventional counterparts, subject to due consideration being given to the specificities of Islamic finance. The Guiding Principles are thus intended to complement the existing stress testing framework so as to contribute to the soundness and stability of the IIFS particularly, and the IFSI as a whole (Paragraph 8). Therefore, consistent with objectives of the IFSB, the STWG has stressed number of times in the ED (see Paragraphs 1, 4, 8, and 9) that the objective of these Guiding Principles is not to reinvent the wheel rather complement the existing stress testing framework such as those of BCBS and CEBS. It should be understood that the ED does not only complement

17

the BCBS’s Principles for Sound Stress Testing Practices and Supervision (20 pages) but also complement CEBS’s Guidelines on Stress Testing (47 pages guidelines which are more operational than BCBS), in addition to other relevant documents issued by BCBS. Hence, The IFSB intends that its Guiding Principles as set out in this document should incorporate the above while making appropriate adaptations to take account of the specificities of IIFS in terms of their risk exposures (Paragraph 4). The STWG has discussed the extensively and agreed with both the length as well as scope of ED. Both documents (i.e. from BCBS and CEBS) have been discussed by the STWG in detail and subsequently updates have been given to Technical Committee in its several meetings. It is important to note that the additional guidance which has been added through Survey that identified the gaps within IFSI and those gaps have been addressed in the Guiding Principles. On the similar note, the long length could be attributed to the fact that the ED attempts to use more operational approach given the IFSI industry feedback collected through Survey. In addition, the ED has also

18

discussed some Principles which were not part of the BCBS and therefore the ED has provided Stress Testing Framework in a logical and a comprehensive manner taking into account the specificities of IIFS and international guidance on stress testing.

24.

Feedbacks from external credit rating agencies and/or central banks on this Exposure-Draft

Moreover, it is important that IFSB and the national supervisory authorities should obtain feedbacks from external credit rating agencies and/or central banks on this Exposure-Draft. Most of these bodies are familiar with Basel's stress testing guidelines (and/or European and American equivalent guidelines) and by which these bodies may not rate banks favorably if they are not complying with American/European/Basel guidelines. ITB

No change. This is part of the due process of the IFSB under Standard Operating Procedures (while developing any Standard) to get feedback from the various stakeholders including international bodies and various IFSB members. It is worth highlighting that the IFSB has received feedback on the ED from the various IFSB member central banks and international organizations such as International Monetary Fund (IMF). Accordingly the feedback has been reflected in the revised ED.

25.

Policies and procedures of stress testing

Requirement for policies and procedures of stress testing can never be treated as a compulsion for IIFS rather it should be treated as a regulatory requirement to start with. BBP

No Change. Policies and procedures are part of the effective stress testing programme and they should be properly documented. See Principle 3.4 for more detail. IIFS should treat them as integral part of their internal risk management rather than documenting because of regulatory compliance requirements.

19

26. Many economic/political crises happened that did not severely impacted banks within Bahrain

The STWG may note that throughout the past two decades, many economic/political crises happened that did not severely impacted banks within Bahrain (in fact they went by un-noticed). To name some:

• ERM crisis in 1992-1993; • Mexican crisis in 1994-1995; • Asian crisis in 1997-1998; • Argentine crisis in 2001; and • Dubai (UAE), 2009-2010

You may agree that some worldwide shocks were advantageous to the region: for example the September 11 attack on New York caused capital flights from America and Europe in this region (i.e. the impact was positive rather than negative)! This probably supports our views that stress-testing mechanisms could reasonably predict financial crises. One could also refer to the recent European Crisis which implemented stress-testing since early 2000 but yet these stress-tests did not adequately predicted the recent crises. ITB

No change. Noted. It is understood that the severity of these crises vary from jurisdiction to another jurisdiction, so the case in Bahrain. It should be noted that the objective of the stress testing is not to accurately predict the next financial crisis rather assessing and capturing vulnerabilities under various stress testing scenarios. It should be also clear that stress testing itself cannot address all risk management weaknesses. For instance, one could clearly see from European Banking stress tests exercises that they were looking to pass the stress test rather to see what banks could get fail. We have see seen that some of the banks that passed the stress test, subsequently went through financial distress.

27.

Regulatory and tax impacts in stress testing

The guiding principle covering the topics such as IIFS should follow regulatory requirements for stress testing and /or guidance from supervisory authorities in their stress testing exercise. However, from regulatory perspective, the IIFS should also take into account regulatory and tax laws changes in the jurisdiction in which it operates which are specifically related to Islamic banking. The business of IIFS is largely based on transactions such as Ijārah, Murābahah, etc which involve transfers of real assets such as land, building, commodities and

Agreed. Now these regulatory and tax impacts have been reflected under the Principle 3.6 (i.e. key risk factors).

20

any adverse regulatory or tax changes can directly affect the costs of doing business and hence the profitability of the IIFS. HKAB

28.

Various cross-border effects and their possible impacts on the stress-tests

We also recognise the importance of considering effects of cross-border economic crises on performance of banks. However, we believe that the Exposure-Draft should give due considerations to the various cross-border effects and their possible impacts on the stress-tests. Impacts of cross-border economic challenges come in two flavors:

• Direct Impact: Cross-border balance sheet linkage which might occur as a result of banks owning assets in ailing economies -> possible high impact; and

• Contagion impact: Effects of spillovers resulting from exogenous global shocks -> possible low impact.

As a result of the above we believe that the Exposure-Draft should not adopt a "one-size-fits-all" approach. Rather, the Exposure-Draft must direct regulatory authorities to define various stress-test parameters /templates (instead of one template) for various possibilities such as the 2 discussed above, ITB

Agreed. Though the cross-border impacts have been outlined in various places of the ED with respect to IIFS, however, the revised Paragraph under Principle 4.3 addresses this concern and include the suggested point with respect to supervisory authorities. The ED recognises this issue and therefore does not recommend “one-size-fits-all" approach (see first Paragraph of Principle 3.3) and hence it has used the principle of “proportionality” in various places to clarify this point. Secondly, as mentioned under the necessary conditions, supervisory authorities should also bear in mind the principle of “proportionality” with a view to establishing effective stress testing regimes in their jurisdictions (see Section 2.5).

29.

Exposure-Draft is placing on stress-testing as a prediction tool

We acknowledge the importance of utilizing "forward looking" reports in addition to "static" and "dynamic" reports in the decision making process. However, we are, somewhat, indifferent with the over-emphasis the Exposure-Draft is placing on

No change. The ED does not attempt to suggest stress testing as a prediction tool rather as risk management tool within risk management of an IIFS. In addition,

21

stress-testing as a prediction tool. ITB

the ED is explaining how stress testing as a risk management tool, can be used by the IIFS to make forward looking assessment of risks and certainly forward looking assessment involves on more quantitative and expert judgment. It is also important to note that the existing models used by IIFS as a risk management tool such as VaR to assess the IIFS’ risks have failed to detect the vulnerabilities because VaR involves fitting the possible magnitudes of a risk exposure under a normal distribution curve, and as such is a type of risk measurement tool (with the weakness that it underestimates risks with ‘fat tailed’ distributions and does not measure them correctly for skewed distributions. Therefore, highlighting the need of having in place alternative tools such as stress testing to assess the risks (see second Paragraph of Principle 3.3).

30.

Standardized risk approach vs. sophisticated modelling approaches

This ED is suitable for IIFS which are trying to move from standardized risk approach to more sophisticated modelling approaches.

Wan

No change. It is expected that gradually most of the IIFS will also be moving to towards more advance approaches compared with what they are using now. The Guiding Principles have been designed keeping in view the impact study results (which provided insights into the approaches). The IFSB is also

22

considering addressing advance approaches in near future.

31.

Immediately to overcome future data requirements

Chief Risk Officers in IIFS should start strategizing internal modeling techniques immediately to overcome future data requirements. The fact that current data is scarce should not hinder banks to start the process of collecting risk factors. Internal models are needed to compute expected loss for internal assets and periodic validation should be conducted independently to verify the model’s accuracy and robustness. Wan

No change. Noted. This is expected from the IIFS once the Guiding Principles are adopted.

32.

Problems with statistical models

We are confident that members of STWG are aware of the fact that over-reliance on statistical models led to economic meltdown of one of the biggest economies in the world (USA) where financial institutions over used V@R as a statistical-model for measuring risks. Some analysis that we have reviewed in this respect attribute the problems with statistical models to: (1) difficulty with predicting extreme rare risks especially those relating to contagion impacts, (2) historical data doesn't necessarily predict future outcomes, and (3) historical data may be biased by data aggregated during periods of economic crises or economic booms. ITB

No change. The STWG has discussed and addressed this issue in the ED. It should be clear that failure of VaR has indicated the use of stress testing to capture the extreme shocks which are normally not addressed within the historical data and therefore, historical data needs to be supplemented by the expert judgment or qualitative criteria. However, the issue of over-reliance has been discussed at the working group level and certainly the STWG has acknowledged it in the second Paragraph of Principle 3.3.

33.

Type-2 Model Risk

The former Head of the Federal Reserve, Alan Greenspan spoke of the “incipient science of stress testing”. We caution against excessive reliance on models that are not well understood or based on insufficient or inadequate data. In seeking to gain

No change. See response above.

23

acceptance for stress testing as a risk management tool we caution against what statisticians call Type-2 model risk, where the model indicates that all is well when it is not. For this reason we will continue to overlay management and Board judgment on the reliability of the results of the stress tests conducted at KFH. KFHK

34.

22 principles majority of them are covered in current CBK guidelines

Of the 22 principles majority of them are covered in current CBK guidelines are general principles. In addition KIB has based on its risk profile included specific scenarios in its internal methodology to ensure that the stress testing is comprehensive. Notwithstanding the principles in the Exposure Draft of IFSB which are either not explicit in the existing guidelines or could potentially be a cause of concern if the same were to be included in CBK guidelines has been discussed. KIB

No change. Noted.

35.

Guidelines are more detailed in nature

Most principles in the proposed IFSB draft are covered at a broad level in the existing CBK guidelines. The proposed IFSB guidelines are more detailed in nature. Thus implementation of the same may need more allocation of time and effort. KIB

No change. Noted.

36.

Vetted for Legal and Shari’ah compliance relevant

The exposure draft is definitely welcome but it needs to be ensured that the same is vetted for Legal and Shari’ah compliance relevant to the

No change. The IFSB has made explicit in the ED that the implementation of the Guiding

24

Kuwait before CBK incorporates the salient features into its regulatory guidelines.

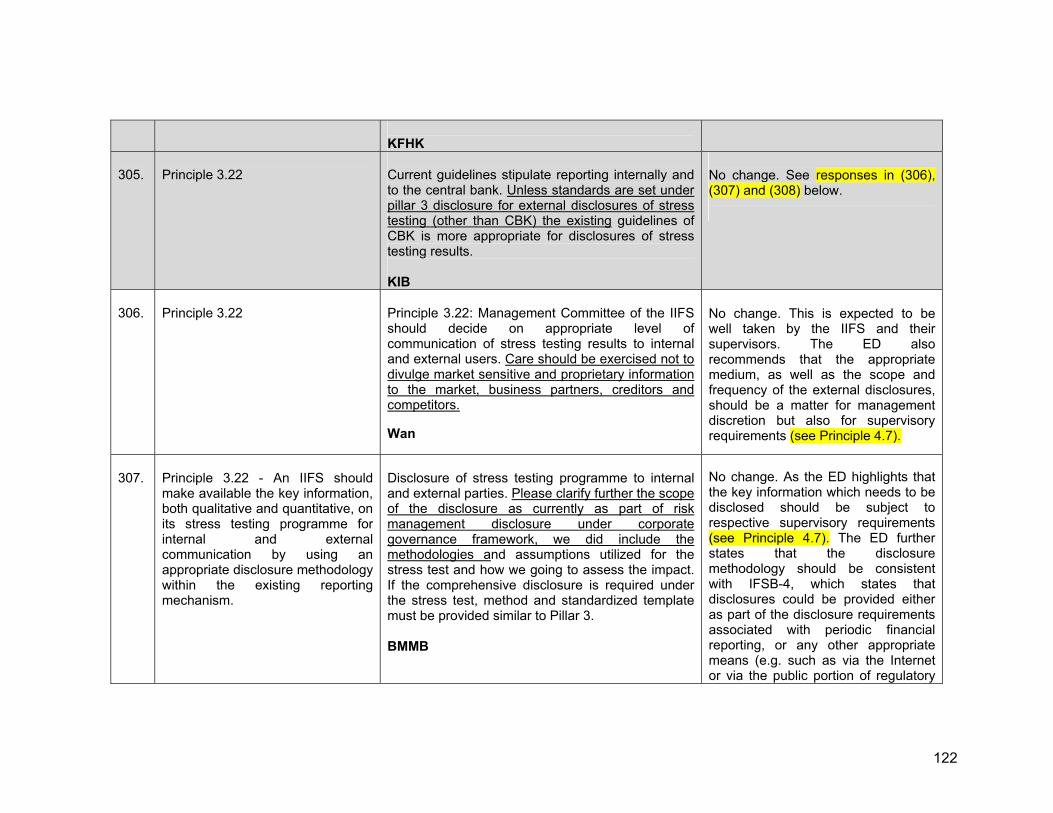

KIB

Principles should be undertaken in compliance with Sharī̀ ah and within the legal framework of the jurisdictions in which IIFS operate and should be commensurate with the size, complexity and nature of each IIFS in line with the IFSB-1.

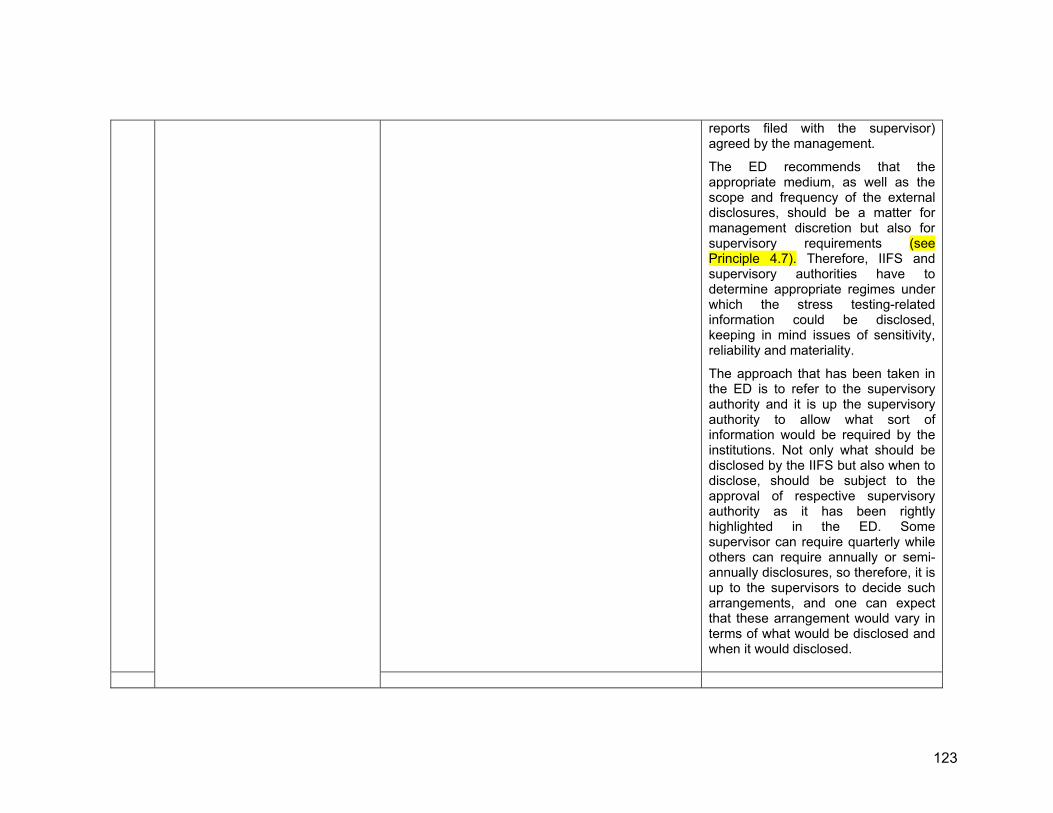

37.

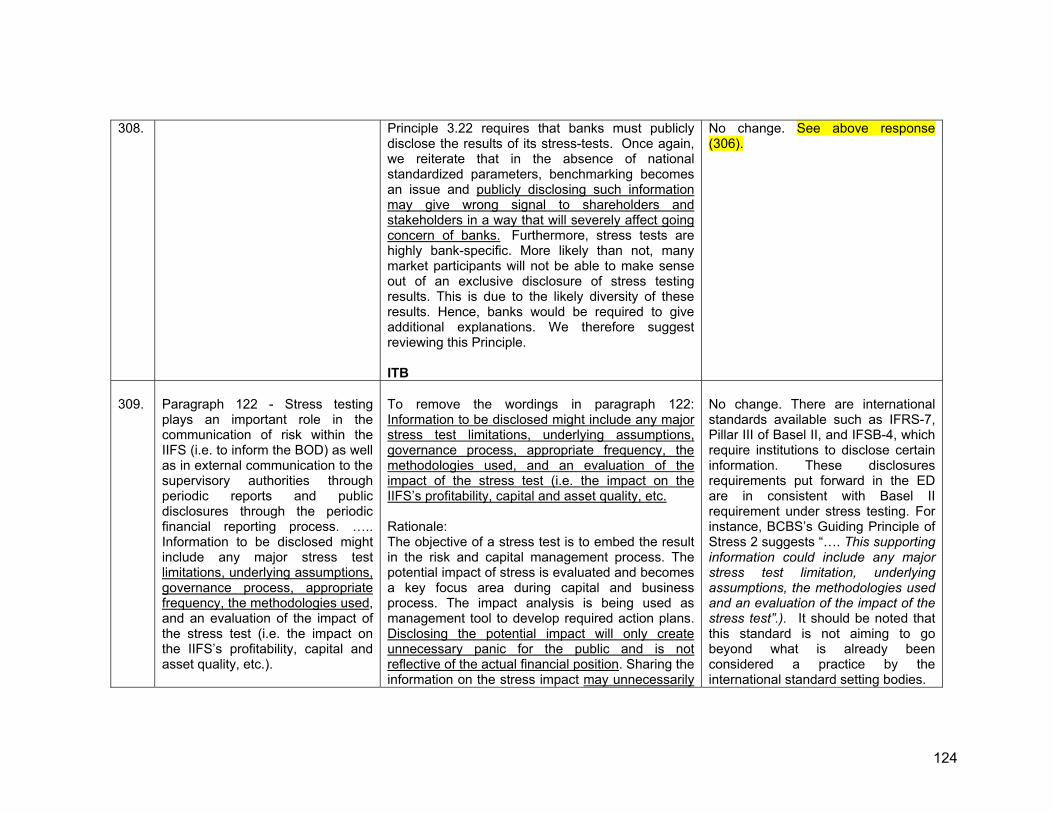

6 principles prescribed are in line with the international standards (BIS)

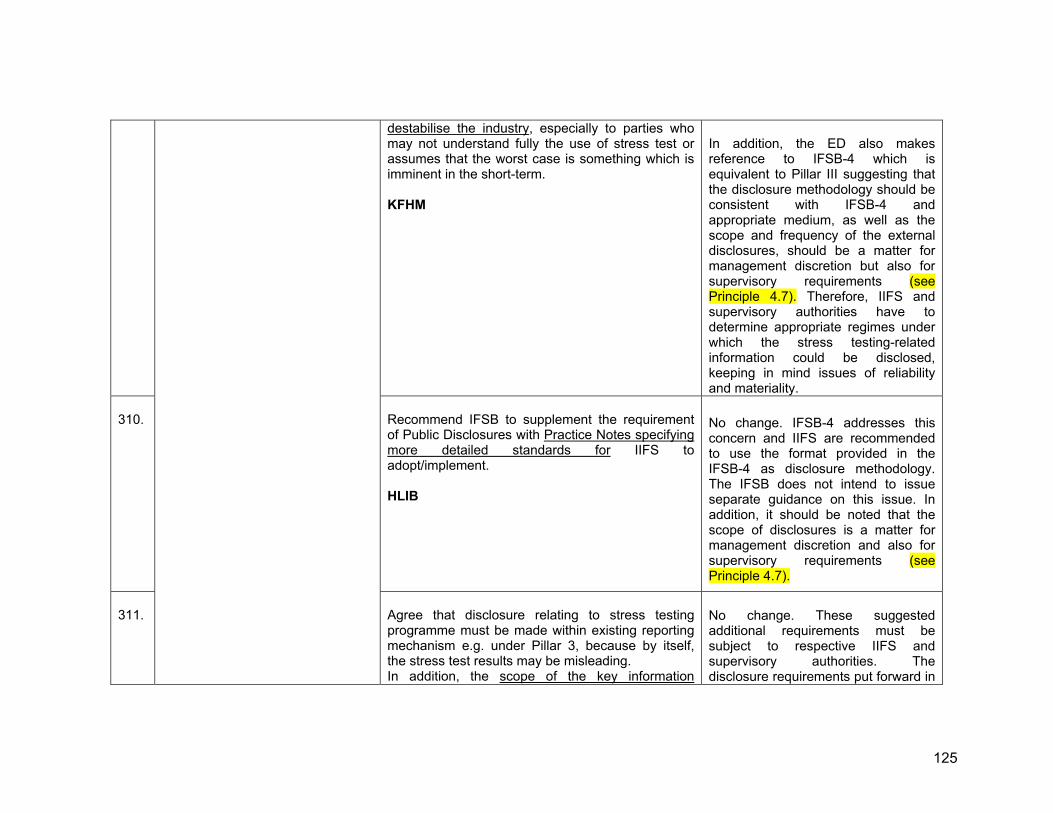

As in other international documents the IFSB document also emphasis on the importance of supervisory review and assessment of stress testing programmes. The 6 principles prescribed are in line with the international standards (BIS) in this regard as is already being followed by CBK. KIB

No change. Noted

38.

Earlier instructions of IFSB

The document referrers at several places to adopting the earlier instructions of IFSB. These should be duly corrected to refer to as “…the instructions as issue by CBK in this regard for Islamic Banks in Kuwait”. KIB

No change. It is obvious that the IFSB can not make reference in the ED to any particular jurisdiction with respect to the implementation of its earlier standards. It is expected that IIFS should make reference to respective equivalent guidance issued by the respective supervisory authority on the specific standard.

39.

Guidelines may not be made mandatory but should be optional depending on applicability

All the prescribe guidelines may not be made mandatory but should be optional depending on applicability to be applied by each IIFS based on their proportionality (i.e. Depending on the size and nature of its activities as already stated in the Exposure Draft). KIB

No change. The Guiding Principles aim to reflect the best practices of stress testing and the IFSB does not intend to make these Principles mandatory to any IIFS rather same could be done by respective supervisory authority. Further the IFSB believes that implementation of these Principles will make IFSI more robust and sound so that IIFS stand

25

on a “level playing field” with their conventional counterparts, subject to due consideration being given to the specificities of Islamic finance. The concept of proportionality is discussed in the ED already.

40.

Output working models could be made jointly by all institutions together

In case of requirement of standardization of stress testing output working models could be made jointly by all institutions together with help from external party. KIB

No change. It is already discussed in Section 2.4.

41.

Cover wide ranging risk management perspectives

IFSB’s guiding principles on stress testing for Institutions offering Islamic Financial Services (IIFS) cover wide ranging risk management perspectives including:

• Forward looking risk quantification of potential risks

• Risk assessment from quantitative as well as qualitative aspects

• Risk assessment based on historical as well as rare and extreme possible scenarios

• Risk assessment based on contingent exposures

WB

No change. Noted

42.

Bank’s stress testing framework should cover….

Bank’s stress testing framework should cover at least following potential aspects:

• How bank’s credit and investment portfolios would behave in case of dramatic changes in economic variables such as profit rates, exchange rates or economic cycles of inflation, recession, tight credit, liquidity squeeze etc. This covers finding out

No change. These aspects are already addressed in the ED and reflected in various Guiding Principles.

26

sensitivity of bank’s assets to different market dynamics.

• Finding out all possible potential threats which could hinder bank’s normal operations in case of funding dry out, liquidity squeeze, lack of market trust, frozen interbank money market, short money supply, higher inflation / interest rates, deposit withdrawal etc.

• Assessing how a stressed scenario could impact bank’s profitability and bank’s capital.

WB

43.

IFSB Stress testing covers all above concerns with well given guidelines to assess potential risks.

We think IFSB’s paper on stress testing covers all above concerns with well given guidelines to assess potential risks. The IFSB paper has also tried covering issues which banks usually face in successful implementation of a wide ranging stress testing platform, issues such as:

• Majority of our stress tests are either sensitivity or scenario based. Banks rarely assess extreme loss, value or reverse testing.

• There is hardly any uniformity in the criteria, methodology or assessment of risk parameters for stress testing. Guidelines about models, reliability & comprehensiveness of data are some other constraints.

• Stress tests and their results are usually taken as granted as a matter of routine process. Results hardly lead to capital allocation. Guidelines lack for capital planning based on specific stress tests.

• Stress tests sometimes play a role of only up to risk awareness.

No change. These concerns and limitations of stress testing are already addressed in the ED and reflected in various Guiding Principles.

27

WB 44.

Compliance only through regulations

Compliance can only be effective if the same is regulated by Central Banks. DIB

No change. This is one of the necessary conditions of the effective stress testing regime. See 2.5 and Principle 4.1.

45.

Comprehensive of the explanation on what issues shall require national regulations

Due explanation was made in quite a detailed manner on the principles to be adhered to by lIFS's concerning the Stress Test in the document titled "Guiding Principles on Stress Testing for IIFS". In our: opinion, the concerned document is to be comprehensive of the explanation on what issues shall require national regulations and on what issues the international regulations shall have to cover all the countries so that a system in such a detailed fashion can be established at IIFS's. On the other hand, there exists DO clarity on such issues as from what institution or institutions the Interest-free Finance Institutions shall be able to acquire the Islamic Benchmark Rate and by what indices they shall take into account the changes in the prices of Houses/Flats or Mortgage if those principles mentioned here are established within IIFS's. CBRT

No change. The ED is already detailed and comprehensive, and detailed and specific framework and clarity on certain issues, keeping in mind the concept of proportionality, is expected to be provided to the IIFS by respective supervisory authority.

46.

Concerning the Benchmark Rate of the Institutions that offer Islamic Financing Service as

On the other hand, we believe that the guidelines on what sorts of stress scenarios could be established concerning the Benchmark Rate of the Institutions that offer Islamic Financing Service as regards to profitability, which issue is not mentioned in the Draft document, is to be included in the aforesaid Regulation as well.

No change. It is addressed in various places, for instance, see rate of return risk, which is addressed in Principle 3.6.

28

CBRT 47.

More interested in the Governance related issues and not the detailed operational ones to get the big picture

As you know our focus, when it comes to Islamic Finance related research, is rather on the Corporate Governance part. Therefore I would rather like to abstain from this one as we can add much more value in our core area. Our complementary focus on the conventional investment industry, socially responsible investments and know how in Islamic Finance is indeed unique and helps us to better grasp the changes in the asset management and finance industry as a whole and globally. I must admit though that when it comes to Islamic Finance we are more interested in the Governance related issues and not the detailed operational ones to get the big picture. MURAT

No change. Noted.

48.

Stress Testing for relevant Islamic capital market intermediaries

Moving forward, the IFSB may wish to conduct a study and undertake assessments on the applicability of developing similar standards relating to Liquidity Risk Management and Stress Testing for relevant Islamic capital market intermediaries, e.g. Islamic stockbroking companies. SCM

No change. Agreed that consideration should also be given to addressing the application of stress testing to risk management in other IFSI segments such as Takāful and capital market firms, and the IFSB may consider this in future.

49.

Commend the efforts of the IFSB and the High level governance principles for stress testing

We did not find it necessary to specifically make comments on the documents as they contain high level governance principles for liquidity risk management and stress testing, with which we are in agreement and feel that they will create the market discipline needed for these functions to be effective. Thank you for inviting us to make comments. Arcapita is always there to support all the initiatives of the IFSB and look forward to

No change. Noted.

29

working with yourselves in the future also. ACB

50.

As usual, we commend the efforts of the IFSB and the Central Bank of Bahrain (as well as other central banks forming part of the IFSB) in developing rules for strengthening the financial sector and maintaining economy robust financial system resilient to economic shocks. ITB

No change. Noted.

51.

The IFSB has done an excellent work in developing a very comprehensive Guiding Principles on Stress Testing taking into considerations the additional areas that are only peculiar to Islamic [finance] such as Shari’ah non-compliance and the various underlying Islamic contracts used in the industry. OCBCA

No change. Noted.

52.

Needless to mention, the IFSB Guiding Principles are very comprehensive and useful and we feel that the same has to be first accepted and implemented by the central banks of the respective GCC countries. In Qatar, recently QCB has closed the Islamic windows of commercial banks and we look forward to their guidance on these important issues. MAR

No change. Noted.

53.

The guiding principles on Stress Testing are very comprehensive but their implementation challenges will need focus on capacity building at IIFS level in terms of IT Systems and human resource.

No change. Noted. IIFS will have to address these challenges before implementing these guidelines.

30

ABP

54.

We have noticed that the document have sound and efficient principles and guidelines, and are primarily to serve Islamic Banks. Also, this document will enhance stability of the overall Islamic Banking Systems. ABL

No change. Noted.

55.

We believe that IFSB has prepared a very comprehensive document on Stress testing. Application of these guidelines would be a benchmark in safeguarding the interests of stakeholders of the bank. BBP

No change. Noted.

56.

The document on “Stress Testing” provides a comprehensive study for supervisory and internal regulatory controls. The Senior Management as well as the Board members needs to be aware of the impacts of the numbers generated through MIS and transform these into meaningful relative qualitative assessment. BAP

No change. Noted. These concerns are already well taken in the ED.

57.

I would congratulate the author(s) on producing such a comprehensive, not to say exhaustive, document. The level of detail will benefit all banks seeking to introduce robust stress testing procedures. Andrew

No change. Noted.

31

58. We share IFSB’s view on the importance of a sound and robust stress testing framework for IIFS and appreciate in this regards. KHFB

No change. Noted.

59.

We strongly support the initiatives of the Islamic Financial Services Board in defining the guiding principles on Stress Testing… Stress testing has been identified as an important tool for pro-active management of would-be vulnerabilities. It encompasses several facets - ranging from pro-active oversight to maintaining transparency to stakeholders - which are all essential in addressing institution- specific and system-wide weaknesses. We are particularly supportive of the fact that the EDs contain tenets that would allow the management of both in Institutions offering Islamic Finance Services (IIFS) and in conventional banks. Consistently handling the challenges provided by these two will lead to clear synergies. We welcome the 28 principles outlined by the Islamic Financial Services. Board (IFSB) on stress testing for Institutions offering Islamic Finance Services (IIFS). Of the 28 principles, it is noteworthy that 6 of these are addressed to the regulators, suggesting that the overall guidance on the practice of stress testing is shared between the IIFS and its regulatory authority. The principles are particularly welcomed since it complements the same practice in conventional banks. Under the overarching objective of financial stability, this complementation between Islamic and conventional banking is an area that should be continuously nurtured. Ultimately, it is governance

No change. Noted.

32

and the management of risks that will define the "state" of a bank, whether operating under Islamic or conventional guidelines. However, stress testing is perhaps the most viable ex ante risk monitoring tool that is available to date and in this sense, its value cannot be understated. BSNP

SECTION 1: INTRODUCTION AND BACKGROUND 60.

Paragraph 1 - …….These Guiding Principles are intended to complement existing and future IFSB standards and guidelines in the banking segment of the IFSI……..

No need for mentioning to complement "future" standards and principles. Only can make reference to the existing standards and principles. CBOS

No change. The IFSB does intend to issue and/or revise its some of standards which will benefit from this guidance. Moving forward, for instance, supervisory review process (IFSB-5), which will include some aspects of stress testing under Pillar II, similarly the guidance on ICAAP will benefit from these Guiding Principles.

61.

Paragraph 3 – “……..It was also observed that there was insufficient integration into institutions’ risk management frameworks, that scenarios were not sufficiently severe, that the dangers considered in "extreme" scenarios were not extreme enough (e.g. Irish banks that had failed disastrously passed the European Union (EU) stress testing exercise), and there was lack of consideration of confluences of events, risk concentrations and second-round

Referring to Irish banks passing an EU stress test. The text should specify that this test was published in July 2011, since the European Banking Authority conducted others tests later in the year. Andrew

Agreed. This has been updated.

33

effects.

62.

Paragraph 5 - …….With regard to the specificities of IIFS, the question remains of how well IIFS will be able to absorb stresses and shocks that are more specific to the Islamic financial market, with regard to credit, market, operational, and (perhaps particularly) liquidity risks. This implies an approach to stress testing (including various specific scenarios) that differs in some respects from that applicable to conventional institutions, which this document aims to set out and to explain.

Credit, market, operational and liquidity risks are not specific risks that are related to the IIFS, as conventional banks have exposure to these kinds of risks as well. Instead, it would be appropriate to make reference to risks that specific to IIFS like displaced commercial risk and fiduciary risk. CBOS

Agreed. The paragraph is updated with rate of return risk and displaced commercial risk. In addition, a cross reference to Paragraph 7 also has been made.

63.

Paragraph 6 -….however, IFSB-1 did not give specific consideration to: (i) how to apply and conduct stress testing; and (ii) what should be the stress scenarios, the calibration of shocks to be applied, etc. …….

Clearly, IIFS would be keen to know how to apply the Guiding Principles contained in the document including illustrations of how to perform Stress Testing. Paragraph 6 of Section 1 states: “…however, IFSB-1 did not give specific consideration to: (i) how to apply and conduct stress testing; and (ii) what should be the stress scenarios, the calibration of shocks to be applied, etc. … The guiding principles in this document aim to complement …IFSB-1 and IFSB-5 in the above respects.” It was not apparent from our review of the ED where the above two issues are addressed and the ED may be perceived as too theoretical and lacking guidance on how to implement Stress Testing in practice. IDB

Agreed. The paragraph is revised and updated in order to clarify the limitations mentioned with respect to IFSB-1. See revised Paragraph 6, which includes following wordings…. however, IFSB-1 did not give specific consideration to “a comprehensive stress testing framework as a key risk management tool within IIFS”. In regard to how to apply the Guiding Principles contained in the ED, it is not the key objective of this ED, broadly speaking respective supervisory authorities are expected to provide the implementation guidance taking into account the local

34

context and specificities. Moving forward, however, this is one of the promising issues which have been raised by the various respondents during the public consultation and the IFSB may consider addressing in detail through “implementation guidance”. See responses in (9) and (10) above.

64.

Paragraph 7 - There are particular considerations to be borne in mind in the case of IIFS. ……special attention to the position of the investment account holders (IAHs) and its implications for risk management. .…the IIFS are also exposed to other unique risks, such as rate of return risk and displaced commercial risk (DCR), and specific aspects of operational and reputational risk such as Sharī̀ ah non-compliance risk …

The para makes reference to risks that IIFS entails beside the investment account holders. It would be appropriate if the Para. starts with explaining or highlighting the specificities of IIFS so as to enable the ordinary reader to capture and follow up why IIFS warrant special treatment when undertaking stress testing. CBOS

Agreed. Consistent with another suggestion by CBOS on the shifting of Para.20 into introduction section, this Para.20 (which is on specificities) has been merged into Paragraph 7. See revised and updated Paragraph 7.

65.

We welcome the efforts of the IFSB to create a level playing field for Islamic business. SAMA

No change. Noted

66.

Paragraph 8 of 1.1 - main premises and objectives)

It might be useful for the document to be a little more explicit about the objectives of stress testing. For supervisors, the objective is to maintain financial stability and this may, or may not, include a desire to avoid the occurrence of individual bank failures. Supervisors would typically test whether

No change. The ED is very specific to the objectives which have been listed in the Section 1.1 and they are divided into two perspectives. One on IIFS stress testing and second on supervisory role of stress testing. The ED focuses more on providing

35

banks will be able to continue to comply with bank regulations (e.g. capital minima, liquidity buffers) under a variety of stress scenarios. Their assumption would be that widespread inability to meet regulatory requirements would likely presage financial instability. Andrew

framework on stress testing and providing minimum expectations such as outlined in Paragraph 9 (b). With respect to supervisory perspective, issue of financial stability is addressed in Paragraph 9 (c). At macro level stress testing, agree with the observation that supervisors would typically test whether banks will be able to continue to comply with bank regulations (e.g. capital minima, liquidity buffers) under a variety of stress scenarios. These considerations are addressed in detail in the ED Principles 3.10, 3.14, and 4.1.

67.

Paragraph 8 - As set out in the objectives of the IFSB as mandated under its Articles of Agreement, the STWG should not “reinvent the wheel” but instead, wherever appropriate, reinforce the existing internationally recognised frameworks or standards for stress testing so that IIFS stand on a “level playing field” with their conventional counterparts, subject to due consideration being given to the specificities of Islamic finance.

We would suggest to rephrase this sentence to be the working group has been mandated to customized and/or complement the existing international guidelines to cater for the specificities of the IIFS. CBOS

No change. This is consistent with the objectives of the IFSB as mandated under its Articles of Agreement.

68.

Paragraph 9 (b) (i) - …benchmark rates…)

It would useful to clarify what hurdle rates would be used for the stress testing, Basle II or Basle III? (Assuming these are applicable in Islamic banking). IMF

No change. The ED complements the Basel II and what has been included in the ED is reference to certain benchmark rates/hurdle rates (as guidance) since it is understandable

36

that the applicability of these rates will vary from IIFS to another IIFS. The footnote 5 of the ED provided some illustration of what benchmark rates/hurdle rates could be used for the stress testing. For instance, benchmark rates include market-based reference interest rates such as LIBOR (London Interbank Offer Rate), EIBOR (Emirates Interbank Offer Rate), etc.)

69.

In addition to stress-testing the benchmark rates, foreign exchange rates, credit quality, etc., IIFS and supervisory authorities should also stress test the new Islamic Interbank Rates (IIBR), wherever applied by the IIFS in order to identify how different portfolios of the IIFS respond to changes in key economic variables. This is important because if the IIBR could really be the alternative to LIBOR, then its rate should be tried and stress-tested to ensure its workability, acceptability and reliability.

Wan

No change. As for as this ED is concerned, it makes reference to general reference rates which could serve as benchmark rates as mentioned in the previous response. Nevertheless, it is up to respective supervisory authorities to require IIFS to take into account specific benchmarks such as suggested. It is expected that these benchmark when developed in isolation, that is, without making reference to prevailing market rates, then the workability, acceptability and reliability would be a key concern for both IIFS and their supervisory authorities and therefore they should be tested at respective supervisory level before requiring to IIFS.

70.

Paragraph 9 (b) (v) - Analyze the IIFS' ability to meet its capital requirements.

Suggest adding the word "economic" to capital to be "economic capital" as stress testing is related to the economic capital. CBOS

No change. Stress testing is not only related to “economic capital” rather also “regulatory capital” and both of these requirements are addressed in the Guiding Principles, particularly in

37

Principle 3.10. See Principle 3.10.

71.

Paragraph 9 (c) - For supervisory authorities, stress testing can be used (i) as a surveillance tool for periodically testing the safety and soundness of the financial system, and (ii) ……to identify “weaknesses” in the financial system and structural (systemic) vulnerabilities arising from the specific risk profiles of IIFS individually and collectively.

The draft could add that stress testing outcomes could also play a role in designing macro-prudential policies. IMF

Agreed. The Paragraph 9 (c) is updated to reflect the suggestion by the IMF.

72.

Paragraph 10 - However, in order to be effective in promoting risk management and for IIFS to develop a robust stress testing framework , stress testing by IIFS would be need to be complemented by a set of infrastructure components that serve as necessary conditions …"

Infrastructure components are considered as prerequisites to conduct stress testing and could not complement to stress testing. We would suggest to change/ replace the word "complement" by the word "require" CBOS

No change. The word “complemented” has been used in the right context as the list of these necessary conditions is not the exhaustive rather some of primary considerations which can enhance the stress testing framework. In addition, this also take into account the fact that stress testing is still being performed even without these conditions, however, having in place these conditions will certainly improve the quality of stress testing framework. Further, one should also keep in mind that stress testing should also be complemented by the observance of international standards for stress testing.

73.

Paragraph 11 (scope of application)…..….The Guiding

We believe it is correct for the Supervisory Authority to decide how to extend the application of this guidance to Islamic windows.

No change. Noted

38

SAMA

74.

Principles are primarily intended to serve the full-fledged banking IIFS with due consideration to proportionality taking account of their size, sophistication and complexity....Supervisory authorities may, at their discretion, extend the application of these Guiding Principles to Islamic “window” operations that are self-contained or other institutions offering Islamic financial services that fall within their jurisdictions).

According to para. 11 of ED13, the Guiding Principles in general do not apply to Islamic windows operations. However, supervisory authorities may, at their discretion, extend the application of these Guiding Principles to Islamic windows operations that are self-contained. It would be helpful if the IFSB could elaborate on the rationale for not requiring the Guiding Principles to apply Islamic windows operations and provide guidance on factors that supervisory authorities should consider when deciding whether an Islamic windows operation should be subject to the Guiding Principles. HKMA

No change. This is not the scope of this ED to elaborate on the rationale for not requiring the Guiding Principles to apply Islamic windows operations. In this respect, supervisory authorities are referred to IFSB-5 (supervisory review process (SRP)) in the footnote which is already added in the Para.11. This is Pillar II (supervisory review process) issue which is to be addressed under revised SRP (IFSB-5) standard (the IFSB has established working group for revising IFSB-5). In this ED, it is left to the respective supervisory authorities to decide how to extend the application of this guidance to Islamic windows, at their discretion, however, the IFSB notes the suggestion of HKMA and the revised SRP can provide guidance on factors that supervisory authorities should consider when deciding whether an Islamic windows operation should be subject to the Guiding Principles.

75.

Para. 12. - The Guiding Principles will be applicable to any IIFS that falls within the scope as stated above, on a fully consolidated basis at the holding company level within a group or sub-group of IIFS, or as appropriate, on an individual basis subject to approval of the

Paragraph No.12 provides that the Guiding Principles will be applicable to the IIFS on a fully consolidated basis at the holding company level. Here it would be required to be clarified that the stress testing would be required to be done individually at subsidiary level and thereafter individually at the holding company level. The results of these individual stress testing would be

Agreed with suggestion. A new footnote in Paragraph 12 has been added to clarify this point.

39

then required to be consolidated for analytical purposes. It is important that stress testing is conducted on an individual basis for each entity as the individual entities would be exposed to different types of internal and external risks which would be required to be appropriately accounted for. The element of correlation of different risks for an individual entity and amongst other entities within the group should also be accounted for when consolidating the results of the stress testing. ITB

76.

supervisory authorities. The Guiding Principles are not intended to be applied at the consolidated level to a group or sub-group that consists of entities other than (banking) IIFS as defined in paragraph 11 above.

… as defined in the standard …"What is intended in the guiding principles not "standard". CBOS

No change. There is no such wording of “as defined in the standard” in the Paragraph 12 of Guiding Principles.

77.

Paragraph 13 - ….. The Guiding Principles describe both qualitative and quantitative aspects of stress testing while keeping in view the principle of proportionality; that small and simple IIFS may focus on the qualitative aspects while larger, more complicated IIFS will require more sophisticated quantitative stress testing techniques. The principle of proportionality is applicable to all aspects of these Guiding Principles, including the governance process, risk identification and scenarios development, methodology, disclosures, …….of the stress tests.

Whilst it is reassuring that IFSB makes some concessions to “small and simple” IIFS in complying with the comprehensive range of requirements detailed in this Guiding Principles paper, it is still a bit sketchy on determination on what constitutes a small bank. More clarity on this would be good, but in the interim we take it respective IIFS will make this call themselves. ARBM

No change. It is outside the scope of the ED to suggest any methodology or criteria which would determine what constitutes a small bank and sophisticated bank rather it is expected that respective supervisory authority would be able to determine such distinction. This is reflected in the Section 2.5, which requires respective supervisory authority to provide clarity on the principle of proportionality.

40

78.

Paragraph 15 – Stock taking initiatives -Survey

We would also appreciate if the IFSB can share with the IIFS the range of stress testing practices and methodologies across the industry. KFHB

No change. Due to confidentiality with other participating IIFS in the Survey exercise in terms of sharing their experiences with respect to stress testing, it is not the policy at the IFSB to share the range of practices and methodologies with other IIFS, collected through the Survey. However, the ED does reflect the best practices that were identified during the Survey at certain places, where appropriate, to guide IIFS and also the executive summary of the findings is presented in the ED and several references to different practices are made in the ED at various places.

79.

Paragraph 16 - The implementation of the Guiding Principles should be undertaken in compliance with Sharī̀ ah and within the legal framework of the jurisdictions in which IIFS operate and should be commensurate with the size, complexity and nature of each IIFS in line with the IFSB-1. The IFSB will expect its members to apply the present Guiding Principles by January 2013, meaning that by this date the guidelines should be transposed into national supervisory guidelines and be reflected in the national supervisory manuals/handbooks, where applicable, and implemented in

No main comments regarding the ED, however, one concern relating to the implementation date January 2013, which we found too early considering other new regulatory requirements. KHCB

No change. The IFSB expects its members to apply the Guiding Principles by January 2013, meaning that by this date the guidelines should be transposed into national supervisory guidelines and be reflected in the national supervisory manuals/handbooks, where applicable, and implemented in supervisory practices, however, respective supervisory authority may extend its implementation deadline depending on (i) the readiness of the IIFS in its jurisdiction (ii) supervisory guidance (iii) and supervisory expectations on the implementation (different phases).

41

80.

We would like to suggest that the proposed implementation timeline of January 2013 should be reviewed and the implementation should be in a phased manner. KFHB

No change. See response in (79) above.

81.

Looking at the many and granular stipulations of this paper, and the infrastructure and resources required to implement same, it is foreseen that some IIFS may struggle to meet the January 2013. It is hoped that some leeway may be given on this. ARBM

No change. This is expected and this will depend on the relevant supervisory authority discretion. See also response in (79) above.

82.

supervisory practices.

The IFSB expects supervisors to include these guidelines in their respective regulation by January 2013. There should be at least 1 semi-annual and full year trial reporting before formal reporting is initiated. KIB

No change. This is up to the relevant supervisory authority discretion. See also response in (79) above.

83.

These principles which are required to be implemented by January 2013 would help banks to assess potential risks by looking beyond the limited period historical data. The recent financial crisis has shown that banks which rely on only historical events, limited scenarios or VaR models could face quick capital evaporating shocks. WB

No change. This has been highlighted in the Paragraph 37 of Principle 3.3.

84.

Paragraph 16 - The implementation of the Guiding Principles should be undertaken in compliance with Sharī̀ ah and within the legal framework of the jurisdictions in which IIFS operate and should be commensurate with the size, complexity and nature of each IIFS in line with the IFSB-1. The IFSB will expect its members to apply the present Guiding Principles by January 2013, meaning that by this

A requirement of approval of the Sharia Board should be incorporated in respect of compliance of

No change. The IFSB has made clear

42

the Guiding Principles implementation. DIB

in the ED that the implementation of the Guiding Principles should be undertaken in compliance with Sharī̀ ah and within the legal framework of the jurisdictions in which IIFS operate and should be commensurate with the size, complexity and nature of each IIFS in line with the IFSB-1.

85.

Implementation timeline for January 2013 will be challenging DIB

No change. See also response in (79) above.

86.

date the guidelines should be transposed into national supervisory guidelines and be reflected in the national supervisory manuals/handbooks, where applicable, and implemented in supervisory practices.

We understand that the implementation date of January 2013 stipulated in the Exposure-Draft is for national regulatory authorities (i.e. members of the IFSB) by which date these regulatory authorities should issue their own guidelines for banks to comply with. Once that is done, we would expect the national supervisory authorities to give the banks sufficient time to comply with these requirements (i.e. by January 2014). ITB

No change. Noted. See response in (79) and (81) above.

SECTION 2: NECESSARY CONDITIONS FOR AN EFFECTIVE STRESS TESTING REGIME 87.

Section 2 – Necessary conditions for an effective stress testing regime

We would like to emphasize that the prerequisites mentioned in the Section 2: Necessary conditions for an effective stress testing regime should be addressed in order to implement the guidelines. KFHB

No change. Noted. This would be expected as without addressing these conditions, it will be relatively difficult for IIFS to implement the Guiding Principles when required by the respective supervisory authorities.

43

And also when supervisory authorities will assess the IIFS’s compliance to these Principles, then it would be implicitly taken into account.

88.

When referring to the costs for banks of developing and implementing such a stress test exercise, one could also elaborate whether there will any cost for the supervisory agency in checking the quality of the models and outcomes by the banks, and supposedly carry out the own top-down calculations. IMF

Agreed. The Para.18 is updated to reflect the suggestion of the IMF.

89.

Para. 18 - ….IIFS should also be aware of the costs of developing and implementing such a stress testing programme. It is recognised that these costs may seem high for some IIFS, particularly small or medium-sized ones. However, the costs must be weighed against the potential loss mitigation, the value of the information and risk control gained, and the capital management that will result from an effective, well-designed stress testing programme.

Again the question arises on what constitutes a “small or medium” IIFS, which we take it the respective IIFS, will make the determination themselves. More details on this would be good, so that there is no debate when IIFS makes the strategic decision on the costs it is willing to defray to set up an effective stress testing programme. ARBM

No change. See response in (77) above.

90.

Paragraph 19 – “……the IFSB recognises that the specific stress testing practices adopted by each IIFS as part of its risk management framework will vary in scope and content depending on the size and nature of its activities, which will determine the likely impact of any potential risk scenarios..….in addition, regulatory requirements for stress testing and/or guidance